Sample Category Title

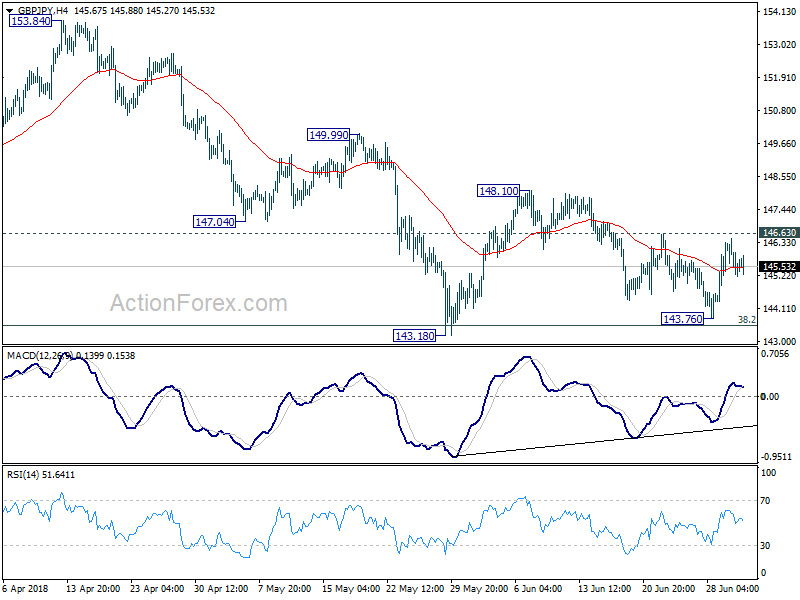

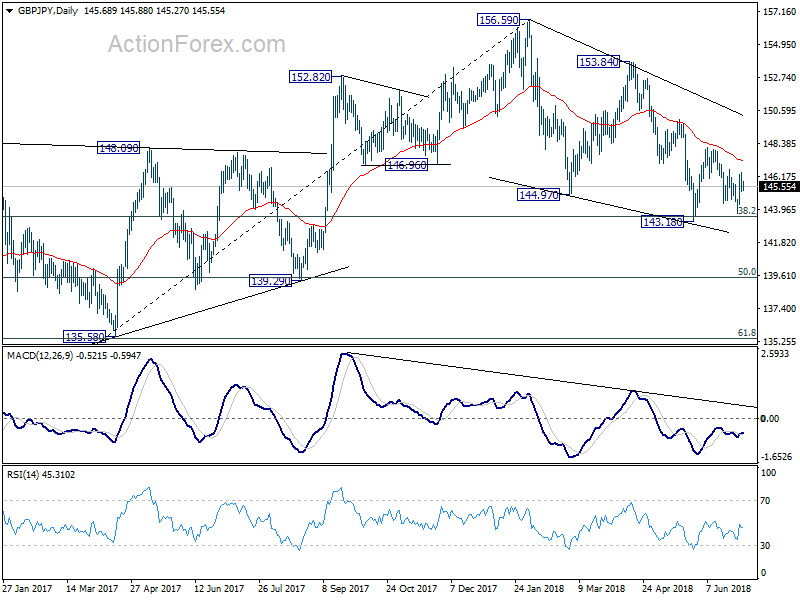

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.11 (P) 145.81; (R1) 146.43; More...

Intraday bias in GBP/JPY stays neutral as range trading continues. On the upside, break of 146.63 will target a test on 148.10 resistance first. Decisive break there will be a strong signal of near term reversal. Further rally would be seen to 149.99 resistance for confirmation. On the downside, break of 148.13 will extend the fall from 156.59 for 139.25/47 cluster support level.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

