Sample Category Title

China Releases Unscheduled June Export To US Data Showing A Dramatic Drop

General Trend:

- Asian equity markets trade mostly lower, despite gains in the US

- Chinese equities extend declines

- Gaming names in China and Hong Kong trade lower on Macau gaming Rev figures yesterday

- Property shares in China continue to drop amid reports of additional curbs

- Macau casino firms decline on weaker than expected monthly revenues

- Fast Retailing expected to report monthly SSS after the Nikkei close

- China releases data for June exports to the US in uncommon move

- PBoC official said China has ‘many’ FX tools, reiterated to keep yuan stable

- China fixed the yuan (CNY) at the weakest since late Aug 2017

- New Zealand Q2 business confidence hits 7-year low

- RBA leaves policy unchanged (as expected), notes the Aussie has depreciated ‘a little’

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.4%

- TOPIX Marine Transportation index -0.9%

- (JP) Japan Jun Monetary Base: ¥502.9T v ¥492.6T prior; y/y: 7.4% v 8.1% prior; Japan companies see inflation in 1 year at 0.9% y/y (prior 0.8%); 3 years at 1.1% y/y (prior 1.1%); 5 years at 1.1% y/y (prior 1.1%) -

- (JP) Japan Fin Min Aso: More trade is good for Japan; if US/China trade war escalates it will affect others

- (JP) Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.037% v 0.048% prior; bid to cover 4.37x v 4.38x prior

Korea

- Kospi opened +0.6%

- (KR) SOUTH KOREA JUN CPI M/M: -0.2% V 0.1%E; Y/Y: 1.5% V 1.7%E

- 003550.KR New chairman and CEO Koo Kwang-mo looking at each unit and how to make it profitable - Korean press

- (KR) Korean press comments on the challenges for South Korea companies on the continued steep decline of the won in recent weeks. The weakening of the won in recent weeks carries both benefits and risks for the Korean economy that is being held back by a simultaneous downturn in investment, consumption and exports.

- (KR) South Korea sells KRW1.65T v KRW1.65T indicated in 30-yr bonds; avg yield 2.565%

- (US) White House confirms Sec of State Pompeo will head to North Korea on July 5th

China/Hong Kong

- Hang Seng opened -1.2%, Shanghai Composite 0.0%

- Hang Seng Services index -5.5%, Materials -4.9%, Energy -4.7%, Consumer Goods -4.1%, Industrial Goods -4.1%, Property/Construction -3.7%, Financials -3.3%, Info Tech -3%

- China Mobile [941.HK]: US Commerce Dept reportedly recommends against China Mobile entry into US market - press

- (CN) Shanghai implements restrictions on housing purchases by enterprises - local press

- Guoco, 53.HK Controlling shareholder offered to acquire the company for HK$135/share (~14% premium to prior close)

- (CN) China PBoC set yuan reference rate at 6.6497 v 6.6157 prior (weakest setting since late Aug 2017)

- (CN) China PBoC Open Market Operation (OMO): Skips OMO operations for the second consecutive day; Net: CNY150B drain v CNY20B drain prior

- (CN) China June exports to the US said to be +3.8% y/y - Chinese press

- (CN) PBOC Deputy Gov Pan Gongsheng: Bond defaults good for long term development of China market; China confident to keep yuan stable in reasonable range, reiterates fundamentals are strong and economy is resilient; China has ample foreign reserves

- (CN) Major state owned China banks seen swapping yuan for dollars in forwards and immediately selling them into spot market to support the yuan

- China Mobile, 941.HK US Commerce Dept reportedly recommends against China Mobile entry into US market - press

Australia/New Zealand

- ASX 200 opened 0.0%

- ASX 200 Telecom index +1.6%, Consumer Discretionary +0.9%, Financials +0.8%, Energy +0.6%, REIT +0.5%; Resources -1%

- (NZ) New Zealand Q2 NZIER Business Confidence: -20 v -11 prior (7-yr low); Capacity Utilization: 92.8% v 93.5% prior

- (AU) Australia Department of Industry, Innovation & Science lowers FY17/18 resource earnings by ~A$3.3B; Raises FY18/19 resource earnings by A$7.8B

- (AU) AUSTRALIA MAY BUILDING APPROVALS M/M: -3.2% V 0.0%E; Y/Y: +3.1% V 9.9%E

- (AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED

North America

- US equity markets ended higher: Dow +0.2%, S&P500 +0.3%, Nasdaq +0.8%, Russell 2000 +0.7%

