Sample Category Title

European Inflation Picture Is Improving, Focus On EU Leader Summit

Notes/Observations

- Major European inflation (German States, Spain) holds above the ECB target area for the 2nd straight month

- Trade conflict between the EU and the US leaving a clear mark on the consumer mood in Germany as economic assessment dips

- EU Leaders begin 2-day summit; Migration issue could determine Europe's fate

Asia:

- New Zealand Central Bank (RBNZ) left its Official Cash Rate unchanged at 1.75% (as expected). Reiterated view that expected to keep rate at this expansionary level for a considerable period of time. Monetary policy to be supportive for some time to come as CPI remained below target

- Japan Preliminary May Retail sales M/M: -1.7% v -0.8%e

- China PBoC sets yuan reference rate at 6.5960 v 6.5569 prior (weakest setting since late Dec 2017)

- China Commerce Ministry (MOFCOM): US planned curbs on technology exports to China may 'backfire'. To carefully monitor US policies on inbound investments; does not support using US national security as grounds to restrict investment. Planned restrictions on US exports to China are likely to undermine President's Trump’s desire to cut the trade deficit

Europe:

- Germany Interior Minister Seehofer (CSU party leader): 'Very optimistic' that officials can solve coalition dispute over migration; not aiming to bring down Govt

- Greece said to be willing to take asylum seekers under a deal with German Chancellor Merkel

- Italy govt reportedly prepared to block the decision on migrations at the EU Leader Summit if EU partners do not agree to include shared responsibilities for at sea rescues

- German Budget Committee said to have approved €343.6B balanced budget plan for 2018 with spending increased by almost 4% from 2017 level without incurring any new debt’

- BOE Dep Gov Cunliffe reiterated concern about households with high debt that could be impacted in a recession

Americas:

- Fed's Bullard (dove, non-voter): going too far with rate increases could pose some risks; we don't need to raise rates preemptively

- Fed's Rosengren (moderate, non-voter): flexible inflation target may help to avoid zero rates; don't let the jobless rate fall too far under the long run level. Had have not seen wages go up rapidly yet

- Bank of Canada's (BOC) Poloz stated that might shift in language represented increased confidence that the economy was performing as we expected and that higher interest rates would be warranted

Economic

- (NL) Netherlands Jun Producer Confidence: 7.7 v 9.8 prior

- (DE) Germany July GfK Consumer Confidence: 10.7 v 10.6e

- (NO) Norway May Credit Indicator Growth Y/Y: 6.0% v 6.3%e

- (FI) Finland May House Price Index M/M: 0.2% v 1.6% prior; Y/Y: 0.8% v 0.6% prior

- (DE) Germany Jun CPI Saxony M/M: 0.1% v 0.5% prior; Y/Y: 2.1% v 2.2% prior

- (ES) Spain Jun Preliminary CPI M/M: 0.3% v 0.2%e; Y/Y: 2.3% v 2.3%e

- (ES) Spain Jun Preliminary CPI EU Harmonized M/M: 0.2% v 0.2%e; Y/Y: 2.3% v 2.3%e

- (ES) Spain May Adjusted Retail Sales Y/Y: -0.4% v +0.7%e; Retail Sales (unadj) Y/Y: -0.3% v 0.7% prior

- (TR) Turkey Jun Economic Confidence: 90.4 v 93.5 prior

- (HU) Hungary May Unemployment Rate: 3.7% v 3.8%e

- (SE) Sweden May Retail Sales M/M: 0.2% v 0.4%e; Y/Y: 3.1% v 2.8%e

- (SE) Sweden May Trade Balance (SEK): -2.6B v -6.1B prior

- (DE) Germany Jun CPI Bavaria M/M: 0.2% v 0.5% prior; Y/Y:2.4 % v 2.3% prior

- (DE) Germany Jun CPI Brandenburg M/M: 0.0% v 0.7% prior; Y/Y: 2.2% v 2.4% prior

- (DE) Germany Jun CPI Hesse M/M: 0.0%v 0.5% prior; Y/Y: 1.8% v 1.9% prior

- (DE) Germany Jun CPI Baden Wuerttemberg M/M: 0.2% v 0.5% prior; Y/Y: 2.4% v 2.3% prior

- (IT) Italy Q1 YTD Deficit to GDP: 3.5% v 2.3% prior

- (DE) Germany Jun CPI North Rhine Westphalia M/M: 0.1% v 0.4% prior; Y/Y: 2.1% v 2.1% prior

