Sample Category Title

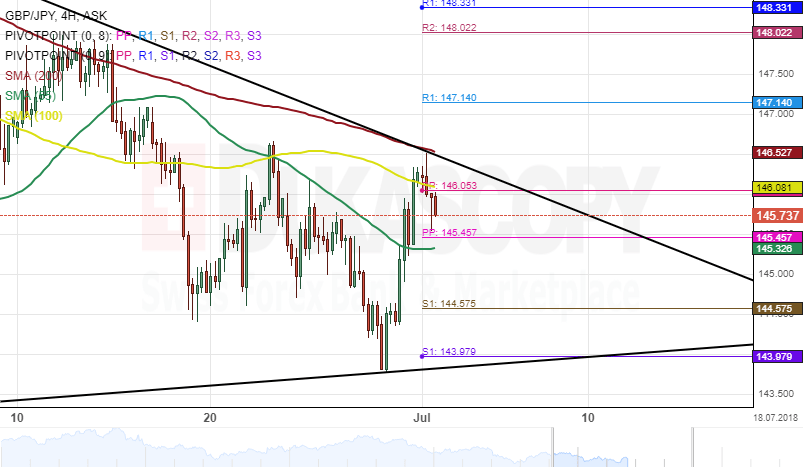

GBP/JPY 4H Chart: Stranded Between SMAs

The bearish sentiment that began late January has guided the GBP/JPY currency pair lower towards the September 2017 low level at 143.16. This mark –8.47% decrease in price during the last six months.

The 200-hour simple moving average has directed the exchange rate further south during the past few weeks. At the time of this analysis, the pair was stranded between SMAs. The 200-hour moving average was providing resistance at 146.54 while the 55-hour SMA was providing support.

In the meantime, technical indicators favour bears to continue controlling the market within this session. Meanwhile, a breakout could be expected from the SMAs within the next trading hours.

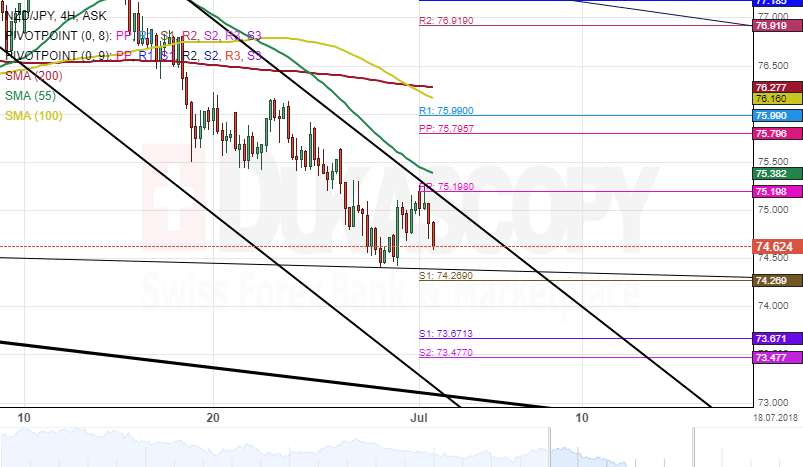

NZD/JPY 4H Chart: Bears Likely To Prevail

The New Zealand Dollar has diminished in trading range against the Japanese Yen during the past few weeks, thus forming a new junior descending pattern. The upper boundary of the junior channel was tested on June 13.

After hitting the weekly pivot point near the 75.19 mark, the NZD/JPY exchange rate reversed south.

Meanwhile, on the daily time frame, technical indicators are still strongly in favour of bearish sentiment.

Everything being equal, it is expected that bears continue to prevail in the market during the following trading session.

