Sample Category Title

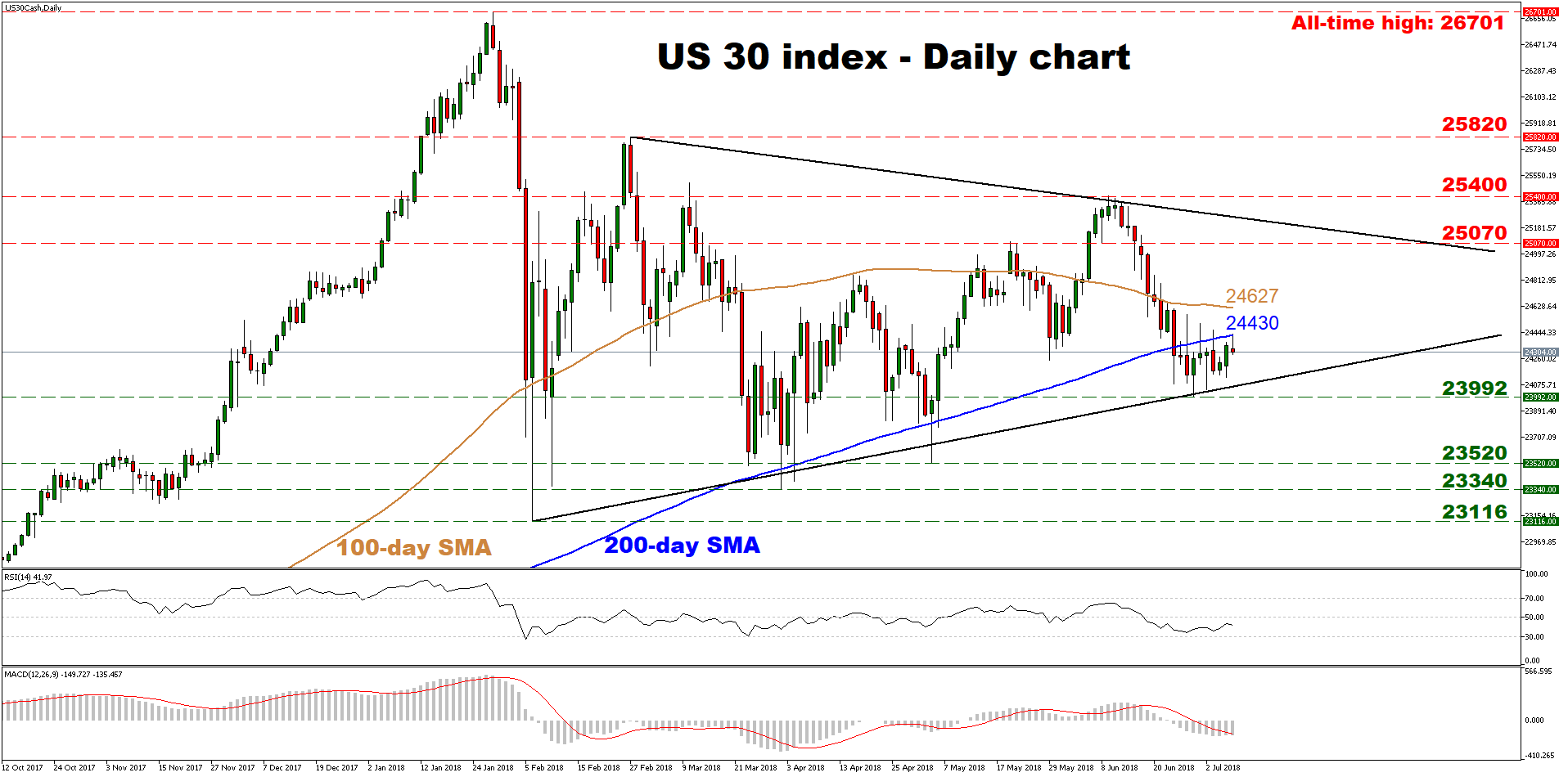

US 30 Index Trades Within A Triangle, Break On Either Side May Determine Bias

The US 30 index has been trading within a symmetric triangle formation since its plunge in early-February, posting higher lows but also lower highs on the daily chart. The outlook currently appears neutral, with a decisive break on either side of the aforementioned triangle needed to determine the medium-term bias.

Looking at short-term momentum oscillators, they suggest the next move may be to the downside. The RSI was recently rejected from near its neutral 50 level and has turned down again, while the MACD is also below its red trigger line.

Further declines could encounter immediate support near the crossroads of the lower bound of the triangle and the two-month low of 23,992. A clear break below that area would turn the bias to negative, and could set the stage for further declines, initially towards the May 3 low of 23,520. Even lower, support may be found around the April 2 trough of 23,340, before the attention shifts to the February 6 bottom of 23,116.

On the flipside, advances could stall initially near the 200- and 100-day moving averages, at 24,430 and 24,627 respectively. Even higher, the intersection of 25,070 and the upper bound of the aforementioned triangle may come into view, with a decisive upside break of that zone turning the outlook to positive and opening the way for the June 11 peaks of 25,400. After that, the February 27 high of 25,820 would be eyed, before the focus turns to the all-time high of 26,701.

Overall, the outlook currently appears neutral, with a significant break on either side of the triangle pattern likely to determine the broader directional wave.