- S&P500 Technology +0.9%, Utilities +0.7%

Europe

- (DE) Chancellor Merkel and Interior Min Seehofer reach compromise over migration - German press; Interior Min Seehofer: confirms CDU and CSU has reached agreement; will stay in post as Interior Min; Chancellor Merkel: will establish transit centers for asylum seekers; CSU/CDU accord preserves European partnership

- (UK) Chambers of Commerce: Govt has managed to make limited progress on just 2 of the 23 issues where clarity is urgently needed so that firms can plan their trade following the UK’s departure from the EU

Levels as of 01:30ET

- Hang Seng -2.5%; Shanghai Composite -0.8%; Kospi -0.2%; Nikkei225 -1.0%; ASX 200 +0.6%

- Equity Futures: S&P500 -0.2%; Nasdaq100 -0.2%, Dax -0.2%; FTSE100 -0.1%

- EUR 1.1621-1.1644; JPY 110.76-111.13; AUD 0.7314-0.7347;NZD 0.6688-0.6719

- Aug Gold -0.2% at $1,239/oz; Aug Crude Oil +0.8% at $74.56/brl; Sept Copper -0.4% at $2.93/lb

Stock Markets And Bond Yields Bounced Back

Market movers today

Today's key event is the Riksbank meeting at 9:30 CEST, where we expect the rate path to be left intact , thus indicating a hike in Q4.

Danish currency reserves data will show whether Danmarks National bank remained sidelined in the FX market in June.

Global markets continue to await the implementation of the tariffs on goods worth USD34bn from both China and the US on Friday, which could trigger a further escalation in the US-China trade war if Trump follows through on his threat to announce tariffs on another USD200bn worth of Chinese goods.

Selected market news

Stock markets and bond yields bounced back yesterday on the back of a strong US ISM manufacturing index for June, which jumped back up close to the highest level in 15 years. There is thus still no evidence of any negat ive effect on the US economy from the higher uncertainty related to trade war fears. We continue to look for moderation in US ISM in the next 3 -6 months, but so far it seems the fiscal boost in the US is giving strong support to the economy.

Risk sent iment is under pressure again in Asia though, as Chinese stocks continue their rout with the Shanghai Composite Index reaching a 28-month low. The CNY also continues the sharp decline with USD/CNY now t rading above 6.70, the highest level since August 2017, see SCMP. There is no sign of China intervening to halt the CNY decline as CNH offshore money market rates have dropped. Normally, China uses higher CNH money market rates to stem depreciat ion pressure. The lack of intervention suggests the Chinese government is allowing the CNY to slide possibly as part of the t rade war with the US. We cont inue to see risk of further CNY weakness in the short term.

In another sign of fears over Chinese growth, indust rial metals continue to slide. The LMEX industrial metals index declined to the lowest level since December last year. We have not yet seen much contagion to developed markets but the development clearly bears watching as further st ress in China and EM could spill over to developed markets.

On a positive note, the polit ical stand-off between German Chancellor Angela Merkel and CDU's sister party the CSU has come to an end, as a compromise was reached late yesterday.

The Reserve Bank of Austral ia this morning left rates unchanged at 1.5%, saying that unchanged policy is consistent with meeting the CPI target over time.

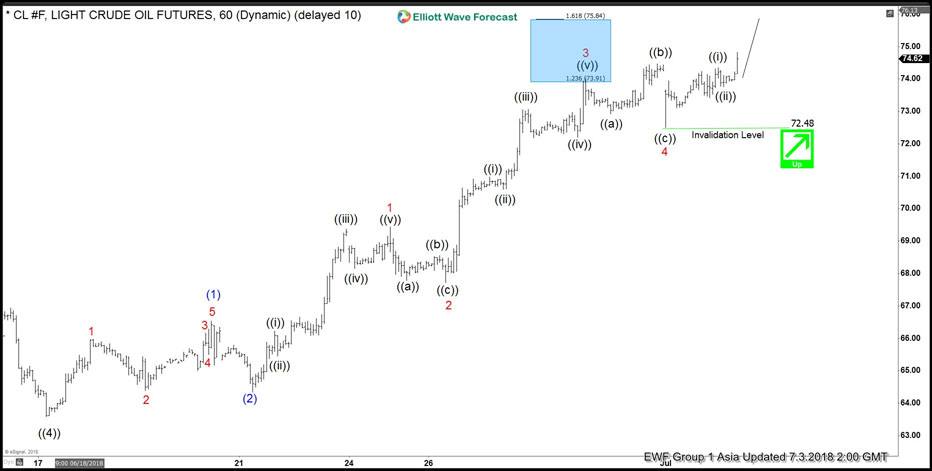

Elliott Wave Analysis: OIL Rallying Higher In An Impulse Structure

OIL short-term Elliott Wave view suggests that the pullback to $63.59 on 6/18/2018 low ended primary wave ((4)). Up from there, the instrument reacting strongly to the upside and internals of that rally higher suggests that it’s taking place in an Impulse Elliott wave structure with extension with lesser degree oscillation showing the sub-division of 5 waves structure in it’s each leg higher.

