Sample Category Title

Silver: White Metal Trading Higher This Morning

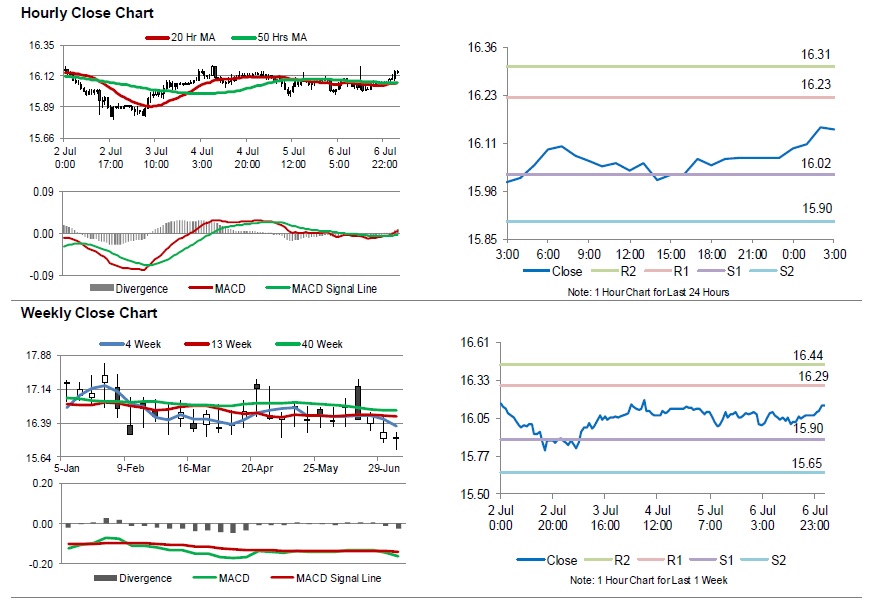

For the 24 hours to 23:00 GMT, Silver declined 0.12% against the USD and closed at USD16.07 per ounce on Friday.

In the Asian session, at GMT0300, the pair is trading at 16.15, with silver trading 0.47% higher against the USD from Friday’s close.

The pair is expected to find support at 16.02, and a fall through could take it to the next support level of 15.90. The pair is expected to find its first resistance at 16.23, and a rise through could take it to the next resistance level of 16.32.

The white metal is trading above its 20 Hr and 50 Hr moving averages.

Crude Oil: Oil Extends Its Gains In The Morning Session

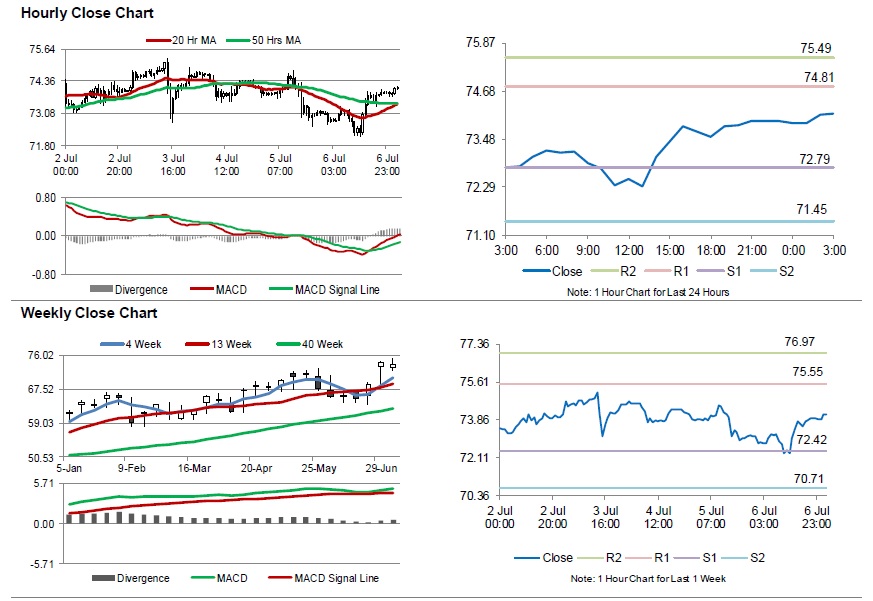

For the 24 hours to 23:00 GMT, Crude Oil rose 1.00% against the USD and closed at USD73.83 per barrel on Friday.

