Sample Category Title

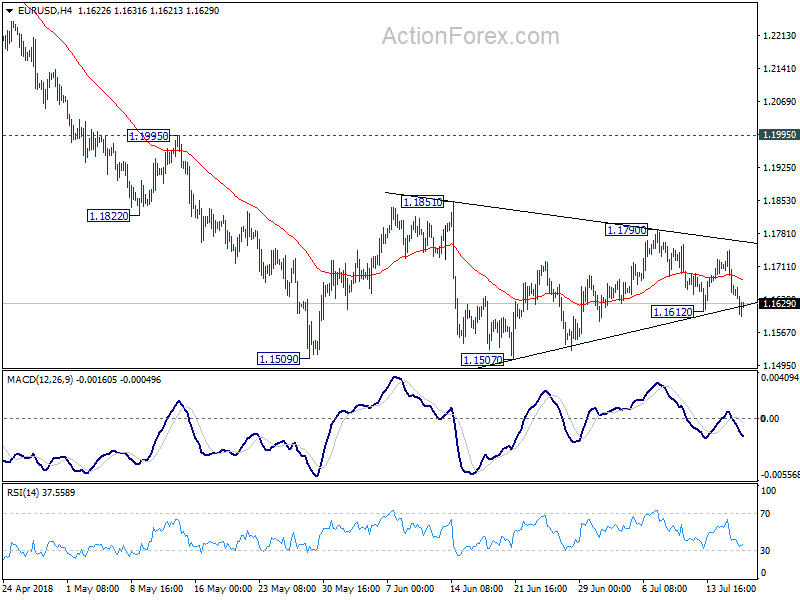

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1625; (P) 1.1685 (R1) 1.1721; More.....

EUR/USD's break of 1.1612 minor support argues that larger decline might be able to resume. Intraday bias is turned to the downside for 1.1507 first. Firm break there will resume whole decline from 1.2555, through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186. On the upside, in case of another rise as consolidation extends, upside should be limited by 1.1851 resistance to bring fall resumption eventually.