- (PT) Portugal Jun Consumer Confidence: 2.8 v 3.3 prior; Economic Climate Indicator: 2.4 v 2.3 prior

- (EU) Euro Zone Jun Business Climate Indicator: 1.39 v 1.40e; Consumer Confidence (Final): -0.5 v -0.5e, Economic Confidence: 112.3 v 112.0e, Industrial Confidence: 6.9 v 6.5e, Services Confidence: 14.4 v 14.1e

- (IT) Italy Jun Preliminary CPI (incl. tobacco) M/M: 0.3% v 0.2%e; Y/Y: 1.4% v 1.3%e

- (IT) Italy Jun Preliminary CPI EU Harmonized M/M: 0.3% v 0.2%e; Y/Y: 1.5% v 1.3%e

Fixed Income Issuance:

- (DK) Denmark sold total DKK900M in 1-month and 6-month Bills

- (IT) Italy Debt Agency (Tesoro) sold total €4.5B vs. €3.5-4.5B indicated range in 5-year and 10-year BTP Bonds

- Sold €2.0B vs. €1.5-2.0B indicated range in 0.95% Mar 2023 BTP bonds; Avg Yield: 1.82% v 2.32% prior; Bid-to-cover: 1.34x v 1.53x prior

- Sold €2.5B vs. €2.0-2.5B indicated range in 2.00% Feb 2028 BTP bonds; Avg Yield: 2.77% v 3.00% prior; Bid-to-cover: 1.26x v 1.48x prior

- (IT) Italy Debt Agency (Tesoro) sold €2.0B vs. €1.5-2.0B indicated range in Sept 2025 CCTeu (Floating Rate Notes); Avg Yield: 1.67% v 2.00% prior; Bid-to-cover: 1.30x v 1.44x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 -0.4% at 3,382, FTSE -0.2% at 7,607, DAX -0.5% at 12,280, CAC-40 -0.3% at 5,313; IBEX-35 -0.7% at 9,593, FTSE MIB -0.4% at 21,480, SMI -0.3% at 8,481 , S&P 500 Futures +0.2%]

- Market Focal Points/Key Themes: European markets opened mixed with an upward bias but moved downward as the session progressed; macro data releases ahead of end of Q2 taking attention; consumer discretionary leads performers; materials underperforming; Ukraine closed for holiday; upcoming earnings expected in the US session include Accenture and Walgreens Boots Alliance

Equities

- Consumer discretionary: BCA Marketplace BCA.UK -0.7% (results), Hennes & Mauritz HMB.SE +0.7% (earnings), L'Oreal OR.FR +0.4% (analyst action), Kering KER.FR +1.2% (analyst action), Zumtobel ZAG.AT -17.0% (results)

- Consumer staples: CHR Hansen CHR.DK -2.7% (results)

- Healthcare: Genfit GNFT.FR +2.3% (study results)

- Industrials: Saint-Gobain SGO.FR -0.1% (analyst action)

- Telecom: Mediaset MS.IT +1.2% (CEO comments), Prysmian PRY.IT -2.4% (capital increase)

- Utilities: Suez SEV.FR -1.3% (analyst action)

Speakers

- German Chancellor Merkel stated that in her parliament ahead of EU Leader Summit that the Euro was stable and reiterated her stance that a stronger Europe was in Germany's best interest. Further Euro Zone reforms were needed after the successful Greek bail-out program. There would be no debt union; every member must stick to their rules (referring to the recent Franco-German agreement on reforms). Not where we wanted to be on the issue of migration and conceded that would not be able to reach a common asylum agreement at the EU Leader summit. Migration could determine Europe's fate. Must talk to the US to avoid a trade war

- ECB Economic Bulletin noted that the underlying inflation expected to pick up towards the end of 2018 and then increase gradually. Economic expansion remained solid and broad-based and was expected to continue. Balance of risks for global activity had worsened and skewed to the downside

- BOE Agents Summary of Business Conditions: Retail sales growth had ticked up over the past month, boosted by stronger sales of seasonal clothing and footwear; growth in consumer services had slowed. Growth in domestic manufacturing output had edged up; growth in export output had eased slightly but remained robust

- EU Leaders said to urge UK to settle with Spain on status of Gibraltar after Brexit

- Hungary govt said to see no economic reason for the current level of the HUF currency (Forint)

- Thailand Finance Ministry: Q2 GDP growth seen lower than the 4.8% annual pace registered in Q1

- BoJ Deputy Gov Wakatabe: no limit to monetary policy

- Libya National Oil Company (NOC) Chairman Sanalla: Libya producing 700K bpd of oil after fighting in East

Currencies

- USD began the EU session on solid footing but saw its best level erode as the trading day progressed.

