Sample Category Title

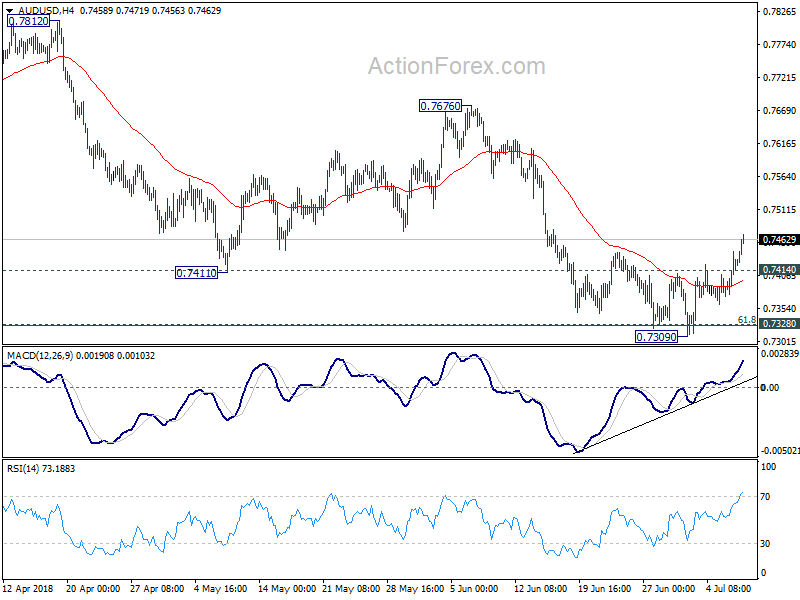

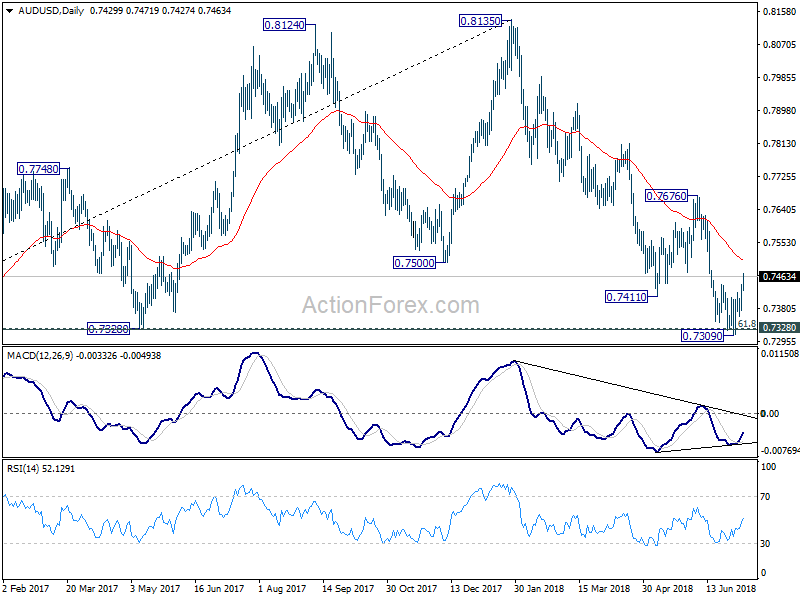

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7387; (P) 0.7416; (R1) 0.7456; More...

Intraday bias in AUD/USD remains on the upside as rebound from 0.7309 short term bottom continues. Further rally could be seen to 55 day EMA (now at 0.7508) and possibly above. But upside should be limited below 0.7676 resistance to bring fall resumption. On the downside, below 0.7414 minor support will turn bias to the downside for retesting 0.7309 low first. Sustained break of 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

Investors Shrug Off Trade Fears, Pound Resilient After Davis Resignation

Trade frictions dominated the headlines last week, but Wall Street investors shrugged off worries of an escalating trade war and instead cheered the U.S. jobs report. 213,000 jobs were added to the U.S. economy in June, easily beating the forecasted 195,000. Meanwhile, May’s figure was revised upward, to 244,000 from 223,000. Wage growth fell short of the anticipated 2.8% y-o-y growth, coming in at 2.7%. However, the combination of strong jobs growth and limited wage inflation has always been a positive ingredient for stocks for a simple reason. Robust jobs growth reflects the strength in the economy, while weak wage inflation gives more flexibility to the Federal Reserve in their tightening process.