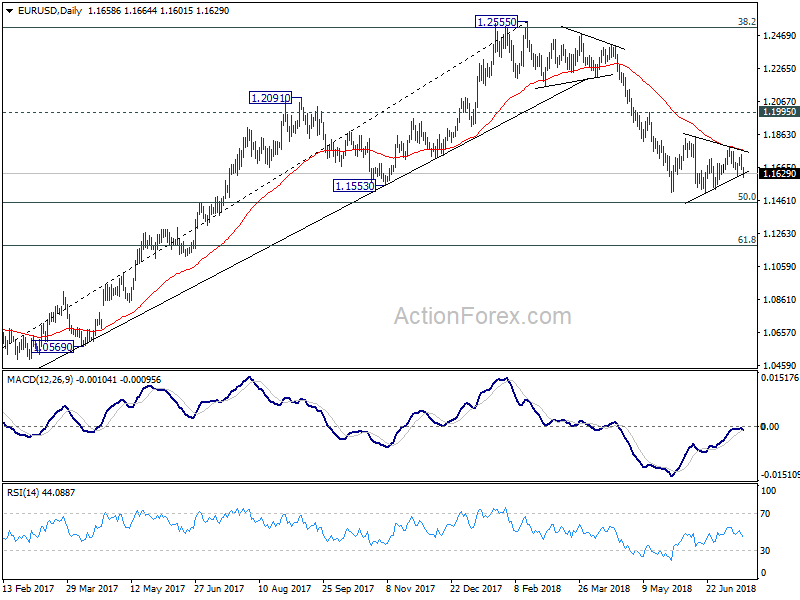

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

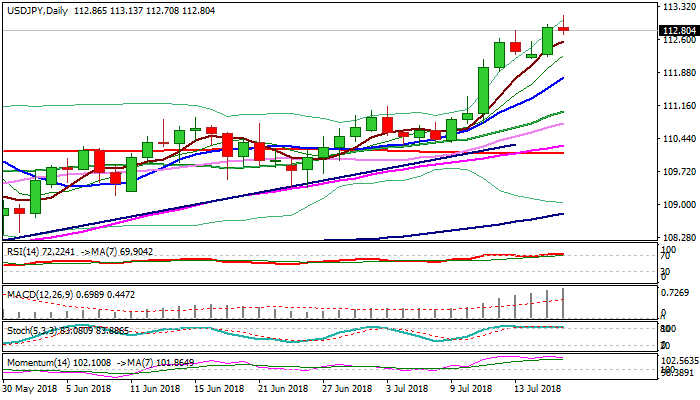

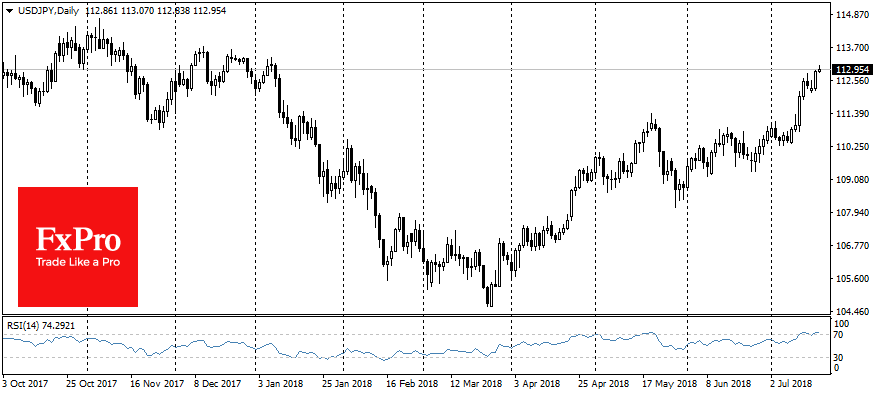

USDJPY Outlook: Eases Below 113 Handle on O/B Conditions / Weak US Housing Data

The pair stands at the back foot in early US trading and dipped to session low at 112.70 after bulls stalled on initial attempt above 113 handle. Overbought daily studies signaled easing which was helped by poor housing data released today. Housing starts fell sharply by 12.3% in June, undershooting forecast for 2.2% fall, while building permits slipped by 2.2% in June against forecasted rise by 2.2%. Risk of deeper pullback remains in play and extension below rising 5SMA (112.57) would generate negative signal for extension towards key support at 112.19 (16 July trough). Today's close above 113 barrier is required to sideline pullback threats and maintain bullish bias.

Res: 113.13; 113.38; 113.63; 113.74

Sup: 112.70; 112.57; 112.19; 111.79

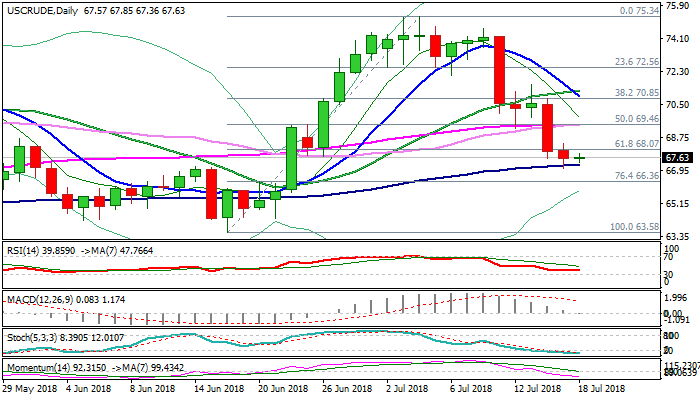

WTI Oil – Bears are Taking a Breather; Crude Inventories Report Eyed for Fresh Signal

WTI oil price trades within narrow consolidation on Wednesday after strong bearish acceleration in past two days hit new 3 1/2 week low at $67.02. Thin daily cloud which twists today, reinforced by rising 100SMA, offered temporary support, where steep seven-day downtrend found footstep. Oversold slow stochastic on daily chart supports the notion, signaling that bears may take a breather here, but firmly bearish techs and negative sentiment suggest limited recovery action. Increased output from main world oil producers keeps oil price under pressure, with increase of weekly crude stocks (API report on Tuesday showed build of 0.63 million barrels vs 6.8 million barrels draw last week), further souring the sentiment. Today's release of EIA weekly crude stocks report is in focus (draw of 3.6 million barrels is forecasted vs previous week's strong fall of 12.6 million barrels). Tuesday's high at $68.42 marks initial resistance while stronger upticks should be capped by converged 55/30SMA's ($69.46), to keep bearish structure intact. Final break below 100SMA would risk extension towards next supports at $66.36 (Fibo 76.4% of $63.58/$75.35 rally) and $65.71 (22 June low).

