Sample Category Title

USD/JPY Under Pressure

Pivot (invalidation): 112.90

Our preference Short positions below 112.90 with targets at 112.55 & 112.40 in extension.

Alternative scenario Above 112.90 look for further upside with 113.10 & 113.30 as targets.

Comment As Long as the resistance at 112.90 is not surpassed, the risk of the break below 112.55 remains high.

GBP/USD The Bias Remains Bullish

Pivot (invalidation): 1.3050

Our preference Long positions above 1.3050 with targets at 1.3100 & 1.3140 in extension.

Alternative scenario Below 1.3050 look for further downside with 1.3015 & 1.2990 as targets.

Comment The RSI lacks downward momentum.

EUR/USD The Bias Remains Bullish

Pivot (invalidation): 1.1630

Our preference Long positions above 1.1630 with targets at 1.1665 & 1.1685 in extension.

Alternative scenario Below 1.1630 look for further downside with 1.1600 & 1.1575 as targets.

Comment The RSI is bullish and calls for further upside.

Bitcoin/Dollar The Downside Prevails As Long As 7504 Is Resistance

7504 is our pivot (invalidation) point.

Our preference The downside prevails as Long as 7504 is resistance.

Alternative scenario Above 7504, look for 7728 and 7861.

Comment The RSI is below 50. The MACD is below its signal line and negative. The configuration is negative. Moreover, the pair stands below its 20 and 50 MAs (respectively at 7360 and 7400).

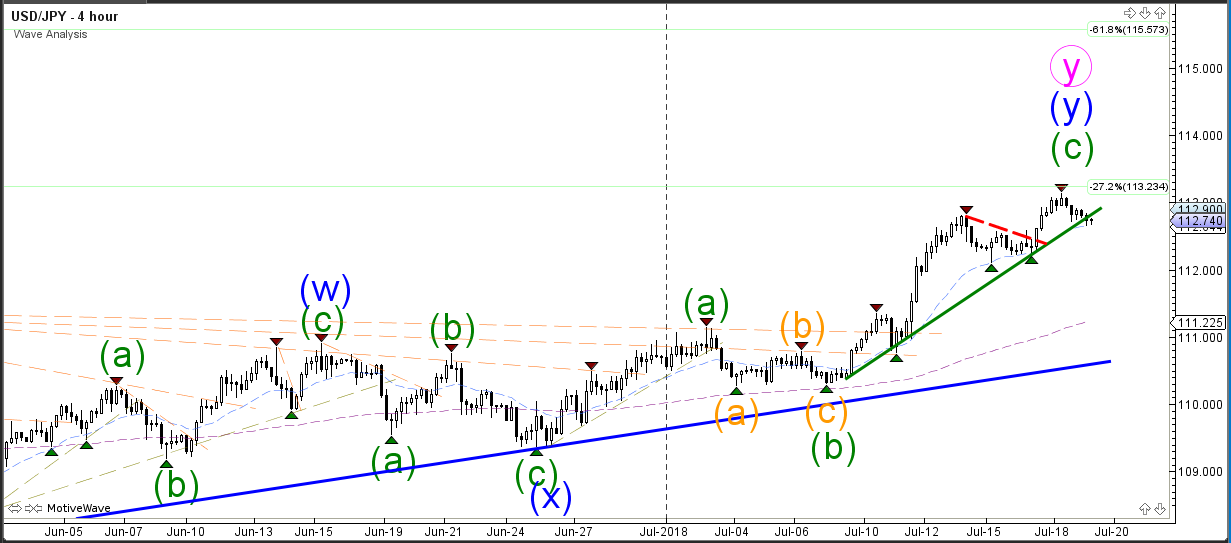

USD/JPY Bounces After Hitting -27.2% Fib Target At 113

The USD/JPY made a bearish bounce after reaching the -27.2% Fibonacci target at 113.23 and price is now challenging the support trend line (green). A new bullish breakout could indicate a continuation towards the -61.8% Fibonacci target whereas a bearish push could indicate the end of the bullish wave Y and the start of a bearish price swing.

