Sample Category Title

Dollar Stays Strong as Sentiment Turns Sour Again on Trump’s Trade Spats

Risk aversions dominate the markets today starting from China, spreading to Asia and Europe. Escalation of trade tensions is the main driving force as the Section 301 tariffs and China's retaliation are set to come to effect this week on July 6. After his threat to impose auto tariffs, Trump stepped up with his confrontation to the European Union, as he called EU "as bad as China, just smaller." Such over-the-top comments are clearly unwelcome by the markets.

China's Shanghai composite resumed recent free fall and closed down -2.52%, dragged Nikkei down -2.21%. Major European indices opened in red. At the time of writing, FTSE is down -0.77%, DAX down -0.50%, CAC down -0.81%. DOW future points to lower open too.

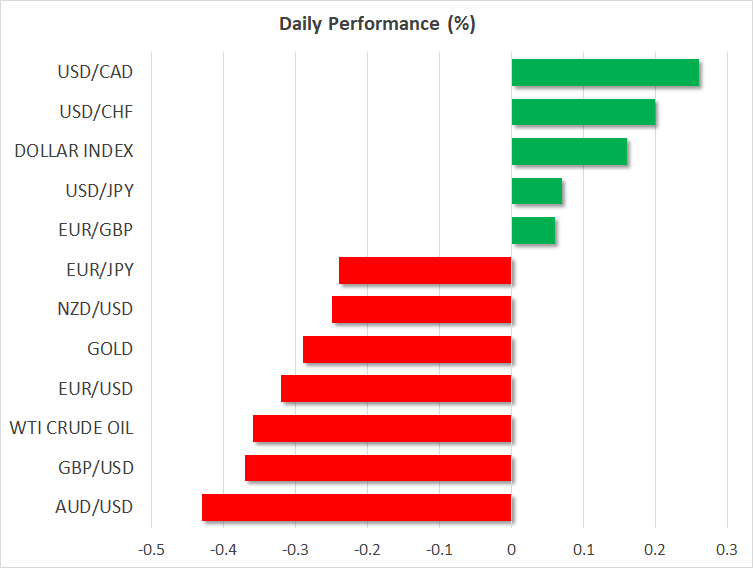

In the currency markets, Dollar continues to ride on trade war fear and is trading as the strongest one for today so far. Yen is back in form on risk aversion, trading as the second strongest. Australian Dollar and New Zealand Dollar are taking turns to be the weakest. Canadian Dollar escape as selloff with a little help from resilient oil price.

Technically, EUR/AUD's break of 1.5823 minor resistance indicates resumption of recent rebound from 1.5271. AUD/USD's with today's decline, is having its sight on 0.7328 key cluster support again.

US Chamber of Commerce to campaign against Trump's trade tariffs policies

Trump's provocative approach in handling trade international relations is starting to back fire in his own yard. , US ambassador to Estonia James D. Melville Jr., who served under six presidents and 11 secretaries of state, announced his early retirement because he cannot tolerate Trump any more.

He said in his private Facebook post that "For the President to say the EU was 'set up to take advantage of the United States, to attack our piggy bank,' or that 'NATO is as bad as NAFTA' is not only factually wrong, but proves to me that it's time to go." And it should be noted that came less that two weeks ahead of NATO summit in Brussels on July 11, 12.

Besides, Reuters reported that the US Chamber of Commerce is launching a campaign today to attack Trump's protectionist trade policy. It's believed that state-by-state analysis would be used for the campaign and it will warn that Americans that Trump is risking a global trade war that will eventually hit their pockets.

Chamber President Tom Donohue was quoted saying that "the administration is threatening to undermine the economic progress it worked so hard to achieve." And he added that "we should seek free and fair trade, but this is just not the way to do it."

Being the largest business group in the US with 3 million members, the Chamber also have long history of being friendly with Republicans. Their stance carries some political significance.

