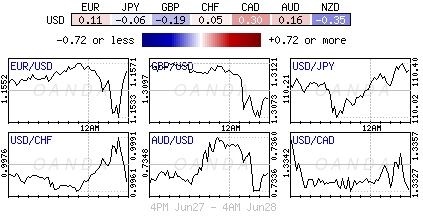

Sample Category Title

US Core PCE Projected Within Breathing Distance Of Fed Inflation Target

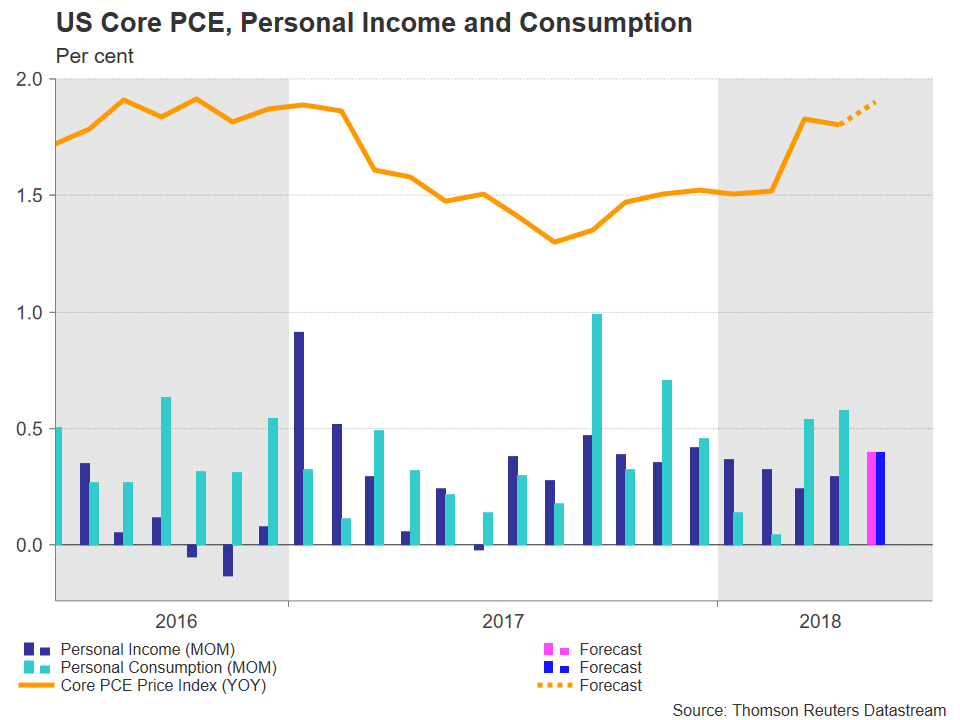

US data on May's core personal consumption expenditure (PCE) price index – this being the Federal Reserve's preferred inflation gauge – are due out on Friday at 1230 GMT, alongside numbers on personal income and consumption. A beat on the inflation front is likely to more conclusively put on the table two additional interest rate increases by the US central bank in 2018, consequently supporting the greenback.

The core PCE price index, that excludes volatile food and energy items and which is targeted by the US central bank, is anticipated to grow by 0.2% m/m, the same pace as in April. This would put the year-on-year growth rate at 1.9%, a tick higher compared to April, and bring the measure even closer to the Fed's target for annual inflation of 2%. Meanwhile, the figure on personal income is forecast to expand by 0.4% m/m, this reflecting an acceleration relative to April's 0.3%, while consumption is expected to slow down to 0.4% m/m, from 0.6%.

Despite the mean projection by FOMC policymakers during the latest meeting by the Fed calling for four 25bps rate increases in total for 2018 – i.e. two additional hikes during H2 2018 – the markets have not priced in such an outcome at the moment. Specifically, Fed funds futures indicate that market participants have fully discounted an additional rate increase in 2018, while they assign a 28% probability for a second one to materialize. A stronger-than-expected core PCE print is anticipated to bring investors closer to the mean view of two more rate hikes held by FOMC members, something which is supportive of a rising dollar.

