Sample Category Title

Into US session: Swiss Franc as strong as Dollar, Sterling selloff accelerates

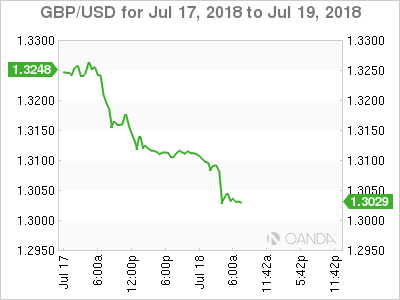

Entering into US session, Sterling remains the weakest one for today as selloff accelerates after CPI miss. Technically, GBP/USD's break of 1.3048 confirms resumption of fall from 1.4376. EUR/GBP is extending the rebound from 0.8620 even though momentum is weak. GBP/JPY's break of 147.63 minor support suggests short term topping at 149.30, ahead of 149.99 resistance. GBP/CHF is on the verge of breaking 1.3022 to resume down trend from 1.3854.

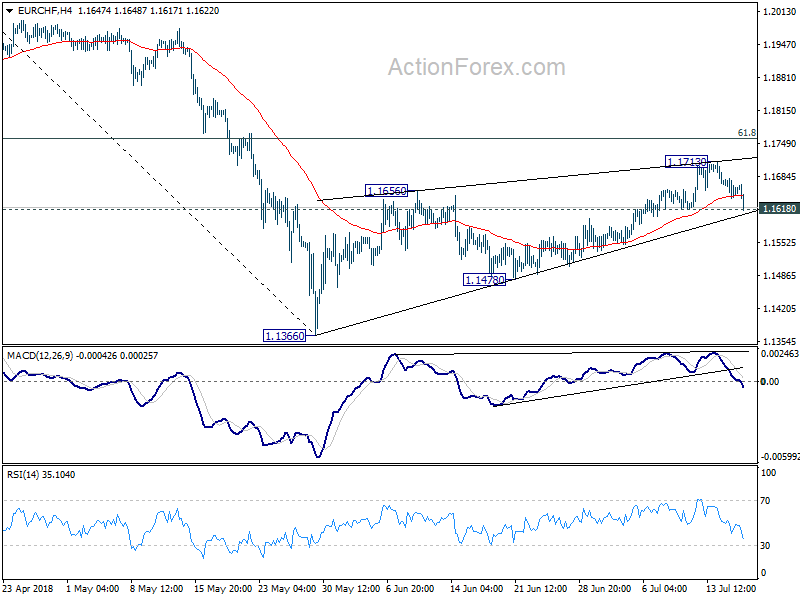

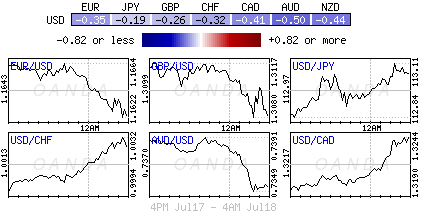

On the other hand, Dollar and Swiss Franc are taking turn to be the strongest one for today. USD/JPY has taken the lead earlier this week, then followed by GBP/USD in breaking out. Focus will now be on which pair to follow, EUR/USD, AUD/USD or USD/CAD. But at the same time, the strength in Swiss Franc is worth a note. EUR/CHF is now pressing 1.1618 minor support. Break there will be an early signal of completion of whole corrective rise from 1.1366. And in that case, we'd see the cross heads back to 1.1366 low.

Is BoE Rate Hike In Doubt After Inflation Data?

- GBP slides as core inflation falls below BoE target;

- August rate hike still well priced in;

- Powell speech may offer little new information on interest rates.

Focus is back on the central banks on Wednesday as we await the second appearance this week of Federal Reserve Chair Jerome Powell and the Bank of England’s interest rate plans are questioned following some softer inflation numbers.

The pound is tumbling again on Wednesday after the latest inflation data for the UK threw a spanner in the works ahead of the BoE meeting in two weeks. There was a growing belief that the central bank will raise interest rates at the August meeting – rightly or wrongly – with the data this week seen providing additional support for such a move but the numbers we’ve seen this morning have done quite the opposite.

Earlier this year when policy makers were preparing a May hike, inflation was much higher and was seen as being a key reason behind the desire to raise rates. Had that number ticked higher again today, as was expected, it would – along with the other data we’ve seen recently – have provided policy makers an opportunity to follow through on previous plans without coming under too much scrutiny.

With that not happening and core CPI falling to 1.9%, below the central bank’s 2% target, the decision becomes that much more difficult and uncertain. Moreover, the timing of the meeting is not ideal, with Brexit talks not going smoothly and only a few months in which they need to be concluded. Ordinarily, it would make much more sense for the Monetary Policy Committee to wait until November when much more clarity will exist over the economy and Brexit, but I’m not sure they will and market pricing appears to currently support this view.

An August rate hike is still 72% priced in, down from 77% yesterday, despite this morning’s release, which suggests investors do not believe policy makers will be deterred. The BoE’s credibility has long be brought into question, most recently in May when after months of hinting at a rate hike, it changed its mind due to first quarter weakness which it believed was transitory. If it holds off again in two weeks despite the bounce back in the economy, people will seriously question whether any attention at all should be paid to the central banks forward guidance. For this reason, I think they will raise rates and hope they won’t be forced to reverse course in the near future, say if Brexit talks collapse.