UK PMI manufacturing rose to 54.4, revival remains in some doubt

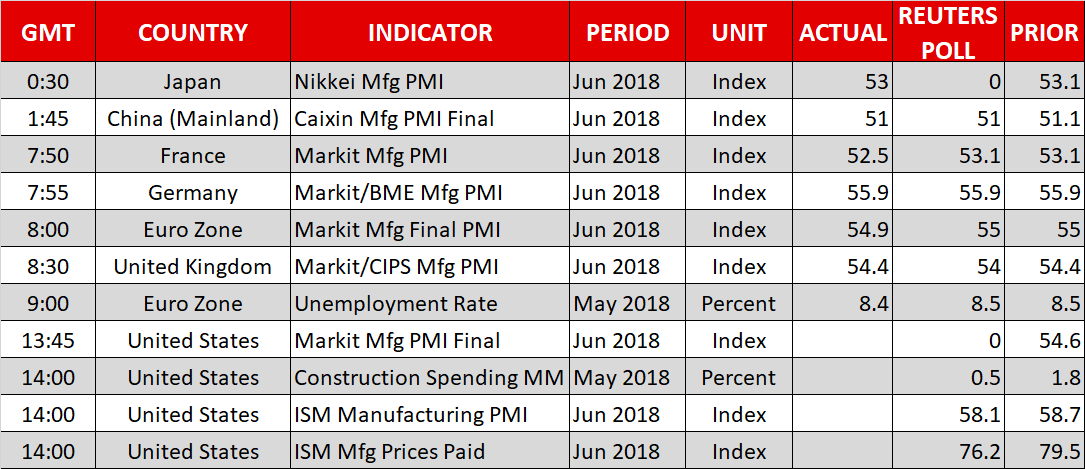

UK PMI manufacturing rose 0.1 to 54.4 in June, above expectation of 53.5. Markit noted that output growth slowed from May's give month high. Meanwhile, input cost inflation picked up, leading to increased selling prices. Rob Dobson, Director at IHS Markit, said in the released that the sector ended Q2 on a "subdued footing". Manufacturing were "increasingly reliant on backlogs of work and inventory building" due to slow downside new order grow. And such position "cannot be sustained far beyond the immediate horizon". He added that "ongoing supply-chain disruptions, including raw material shortages, and signs of a renewed upswing in input price inflation may also jeopardise stronger manufacturing growth". And "the UK economy will need to look to other sectors if GDP growth is to match expectations in the latter half of the year"

Eurozone PMI manufacturing hit 18-month low, mounting worries on tariffs and trade wars

Eurozone PMI manufacturing was finalized at 54.9, revised down from 55.0. That's also an 18-month low. Markit noted that growth of output and new orders slowed further as upturn in new export business remains subdued. Also, supply chain pressure and rising oil prices took input cost inflation to four-month high. Among the countries, the Netherlands stayed strong at 60.1 even hitting 6-month low. Ireland hit 5-month high at 56.6. Italy rebounded and hit 2-month high at 53.3. France deteriorated to 16-month low at 52.5.

Chris Williamson, Chief Business Economist at IHS Markit said in the release that "the biggest concern is the extent to which export order book growth has cooled since the start of the year, and could soon go into decline. "The survey reveals mounting worries from companies relating to the impact of tariffs and trade wars, suggesting firms are bracing themselves for the potential for further export losses." ""At the same time there are signs that political uncertainty is also dampening business spirits, most evidently in Italy, which was consequently the second-worst performer of all countries surveyed in June ahead of France."

Other PMIs from Eurozone saw Germany PMI manufacturing was finalized at 55.9 in June, unrevised. France PMI manufacturing was revised lower to 52.3, down from 53.1, in June. Italy manufacturing PMI rose to 53.3 in June, up from 52.7 and beat expectation of 52.6.

Also from Eurozone, Unemployment rate was unchanged at 8.4% in May. From Swiss, SVME PMI dropped to 61.1 in June, retail sales dropped -0.1% yoy in May.

Japan Tankan: Large manufacturing sentiments deteriorated for another quarter

The BoJ's quarterly Tankan survey showed notable worsening in manufacturer's sentiments in Q2. The Larger Manufacturing Index dropped to 21, down from 24 and missed expectation of 23. It's also a second straight quarterly decline from Q4's 26, the first time since 2012. Large Manufacturer outlook rose to 21, up from 20. Large Non-Manufacturing index rose to 24, up from 23, beat expectation of 23. Large Non-Manufacturing Outlook rose to 21, up from 20 but missed expectation of 22. Large all industry capex rose 13.6%, beat expectation of 0.2%.

Japan PMI manufacturing revised down to 53.0

Japan PMI manufacturing was finalized at 53.0 in June, revised down from 53.1. Joe Hayes, Economist at IHS Markit noted that "Japan manufacturing PMI data continue to signal that the sector's current expansion phase still has legs. Output growth edged up in June, supported by further inflows of new work and an accelerated rate of employment growth." However, "concerns do remain however, as new order growth eased to a ten-month low and export sales decreased for the first time since August 2016. Moreover, with input price inflation jumping to a three-and-a-half year high, manufacturers may be forced to absorb higher cost burdens in order to remain competitive, particularly if the yen faces further safe haven demand."