The music may stop playing at any time however, if investors become convinced that the trade dispute is moving in the wrong direction. So far, the U.S. has imposed tariffs on $34 billion of imports from China, as did China on U.S. imports. This stage has been clearly priced in and when looking at Asian equityperformance today, investors seem unconvinced that an all-out trade war will be launched. However, given President Trump’s unpredictability, the upside momentum is likely to remain limited, particularly in cyclical stocks until we have more clarity on trade.

In FX markets the Dollar Index fell to its lowest level since 14June, to trade below 94 as a result of the stagnant wage growth. Traders need to keep a close eye on Thursday’s U.S. Consumer Price Index which is anticipated to increase 2.9% y-o-y, making it the largest annual rise since February 2012. If the CPI crossesthe 3% benchmark,expect dollar bulls to return strongly as it means the Fed has no alternative but to keep tightening policy further.

Meanwhile, the pound was surprisingly steady after the resignation of the Brexit Secretary David Davis. GBPUSD traded near 1.3300 at the time of writing. Trading the pound is going to be tricky in the coming days and will depend predominantly on how the negotiations with the E.U. develop after Davis’ resignation and the survival of Theresa May. However, from Monday’s market reaction, traders seem to believe we’re still heading towards a soft Brexit.

Oil prices started the week on a positive note despite the fact that U.S. active Oil rigs rose by 5 last week. Trump’s tweets on pushing OPEC to increase production proved to have limited impact on dragging prices so far. Backwardation continued to steepen on the Brent and WTI futures curves, reflecting tightness in Oil markets. All eyes will be on OPEC’s production this month,particularly from Saudi Arabia, after Trump urged the organization to act to bring prices down.

Equities Remain Positive In Light Of Trade Tariffs

General Trend:

- Asian equities rise as markets in China and Hong Kong advance

- Chinese yuan and Aussie gain amid rise in Chinese equities

- China FX reserves rose in June for the first time in 4 months, government cites factors including rise in the US dollar

- Some analysts see risk that the RBA’s rate guidance could be altered due to global trade situation

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.2%

- TOPIX Electric Appliances index +1.4%, Information & Communications +1.4%, Real Estate +1.3%, Securities +1.2%, Iron & Steel +0.7%

- Japanese automakers and megabanks trade generally higher

- (JP) Japan Jun Lending Ex-Trusts y/y: 2.1% v 1.9% prior; Including Trusts y/y: 2.2% v 2.0% prior

- (JP) JAPAN MAY BOP CURRENT ACCOUNT BALANCE: ¥1.94T V ¥1.27TE; ADJ CURRENT ACCOUNT: ¥1.85B V -¥1.18TE; Trade Balance BoP Basis -¥303.9B v -¥483.1Be

- Honda, 7267.JP To partner with Panasonic in the area of portable lithium-ion batteries - Japanese Press

- 4523.JP Eisai and Biogen Announce Phase 2 Positive Topline Results of the Final Analysis for BAN2401 at 18 Months (+16% daily limit)

- (JP) BoJ Gov Kuroda: Reiterates will adjust monetary policy as needed to maintain economy's momentum to achieve its price target

- (JP) METI: Sees Japan July-Sept quarter crude steel production +2.3% y/y

Korea

- Kospi opened +0.2%

- (KR) South Korea H1 Avg grain price +19.8% y/y, the largest increase on record - Korean press

- (KR) South Korea trade ministry is working on finalizing the members of the delegation for Washington's public hearing on auto tariffs, scheduled for later this month - Korean press