Attention will now turn to Powell’s testimony on the semi-annual monetary policy report in front of the House Financial Services Committee, where the Fed Chair is once again expected to deliver a very upbeat assessment of the economy and stick to previous views on rate hikes. The Fed has become one of the less interesting central banks due to its reliability and transparency – something that is very much a goal of all central banks – which is likely to make today’s appearance less of a market moving event.

That’s not to say that it doesn’t have the potential to cause market swings, rather that what Powell will say will likely already be priced in and so any movements are less likely to be significant. He may surprise us, should he get into a deeper discussion on trade wars for example and the implications for monetary policy, but as yet this is not something that has had an impact on the outlook.

Fed Powell Advances The Dollar

Wednesday July 18: Five things the markets are talking about

U.S assets get another leg up from rookie Fed Chair Jerome Powell who again expressed optimism over the U.S’s economic growth and stable inflation, telling Congress yesterday that domestic data should keep the central bank on track to raise “gradually” short-term interest rates. However, as per usual, there was a disclaimer – it was too soon to say if trade disputes might interfere with his plans.

To date, the Fed has refrained from commenting on trade policy, saying it is outside of their remit, yet Powell did caution that “open economies have fared better than closed ones.”

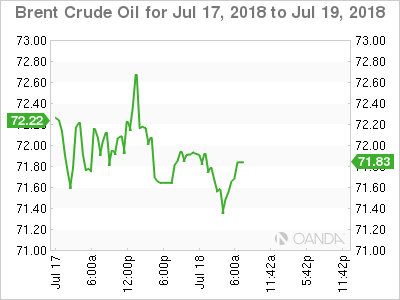

Elsewhere, commodity prices continue their decent, dragged down mostly by crude prices, which are off another -1% on a surprise U.S. crude stockpile report, while the ‘big’ dollar is outperforming its G10 currency pairs, with many EM currency pairs trading atop their multi-year lows outright.

In fixed income, Treasury yields have backed up along with most European bonds. Global equities have had a mixed overnight session.

On tap: Fed Chair Powell will testify for a second day on the hill today (10:00 am EDT).

1. Stocks mixed results

In Japan, the Nikkei share average advanced to a one-month high overnight as exporters – in particular, the auto sector – found support after the dollar hit a six-month high against the yen (¥113.04). The Nikkei gained +0.4%, as too did the broader Topix.

Down-under, Aussie stocks rallied after four consecutive session losses in the past six sessions, supported by one of the country’s biggest companies by market cap. The S&P/ASX 200 rallied +0.7% as BHP Billiton jumped +3.3% following an upbeat production update. In S. Korea, stocks slid to session lows in some heavy trading. After jumping as much as +0.9% on the open, the Kospi finished down -0.3%, recording its third-straight drop.

In Hong Kong and China, stocks came under renewed pressure from a weaker yuan, which has reduced appetite. In Hong Kong, the Hang Seng index fell -0.2%, while the China Enterprises Index lost -0.1%, while in China, the blue-chip CSI300 index fell -0.5%, while the Shanghai Composite Index lost -0.4%.

Note: Overnight, China’s yuan hit a two-week low outright, breaching the key ¥6.700 level – a rising dollar raises concerns of further capital outflows.

In Europe, regional bourses have opened slightly lower and are trading sideways. The financial sector remains the best performer in muted volatility, while tech stocks are underperforming.

U.S stocks are set to open ‘flat.’

Indices: Stoxx50 -0.2% at 3,446, FTSE +0.1% at 7,608, DAX flat at 12,562, CAC-40 flat at 5,412; IBEX-35 flat at 9,714, FTSE MIB +0.4% at 21,906, SMI -0.4% at 8,812, S&P 500 Futures flat.

2. Oil prices fall on rise in U.S stocks, gold lower

Oil prices again have come under renewed pressure after yesterday’s data reveal a rise in U.S crude inventories last week, defying markets expectations for a “big drop,” while concerns about weak demand again have resurfaced.

Brent crude oil is down -60c at +$71.56 a barrel – the benchmark hit a three-month low yesterday – while U.S light crude is down -50c at +$67.58, not far off Tuesday’s one-month low of $+67.03 per barrel.

Expect today’s price action to largely depend on what the EIA release comes in at. Yesterday’s API data showed an unexpected rise of more than +600K barrels in national crude inventories. For today, the market is forecasting a decline of -3.6M barrels in U.S crude stocks for the week through July 13 (10:30 am EDT).

Also putting pressure on energy prices for the past month is Saudi Arabia and other OPEC members agreeing to increased production, while investors have also begun to worry about the impact on global economic growth and energy demand of the escalating Sino-US trade dispute.

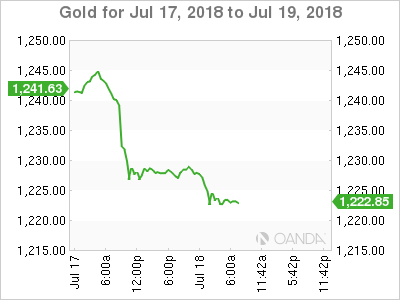

Ahead of the U.S open, gold prices have slipped to a new 12-month low as the ‘big’ dollar firms after Fed Chairman Powell’s U.S economic outlook reinforced the markets views that the central bank is on track to “steadily” hike interest rates. Spot gold is down -0.2% at +$1,224.16 an ounce. U.S gold futures for August delivery are -0.2% lower at +$1,224.30 an ounce.