China Caxin PMI manufacturing dropped to 51.0, deteriorating exports and weak employment

China Caxin PMI manufacturing dropped 0.1 to 51.0 in June, met expectations. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said in the release that "index for new export orders fell to a low for the year so far and remained in contraction territory, pointing to a grim export situation amid escalating trade disputes between China and the U.S., which led to weak demand across the manufacturing sector." Also, "employment index dropped for the second consecutive month, indicating worsening layoffs." "Overall, the manufacturing PMI survey pointed to strengthening price pressures in June. Deteriorating exports and weak employment, along with companies' destocking and poor capital turnover, put pressure on the manufacturing sector."

Released over the weekend, the official China PMI manufacturing dropped -0.4 to 51.5 in June. Official PMI non-manufacturing rose 0.1 to 55.0.

Would RBA turn dovish on global trade risks?

RBA rate decision and statement are something that's worth a watch in the upcoming Asian session. There is no doubt that RBA will keep interest rate unchanged at 1.50%. The may problem is that RBA's communications have been rather confusing recently. In the May meeting minutes released on June 19, RBA omitted the language saying that it is "more likely that the next move in the cash rate would be up, rather than down". But in between, the meeting and the minutes, Governor Lowe said that it "is likely that the next move in interest rates will be up, not down". So, what is RBA trying to tell? Lowe ought to make use of this week's statement to clear the picture.

Also, last week's more dovish than expected RBNZ statement prompted some speculations that RBA could follow suit. It should be noted that in the background, there is tremendously high risks of escalation in trade tension between the US and China. Based on its close ties with both countries, Australia will inevitably be affected.

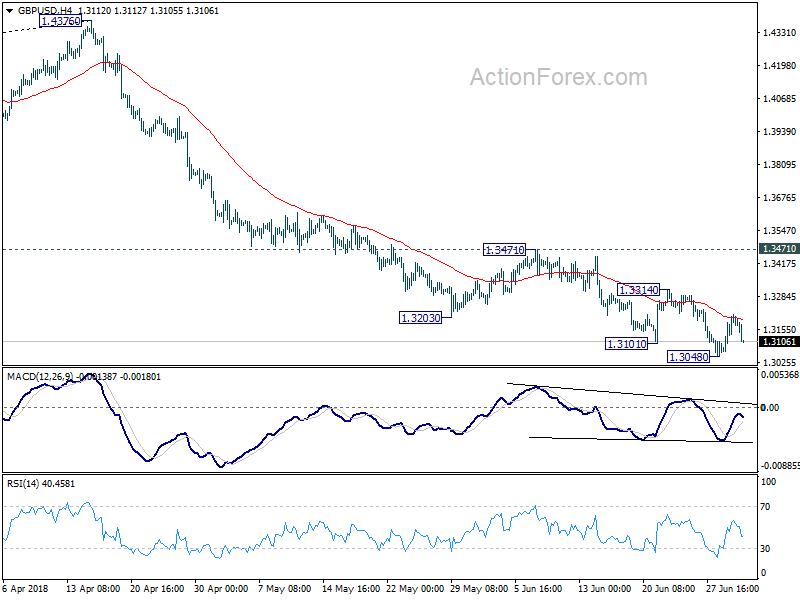

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3111; (P) 1.3163; (R1) 1.3258; More...

GBP/USD is rejected by 4 hour 55 EMA and drops notably today. But it's staying above 1.3048 temporary low and intraday bias remains neutral. More consolidations could be seen but in case of another rise, upside should be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