Dollar Moves With Caution Ahead Of NFP Employment Report

Here are the latest developments in global markets:

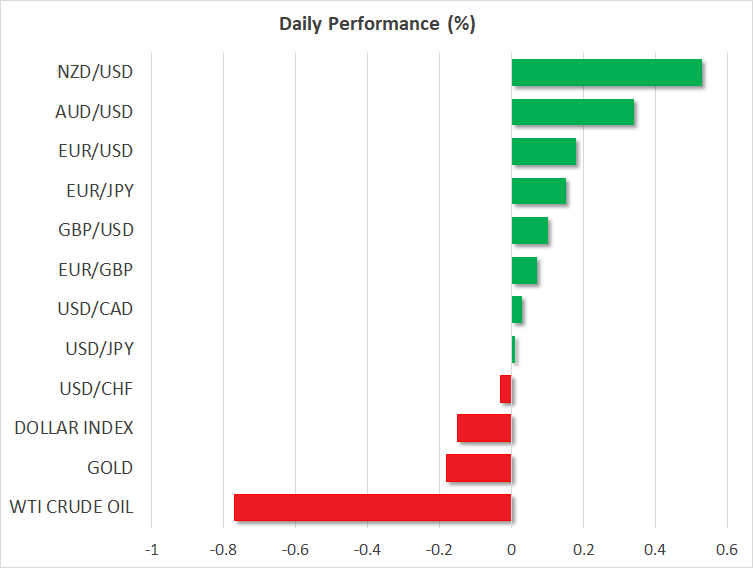

FOREX: The US started collecting a 25% import tariff on Chinese products worth $34 billion on Friday midnight. According to media, China has immediately activated its countermeasures today as well, with dollar/yen remaining unaffected at 110.63 (+0.01%) as investors have already priced in the news, turning focus to the all-important NFP employment report due later on Friday instead. The dollar index, though, which gauges the greenback’s strength against six major currencies was struggling to gain ground, easing to 94.33 (-0.15%) as a strengthening euro continued to weigh on the index. Euro/dollar managed to break slightly above the 1.17 key level (+0.14%) after data out of Germany showed that industrial production had surprisingly recovered by 2.6% m/m in May after tumbling by 1.3% previously, posting its largest increase since the start of the year. Analysts had predicted a smaller growth of 0.3%. Pound/dollar paused at 1.3222, with investors waiting for the UK prime minister to give details on her Brexit plan to her cabinet today at the Chequers meeting. Yesterday, the German Chancellor who held a news conference with the British Prime Minister said that the Brexit plan was “unworkable” according to a Bloomberg report, sending the pair down to 1.3200. Euro/pound changed hands slightly higher at 0.8848 (+0.10%). In antipodean currencies, aussie/dollar stretched up to 0.7412 (+0.34%), while kiwi/dollar was the best performer, hitting a one-week high of 0.6826 (+0.50%). Dollar/loonie remained flat at 1.3138.

STOCKS: European equities opened higher on Friday but soon turned lower, pressured by concerns that the US-Sino trade dispute could turn into a bigger global trade war. The pan-European STOXX 600 slipped by 0.10% at 1130 GMT, with energy sectors losing the most, while the blue-chip Eurostoxx 50 was down by 0.21%. The German DAX 30 was flat, the French CAC 40 retreated by 0.09%, while the Italian FTSE MIB fell by 0.25%. The British FTSE 100 declined by 0.33%, whilst in the US, futures tracking major stock indices were mixed.

COMMODITIES: Oil prices were trading weaker on news that Saudi Arabia had increased its supply by 500,000 barrels per day in June to mitigate supply shortages elsewhere. Still, losses were capped by fears that retaliatory measures from China could include trade barriers on oil products. Meanwhile in Vienna, where representatives from the EU, Russia, China, and Iran gathered to discuss the Iranian nuclear deal and how to proceed with the agreement without the US, an Iranian official stated that pact members should fully compensate Tehran for US sanctions to persuade it to stay in the deal. WTI crude and Brent were last seen lower at $72.37/barrel (-0.78%) and at $76.70/barrel (-0.89%) respectively. In precious metals, gold was down on the day at $1,254.65/ounce (-0.19%).

Day Ahead: US payrolls & wage data and Canadian jobs figures on the agenda

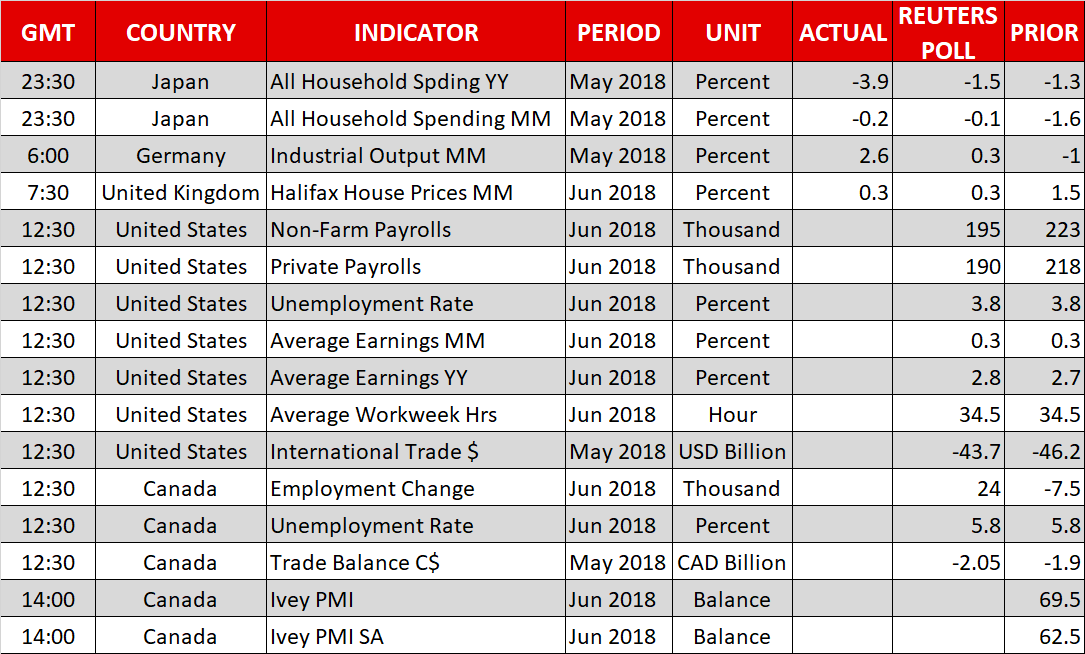

The main event today will be the US employment report for June at 1230 GMT. Nonfarm payrolls are anticipated to have risen by 195K from 223K in the preceding month. The unemployment rate is projected to remain unchanged at a the18-year low of 3.8%, while average hourly earnings are expected to increase by 2.8% in yearly terms, from 2.7% previously.