Res: 67.85; 68.07; 68.42; 69.46

Sup: 67.24; 67.02; 66.36; 65.71

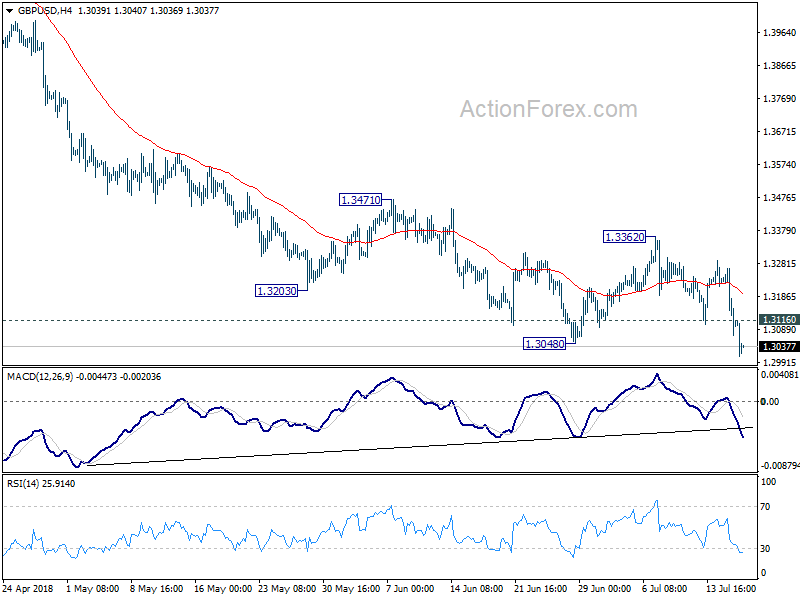

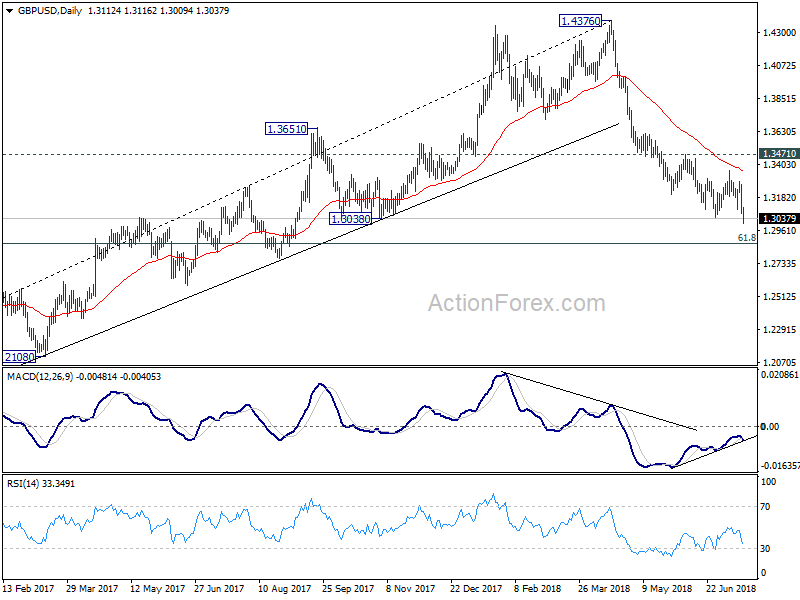

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3036; (P) 1.3152; (R1) 1.3233; More...

GBP/USD drops to as low as 1.3009 so far today. The break of 1.3048 low confirms resumption of whole decline from 1.4376. Intraday bias remains on the downside for 1.2874 fibonacci level next. Sustained break there will carry larger bearish implications. On the upside, above 1.3116 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 1.3362 resistance to bring fall resumption.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3471 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

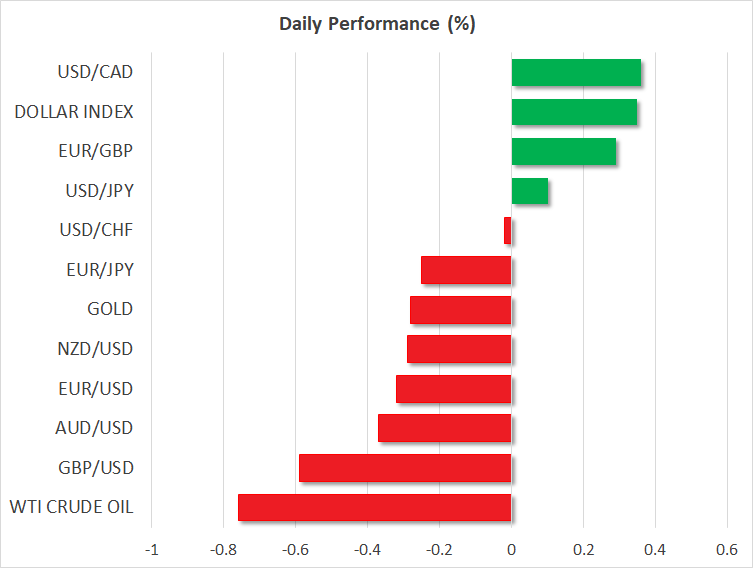

Sterling Hammered after CPI, Dollar Overwhelmed by Swiss Franc and Yen

Sterling's selloff accelerates as UK CPI missed market expectations. And that lowers the chance of a should-be-done-deal August BoE hike. In the background, Brexit uncertainty is also weighing on sentiments towards the Pound. Meanwhile, Australian Dollar and Euro are trading as the second and third weakest ones. Dollar is generally firm today as support by Fed Chair Jerome Powell's optimistic comments. But the greenback is firstly overwhelmed by the strength in Swiss Franc. Yen is also lifted by some buying in early US session as China seems to be stepping up with its rhetorics against US protectionism again.

