Sample Category Title

PMI Data From The UK And Canada Expected To Show Some Weakness

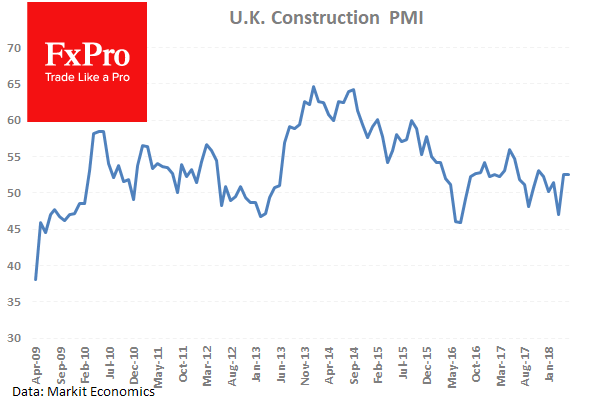

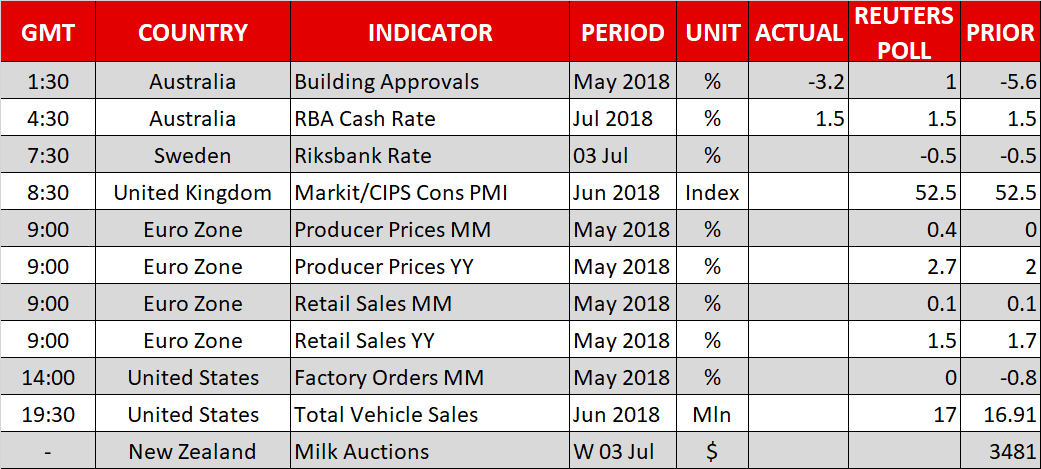

At 08:30 GMT, UK Construction PMI (Jun) will be out with an expected headline number of 52.0 from a prior number of 52.5. The consensus is for the numbers today to remain in line with expectations after the data stabilized around 52.5 for the last two months, up from the low created in April at 47.0. The industry has recovered somewhat but is well off the peak from 2014 of 64.6. GBP pairs may see an impact from this data release.

At 13:30 GMT, Canadian Markit Manufacturing PMI (Jun) is expected to be 55.4 against the previous 56.2. This data set broke above the high from February at 55.9, when it matched the April 2017 number. The expectation for this reading to fall slightly from the high, as trade tensions start to impact manufacturing planning. CAD pairs may see prices move after this data release.

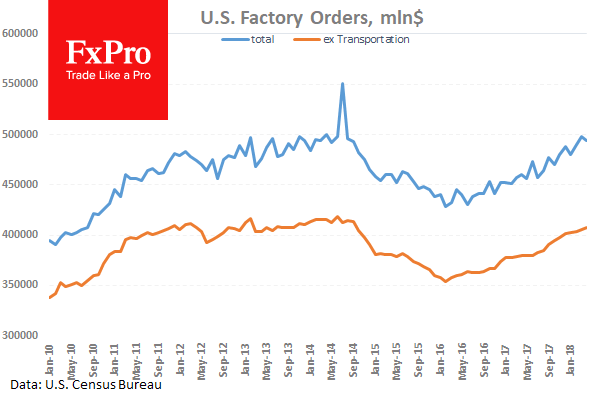

At 15:00 GMT, US Factory Orders (MoM) (May) are expected to be 0.0% from -0.8% previously. This data is expected to move to zero from negative territory today. If the increase in expectations comes to pass it represents a small drop as the recent range of this data point over the last three years has been between +3% and -3.5%. USD crosses can be moved by this data.

Tentative – Global Dairy Trade Price Index is expected to be released with a previous reading of -1.2%. There have now been two negative readings in a row as Dairy prices come under pressure. NZD pairs can be affected by this data release.

At 16:00 GMT, ECB’s Praet is due to deliver a keynote speech at a Gala Dinner hosted by the National Bank of Romania in Bucharest, Romania. EUR crosses can be moved by any comments made in relation to ECB policy.