Above from $63.59 low, intermediate wave (1) ended in 5 waves structure at $66.53 high. Down from there, intermediate wave (2) pullback ended at $64.34 low. Up from there, intermediate wave (3) higher remains in progress with lesser degree cycles also showing the advance of 5 waves structure in Minor wave 1 & Minor wave 3 thus favoring more upside.

The internals of that advance ended Minor wave 1 of (3) at $69.44, Minor wave 2 of (3) ended at 67.72 low. The Minor wave 3 of (3) ended at $73.99 & Minor wave 4 of (3) ended at $72.48. Then above from there Minor wave 5 of (3) remains in progress. And as far as it stays above $72.48 instrument can reach as high as Minor wave 5=Minor wave 1 target area at $77.60-$78.84. Afterwards, the instrument is expected to do an intermediate wave (4) pullback in 3, 7 or 11 swings before further upside is seen. We don’t like selling it into a proposed pullback.

OIL 1 Hour Elliott Wave Chart

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.39; (P) 110.67; (R1) 110.96; More...

USD/JPY continues to lose upside momentum as seen in 4 hour MACD. But there is no sign of topping yet. Intraday bias stays cautiously on the upside for 111.39 high. Break there will also resume the rise from 104.62 and target 114.73 key resistance. On the downside, though, below 110.55 minor will argue that a temporary top is at least formed. More importantly, the corrective pattern from 111.39 could then extend with another down leg. Hence, in that case, intraday bias will be turned to the downside for 109.36 support and below.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

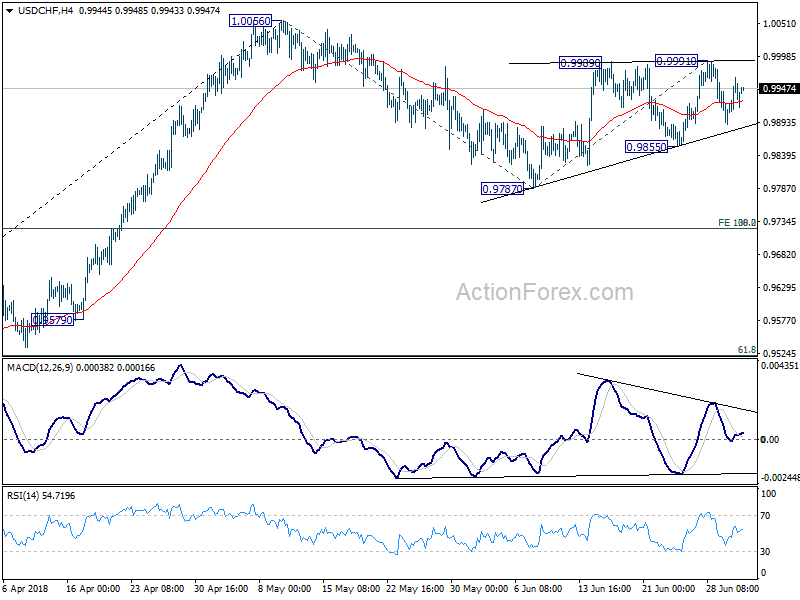

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9901; (P) 0.9933; (R1) 0.9969; More...

USD/CHF is staying in consolidation in range 0.9855/9991. Intraday bias remains neutral for the moment. On the downside, below 0.9855 will resume the corrective decline from 1.0056, likely through 0.9787 support. But downside should be contained by 0.9722/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9991 at 0.9722) to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