The USD/JPY is either building a bearish correction, which could indicate more bullishness if price stays above the support levels and breaks above the resistance, or price is starting a new downtrend, but then price needs to break through the support.

EUR/USD Triangle Pattern After Bearish ABC Zigzag

The EUR/USD made a bullish bounce at the support trend line and triangle chart pattern, which is a key decision zone for a bull reversal or bear breakout.

The wave patterns indicated in the image are expecting a bullish bounce as part of a WXY (pink) correction. A bearish breakout could still be part of an expanded wave X (pink) unless price shows strong bearish momentum, which could indicate a bearish breakout and trend.

As an exception, the EUR/USD 1 hour chart offers two scenarios where both a bearish and bullish ABC pattern could be taking place. The breakout direction could indicate which ABC pattern might prevail although traders need to watch out for false breakouts as well.

Today Is A Quiet Day In Terms Of Data Releases

Market movers today

Today is a quiet day in terms of data releases. We look forward to getting the Philly Fed index in the afternoon, as it may give a further indication of whether ISM manufacturing fell in July, which the corresponding Empire index signalled.

UK retail sales are due out at 10:30 CEST but they are very volatile by nature and do not really say much about actual private consumption as measured in GDP. We still believe the Bank of England will hike at its August meeting but the likelihood has declined after the lower-than-expected inflation print yesterday.

Selected market news

There were no surprises in Fed Chair Jerome Powell's second day of testimony in front of the House Financial Services Committee, where the overall message was repeated that the FOMC will continue hiking the interest rate gradually. Like Tuesday's session in the Senate, questions yesterday were related mainly to the flattening of the yield curve and the impact on the economy from tariffs.

The 2Y10Y US yield curve steepened slightly yesterday with yields on 10Y US Treasuries rising about 2bp to 2.885%, while the broad-based DXY dollar index was little changed and thus maintained this week's gains.

The Bank of Japan (BoJ) lowered purchases of longer-dated Japanese government bonds at its regular operations this morning. The BoJ cut buying in the 10-25Y segment by JPY10bn and also cut buying in the ultra-long end with maturities beyond 25Y by JPY10bn from JPY70bn to JPY60bn. It is the fourth time since May where the BoJ has cut its overall purchases. The reduction in the purchases was widely expected in the market and comes after substantial flattening pressure on the government bond yield curve and rally in USD/JPY, which broke above 112 last week.

The weekly flow data from Norges Bank showed that foreign banks (proxy for speculative flows) last week were side-lined in NOK FX. Our expectation is that they will remain so until the very end of this month/beginning of August, which at that time will contribute to a lower EUR/NOK. In the meantime, we expect the cross to continue range trading.

In the FX majors, EUR/GBP has reached new highs following yesterday's disappointing inflation release and EUR/GBP bounced above 0.89 while GBP/USD temporarily broke below the key support level at 1.3050. While the lower-than-expected inflation in the UK on the margin reduces the probability of a rate hike August, it remains our base case that the Bank of England will raise the Bank Rate by 25bp on 2 August. Market pricing of an August hike declined 2bp to 19bp yesterday. Given the already high pricing of an August rate hike and the risk of continued political uncertainty in the UK related to Brexit, we prefer staying side-lined in the cross for now.