GBPUSD Remains In Bearish Mode, Struggles Below 50.0% Fibonacci

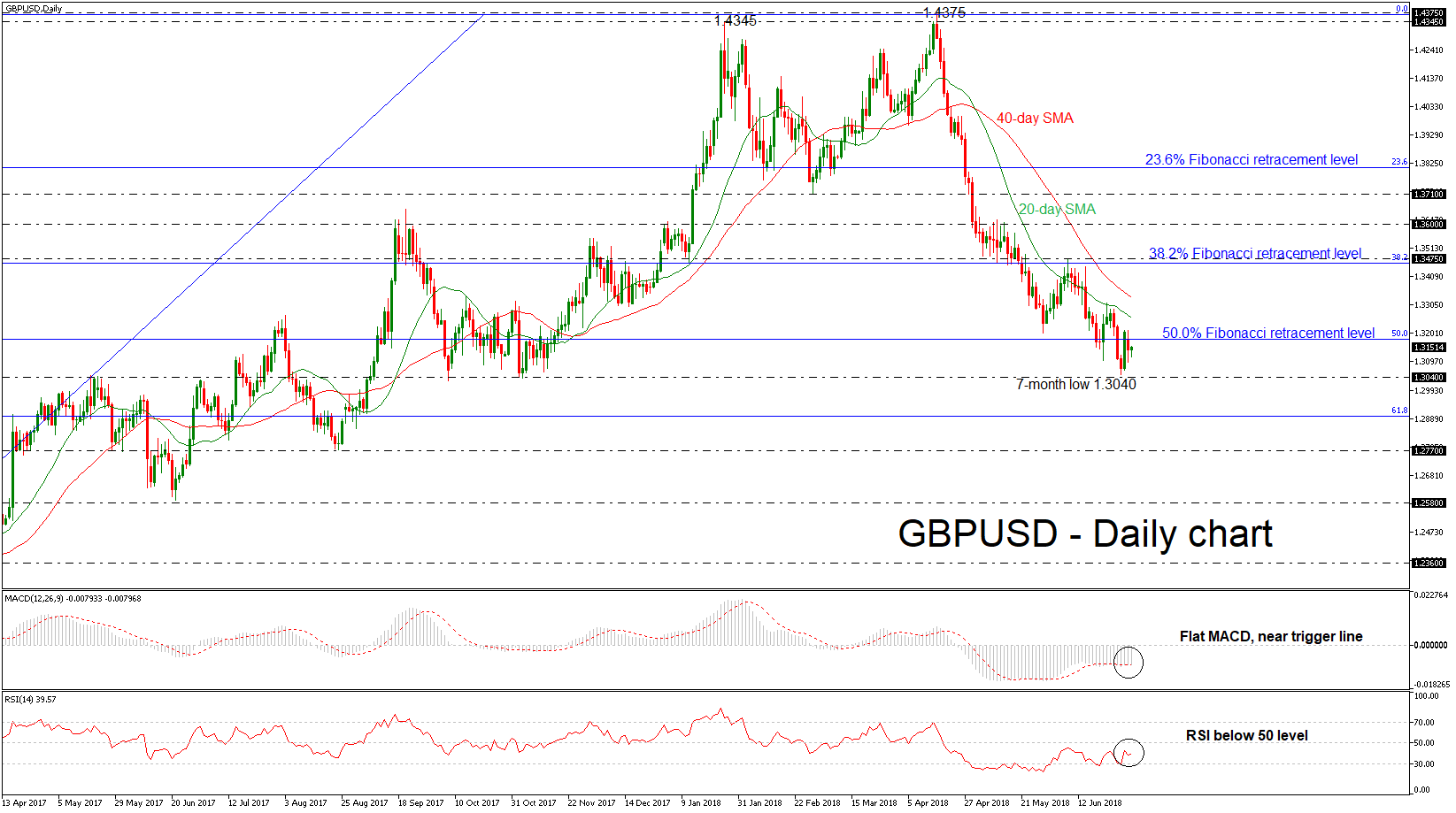

GBPUSD started the week in negative territory and slipped below the 50.0% Fibonacci retracement level of the upleg from 1.2100 to 1.4375, around 1.3180. The price has been extending its bearish bias after the touch on the 1.4375 resistance on April 17. Since then, the cable continues the downward movement, shifting the bullish outlook to bearish.

Short-term momentum indicators are holding below their neutral levels. The MACD oscillator stands near its red-trigger line with weak momentum, while the Relative Strength Index (RSI) lies below the threshold of 50 and is flattening. Moreover, the price action stands below the 20- and 40-simple moving averages (SMAs), suggesting further losses.

Should prices head lower, immediate support could some at the 1.3040 taken from the latest lows. A drop below this area would take the pair closer to the 61.8% Fibonacci near the 1.2900 psychological level, which acts as major support.