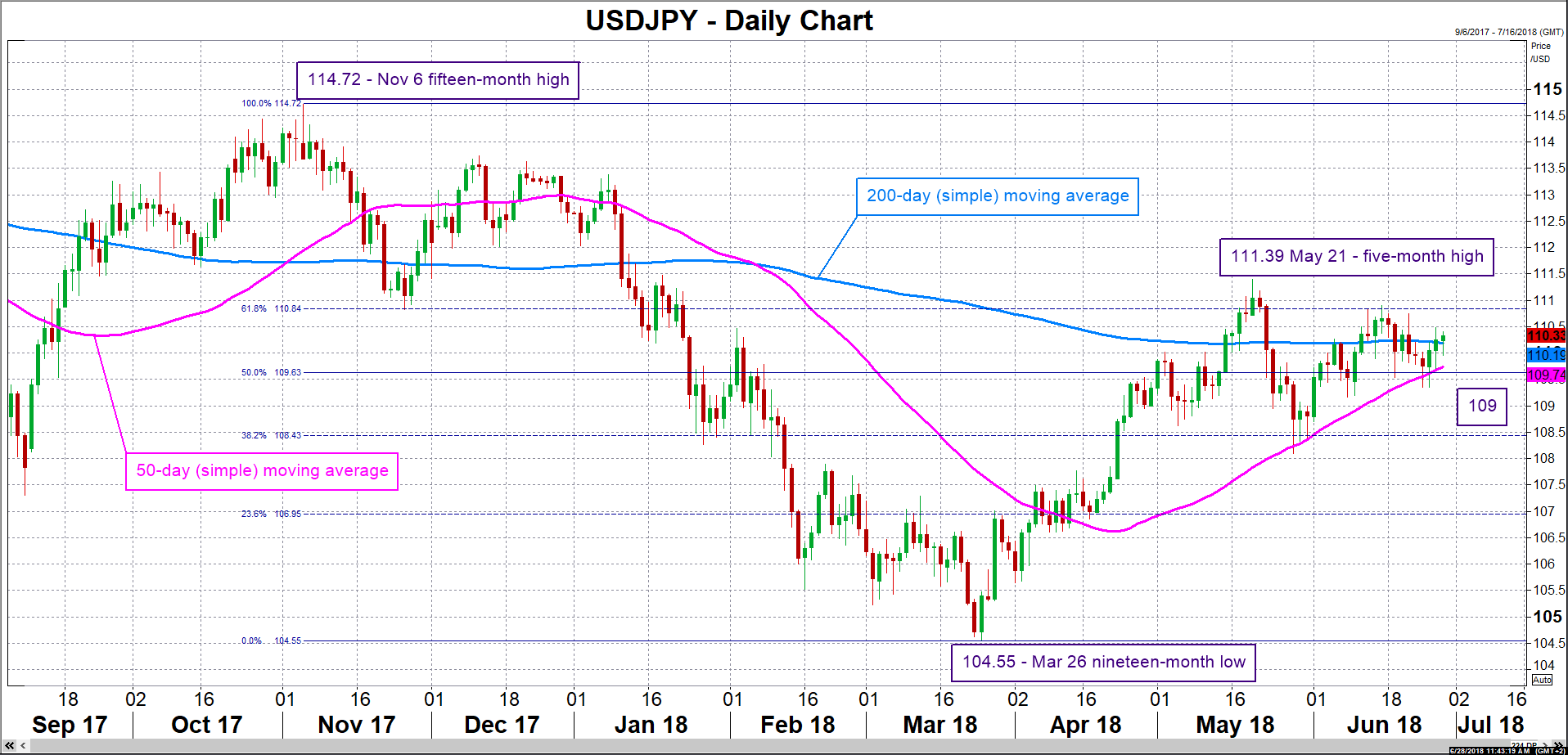

In terms of market reaction and focusing on dollar/yen, an advancing pair on the back of readings that positively surprise may meet resistance around the 61.8% Fibonacci retracement level of the November 6 to March 26 downleg at 110.84, with the region around it encapsulating the 111 round figure as well. This is of course predicated on a conclusive break off the current level of the 200-day moving average line at 110.19 taking place first. Stronger gains would turn the focus to the five-month high of 111.39 and then to the 112 handle. On the downside and in case of a data miss, support could come around the 50% Fibonacci point at 109.63; notice that the 50-day MA at 109.74 is also part of the region around this mark. More bearish movement would shift the focus to the 109 handle.