- (KR) US Sec of State Pompeo visit to North Korea seemed to be viewed negatively by North Korea after accusing the US of "gangster-like tactics" and increasing the "risk of war". Pompeo commented: the two sides had “good-faith, productive conversations which will continue in the days and weeks ahead

- (KR) South Korea Finance Min Official: May issue 50-yr bonds on regular basis depending on market demand; plans to help develop liquid market for 50-yr gov't bonds

- (KR) South Korea Deputy Fin Min Hung-kwon: CPI to accelerate in H2 due to rise in global oil prices - Korean press

China/Hong Kong

- Hang Seng opened +1.0%, Shanghai Composite +0.2%

- Hang Seng Services index +2.5%, Consumer Goods +2.4%, Property/Construction +2.3%, Info Tech +2.1%, Energy +1.9%, Industrial Goods +1.9%, Materials +1.8%, Telecom +1.7%, Financials +1.4%,

- (CN) China PBOC Gov Yi Gang: Reiterates to maintain prudent and neutral monetary policy

- (CN) CHINA JUN FOREIGN RESERVES: $3.1121T V $3.1106T PRIOR (first rise in 4 months)

- (US) On Friday, the USTR set a 90-day deadline for exclusions from the tariffs on goods from China

- (CN) There is speculation that China might delay new rules aimed at wealth management products due to market turmoil - Chinese press

- Xiaomi IPO opens for trade, 1810.HK Opens for trade at HK$16.60/shr v HK$17.00/shr pricing

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 3rd consecutive day: Net: CNY0B drain v CNY110B drain prior

- (CN) China PBoC set yuan reference rate at 6.6393 v 6.6336 prior

- (CN) China financial institutions and economists see H1 GDP growth at 6.7% - Xinhua

- (CN) China FX Regulator SAFE: In June FX reserves rose due to fall in non-dollar currencies against the US dollar and asset price changes

- (CN) China Securities Regulatory Commission (CSRC) planning to allow foreign individual investors to trade domestic A shares through local brokers - SCMP

- (CN) China continues to try and get EU to join it in coalition against US trade policies; to offer preferential treatment and faster investment negotiations

- Looking ahead: China June CPI and PPI due in tomorrow’s session

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX Financials index +0.4%

- (AU) Australia senior Labor official calling for a royal commission into retail electricity pricing; Greens are looking to introduce a bill for a commission of inquiry into the space - Australian

- SPK.AU NZ Commerce Commission: To move forward with proceedings related to historical billing; Affirms FY18 guidance

- (AU) NAB notes chatter that trade, higher bank funding costs and tighter credit conditions could mean that the RBA’s next move could be a rate cut, suggests investors could start to price in some probability of a rate cut but hurdle for rate cut is seen as high– US financial press

North America

- (US) Trump Administration suspends risk adjustment payments related to the Affordable Care Act (ACA) - US financial press

- Looking ahead: US President Trump to attend NATO summit which he is supposed to reiterate position on more equal funding; then will attend meeting with President Putin

Europe

- (EU) ECB Coeure: ECB is not complacent to trade-war risks, June decision took account of trade and other risks

- (UK) Brexit Sec David Davis has resigned from govt

- (UK) Resigned Brexit Sec Davis: PM May's policy now more likely to break manifesto pledge, have been a significant number of times over the last year have disagreed with May; General direction of May's policy will leave UK in a "at best a weak negotiating position" - resignation letter

- (UK) British Chambers of Commerce (BCC): Bank of England (BoE) rhetoric around raising rates looks 'ill-judged'

- (IE) Ireland Jun Construction PMI: 58.4 v 61.8 prior

Levels as of 01:30ET

- Hang Seng +1.5%; Shanghai Composite +1.8%; Kospi +0.6%; Nikkei225 +3.0%; ASX 200 +0.3%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.3%, Dax +0.4%; FTSE100 +0.4%