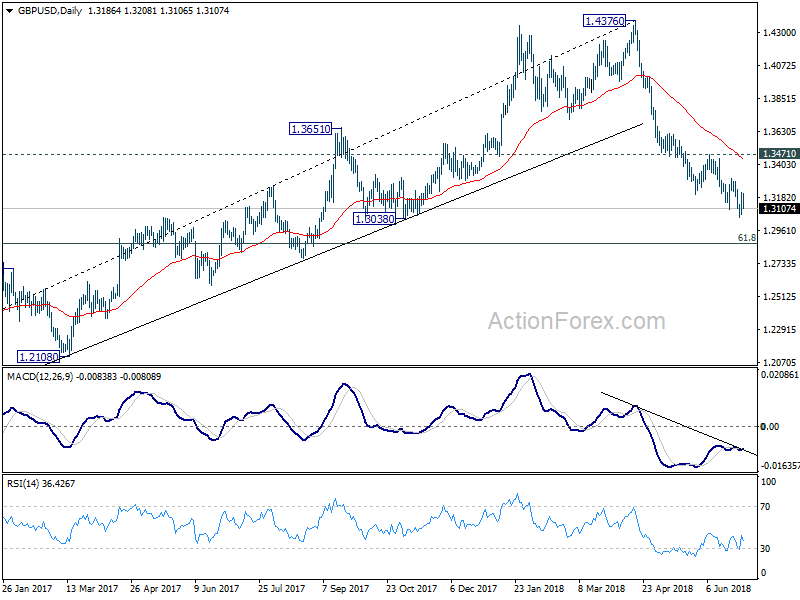

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4179). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Jun | 57.4 | 57.5 | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 21 | 23 | 24 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q2 | 21 | 21 | 20 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Index Q2 | 24 | 23 | 23 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Outlook Q2 | 21 | 22 | 20 | |

| 23:50 | JPY | Tankan Small Manufacturing Index Q2 | 14 | 14 | 15 | |

| 23:50 | JPY | Tankan Small Manufacturing Outlook Q2 | 12 | 11 | 12 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Index Q2 | 8 | 9 | 10 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Outlook Q2 | 5 | 7 | 5 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 13.60% | 9.20% | 2.30% | |

| 0:30 | JPY | PMI Manufacturing Jun F | 53 | 53.1 | 53.1 | |

| 1:00 | AUD | TD Securities Inflation M/M Jun | 0.00% | 0.00% | ||

| 1:45 | CNY | Caixin PMI Manufacturing Jun | 51 | 51 | 51.1 | |

| 7:15 | CHF | Retail Sales Real Y/Y May | -0.10% | 2.60% | 2.20% | |

| 7:30 | CHF | SVME PMI Jun | 61.1 | 61.1 | 62.4 | |

| 7:45 | EUR | Italy Manufacturing PMI Jun | 53.3 | 52.6 | 52.7 | |

| 7:50 | EUR | France Manufacturing PMI Jun F | 52.5 | 53.1 | 53.1 | |

| 7:55 | EUR | Germany Manufacturing PMI Jun F | 55.9 | 55.9 | 55.9 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Jun F | 54.9 | 55 | 55 | |

| 8:30 | GBP | PMI Manufacturing Jun | 54.4 | 53.5 | 54.4 | 54.3 |

| 9:00 | EUR | Eurozone Unemployment Rate May | 8.40% | 8.50% | 8.50% | 8.40% |

| 13:45 | USD | US Manufacturing PMI Jun F | 54.6 | 54.6 | ||

| 14:00 | USD | Construction Spending M/M May | 0.50% | 1.80% | ||

| 14:00 | USD | ISM Manufacturing Jun | 57.9 | 58.7 |

US Chamber of Commerce to campaign against Trump’s trade tariffs policies

Reuters reported that the US Chamber of Commerce is launching a campaign today to attack Trump's protectionist trade policy. It's believed that state-by-state analysis would be used for the campaign and it will warn that Americans that Trump is risking a global trade war that will eventually hit their pockets.

Chamber President Tom Donohue was quoted saying that "the administration is threatening to undermine the economic progress it worked so hard to achieve." And he added that "we should seek free and fair trade, but this is just not the way to do it."

Being the largest business group in the US with 3 million members, the Chamber also have long history of being friendly with Republicans. Their stance carries some political significance.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1627

My outlook is bearish, for a break through 1.1600 support, towards 1.1510 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1690 | 1.1730 | 1.1600 | 1.1510 |

| 1.1730 | 1.1830 | 1.1510 | 1.1300 |

USD/JPY

Current level - 110.62

The uptrend remains intact, heading towards 111.40. Initial support is projected at 110.40.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.40 | 111.40 | 110.40 | 107.80 |

| 111.40 | 114.40 | 109.40 | 106.70 |

GBP/USD

Current level - 1.3153

The recent rise has capped at 1.3215 and the outlook is bearish, for another leg towards 1.3040.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3215 | 1.3618 | 1.3120 | 1.3040 |

| 1.3310 | 1.3990 | 1.3040 | 1.2770 |

Equities Retreat Amid Risk-Off Tones, Aussie Softens Ahead Of RBA Decision

Here are the latest developments in global markets:

FOREX: Dollar/yen traded at 110.75 (+0.08%) on Monday, giving back most of the gains it posted earlier in the session when it briefly touched a one-month high of 111.05, with the yen failing to capitalize substantially on the broader risk-off mood seen in other asset classes, like equities. Meanwhile, the dollar index was up by 0.15% at 94.77. Euro/dollar was down by 0.35%, hovering just above 1.1640 as concerns of a political crisis in Germany cast a shadow. The nation’s Interior Minister Seehofer offered to resign amid continued disagreements with Chancellor Merkel’s immigration policy; the two will continue talks today in hope of finding common ground. Pound/dollar was also on the back foot, lower by 0.39%, with the British currency struggling even despite reports the UK government has produced a new option for handling customs – a thorny issue in the Brexit negotiations. In the antipodeans, aussie/dollar (-0.49%) and kiwi/dollar (-0.35%) moved lower, trading close to the respective 18-month and 24-month lows they posted last week. Dollar/loonie was up by 0.33% at 1.3170 amid a tumble in oil prices, recovering some of the losses it posted on Friday.

STOCKS: European equities were a sea of red on Monday at 1000 GMT, as the political turbulence in Germany and the risk of further escalation in trade tensions sapped risk appetite. The EU Commission reportedly warned the US that introducing tariffs on imported cars – which President Trump has threatened – could elicit counter-levies from the US’s major trading partners, resulting in up to $294bn of US goods being subject to tariffs. The benchmark European STOXX 600 was down by 0.88%, while the blue-chip STOXX 50 fell 0.92%. The German DAX 30 (-0.55%), the French CAC 40 (-1.05%), the British FTSE 100 (-0.95%), and the Spanish IBEX 35 (-1.12%) all felt the heat as well. The negative sentiment looks set to roll over into Wall Street, with futures tracking major US indices like the S&P 500 and Dow Jones pointing to a much lower open today.

COMMODITIES: Oil prices recovered some of their earlier losses on Monday, though were still in the red for the day. WTI was down by 0.37% at $73.79, while Brent dropped by 0.68% to $78.64. Both benchmarks opened with notable gaps to the downside following tweets from President Trump over the weekend that Saudi Arabia’s King Salman had agreed to his nation raising its oil production. Nonetheless, the fact that the dip in prices was quickly bought – even despite a broader risk-off atmosphere and a stronger dollar – suggests that the bullish sentiment surrounding oil markets likely remains intact for now. In precious metals, gold was down by nearly 0.3% at $1248 per troy ounce, staying within breathing distance of its lows for the year achieved last week, at $1245.

Day Ahead: US ISM Manufacturing PMI eyed ahead of RBA decision

In the remainder of the day, the calendar will be light in terms of economic data, with US ISM manufacturing PMI being the only major pending release. Later, during the Asian trading session on Tuesday, attention will turn to the Reserve Bank of Australia (RBA) rate decision.

The Institute for Supply Management (ISM) manufacturing PMI reading is due out of the US at 1400 GMT. The index is expected to inch down by 0.6 points to 58.1 in June, from 58.7 in the preceding month. Any value above 50 indicates that the sector is growing. A higher-than-expected print could push the US dollar higher on expectations for a more aggressive rate-hike path by the Fed. The opposite holds true as well.

Other releases that might draw some attention out of the US are Markit’s final reading on June manufacturing PMI (1345 GMT), and May’s construction spending figures (1400 GMT).

As for central bank meetings, the RBA will announce its rate decision during the Asian trading session on Tuesday, at 0430 GMT. Policymakers are widely anticipated to keep interest rates unchanged and as such, attention will turn to the phrasing of the accompanying statement. While Australian economic data have been decent lately – with a stronger-than-anticipated GDP print for Q1 – the trade standoff between the US and China has also escalated quite substantially, amplifying the downside risks for export-reliant economies like Australia. Should the RBA take a page out of the RBNZ’s book and highlight those risks, the aussie could extend its recent losses. On the contrary, if the RBA refrains from appearing too concerned, or if it places more emphasis on encouraging developments like the recent decline in the exchange rate, then the aussie could rebound.