- EUR/USD was approaching its recent cycle lows but managed to hold above the 1.15 level for the 3rd time this year. The trade conflict between the EU and the USA seemed to be intensifying and left a clear mark on the consumer mood in Germany. Dealers looked ahead to the Italian issuance in the session and noted that Italian government bonds would likely hold up well ahead of the upcoming auctions in the 5-year and 10-year range. Snippets of Jun inflation data for Germany and Spain showed CPI just above the ECB target level for the 2nd straight month.

- GBP/USD was at 7-month lows as its tested 1.3070 as EU leaders began a 2-day summit with Brexit clarity as one of the main topics

- Emerging market currencies remained under pressure. The INR currency (Rupee) hit a fresh record low at 69.00/dollar as oil prices reached a 4-year high. South Africa ZAR curreny (Rand) also besieged by domestic politics to hit a 7-month low just under the 14.00 level against the USD. TRY currency (Lira) was initially off by 0.5% against the USD and EUR but moved off its worst level.

Fixed Income

- Bund Futures trade 6 ticks lower at 162.38 as the German states inflation readings offer some support for the euro. Upside targets 162.75 followed by 163.25, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.33 higher by 2 ticks following the move in Treasuries. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Thursday's liquidity report showed Wednesday's excess liquidity declined from €1.806T to €1.801T. Use of the marginal lending facility fell from €98M to €97M.

- Corporate issuance saw no deals priced in the primary market

Looking Ahead

- (ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to leave 7-Day Reverse Repo Rate unchanged at 4.75% (no set time) 3455-yea d 10-yarBTPBonds

- (EG) Egypt Central Bank Interest Rate Decision: Expected to leave key rates unchanged

- (BE) Belgium Jun CPI M/M: No est v 0.2% prior; Y/Y: No est v 1.8% prior

- (CA) Canada Jun CFIB Business Barometer: No est v 62.5 prior

- (BR) Brazil May Central Govt Budget Balance (BRL): No est v 7.2B prior

- (EU) EU leaders begin 2-day Summit in Brussels

- (US) Fed releases part 2 of stress tests results (firms will learn whether they can boost buybacks and dividends to shareholders)

- 05:30 (ZA) South Africa May PPI M/M: 0.5%e v 1.0% prior; Y/Y: 4.4%e v 4.4% prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month bills; Avg Yield: % v 0.40% prior; bid-to-cover: x v 2.00x prior (Jun 14th 2018)

- 05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Rate bonds

- 06:00 (UK) BOE’s Bailey on payments

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Central Bank (BCB) Quarterly Inflation Report

- 07:00 (BR) Brazil Jun FGV Inflation IGPM M/M: 1.8%e v 1.4% prior; Y/Y: 6.8%e v 4.3% prior

- 07:00 (ES) Spain May YTD Budget Balance: No est v -€5.9B prior

- 08:00 (DE) Germany Jun Preliminary CPI M/M: 0.1%e v 0.5% prior; Y/Y: 2.1%e v 2.2% prior

- 08:00 (DE) Germany Jun Preliminary CPI EU Harmonized M/M: 0.2%e v 0.6% prior; Y/Y: 2.1%e v 2.2% prior

- 08:00 Poland Central Bank (NBP) Jun Minutes

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Q1 Final GDP Annualized (3rd reading) Q/Q: 2.2%e v 2.2% prelim; Personal Consumption: 1.0%e v 1.0% prelim

- 08:30 (US) Q1 Final GDP Price Index: 1.9%e v 1.9% prelim; Core PCE Q/Q: No est v 2.3% prelim

- 08:30 (US) Initial Jobless Claims: 220Ke v 218K prior; Continuing Claims: 1.72Me v 1.723M prior

- 08:30 (CL) Chile Central Bank Jun Meeting Minutes

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (RU) Russia Gold and Forex Reserve w/e Jun 22nd: No est v $462.4B prior

- 09:30 (UK) BOE’s Haldane (chief economist, dissenter) in London

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 10:45 (US) Fed’s Bullard (dove, non-voter) in St Louis