Briefly looking at other measures of US price pressures, headline CPI beat analysts' forecasts to increase by 2.8% y/y in May, its fastest since early 2012, while core CPI, which similar to the core PCE excludes food and energy from its calculations, also recorded stronger growth in May, rising by 2.2%, from 2.1%.

Turning back to USDJPY, it should be kept in mind that besides economic releases, flows on the back of developments relating to global trade can also move the pair. In particular, escalating tensions between the US and its trading partners are likely to divert funds to the safe-haven perceived yen, weighing on the pair, and vice versa.

Lastly, final estimates on Q1 GDP growth in the world's largest economy are projected to confirm growth standing at 2.2% on an annualized basis during the quarter. The numbers are scheduled for release today at 1230 GMT.

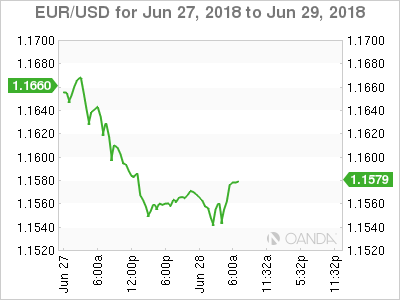

Eurozone’s Inflation Prints Due As EU Summit Casts Shadow

The Eurozone will see the release of its preliminary inflation data for June on Friday, at 0900 GMT. Forecasts point to another slight acceleration in prices pressures, which although may be energy-driven would still enhance the narrative that inflation is moving in the desired direction, potentially helping the euro recover some of its recent losses. Besides the data, the outcome of the EU summit could also prove crucial for the common currency's fortunes.

