Sample Category Title

RBA Meeting: Juggling Risks

The Reserve Bank of Australia (RBA) will announce its rate decision on Tuesday, at 0430 GMT. With the Bank almost certain to make no changes to its policy, price action will be dictated by any changes in the phrasing of the accompanying statement. Recent price action suggests investors may be anticipating a more cautious stance. This implies that the risks surrounding the aussie’s reaction may be asymmetrical, with the expected concerned tone leading to a modest decline, but a more neutral bias potentially triggering a sizeable relief rally.

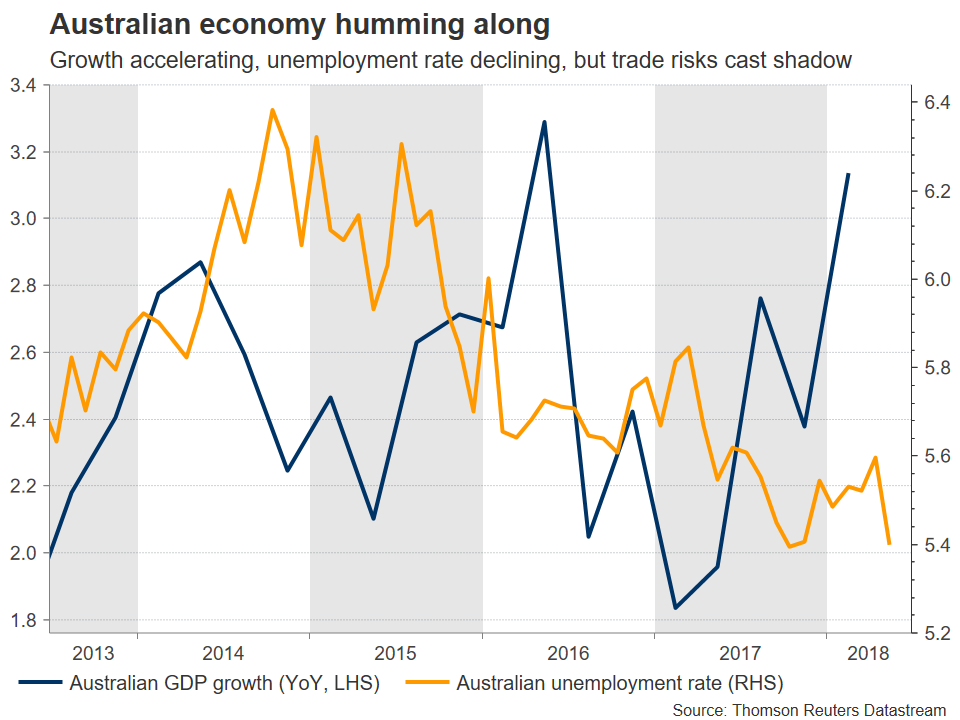

The RBA will have a tough balancing act at its hands when it gathers tomorrow. On the one hand, the domestic Australian economy is humming along nicely. Economic growth was stronger than anticipated in the first quarter, the labor market continued to post slow but steady gains in recent months, and the exchange rate has declined substantially – making Australia’s exports more competitive. Additionally, housing prices have started to correct lower, alleviating fears of financial risks and asset bubbles related to low interest rates.

On the other hand, international developments and most notably trade frictions, present downside risks. The US-China standoff has escalated lately, and should the situation deteriorate any further, Australia will likely be among the first nations to be caught in the crossfire. Not only due to its heavy dependence on commodity exports, which would take a hit in case of a trade war, but also due to its deep economic ties with China. Then, there’s the issue of higher US interest rates. Although the RBA maintains its own policy unchanged, rising borrowing costs in the US are spilling over into slightly higher rates for Australian banks, costs that will reportedly be passed onto consumers soon. This is particularly worrisome, as Australian households are heavily indebted already, and thus may struggle faced with higher rates.