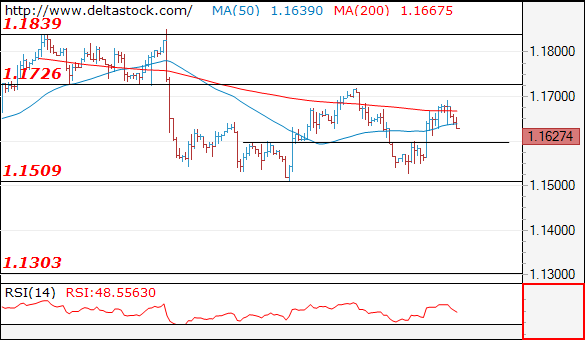

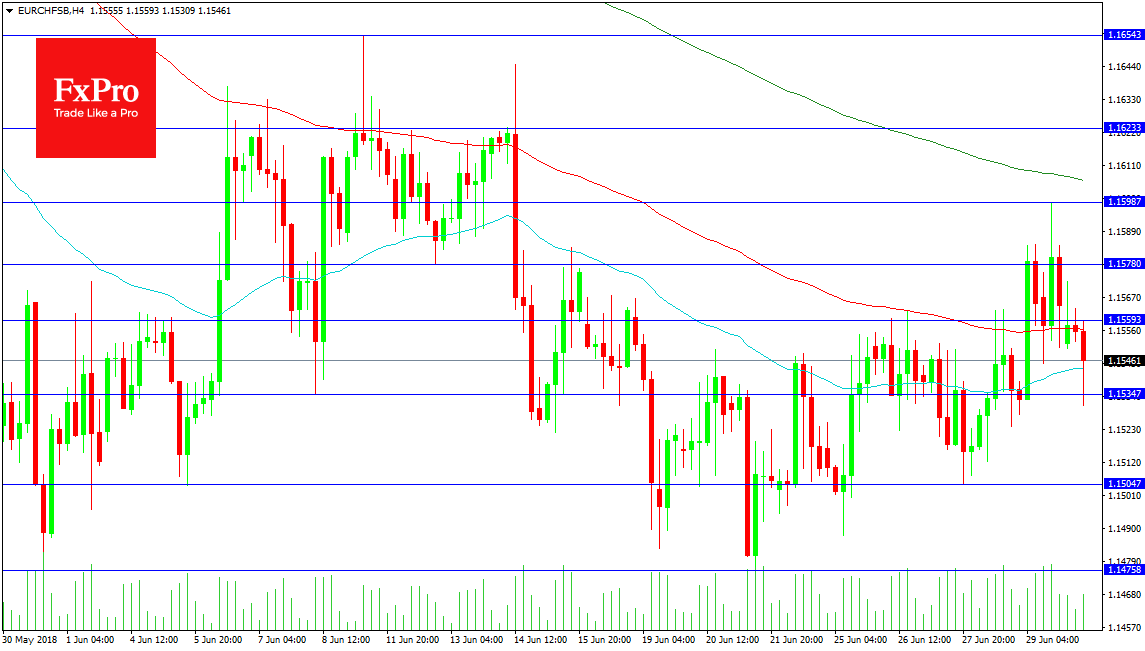

Forex Analysis: EURCHF

This pair is consolidating at present. The price is moving between 1.16500 and 1.14750. It is currently sitting between its 50 MA and its 100 MA at 1.15433 and 1.15564 respectively. Resistance comes in at the 1.15593 level followed by 1.15780 above. The recent high from Friday comes in at 1.15987 with the 1.16000 level just above followed by the 200 period MA at 1.16062. From there the 1.16233 level was where sellers have started to engage with the market and buyers took profit. The June high was 1.16543 on the 11th of the month.

Support can be seen at 1.15347 close to today’s low of 1.15309. Below this area there is buyers lurking around 1.15000. A drop from this level to the 1.14758 zone can also see buyers engage with the market. Further support is found at 1.14615 down to 1.14500. The 1.14000 remains an area of interest below.