On the flip side, there is immediate resistance just above the current market price, the 50.0% Fibonacci. A significant leg above this hurdle would drive the price until the 20- and then the 40-SMAs at 1.3260 and 1.3335 respectively. A breach of these levels would hit the 38.2% Fibonacci near 1.3475.

Overall, GBPUSD has been developing within a downtrend since April 17 started an aggressive bearish rollercoaster. The medium-term picture remains negative as the price is still moving below the moving averages.

Euro Cheers German Deal, Awaits Producer Price & Retail Sales Data

Here are the latest developments in global markets:

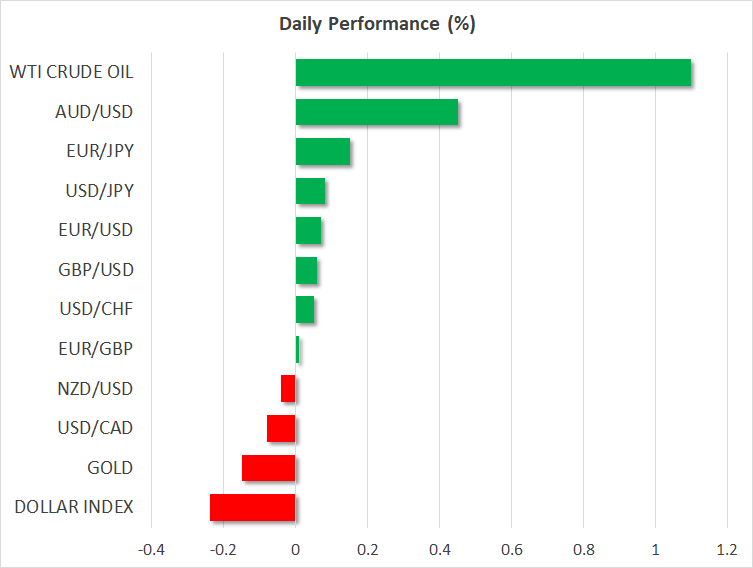

FOREX: The US dollar index is down by 0.24% on Tuesday, giving back some of the gains it posted in the previous session. The euro rebounded somewhat following news that the German political deadlock had been solved, while the aussie gained in the aftermath of the RBA’s policy meeting.

STOCKS :US markets managed to erase earlier losses and close higher on Monday, boosted by a rally in technology stocks. The tech-heavy Nasdaq Composite gained 0.76%, while the S&P 500 and the Dow Jones climbed by 0.31% and 0.15% respectively. The positive sentiment appears to have lingered, as futures tracking the Dow, S&P, and Nasdaq 100, all suggest a higher open today. In Asia, markets were mostly lower. In Japan, the Nikkei 225 and Topix fell by 0.12% and 0.15% correspondingly, while in Hong Kong, the Hang Seng dropped 1.53% on its first day back from holidays. In China, the CSI 300 rose, albeit only by 0.03%. Europe was more cheerful. Futures tracking all the major indices point to a notably higher open today, following news that the political crisis in Germany has been resolved.

COMMODITIES: Oil prices continued to ascend, with WTI crude rising 1.1% to reach a fresh three-and-a-half year high on Tuesday, propelled higher by headlines that oil exports from two of Libya’s largest ports were halted amid military tensions. Reports suggest that as much as 850,000 barrels per day may be removed from the market. Meanwhile, weekly API data (2030 GMT) might offer some short-term direction to oil prices. In precious metals, gold is down by 0.15%, currently trading near $1,244 per troy ounce. It touched a new low for the year at $1,238 earlier on Tuesday, before rebounding somewhat. The technical picture remains negative, though the area around $1,238 appears to be a strong support zone; it also halted the metal’s decline back in December.

Major movers: Euro steadies on German accord; aussie rebounds after RBA

The euro is a little higher on Tuesday, recovering some of its losses from the previous session, following positive headlines out of Germany. The political crisis that was seen as threatening the stability of Angela Merkel’s coalition government has reportedly passed, after she managed to strike a deal with the “rebels” in her cabinet on immigration.

In the UK, sterling failed to capitalize on news that the government has prepared a new plan for handling customs after Brexit; an issue that has been a thorn in negotiations so far. The proposal will be presented to UK ministers on Friday, and is expected to be followed by a White Paper outlining the UK’s preferred path. Judging by the subdued market reaction so far though, investors do not anticipate this to be the “smoking gun” that breaks the deadlock in the negotiations. With the political crisis in Germany now resolved, but Brexit uncertainties still riding high, the risks surrounding euro/sterling may be tilted to the upside over the coming days.

Overnight, the RBA kept its policy untouched and maintained a fairly neutral bias. It highlighted concerns around global trade, but also took note of the strength in the domestic economy. The key message was that while Australia is humming along nicely, many global uncertainties persist, and policy will stay unchanged for a while. Aussie/dollar is 0.45% higher today, but continues to trade close to 18-month lows. The pair will remain highly sensitive to trade issues; note the US and China will slap tariffs on each other on Friday, and further escalation should not be ruled out. Absent any improvement in trade tensions, the outlook for the aussie may remain negative.