Baker Hughes disclosed that the number of active oil rigs in the US rose by 5 to 863 in the week ended 06 July 2018.

In the Asian session, at GMT0300, the pair is trading at 74.12, with oil trading 0.39% higher against the USD from Friday’s close.

The pair is expected to find support at 72.79, and a fall through could take it to the next support level of 71.45. The pair is expected to find its first resistance at 74.81, and a rise through could take it to the next resistance level of 75.49.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

BOC Preview – Rate Hike Fully Priced In, Data and Trade with US Continue to Guide Future Path

Since the BOC meeting in May, at which the policymakers removed the “cautious” rhetoric, the market has been raising its bet on a July rate hike. As of today, the market has priced in over 90% chance of a +25 bps rate hike at this week’s meeting. GDP growth in April (released in June) reinforced the underlying strength in domestic economy. The employment situation remained firm. However, while June payrolls increased, the unemployment rate also climbed higher. Headline CPI in May missed expectations but still exceeded BOC’s target of +2%. Core CPI eased for a second consecutive month. The ongoing uncertainty is future trade relations with the US, including NAFTA renegotiation, and US’ imposition of trade tariff and Canada’s retaliatory measures. After all, BOC’s monetary policy stance should continue to be data-dependent.

GDP growth in April eased to +0.1% q/q, but beat expectations of no growth. In the first quarter, GDP expanded +0.3% q/q and an annualized rate of +1.3%. The moderation in April growth was attributed to temporary factors, including to adverse weather a number of maintenance shutdowns in the oil sands sector, which would have dissipated in the second quarter. Headline inflation rate steadied at +2.2% y/y in May, compared with consensus of +2.6%. Energy prices, surging +11.6% as driven by a +23% jump in gasoline price, were offset by falling prices in other areas including telephone services, traveler accommodation and computers. Excluding energy, inflation steadied +1.6%, down from +1.9% in April. Core CPI, excluding energy and food, eased to +1.7%, from +1.8% in April and +1.9% in March. BOC’s three core measures all averaged at +1.9% for the month.

On the job market, payrolls in June increased +31.8K, beating consensus of +24K and May’s contraction of -7.5K. The increase in payrolls mainly came from goods-producing. Indeed, services employment fell after 4 months of solid gains. Unemployment rate climbed +0.2 percentage point to +6%. Since the rise in the unemployment rate was driven by a +0.2 percentage point growth in the participation rate, and given the fact that the unemployment rate still stays at the lowest level in decades, the overall job market in Canada remains upbeat. Wage growth eased slightly to +3.5% y/y. The strongest momentum came from Ontario and British Columbia provinces. Both provinces raised minimum wages this year.

While economic developments have largely come in line with BOC’ April forecast, the major uncertainty is the uncertain trade relations between Canada and the US. Besides the slow progress of NAFTA negotiations, US unexpected imposition of steel and aluminum tariff on Canada has triggered retaliatory measures from the latter. Meanwhile, Trump has lately threatened to impose tariff on auto imported from Canada. These have inevitably posed downside risk on Canada’s growth outlook

We expect BOC to adopt a so-called “dovish tightening” at the upcoming meeting. While announcing to raise the policy rate by +25bps to 1.5%, policymakers would reaffirm the uncertainty of the trade outlook and reiterate that further monetary policy decision would depend on incoming data.

Market Morning Briefing: Pound Is Trading Close To Resistance On Daily Candles Near 1.33

STOCKS

Dow (24456.48, +0.41%) moved up while support near 24000 holds just now. Some sideways trade in the 24000-24750 region is possible in the coming sessions before the index moves up further. Near term looks bullish.

Dax (12496.17, +0.26%) has also moved up and looks bullish for the coming sessions targeting 12800-13000.

Nikkei (22063.74, +1.26%) has broken above 22000 level and if the index sustains above 22000, it could target higher levels of 22400-22600 in the medium term.

Shanghai (2789.08, +1.52%) has room on the downside towards 2700-2650. We do not expect a fall below 2650 in the longer run. The fall is likely in its last phase of the fall and would soon start rising back towards 2800+ levels to move higher in the longer run.