In other markets, major European indices are trading in blue at the time of writing. Notably FTSE is lifted by the sharp by in Sterling and it's up 0.63%. DAX is trading up 0.65% while CAC is up 0.40%. Earlier today, China SSE suffered another day of decline, by -0.39% to 2787.26. Nikkei, though, rose 0.43%. WTI crude oil is extending this week's sharp fall and hits as low as 67.37, now at 67.61. Spot gold hits as low as 1221.25 and is set to take on 1220 handle.

Technically, GBP/USD's break of 1.3048 confirms resumption of fall from May top at 1.4376. EUR/GBP's recent rally resumes albeit with weak momentum. GBP/JPY's break of 147.63 suggests near term reversal, back towards 143.76 support. USD/CAD's break of 1.3216 is now paving the way to retest 1.3385. AUD/USD's break of 0.7359 minor support would like bring deeper fall to 0.7309 low. Also, EUR/CHF's break of 1.1618 support suggests that the corrective rise from May's low at 1.1366 is possibly finished.

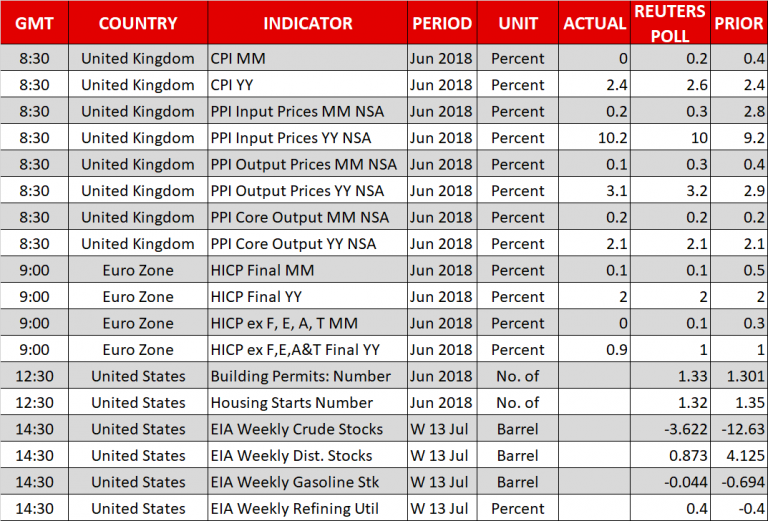

Released from US, housing starts dropped 1.17M annualized rate in June. Building permits dropped to 1.27M. Eurozone CPI was finalized at 2.0% yoy in June, core CPI at 0.9% yoy.

Sterling hammered after CPI miss, August BoE hike in doubt

Sterling drops sharply as UK consumer inflation missed market expectations. Headline CPI was unchanged at 2.4% yoy in June, below expectation of 2.6% yoy. Core CPI slowed to 1.9% yoy, down from 2.1% and missed expectation of 2.2%. RPI accelerated to 3.4% yoy, up from 3.3% yoy but missed expectation of 3.5% yoy. Also from UK, PPI input rose to 10.2% yoy, up from 9.6% yoy and above expectation of 10.2% yoy. PPI output rose to 3.1% yoy, up from 3.0% yoy but missed expectation of 3.2% yoy. PPI output core was unchanged at 2.1%, below expectation of 2.3%.

BoE has been expecting pickup in inflation that is now not happening. And indeed core CPI actually slowed. The once near confirmed August BoE rate hike is now back as a question. Tomorrow's retail sales data will be another test for the Pound. And there will be UK PMIs in around two weeks' time. The path to a hike is not easy for BoE.

Everyone's preparing for no-deal Brexit as uncertainty stays

In the background, there Brexit uncertainty is always there despite all the things the Prime Minister Theresa May has done. May insisted to the Parliament today that "the Chequers agreement, the white paper are the basis for our negotiation with the European Union and we have already started those negotiations." And she also added that the EU "need to be in no doubt that we are making those preparations" for no deal Brexit.