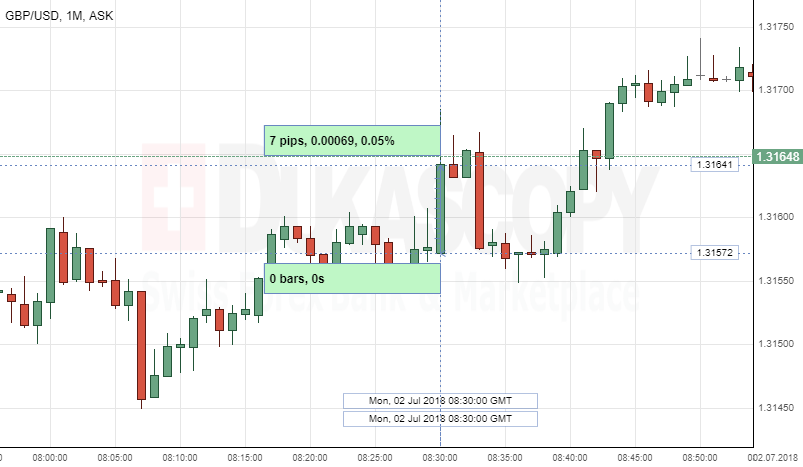

GBP/USD: UK Manufacturing PMI

The British Pound strengthened against the Greenback, following the UK Manufacturing PMI data release on Monday at 08:30 AM. The GBR/USD currency pair gained seven pips, or 0.05%, to continue fluctuating in the 1.3155 area.

The Markit released the monthly UK Purchasing Managers' Index data that came out better-than-expected of 54.4, and stayed unchanged from the previous period.

Rob Dobson stands: "The slowdown in new order growth since earlier in the year has also left manufacturers increasingly reliant on backlogs of work and inventory building to maintain higher output."

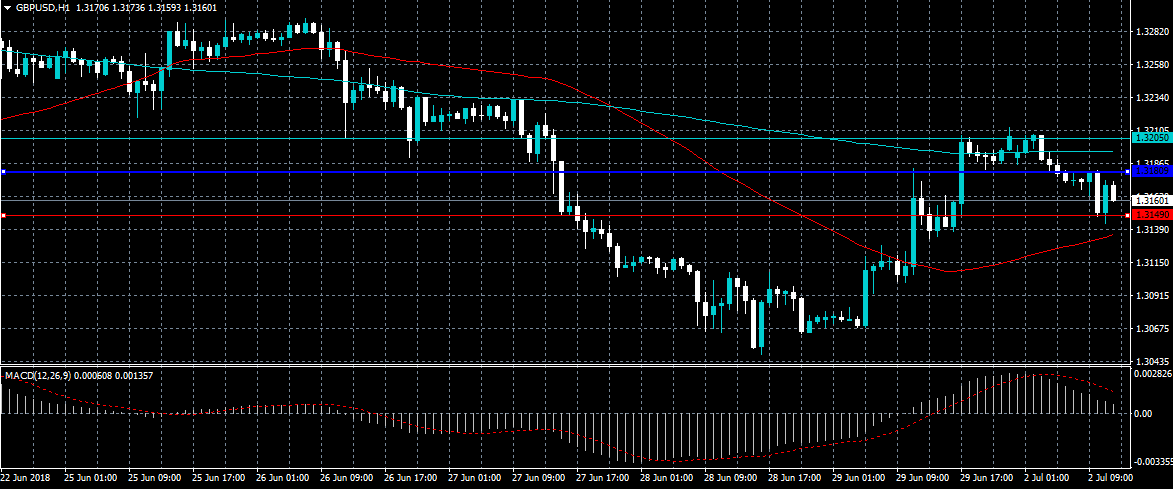

GBPUSD Turning Bearish Below 1.3180

The British pound has started to trade lower against the greenback, as the US dollar index once again starts to firm in early-week trading. The GBPUSD pair has so far found support from the 1.3143 level, although dip-buying is still prevalent after Friday’s rapid advance. Sellers will now try to keep price contained below the 1.3149 support level, while buyers will look to edge price above the 1.3180 level.

The GBPUSD pair is bearish while trading below the 1.3180 level, further declines towards 1.3124 and 1.3101 seems possible.

If the GBPUSD pair moves above the 1.3180 level, buyers may test towards the 1.3205 and 1.3245 levels.

EURUSD Intraday Bearish Below 1.1674 Level

The euro currency has come under selling pressure against the US dollar, as reports surface of problems inside the current German coalition government. The EUR/USD pair has so far fallen towards the 1.1624 level, after finding strong resistance from the 1.1690 level earlier today. Euro sellers will attempt to move price below the 1.1624 level, while buyers will look to move the pair back above the 1.1674 level.