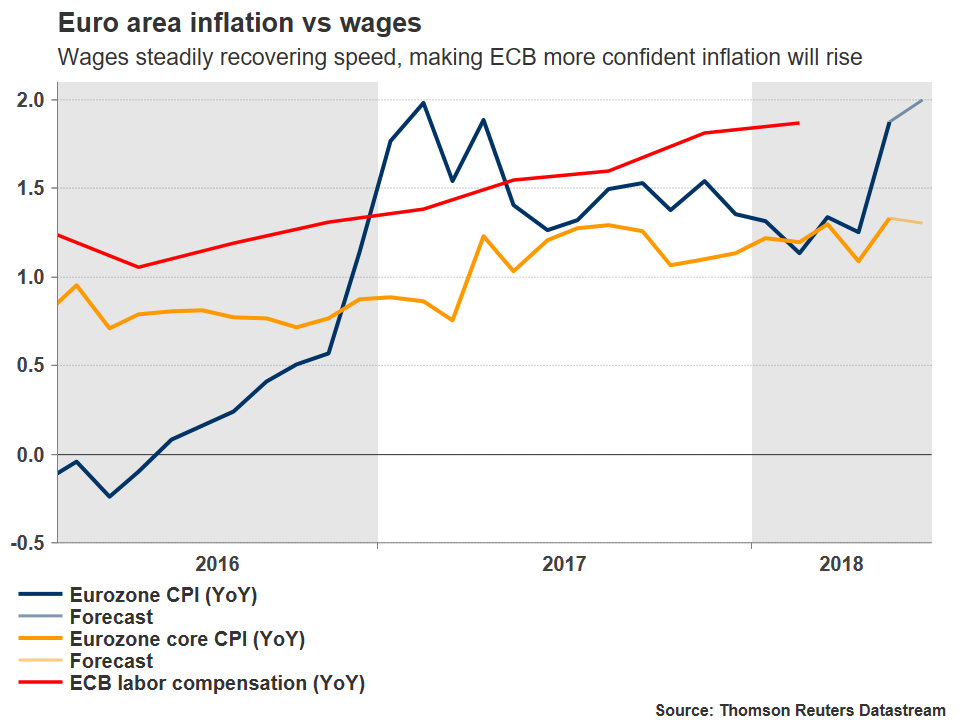

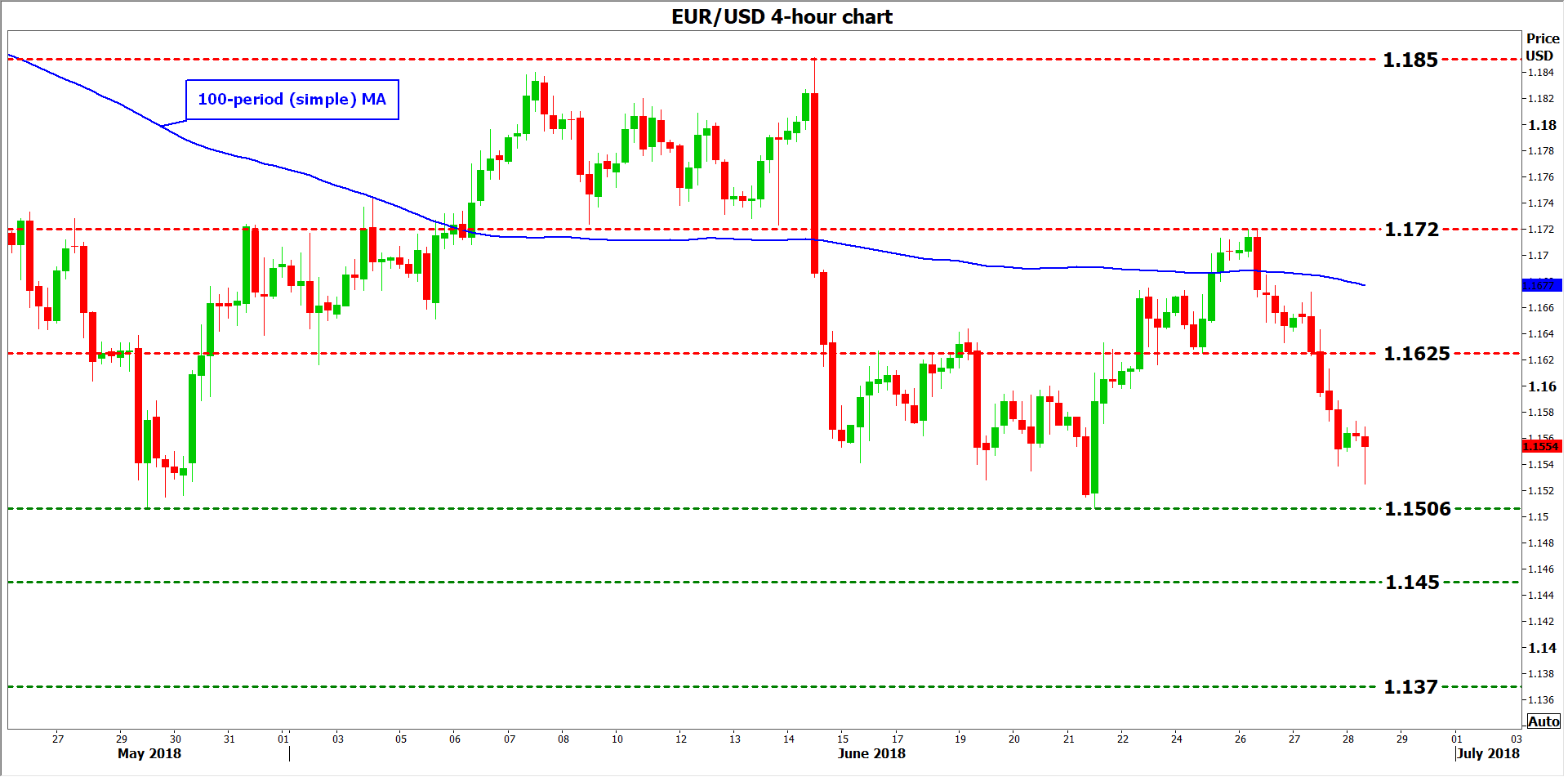

The common European currency stabilized somewhat in recent weeks, with euro/dollar oscillating in a range between 1.1506 and 1.1850 so far in June. While Italian political risks eased somewhat, helping the euro to post a small relief rally, the European Central Bank (ECB) appeared dovish at its June policy meeting, triggering a renewed selloff. Although the Bank announced an end-date to its QE program – noting increased confidence that inflation will move higher amid solid economic performance and a pickup in wages – it also stressed interest rates will remain unchanged for at least another year, dampening expectations for any aggressive moves.