Irish taoiseach, Leo Varadka warned today that "We can't make assumptions that the withdrawal agreement will get through Westminster. " And he added that "It's not evident, or not obvious, that the government of Britain has the majority for any form of Brexit, quite frankly." He's government is stepping up the preparation for a no-deal Brexit. EU chief Brexit negotiator Michel Barnier will report to European Council regarding May's white paper. And, it's reported that Barnier's draft document including words like the consequences of no-deal Brexit will be "very real for citizens, professionals and business operators".

China to take further action to balance impacts of US steel tariffs

The Chinese Ministry of Commerce said in a statement today that it will take "further actions" to balance the impacts of the US section 232 steel and aluminum tariffs. It condemns the US of using "national security" as excuse for practicing trade protectionism. And criticized the steel tariff measures are a " a serious damage to multilateral trade rules and undermine the legitimate rights and interests of WTO members". Further then that, the US "refused to respond" to Chin's WTO complaints.

Fed Powell to have second half of Congressional Testimony

Fed chair Jerome Powell will have his second half of Congressional testimony today, at the House Financial Services Committee. As a recap to his remarks yesterday, he painted an optimistic picture of the US economy. He noted that "with appropriate monetary policy, the job market will remain strong and inflation will stay near 2 percent over the next several years." And, "risk of the economy unexpectedly weakening as roughly balanced with the possibility of the economy growing faster than we currently anticipate." He also affirmed the known policy path and said "the best way forward is to keep gradually raising the federal funds rate."

Later in the Q&A section, he also talked about the hot topic of flattening yield curve and recession. Powell pointed out that what matters is the yield at the long end as an indication of the so called neutral rate. Right now, 30 year yield is at around 2.96 after hitting as high as 3.247 earlier this year. 10 year yield is at around 2.85 after hitting as high as 3.115.

Regarding US trade policy, Powell didn't comment directly as expected. It should be reminded that Powell has already made his stance clear before. He doesn't comment on policies he doesn't make. And to guard the line of independence of Fed, he has to refrain from commenting on the administration's policies too. Instead, he takes them as given. Though, he was willing to talk about trade from "principles" perspective. And to him, countries that embraced free trade and low tariffs used to have better results and higher productivity. Countries that have been more protectionist "have done worse".

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3036; (P) 1.3152; (R1) 1.3233; More...

GBP/USD drops to as low as 1.3009 so far today. The break of 1.3048 low confirms resumption of whole decline from 1.4376. Intraday bias remains on the downside for 1.2874 fibonacci level next. Sustained break there will carry larger bearish implications. On the upside, above 1.3116 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 1.3362 resistance to bring fall resumption.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3471 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | 0.00% | -0.22% | ||

| 08:30 | GBP | CPI M/M Jun | 0.00% | 0.20% | 0.40% | |

| 08:30 | GBP | CPI Y/Y Jun | 2.40% | 2.60% | 2.40% | |

| 08:30 | GBP | Core CPI Y/Y Jun | 1.90% | 2.20% | 2.10% | |

| 08:30 | GBP | Retail Price Index M/M Jun | 0.30% | 0.40% | 0.40% | |

| 08:30 | GBP | Retail Price Index Y/Y Jun | 3.40% | 3.50% | 3.30% | |

| 08:30 | GBP | PPI Input M/M Jun | 0.20% | 1.60% | 2.80% | 3.30% |

| 08:30 | GBP | PPI Input Y/Y Jun | 10.00% | 10.10% | 9.20% | 9.60% |

| 08:30 | GBP | PPI Output M/M Jun | 0.30% | 0.20% | 0.40% | 0.50% |

| 08:30 | GBP | PPI Output Core Y/Y Jun | 3.10% | 3.10% | 2.90% | 3.00% |

| 08:30 | GBP | PPI Output M/M Jun | 0.20% | 0.10% | 0.20% | |

| 08:30 | GBP | PPI Output Core Y/Y Jun | 2.10% | 2.30% | 2.10% | |

| 08:30 | GBP | House Price Index Y/Y May | 3.00% | 3.80% | 3.90% | 3.50% |

| 09:00 | EUR | Eurozone CPI M/M Jun | 0.10% | 0.10% | 0.50% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 2.00% | 2.00% | 2.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 0.90% | 1.00% | 1.00% | |

| 12:30 | USD | Housing Starts Jun | 1.17M | 1.32M | 1.35M | 1.34M |

| 12:30 | USD | Building Permits Jun | 1.27M | 1.33M | 1.30M | |

| 14:30 | USD | Crude Oil Inventories | -3.4M | -12.6M | ||

| 18:00 | USD | Federal Reserve Beige Book |

China to take further action to balance impact of US steel tariffs

The Chinese Ministry of Commerce said in a statement today that it will take "further actions" to balance the impacts of the US section 232 steel and aluminum tariffs. It condemns the US of using "national security" as excuse for practicing trade protectionism. And criticized the steel tariff measures are a " a serious damage to multilateral trade rules and undermine the legitimate rights and interests of WTO members". Further then that, the US "refused to respond" to Chin's WTO complaints.