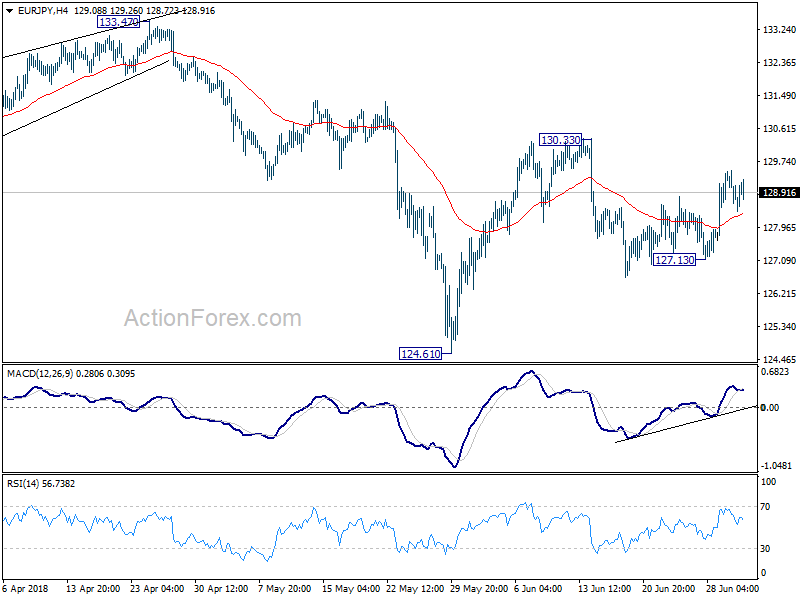

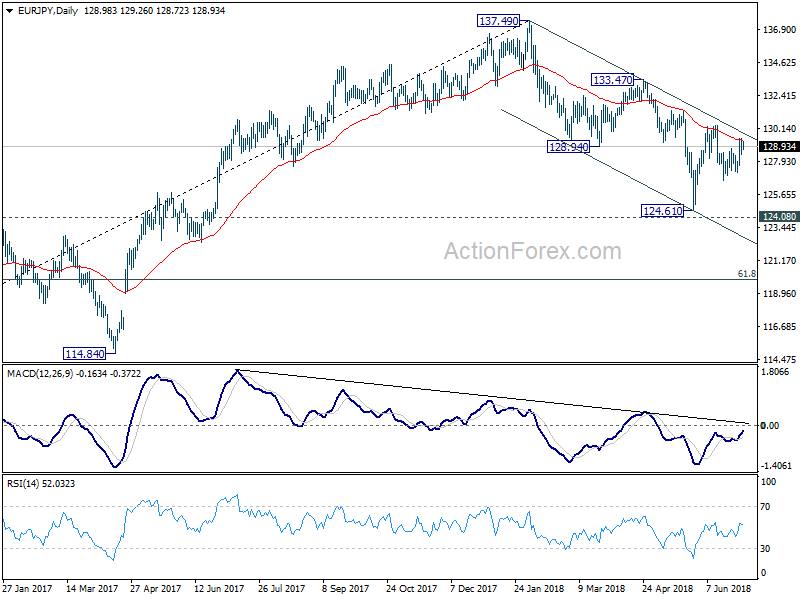

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.47; (P) 128.99; (R1) 129.57; More....

Intraday bias in EUR/JPY stays neutral at this point. On the upside, break of 130.33 will resume the rebound from 124.61. And by then, EUR/JPY should have also taken out near term falling channel decisively. That would be a strong sign of trend reversal. In that case, further rise should be seen to 133.47 resistance for confirmation. On the downside, break of 127.13 will bring retest of 124.61 low instead.

In the bigger picture, for now, EUR/JPY is holding above 124.08 key resistance turned support. Fall from 137.49 could be proven to be a correction. Decisive break of 133.47 resistance will confirm its completion and should extend the rise from 109.03 (2016 low) through 137.49 high. However, firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below.