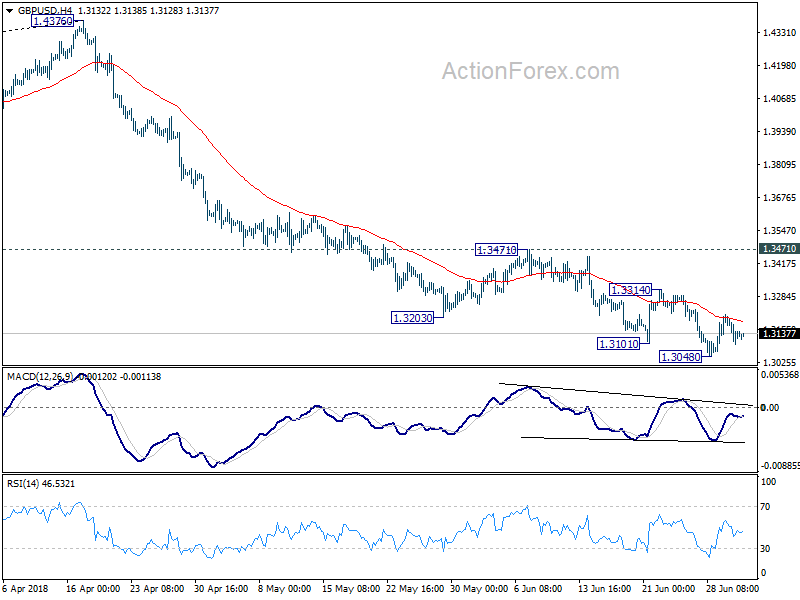

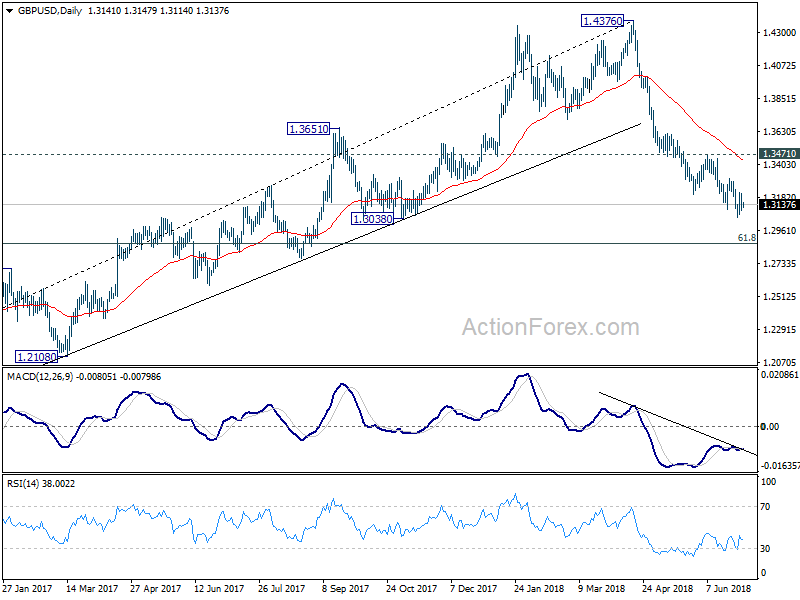

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3087; (P) 1.3151; (R1) 1.3208; More...

Outlook in GBP/USD remains unchanged as consolidation from 1.3048 continues. Intraday bias stays neutral at this point. In case of another recovery, upside should be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4121). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