- 11:00 (US) Jun Kansas City Fed Manufacturing Activity: 26e v 29 prior

- 12:00 (US) Fed’s Bostic (voter, dove)

- 13:00 (US) Treasury to sell 7-Year Notes

- 15:00 (US) May Agriculture Prices Received: No est v -3.1% prior

Markets Are Nervous, Sterling Slumps

Risk aversion lingers

Since the beginning of the week, financial markets have been stuck in limbo as trade war uncertainties linger. Asian equities closed in red as risk-off sentiment prevailed. The Nikkei closed flat, while Chinese equities continued to suffer with the CSI 300 falling 1.03%. Indonesian equities suffered the most in Asian EM complex as the JCI erased 1.67%. However, European equities have been rather hesitant in early trading session, which suggests we may be out of the wood; however, the lack of good news could most likely translate into further weakness. The VIX indexed eased to 17.09 from 17.91.

In the FX market, investors continued to favour less risky asset. After surging across the board yesterday, the greenback consolidated gains this morning with the Dollar Index stabilising around 95.40. The index is currently testing the key 95.50 resistance area (high from June 21st). Given the highly uncertain environment, a breakout cannot be ruled; however, the buck is in overbought territory against most of its peers, which suggests that a pullback is highly probable.

EUR/USD is testing the support that lies at 1.1510 (low from May 29th and June 21st), USD/CHF failed to break the 0.9990 resistance (high from June 18th), while kept on treading water between 109.20 and 110.90. In the absence of fresh news, the market will stay in wait-and-see mode.

Further weakness for the pound

As the European Union final summit regarding the migration crisis is taking place today, expectations of further advance in Brexit are set aside, despite recent request from EU and UK businesses to show measurable progress in the arrangement (i.e. Irish custom border).

Accordingly, industrials are becoming nervous, such is the case of Airbus’ recent statement warning of leaving the country if no deal would be found until 2019. Private company Heathrow Airport Holdings, went one step further, announcing its departure from Oxford headquarter to the Netherlands, in order to remain under EU law after Brexit.

Since Brexit negotiations are placed at a lower priority on Europe’s agenda, disappointment is felt on the pound side. Although Bank of England interest rate increase (2 August 2018 earliest) weighs on the balance, we would rather favor a bearish bias for the GBP/USD pair. Indeed, as one of the weakest currency on a quarterly basis, GBP/USD is currently trading at November 2017 range, valued at 1.3090 and heading along 1.3070 in the short term.

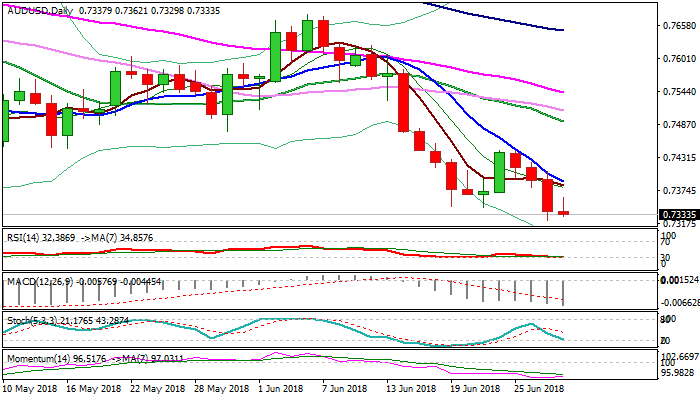

AUDUSD Outlook: Close Below Key Fibo Support At 0.7325 To Signal Further Weakness

The Aussie dollar is consolidating above new low at 0.7322 (the lowest since Jan 2017) posted on Wednesday.

Three-day descend is taking a breather but negative sentiment and bearish techs keep the downside in focus as Wednesday’s fall also cracked important support at 0.7325 (Fibo 61.8% of larger 0.6825/0.8135 rally).

Close below 0.7328 (09 May 2017 low) and 0.7325 Fibo support would generate bearish signal for extension of broader downtrend from 0.8135 (2018 high) towards 0.7160 (late Dec 2016 higher base) and 0.7135 (Fibo 76.4% of 0.6825/0.8135 rally).

Falling 10 SMA marks solid resistance at 0.7390 (reinforced by the base of thick 4-hr cloud), where extended upticks should be capped to keep intact pivotal lower base at 0.7340 zone.