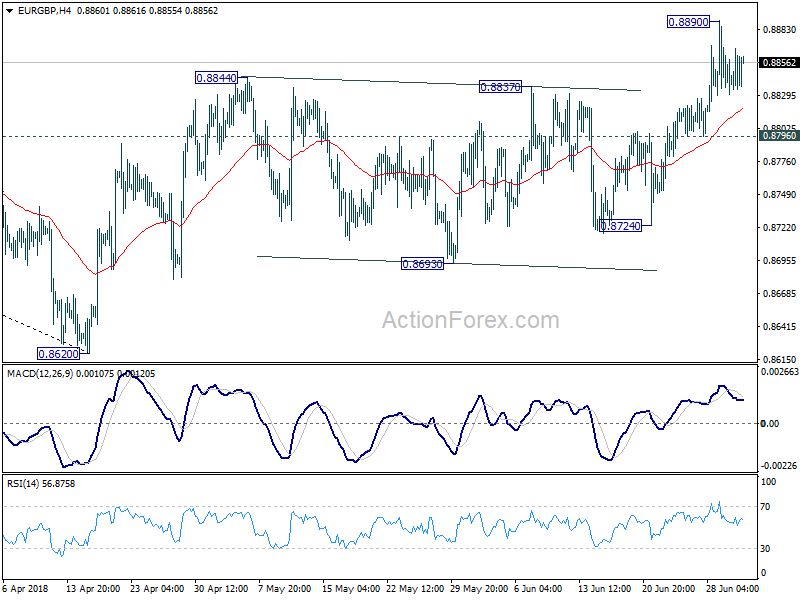

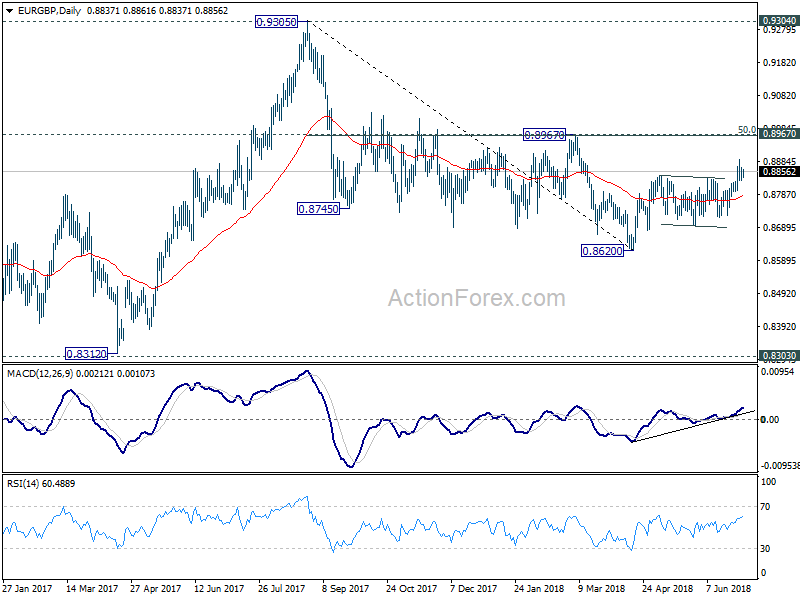

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8833; (P) 0.8852; (R1) 0.8876; More...

EUR/GBP is staying in consolidation below 0.8890 temporary top and intraday bias remains neutral. In case of deeper retreat, downside should by contained by 0.8796 minor support to bring rally resumption. On the upside break of 0.8890 will resume the rebound from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963).