The key takeaway was that the ECB will move ultra-cautiously towards normalizing policy, and that its actions are highly dependent on its economic forecasts materializing, implying that any sharp deterioration in Eurozone data has the capacity to delay, or even derail, such plans. This puts even more weight than usual on upcoming data, and most notably on the bloc's inflation prints.

In June, the Eurozone's preliminary CPI rate is projected to have ticked up to 2.0% in yearly terms, from 1.9% back in May. This would bring it above the ECB's target of “below, but close to, 2%”. That said, the core CPI rate – which excludes volatile food and energy items – is expected to have held steady at 1.3%, signaling that the acceleration in the headline print may be owed primarily to energy effects. Importantly, the ECB typically “looks through” energy-induced movements, as it considers them transitory effects that will fade over time and should thus not influence policy decisions.

As for gauges of inflationary pressures, the bloc's Markit Composite PMI showed that average selling prices for goods and services rose at the third-fastest pace in the last seven years in June. In isolation, this suggests an upside surprise in the CPIs may be somewhat more likely than a downside one.

Technically, looking at euro/dollar, resistance to advances may be found around 1.1625, defined by the inside swing low on June 25. A potential upside break could open the way for 1.1720, the high of June 26, with even further bullish extensions bringing into scope the June 14 peak of 1.1850.

On the downside – in case a negative surprise in the CPIs generates speculation for an even more cautious ECB – immediate support to declines could come near the 11-month low of 1.1506, posted on May 29. Even lower, attention could shift to the 1.1450 zone, marked by the peak of 29 June, 2017. A downward violation would increasingly bring into view the 1.1370 area, identified by the lows of 13 July, 2017.

Finally, besides the inflation data, the other major theme that could impact price action in euro/dollar is the EU summit that will conclude on Friday. German Chancellor Merkel's fragile coalition government is at risk of collapsing should she return home without a deal on immigration, potentially sending Europe's largest economy to early elections. Any signs of political instability in Germany could act as a drag on the euro, and vice-versa.

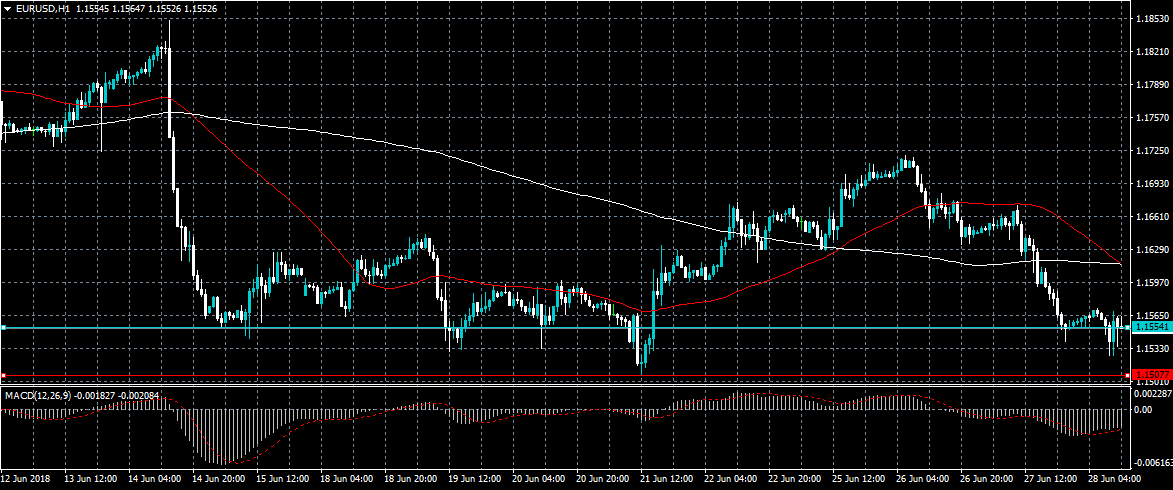

EURUSD Strongly Bearish Below 1.1554

The euro continues to fall against the greenback on Thursday, with the EURUSD pair earlier touching a fresh weekly trading low, at 1.1526, as the US dollar index climbs towards the 95.50 level. Downside pressure is building on the EURUSD pair across numerous indicators, with further intraday losses increasingly likely. Sellers will target below the 1.1507 level for further losses, while buyers will try to defend the key 1.1554 level.