Res: 0.7362, 0.7390, 0.7407, 0.7423

Sup: 0.7322, 0.7283, 0.7268, 0.7200

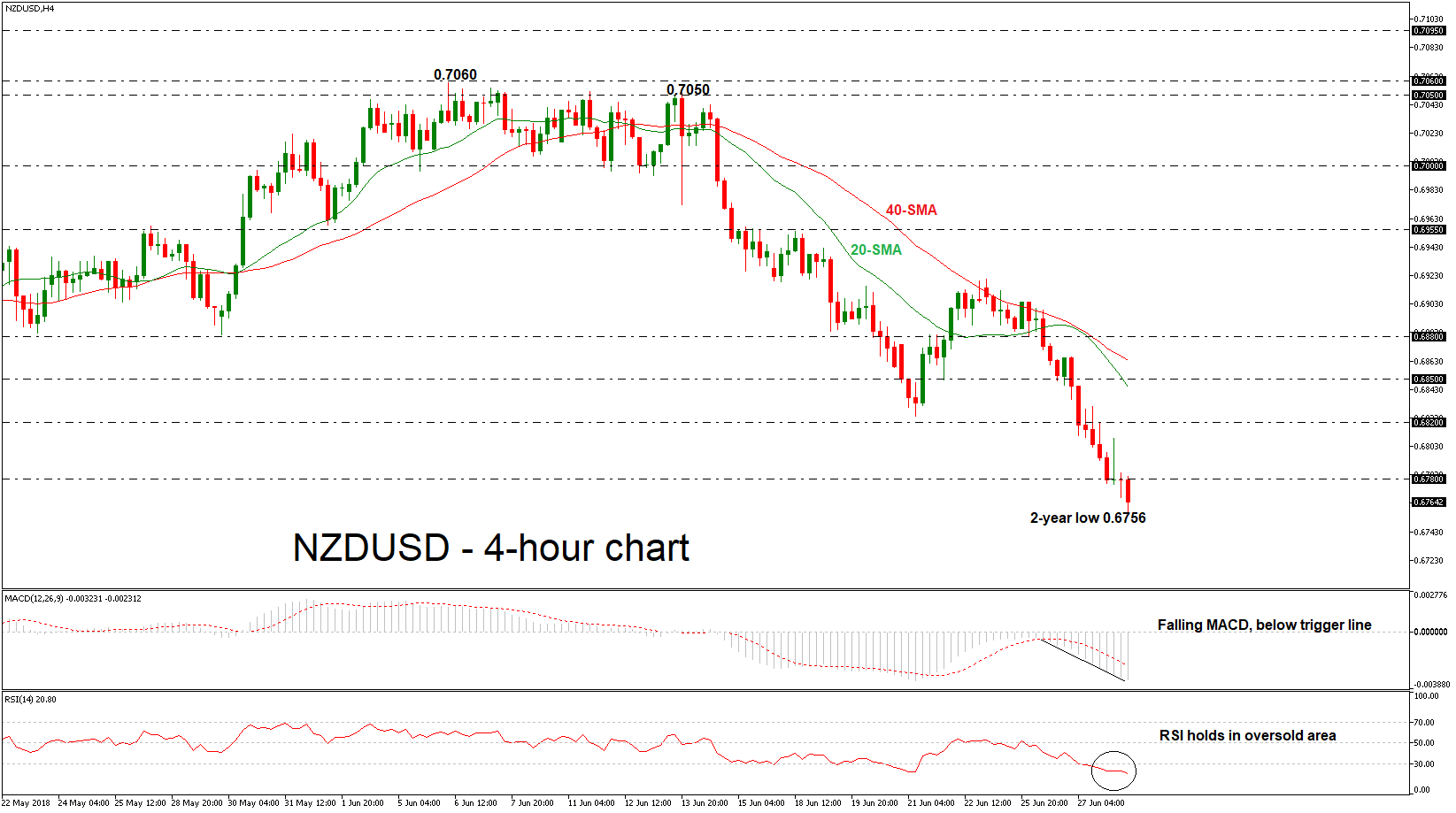

NZDUSD Plunges To 2-Year Low, Continues Dramatic Tumble

NZDUSD plummeted to a more than two-year low of 0.6756 during early Thursday’s session and is set to complete the fourth red day in a row. The aggressive bearish rally started after the bounce off the 0.7060 resistance level at the beginning of June and the bears seem to have full control of this market.