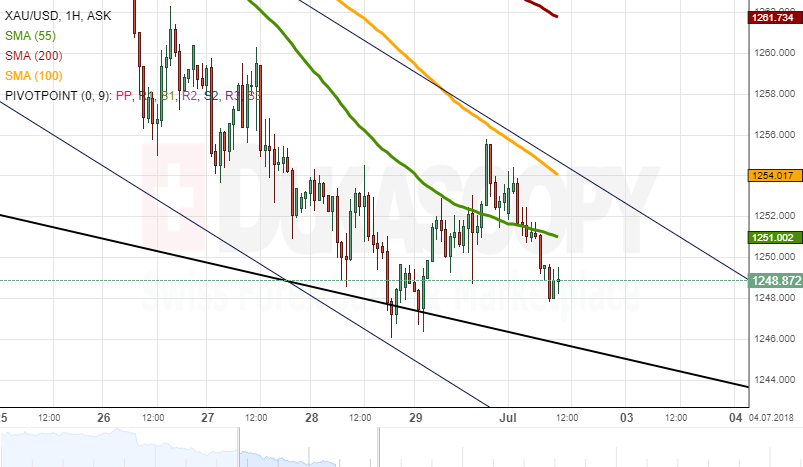

Gold Analysis: Declines Below 1,250 Mark

On Monday morning the yellow metal traded below the 1,250.00 level. It had retreated down to that level after it had passed the support of the 55-hour simple moving average.

The metal was set to decline down to the support provided by the lower trend line of the dominant descending pattern near the 1,245.00 mark. The retreat of the price was about to be caused by the 55 and 100-hour simple moving averages, which were steadily going downwards, as they were set to provide resistance to the commodity.

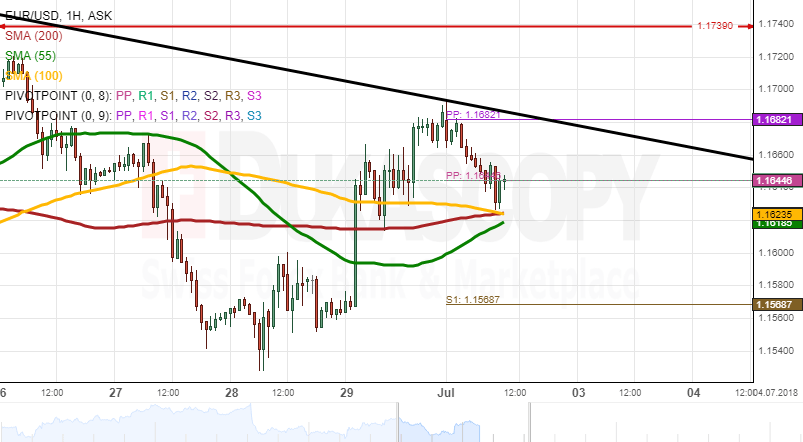

EURUSD Analysis: Meets Resistance

The common European currency after the large Friday's jumps against the US Dollar met with the resistance of a dominant descending channel. The event took place just as the last week's trading ended near midnight between Friday and Saturday.

On Monday the currency pair declined down until the decline was stopped by the combination by all of the three SMAs that are used by Dukascopy Analytics on technical charts.

A trader needs to watch the SMAs. They will either push the rate higher or, as they are passed, the rate would drop down to the next support level. The next support level below the SMAs on Monday was the weekly S1 at 1.1570 mark.

