Sample Category Title

Canada’s Goods Trade Deficit Widens to $2.8 Billion May

Canada's goods trade deficit widened to a larger-than-expected $2.8bn in May from a slightly revised $1.90bn in April (previously $1.86bn). Exports were flat during the month, weighed on by shipments of motor vehicles and parts as well as metal ores and non-metallic mineral products. Imports rose 1.7%, lifted by aircraft and other transportation equipment and energy products.

In real or volume terms, exports dropped by 1.0% on the back of lower exports of metal ores and non-metallic minerals. Meanwhile, import volumes rose 1.2% on the month.

May's report marked just the second time in eight months that exports didn't increase. Shipments of motor vehicles and parts fell 3.6% during the month. A supply disruption of auto parts from the U.S. contributed to a decline in exports of passenger cars and light trucks. Exports of metal ores and non-metallic mineral products also fell significantly (-14.6%), though this decline coincided with work stoppages in iron mines in April and May. On the flipside, exports of aircraft and other transportation equipment and parts advanced a robust 7.8% during the month on the back of exports of transportation equipment to Saudi Arabia. Exports of forestry products and building and packaging materials also saw a notable gain (+3.1%).

Imports advanced 1.7% in May, partially reversing April's 2.8% drop. Imports of aircraft and other transportation equipment and parts rose 17.7%, the fifth consecutive gain for this category. Statistics Canada noted that the gain was driven by the import of several airliners from the United States. Imports of energy products also contributed to May's gain as a number of Canadian refineries were temporarily shut down during the month, causing higher imports to meet domestic demand for refined petroleum products.

Canada's merchandise trade surplus with the U.S. narrowed to $3.3 in May from $3.7 in April as imports advanced 1.0% and exports dipped 0.2%.

Key Implications

On balance, this report provided a "so-so" last look at Canada's trade picture before the implementation of the steel and aluminum tariffs by the U.S. on June 1st. Export volumes dropped during May, though part of this decline can be put to temporary factors in the automotive and metal ore sectors that could reverse in coming months. Meanwhile, a relatively broad-based gain in imports across categories points to rising domestic demand.

Despite the softer showing for export volumes and a partial rebound in real imports in May, net trade is still on track to add to growth in the second quarter – consistent with our forecast.

The trade picture has become more complicated in recent months, with the imposition of steel and aluminum tariffs by the U.S. government and retaliatory Canadian tariffs likely to weigh on trade of these products and restrain output. Meanwhile, the prolonged NAFTA negotiations continue to add a layer of uncertainty to the trade backdrop. Fortunately, solid U.S. demand combined with a loonie which has lost some steam in recent months should provide some offset to these factors.

U.S. Trade Deficit the Lowest in 19 Months as Soybean Exports Surge in Advance of Tariffs

The U.S. trade deficit improved to $43.1 billion in May from $46.1 billion in April, the smallest deficit since October 2016.

Nominal exports rose 1.9%, led by food and beverage exports (soybeans), which were up a robust 14.1%. Imports rose a smaller 0.4%, following two months of declines. Capital goods saw the strongest import growth, up 3.6%, offset by falling automotive (-1%) and consumer goods (-0.9%) imports.

Adjusted for inflation, real goods exports rose 1.7%, while real goods imports were up 0.2%.

Key Implications

Tariffs and the threat of tariffs are already distorting international trade figures as businesses try to get ahead of the trade action. For the moment, international trade is helping the U.S. economy at the same time that domestic demand is running full bore. With a strong gain in exports and weak import growth, net exports look to add at least a percentage point to second quarter real GDP growth, enough to push it past the 4% mark.

Import weakness is unlikely to last, given the strength in domestic spending and a strong U.S. dollar, and some of the recent export strength is likely to reverse as trade barriers come into effect. Indeed, tariffs on steel and aluminum and now $34 billion in Chinese goods, and reciprocal retaliatory measures against U.S. goods will cloud the trade picture over the foreseeable future.