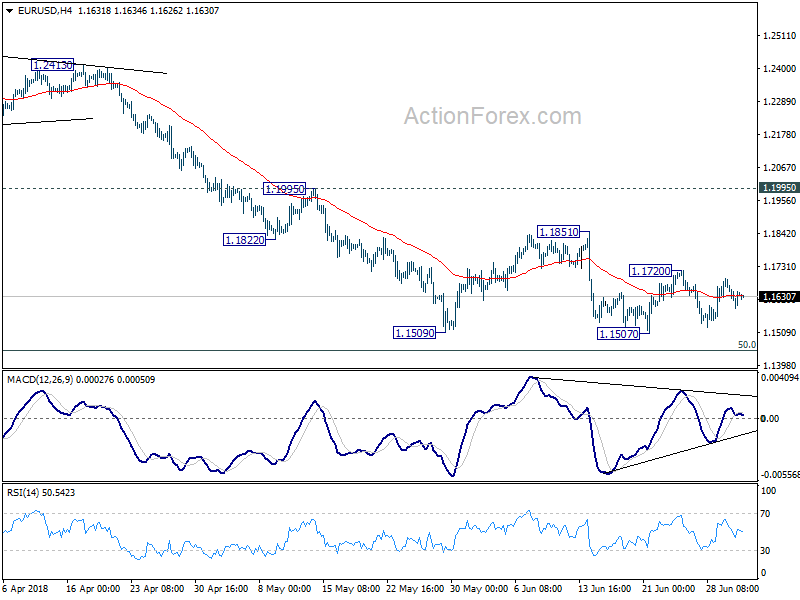

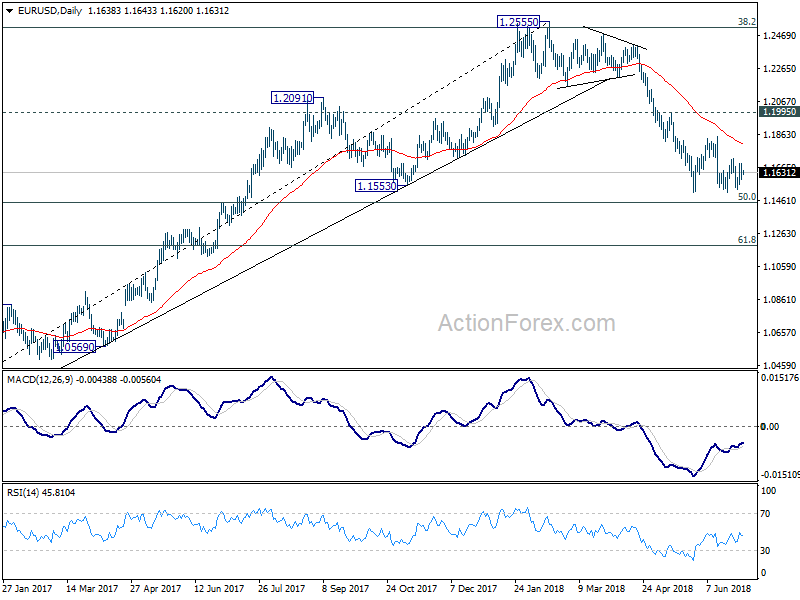

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1589; (P) 1.1641 (R1) 1.1691; More.....

Outlook in EUR/USD remains unchanged as consolidations continue above 1.1507 temporary low. Intraday bias remains neutral for the moment. Stronger recovery cannot be ruled out. But in that case, upside should be limited by 1.1851 resistance to bring fall resumption. Decline from 1.2555 is still in progress. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

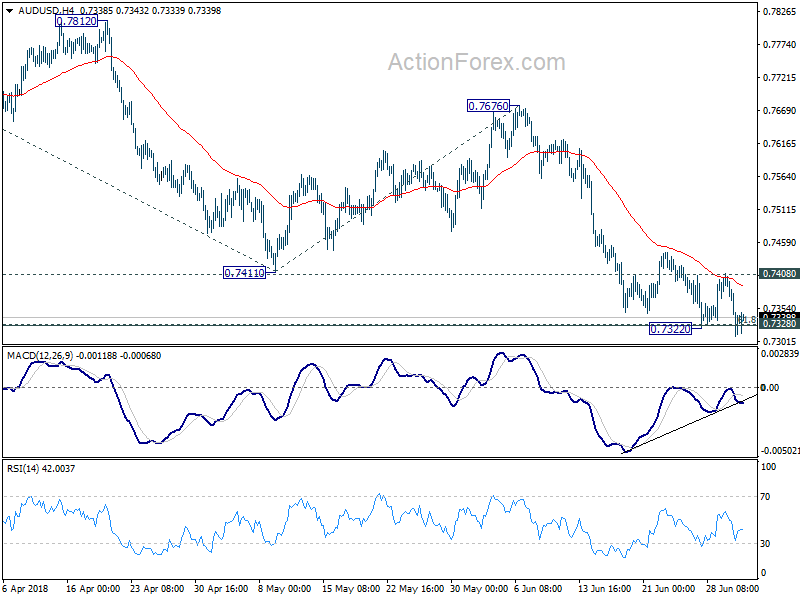

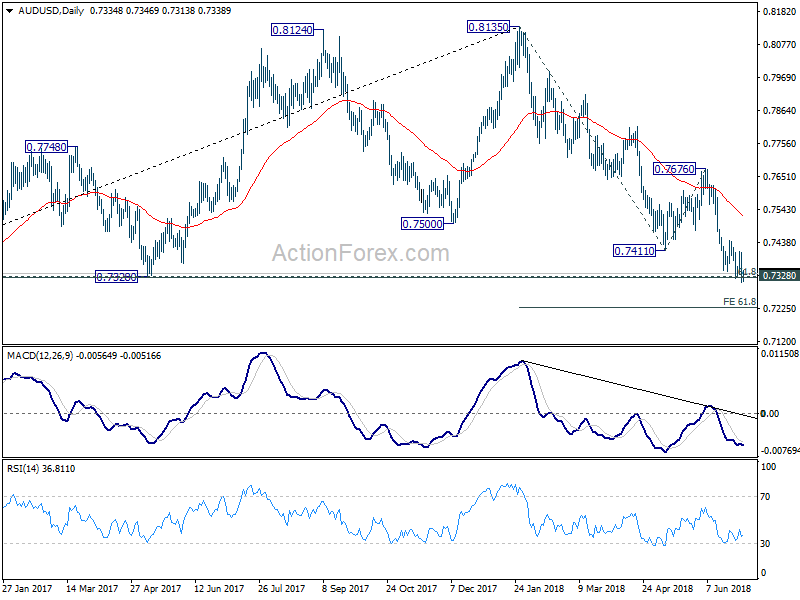

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7297; (P) 0.7353; (R1) 0.7397; More...