The news apparently gives Yen a lift. But a bit more time is needed to gauge if China is getting out from the quiet mode against the US on trade war.

Canadian Dollar Dips, Investors Eye US Housing Numbers

The Canadian dollar continues to have a quiet week. In the Wednesday session, USD/CAD is trading at 1.3238, up 0.37% on the day. In economic news, there are no Canadian events. In the U.S, markets are expecting mixed construction numbers – Building Permits are expected to climb to 1.33 million, while Housing Starts are forecast to drop to 1.32 million. Later in the day, Federal Reserve Chair Jerome Powell testifies before the House Financial Services Committee. On Thursday, Canada releases the ADP Nonfarm Employment Change. The U.S will publish the Philly Fed Manufacturing Index and U.S unemployment claims.

With trade tensions hovering, investors are keeping a close eye on the Canadian manufacturing sector. Manufacturing Sales in May rebounded with a gain of 1.4%, after a decline of 1.3% a month earlier. Last week, the Bank of Canada raised rates by a quarter-point last week, to 1.50%. This is the highest level since December 2008. Will we see more rate hikes in 2018, as will likely be the case in the U.S? The BoC rate statement said that “higher rates will be needed” in order to keep inflation close to the target of 2 percent. Policymakers are keeping a close eye on the simmering trade war, which has seen Canada and the U.S impose tariffs on each other’s products. If the Canadian economy can escape the trade war relatively unscathed, we could see another rate hike at the BoE policy meeting in September.

Fed Reserve Chair Jerome Powell reaffirmed his positive outlook on the U.S economy in testimony before the Senate Banking Committee. Powell said that he expected the labor market to remain tight and inflation to stay close to the Fed’s target of 2 percent for the next several years. Powell added that the Fed would continue to gradually raise interest rates. Lawmakers appeared satisfied with current monetary policy, but Powell did face some pointed questions regarding the escalating trade war, which has raised concerns that economy could take a downturn if the tariff battles continue.

Pound Touches 10-Month Low After UK Inflation Misses Forecasts, Dollar Unlocks Fresh Highs

Here are the latest developments in global markets:

FOREX: The US dollar extended its bullish rally against the Japanese yen towards a fresh 6-month high of 113.13, adding 0.08% to its performance on Wednesday. Markets reacted positively after the Fed Chair, Jerome Powell, gave a bullish assessment of the US economy, reducing their exposure to safer assets such as the yen. Also, the US dollar index gained 0.33% and surpassed the 95.00 handle. Sterling plummeted to 10-month lows (-0.61%) today, pausing at 1.3000 after the UK’s headline inflation stood unchanged at 2.4% y/y in June instead of picking up to 2.6% as analysts had forecasted. Brexit-linked political risks were also weighing in the background. The Eurozone’s final headline CPI figures (harmonized) for June came in line with expectations, though core measures disappointed, sending euro/dollar down to 1.1614 (-0.35%). In antipodean currencies, aussie/dollar and kiwi/dollar were struggling, with the former dropping to 0.7354 (-0.43%) and the latter easing to 0.6759 (-0.35%). Dollar/loonie broke above the 1.3200 key-level to touch an almost 3-week peak at 1.3247 (+0.44%).

STOCKS: European equities jumped after a mixed Asian session on Wednesday, gaining on a weaker euro and positive earnings updates. The pan-European STOXX 600 was up by 0.43% at 1110 GMT with almost every section in positive territory. The blue-chip Euro STOXX 50 traded higher by 0.60%, creating a 1-month high. The German DAX 30 climbed by 0.68%, the French CAC 40 rose by 0.45%, while the Italian FTSE MIB moved down by 0.12%. UK’s FTSE 100 advanced by 0.57%. Futures tracking US stock indices were mixed, with the Dow Jones in the green pointing to a positive open, whereas the S&P and the Nasdaq were in the red, indicating a negative open.