In case these data come out stronger than anticipated – particularly on the wage front – markets are likely to begin pricing in a higher probability that the Fed may deliver four quarter-point rate hikes this year, from three that are already priced in. On the other hand, a disappointment would possibly generate some skepticism as to how many hikes the Fed will deliver this year, thereby weighing on the greenback.

Canada will also release its own employment data for June at 1230 GMT. The unemployment rate is forecast to have held steady at 5.8%, while the net change in employment is anticipated to have rebounded by 24.0k, following a sharp decline of 7.5K in May. A positive surprise in data would likely bring encouraging news to the loonie in which case a possible bullish retracement is expected.

Remaining in Canada, Ivey PMI readings will also come into view today at 1400 GMT, though it is worth noting that the loonie has recently shown little reaction to these numbers. The forecast is for the index to tick higher to 63.2 in June from 62.5 the prior month.

Later in the day, Baker Hughes will report on the US oil rig counts for the week ending June 29.

Also, today the British Prime Minister, Theresa May, will meet with her senior ministers to have a discussion for reaching a common ground on the UK’s future trading relationship with the EU after Brexit. Until now, PM May’s advisors suggested two proposals, but none of them gained the full support of her party.

Forex Analysis: Gold And USDJPY

The major economic data release for today will be the U.S. Non-Farm Payrolls (NFP) and Average Hourly Earnings. The US economy is expected to add another 195K jobs in June with hourly earnings growing to an annualized 2.8% from 2.7% in May. The stronger growth should keep the Federal Open Market Committee (FOMC) on course to implement four rate hikes in 2018 as planned. Provided there is no drastic deviation from expectation, the reaction to NFP should be temporary.

The focus could quickly shift to risk sentiment due to the ongoing trade war. China’s Premier Li has been reacting to the imposition of tariffs this morning with the message that a trade was is never a solution and China will never start a trade war. Li also said that if any party resorts to increase of tariffs, China would take measures in response in order to protect China’s interest. According to a reports China is said to have applied tariffs to the same value of US goods at the same rate effective from 12:01 PM Friday.

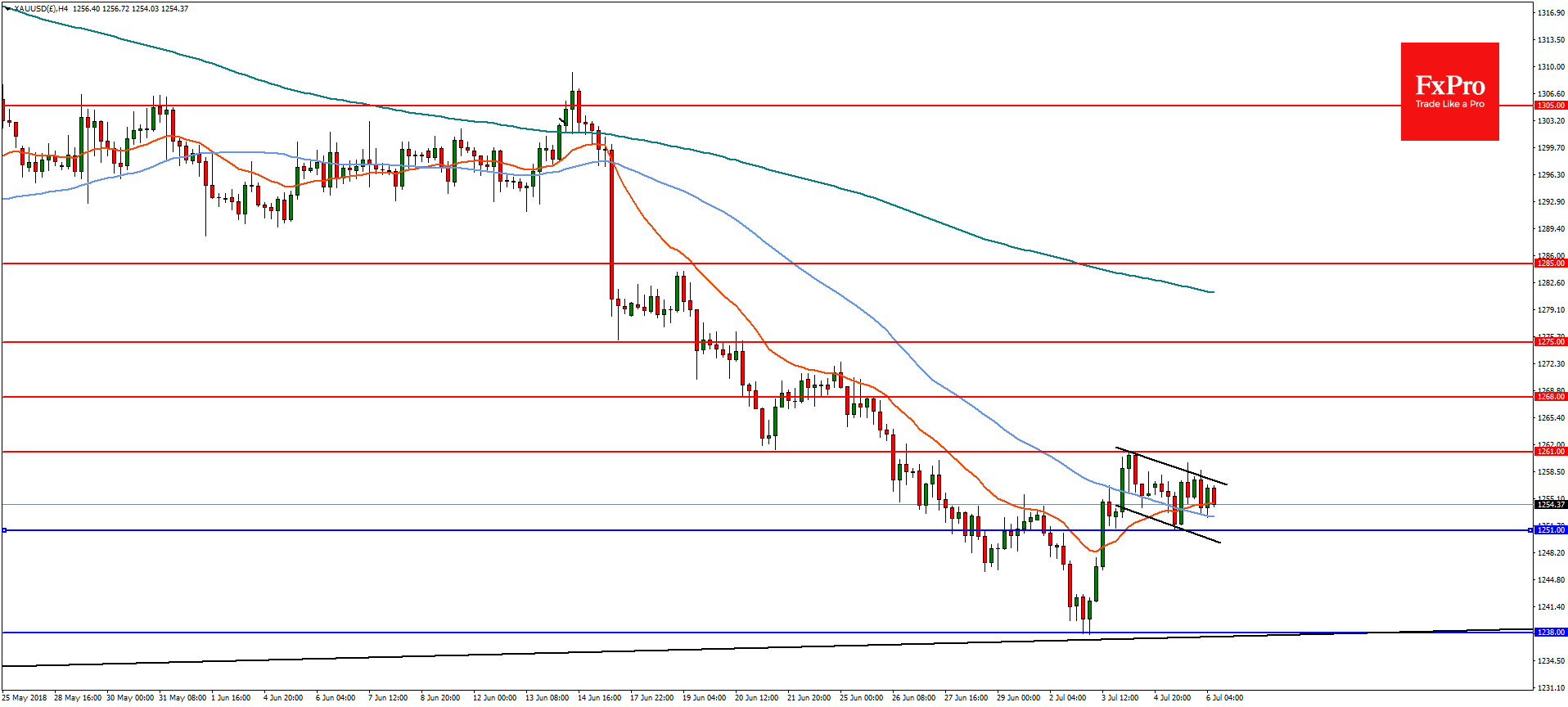

GOLD

In the 4-hourly timeframe, Gold recovered from a major horizontal and trend line support at 1238 but has not been able to build on the rebound and is now forming a possible bull flag. The break to the upside would give a measured target at 1275 with resistance at 1261 and the 23.6% retracement of the April highs at 1268. However, a reversal and break of 1251 will likely see another test of the lows at 1238.