Sunset Market Commentary

Markets

Today, two factors dominated global markets’ trading. Firstly, this morning, the US started imposing tariffs on $34 bln of Chinese imports. In response, China also imposes tariffs on a similar amount of US products. Both actions were more or less expected and no surprise for markets. There was little negative impact on global equities. Investors were mainly looking out for signs whether or the not the process would escalate further. In the meantime, core bonds hovered in tight ranges, holding near recent levels. In the afternoon, the focus turned to the US payrolls report. The report was quite similar to what was often reported over the previous months/quarters. Payrolls’ growth was strong (213k and a 37k upward revision of the previous two months) but wage growth again disappointed at 0.2% M/M (0.3% expected). The latter was most relevant for markets. Slow wage growth indicates that further Fed tightening might continue at a gradual pace. Core US/European yields declined slightly after the publication of the payrolls. The 2 & 5-y yield decline 2 bp. The 30-y eases 1.5 bp. Changes on the German yields curve also moved less than 2bp. This time, the very long end underperformed (30-y +0.5 bp). Intra-EMU spreads versus Germany (10-y) narrow marginally with Italy (-4bp) and Portugal (-2 bp) doing best. So, the payrolls were not able to give bond market a new, directional impetus.

Yesterday, EUR/USD made some cautious progress (ECB interest rate debate and risk sentiment becoming less sensitive for the trade war theme). This trend continued today. This morning, markets didn’t know what to conclude from the US and China imposing tariffs on mutual imports. However, this new stage in the trade war didn’t cause any outright risk-off reaction. This constructive reaction also helped EUR/USD to hold north of 1.17. In the afternoon, the US payrolls triggered some modest further USD losses as wage growth disappointed again. The dollar probably won’t get much additional interest rate support anytime soon. EUR/USD cleared the 1.1720 resistance and trades currently in the mid 1.17 area. However, the next resistance at 1.1850 still looks quite far away. USD/JPY also lost a few ticks after the payrolls but still trades in well-known territory in the mid 110 area. Whatever, the payrolls again didn’t change the broader picture for USD trading in any profound way.

Sterling traders basically stayed side-lined. There were no really important UK data. Markets eagerly await the outcome of a key UK Cabinet meeting. At this meeting, the UK PM is trying to reach a consensus on what relationship the UK will try to pursue with the EU after Brexit. However, as the UK government/conservative party are highly dived on the issue, the outcome involves quite a binary risk for sterling trading. EUR/GBP didn’t go anywhere for most of the day. EUR/GBP gained a few ticks in line with EUR/USD after the US payrolls. The pair trades in the 0.8860 area. Cable also profited slightly from the USD decline after the payrolls (1.3270 area).

News Headlines

German industrial production rebounded at a faster than expected pace in May. Production grew 2.6% M/M and 3.1% Y/Y. The consensus only expected production to rise 0.3% M/M and 1.5% Y/Y. The April figure was downwardly revised (-1.3% M/M vs -1.0%). Even so, the data suggest German growth remained at a decent level in Q2 even as the growth momentum turned less strong than was the case last year and as special factors were at work in Q1.

US nonfarm payrolls confirmed the great shape of the US labor market. The economy added 213k jobs in June, more than the 195k expected, but less than the 244k in May. The unemployment rate ticked up from the record low 3.8% to 4% in June but is counterbalanced by an increase of the participation rate (62.9% vs 62.7% expected). Average Hourly Earnings rose 0.2% M/M and 2.7% Y/Y in June, lower than lower than the 0.3% M/M and 2.8% Y/Y expected. This slow wage growth suggests ongoing moderate inflationary pressure.

U.S. Job Market Still Strong, Despite Uptick in the Unemployment Rate

Once again, U.S. non-farm payrolls beat expectations, rising 213k in June. That followed through on a solid 244k tally in May. In fact, job gains over the past two months were revised upwards 37k.

The unemployment rate rose two ticks to 4%, but that is less concerning given that it was in part due to an increase in the labor force participation rate, from 62.7% in May to 62.9% in June.

The headline participation rate has been relatively flat over the past two years. More importantly, however, the participation rate for core age workers (25-54 yrs) rose two ticks to 82% in June, continuing the improving trend seen over the past three years. It still remains about one percentage point below its pre-recession peak, suggesting there is still some labor market slack.

Goods sector hiring held up well in June, rising 53k positions, boosted by 36k new jobs in manufacturing. Mining (4k) and construction (+13k) also gained new jobs.