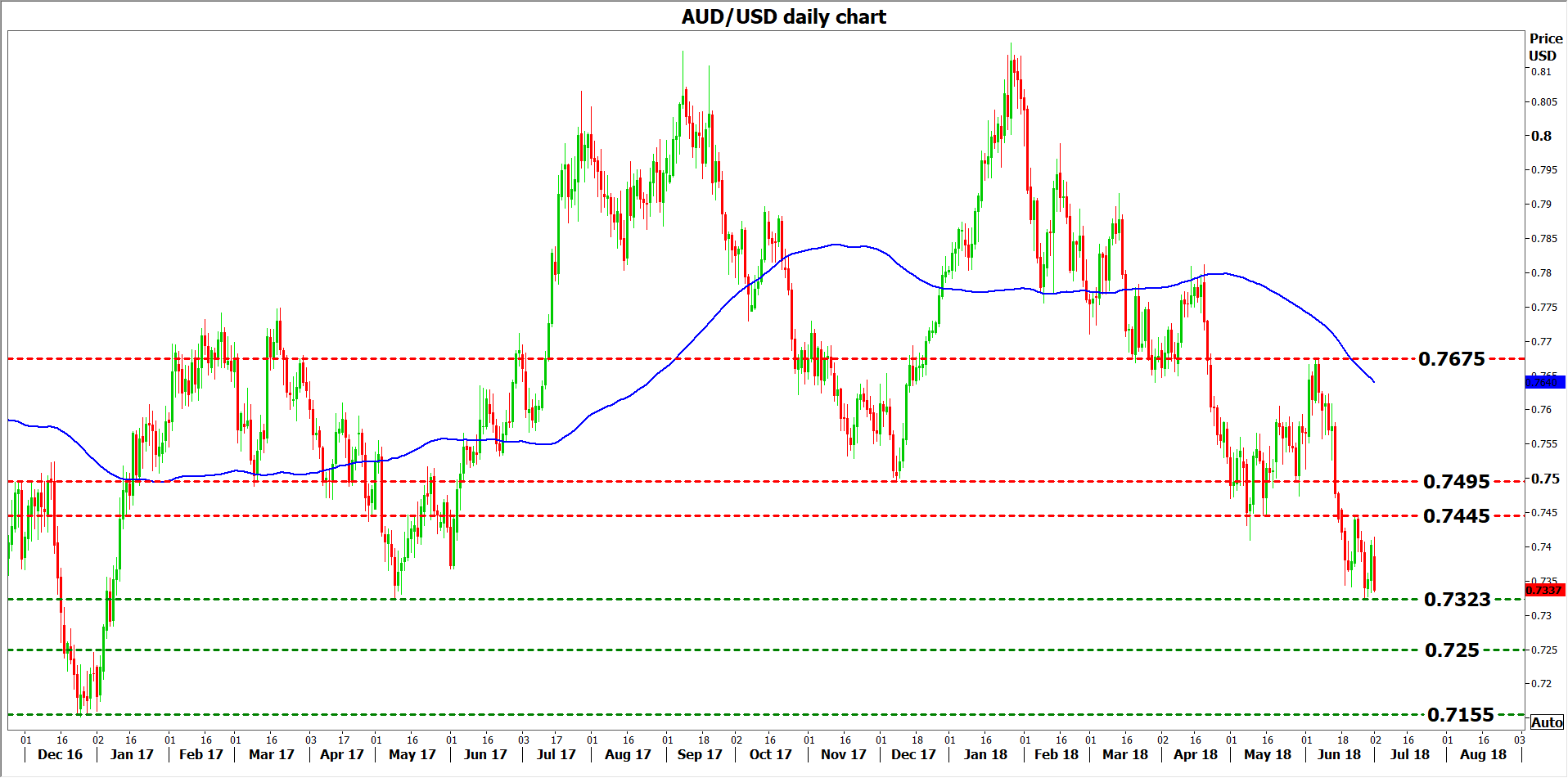

The question is how the Bank will deal with such uncertainties. Will it strike a more concerned tone, as the RBNZ did last week, or will it maintain its neutral “wait and see” attitude? Judging from recent price action, markets seem to be gearing up for the former scenario. Aussie/dollar is trading near an 18-month low awaiting for the rate decision, while any surviving speculation for a near-term RBA rate increase has evaporated. At the time of writing, Australia’s OIS no longer indicate any likelihood for a rate hike this year, but instead suggest a tiny probability for a rate cut.