The Chinese yuan continued to slide, touching an eleven-month low against the dollar. While the move appears market-driven, possibly on the back of trade worries, the fact that the Chinese authorities have not intervened to halt – or at least slow – the drop suggests they may be somewhat comfortable with a depreciating currency at this point.

Day ahead: Eurozone producer prices and retail sales due; US factory orders and UK construction PMI also out; Riksbank decides

Tuesday’s calendar features a few releases of relative importance, including eurozone producer prices and retail sales, as well as factory orders out of the US.

At 0730 GMT, the Swedish central bank – the Riksbank – will be announcing its interest rate decision, with the monetary policy report being released at the same time. A press conference by the Bank’s governor will follow at 0900 GMT.

The UK will be seeing the release of construction PMI data for June at 0830 GMT. This comes one day ahead of the respective print for the all-important for the UK economy services sector.

Eurozone producer prices and retail sales for May are due at 0900 GMT. Producer prices are expected to accelerate on both a monthly and yearly basis. As regards retail sales, those are projected to grow by 0.1% m/m, the same as in April, while they’re anticipated to ease to 1.5% on an annual basis from 1.7% in the previously tracked month.

US factory orders are slated for release at 1400 GMT. No monthly growth in orders is expected during May, after April’s contraction by 0.8%. Meanwhile, data on total vehicle sales out of the world’s largest economy will be made public at 1930 GMT.

The outcome of the bi-weekly milk auction will be known later today, though there’s no specific time of release. Kiwi pairs will be generating attention as the data are made public; dairy products are New Zealand’s largest goods export earner, with higher prices seen as supporting the NZD.

Trade remains a dominant theme in markets only a few days before US tariffs on Chinese-imported goods become effective (July 6). In the meantime, volatility in the yuan is something that is being monitored by officials in the Chinese central bank (PBOC).

ECB Chief Economist Peter Praet will be giving a speech at 1400 GMT.