In the 4-hour chart, the RSI is currently increasing its negative momentum in the oversold zone, while the MACD is moving lower in the negative territory, both hinting that the next move in prices could be on the downside rather than on the upside.

Further bearish movement could drive the price towards the next major support level of the 0.6670 barrier, taken from the low on May 2016.

In case of an upward attempt, NZDUSD would likely meet resistance at the 0.6780 barrier, which stands slightly above the current market price. A break above this level would ease the downside pressure and touch the 0.6820 resistance.

In the bigger picture, the price remains in a bearish mode and is ready to post the third consecutive negative month. Also, the pair is developing below the 20- and 40-simple moving averages (SMAs) in all timeframes from short- to long-term.

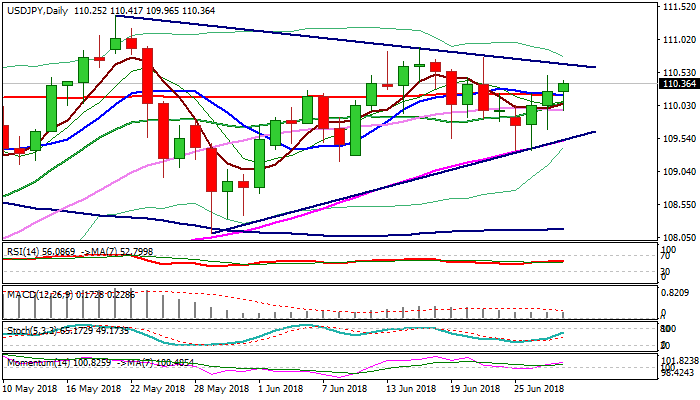

USDJPY Outlook: Bulls Show Hesitation Above 200SMA, Fundamentals Seen As Key Driver

The pair holds firm tone and trades above 200SMA in early Thursday's trading, but the upside was so far limited as dollar's bulls started to lose traction after comments from President Trump about tariffs on China were less harsh than expected. Bullish techs continue to underpin but fundamentals may weaken structure. In addition to trade war concerns, release of US Q1 GDP data could also influence dollar's performance. The GDP is expected to stay unchanged at 2.2% in Q1 which could signal stabilization after steady descend since October last year and support dollar on better than expected release. Bulls eye trendline resistance at 110.66, violation of which would generate initial bullish signal for test of 110.90 (15 Jun high) and open way for 111+ gains. Weekly close above 200SMA is needed to confirm scenario. Conversely, return and close below 200SMA (110.19) and psychological 110.00 support would generate negative signal and increase risk of further weakness.

Res: 110.49, 110.66, 110.90, 111.39

Sup: 110.19, 110.00, 109.70, 109.51

European Markets Continue To Slide | Gold Still Under Curse While Oil Having Cinderella Moment

- Little optimism about Trump's less harsh measure on Chinese investment

- Oil market is having more Cinderella moments than one could imagine

- Gold isn’t seeing any meaningful signs of life

European markets have failed to shake off the sell-off momentum from Wall Street, traders have shown little optimism about the Trump administration's less harsh measure on Chinese investment. The German July consumer confidence data has also provided more hopes as actual number (10.7) came ahead of the forecast (10.6). The euro currency still remains under pressure despite an upbeat reading on German consumer climate. Euro traders would be watching the ECB’s economic bulletin closely today. The ECB is set to wind up the quantitative easing program later this year and the economic bulletin would provide more aid for traders about the ECB's hawkish behaviour towards its monetary policy.

Furthermore, the unity between the EU leaders would be put to test when they will meet in Brussels today. There are many issues which will test the bloc’s unity. Germany would make sure that it isn’t the country which is sharing the economic burden while Italy would have to answer and confirm its stance on the immigration issue, especially given that the country refused to accept the ship full of immigrants.

The oil market is having more Cinderella moments than one could imagine. The WTI price touched multiyear high and now it has eased off as speculators decided to reduce their positions. This has created some weakness for the price. The open interest for crude oil market is still showing more positive outlook hence it is possible that the current weakness may not last for long. The situation over in Libya continue to remain unstable, government and rebels both struggling to gain more grounds and this instability is impacting the supply. From a technical point of view, we think the bull momentum is strong but the RSI is overbought zone and traders should take caution.