This has two implications. Firstly, that if the Bank indeed strikes a cautious tone as investors seem to anticipate, then the negative reaction in the aussie may be relatively modest, as that much is already expected. Secondly, anything less than a dovish stance could come as a hawkish surprise for the market, potentially leading to a substantial relief bounce in the Australian currency.

Technically, looking at aussie/dollar, further declines could encounter immediate support near the 18-month low of 0.7323, with a downside break shifting attention to the 0.7250 zone, defined by the inside swing high on 30 December 2016. Even lower, the declines may stall near 0.7155, the bottom of 28 December 2016.

Conversely, if the Bank is less dovish than investors expect, resistance to advances may come around 0.7445, this being the high of June 25. If the bulls pierce through it, eyes would turn to the 0.7495 territory, marked by the inside swing low on May 29. Higher still, the area around 0.7675 may provide resistance.

EURNZD Creates 7-Month High; Bullish Bias in Short-Term

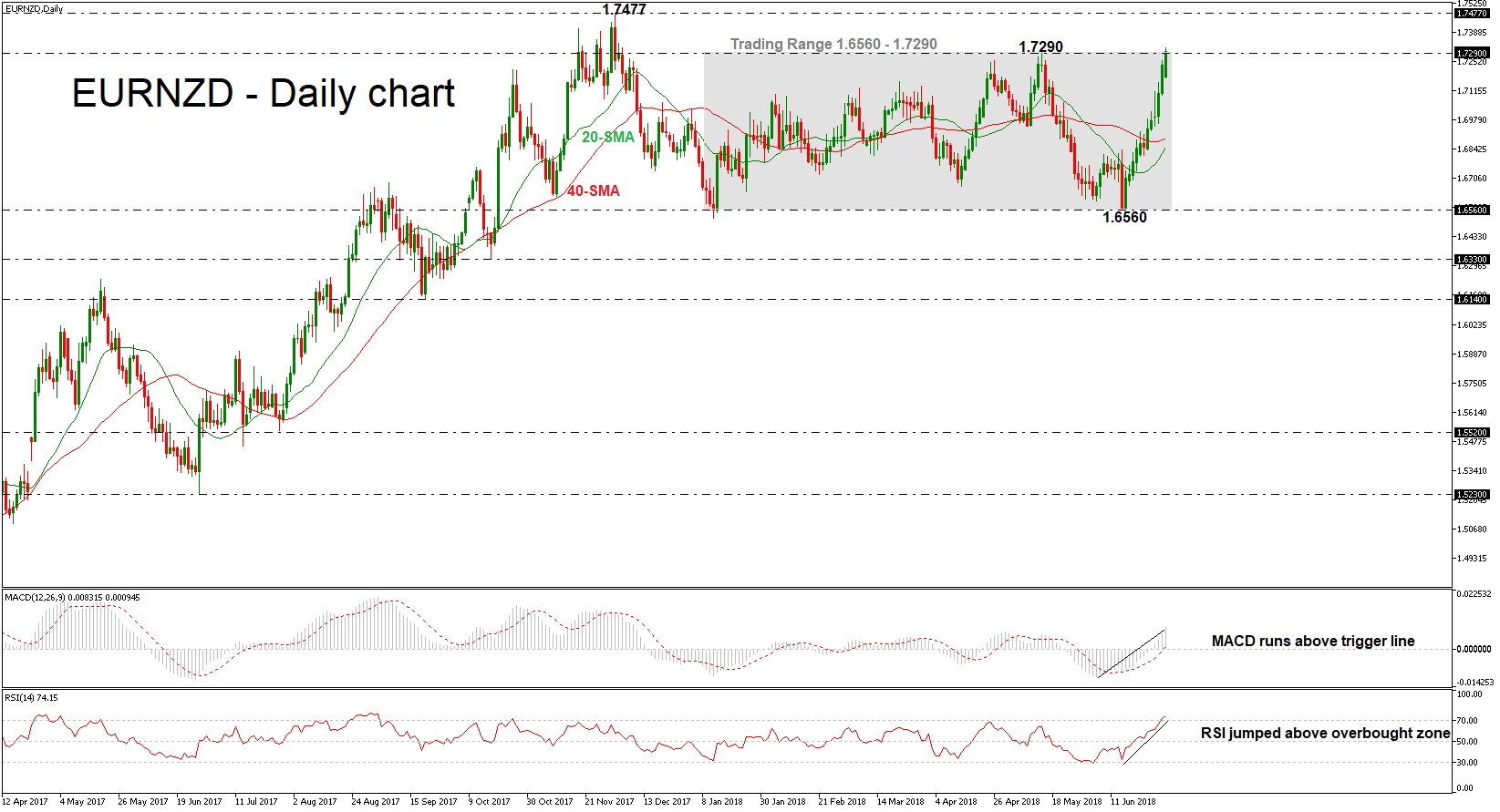

EURNZD has been overperforming over the last two weeks, after the rebound on the 1.6560 support barrier. The price reached a fresh seven-month high of 1.7317, during today’s trading session but currently, it remains below the 1.7290 resistance level.

In the daily timeframe, the MACD oscillator is strengthening its positive momentum as it lies above its red-trigger and the zero lines. Moreover, the RSI indicator entered the overbought zone after the bounce off the bearish threshold of 30.

If price action climbs above 1.7290 (immediate resistance), there is scope to test 1.7477, taken from the peak on December 2017.

On the flip side, if the pair fails to extend gains would change direction and shift the focus to the downside. The next support to watch is the 40 and then the 20 simple moving averages (SMAs) in the daily chart at 1.6894 and 1.6852 respectively.

When looking at the bigger picture the pair lacks a clear as it has been holding within a narrow range of 1.6560 – 1.7290 over the last six months.

Sunset Market Commentary

Markets

Most European equity markets opened with losses of about 1% or even more as the negative sentiment spilled over from Asia. However, despite lingering political uncertainty in Germany, the sell-off already reached an intra-bottom soon after the open. Side-effects on bonds (and on the major FX cross rates) remained modest. US equities futures/markets also trade with substantial losses, but for now the risk off doesn’t intensify. Changes in German yields currently are now more than 1.5 bp. US yields decline between 0 bp (2-y) and 2 bp (10-y). However, this ‘bigger’ decline follows a more substantial rise late in US dealings on Friday. Intra-EMU bond markets also showed a mixed picture with Greece (+3 bp) and Itialy (+6bp) underperforming.