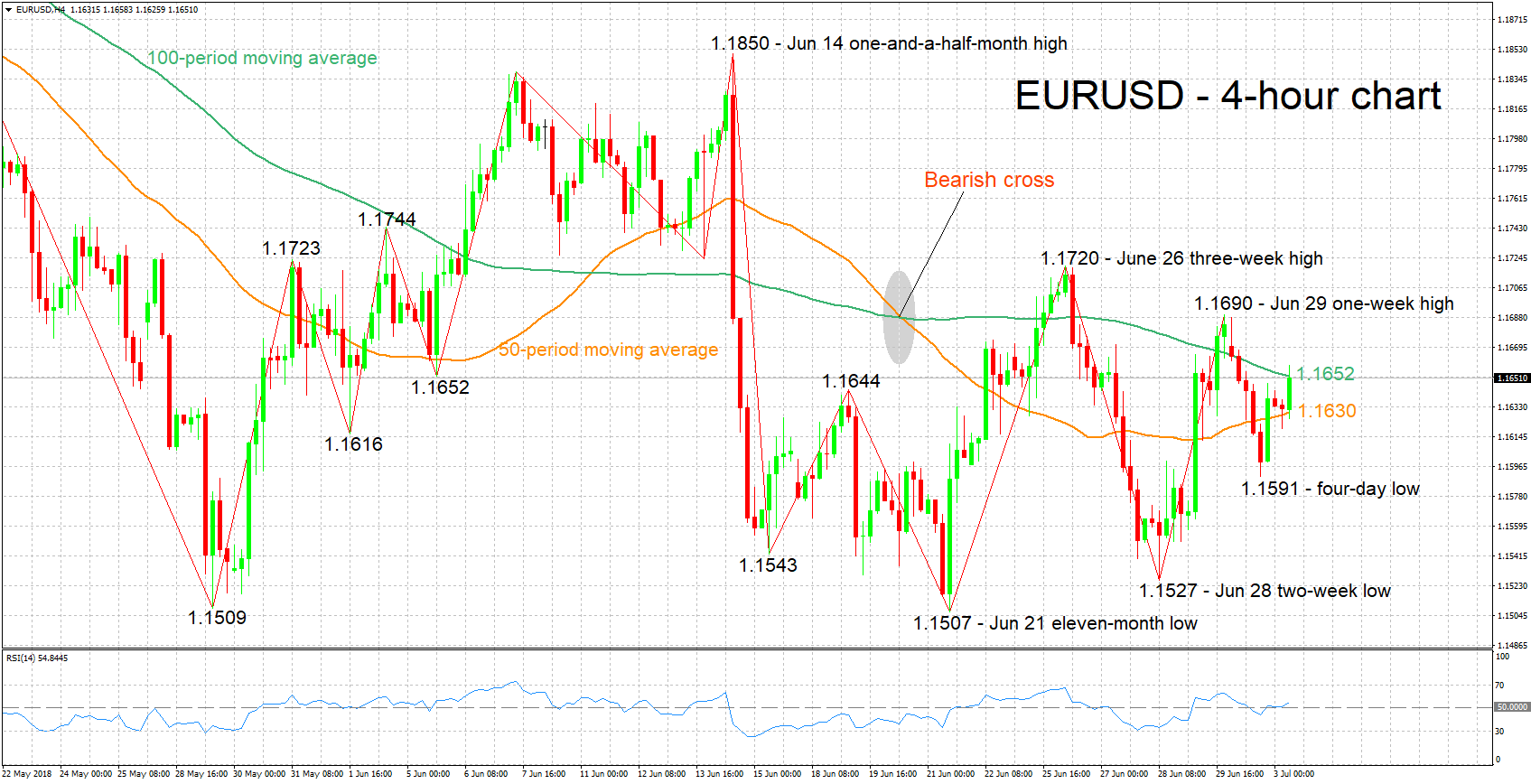

Technical Analysis: EURUSD neutral-to-bullish in the short-term

EURUSD has managed to climb after hitting a four-day low of 1.1591 on Monday and is currently challenging the current level of the 100-period moving average line (1.1652) on the 4-hour chart. The RSI has moved above the 50 neutral-perceived level and continues to rise. Notice though that the indicator is still close to neutral levels and does not maintain a steep positive slope, overall projecting a neutral-to-bullish picture in the short-term.

Upbeat data out of the eurozone are likely to boost the pair. Immediate resistance is taking place around the 100-period MA at 1.1652, with the attention falling to the one-week high of 1.1690 from late June in case of a break to the upside.

Disappointing figures on the other hand are expected to see EURUSD coming under selling pressure. Support could come around the 50-period MA at 1.1630 and then from the region around yesterday’s four-day low 0f 1.1591 (including the 1.16 handle).

EURUSD Intraday Bullish Above 1.1600

The euro currency has started to move higher against the US dollar after Angela Merkel struck a migration deal with her coalition partners, which helped to avoid a political crisis in Germany. The EURUSD pair currently trades around the 1.1630 region, and retains an intraday bullish bias while trading above the 1.1600 support level. EURUSD traders now look towards key Retail Sales and Inflation data from the eurozone economy this morning.

The EURUSD pair is intraday bullish while trading above the 1.1600 level, key resistance is found at the 1.1674 and 1.1724 levels.

If EURUSD pair falls below the 1.1600 level, key technical support is found at the 1.1580 and 1.1544 levels.

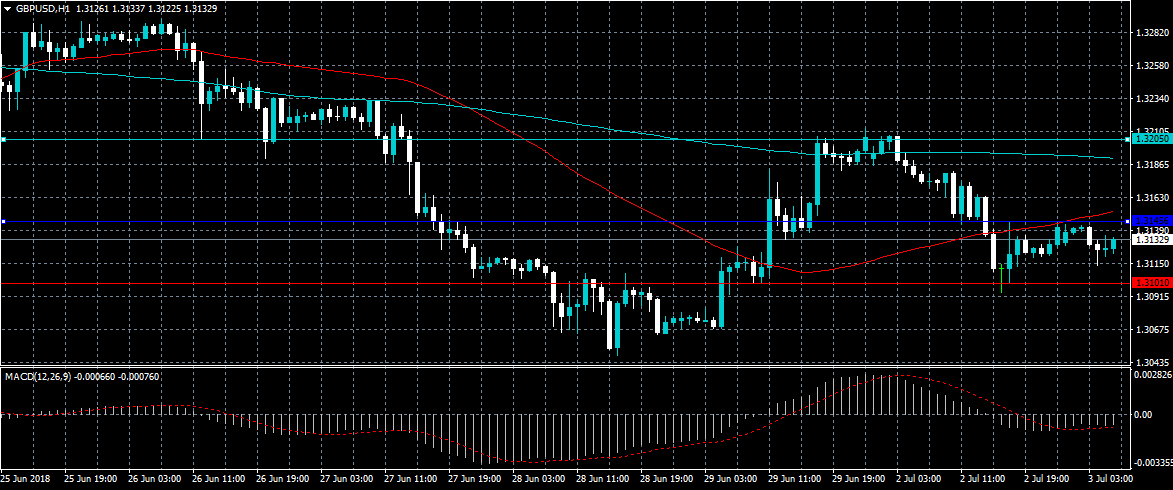

GBPUSD Intraday Bullish ABove 1.3101

The British pound has started to move higher against the US dollar after sellers failed to hold price below the key 1.3101 support level on Monday. The GBPUSD pair currently trades around the 1.3130 region, and retains a bullish intraday bias while trading above the key 1.3101 level. Sterling traders now look to the release of key PMI Construction data from the United Kingdom economy this morning.