The EURUSD pair is bearish while trading below the 1.1674 level, key intraday support is found at the 1.1600 and 1.1554 levels.

If EURUSD buyers move price back above the 1.1674 level, the pair may correct back towards the 1.1690 and 1.1719 levels.

DAX Slips As German, Eurozone PMIs Soften

The DAX index has started the week with losses. In the Monday session, the DAX is at 12,237, down 0.56% on the day. In economic news, the focus is on manufacturing reports. German and eurozone manufacturing PMIs were within expectations, with readings of 55.9 and 54.9, respectively. Later in the day, the eurozone releases PPI and the unemployment rate. On Tuesday, the eurozone releases retail sales.

European equity markets remain under pressure and the DAX had another rough week, declining 1.5 percent. Recent trade tensions are threatening to hamper the eurozone export sector, which in turn could weigh on manufacturing output. Investors are keeping a close eye on German and eurozone manufacturing PMIs, which are bellwethers of the strength of the manufacturing sector. In June, the German and eurozone readings pointed to expansion but also continued a downward trend. Both PMIs have now dropped for six straight months, raising concerns among investors about the strength of the eurozone economy. Germany, the locomotive of the eurozone, produced soft consumer numbers last week. Retail Sales plunged 2.1%, its steepest decline in 2018. As well, Preliminary CPI fell to 0.1%, down from 0.5% a month earlier.

On Friday, EU leaders meeting in Brussels announced with great fanfare that they had reached an agreement on migration. However, the deal was short on details appears to be a stopgap which papers over the deep divisions that still remain in the EU over immigration. German Chancellor Angela Merkel didn’t have much time to celebrate the news, as her fragile coalition is in crisis. On Sunday, German Interior Minister Horst Seehofer offered to resign, saying the migrant deal didn’t go far enough in protecting Germany from illegal immigration. Seehofer heads the CSU, which is the junior coalition partner in the coalition. Merkel will have to find a way to keep Seehoger on board if she wants to stay in power, and if this political crisis continues, investors could get nervous and send the DAX lower.

Global Risk Aversion Driven By Trade Concerns And German Political Risks

Notes/Observations

- Q3 begins with trade war concerns, German political risk and divergence in monetary policy across the world

- Major European manufacturing PMI readings come in mixed but remain in expansion Germany confirmed a decline, France revised lower and UK had a small beat.

- Italy's unemployment rate fell in May to its lowest in almost six years

- German Chancellor Merkel's ruling coalition meets in last-ditch talks over the migration dispute that is threatening her leadership

Asia:

- China’s manufacturing activity slips amid trade war with US

Europe:

- Germany's CDU and CSU are said to meet again later this evening

- EU makes written submission to US Commerce Dept warning that EU and others will likely respond to tariffs on foreign autos, by targeting $300B in US goods in retaliation

Americas:

- (CA) Canada began imposing retaliatory tariffs on US goods following the Trump administration's new tariffs on Canadian steel and aluminum

Energy:

- White House corrects Trump tweet on Saudi Arabia oil boost (Trump asked Saudi King to increase production by 2M bpd and that he agreed)

- Iran official: change to OPEC output levels require an emergency meeting

Economic Data:

- (IN) India Jun Manufacturing PMI: 53.1 V 51.2 PRIOR

- (IE) Ireland Jun Manufacturing PMI: 56.6 v 55.4 prior (61st month of expansion)

- (RU) Russia Jun Manufacturing PMI: 49.5 v 50.5e (2nd consecutive contraction)

- (SE) Sweden Jun Manufacturing PMI: 54.2 v 55.2e

- (AU) Australia Jun Commodity Index (AUD): 108.6 v 109.2 prior; Commodity Index SDR Y/Y: 6.6% v 3.5% prior

- (NL) Netherlands Jun Manufacturing PMI: 60.1 v 60.0e (58th month of expansion, 9-month low)

- (HU) Hungary Jun Manufacturing PMI: 53.0 v 55.2 prior (31st month of expansion)