The risk-off correction In Asia also supported the dollar. However, the USD gains were much more modest than was the case in a similar context of late. EUR/USD settled close to, mostly slightly below the mid 1.16 area during the morning session. European eco data were close to expectations with no implications for euro trading. USD buying picked up slightly early in US dealings. The trade-weighted dollar is returning to the 95 area. Until now, there is only modest additional damage for the euro from the political crisis in Germany . However, this might still change as crucial talks between Chancellor Merkel and the CSU are scheduled later this evening. USD/JPY is holding strong despite the equity losses (110.85 area). EUR/USD is changing hands in the low 1.16 area going into the publication of the US manufacturing ISM.

Today, sterling declined modestly against a stronger dollar. At the same time, the UK currency drifted basically sideways against the euro. Sterling and the euro were more or less equally affected by the global risk off sentiment. The UK manufacturing PMI wasn’t too bad (54.4 from 54.3, 54.0 expected). However, the report didn’t change investors’ global assessment on the UK economy with Brexit uncertainty still omnipresent. In this respect, UK PM May is said to try a next attempt to find a united view on Brexit within her Conservative party later this week. For now there is no indication that this attempt will be more successful than previous ones. Despite ongoing political uncertainty in Europe, sterling failed to make again further progress against the euro. EUR/GBP hovers in the 0.8858 area. Cable returned to the 1.31 area, reversing part of Friday’s rebound.

News Headlines

Final talks between Seehofer and Merkel concerning the EU migration deal are scheduled at 5 p.m. today. Without a compromise, the party bloc risks a breakup. That would plunge Germany in a political crisis as a CSU-CDU split up could leave Merkel without a parliamentary majority.

The European Union took a first step in a possible lawsuit against Poland’s ruling populist Law and Justice Party. Nearly 3 years ago, the party started revamping the country’s “inefficient and corrupt” Supreme Court by putting it under its control. In a worst case scenario, Poland gets stripped of its EU voting rights.