Important level to watch in Nifty (10772.65, +0.21%) is 10800. While the index trades below 10800, bearishness could persist. A sustained break above 10800 would trigger some medium term bullishness. Watch price action near 10800.

COMMODITIES

Gold (1259.50) has chances of testing 1270-1280 on the upside while above 1240.Near term looks bullish.

The Gold-WTI ratio could test resistance near 19 and could come off from there by end of the week.

Brent (77.50) and Nymex WTI (74.12) may come down to test 75 and 65 respectively before again moving up in the medium term. Immediate view is bearish with important supports near 75 and 65 respectively.

Copper (2.8610) has tried to move up a bit. But while the price remains below 2.90/95, bearishness is likely to continue.

FOREX

Euro (1.1761): With Dollar weakening due to the trade war initiation on Friday, Euro strengthened past resistance near 1.172 and could now move up to 1.185 in 1-2 weeks. The early part of this week could see an upmove towards 1.18. Some resistance near 1.1816 (13 weeks MA) could provide a pause in the upmove towards 1.185. The ECB Meeting minutes’ release on Thursday would be very important.

Dollar Index (93.92): Dollar weakened on Friday due to the beginning of the US-China trade war. It is currently at support near 93.8 on daily candles and daily line chart. This support could prove to be an interim one, with a further downmove towards 93.2 looking likely by next week.

Dollar Yen (110.46): Looking at weekly candles and 3 day line chart, some scope for 1 more week of ranging to bullish movement towards 111.5 seems possible. However with long term resistance @ 111.5, we are expecting Dollar Yen to turn bearish soon. A decisive break below 110.25-110.00 would be required for it to turn bearish.

Euro Yen (129.91): Euro Yen is currently close to resistance on both short term and long term charts. With our forecast for the current week being bullish for Euro and ranged to bullish for Dollar Yen, we might just see Euro Yen test levels near 130-131. However, with Dollar Yen expected to turn bearish after few sessions, Euro Yen could also turn bearish parallely.

Pound (1.3295): As per expectation, Pound is trading close to resistance on daily candles near 1.33 and might dip from here in this week towards 1.32-1.31. Pound seems to be bearish in the medium term. A break of 1.30 would be important for medium term bearishness.

Dollar Rupee (opened at 68.57):

Resistance at 69.00-10 has held well. Global Dollar weakness might be reflecting in the gap-down opening today.

INTEREST RATES

The first official tariff announcement between US and China happened on Friday and gave further impetus to the risk averseness sentiment prevailing at present.

German 10 year bond yield (0.292%) has broken support near 0.3% and could dip lower towards 0.2% in the coming 1-2 weeks.

US 10 year yield (2.84%), 30 Year (2.944%), 5 Year (2.7365%), 2 Year (2.549%):

The US 10-2 Yield Spread (0.291%) could fall towards 0.2% in the weeks ahead. This fall could turn out to be faster than markets are expecting.

The 10 Year yield looks bearish towards 2.75% while the 30 Year yield could test levels near 2.9%.

China foreign currency reserves rose 0.05% in June

China's foreign currency reserves rose USD 1.5B in June to USD 3.1121T, up 0.05%. The State Administration of Foreign Exchange spokesperson said that the China's foreign exchange market was "generally stable". Due to strength in the US Dollar and change in asset pricing, the overall currency reserve rose slightly.

SAFE also noted that since the start of the year, China's economy has "maintained a steady trend". But there were "divergence" in global recovery, heightened trade friction, capital out-flow and currency depreciation pressure in emerging markets. Though, China's cross-border capital flowed remained stable.

Sterling spiked on Brexit plan but reversed after Davis’s resignation

UK Prime Minister Theresa May appeared to have united her cabinet on the Brexit plan after the locked-up meeting at the Chequer last Friday. A key element of the plan is to establish a UK-EU free trade area with a common rule book for industrial goods and agricultural products. And the UK would commit by treaty to ongoing harmonization with EU rules on goods. However, on services, the UK will strike different arrangements for regulatory flexibility. And for financial services, the UK will seek arrangements that preserve the mutual benefits of integrated markets and protect financial stability. And, with the plan, the UK believed that the problem of Irish border would be avoided an a backstop plan won't be needed. The full document is expected to be published this week.