- EUR 1.1743-1.1767; JPY 110.35-110.53; AUD 0.7428-0.7464;NZD 0.6830-0.6845

- Aug Gold +0.4% at $1,260/oz; Aug Crude Oil +0.4% at $74.11/brl; Sept Copper +1.7% at $2.87/lb

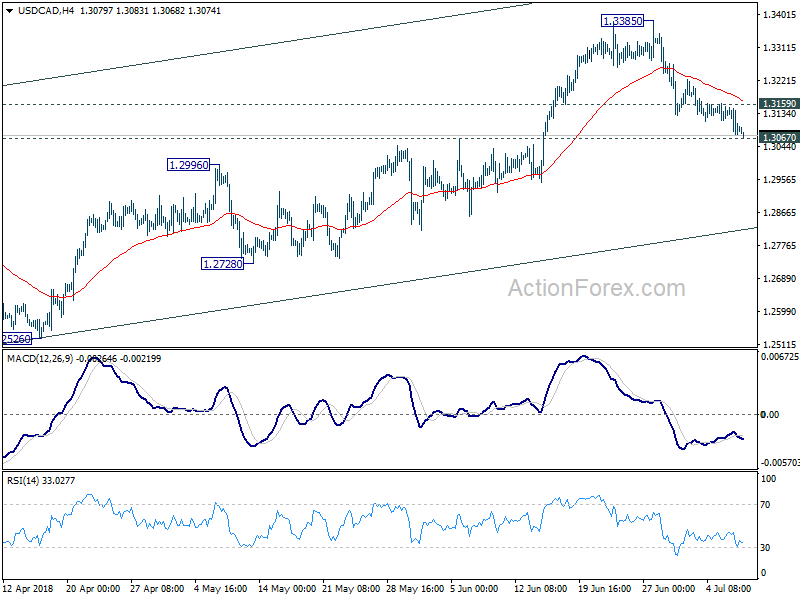

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3059; (P) 1.3109; (R1) 1.3145; More...

USD/CAD's decline from 1.3385 continues today an reaches as low as 1.3083 so far. At this point, we're still expecting strong support around 1.3067 resistance turned support to bring rebound. Above 1.3159 minor resistance will flip bias back to the upside for retesting 1.3385. However, firm break of 1.3067 will bring deeper fall to channel support (now at 1.2825).

In the bigger picture, as long as channel support (now at 1.2825) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

Sterling Volatile on Brexit Jitters, Yen Lower as Chinese Stocks Lead Asian Rebound

Yen trades broadly lower today, followed by Dollar, as Asian markets recovered broadly. China's Shanghai SSE composite leads the way by gaining 1.9% and breaches 2800 handle. It looks like some solid support was obtained between 2016 low at 2638 and 2700 psychological. Current momentum warrants a near term rebound which would likely support other Asian markets too. Nikkei also closed higher by 1.21% at 22052.18. Receding risk aversion is support the Australian Dollar, which is so far trading as the strongest one. Euro follows as the second strongest. Some volatility is seen in Sterling on Brexit jitters. Canadian Dollar also extends recent rebound on anticipation of a BoC rate hike later in the week.

Technically, the immediate level the watch today is 1.3067 in USD/CAD. Firm break will at least extend the pull back from 1.3385 to channel support at 1.2825. That will also raise the chance of medium term reversal, but it's too early to tell. 0.9855 support in USD/CHF, if broken, will bring Swiss Franc into the rally party against Dollar. Also, break of 130.33 resistance in EUR/JPY will be a solid indication of reversal of the fall from 137.49.

Sterling spiked on Brexit plan but reversed after Davis's resignation

UK Prime Minister Theresa May appeared to have united her cabinet on the Brexit plan after the locked-up meeting at the Chequers last Friday. A key element of the plan is to establish a UK-EU free trade area with a common rule book for industrial goods and agricultural products. And the UK would commit by treaty to ongoing harmonization with EU rules on goods. However, on services, the UK will strike different arrangements for regulatory flexibility. And for financial services, the UK will seek arrangements that preserve the mutual benefits of integrated markets and protect financial stability. And, with the plan, the UK believed that the problem of Irish border would be avoided an a backstop plan won't be needed. The full document is expected to be published this week.