Friday is said to be yet another crucial day for Brexit. British PM May will then convene her cabinet, present a new post-Brexit customs plan and hold talks consequently, intended to agree on a final Brexit strategy.

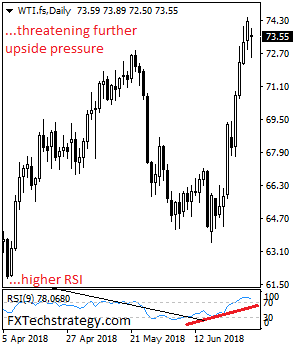

CRUDE OIL: Looks To Resume Broader Uptrend

CRUDE OIL: The commodity looks to recover further higher. On the downside, support resides at the 73.00 level where a break will expose the 72.50 level. A cut through here will set the stage for a run at the 72.00 level. Further down, support resides at the 71.50 level. On the upside, resistance resides at the 74.00 level. Further out, resistance comes in at the 74.50 level. A break above here will aim at the 75.00 level and then the 75.50 level followed by the 76.00 level. All in all, CRUDE OIL remains biased to the upside

US ISM manufacturing rose to 60.2 despite trade war threat

US ISM manufacturing index rose to 60.2 in June, up from 58.7 and beat expectation of 57.9. Prices paid component dropped to 76.8, down from 79.5 and missed expectation of 78.2. Employment component dropped to 56.0, down from 56.3.

Some quotes from the respondents:

- "U.S. tariff policy and lack of predictability, along with [the] threat of trade wars, [is a] causing general business instability and [is] drag on growth for investments." (Electrical Equipment, Appliances & Components)

- "We export to more than 100 countries. We are preparing to shift some customer responsibilities among manufacturing plants and business units due to trade issues (for example, we'll shift production for China market from the U.S. to our Canadian plant to avoid higher tariffs). Within our company, there is a sense of uncertainty due to potential trade wars." (Food, Beverage & Tobacco Products)

- "The Section 232 steel tariffs are now impacting domestic steel prices and capacity. Base steel prices have already increased 20 percent since March." (Fabricated Metal Products)

- "The economy and product demand still continue to be strong. Having trouble finding people [to fill] blue collar positions. Lead times for parts and materials are moving out, and we are seeing commodity cost pressures increases with the threat of tariffs. Additionally, suppliers are asking for more price increases." (Machinery)

- "The uncertainty of U.S. tariffs and the Canada/Mexico/E.U. retaliatory tariffs continues to cloud strategic planning efforts. Contingency planning (for tariffs) is consuming large amounts of manpower that could be used for more productive projects. The tariffs are improving margins in our raw material businesses; however, our businesses which are further up the supply chain are seeing significant inflation." (Miscellaneous Manufacturing)

- "The steel tariffs continue to drive uncertainty. Projects and services using steel have limited days that prices are good for. Trucking is tight, requiring advanced planning and increasing costs." (Paper Products)

US Chamber of Commerce launches “Trade Works. Tariffs Don’t” campaign

Follow up on an earlier post, the US Chamber of Commerce launches a campaign today titled "Trade Works. Tariffs Don't" . It warns that "the administration's new tariffs threaten to spark a global trade war."

Such tariffs prompted retaliations with dollars in billions of dollars in tariffs on American-made products. And it criticized that tariffs by the US are " nothing more than a tax increase on American consumers and businesses–including manufacturers, farmers, and technology companies". Retaliation by other countries will "make American-made goods more expensive, resulting in lost sales and ultimately lost jobs here at home."

It emphasized that this is the wrong approach, and it threatens to derail our nation's recent economic resurgence.

This is the link to an interactive map that shows the impacts state by state.

The chamber also urged Americans to "Send a Message to Congress" to voice out objections against the tariffs.

EU comments on US auto tariffs investigations full statement

Earlier today, Politico reported EU's comments on US section 232 cars investigation submitted to US Department of Commerce last Friday. Below is the full statement from European Commission. Also, EU requested to participate in public hearing on July 19/20.