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

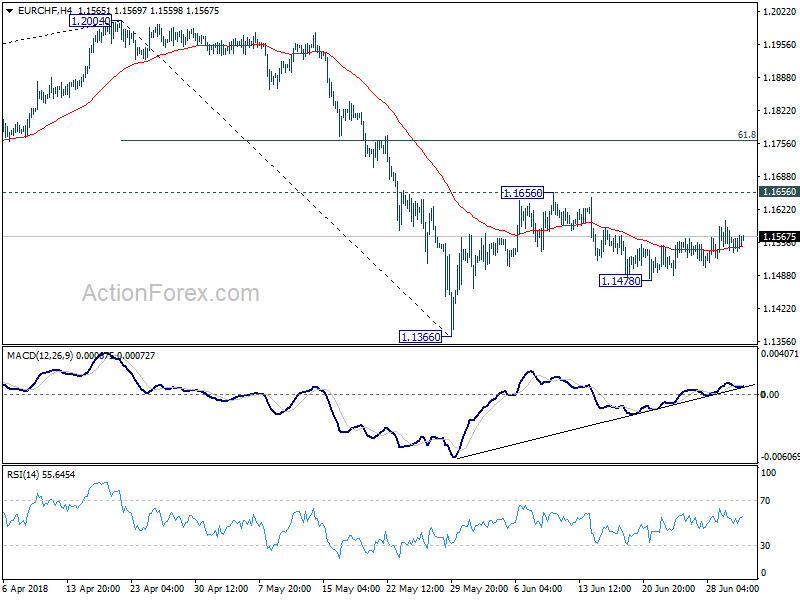

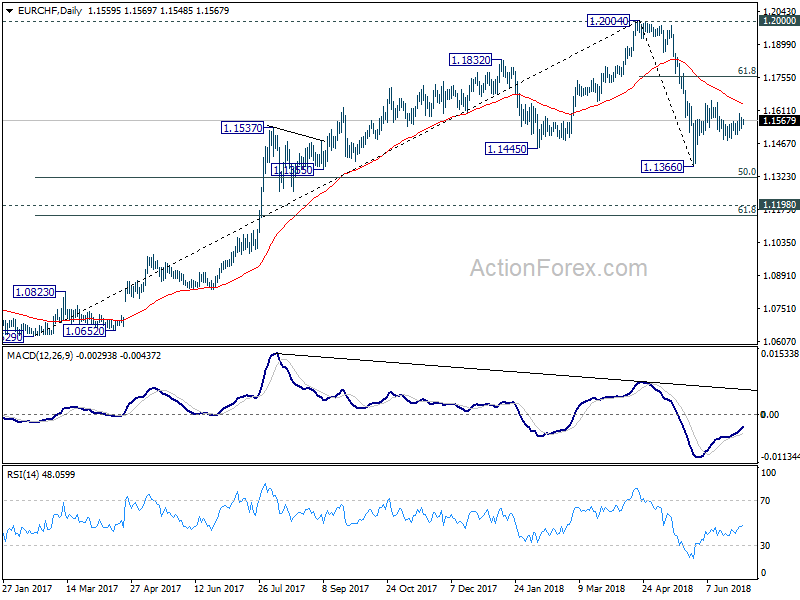

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1537; (P) 1.1561; (R1) 1.1588; More....

EUR/CHF is staying in corrective trading in range of 1.1478/1656. Intraday bias remains neutral first. On the upside, break of 1.1656 will resume the rebound from 1.1366 to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But we would expect strong resistance from there to limit upside. For now, we'd expect at least one more falling leg before the correction from 1.2004 completes. Below 1.1478 will turn bias to the downside for 1.1366 and below.

In the bigger picture, EUR/CHF was solidly rejected by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

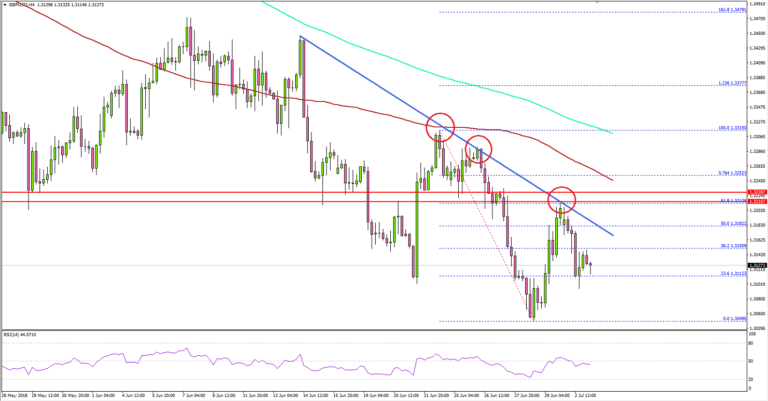

GBP/USD Upsides Remained Capped By 1.3200

Key Highlights

- The British Pound recovery faced a strong selling interest near 1.3200-10 against the US Dollar.