Environment Secretary Michael Gove, on the the highest-profile Brexit campaigners, endorsed the plan. He told BBC that "One of the things about politics is that you mustn't, you shouldn't, make the perfect the enemy of the good. And one of the things about this compromise is that it unites the cabinet." And he urged that "All those of us who believe that we want to execute a proper Brexit, and one that is the best deal for Britain, have an opportunity now to get behind the Prime Minister in order to negotiate that deal."

However, the situation is complicated today as Brexit Minister David Davis resigned as he was not willing to be a "reluctant conscript" to the plan. He complained that "the general direction of policy will leave us in at best a weak negotiating position, and possibly an inescapable one." And the so called "common rule book" with the EU will hand "control of large swathes of our economy to the EU and is certainly not returning control of our laws". Separately, it's reported that Steve Baker, a minister in the Brexit department has also resigned.

Sterling spiked higher earlier today and reversed on Davis's resignation.

BCC pushes for clarify and Brexit hedge

According to the Quarterly Economic Survey of the British Chambers of Commerce (BCC), the UK economic conditions "remain sluggish" despite modest improvement in Q2. The survey showed that the economy is in a "holding pattern" and the annual growth this year is set to be the "lowest since the financial crisis." It called for a push to "fix the fundamentals" to create a "Brexit hedge". And the government should provide clarity on the "real-world questions" after Brexit to give businesses a clear path that would enable them to invest and grow.

Adam Marshall, Director General of the BCC also noted in the release that "amid growing international uncertainty, from escalating trade disputes to oil price rises, the UK economy continues to grow at a sluggish rate. Brexit is a key factor – but long-standing structural issues are also holding companies' growth back." And he emphasized again that

"Business needs clarity on Brexit, and a strong domestic agenda that creates a 'Brexit hedge' as we navigate turbulence over the next few years."

ECB Coeure: Europe United to respond to US shift from hegemonia to arkhe

ECB Executive Board Member Benoit Coeure the recent developments in trade war "doesn't have the potential to derail the recovery" of the Eurozone. Just after ECB announced to end the asset purchase program in December, the risks of US-China trade war has turned from rhetorics into reality. And the US is threatening tariffs on European Union autos. But Coeure said that the June monetary policy decision "already takes the risks into account" and there is "no reason to change policy expectations" right now. He added the the impact of trade tensions on business confidence is so far "limited" and "the backdrop is very strong resilient growth in the Eurozone".

Coeure also delivered a speech titled "Asserting Europe's Leadership". He noted that US leader in the past seven decades was "hegemonia" built on "trust and common identities". But the "America First" policy marked a departure from a "legitimate hegemon". It's turning into "arkhe" where "policies and doctrines are imposed on others, without their consent and regardless of the consequences". And, "international agreements are repealed, the international rule of law is questioned and other nations are challenged."

Coeure said EU's response, as seen with ancient Greeks, were alliances against arkhe. That is, "Europe united" against "America first". In particular, he stressed the importance of "completing the euro area's architecture" as it's necessary for Europe to attain other objectives on fostering cooperation on security and defence, speak with one voice on international affairs and to complete the Single Market.

BoJ Kuroda to maintain ultra loose policy until inflation hits target

BoJ Governor Haruhiko Kuroda said at a quarterly meeting of regional branch managers that the central bank would maintain its ultra-loose monetary policy until inflation hits 2% target. He added that the economy is expanding moderately and is expected to continue with it. Consumer inflation, however, is moving between 0.5% to 1.0%.

BoJ will continue to pursue current policy under the yield curve control framework for as long as needed. The monetary policy will be adjusted when necessary to maintain economic momentum.

China foreign currency reserves rose 0.05% in June

China's foreign currency reserves rose USD 1.5B in June to USD 3.1121T, up 0.05%. The State Administration of Foreign Exchange spokesperson said that the China's foreign exchange market was "generally stable". Due to strength in the US Dollar and change in asset pricing, the overall currency reserve rose slightly.