EU comments on US section 232 Cars investigation

The European Union has on Friday 29 June submitted written comments to the US Department of Commerce in the framework of the on-going Section 232 National Security Investigation of imports of automobiles, including cars, SUVs, vans, light trucks and automotive parts.

The EU has also requested to participate in the public hearing to be held by the Department of Commerce scheduled for 19 and 20 July.

The EU takes the view, as was the case of the section 232 steel and aluminium tariffs, that this current investigation lacks legitimacy, factual basis and violates international trade rules. The EU reiterates its firm opposition to the proliferation of measures taken on supposed national security grounds for the purposes of economic protection. This development harms trade, growth and jobs in the US and abroad, weakens the bonds with friends and allies, and shifts the attention away from the shared strategic challenges that genuinely threaten the market-based Western economic model.

The EU written comments relate to various areas on which input was requested by the US Department of Commerce to conduct its current investigation. The EU submits that:

1. Imports of European automobiles in the US are stable, in line with US production and responding to market signals. Automobile imports from the EU do not threaten or impair the health of the US industry and economy. The EU and US industry specialise in largely different market segments and over the last 5 years imports from the EU have been stable and correlated to US general GDP growth.

2. There is no economic threat to the US automobile industry which is healthy, having steadily expanded domestic production in the last 10 years. Imposing restrictive measures would undermine the current positive trends of the US automobile and automotive parts sector and negatively impact US GDP by up to 13-14 billion USD.

3. EU car companies contribute significantly to US welfare and employment. They are well integrated in the US value chain and export about 60 % of automobiles to third countries including the EU, contributing to improving the US trade balance. They provide 120,000 direct upstream jobs in manufacturing plants and 420,000 jobs with dealers. Trade restrictions are likely to lead to higher input costs for US based producers, thus in effect a tax on the American people.

4. EU car companies foster innovation through research and develop the local workforce. Rather than posing a threat to national security, they are a driver for securing long-term economic stability and competitiveness. Almost a fifth of research and development expenditures in the US is derived from foreign-owned subsidiaries. The EU automotive industry also actively contributes to enhancing the skillsets of the US workforce.

5. The impact on the US economy will be aggravated significantly by the likely countermeasures of US Trading partners, as evidenced by the reaction to the US section 232 tariffs on steel and aluminium. On the basis of the current section 232 investigation into automobile and automotive parts, US trade restrictive measures could result in a very significant volume of US exports affected, estimated at USD 294 billion (or around 19 % of US total exports in 2017).

6. Trade restrictive measures would be contrary to international trade rules. There are no exceptions under the General Agreement on Tariff and Trade (GATT) that justify import restrictions by a developed country to protect a domestic industry against foreign competition, unless in the form of permitted trade remedy measures. Although the General Agreement on Tariff and Trade (GATT) provides for security exceptions, the scope of these exceptions has been circumscribed carefully for specific situations and conditions, which are absent in this case.

7. There is no national security threat from imports of automobile and automotive parts. Without prejudice, we underline that the Department of Commerce's analysis of national security must be narrowly tailored to focus on direct threats to national security, in particular defense applications. US needs for vehicles or vehicle parts for defence or military purposes, mainly Light Tactical Vehicles, appear to be covered by US-based specialised suppliers. These operate in a niche market that is independent and unrelated to the US automobile industry. As only products from US based manufacturers are used by the US military, any trade restrictions imposed on the passenger car, light trucks and car parts market cannot be justified on national security grounds.