Services sector hiring decelerated somewhat, but still rose a solid 149k new jobs. Strength was seen in business services (+55k) and health care (+25k), while the retail sector shed 22k jobs, reversing the May gain.

One somewhat sour note was modest growth in wages, up 0.2% in June, against expectations for a 0.3% increase. On a year-on-year basis, growth in average hourly earnings ticked down to 2.7%.

Key Implications

We are running out of pithy headlines to describe the strength of the US job market. June marks two straight months of better than expected job growth, and upward revisions to historical job gains. At 4%, the unemployment rate is still very low, and the increase in labor force participation is a good sign that a healthy job market is drawing more workers back to the workforce.

The fact that wage growth isn't stronger remains a bit of a puzzle. But we take consolation that other measures of wage gains that aren't affected by demographics or industry mix show healthier gains for workers. Still the job market is strong enough to warrant continued gradual rate hikes by the Federal Reserve.

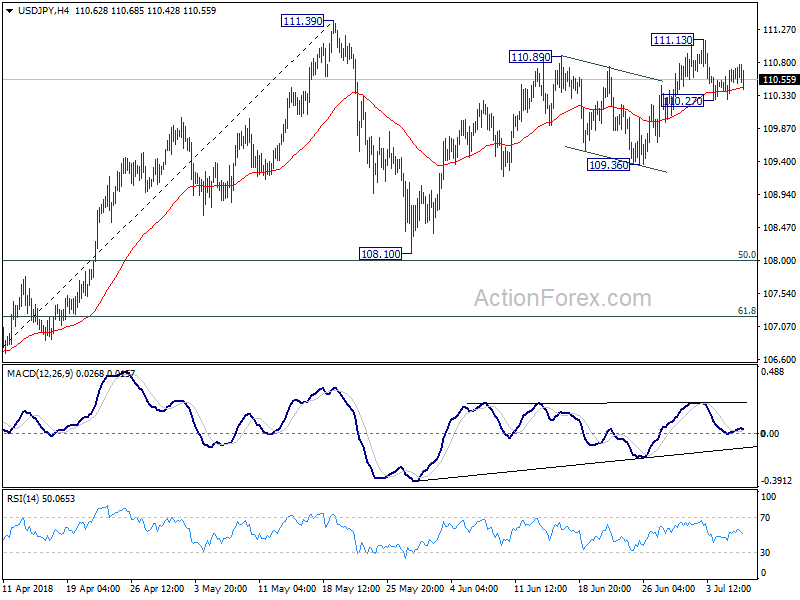

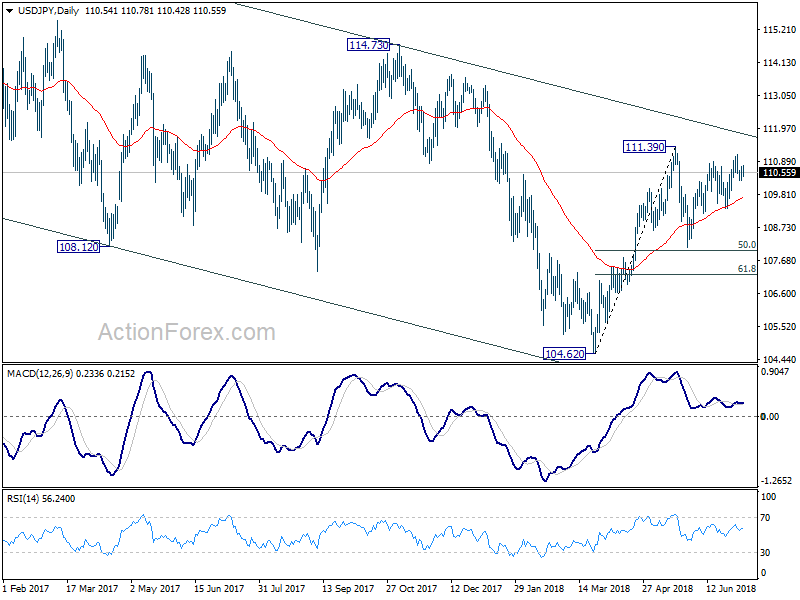

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.39; (P) 110.56; (R1) 110.82; More...