USDJPY

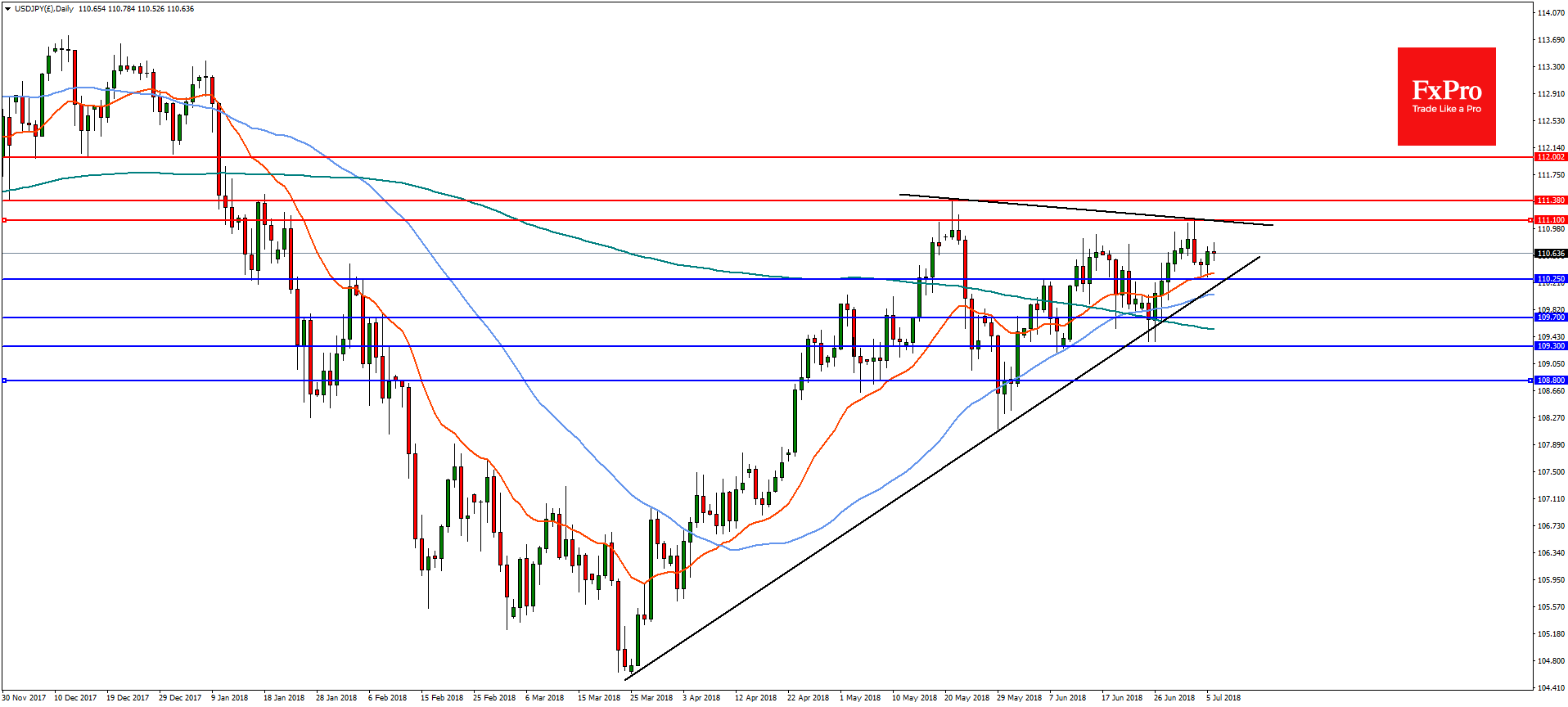

An escalation of trade war could cause a reaction in the USDJPY with a sell off possible. On the daily chart, a break of the March trend line and horizontal support near 110.25 could open the way for declines to near term support at the 23.6% retracement of the March lows at 109.70 followed by 109.30 and 108.80. On the flip-side a break of 111.10 would find resistance at 111.30 and then 112.00.

USDJPY Still Trapped In Narrow Range

The US dollar continues to trade within a narrow-range against the Japanese yen currency, as traders await the latest monthly jobs report from the United States economy. The USDJPY pair is currently stabilizing above the 110.50 level, despite fears about US trade tensions with China. Sellers will try to break below the 110.25 support level, while buyers will try to clear the 110.80 resistance level.

The USDJPY pair is bearish while trading below the 110.25 level, key support is found at the 109.54 and 109.00 levels.

If the USDJPY pair moves above the 110.80 level, buyers will likely test towards the 111.00 and 111.40 resistance levels

EURUSD Still Bullish Above 1.1674 Level

The euro continues to make fresh gains against the US dollar, with the EURUSD pair earlier setting a new monthly trading-high, just above the 1.1720 level. Traders now await the release of the important Nonfarm Payrolls job report from the United States economy. Buyers need a sustained break above the 1.1719 level, while sellers need a confirmed technical break below the 1.1674 support level.

The EURUSD pair is bullish while trading above the 1.1719 level, key resistance remains at the 1.1750 and 1.1780 levels.

If the EURUSD pair moves below the 1.1674 level, key support is found at the 1.1648 and 1.1600 levels.