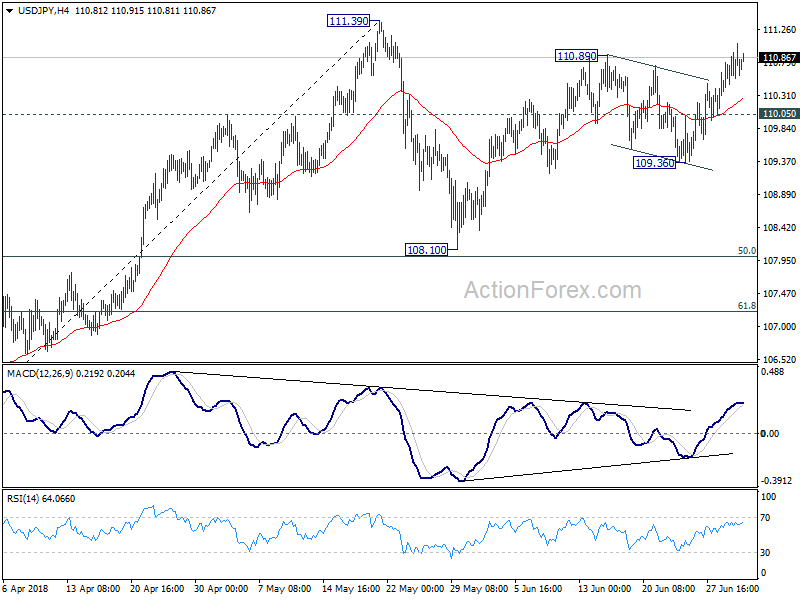

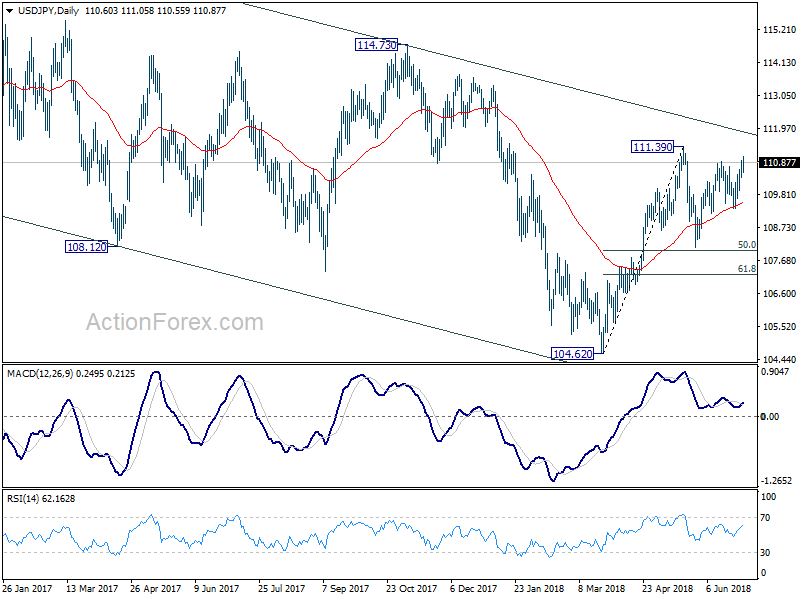

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.39; (P) 110.67; (R1) 110.96; More...

Intraday bias in USD/JPY stays mildly on the upside. Current rebound from 108.10 should target a test on 111.39 high. Break there will also resume the rise from 104.62 and target 114.73 key resistance. However, below 110.05 will turn bias to the downside for 109.36 to extend the corrective pattern from 111.39.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

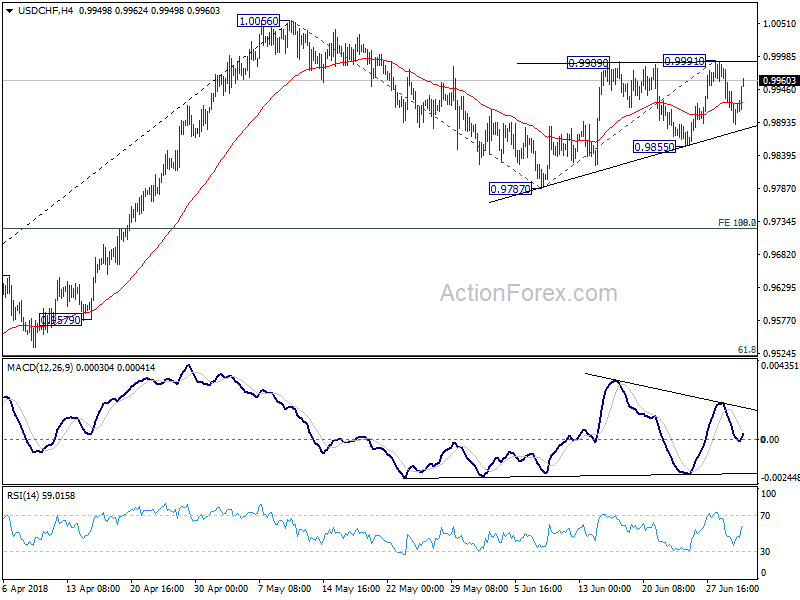

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9869; (P) 0.9928; (R1) 0.9963; More...