Environment Secretary Michael Gove, on the the highest-profile Brexit campaigners, endorsed the plan. He told BBC that "One of the things about politics is that you mustn't, you shouldn't, make the perfect the enemy of the good. And one of the things about this compromise is that it unites the cabinet." And he urged that "All those of us who believe that we want to execute a proper Brexit, and one that is the best deal for Britain, have an opportunity now to get behind the Prime Minister in order to negotiate that deal."

However, the situation is complicated today as Brexit Minister David Davis resigned as he was not willing to be a "reluctant conscript" to the plan. He complained that "the general direction of policy will leave us in at best a weak negotiating position, and possibly an inescapable one." And the so called "common rule book" with the EU will hand "control of large swathes of our economy to the EU and is certainly not returning control of our laws". Separately, it's reported that Steve Baker, a minister in the Brexit department has also resigned.

Sterling spiked higher earlier today and reversed on Davis's resignation.

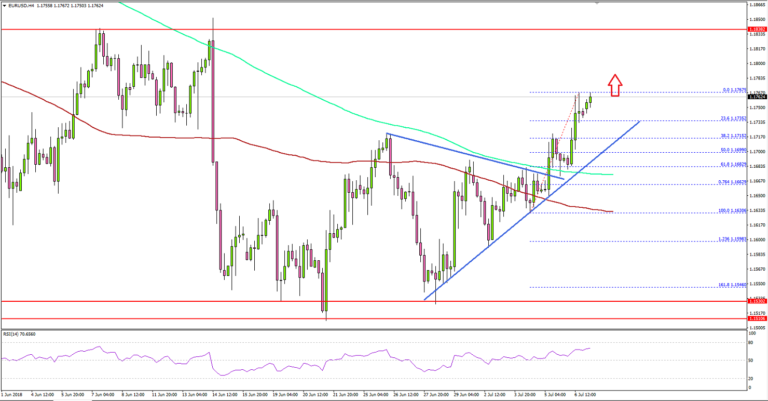

EUR/USD Could Accelerate Gains Above 1.1750

Key Highlights

- The Euro traded higher recently and moved above the 1.1680 resistance against the US Dollar.

- There is a major bullish trend line formed with support at 1.1715 on the 4-hours chart of EUR/USD.

- The US NFP figure in June 2018 posted 213K, more than the forecast of 195K.

- Today in the US, the Consumer Credit Change in May 2018 will be released, which is forecasted to post $11.50B, more than the last $9.26B.

EURUSD Technical Analysis

The Euro gained traction this past week and moved above the 1.1680 and 1.1700 resistance levels against the US Dollar. The EUR/USD pair is currently placed in a bullish zone and it could trade further above 1.1750.

Looking at the 4-hours chart, the pair started a fresh upside wave from the 1.1630 swing low. It broke the 1.1650 and 1.1680 resistance levels. There was also a break above a major bearish trend line with resistance at 1.1665.

The pair closed above the 1.1680 resistance, 100 simple moving average (red, 4-hours) and the 200 simple moving average (green, 4-hours). The pair traded as high as 1.1767 and is currently consolidating gains.

An initial support is near the 1.1720 level and the 38.2% Fib retracement level of the last wave from the 1.1630 low to 1.1767 high. There is also a major bullish trend line formed with support at 1.1715 on the 4-hours chart of EUR/USD.

Therefore, as long as the pair is above the 1.1715-1.1720 support area, there are chances of more upsides in the near term. On the upside, resistances are at 1.1780 and 1.1800.

Recently in the US, the Nonfarm Payrolls report for June 2018 was released by the US Department of Labor. The market was looking for an increase of 195K jobs, compared with the last 223K.

The result was well above the forecast, as the US NFP figure in June 2018 posted 213K. The last reading was also revised up from 223K to 244K. On the flip side, the unemployment rate increased sharply from 3.8% to 4.0%.

The report added that:

The unemployment rate rose by 0.2 percentage point to 4.0 percent in June, and the number of unemployed persons increased by 499,000 to 6.6 million. A year earlier, the jobless rate was 4.3 percent, and the number of unemployed persons was 7.0 million.