AUD/USD's fall resumed after brief consolidation and edged lower to 0.7309. Intraday bias is back on the downside. Sustained break of f 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will target 61.8% projection of 0.8135 to 0.7411 from 0.7676 at 0.7229 next. On the upside, however, break of 0.7408 resistance will indicate short term bottoming and bring stronger rebound back towards 0.7676 resistance.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

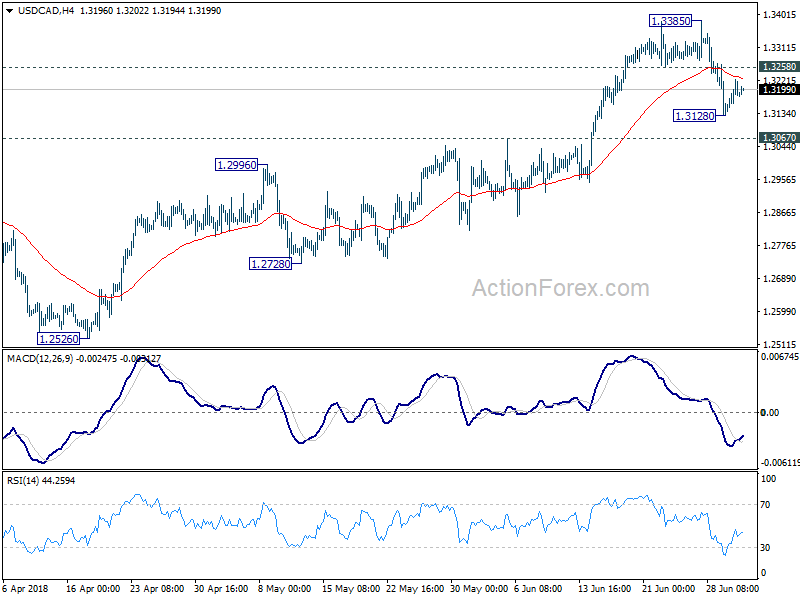

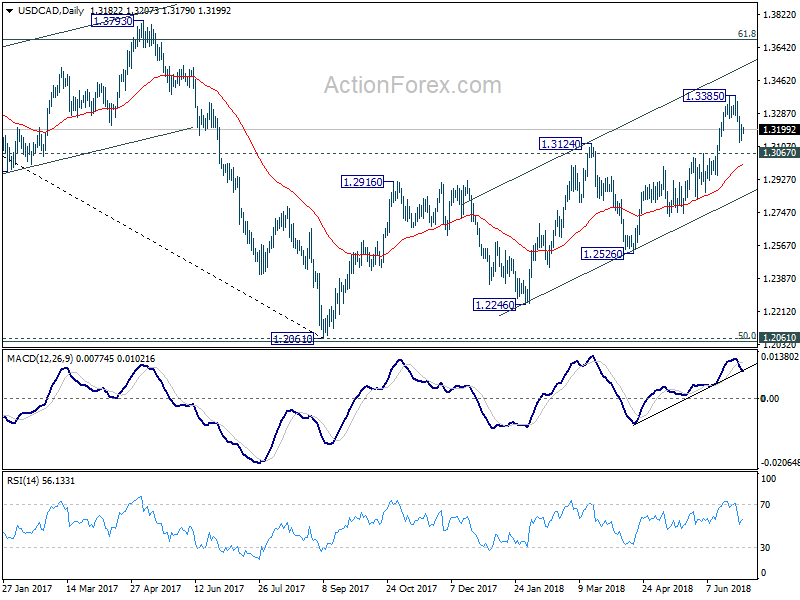

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3141; (P) 1.3185; (R1) 1.3230; More...

A temporary low is formed at 1.3128 in USD/CAD with 4 hour MACD crossed above signal line. Intraday bias is turned neutral first. While fall from 1.3385 could still extend, we'd expect downside to be contained there to bring rebound. On the upside, above 1.3258 minor resistance will bring retest of 1.3385. However, firm break of 1.3067will bring deeper decline to channel support (now at 1.2839).

In the bigger picture, as long as channel support (now at 1.2825) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above.