3. Sovereign yields on the move

In Europe, investor uncertainty over global growth is compressing German 10-year yields, and the hunt for yield then sees demand spill over to other debt further out the curve. The gap between German 10- and 30-year Bund yields are at its narrowest in over five-weeks at +67 bps.

In the U.S, the Fed Chair Powell indicating an “unsurprising” preference for a continued steady rise in interest rates is inevitably flattening the U.S government yield curve. The spread between the two-year and 10-year Treasury bonds is narrowing and is last at +24.7 bps.

The yield on 10-year Treasuries has climbed +1 bps to +2.87%, the highest in more than two weeks. In Germany, the 10-year Bund yield has gained less than +1 bps to +0.35%, while in the U.K; the 10-year Gilt yield has rallied less than +1 bps to +1.258%.

4. Dollar goes from strength to strength

The mighty U.S dollar is holding onto its recent gains in the aftermath of Fed chair Powell’s testimony yesterday. With the Fed chair reiterating that interest rates would continue to increase gradually again supports interest rate differentials trading strategies.

Note: Euro and U.K inflation data this morning remained underwhelming (see below).

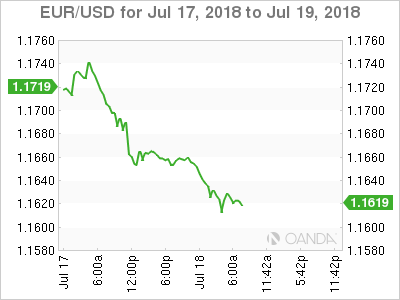

EUR/USD is a tad softer by approx. -0.3% at €1.1622, while weaker-than-expected U.K inflation data for June sent sterling to multi-month lows against the dollar and the euro.

GBP/USD has fallen to a 10-month low of £1.3010 and EUR/GBP has rallied to a four-month high of €0.8923. Also, Brexit concerns continued to weigh upon the pound as PM May’s government again survived a recent Brexit amendment vote by a “slim” margin.

Note: U.K’s June CPI was the key focus with prospects of an August rate hike in the balance. Odds for a hike have diminished a tad, now down to +72%.

5. U.K inflation steady in June

Data this morning showed that annual inflation in the U.K. held steady last month, as summer-clothing sales offset a rise in petrol prices.

As reported from the ONS, consumer prices rose +2.4% on the year and keeps annual price-growth in excess of the Bank of England’s (BoE) +2% target.

Today’s data should keep the BoE in line to hike again next month – only politics and trade disputes could derail Governor Carney’s agenda.

Digging deeper, the data shows that prices charged by companies at the factory gate accelerated in June, gaining +3.1% on year compared with an annual rise of +3% a month earlier, in a sign that inflationary pressures are building. Raw material costs jumped +10.2% on year according to the ONS.

Note: U.K policy makers have said they expect to raise borrowing costs three or more times during the next few years to bring inflation back to their goal.

EUR/USD – Euro Dips To 2-Week Low, Eurozone CPI Hits 2 Percent

EUR/USD is lower in the Wednesday session, following the downward trend which was seen on Tuesday. Currently, the pair is trading at 1.1619, down 0.37% on the day. The pair is currently at its lowest level since July 2. On the release front, Eurozone Final CPI edged up to 2.0%, matching the estimate. Final Core CPI dipped to 0.9%, short of the estimate of 1.1%. The markets are expecting mixed construction numbers – Building Permits are expected to climb to 1.33 million, while Housing Starts are forecast to drop to 1.32 million. Later in the day, Federal Reserve Chair Jerome Powell testifies before the House Financial Services Committee. On Thursday, the U.S releases the Philly Fed Manufacturing Index and U.S unemployment claims.

A milestone was reached on Thursday, as Eurozone Final CPI reached the 2.0% threshold in the June release. On an annualized basis, Final CPI also came in at 2.0%. This marks the highest level since February 2017. As the ECB prepares to wind up its asset-purchase program, the markets are looking for clues about a possible rate hike. Such a move would likely have a significant impact on the markets, as the ECB last raised rates back in 2011. If inflation levels continue to rise, there will be more pressure on the ECB to consider a rate hike sooner rather than later.

Fed Reserve Chair Jerome Powell reaffirmed his positive outlook on the U.S economy in testimony before the Senate Banking Committee. Powell said that he expected the labor market to remain tight and infatlion to stay close to the Fed’s target of 2 perecent for the next several years. Powell added that the Fed would continue to gradually raise interest rates. Lawmakers appeared satisfied with current monetary policy, but Powell did face some pointed questions regarding the escalating trade war, which has raised concerns that economy could take a downturn if the tariff battles continue.

With global protectionist winds getting stronger by the week, Japan and the EU signed a free trade agreement on Tuesday. At the signing ceremony, Prime Minister Shinzo Abe and European Council head Donald Tusk said that the deal is a response to growing concerns about protectionism. The agreement will eliminate most tariffs between the EU and Japan, and will be particularly beneficial for Japanese car makers and European food producers. No less important, the agreement marks the largest free trade agreement in the world, as the EU and Japan cover about one-third of global GDP and some 600 million people.