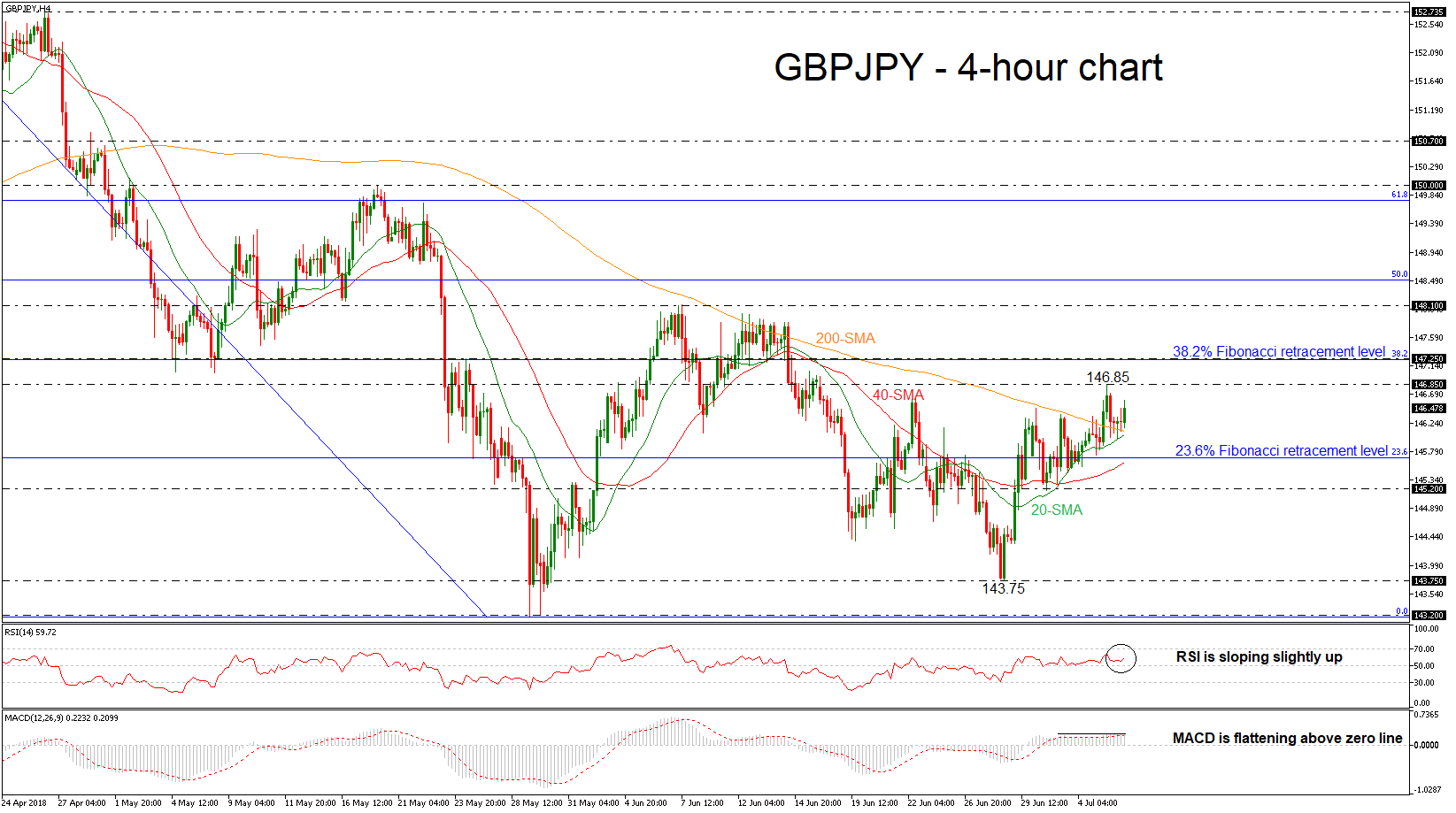

GBPJPY Maintains Weak Bias In Near Term, Medium-Term Outlook Looks Mostly Bearish

GBPJPY is still developing above the moving averages in the 4-hour chart but with weak movement over the last couple of sessions. Also, the price touched a new two-week high of 146.85 on Thursday but reversed some of its gains.

Looking at the short-term timeframe, the Relative Strength Index (RSI) hovers above the threshold of 50 and is sloping slightly to the upside. However, the MACD oscillator is flattening above the zero line and seems too weak for any strong upside movement in price action.

Upside moves are likely to find resistance at 146.85. Rising above this area would help shift the focus to the upside towards the 38.2% Fibonacci retracement level of the downleg from 153.80 to 143.20, which overlaps with the 147.25 resistance level.

On the flip side, in case of a drop below the 200- and then the 20-simple moving average (SMA), it would increase downside pressures towards the 23.6% Fibonacci of 145.70. Breaking this level could see a re-test of the 145.20 support, taken from the low on July 2.

In the longer timeframe, GBPJPY is set to complete the fourth bullish day in a row but remains in a downtrend, below 146.85.