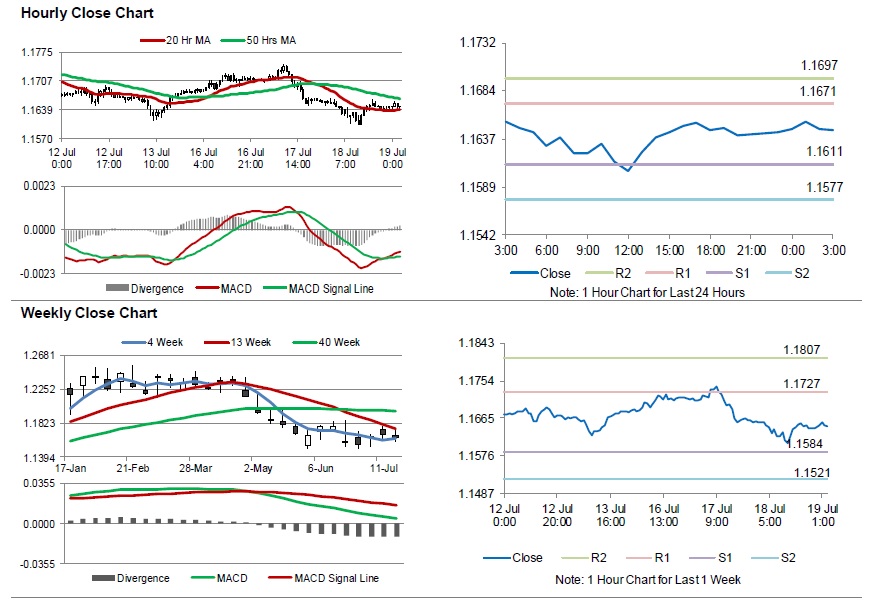

Euro-Zone’s Inflation Increases As Initially Estimated In June

For the 24 hours to 23:00 GMT, the EUR declined 0.09% against the USD and closed at 1.1644.

On the data front, Euro-zone's final consumer price index climbed 2.0% on an annual basis in June, at par with market expectations and confirming the preliminary print. The index had risen 1.9% in the prior month. Additionally, seasonally adjusted construction output rose 0.3% on a monthly basis in May. In the previous month, construction output had recorded a revised rise of 1.40%.

In the US, data revealed that building permits unexpectedly fell by 2.2% on a monthly basis to an annual rate of 1273.0K in June, for the third consecutive month and defying market consensus for a rise to a level of 1330.0K. In the preceding month, building permits had recorded a level of 1301.0K. Further, housing starts plunged 12.3% on a monthly basis to an annual rate of 1173.0K in June, reaching a 9-month low level and compared to market expectations for a drop to a level of 1320.0K. Housing starts had posted a revised level of 1337.0K in the prior month. Moreover, the nation's MBA mortgage applications eased 2.5% in the week ended 13 July 2018, compared to an advance of 2.5% in the previous week.

Meanwhile, according to the Federal Reserve's (Fed) Beige Book report, economic activity in the US continued to expand at a moderate pace in June. Further, it revealed that overall prices and employment increased at a modest to moderate pace. However, businesses expressed concerns over tariffs and new trade policies.

In the Asian session, at GMT0300, the pair is trading at 1.1646, with the EUR trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.1611, and a fall through could take it to the next support level of 1.1577. The pair is expected to find its first resistance at 1.1671, and a rise through could take it to the next resistance level of 1.1697.

Amid no major macroeconomic releases in the Euro-zone today, investors would look forward to the US initial jobless claims followed by the Philadelphia Fed manufacturing survey for July and the leading index for June, slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

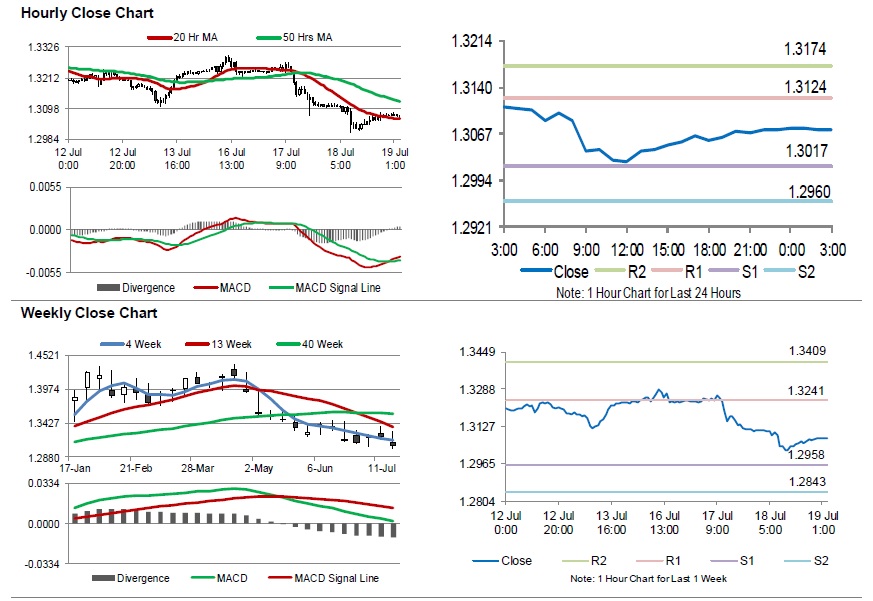

Weak Inflation Data, Dull Prospects For August Rate Hike

For the 24 hours to 23:00 GMT, the GBP declined 0.24% against the USD and closed at 1.3075 amid weak inflation figures.