Intraday bias in USD/JPY remains neutral as it's bounded in range of 110.27/111.13. On the downside, below 110.27 will bring deeper fall to 109.367 support. Break there will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

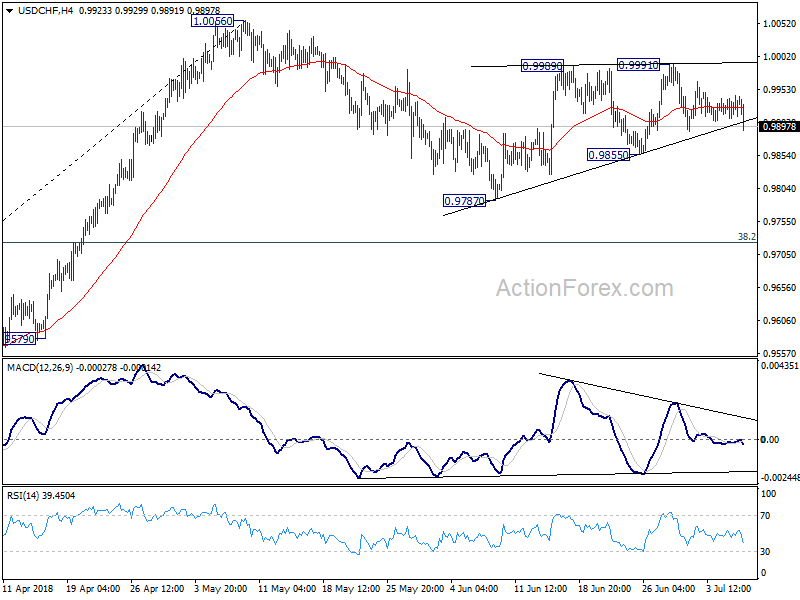

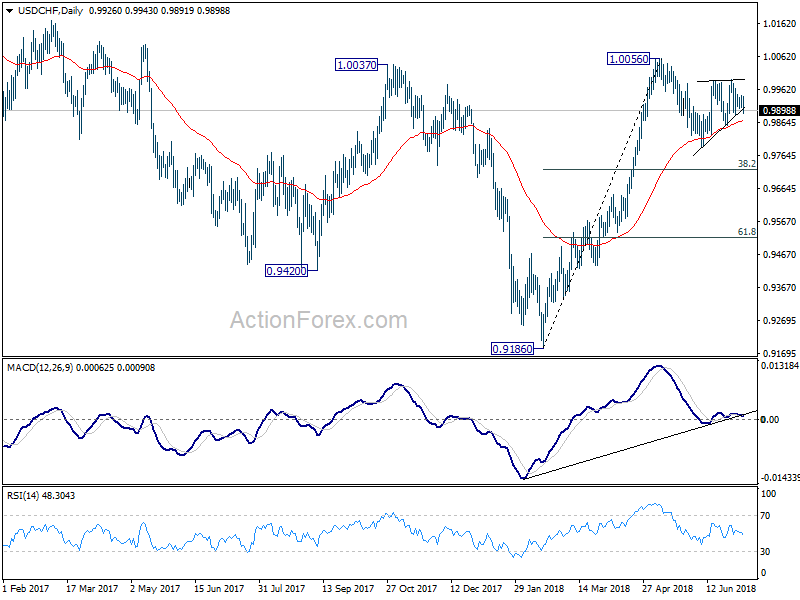

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9913; (P) 0.9929; (R1) 0.9951; More...