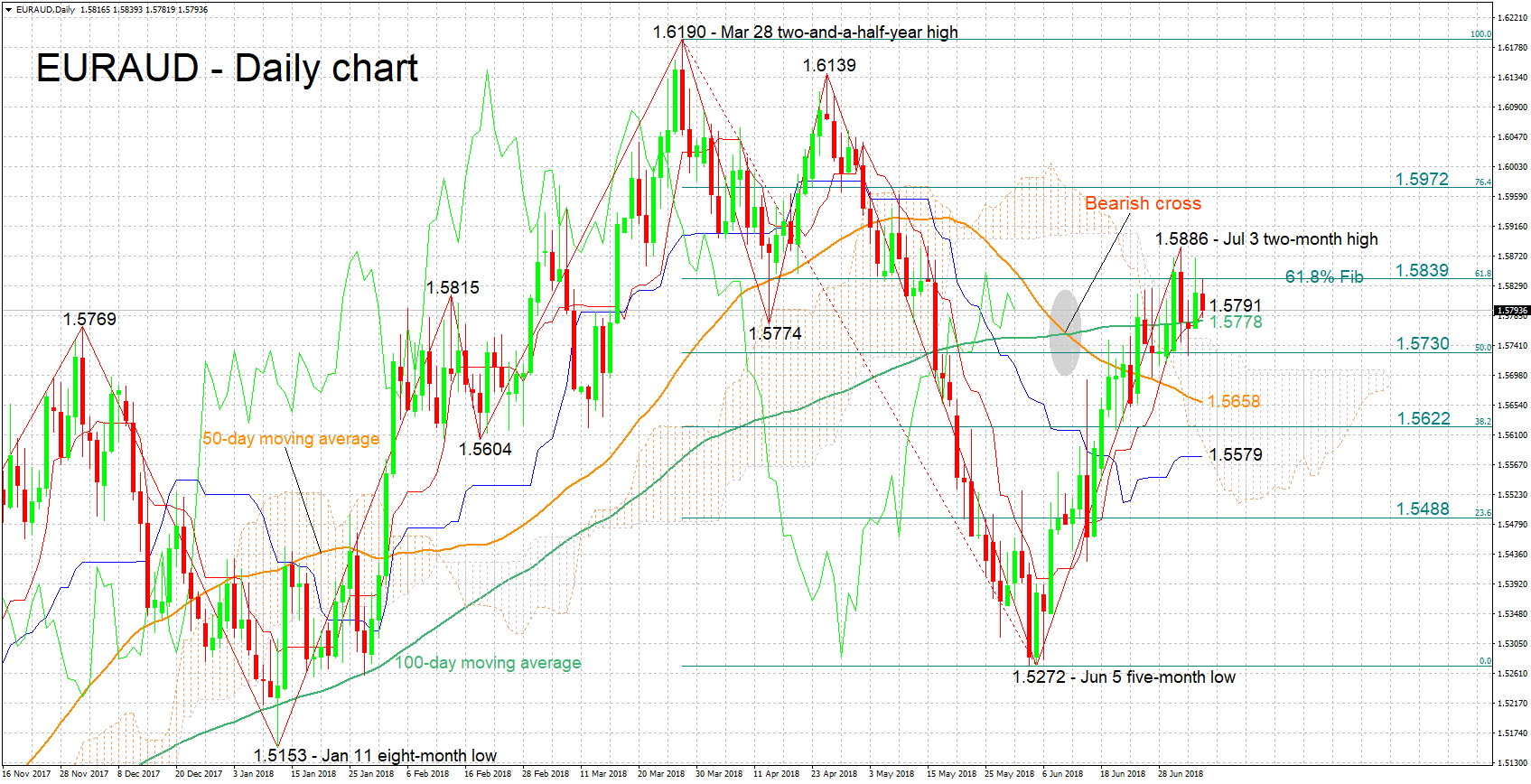

EURAUD Bullish Bias Eases, Trades Above Moving Averages

EURAUD has posted considerable gains after hitting a five-month low of 1.5272 on June 5. On Tuesday, the pair touched a two-month high of 1.5886.

The Tenkan-sen is above the Kijun-sen, pointing to a positive short-term bias. However, the fact that the Kijun-sen has flatlined is an indication of easing positive momentum in the near-term.

Further upside movement could meet resistance around the 61.8% Fibonacci retracement level of the March 28 to June 5 downleg at 1.5839. Stronger gains would turn the attention to the area around the two-month high of 1.5886 from earlier in the week which also encapsulates the 1.59 round figure.

On the downside, support may come around the current level of the 100-day moving average at 1.5778. The zone around this point includes the Tenkan-sen (1.5791), as well as the Ichimoku cloud top (1.5752). Further below, the 50% Fibonacci mark at 1.5730 would be eyed next.

Regarding the medium-term picture, the price action has defied the negative signal given by the bearish cross recorded in early to mid-June when the 50-day MA moved below the 100-day one. Specifically, since Thursday (yesterday), trading activity has been taking place above both the 50- and 100-day MA lines, as well as above the Ichimoku cloud, supporting the existence of a bullish tilt in the medium-term. Things are still “fragile” though, with a fall below the 100-day MA and back into the cloud setting the scene for a neutral outlook.

Overall, the short-term bias remains bullish though it seems to have lost part of its steam, while the medium-term outlook is positive, albeit only marginally so.

Forex Analysis: EURUSD

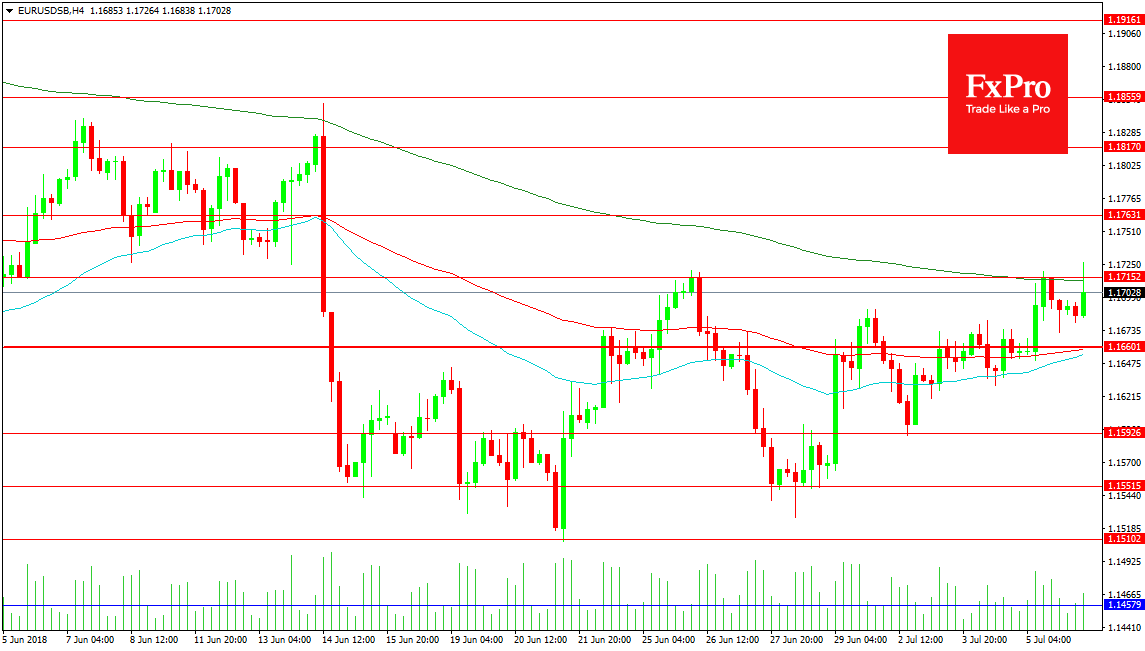

The EURUSD pair is moving back higher after reaching a 3 week high at 1.17264 today and testing its 200 period MA in a 4 hour timeframe. The price has been consolidating between 1.17200 and 1.15100 since it dropped after the ECB meeting last month. A break higher would seek to retrace that move and reach the 1.18500 area but there is resistance to overcome at 1.17630 and 1.18000 followed by 1.18170. An overshoot would look to retest 1.19000 followed by 1.19160. The release of the Nonfarm Payrolls data today could provide the catalyst for such a move.