Intraday bias in USD/CHF remains neutral as it's staying in range of 0.9855/9991. On the downside, below 0.9855 will resume the corrective decline from 1.0056, likely through 0.9787 support. But downside should be contained by 0.9722/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9991 at 0.9722) to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

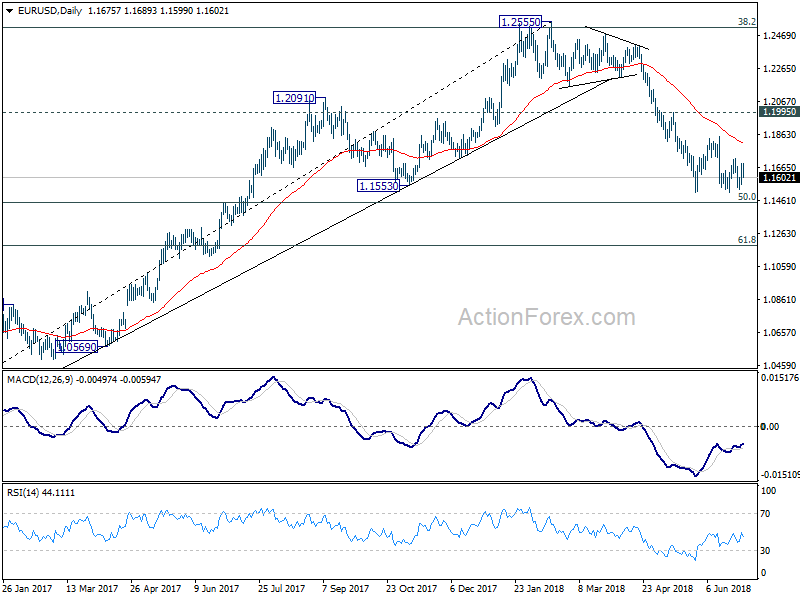

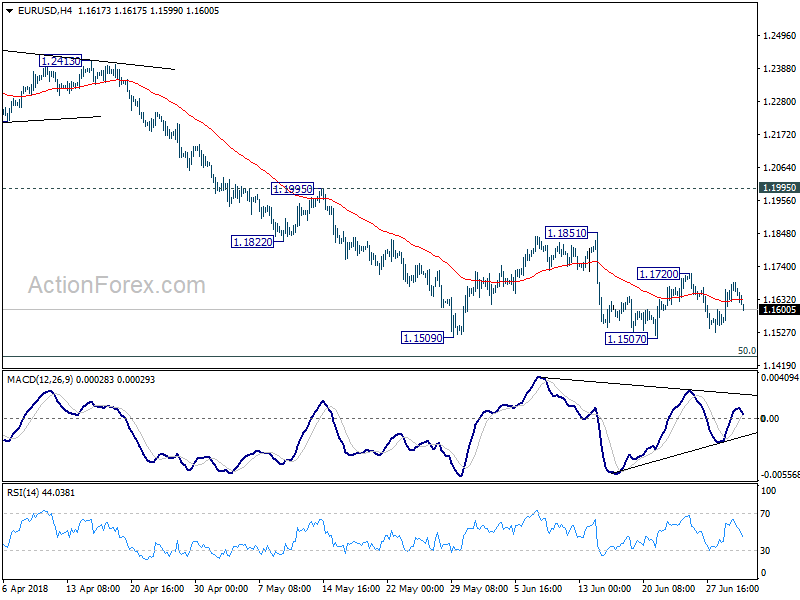

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1598; (P) 1.1645 (R1) 1.1730; More.....

Intraday bias in EUR/USD remains neutral for the moment as it's staying in established range above 1.1507 temporary low. Another recovery cannot be ruled out. But upside should be limited by 1.1851 resistance to bring fall resumption. Decline from 1.2555 is still in progress. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.