In the economic news, UK's consumer price index climbed 2.4% on an annual basis in June, marking its slowest pace in 14 months, falling short of market expectations for a rise of 2.6%. The index had registered a similar rise in the previous month. Moreover, non-seasonally adjusted output producer price index rose 3.1% on an annual basis in June, less than market expectations for an advance of 3.2%. In the prior month, output producer price index had registered a revised rise of 3.0%. Further, the nation's retail price index increased 3.4% on monthly basis in June, compared to an advance of 3.3% in the prior month. Market participants had envisaged the index to rise 3.5%. Additionally, UK's house price index jumped 3.0% on yearly basis in May, rising at its weakest pace in 5-years, while market consensus was for an advance of 3.7%. In the preceding month, the index had recorded a revised gain of 3.5%.

In the Asian session, at GMT0300, the pair is trading at 1.3074, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.3017, and a fall through could take it to the next support level of 1.2960. The pair is expected to find its first resistance at 1.3124, and a rise through could take it to the next resistance level of 1.3174.

Going ahead, traders would focus on UK's retail sales data for June, due to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

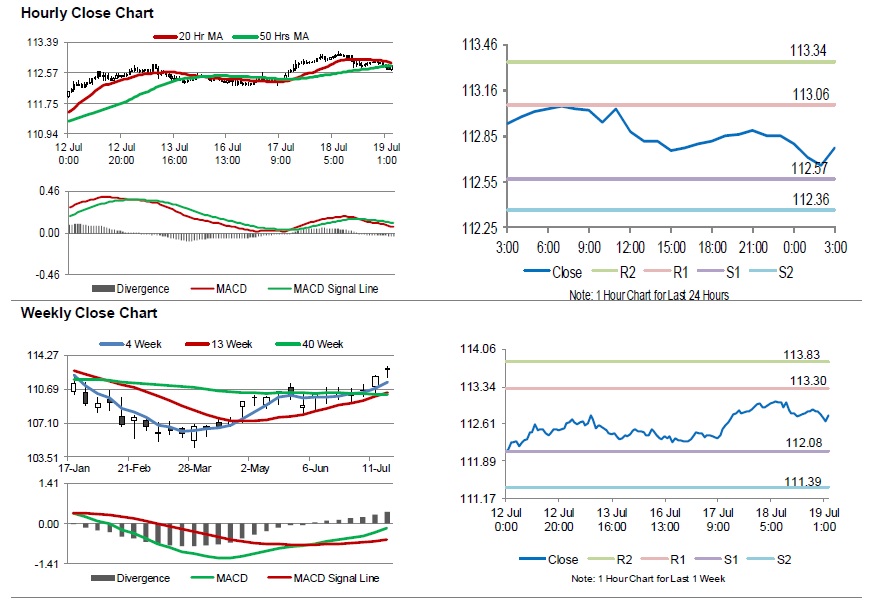

Japan Reported A Trade Surplus In June

For the 24 hours to 23:00 GMT, the USD declined 0.09% against the JPY and closed at 112.85.

In the Asian session, at GMT0300, the pair is trading at 112.77, with the USD trading 0.07% lower against the JPY from yesterday’s close.

The Japanese yen climbed against the dollar, after Japan posted a trade surplus of ¥721.4 billion in June, following a trade deficit of ¥578.3 billion in the prior month.

The pair is expected to find support at 112.57, and a fall through could take it to the next support level of 112.36. The pair is expected to find its first resistance at 113.06, and a rise through could take it to the next resistance level of 113.34.

Going forward, investors would closely monitor Japan’s final machine tool orders for June, due to be released in a while and the national consumer price index for June, set to release overnight.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.