The EURUSD pair is strongly bearish while trading below the 1.1554 level, key intraday support is located at the 1.1507 and 1.1458 levels.

If EURUSD buyers hold price back above the 1.1554 level, a correction back towards the 1.1580 and 1.1600 levels is possible.

USDJPY Only Intraday Bullish Above 110.00

The US dollar has moved above the key 110.00 level against the Japanese yen, hitting 110.48, on reports that Chinese investments inside the American economy will not be facing taxes from the US administration. The USDJPY pair is also receiving a boost from broad-based strength in the US dollar index. Sellers will look to move price below the 110.00 level, while buyers will look to break the 110.48 level and advance the rally towards the 111.00 level.

The USDJPY pair is intraday bullish while trading above the 110.00 level, further upside towards the 110.78 and 111.00 levels seems possible.

If the USDJPY pair moves below the 110.00 level, key support is found at the 109.54 and 109.00 levels.

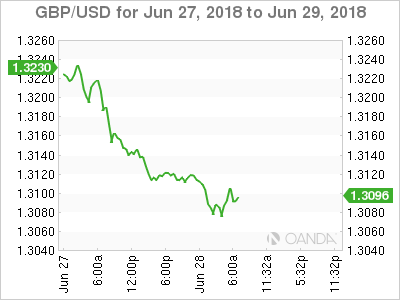

Forex Analysis: GBPUSD

The GBPUSD pair is continuing its decent lower and has reached a low of 1.30664 today just above support at 1.30586. The next level of support is 1.30000 which is a big psychological level for traders that will see buyers emerge t defend the level. The likelihood of sellers taking profit in this area also exists and can see the price bounce from the channel bottom back towards 1.32000. The GBPUSD was weal yesterday despite trade headlines with the down trend being maintained.

Resistance can be seen at 1.32246 and the channel top at 1.33745 with a break above this area giving long traders confidence of a move to test 1.34594. A above this level the moving averages come into play with the 50 DMA at 1.34412 and the 200 DMA at 1.35228 followed by the 100 DMA at 1.35630. From here the next level of resistance is 1.36135 followed by 1.37117 which is the February low.

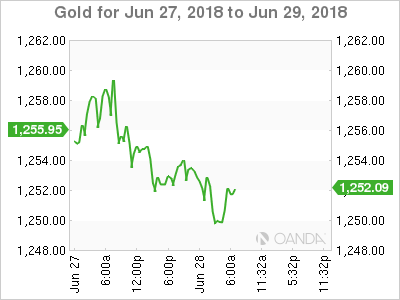

Forex Analysis: Gold

The gold chart has played out as a double top with a break under 1300.00 signalling a move down to 1240.00 from its highs at 1365.00. We have now reached the 1250.00 area and some profits are likely to be taken from here on down. Should 1240.00 be broken support can be found at 1236.45 followed by 1229.40. Below this area a drop to 1200.00 could be forecasted with 1204.50 on the way as satellite support.

Resistance above the current level comes in at 1265.25 with the descending blue trend line at 1271.50. A break out higher would give long traders a chance to enter or add to their positions provided 1276.95 is cleared. At this point 1300.00 becomes a target with 1289.45 and the 50 DMA at 1293.44 providing resistance. The rising red trend line should reach 1300.00 before price encounters the level and can provide additional interest at that point. The 200 DMA is sitting on 1300.00 and the move under this MA by the 50 DMA provided a death cross for the chart last week. The 100 DMA at 1302.80 is in danger of following suit.

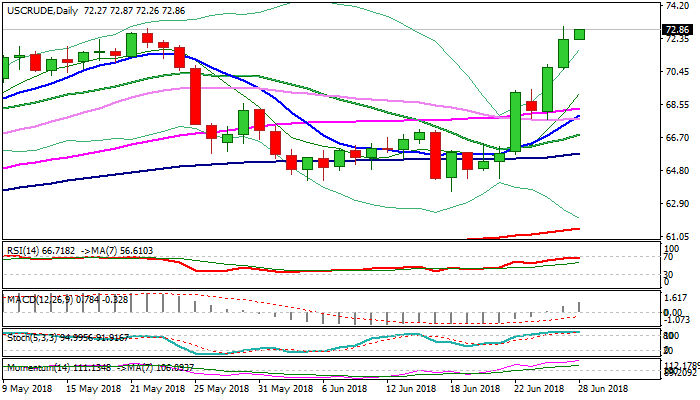

WTI OIL Outlook: Oil Price Could Extend Rally Towards $76.35 Fibo Barrier On Sustained Break Above $72.89 Pivot

WTI oil is consolidating under new high at $73.04 (the highest since Nov 2014) on Thursday, taking a breather after steep five-day rally fully retraced $72.89/$63.58 correction leg and signaled continuation of larger uptrend from $26.04 (Feb 2016 low).