USD/CHF drops notably in early US session but stays above 0.9855 minor support. Intraday bias remains neutral first. On the downside, break of 0.9855 will extend the corrective pattern from 1.0056 with another fall. Intraday bias would be turned to the downside for 0.9787 and below. But downside should be contained by 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

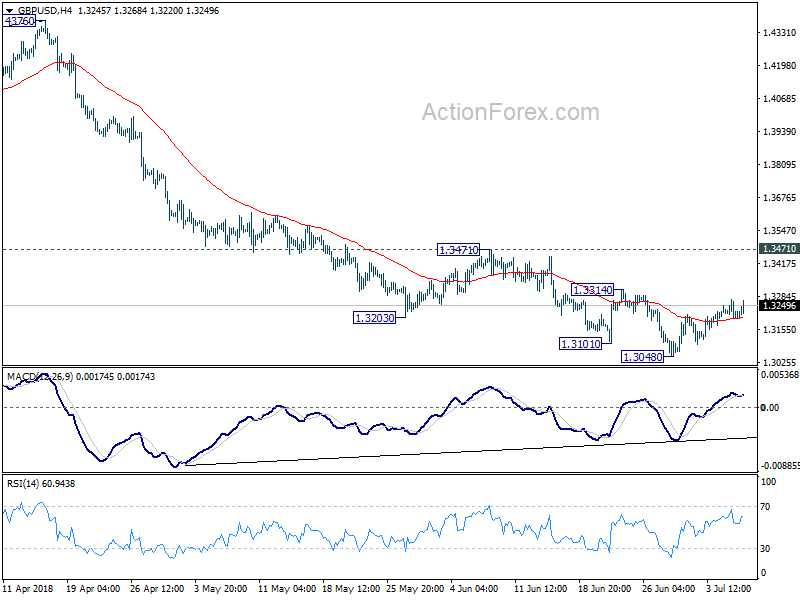

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3178; (P) 1.3226; (R1) 1.3269; More...

No change in GBP/USD's outlook. Recovery from 1.3048 could extend higher. But we'd still expect upside to be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

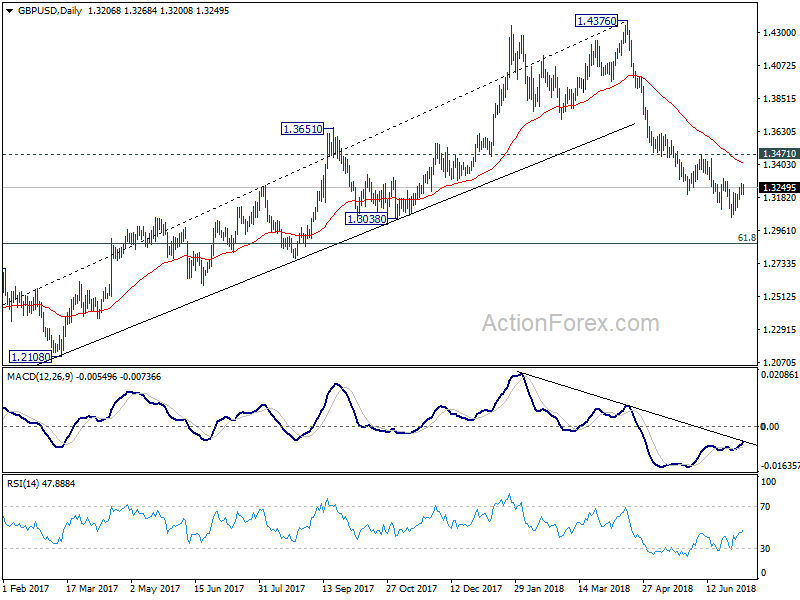

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4121). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

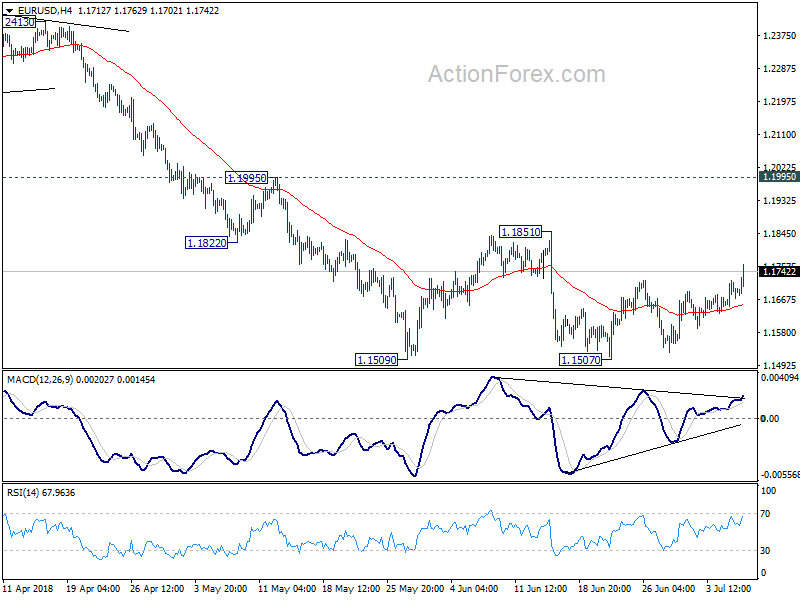

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1654; (P) 1.1687 (R1) 1.1726; More.....