SAFE also noted that since the start of the year, China's economy has "maintained a steady trend". But there were "divergence" in global recovery, heightened trade friction, capital out-flow and currency depreciation pressure in emerging markets. Though, China's cross-border capital flowed remained stable.

On the data front

Japan current account surplus narrowed to JPY 1.85T in May. Bank lending rose 2.2% yoy in June. Swiss unemployment rate dropped to 2.6% in June. German trade surplus widened to EUR 20.3B in May. Eurozone will release Sentix investor confidence.

BoC rate hike as the main focus of the week

BoC rate decision is a major focus for the week ahead. After recent comments from Governor Stephen Poloz and solid job data, markets are expecting the central bank to lift policy rate by 25bps to 1.50%. However, as Poloz pointed out too, there are risks to the out that couldn't be reflected in economic models. For Canada, a major risk is trade tension with the US, with threat of auto tariffs now at stake. Hence, we'd be beware of a dovish hike that signals more cautious path ahead. Suggested reading on BoC: BOC Preview – Rate Hike Fully Priced In, Data and Trade with US Continue to Guide Future Path

On the data front, UK productions will be another set of data needed to solidify the case of an August BoE hike. UK will also report monthly GDP figure for the first time. US will look into CPI and PPI. Other key data include China CPI, PPI and trade balance, German ZEW. ECB will also release monetary meeting accounts. Here are some highlights for the week::

- Monday: German trade balance; Swiss unemployment rate; Eurozone Sentix investor confidence

- Tuesday: Australia NAB business confidence; China CPI and PPI; Japan machine tools orders; UK productions, monthly GDP, trade balance, NEISR GDP estimate; German ZEW economic sentiment; Canada housing starts

- Wednesday: Japan CPPI, machine orders, tertiary industry index; Australia Westpac consumer sentiment; home loans; US PPI; BoC rate decision

- Thursday: UK RICS house price balance; German CPI final; Eurozone industrial production, ECB meeting accounts; US CPI jobless claims; Canada new housing price index

- Friday: New Zealand Business NZ manufacturing index; China trade balance; Swiss PPI; US import prices, consumer sentiments

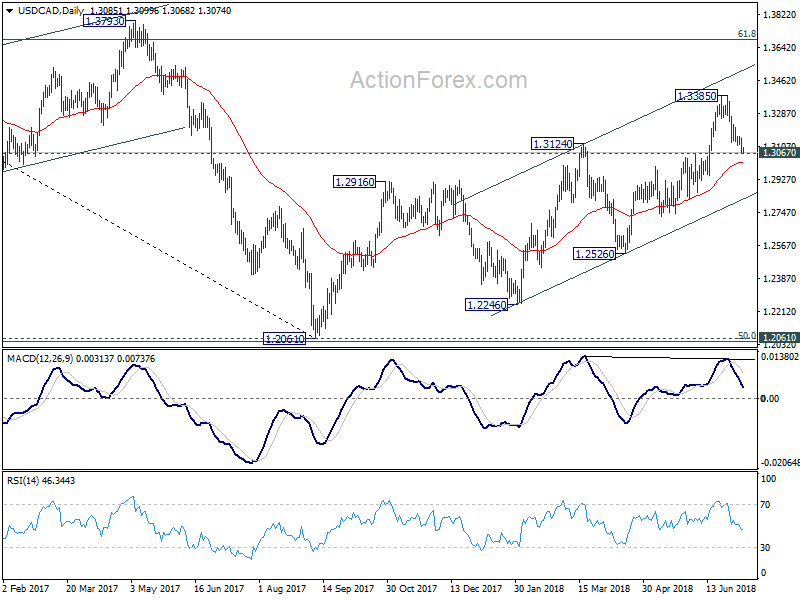

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3059; (P) 1.3109; (R1) 1.3145; More...