Yen and Dollar Strong on Asian Market Rout, Aussie Steady after RBA

After initial selloff, the US markets staged an impressive rebound overnight. DOW hit as low as 24077.56 but reversed to close at 24307.18, up 0.15%. S&P 500 gained 0.31% while NASDAQ rose 0.76%. However, investor sentiments turned sour again in Asian session as China leads decline again. At the time of writing, Shanghai SSE composite is trading down -1.27%. Hong Kong HSI is back from holiday and is down -2.73%. Nikkei is down -0.83%. Singapore Strait Times is down -0.49%.

In the currency markets, Yen and Dollar continue to be the strongest one for the week, with Yen slightly stronger for today. New Zealand Dollar remains under broad based pressure. Australia Dollar, while staying the second weakest for the week, recovers as RBA didn't deliver any dovish surprise.

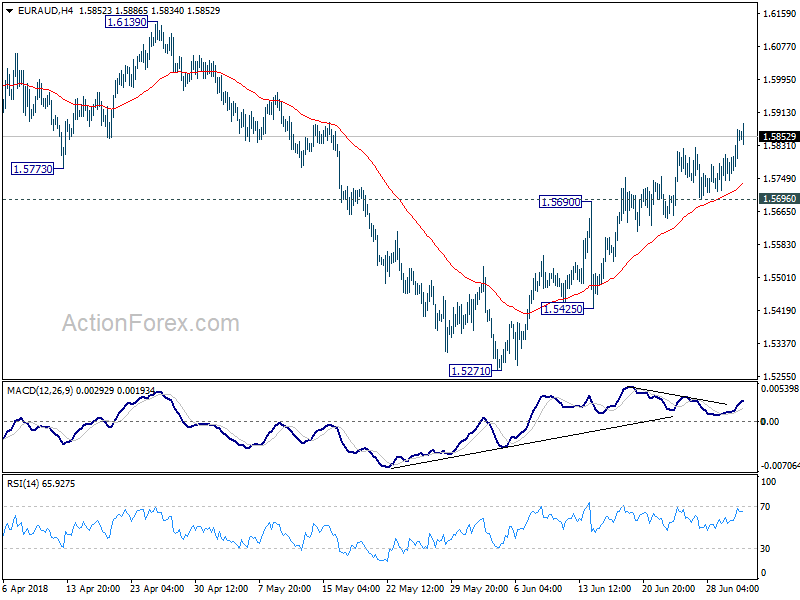

Technically, AUD/USD's break of 0.7328 support overnight suggests down trend resumption. Further fall is now expected to next projection level at 0.7229. EUR/AUD extended recent rally to as high as 1.5886 and its on course for 1.6 handle. USD/JPY is struggle to find momentum after breaching 111 and we might see more consolidations first. EUR/USD and GBP/USD are saying in range above 1.1507 and 1.3048 as consolidations are extending.

RBA kept cash rate at 1.50%, sounds less concerned on exchange rate

RBA left cash range unchanged at 1.50% as widely expected. Overall reaction from the markets is muted as the statement provides little new information.. On the economy it noted that recent data "continue to be consistent" with the central bank's forecast of "a bit above 3%" GDP growth in 2018 and 2019. National income was given a boost by higher commodity prices. But term's of trade are expected to decline over the next few years. Labor market development remains "positive" but wages growth remains "low". Inflation is expected to remain low "for some time too. RBA maintain the view that further process in lower unemployment will lift inflation back to target. But the progress is likely "to be gradual."

A more notable change is that RBA omitted "An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.". It looks like, after the depreciation since January, RBA is less concerned on exchange rate.

Trump holds WTO hostage to request for improvements

While meeting with Dutch Prime Minister Mark Rutte in Washington, US President Donald Trump issued fresh warning to the WTO. When asked is he's preparing to pull out of the WTO, Trump said it has treated the US "very, very badly and I hope they change their ways". He added that the US has a "a big disadvantage with the WTO. And we're not planning anything now, but if they don't treat us properly, we'll be doing something," That came after earlier report Axios, based on unnamed source, that Trump has completed to his officials "I don't know why we're in it. The WTO is designed by the rest of the world to screw the United States."

In an CNBC interview, Tony Fratto, deputy press secretary under President George W. Bush, blasted the idea of leaving WTO. He said, "to say that the United States is a loser in a WTO world is just completely inaccurate. We created the WTO as the dominant economy in the world to serve our interests." While improvements are needed, there are better ways than "to hold it hostage and to threaten to pull out of it." And He added that pulling out of WTO is a "ridiculous idea".