A break under 1.16600 would under normal trading conditions require a lot of energy given the fact that the 100 and 50 period Moving Averages are in close proximity at 1.16585 and 1.16543 respectively. But NFP day is not a normal market trading day and it pays to broaden the view when looking for support and resistance. There for a break under this level can be part of the initial reaction to the data and the market may need time to decide on a firm move and new trend. A break under 1.15926 and the 1.16000 would be of more significance. The lows over the last three weeks have been bought between 1.15515 and 1.15100 so expect buyers to engage in that zone. A loss of that area can result in a move lower to 1.14579.

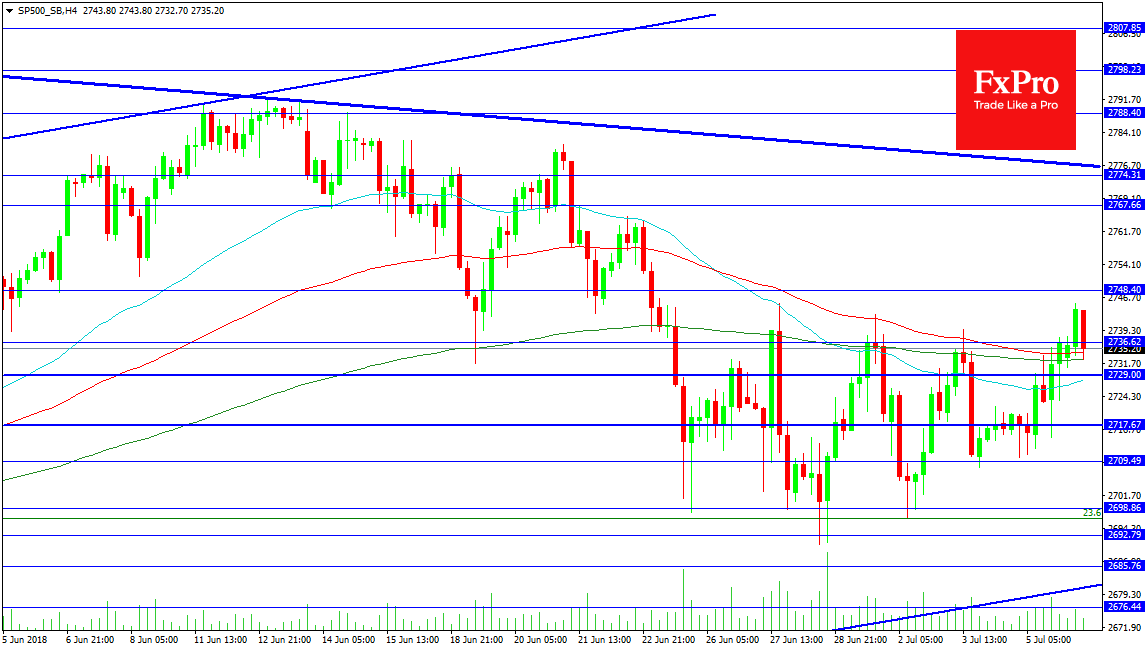

Forex Analysis: S&P 500

The US 500 Index has moved higher overnight but has now retraced some of this move on the run into Nonfarm Payrolls data. The US/China Trade Tariffs went into place overnight with minimal market reaction. The market is awaiting confirmed reports on the tariff process with one eye on economic data. The price has consolidated in a range between 2745.00 and 2690.00 and NFP data can see this range breeched and widened. Resistance can be seen at 2767.60 followed by 2274.30 and the falling trend line just above at 2776.70. A break higher would need to clear 2792.00 and then test 2800.00/2802.50.

Support can be seen at the 100 and 200 period MA on the 4 hour chart, with the latter supporting the current candle at 2732.66. However these points are very close to the current price and can be ignored once NFP is released. Also quite close is the 2729.00 level and the 50 MA at 2727.80. Below is the 2717.67 level and 2709.49 below which buyers have entered the market. The 2700.00 round number has been less useful that the 2698.80 level in recent times and this can be a point of interest today. A s mentioned earlier a loss of 2690.00 could see a deeper bearish reaction develop leading to a test of trend line support at 2681.00.

Global Indices Rise As US-China Tariffs Enter Into Effect

Notes/Observations

- All eyes on today's Wage and Non-Farm Payroll data; wages expected to post a solid 0.3% monthly increase while payrolls are eyed between 180-200K

- PM May aims to resolve splits within cabinet over shape of Brexit at her Chequers meeting; the showdown threatens to throw talks with the EU into disarray

Asia:

- First round of US tariffs on $34B worth of goods on China officially take effect

- China reciprocal tariffs take effect on US products; China Commerce Ministry (MOFCOM): Reiterates has to fight back, forced to retaliate on tariffs; will continue evaluating impact of US tariffs

- China Central Bank Advisor forecasts small 0.2% impact to Chinese domestic GDP as a result of $50B US tariffs

- Samsung Electronics declines as Q2 prelim results missed ests

Europe:

- German Press reports suggest JP Morgan and ICBC could look at taking stakes in Deutsche Bank; according to the same report German Chancellor Merkel asked UBS Chairman for his assessment on Deutsche Bank situation

- Italy Stats Agency (ISTAT) Monthly Economic Outlook: Sees economy slowing down in coming months

Energy:

- (US) National Hurricane Center (NHC): Beryl becomes first hurricane of Atlantic season

Economic Data:

- (JP) Japan May Preliminary Leading Index CI: 106.9 V 106.6E; Coincident Index: 116.1 V 116.1E

- (DE) GERMANY MAY INDUSTRIAL PRODUCTION M/M: 2.6% V 0.3%E; Y/Y: 3.1% V 1.5%E

- (NO) Norway May Industrial Production M/M: -0.9% v -1.4% prior; Y/Y: -1.6% v -1.9% prior

- (RO) Romania Q1 Final GDP (3rd reading) Q/Q: 0.1% v 0.0% prelim; Y/Y: 4.0% v 4.0%e

- (DK) Denmark May Industrial Production M/M: -1.5% v +1.2% prior

- (ZA) South Africa Jun Gross Reserves: $50.6B v $51.2B prior; Net Reserves: $42.5B v $42.9B prior

- (AU) Australia Jun Foreign Reserves (AUD): 75.8B v 82.5B prior

- (FR) FRANCE MAY TRADE BALANCE: -€6.0B V -€5.1BE

- (FR) France May Current Account: -€2.9B V -€1.3B prior

- (HU) Hungary May Industrial Production SA M/M: 1.9% v 1.7%e; Y/Y: 3.8% v 2.1%e

- (CH) Swiss Jun Foreign Currency Reserves (CHF): 748.5B v 740.9B prior

- (MY) Malaysia End-Jun Foreign Reserves: $104.7B v $107.9B prior

- (AT) Austria Jun Wholesale Price Index M/M: 0.2% v 1.4% prior; Y/Y: 6.3% v 5.2% prior

- (PL) Poland Jun Unemployment Rate: 5.9% v 6.1% prior - Polish press

- (UK) JUN HALIFAX HOUSE PRICES M/M: 0.3% V 0.2%E; 3M/Y: 1.8% V 1.6%E

- (SE) Sweden Jun Budget Balance (SEK): -17.3B v +50.6B prior

- (IT) Italy May Retail Sales M/M: +0.8% v +0.5%e; Y/Y: 0.4% v -4.6% prior

- (RU) Russia Narrow Money Supply w/e Jun 29th: 10.10T v 10.16T prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.3% at 3451, FTSE +0.1% at 7,612, DAX +0.2% at 12,490, CAC-40 +0.3% at 5.384; IBEX-35 +0.4% at 9.903, FTSE MIB +0.3% at 21.978, SMI +0.1% at 8.682, S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European stocks open higher across the board and maintained positive as the session progressed; tariffs take effect between US and China, but risk sentiment remains positive; consumer goods and media sectors best performers; materials stocks slightly underperforming; Czechia closed for holiday; Ross Royce sells Commercial Marine unit to Kongsberg; focus on upcoming NFP in US session

Equities

- Consumer discretionary: BCA Marketplace BCA.UK -1.6% (Apax won't issue bid), L'Oreal OR.FR +0.1% (analyst action), Hella HLA.DE +1.3%(asset sale), Wilmington Group WIL.UK -22.1% (trading update)

- Financials: Eurazeo RF.FR +5.9% (analyst action)

- Industrials: Aena Aeropuertos AENA.ES +1.2% (analyst action), Assa Abloy ASSAB.SE -6.9% (Prelim results), Kongsberg Gruppen KOG.NO -4.7% (acquisition), Rolls Royce RR.UK -0.2% (asset sale), ThyssenKrupp TKA.DE -1.0% (CEO resignation)

- Materials: ArcelorMittal MT.NL +1.4% (analyst action)

- Technology: Parrot PARRO.FR +3.3% (asset sale)

- Telecom: Inmarsat ISAT.UK -8.2% (rejects offer from Ecostar)

Speakers

- (CN) China Foreign Ministry spokesperson Lu Kang: Retaliatory tariffs on US goods are now in effect - press conf

Currencies

- Dollar slightly softer against its major trading partners as US/China tariffs kick in; U.S. wage and jobs data eyed

Fixed Income

- Bund Futures trade 7 ticks higher at 162.67 following the move in Treasuries. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.31 higher by 2 ticks as PM May faces a decisive battle over the weekend. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Friday's liquidity report showed Thursday's excess liquidity rose from €1.852T to €1.873T. Use of the marginal lending facility fell from €50M to €0M.

- Corporate issuance saw no deals priced in the primary market

Looking Ahead

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (BR) Brazil Jun IBGE Inflation IPCA M/M: 1.3%e v 0.4% prior; Y/Y: 4.4%e v 2.9% prior

- 08:00 (CL) Chile Jun CPI M/M: 0.2%e v 0.3% prior; Y/Y: 2.6%e v 2.0% prior, CPI Ex Food and Energy M/M: 0.0%e v 0.3% prior; Y/Y: No est v 1.6% prior

- 08:00 (PL) Poland Jun Official Reserves: No est v $111.8B prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Jun Change in Nonfarm Payrolls: 195Ke v 223K prior

- 08:30 (US) Jun Unemployment Rate: 3.8%e v 3.8% prior

- 08:30 (US) Jun Average Hourly Earnings M/M: 0.3%e v 0.3% prior; Y/Y: 2.8%e v 2.7% prior; Average Weekly Hours: No est v 34.5 prior

- 08:30 (US) May Trade Balance: -$43.7Be v -$46.2B prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:30 (US) Jun Unemployment Rate: No est v 3.8% prior

- 08:30 (CA) Canada Jun Net Change in Employment: +20.0Ke v -7.5K prior; Unemployment Rate: 5.8%e v 5.8% prior

- 08:30 (CA) Canada May Int'l Merchandise Trade (CAD): -2.2Be v -1.9B prior

- 10:00 (CA) Canada Jun Ivey Purchasing Managers Index (Seasonally Adj): No est v 62.5 prior

- 10:30 (TR) Turkey Jun Cash Budget Balance (TRY) : No est v B prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 13:00 (US) Weekly Baker Hughes Rig Count data