COMMODITIES: Oil was one of the biggest movers over the last couple of days, posting new multi-week lows as OPEC and Russia increased supply while concerns over supply shortages in other places eased. Moreover, the US Treasury Secretary Mnuchin said on Tuesday that some crude importers may receive waivers to continue buying supplies from Iran. WTI plunged further (-0.76%) to $67.56/barrel, the lowest in four weeks after the API weekly report on US crude oil stocks indicated a rise in inventories. Moreover, Brent oil plummeted by 0.80% towards $71.58/barrel, posting a fresh 3-month low. In precious metals, gold dived to a 1-year low on Wednesday, losing 0.34% as the dollar firmed after Powell’s testimony.

Day ahead: Powell testifies before the House Financial Services Committee; US housing data & Australian jobs report pending

The Fed chief, Jerome Powell, will be testifying before the House Financial Services Committee at 1400 GMT today, telling the Senate Banking Committee on Tuesday that the US economy is “growing considerably stronger” to absorb higher interest rates this year even under rising trade risks. Following the testimony, traders will be closely listening to the Q&A session which could find lawmakers challenging Powell’s bullish tone yesterday. A few hours later at 1800 GMT, the Fed will separately publish its Beige Book which tracks the health of the economy based on the its own sources across the nation, while prior to Powell’s speech, US data on building permits and housing starts due at 1230 GMT could bring some volatility to the dollar as well. Analysts believe that building permits increased by 1.33 million in June, slightly less than in May when the figure posted an increase of 1.30mn. Housing starts, however, are expected to ease, falling from 1.35mn to 1.32mn.

In other data releases of notice, Japan is scheduled to release trade stats for the month of June at 2350 GMT. While exports are expected to grow at a slower pace of 7.0% y/y compared to 8.1% in May, imports could post a steeper slowdown, expanding by 5.3% y/y after recording an expansion of 14.0% in the previous month. A fact that could turn the trade balance positive as analysts predict, from -580.5bn yen to 534.2bn yen. Japan’s trade balance with the US and the EU separately could attract greater interest as the country has been subject to US tariffs on Japanese steel and aluminum imports since early June, with Japan refusing to accept a bilateral trade partnership as the US desires, while trade with the EU could operate under fewer restrictions in the future if the EU and the Japanese parliaments approve one of the biggest free trade deals in the world signed between the sides yesterday. Still, as the yen tends to be relatively less sensitive to data releases, the currency is not expected to react much in the wake of the data.

Meanwhile in Australia, investors will be waiting for June’s jobs report early on Thursday at 0130 GMT, which could show that the unemployment and the participation rates stood unchanged at 5.4% and 65.5% respectively. The number of employees, though, could increase by 17k, more than the 12k rise tracked in May. While wage growth is what the RBA mainly wants to see rising, minutes from its latest policy meeting showed that policymakers are optimistic that a tightening labor market could eventually drive earnings higher, helping the indebted citizens to cover their liabilities and at the same time for inflation to accelerate towards the RBA’s price target.

In oil markets, the Energy Information Administrations will issue its weekly report on US oil inventories at 1430 GMT. Yesterday, API figures indicated an addition of 0.62mn barrels in US crude oil stocks, pushing oil prices downwards. Should EIA numbers identify an increase or a smaller decline than analysts are forecasting, the market could face stronger downside pressure. For the week ending July 13, projections are for a fall of 3.622mn barrels compared to a loss of 12.63mn in the preceding week, the largest downfall since September 2016.

In equity markets, earnings season continues with American Express, Alcoa, eBay, IBM being among companies releasing quarterly results after the market closes today.

DAX Climbs To 4-Week High As Eurozone CPI Rises To 2 Percent

The DAX index has posted considerable gains in the Wednesday session. Currently, the DAX is at 12,750 up 0.71% on the day. On the release front, there are no major German or eurozone events.

A milestone was reached on Thursday, as Eurozone Final CPI reached the 2.0% threshold in the June release. On an annualized basis, Final CPI also came in at 2.0%. This marks the highest level since February 2017. As the ECB prepares to wind up its asset-purchase program, the markets are looking for clues about a possible rate hike. Such a move would likely have a significant impact on the markets, as the ECB last raised rates back in 2011. If inflation levels continue to rise, there will be more pressure on the ECB to consider a rate hike sooner rather than later.

With global protectionist winds getting stronger by the week, Japan and the EU signed a free trade agreement on Tuesday. At the signing ceremony, Prime Minister Shinzo Abe and European Council head Donald Tusk said that the deal is a response to growing concerns about protectionism. The agreement will eliminate most tariffs between the EU and Japan, and will be particularly beneficial for Japanese car makers and European food producers. No less important, the agreement marks the largest free trade agreement in the world, as the EU and Japan cover about one-third of global GDP and some 600 million people.