- There is a key bearish trend line formed with resistance at 1.3180 on the 4-hours chart of GBP/USD.

- The UK Manufacturing PMI in June 2018 increased from the last reading of 54.3 to 54.4.

- Today in the US, the Factory Orders report for May 2018 will be released, which is expected to remain flat at 0% (MoM).

GBPUSD Technical Analysis

The British Pound started an upside correction from the 1.3050 swing low against the US Dollar. However, the GBP/USD pair faced a strong selling interest near 1.3200-10, resulting in a fresh decline.

Looking at the 4-hours chart, the pair formed a decent support at 1.3049 low and jumped above the 1.3100 resistance. There was also a break above the 50% Fib retracement level of the last decline from the 1.3315 high to 1.3049 low.

However, the upside move was capped by the 1.3200-10 resistance zone. Moreover, a key bearish trend line with current resistance at 1.3180 also prevented gains. Lastly, the 61.8% Fib retracement level of the last decline from the 1.3315 high to 1.3049 low stopped gains.

The pair started a new downside move and is currently trading well below 1.3200. On the downside, the last low of 1.3050 is a decent support. Below this, the pair may perhaps test the 1.3000 handle.

Recently in the UK, the Manufacturing Purchasing Managers Index (PMI) for June 2018 was released by both the Chartered Institute of Purchasing & Supply and the Markit Economics. The market was looking for a decline from the last reading of 54.4 to 54.0.

However, the result was better as the PMI came in at 54.4, but the last reading was revised to 54.3. Overall, the result was positive, but it failed to help GBP/USD.

The US Dollar is once again gaining traction. Both EUR/USD and GBP/USD are showing signs of more declines, and USD/JPY is likely preparing for more gains above 111.15.

Economic Releases to Watch Today

- Euro Zone Retail Sales for May 2018 (YoY) – Forecast +1.4%, versus +1.7% previous.

- Euro Zone Retail Sales for May 2018 (MoM) – Forecast +0.1%, versus +0.1% previous.

- US Factory Orders May 2018 (MoM) – Forecast 0%, versus -0.8% previous.

BoJ said to downgrade inflation forecast in upcoming July meeting

The Nikkei Review reported earlier this week that BoJ will likely lower inflation forecast at the upcoming quarterly Outlook for Economic Activity and Prices. The new projections will be published after July 30-31 meeting.

Back in April, BoJ projected inflation to hit 1.3% in fiscal 2018 and 1.8% for fiscal 2019. In the upcoming projections, BoJ could lower than to 1.0% in fiscal 2018 and 1.5% in fiscal 2019. That will bring the figures in-line with forecasters surveyed by Japan Center for Economic Research, which expected 0.94% inflation in fiscal 2018.

BoJ scrapped its "timeline" of hitting 2% inflation target around fiscal 2019, back in the April statement. But it's been clarified multiple times by BoJ communications that the "timeline" was merely a projection, not a target.

White House confronts Canada for retaliation tariffs

White House spokeswoman Sarah Sanders issued fresh confrontation to Canada as the latter retaliation tariffs on US steel tariffs took effect. Sanders said in a media briefing that "escalating tariffs against the United States does nothing to help Canada. It only hurts American workers." Sanders added that "we've been very nice to Canada for many years, and they've taken advantage of that - particularly advantage of our farmers." And, "the president is working to fix the broken system, and he's going to continue pushing for that."

Canada officially slapped tariffs on more than USD 12B of US goods effective on July 1. A range of products were targeted including steel and aluminum, coffee, pizza, condiments, whiskers etc. Chrystia Freeland, Canada's minister of foreign affairs said that "we will not escalate, and we will not back down."

Trump holds WTO hostage to request for improvements

While meeting with Dutch Prime Minister Mark Rutte in Washington, US President Donald Trump issued fresh warning to the WTO. When asked is he's preparing to pull out of the WTO, Trump said it has treated the US "very, very badly and I hope they change their ways". He added that the US has a "a big disadvantage with the WTO. And we're not planning anything now, but if they don't treat us properly, we'll be doing something," That came after earlier report Axios, based on unnamed source, that Trump has completed to his officials "I don't know why we're in it. The WTO is designed by the rest of the world to screw the United States."