The GBPUSD pair is intraday bullish while trading above the 1.3101 level, key resistance is found at the 1.3145 and 1.3205 levels.

If the GBPUSD pair trades below the 1.3101 level, heavy declines towards the 1.3065 and 1.3030 support levels remain possible.

EURO Gains After Mekrkel Makes A Deal With Interior Minister

The euro is up slightly against the dollar after Angela Merkel agreed with interior minister Horst Seehofer on a new border control plan.

According to the deal, Germany will set up major holding and processing centres for asylum seekers at the German borders. Horst believes that this will help the country prevent or reduce illegal entry by migrants via the Austrian-Germany border. There is a long way to go before the new policy becomes government policy because the deal requires consent from the social democrats.

In other news, major economic data from the US is expected today including durable goods and factory order numbers, which will give traders an indication of how well the economy is performing. From the EU, releases will include retail sales and employment numbers from Spain.

The dollar index is up after yesterday’s PMI data from the Institute of Supply Management (ISM). The data showed that the PMI was up in June to 60.2. This was better than the expected 58.4 and the 58.7 released in June. The figures served as a positive boost for the dollar at a time when manufacturers are facing a big challenge in their industry. On the other hand, construction rose by 0.4%, which was lower than the expected 0.5%.

In late January, the Australian dollar started to slide after reaching a high of 0.8134 against the dollar. Today, the pair is trading at 0.7338, which is the lowest level since September last year. The decline was due to dovish statements from the RBA and the hawkishness of the Fed. Today, the data on building approvals for the month of May disappointed. The approvals declined by 3.2%, which was worse than the expected 1.0% increase. The RBA left interest rates unchanged at 1.50%.

EUR/USD

The EUR/USD pair is trading at 1.1632, which is higher than yesterday’s intraday low of 1.1590. The latter was the pair’s 38.2% Fibonacci Retracement level while the current price is slightly above the 50% level. Traders will focus on the deal between Angela Merkel and her coalition partners. Depending on the news, the pair could continue the upward momentum, which will see it cross yesterday’s high of 1.1690. The alternative scenario is where the pair slides. If it does, it will likely test the 1.1574, which is the 23.6% Fibonacci Retracement level.

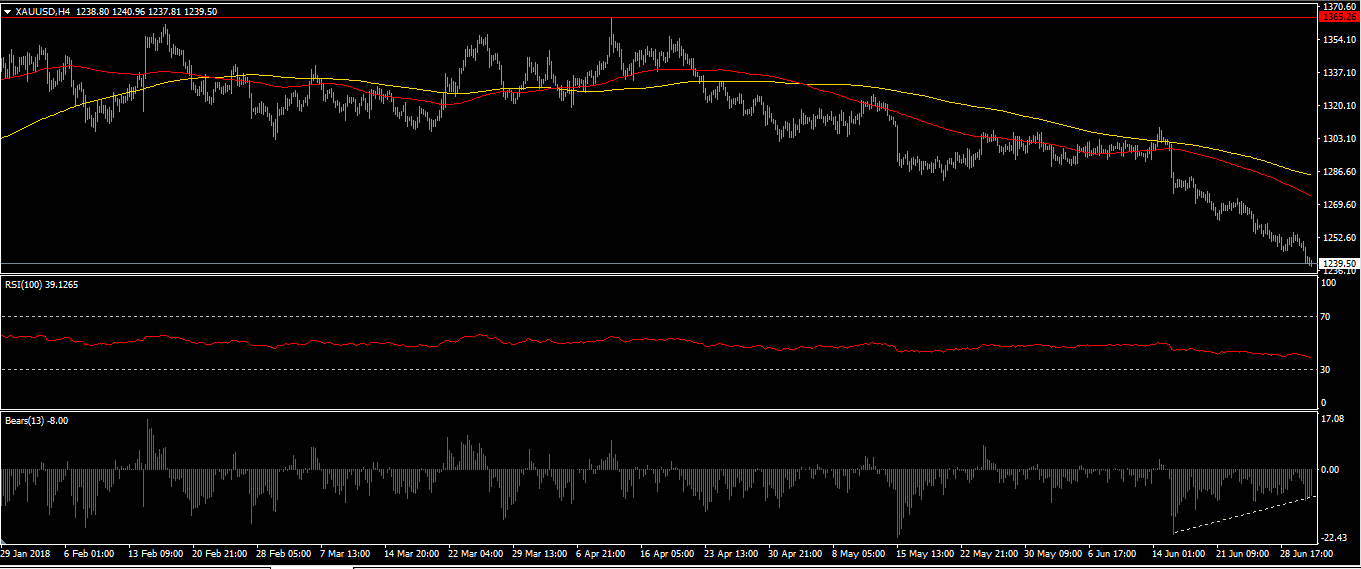

XAU/USD

The XAU/USD pair has continued to slide and is currently trading at the lowest level since December last year. The decline of gold is mostly because of a strong dollar. The pair is currently at $1239.41. The price is below the 100 and 200-day moving average. The pair is likely to remain at these lows as traders wait for the RSI to cross the oversold level of 30.