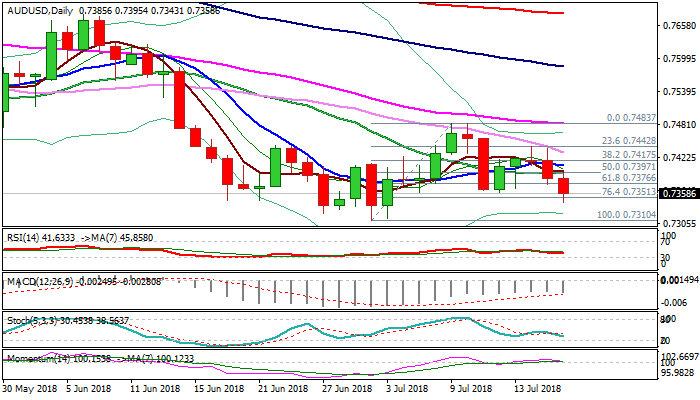

AUDUSD Outlook: Bears Eye Key Support At 0.7310

The Aussie dollar extended weakness through key near-term support at 0.7360 (12 July lo) on Wednesday, after previous day's weakness completed Doji bearish reversal pattern on daily chart, while today's break below 1.1760 pivot signals completion of failure swing pattern and generates another bearish signal.

Positive greenback's sentiment on more hawkish than expected Powell on Tuesday keeps the Aussie pressured for final push towards key supports at 0.7325/10 (Fibo 61.8% of larger 0.6825/0.8135 ascend / the lowest since Nov 2016), break of which would signal extension of broader uptrend from 0.8135 (2018 high, posted on 26 Jan).

Daily techs in strong bearish setup support negative scenario, with converged 5/20SMA (0.7395) which mark solid resistance, expected to keep the upside limited

Res: 0.7376, 0.7395, 0.7417, 0.7442

Sup: 0.7343, 0.7325, 0.7310, 0.7250

Hopes For A Aug BOE Rate Hike Dimmed But Not Totally Dashed After Softer UK CPI Data

Notes/Observations

- UK Jun CPI data comes in lower-than-expected; rate hike expectations for Aug diminishes slightly (but not totally dashed)

- Euro Zone Final CPI saw core revised lower (in-line with recent national CPI readings)

Asia:

- South Korea Fin Min Kim: Cuts 2018 GDP growth forecast from 3.0% to 2.9% (in-line with recent speculation)

Europe:

- UK MPs vote against an amendment to the Trade Bill calling for all free trade deals after Brexit to be subject to Parliamentary scrutiny and approval (Note: win for May govt)

- UK Govt said to have cancelled plans to close parliament early for summer break

- ECB's Rehn: markets appeared to be correctly reading the ECB's forward guidance for a potential rate hike in Oct 2019

- European Union reportedly exploring talks with President Trump on reducing car tariffs. EU President Juncker to meet with President Trump on July 25th in Washington

- Efforts to produce consensus on a G20 communique are on track and have faced no meaningful opposition from the US

Americas

- US Treasury Dept: Sec Mnuchin had no plans for a bilateral meeting with China at the weekend G20 meeting in Argentina.

- Fed’s George (hawk) said there is still uncertainty about how far and how fast the Fed should raise rates; unclear about inverted yield curve

Energy:

- Weekly API Oil Inventories: Crude: +0.6M v -6.8M prior

Economic Data:

- (AT) Austria Jun CPI M/M: 0.2% v 0.2% prior; Y/Y: 2.0% v 1.9% prior

- (PL) Poland Jun PPI M/M: 0.3% v 0.5%e; Y/Y: 3.7% v 3.6%e

- (PL) Poland Jun Sold Industrial Output M/M: 4.2% v 3.5%e; Y/Y: 6.8% v 6.3%e, Construction Output Y/Y: 24.7% v 20.2%e

- (ZA) South Africa Jun CPI M/M: 0.4% v 0.6%e; Y/Y: 4.6% v 4.8%e

- (ZA) South Africa Jun CPI Core M/M: 0.2% v 0.4%e; Y/Y: 4/2% v 4.4%e

- (UK) Jun CPI M/M: 0.0% v 0.2%e; Y/Y: 2.4% v2.6%e; CPI Core Y/Y: 1.9% v 2.1%e; CPIH Y/Y: 2.3% v 2.5%e

- (UK) Jun RPI M/M: 0.3% v 0.4%e; Y/Y: 3.4% v 3.5%e, RPI-X (ex-mortgage interest payment) Y/Y: 3.4% v 3.6%e, Retail Price Index: 281.5 v 281.9e

- (UK) Jun PPI Input M/M: 0.2% v 0.4%e; Y/Y: 10.2% v 10.1%e

- (UK) Jun PPI Output M/M: 0.1% v 0.3%e v 0.4% prior; Y/Y: 3.1% v 3.2%e

- (UK) Jun PPI Output Core M/M: 0.2% v 0.2%e; Y/Y: 2.1% v 2.1%e

- (UK) May ONS House Price Index Y/Y: 3.0% v 3.7%e

- (EU) Euro Zone Jun Final CPI Y/Y: 2.0% v 2.0%e; CPI Core Y/Y: 0.9% v 1.0%e v 1.0% advance

- (EU) Euro Zone May Construction Output M/M: 0.3% v 1.4% prior; Y/Y: 1.8% v 1.2% prior

- (IL) Israel July CPI 12-month Forecast: 1.1% v 1.0% prior

Fixed Income Issuance:

- (DK) Denmark sold total DKK2.34B in 2020 and 2027 DGB bonds

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.5% at 386.8, FTSE +0.5% at 7667, DAX +0.4% at 12768, CAC-40 +0.5% at 5449, IBEX-35 +0.1% at 9724, FTSE MIB -0.1% at 21,946, SMI +0.7% at 8887, S&P 500 Futures flat]

- Market Focal Points/Key Themes: European Indices trade higher across the board following a higher close in the US overnight and mostly positive earnings out of Europe. Swedish Orphan, Tele2 trade higher after beats on the top and bottom line and raised outlook. Novartis, ASML, Easyjet, Akza Nobel are among other notable risers after earnings. Danske Bank drops sharply after missing on the both Revs and profits and lower outlook while Smith Group trades 8% lower after a temporary suspension of some medical products which will lead to a revenue decline for the full year. Looking ahead notable earners include Bank names Morgan Stanley, M&T Bank and US Bancorp, alongside Abbott and WW Grainger.