On the other hand, former Trump advisor Dan DiMicco also told CNBC that "If the WTO can't be any more effective than it has been the last 20 years … then the WTO is not helping the world trading system, it's hurting it, and we should be prepared to walk away."

White House confronts Canada for retaliation tariffs

White House spokeswoman Sarah Sanders issued fresh confrontation to Canada as the latter retaliation tariffs on US steel tariffs took effect. Sanders said in a media briefing that "escalating tariffs against the United States does nothing to help Canada. It only hurts American workers." Sanders added that "we've been very nice to Canada for many years, and they've taken advantage of that - particularly advantage of our farmers." And, "the president is working to fix the broken system, and he's going to continue pushing for that."

Canada officially slapped tariffs on more than USD 12B of US goods effective on July 1. A range of products were targeted including steel and aluminum, coffee, pizza, condiments, whiskers etc. Chrystia Freeland, Canada's minister of foreign affairs said that "we will not escalate, and we will not back down."

BoJ said to downgrade inflation forecast in upcoming July meeting

The Nikkei Review reported earlier this week that BoJ will likely lower inflation forecast at the upcoming quarterly Outlook for Economic Activity and Prices. The new projections will be published after July 30-31 meeting.

Back in April, BoJ projected inflation to hit 1.3% in fiscal 2018 and 1.8% for fiscal 2019. In the upcoming projections, BoJ could lower than to 1.0% in fiscal 2018 and 1.5% in fiscal 2019. That will bring the figures in-line with forecasters surveyed by Japan Center for Economic Research, which expected 0.94% inflation in fiscal 2018.

BoJ scrapped its "timeline" of hitting 2% inflation target around fiscal 2019, back in the April statement. But it's been clarified multiple times by BoJ communications that the "timeline" was merely a projection, not a target.

On the data front

Japan monetary base rose 7.4% yoy in June, below expectation of 8.4% yoy. Australia building approvals dropped -3.2% mom in May, below expectation of -1.0%. UK PMI construction, Eurozone retail sales will be featured in European session. Canadian PMI manufacturing and US factory orders will be featured later in the day.

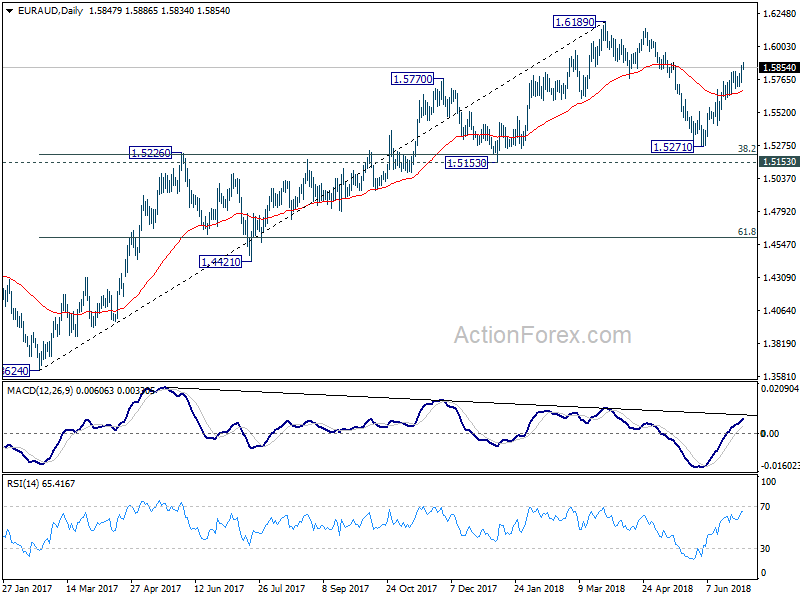

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5780; (P) 1.5826; (R1) 1.5903; More....

EUR/AUD's rally continues today and reaches as high as 1.5886 so far. Intraday bias is now on the upside as rise from 1.5271 should target a test on 1.6139/89 resistance zone. However, as the rebound from 1.5271 is not clearly impulsive yet and momentum isn't too convincing. Break of 1.5695 minor support could be an early sign of near term topping. In such case, focus will be back on 1.5425 support.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is not completed yet. Break of 1.6189 will target 1.6587 key resistance (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Jun | 7.40% | 8.40% | 8.10% | |

| 1:30 | AUD | Building Approvals M/M May | -3.20% | -1% | -5.00% | -5.60% |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:30 | GBP | Construction PMI Jun | 52 | 52.5 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M May | 0.20% | 0.10% | ||

| 13:30 | CAD | RBC Canadian Manufacturing PMI Jun | 56.2 | |||

| 14:00 | USD | Factory Orders May | 0.10% | -0.80% |