- (TR) Turkey Jun Manufacturing PMI: 46.8 v 46.4 prior (3rd straight contraction)

- (PL) Poland Jun Manufacturing PMI: 54.2 v 53.0e (43rd month of expansion)

- (ES) SPAIN JUN Manufacturing PMI: 53.4 V 53.6E (56th month of expansion)

- (CH) Swiss Jun Manufacturing PMI: 61.6 v 61.0e

- (CZ) Czech Jun Manufacturing PMI: 56.8 v 55.8e (23rd month of expansion)

- (IT) ITALY JUN Manufacturing PMI: 53.3 V 52.5E (22nd month of expansion)

- (FR) FRANCE JUN FINAL Manufacturing PMI: 52.5 V 53.1E (revised lower but still confirms its 21st month of expansion)

- (DE) GERMANY JUN FINAL Manufacturing PMI: 55.9 V 55.9E (confirms 42nd month of expansion)

- (EU) EURO ZONE JUN FINAL Manufacturing PMI: 54.9 V 55.0E (revised lower)

- (IT) ITALY MAY PRELIMINARY UNEMPLOYMENT RATE: 10.7% V 11.1%E (near 6-year low)

- (GR) Greece Jun Manufacturing PMI: 53.5 v 54.2 prior (13th month of expansion)

- (UK) Jun Manufacturing PMI: 54.4 V 54.0E (23rd month of expansion)

- (EU) EURO ZONE MAY UNEMPLOYMENT RATE: 8.4% V 8.5%E

- (BE) Belgium May Unemployment Rate: 6.0% v 6.0% prior

- (DK) Denmark Jun PMI Survey: 49.7 v 47.8 prior

- (ZA) South Africa Jun Manufacturing PMI: 47.9 v 49.8 prior

Fixed Income Issuance:

Norway sells NOK4.0B vs. NOK4.0B indicated in 6-month bills; Avg Yield: 0.71% v 0.71% prior; Bid-to-cover: 2.58x v 2.63x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 -1.1% at 3,365, FTSE -0.9% at 7,566, DAX -0.4% at 12,255, CAC-40 -1.0% at 5,273; IBEX-35 -1.3% at 9,503, FTSE MIB -1.5% at 21,299, SMI -1.0% at 8,525, S&P 500 Futures -0.5%]

- Market Focal Points/Key Themes: European stocks open lower across the board and maintained trend as session advanced; light corporate news flow keeps focus on raft of macro data; concern still over immigration issue discord in German parliament; consumer discretionary one of few sectors performing positively; materials stocks and financials lead to the downside; Tesco enters talks with Carrefour for strategic alliance; Airbus reportedly fails to meet delivery for A320neo due to Pratt & Whitney engine troubles; Candada, Chile, Colombia and Venezuela closed for holiday

Equities

- Consumer discretionary: Carrefour CA.FR +0.3% (talks with Tesco) Tesco TSCO.UK +0.4% (talks with Carrefour)

- Energy: Fred Olsen Energy FOE.NO -15.2% (fails to secure debt extension), REC Silicon REC.NO -14.4% (lay-offs)

- Industrials: Airbus AIR.FR -2.1% (reportedly misses delivery), ThyssenKrupp TKA.DE -1.6% (deal with Tata)

Speakers

- (UK) Gov't official confirms cabinet to debate 3rd customs option

Currencies

- EUR/USD rocked after CSU party leader Seehofer offered to resign over the migration dispute, pared losses after CDU said they will pursue migrant pacts with partners

- USD/MXP (peso) initially rallied as Mexican Leftist wins Presidential Election (majority of move took place last week). Peso eventually weakened as investors weigh a leftist presidency.

Fixed Income

- Bund Futures trade 26 ticks higher at 162.68 as trade tensions heighten. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.26 higher by 22 ticks as PM May’s Brexit moment of truth approaches at the “body bag summit”. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Monday's liquidity report showed Friday's excess liquidity declined from €1.793T to €1.781T. Use of the marginal lending facility rose from €30M to €59M.