Movers

- Consumer Discretionary Easyjet [EZJ.UK]+2% (Earnings), Swatch [UHR.CH]+1.1% (Earnings)

- Financials Danske Bank [DANSKE.DK] -8% (Earnings)

- Healthcare Swedish Orphan [SOBI.SE] +10% (Earnings), Novartis [NOVN.CH] +2% (Earnings)

- Technology ASML [ASML.NL]+5% (Earnings), Smith Group [SMIN.UK] -8% (Trading update), Software AG [SOW.DE] -5% (Earnings)

- Materials BHP [BHP.AU] +3% (Production)

- Telecoms Tele2 [TEL2B.SE]+14.6% (Earnings)

Speakers

- ECB Working Paper on monetary policy and household inequality expressed concerned about the recent economic activity

- UK PM May said to have threatened hardliners with election if they defeated her Brexit plans on customs union

- Ireland Dep PM Coveney (also foreign Min): UK continued to be committed to backstop but needs to come up with a plan that works. Amendments in UK Parliament this week had not been very helpful. Reiterated view that both UK and EU needed to intensify talks; believed that there will be a Brexit agreement

- Bank of Korea (BOK) Board member Koh: Policy rate could stay below the Fed level for a prolong period of time

Currencies

- USD holding onto its recent gains in the aftermath of Fed chair Powell's testimony on Tuesday. The Fed chief reiterated that interest rates would continue to increase gradually and that the economic backdrop was good

- European inflation data was in focus during the session.

- EUR/USD was softer by approx. 0.3% ahead of the Euro Zone final CPI reading for June. Some analysts were concerned that core HICP could be revised down following the national releases

- Brexit concerns continued to weigh upon the GBP currency as the PM May govt survived recent Brexit amendment votes by slim margins. UK Jun CPI was the key focus with prospects of a Aug rate hike depending on the situation. The GBP currency tested the 1.3000 area for its lowest level since early Sept as lower-than-expected CPI dimmed the prospects for a Aug BOE rate hike.

Fixed Income

- Bund Futures trade 20 ticks higher at 162.97 as the euro zone confirms Jun CPI YoY at 2.0%. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.65 higher by 32 ticks as UK inflation comes in softer than expected. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Wednesday's liquidity report showed Tuesday's excess liquidity fell from €1.850T to €1.849T. Use of the marginal lending facility dropped from €95M to €45M.

- Corporate issuance saw 2 issuers raise $4.8B in the primary market

Looking Ahead

- (SA) Saudi Arabia May Oil Production:

- 05:30 (DE) Germany to sell €1.0B in 1.25% Apr 2048 Bunds

- 05:30 (PL) Portugal Debt Agency (IGCP) to sell €1.5-1.75B in 6-month and 12-month bills

- 06:00 (PT) Portugal Jun PPI M/M: No est v 1.4% prior; Y/Y: No est v 3.1% prior

- 06:45 (US) Daily Libor Fixing

- 07:00 (RU) Russia to sell 2021 and 2029 OFZ bonds

- 07:00 (US) MBA Mortgage Applications w/e July 13th: No est v 2.5% prior

- 07:00 (BR) Brazil July IGP-M Inflation (2nd Preview): 0.4%e v 1.8% prior

- 07:00 (ZA) South Africa May Retail Sales M/M: 0.5%e v -1.2% prior; Y/Y: 0.8%e v 0.5% prior

- 07:00 (UK) Weekly PM May question time in House of Commons

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Jun Housing Starts: 1.320Me v 1.350M prior; Building Permits: 1.330Me v 1.301M prior (RU) Russia Jun PPI M/M: No est v 3.9% prior; Y/Y: No est v 12.0% prior

- 10:00 (US) Fed Chair Powell testifies in Congress (2nd day of his semi-annual testimony)

- 10:00 (CA) Canada to sell 2-year notes

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 14:00 (US) Federal Reserve Beige Book