The precious metal isn’t seeing any meaningful signs of life as the dollar index has a strong influence. Only a weaker dollar index would bring the shine back for the metal. For now, there is only one clear trend for the dollar index which is skewed to the upside. The dollar index's strength is mainly powered by hopes for higher rates and rising yields and there seems to be no change in this any time soon.

Political and economic uncertainties aren't having any strong effects on the gold demand. In fact, looking through the lens of the political instability, things are much calmer after President Trump has softened its stance towards China. Having said this, the bitter US-China row could pick up steam anytime so we would not bank too much on Trump's current softening stance towards China.

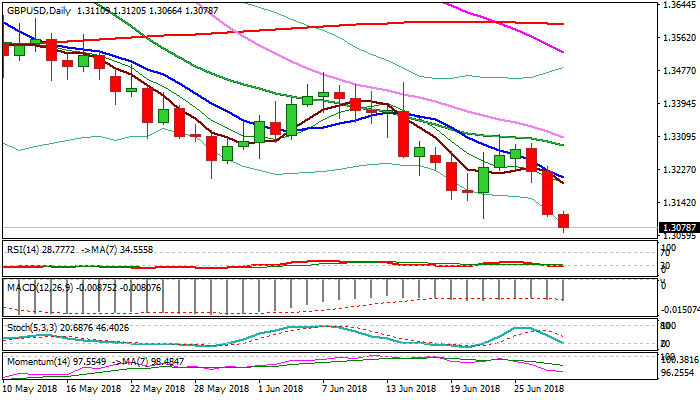

GBPUSD Outook: Break Of 1.3101 Pivot Pressures Nov Low At 1.3038 And Eyes Psychological 1.30 Support

Cable broke below key support at 1.3101 on Thursday, extending bear-leg from 1.33 zone into third straight day.

Strong bearish sentiment was boosted by comments from BoE’s Deputy Governor who offered no hints about vote for rate hike in August’s policy meeting.

Pound remains under pressure on concerns about the impact on Brexit as well as possibility that BoE may not increase interest rates this year.

Eventual break through 1.3101 pivot cracked weekly 100SMA (1.3071) and pressures support at 1.3038 (03 Nov 2017 low) violation of which would expose psychological 1.30 support. Bearish daily/weekly techs and negative sentiment support scenario, but bears may show hesitation at 1.30 support as studies are oversold.

Falling 10SMA (1.3204) is expected to cap corrective upticks and keep bears intact.

Res: 1.3101, 1.3120, 1.3150, 1.3204

Sup: 1.3066, 1.3038, 1.3026, 1.3000

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

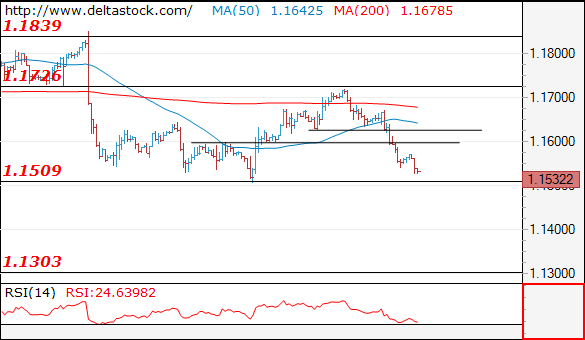

EUR/USD

Current level - 1.1532

While 1.1509 is intact, there is still a chance for another corrective leg towards 1.1670 area. A violation of 1.1509 will expose 1.1300 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1600 | 1.1730 | 1.1510 | 1.1510 |

| 1.1670 | 1.1830 | 1.1510 | 1.1300 |

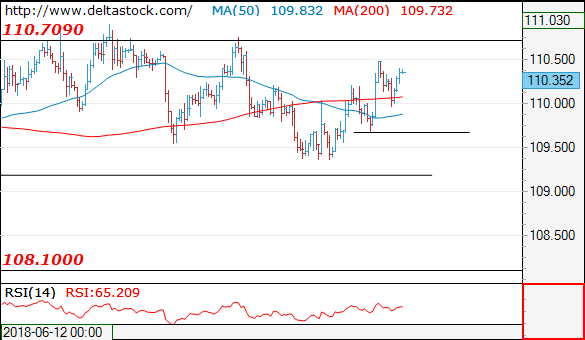

USD/JPY

Current level - 110.35

My outlook is counter-trend, for a reversal and slide towards 109.20. Crucial on the upside is 110.70-90 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 110.80 | 111.40 | 109.70 | 107.80 |