- Corporate issuance saw just $3.2B priced last week

Looking Ahead

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 08:00 (CZ) Czech Jun Budget Balance (CZK): No est v -23.1B prior

- 08:05 (UK) Baltic Dry Bulk Index

- 09:00 (BR) Brazil Jun Manufacturing PMI: No est v 50.7 prior

- 09:00 (SG) Singapore Jun Purchasing Managers Index (PMI): 52.5e v 52.7 prior; Electronic Sector: No est v 52.3 prior

- 09:45 (US) Jun Final Markit Manufacturing PMI: 54.6e v 54.6 prelim

- 10:00 (US) May Construction Spending M/M: 0.5%e v 1.8% prior

- 10:00 (US) Jun ISM Manufacturing: 58.2e v 58.7 prior; Prices Paid: 74.3e v 79.5 prior

- 10:00 (MX) Mexico Central Bank Economist Survey

- 10:00 (MX) Mexico May Total Remittances: No est v $2.7B prior

- 10:30 (MX) Mexico Jun Manufacturing PMI: No est v 51.0 prior

- 12:00 (IT) Italy Jun New Car Registrations Y/Y: No est v -2.8% prior

- 13:00 (MX) Mexico Jun IMEF Manufacturing Index: No est v 51.0 prior; Non-Manufacturing Index: No est v 51.1 prior

- 16:00 (US) Weekly Crop Progress Report

America Booms

America booms

The US economy is firing on all cylinders with net exports above expectations, which defies the backdrop of protectionism. Q2 GDP growth could hit 4.5% annualised; new jobs may top 200.000 t as well. 10-year T-Bills fell to 2.88% (further flattening the curve), which should slow the progression of the USD higher, but a fourth rate hike for 2018 might be on its way. It would be interesting if there were any conversation over global trade outlook.

President Trump’s latest tweet-storm is to demand that OPEC increase crude oil output by 1-2 million barrel/day. Friday could bring additional Trump tariffs, and retaliation from the Chinese. Global growth remains firm, but there is a feeling that the world’s ability to shrug off attacks on trade might becoming less effective. Weakness in CNY and Chinese equities highlight this. Capital outflows from China have accelerated. With Asia nations extremely exposed to higher oil prices (alongside weaker commodity demand), stronger US interest rates, fear of stagflation and protectionism, currencies should under perform.

The Mexican landside of Andrés Manuel López Obrador (AMLO) has not provided a big MXN boost. The peso had been trading on political uncertainty prior to Sunday but moving forward it will be driven by NAFTA. The AMLO-Trump relationship is totally untested. Given Trump’s nature to be kinder to friends, relations between the two will be critical. We remain bearish on MXN in the current uncertain risk off environment.

Bias to dollar over euro

In Europe the focus is on German politics and economics. Purchasing data should show a small increase. While Chancellor Angela Merkel managed to float a refugee resettlement deal, partner-party CSU Chairman and interior Minister Horst Seehofer vetoed. We have a slight USD bias, given political uncertainty in the Eurozone and higher interest rates in the US. With low liquidly and summer conditions, volatility and wide price swings should dominate this week.

EUR/USD – Euro Dips As Manufacturing PMIs Continue To Soften

EUR/USD has started the week with losses, after posting gains on Friday. In the Monday session, the pair is trading at 1.1642, down 0.37% on the day. On the release front, the focus on both sides of the pond is on manufacturing reports. German and eurozone manufacturing PMIs were within expectations, with readings of 55.9 and 54.9, respectively. Later in the day, the eurozone releases PPI and the unemployment rate. In the U.S, today’s key event is ISM Manufacturing PMI, with the markets bracing for a drop to 58.2 points.

Recent trade tensions are threatening to hamper the eurozone export sector, which in turn could weigh on manufacturing output. This has put the spotlight on German and eurozone manufacturing PMIs, which are bellwethers of the strength of the manufacturing sector. In June, the German and eurozone readings pointed to expansion but also continued a downward trend. Both PMIs have now dropped for six straight months, raising concerns among investors about the strength of the eurozone economy. Germany, the locomotive of the eurozone, produced soft consumer numbers last week. Retail Sales plunged 2.1%, its steepest decline in 2018. As well, Preliminary CPI fell to 0.1%, down from 0.5% a month earlier.