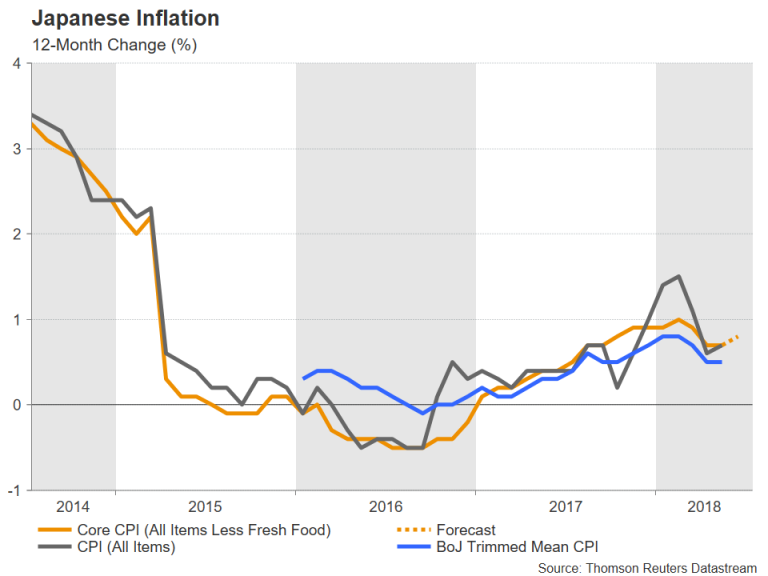

Japanese Inflation To Nudge Up As BoJ Considers Cutting Forecasts

Inflation numbers for June will be watched out of Japan on Friday (Thursday, 23:30 GMT) ahead of the Bank of Japan's policy meeting at the end of July. With progress towards meeting its 2% inflation target having stalled, the central bank might find some relief from an expected upward tick in core CPI. However, any acceleration in price growth is unlikely to be in enough in preventing the BoJ from lowering its inflation outlook when it meets later this month.

After years of ultra-loose and unconventional monetary policy, things were looking up for the Bank of Japan at the beginning of the year when core CPI – its targeted inflation measure – hit a 3-year high of 1% year-on-year in February. However, since then, core CPI, which excludes fresh food prices, has eased to 0.7% y/y, increasing the distance from the BoJ's goal of 2%. Data due on Friday is expected to show inflation moving higher again, with core CPI edging up to 0.8%.

That trend could continue in the coming months as the recent rally in oil prices should push up fuel costs. (Unlike in most countries, Japan's core measure of inflation includes energy prices). However, the effects of higher fuel prices are not expected to be large enough to offset broader weakness in Japanese consumer prices. Looking at a more accurate gauge of underlying inflation – the BoJ's trimmed mean CPI has fallen to just 0.5% y/y after rising to 0.8% earlier in the year, suggesting the absence of underlying price pressures.

With a Bank of Japan policy meeting scheduled for July 30-31, there have been numerous reports that the Bank will cut its inflation forecasts in its latest quarterly outlook to be published after the meeting. Indications are that the BoJ will lower its projection for core CPI for fiscal year 2018 to 1.0% from 1.3% in April's forecasts. For fiscal year 2019, the projection of 1.8% may be cut to 1.5%, which would mean the central bank does not expect to meet its 2% target before fiscal year 2020.