| 111.40 | 114.40 | 108.60 | 106.70 |

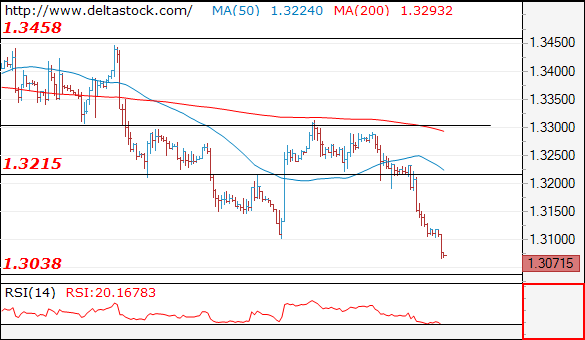

GBP/USD

Current level - 1.3071

The break through 1.3100 low shows a renewal of the general downtrend, towards 1.3040 and 1.2980. Initial resistance lies at 1.3100, followed by 1.3200 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3100 | 1.3618 | 1.3040 | 1.3040 |

| 1.3200 | 1.3990 | 1.2980 | 1.2770 |

ECB: Rise in protectionism could be significant risks to global activity

In its monthly bulletin, ECB noted that "euro area economic expansion remains solid and broad-based across countries and sectors, despite recent weaker than expected data and indicators." In the June Eurosystem macroeconomic projections, annual real GDP growth is projected to be at 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020.. HICP inflation is projected to be at 1.7% in 2018, 2019 and 2020.

On the global scale, ECB noted, that "following a year of strong and highly synchronised growth, global momentum slowed somewhat in the early part of 2018." While, growth is expected to rebound in near term, it warned that "the implementation of higher trade tariffs, amid ongoing discussions of further protectionist measures, represents a risk to the global economic outlook."

The US steel and aluminium tariffs so far "affect only a small proportion of global trade and are expected to have only a small global macroeconomic effect". However, "the risks of further protectionist steps have risen". Firstly, US "threatened to increase tariffs on USD 50 billion of Chinese goods, to which China pledged to retaliate. Secondly, "the United States launched an investigation into the national security implications of automobile imports."

ECB added that "expectations of an escalation in the dispute could affect investment decisions, with potential effects on global growth". And, "risks to global activity from a widespread rise in protectionism could be significant."

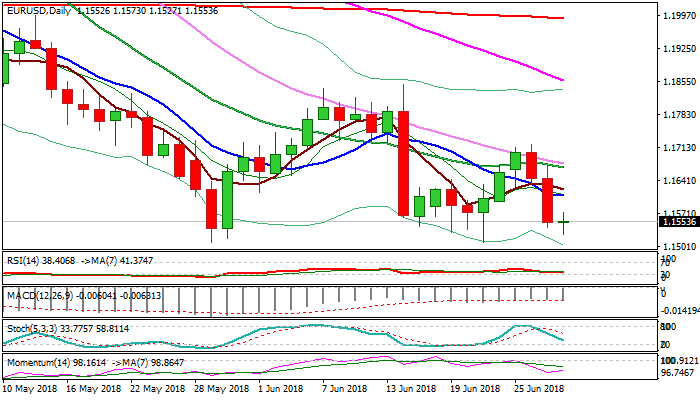

EURUSD Outlook: Break Through 1.1509/08 Base Could Spark Stronger Bearish Acceleration

The Euro remains in red on Thursday and extends descend from week's high at 1.1720, pressuring key supports at 1.1509/08 (29 May/21 Jun lows). Steady dollar keeps the single currency under pressure which could intensify on political complications in Germany. Wednesday's close below falling 10SMA turned daily MA's in full bearish configuration, with growing bearish momentum and overall negative sentiment for the single currency, signaling further weakness. Bearish engulfing pattern is forming on weekly chart which could increase pressure on Euro. Eventual break below 1.1509/08 base would open way for test of Fibo support at 1.1447 (50% retracement of larger 1.0340/1.2555 ascend and 1.14 zone in extension. Meanwhile, bounces on month-end profit taking could be anticipated. Upticks are expected to offer better positions ahead of fresh weakness as sentiment could sour further if political situation in Germany intensifies. Broken 10SMA offers initial resistance at 1.1610, while stronger upticks should be capped by falling 20SMA (1.1670).

Res: 1.1573, 1.1610, 1.1622, 1.1670

Sup: 1.1527, 1.1508, 1.1447, 1.1400