In an CNBC interview, Tony Fratto, deputy press secretary under President George W. Bush, blasted the idea of leaving WTO. He said, "to say that the United States is a loser in a WTO world is just completely inaccurate. We created the WTO as the dominant economy in the world to serve our interests." While improvements are needed, there are better ways than "to hold it hostage and to threaten to pull out of it." And He added that pulling out of WTO is a "ridiculous idea".

On the other hand, former Trump advisor Dan DiMicco also told CNBC that "If the WTO can't be any more effective than it has been the last 20 years … then the WTO is not helping the world trading system, it's hurting it, and we should be prepared to walk away."

Risk Is In The Air

Risk is in the air

Despite global risk mounting with hurdles abound, US equity markets managed to eek out small wins after spending most of the session struggling in the red. The major indexes struggled to find traction as the ongoing slowdown in global growth data, escalating trade war rhetoric, and a nervy Brexit meeting around the corner continued to weigh on investor sentiment. But it was the impervious FANG technology stocks to the rescue, led by Facebook, Apple and Google parent Alphabet climbing more than 1%.that lifted investors spirits off the mat yet again.

And despite the reluctant rally, the unyielding US economic power plant continues to churn out robust economic data and yet again sets the global high bar. The US economy has been on a relentless run through 2018, and the overnight ISM Manufacturing didn’t fail: the headline number defied gravity, coming in at 60.2 (vs 58.5 forecast)

But with darkening skies rolling in and the perfect storm -cloud of risk accumulation brewing, it’s been a robust start to the week for the US dollar as investors look for refuge ahead of the July 4th US holiday.

Oil market

Oil prices have shaded back to the downside as increased market chatter suggests higher production numbers from Russia and Saudi Arabia as more estimates of June output circulate. But the market remains supported by a production outage in Libya and the overhang from recent US supply data which suggest US supplies are running very tight.

The Libyan power struggle between the Tripoli-based National Oil Corp. that is internationally recognised and controls the export sales and the NOC-East group based in Benghazi that currently has physical control of the infrastructure is particularly disruptor removing 850,000 barrels from the supply chain and all but wipes out the planned increase from the OPEC+ coalition.

Again this disruption merely highlights just how tight this global supply and demand balancing act is.

Gold market

All that glitters positively isn’t Gold as the not so shiny metal is plumbing 2018 lows and moving within striking distance of the critical December lows of 1236.50. Its all about the USD demand rather than any news specific as the markets insatiable demand for USD to ride out yet another building perfect storm has the USD glittering. As such Gold is especially vulnerable in such an environment

Currency market

EUR: German CSU leader says the migrations clash with Merkel resolved, which caused the EURUSD to knee-jerk higher to 1.1648

JPY: Given the market continues to slip up on virtually every other headline, USDJPY does look high but remains stuck between general USD strength and risk-off sentiment.

AUD: China economic engine is slowing down as the Chinese authorities remain committed to financial deleveraging.Should continue to weigh negatively on the AUD

Asian Markets

Not a great start to the second half of year for regional risk assets as the USD continues to grind higher against the local basket of currencies.

CNH: The market is looking beyond trade wars and checking under the hood to see if its a case of adding oil or the mainland economic engine is in need of a rebuild. Beyond the potential credit- crunch mainland authorities have been dealing with, the latest run of economic data and indeed this weekends PMI’s didn’t help matters. With an asset bubble and waning growth momentum staring traders in the face, USDCNH has been in huge demand since yesterday open. But keep in mind, a PBoC advisor said last week 6.70 is a level for watch watchers so this could this level could be a line in the sand which may prompt authorities to take action. Indeed Big Trouble in Big China.

MYR: Very much a locally driven markets in the absence of offshore inflows which have the currency and bond markets trading in very tight ranges. While Oil prices remain supportive, Asia EM sentiment should continue to dictate the price action.

Eco Data 7/3/18

[php_everywhere instance="1"]