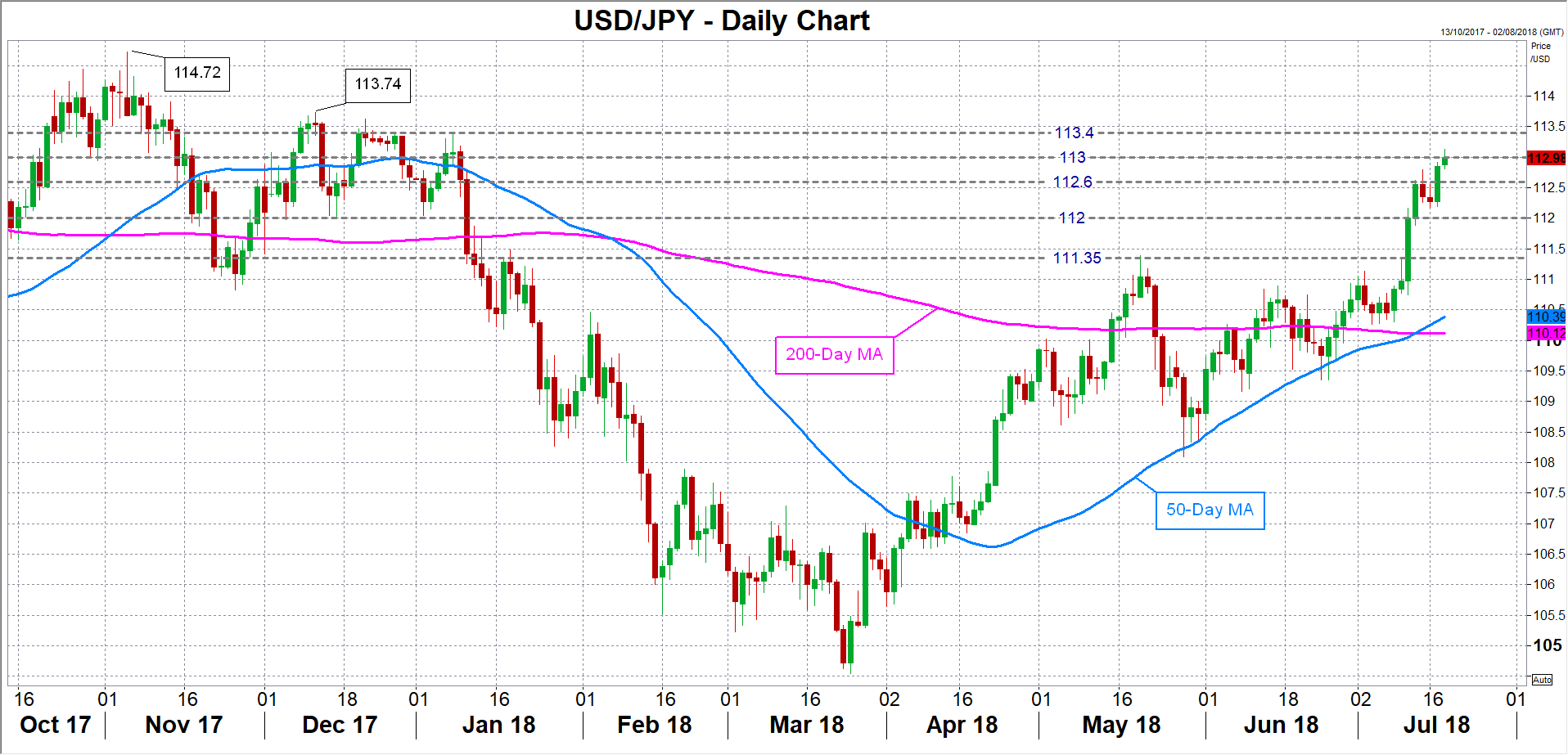

If Friday's inflation data confirms the muted price outlook in Japan, the yen could face downside pressure in anticipation of a dovish BoJ at the July meeting. Bearish bets against the Japanese currency could lift dollar/yen further beyond the 113 handle after this week breaking above the level for the first time since January. Above 113, the pair could meet some resistance near 113.40 before being able to challenge the December and November tops of 113.74 and 114.72, respectively.

However, a surprisingly strong inflation reading could provide traders with an excuse for profit-taking given the recent sharp gains in dollar/yen. The pair could seek immediate support around 112.60 on any sell-off. A breach of that support could accelerate the decline towards the next key area around the psychological 112 level, while below that mark, focus would turn to 111.35, a previous support and resistance point.

It should be noted though that in general, risk sentiment remains the strongest driver for the safe-haven yen so unless there is a big beat or miss in the numbers, any reaction to the data will likely be limited.

Bitcoin Surges As USD Bounces Back

Bitcoin crosses $7,500 as momentum builds up

Cryptocurrencies surged across the board on Tuesday evening as Bitcoin crossed the $7,000 threshold for the first time in the last four weeks. During the Asian session, the largest cryptocurrency by market capitalisation hit $7,543 as it added $780 (+11.60%) in less than 10 hours. Ethereum followed the lead and climbed to $514, up more than $45 on the day. Looking at the big picture, the total market capitalisation increased by almost $30 billion to reach $300 billion, its highest level since mid-June.

Given the lack of fresh news in crypto industry, the reason behind the rally remains unclear. However, there are a lot of moving pieces as investors await regulators to provide rulings on key topics. More specifically, the SEC will have to decide whether it approves the creation of a Bitcoin ETF. The Chicago Board Options Exchange (CBOE) has filed for a rule, which would enable the listing of such type of products. The SEC is expected to come with a decision on August 10; however, a 45-day extension cannot be ruled out. Finally, on the technical side, the price of Bitcoin seems to have reach the bottom. The $5,922 support (low from February 2) was broken on June 29 but bulls outnumbered bears as the price quickly bounced back. This morning Bitcoin tumbled on $7,560, which correspond to the top of March downtrend channel. Of break of that level would open the door towards $9,180 (200dma), the next resistance area lies at between $9,795 and $10,000 (high from May 4th and psychological level).

Given the quick appreciation of Bitcoin, a period of consolidation is more than likely. However, in the longer-run Bitcoin should continue to appreciate as the regulatory background improves.

Rebound for the pound ?

Despite May 3-month unemployment data given at 1975 low (4.20%), sterling dropped against its major peers amid disappointing wage growth and mounting uncertainties relating to yesterday’s parliamentary vote.

Indeed, despite a tight majority (6 votes difference), May’s government had the final word on an amendment bill that would have required the UK to try negotiating a customs union arrangement with the EU in the scenario of a no-deal by 21. January 2019 deadline, which already supports free trade for goods. Prior vote on an amendment to remain within EU medicines regulatory framework endured a different fate as it got accepted by a small majority of four votes.

Accordingly, the narrow victory against soft-Brexit supporter MPs is an obvious sign that May is having difficult times to maintain a majority of supporter of her Brexit plan within the Parliament. Therefore, risk of seeing May being overthrown is mounting due to a greater number of soft-Brexit advocates within the parliament and increasing questioning of May’s leadership. Recent amendment refusal will not be helping the situation in any case, as it rather reinforces the course of a hard Brexit.

Hence, amid rising uncertainties around Brexit orientation, the BoE will be looking at UK – EU negotiation development before announcing further rate hikes after 2. August 2018 meeting. In any case, recent labor market data, and most certainly June inflation data as well, will tend towards further policy tightening.

As August rate hike is a priced in scenario and inflation data will remain pound supportive, the pair will most likely benefit from a weak boost in the short-term, which will most probably fade out due to increasing political worries. GBP/USD is approaching its 03. November 2017 range, currently trading along 1.3083 and heading towards 1.3070.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1635