AUD/USD

The Australian dollar has dropped by almost 6 percent this year. This is partly because of the dovishness of the Reserve Bank of Australia (RBA). The AUD/USD pair is currently trading at 0.7337, which is higher than yesterday’s close of 0.7310. The price is below the 50-day moving average and in line with the 25-day moving average. Today, the downward momentum could continue after the RBA made no major policy changes.

Will China’s Renminbiring The Alarm Bell?

The slight gains in U.S. equities on Monday failed to influence Asian investors as trade fears and the Renminbi's slide continued to drive risk aversion.

This sharp depreciation in the Chinese currency is worrying investors. In August 2015, USDCNY appreciated from 6.21 to 6.44, a two-day gain of 3.85%. As a result, global stock markets sold off sharply as investors feared the beginning of a currency war. With trade tensions increasing day by day, Beijing might be playing this game as a tool in its trade war with the U.S. However, such a strategy will be a double-edged sword as it might also lead to a flight of capital which the PBoC is well aware of.

Although the Chinese currency depreciated 3.23% in June, it didn't sound quite so alarming, given that the Dollar appreciated against most major currencies in May and June. Going forward it's going to be about the pace and magnitude of the currency moves that will drive equity markets. CNYUSD traded at 6.70 at the time of writing and will keep a close eye on 6.96,the lowest level reached in January 2017.

Caution is warranted at this current stage, as the ongoing trade dispute moves from announcements to implementations. Canada confirmed over the weekend that it had imposed tariffs on U.S. exports worth 16.6 billion CAD. The U.S. is set to impose a 25% tariff on up to $34 billion of Chinese products on Friday. Meanwhile, there are reports that the European Commission will impose tariffs on nearly $300 billion on U.S. products if President Trump targets the European auto industry. This sounds like a serious trade war!

Major currency markets were steady early Tuesday with the Euro, Pound, and Yen trading in narrow ranges against the dollar. The economic calendar doesn't hold tier one data today, but it's worth watching the Eurozone retail sales figures after consumer confidence dipped to itslowest level since last October and Oil prices are making another attempt to reach $80.

Oil bulls seem to have returned after Libya suspended Oil exports from two key ports. If Libya's Oil doesn't return fast to the market it will be an important test to OPEC's spare capacity, especially given that output from Venezuela and Iran is expected to fall significantly in the next couple of months.

EURUSD Is Blocked In The 1.1500/1.1720 ST Consolidation Range

Markets

Yesterday, global markets started in risk off modus as investors pondered the impact from the trade war especially on Asian/EM economies. The German political crisis was also a source of uncertainty. However, global risk sentiment improved throughout the session. The US Manufacturing ISM was strong/better than expected (60.2). Initially, the report had little impact on markets. Later in US dealings, equity sentiment improved further and (US) bonds lost some further ground. The US yields curve bear flattened with yields rising between 2 bp (2-y) and 0.4 bp (30-y). Changes in German yields were negligible with the short end slightly out performing (2y -1.5bp). After the close of the European markets, the CDU-CSU coalition partners reached a compromise on migration policy. So, an immediate political crisis is probably averted.

This morning, Asian markets fail to join the risk rebound in the US yesterday. China again underperformed, but sentiment tentatively improves toward the end of the session. Later today, the eco calendar is thin. EMU retail sales are no market mover and neither are US factory orders. Sentiment on risk and headlines on global trade will have to guide trading. Until now, sentiment on US equity markets remains fairly constructive, but uncertainty on EM/China probably will keep the downside in core bond rather well protected. Some further consolidation near recent levels might be on the cards for the Bund and the US 10-y Note future.

Yesterday, the dollar succeeded a gradual intraday uptrend for most of the session. EUR/USD filled bids just below 1.16 at the end of the European session. EM uncertainty and at the same time a slight rise in US yields supported the US currency. Late in the session the euro spiked higher as a German political crisis was avoided. EUR/USD finished the day at 1.1639 (from 1.1684). USD/JPY closed at 110.90.

This morning, the (trade-weighted) dollar (DXY) trades little changed just below 95. However, the ‘free-fall' of the yuan continues unabatedly. USD/CNY jumped north of the 6.70 mark! Markets are looking for indications of the PBOC taking action to stop the sell-off. The likes of the Korean won also remain under pressure, but spill-over effects to the euro (or the yen) remain limited. EUR/USD is blocked in the 1.1500/1.1720 ST consolidation range. That said, the dollar probably will remain the benefit of the doubt.