The Potential Of USD Growth Is Limited

Powell's speech with the semiannual report in the U.S. Congress contained an optimistic view on the economic outlook. Such a tone has reduced fears that trade wars will negatively affect economic valuations. The Fed's confidence that the years ahead of the low unemployment and sustained growth have increased the demand for risks at the stock markets.

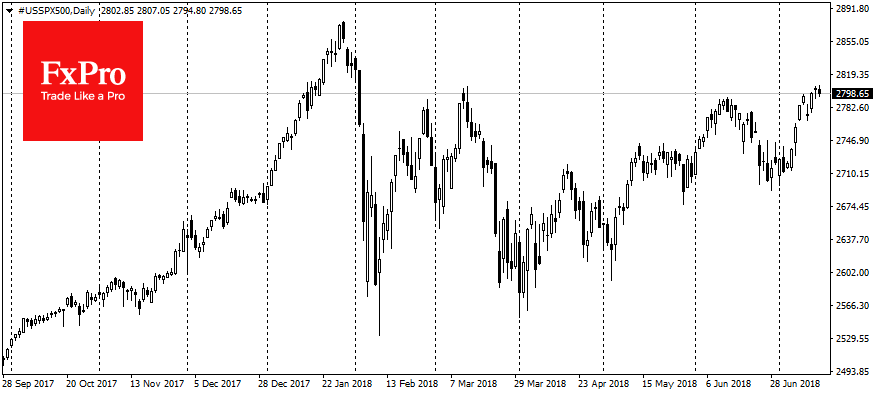

As a result, S&P500 has overcome the downturn of the previous two trading sessions and has updated the highs since February, rising by 0.6%. The credibility of the Fed's forecasts is an important factor for markets. The optimism in the estimates supports the stock indices. In the morning the Asian platforms have picked up the relay, also adding about 0.6%-1.0%.

As a result, S&P500 has overcome the downturn of the previous two trading sessions and has updated the highs since February, rising by 0.6%. The credibility of the Fed's forecasts is an important factor for markets. The optimism in the estimates supports the stock indices. In the morning the Asian platforms have picked up the relay, also adding about 0.6%-1.0%.

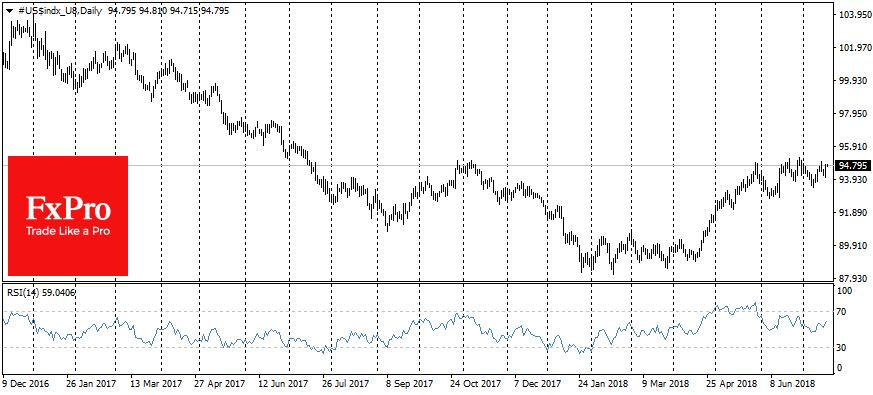

Powell's speech also helped U.S. currency. The dollar index has added 0.5% on comments that the Fed intends the raising of rates regularly further. As a result, the Dollar index returned to the area of the trading range highs for the last year. The EURUSD pair fell to 1.1650 to start of the Wednesday, USDJPY has reached 113 – the highest level for the last six months.

It should be noted that the simultaneous growth of the dollar and American stocks is quite rare and short-term phenomenon. Strengthening of the dollar reduces the competitiveness of American companies and it is often caused by a tighter monetary policy that harms equities. However, this time it is still more likely that markets will continue to grow, while USD will lose its momentum.

Entered tariffs and strengthened over the last year oil spur inflation, which undermines the real value of the dollar. A recent update of IMF projections has highlighted the trend towards accelerating growth in Emerging economies and slowing the developed. The impressive US trade deficit is alarming, which also negatively affects the currency exchange rate. It should also be noted that the Fed's plans for 4 increases this year were confirmed by yesterday's speech but had already been taken into account by the markets earlier. Under these conditions, the dollar again could become in the offensive, as it was in the 2000s, when the dollar retreated to most currencies.

From the technical perspective, strengthening of the dollar in the area of current highs, near 95 on the index DXY In November of the last year, and also in May-June of this year was accompanied by increasing of pressure on the American currency. This area of resistance can act again as a serious obstacle if new drivers for the dollar do not appear.