The slide through 1.1700 signals a reversal of the upmove since 1.1610 and the bias is bearish, for a dip to 1.1510 lows. Minor resistance lies at 1.1645 and crucial on the upside is 1.1665.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1645 | 1.1750 | 1.1610 | 1.1510 |

| 1.1700 | 1.1830 | 1.1510 | 1.1300 |

USD/JPY

Current level - 113.04

The climb above 112.80 signals a completion of the consolidation pattern, so the uptrend is renewed, heading towards 113.70, en route to 114.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.70 | 114.50 | 112.80 | 111.40 |

| 114.50 | 114.50 | 112.17 | 109.30 |

GBP/USD

Current level - 1.3094

The violation of 1.3190 signals a reversal of the positive bias and the outlook is bearish, for a test of 1.3040 lows. Initial resistance is projected at 1.3140, followed by 1.3190.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3140 | 1.3460 | 1.3040 | 1.3040 |

| 1.3190 | 1.3620 | 1.3040 | 1.2770 |

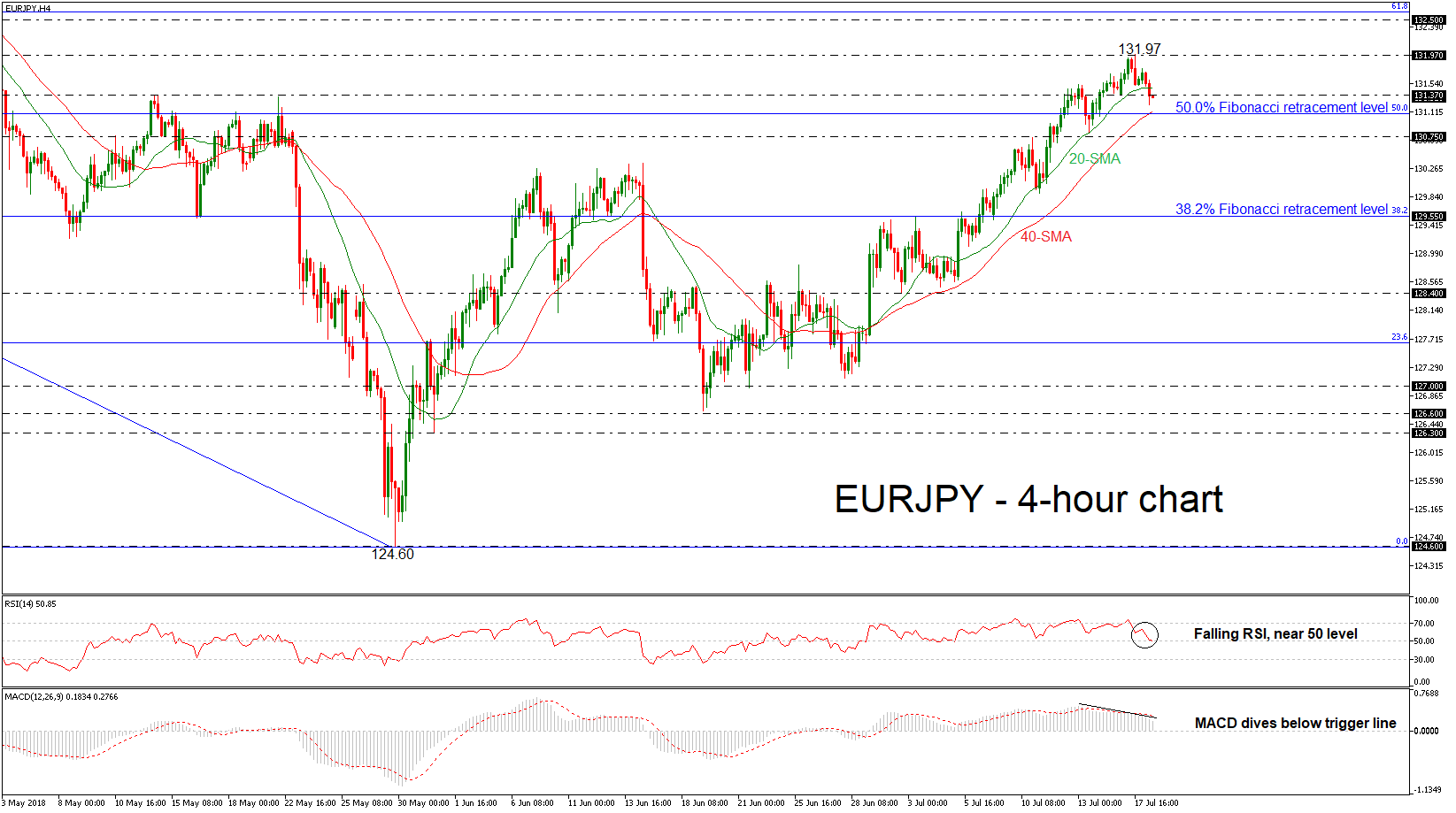

EURJPY Fairly Bearish, Holds Below 2-Month High Near 132.00

EURJPY started an aggressive bearish rally today after it reached a two-month high of 131.97 on Tuesday. The sharp sell-off creates a new structure of downward correction in the pair as it also fell below the 20-day simple moving average (SMA) in the near-term.

The momentum indicators, in the 4-hour chart, are supportive of the bearish picture, with the RSI falling towards the threshold of 50 with strong movement, while the MACD oscillator is slipping below its trigger line and is approaching the zero line.

The immediate support to have in mind is the 50.0% Fibonacci retracement level of the downleg from 137.50 to 124.60, around 131.10. This level coincides with the 40-SMA in the near term. Should prices drop lower again, the next support could come from the 130.75 level taken from the high on July 10.

In case of an upward attempt, the single currency would retest the two-month high (131.97) against the yen. A break above this significant obstacle would ease the downside correction and open the door towards the 132.50 hurdle where the price topped during April.

Having a look at a longer timeframe, EURJPY is still in a rising mode after the rebound on the 124.60 support and found resistance at the 200-day SMA on Tuesday.