On Friday, the euro moved higher, in response to a dramatic announcement that EU leaders had hammered out a deal on migration. However, the deal was short on details appears to be a stopgap which papers over the deep divisions that still remain in the EU over immigration. German Chancellor Angela Merkel didn’t have much time to celebrate the news, as her government is again in crisis. On Sunday, German Interior Minister Horst Seehofer offered to resign, saying the migrant deal didn’t go far enough in protecting Germany from illegal immigration. Seehofer heads the CSU, which is the junior coalition partner in the coalition. Merkel will have to find a way to keep Seehoger on board if she wants to stay in power, and if this political crisis continues, the euro could lose ground.

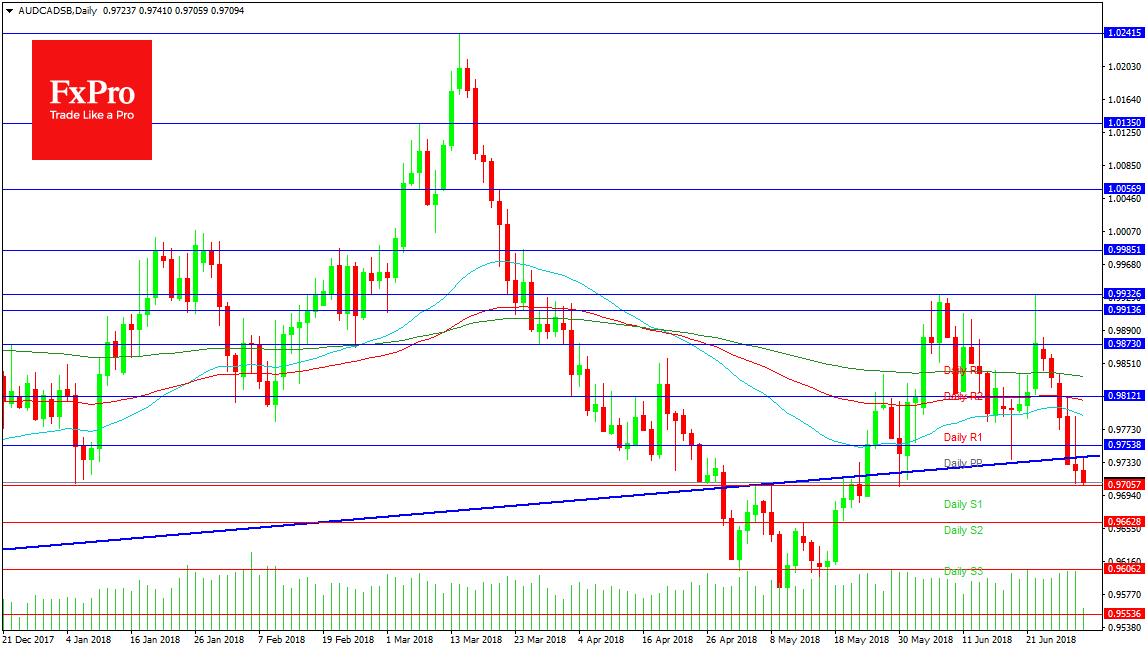

Forex Analysis: AUDCAD

The AUDCAD pair is pushing lower again today as it rejects trend line support now turned resistance at 0.97410. The fall last week took the price under the trough of the double top at 0.99326 and now points to a move to its target at 0.95424. Support at 0.97057 is last week’s low, plus the January support level, and is holding price up for now. Below this area 0.96628 comes into play followed by 0.96062. The 2018 low is found at 0.95536 which can see buyers engage and try to manoeuvre the market into a trading range up to 0.99300.

Resistance from the current level comes in at the blue trend line followed by the 0.97538 level. A move higher engages with the moving averages with the 50 DMA at 0.97898 followed by the 100 DMA at 0.98072. This leads to the 0.98121 price level with the 200 DMA above at 098358. A break higher would meet resistance at 0.98730 and the range top at 0.99326. A breakout from here would target 0.99850 initially followed by 1.00000 and eventually the 2018 top at 1.02415.