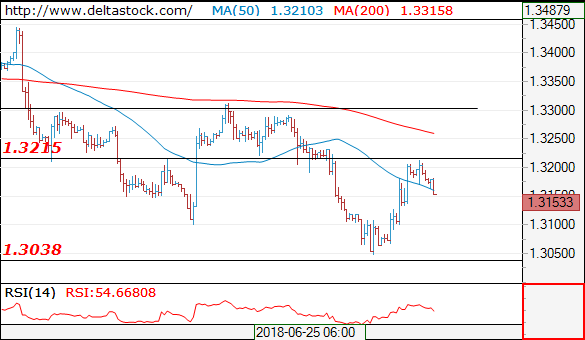

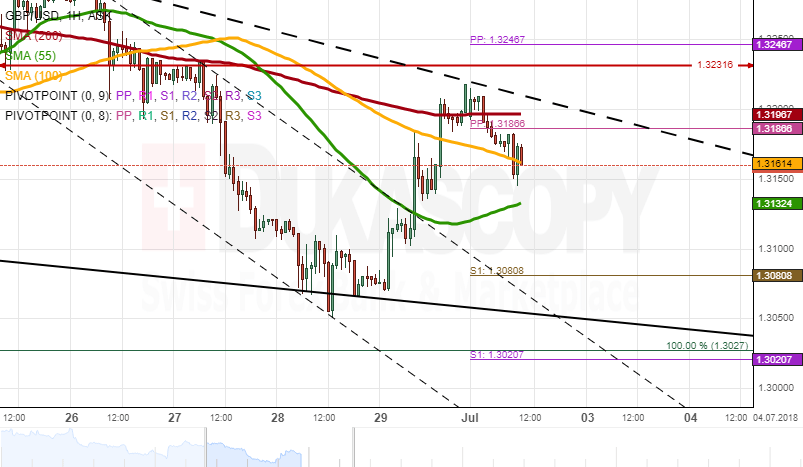

GBPUSD Analysis: Bounces Off Resistance

As many other US Dollar involving currency pairs, the GBP/USD has bounced off a resistance line. However, if one zooms out the chart, it can be observed that the currency exchange rate has bounced off a medium term resistance line.

Meanwhile, it is set to surge in the borders of a large scale descending channel pattern. The surge should occur, as the rate forms a new junior and medium term ascending pattern. Although, instead of that the rate faces various resistance lines, pivot points and simple moving averages.

Due to these factors combined, the GBP/USD is a rate, whose medium term movements are almost impossible to forecast.

Into US session: Dollar and Yen strong as trade risks weigh down global stocks

Heading into US session, Dollar continues to lead the way higher, followed by Yen. Australian Dollar and New Zealand Dollar are taking turns to be the weakest. But Canadian Dollar is supported by resilience in oil price, as WIT regains 74 handle.

Risk aversion is back in the market, started from Asia where China's SSE dropped -2.52%, leading others lower. Nikkei also lost -2.21%. European indices followed and open sharply lower initially. German DAX dipped to as low as 12132.72 but is now back at 12270, just down -0.3%. FTSE, on the other hand, is down -1%, pressing 7550. CAC is also down -0.85%.

Based on the actions in DAX, German Chancellor Angel Merkel's problem with her own coalition seems to be not too bothered by the market. Instead, it's likely the worries on trade war that's weighing down on sentiments. In particular, Europeans could be feeling quite upset as Trump said the EU is "as bad as China, just smaller".

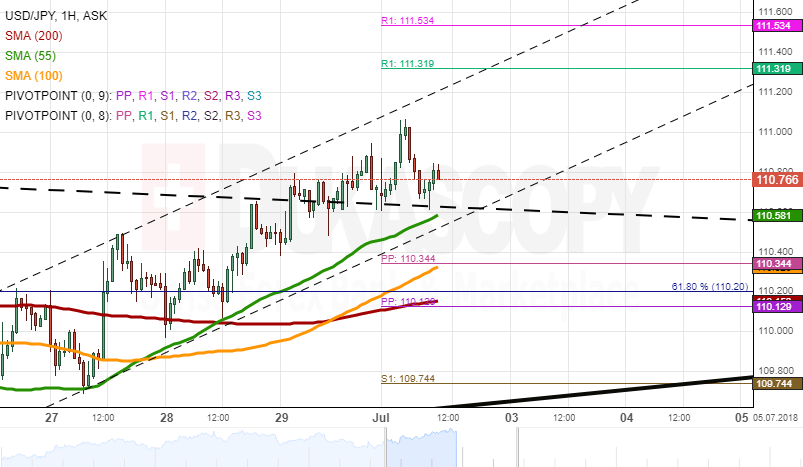

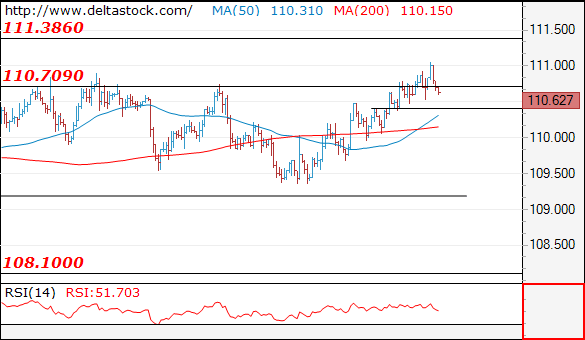

USDJPY Analysis: Finds Support In SMA

After booking a new high level against the Japanese Yen, the US Dollar retreated during the early hours of Monday's trading session. However, by the middle of the day the currency exchange rate had stopped the decline. Namely, the decline was stopped by the support of the 55-hour simple moving average near the 110.60 mark.

Moreover, the currency exchange rate was expected to surge even more in the upcoming trading sessions. The basis for this assumption is the fact that above the currency exchange rate there were no resistance levels up to the 111.30 mark.