The rise in the unemployment rate increased bearish pressure on the US Dollar. EUR/USD and GBP/USD gained traction and moved higher after the result, but gains were limited.

Economic Releases to Watch Today

- Germany's Trade Balance for May 2018 – Forecast €20.0B, versus €19.4B previous.

- Germany's Imports of goods and services May 2018 – Forecast +0.6%, versus +2.2% previous.

- Germany's Exports of goods and services May 2018 – Forecast +0.4%, versus -0.3% previous.

- US Consumer Credit Change May 2018 – Forecast $11.50B, versus $9.26B previous.

UK Brexit Minister David Davis’s resignation letter to PM May

The following is David Davis's resignation letter to Prime Minister Theresa May.

Dear Prime Minister,

As you know there have been a significant number of occasions in the last year or so on which I have disagreed with the Number 10 policy line, ranging from accepting the Commission's sequencing of negotiations through to the language on Northern Ireland in the December Joint Report. At each stage I have accepted collective responsibility because it is part of my task to find workable compromises, and because I considered it was still possible to deliver on the mandate of the referendum, and on our manifesto commitment to leave the Customs Union and the Single Market.

I am afraid that I think the current trend of policy and tactics is making that look less and less likely. Whether it is the progressive dilution of what I thought was a firm Chequers agreement in February on right to diverge, or the unnecessary delays of the start of the White Paper, or the presentation of a backstop proposal that omitted the strict conditions that I requested and believed that we had agreed, the general direction of policy will leave us in at best a weak negotiating position, and possibly an inescapable one.

The Cabinet decision on Friday crystallized this problem. In my view the inevitable consequence of the proposed policies will be to make the supposed control by Parliament illusory rather than real. As I said at Cabinet, the common rule book policy hands control of large swathes of our economy to the EU and is certainly not returning control of our laws in any real sense.

I am also unpersuaded that our negotiating approach will not just lead to further demands for concessions.

Of course this is a complex area of judgment and it is possible that you are right and I am wrong. However, even in that event it seems to me that the national interest requires a Secretary of State in my Department that is an enthusiastic believer in your approach, and not merely a reluctant conscript. While I have been grateful to you for the opportunity to serve, it is with great regret that I tender my resignation from the Cabinet with immediate effect.

Yours ever,

David

BCC pushes for clarify and Brexit hedge

According to the Quarterly Economic Survey of the British Chambers of Commerce (BCC), the UK economic conditions "remain sluggish" despite modest improvement in Q2. The survey showed that the economy is in a "holding pattern" and the annual growth this year is set to be the "lowest since the financial crisis." It called for a push to "fix the fundamentals" to create a "Brexit hedge". And the government should provide clarity on the "real-world questions" after Brexit to give businesses a clear path that would enable them to invest and grow.

Adam Marshall, Director General of the BCC also noted in the release that "amid growing international uncertainty, from escalating trade disputes to oil price rises, the UK economy continues to grow at a sluggish rate. Brexit is a key factor – but long-standing structural issues are also holding companies' growth back." And he emphasized again that

"Business needs clarity on Brexit, and a strong domestic agenda that creates a 'Brexit hedge' as we navigate turbulence over the next few years."

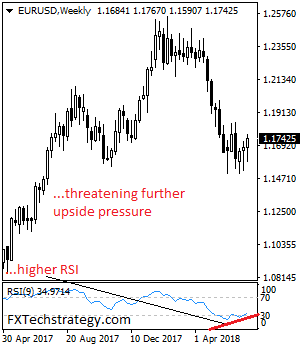

EURUSD – Faces Further Upside Pressure On Correction

EURUSD - The pair still faces further upside pressure on recovery. On the upside, resistance comes in at 1.1700 level with a cut through here opening the door for more upside towards the 1.1750 level. Further up, resistance lies at the 1.1800 level where a break will expose the 1.1850 level. Conversely, support lies at the 1.1600 level where a violation will aim at the 1.1550 level. A break of here will aim at the 1.1500 level. Below here will open the door for more weakness towards the 1.1450. All in all, EURUSD faces further upside pressure but with caution of a recovery.