EUR/USD"s rebound extends to as high as 1.1762 so far today. Intraday bias is mildly on the upside for further rise. Still, price actions from 1.1507 are seen as a correction. Hence, upside should be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

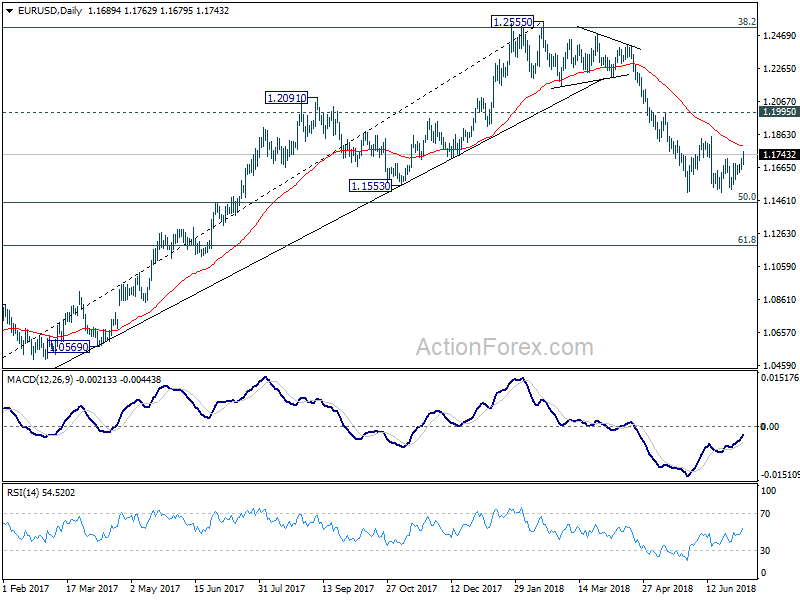

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Dollar Pullback Resumes as NFP Risks Cleared

Dollar trades notably lower in early US session despite stronger than expected headline NFP number. The rise in unemployment rate and slower than expected wage growth could be the factors. But it's more likely just continuing this week's pull back after NFP risk is cleared. Yen is following as the second weakest one for today. Meanwhile, Aussie and Kiwi are trading as the strongest, followed by Euro.

Non-farm payroll report showed 213k growth in June, above expectation of 190k. Prior month's figure was revised up from 223k to 244k. Unemployment rate rose to 4.0%, up from 3.8%. But that's mainly thanks to rise in participation rate from 62.7% to 62.9%. Wage growth was a miss though as average hourly earnings rose 0.2% mom versus expectation of 0.3% mom. Also from the US, trade deficit narrowed slightly to USD -43.1B in May.

From Canada, the employment market rose 31.8k in June, above expectation of 24.0k. Unemployment rate rose to 6.0%, up from 5.8%. Also, that's due to rise in participation rate from 65.3% to 65.5%. Trade deficit widened to CAD -2.8B in May.

Released earlier today, Swiss foreign currency reserves rose to CHF 749B in June. German industrial production rose 2.6% mom in May. Japan leading index rose to 106.9 in May. Japan household spending dropped -3.9% yoy in May, labor cash earnings rose 2.1% yoy.