Yesterday, sterling declined against a broadly stronger dollar but hovered sideways against the euro. The UK manufacturing PMI was slightly stronger than expected (54.4) but was largely ignored. Today, the UK construction PMI is expected unchanged at 52.5. There will again be plenty of Brexit headlines as UK PM May tries to find consensus on a Brexit plan ahead of a key Cabinet meeting later this week. More EUR/GBP consolidation in the mid 0.88 area might be on the cards as long as visibility on the Brexit remains low.

News Headlines

Angela Merkel and her interior minister Seehofer have finally agreed on a migration deal, after the CSU-CDU coalition was in danger yesterday. The deal agrees that asylum seekers who are already registered in another EU country will be held at transit centers on the German-Austrian border before they are sent back.

US manufacturing remains strong despite the trade war worries, according to the ISM Manufacturing index. The ISM index rose to 60.2 in June from 58.7 in May while economists expected a drop to 58.5. This strong outcome proves the US economy is not slowing down despite nervousness about trade wars.

US President Trump has fueled the rumors that the US is thinking about leaving the WTO. Trump openly stated that "the WTO has treated the US very, very badly". He suggested they would take action if they don't treat the US properly. However, Trump's commerce secretary said reforms are needed but a withdrawal is not on the table.

PBoC Yi: Yuan fluctuation due to USD strength and external uncertainties

China's Central Bank, PBoC, issued a statement in its website regarding Governor Yi Gang's response to China Securities Journal regarding recent decline in the Yuan.

Yi acknowledged the fluctuation in the exchange rate and said the central bank is "pay closing attention". He attributed to the decline of Chinese Yuan to strength of the US Dollar, external uncertainties and some procyclical behaviors.

He also noted that the "managed floating exchange rate system" is based on market supply and demand. And "practice over the years has proven that this system must be effective and must be adhered to".

At the same time, China is committed to deepen the reform of exchange rate marketization and use sufficient policy tools to " maintain the basic stability of the RMB exchange rate at a reasonable and balanced level."

Full release in simplified Chinese.

Suggested reading, our report Has China Given Green light to Renminbi Selloff?

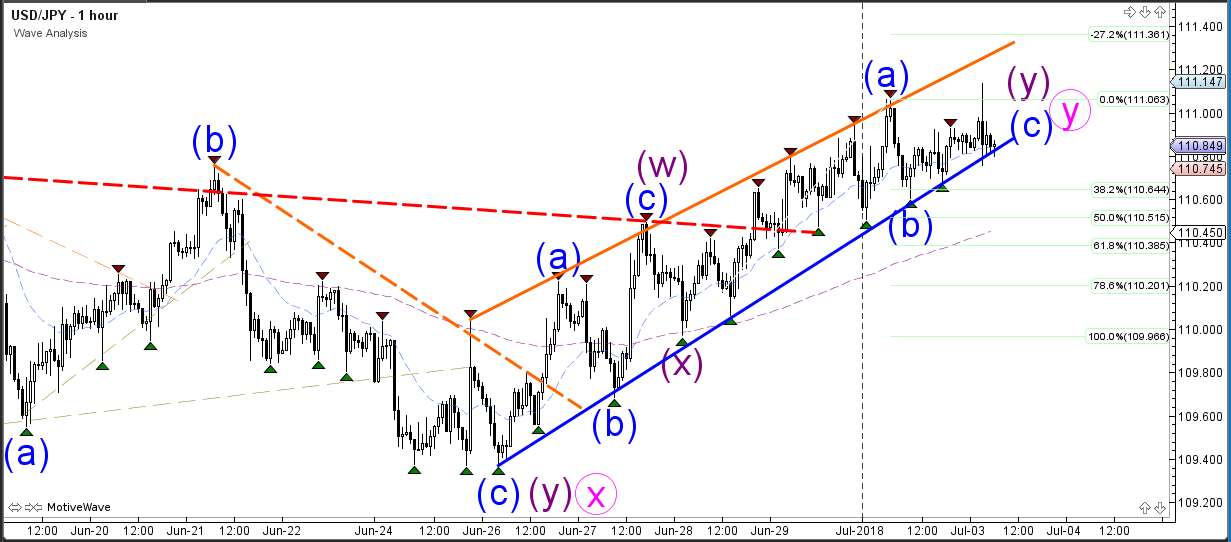

USD/JPY Builds Corrective Pattern In Uptrend Channel

The USD/JPY remains in an uptrend channel, although price action is becoming choppier and more corrective. A bullish break above the previous top at 111.40 could confirm the wave Y (pink) whereas a bearish break below the support trend lines (blue) could indicate an expanded wave X (pink) at a lower spot.

The USD/JPY could move up to the Fibonacci targets if price bounces at the support zone (blue). For the moment, that does seem the most likely scenario when taking into account the uptrend. However, a break below 110.50 would seriously challenge this particular market structure.