USD/CAD's decline from 1.3385 continues today an reaches as low as 1.3083 so far. At this point, we're still expecting strong support around 1.3067 resistance turned support to bring rebound. Above 1.3159 minor resistance will flip bias back to the upside for retesting 1.3385. However, firm break of 1.3067 will bring deeper fall to channel support (now at 1.2825).

In the bigger picture, as long as channel support (now at 1.2825) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account Total (JPY) May | 1.85T | 1.18T | 1.89T | |

| 23:50 | JPY | Bank Lending incl Trusts Y/Y Jun | 2.20% | 2.00% | 2.00% | |

| 5:00 | JPY | Eco Watchers Survey Current Jun | 48.1 | 48.2 | 47.1 | |

| 5:45 | CHF | Unemployment Rate Jun | 2.60% | 2.50% | 2.60% | 2.70% |

| 6:00 | EUR | German Trade Balance (EUR) May | 20.3B | 20.3B | 19.4B | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jul | 9 | 9.3 |

GBPUSD Further Bullish ABove 1.3300 Level

The British pound continues to trade towards the key 1.3300 resistance level against the US dollar, after another bullish weekly price-close. The British pound is also receiving a boost from UK Prime Minister Theresa May’s plans for a soft Brexit deal were revealed over the weekend. GBPUSD bulls will now need to hold price above the 1.3300 level for further upside advancement, while sellers will look for rejection around this key technical area.

The GBPUSD pair is strongly bullish while trading above the 1.3300 level, key resistance is found at the 1.3373 and 1.3400 levels.

If the GBPUSD pair fails around the 1.3300 level, sellers will likely test towards the 1.3255 and 1.3205 support levels.

EURUSD Intraday Bullish Above 1.1724 Level

The euro has broken higher against the US dollar, following softer than expected wage earnings data inside Friday’s key United States monthly jobs report. The EURUSD pair is now trading at its highest level since the day of the last European Central Bank meeting policy meeting. Bulls will look to reclaim the 1.1800 handle, while sellers to look to test towards the key 1.1724 support level.

The EURUSD pair remains intraday bullish while trading above the 1.1724 level, key resistance is found at the 1.1800 and 1.1851 levels.

If the EURUSD pair moves below the 1.1724 level, key technical support is found at the 1.1713 and 1.1685 levels.

BTCUSD Bulls Need To Hold Price Above $6,700

Bitcoin continues to trade towards the $6,650 resistance level in early Monday trading, after finding strong technical support just the $6,400 level on Friday. BTCUSD bulls now need to break above the $6,700 level to validate the bullish inverted head and shoulders price pattern across various time frames. BTCUSD sellers will attempt to break the key $6,400 level for a technical test of the $6,220 level.

The BTCUSD pair is strongly bullish while trading above the $6,700 level, further upside towards the $7,000 and $7,400 levels remains possible.

If the BTCUSD pair moves below the $6,400 level, sellers will likely test towards the $6,250 and $6,058 support levels.

German Trade Data Headlines Slow Monday Session In Financial Markets

Monday is expected to be a slow session from the perspective of economic data, with only a few European reports scheduled to make headlines. This will give investors more time to absorb Friday’s US nonfarm payrolls report, which is arguably the most closely watched data release of the month.

Action begins with a report on Swiss unemployment. Switzerland’s jobless rate is forecast to rise slightly to 2.7% in June compared with 2.6% the month before. This will be followed by a report from the German government detailing the national trade balance for May. Berlin’s surplus is projected to widen slightly to €20 billion from €19.4 billion in April.

Later in the session, Sentix will report on Eurozone investor confidence for July. The confidence index is forecast to fall to 7.9 in July compared with 9.3 in June.

In terms of monetary policy, the Bank of England’s Ben Broadbent will deliver a speech at 07:50 GMT. In North America, Federal Open Market Committee (FOMC) member Neel Kashkari will deliver a speech at 13:10 GMT.