Chinese Premier Li: Trade war is never a solution

In response to the start of US section 301 tariffs on USD 34B in Chinese import, Chinese Foreign Ministry spokesman Lu Kang said in a daily media briefing that "after the United States unfairly raised tariffs against China, China immediately put into effect raised tariffs on some U.S. goods." Lu also reiterated that "On the specifics of the trade issue, from the start China's position has been very clear and consistent. The United States at all levels is very clear on China's position,"

Commenting on the issue, Chinese Premier Li Keqiang said in Bulgaria that trade war is "never a solution" and there will be no winner. And, "it benefits no one and it would undermine the multilateral free trade process," he said. "If one insists on waging a trade war it would hurt others and themselves." He reiterated that China is committed to further opening up its markets. But, "if any party resorts to increase of tariffs, china would take measures in response to protect china development interests and safeguard multilateral trade regime and rules."

Trump threatens tariffs on USD 500B of Chinese goods

US Section 301 tariffs on USD 34B of Chinese imports takes effect today. Ahead of that, Trump raised his threat again and warned of tariffs on up to USD 500B of Chinese goods. He told reports that "you have another 16 (billion dollars) in two weeks, and then, as you know, we have $200 billion in abeyance and then after the $200 billion, we have $300 billion in abeyance. Ok? So we have 50 plus 200 plus almost 300."

Japan cabinet revised down fiscal 2018 growth forecast

Japan Cabinet Office presented new economic projections at the Council on Economic Fiscal Policy today.

For current fiscal 2018, the economy is projected to grow 1.5% in real term. That's a downgrade from prior projection of 1.8%, down at the start of the year. In nominal terms, the economy is projected to grow 1.7%, sharply lower from prior forecast of 2.5%, due partly to slowdown in property investment.

The office forecasts the economy to grow 1.5% in the fiscal-2019, in price adjusted real terms. That's after adjustment to the planned sales tax hike in October 2019. In nominal term, GDP is projected to grow 2.8%.

For the current fiscal 2018, overall CPI is projected to be at 1.1%, unchanged from prior estimate. Overall price CPI is forecast to rise 1.5% in fiscal 2019. With adjustment on the sales tax hike, overall CPI is projected to slow to 1.0%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1654; (P) 1.1687 (R1) 1.1726; More.....

EUR/USD"s rebound extends to as high as 1.1762 so far today. Intraday bias is mildly on the upside for further rise. Still, price actions from 1.1507 are seen as a correction. Hence, upside should be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y May | -3.90% | -1.50% | -1.30% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y May | 2.10% | 0.90% | 0.80% | 0.60% |

| 05:00 | JPY | Leading Index CI May P | 106.90% | 106.50% | 106.20% | |

| 06:00 | EUR | German Industrial Production M/M May | 2.60% | 0.30% | -1.00% | -1.30% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 749B | 741B | ||

| 12:30 | CAD | Net Change in Employment Jun | 31.8K | 24.0K | -7.5K | |

| 12:30 | CAD | Unemployment Rate Jun | 6.00% | 5.80% | 5.80% | |

| 12:30 | CAD | International Merchandise Trade (CAD) May | -2.8B | -3.6B | -1.9B | |

| 12:30 | USD | Change in Non-farm Payrolls Jun | 213K | 190K | 223K | 244K |

| 12:30 | USD | Unemployment Rate Jun | 4.00% | 3.80% | 3.80% | |

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.20% | 0.30% | 0.30% | |

| 12:30 | USD | Trade Balance May | -43.1B | -47.0B | -46.2B | -46.1B |

| 14:00 | CAD | Ivey PMI Jun | 64.8 | 62.5 | ||

| 14:30 | USD | Natural Gas Storage | 76B | 66B |

Non-farm Payrolls rose 213k, beat expectations. But unemployment rate and wage growth miss

Dollar trades notably lower in early US session despite stronger than expected headline NFP number. Non-farm payroll report showed 213k growth in June, above expectation of 190k. Prior month's figure was revised up from 223k to 244k. Unemployment rate rose to 4.0%, up from 3.8%. But that's mainly thanks to rise in participation rate from 62.7% to 62.9%. Wage growth was a miss though as average hourly earnings rose 0.2% mom versus expectation of 0.3% mom. Also from the US, trade deficit narrowed slightly to USD -43.1B in May.

From Canada, the employment market rose 31.8k in June, above expectation of 24.0k. Unemployment rate rose to 6.0%, up from 5.8%. Also, that's due to rise in participation rate from 65.3% to 65.5%. Trade deficit widened to CAD -2.8B in May.