On Friday, the US Labor Department reported that initial jobless claims rose by 213,000 last month, following an upwardly revised gain of 244,000 in May. Analysts in a median estimate had called for a gain of 195,000 for June. Average hourly earnings were less than desirable at 0.2% month-on-month and 2.7% annually.

In terms of upcoming releases, Chinese inflation data will make headlines early on Tuesday. Later in the day, the UK government will release revised Q1 GDP, manufacturing production, industrial production and the goods trade balance for the month of May.

EUR/USD

Europe’s common currency maintained its uptrend on Monday, as the EUR/USD exchange rate edged up 0.1% to 1.1753. The pair has gained more than 100 pips over the past five sessions, with the bulls eyeing immediate resistance at 1.1765. On the opposite side of the spectrum, immediate support is located at 1.1720.

GBP/USD

Cable regained momentum last week, with prices coming within a few pips of the 1.3300 level. However, gains have stalled following David Davis’ resignation as Brexit secretary. The GBP/USD exchange rate now sits at 1.3290. Immediate resistance is likely found at 1.3315, followed by 1.3350. On the flipside, immediate support levels include 1.3250 and 1.3210.

USD/JPY

After finally breaking above 111.00 last week, USD/JPY has fallen back into a familiar range. USD/JPY is currently trading around 110.40, which puts it above its long-term DMAs. Market participants are eyeing 110.25, the weekly low, as the next critical test of support. A break below that level could ignite a bigger reversal for the pair.

The US Jobs Report Published On Friday Was Mixed

Market movers today

Market action is likely to be driven by political developments rather than data releases, of which there are none of note today.

The trade war has become a permanent fixture in the universe of market drivers. Markets may also look at foreign policy developments as Trump tours Europe, the end of the North Korea-US honeymoon, the upcoming NATO and Trump-Putin summit.

Selected market news

The trade war between the US and China escalated on Friday. Washington and Beijing imposed tariffs on USD34bn worth of goods on each other. President Trump indicated that tariffs would be imposed on a further USD16bn worth of imports, followed by USD200bn and then USD300bn, encompassing China's exports to the US in their entirety. Neither side appears to be backing down. Risk assets took the escalation in their stride.

The US jobs report published on Friday was mixed, with an increase in non-farm payrolls, but soft wage growth figures. Non-farm payrolls beat expectations and came in at 213,000, while average hourly earnings decelerated and came in below expectations, at 0.2% m/m. The jobless rate increased from 3.8% to 4.0%. We still expect the US to hike rates twice, bringing the total number of hikes to four in 2018.

The UK cabinet unravels. Brexit Secretary David Davis and his Deputy Steve Baker have resigned. The resignations come two days after Prime Minister Theresa May thought she had won a crucial victory over Brexit hardliners when her plan for establishing free movement of industrial and agricultural goods was signed off. Free trade over goods would resolve the prickly problem concerning the border with Ireland.

Market action. USD is weaker on the mixed US job report but majors will stay focused on trade war developments this week: escalation should on net be USD positive but there are mounting Fed concerns that could dampen the possible impact. The recent GBP strength has been challenged by disarray in the British cabinet over May's Brexit plan, but mind the stream of UK activity data this week, key to the Bank of England. The Scandies await Thursday's Swedish inflation data, which could notably halt the recent rebound in SEK.

10Y German government bond yields continue to grind lower on the back of the US-China trade war, Brexit and the mixed US labour market report etc.

Today, the Japanese Balance of Payment statistics showed that Japanese investors sold the most German sovereign bonds in three years during May. They also sold Italian and French sovereign bonds. We expect that if German yields continue to decline and given the political uncertainty in Italy, that we will see more sell-off in Germany and Italy from Japan. They bought small amounts in Danish and Swedish sovereign bonds and Danish mortgage bonds.

This week's supply of EU bonds will come from the Netherlands (10Y), Germany (inflation linked bonds and 10Y nominals), Portugal (10Y and 15Y) and Italy. The main focus will be on Italy. We expect to see a bit more spread widening ahead of the Italian auction.