Oil price advanced strongly in positive environment as output shortage from Libya and Venezuela, sanctions on Iran’s oil export and unexpected supply reduction from Canada were among key factors that boosted oil price.

In addition, lower than expected output increase from OPEC and non-OPEC key oil producers, further supported bulls along with upbeat US crude inventories, which showed over 9 million barrels draws last week (API and EIA reports) and heavily beating forecasts.

Oil maintains strong bullish momentum which could drive the price higher. Close above previous high at $72.89 is seen as initial requirement as Wednesday’s spike to new high at $73.04 was short-lived and failed to close above $72.89 pivot at initial attempt.

Sustained break above $72.89 would open $74.94 (04 Oct 2011 low) and could challenge next key barrier at $76.35 (Fibo 61.8% of $107.45/$26.04 2014/2016 fall in extension, break of which would expose psychological $80 barrier.

No firmer signs of corrective action for now despite overbought conditions on daily chart, but repeated failure to close above $72.89 could be initial signal of correction.

Solid supports at $70.00/$69.50 zone should keep the downside protected.

Res: 73.04, 74.94, 76.35, 78.64

Sup: 72.26, 71.72, 70.81, 70.00

Markets Remain Under Pressure On Trade Concerns

- Investors remain cautious despite brief bounce on Wednesday;

- EU summit eyed as Merkel hopes for unified solution on immigration issue.

It's been a relatively slow start to trading on Thursday and, as has been the case for most of the last week, investors remain fixated on trade disputes which continues to weigh on risk appetite.

Once again European indices are trading in the red early in the session, while US futures are pointing to a flat start after selling off on Wednesday afternoon. Donald Trump and members of his administration may have cleared up reports regarding Chinese investment in US tech firms which appeared to give stocks a temporary boost but it didn't last very long and investors were quickly reverting back to risk aversion mode.

With Trump picking fights on multiple fronts and no sides showing any willingness to back down, we may have to get used to this risk averse environment in the near-term. Markets have a tendency to move on though if we go a few weeks without any further escalation and gradually become less sensitive to the rants and reactions of those involved.

There are some data releases today which may provide a small distraction to the trade spats, with the final US first quarter GDP number being released alongside weekly jobless claims. We'll also hear from a couple of Federal Reserve policy makers which will be of interest given the central bank's recent revision to its forecasts for interest rate hikes this year.

The European Union has its own problems to deal with right now and Trump is not making Angela Merkels life any easier there either. An EU summit today is likely to focus on the issue of immigration, with the new populist Italian government adopting a tough stance on those attempting to make the trip from Libya, forcing other countries to step in and accept the rescue ships.

It's not just the Italian government that adopting such a tone, Angela Merkel's own coalition is at risk of falling apart over the issues, meaning a rare period of uncertainty for what has been a very stable and important country in the eurozone over the last decade. Given the differences that exist, it's hard to see the countries coming to an agreement on the issue which could lead to further political instability in the block.

EU Malmstrom: To take provisional safeguard measures for steel industry starting mid-July

EU Trade Commissioner Cecilia Malmstrom said there could be provisional safeguard measures for the steel industry starting mid-July. The European Commission is still in process of investigation the measures needed after US steel and aluminum tariffs.

Malmstrom said "this is an investigation that will probably take until the end of the year before we can get the full picture." But she emphasized that "we are seriously contemplating to have provisional measures in place, I would say mid-July could be some provisional measures. Exactly what form that will take is still under discussion."

Separately, UK International Trade Minister Liam Fox said separately in the parliament that "we are looking to see what impact there may be from any diversion and whether we need to introduce safeguards to protect UK steel producers." And, "the earliest time that is likely to happen would be early to mid-July. We are already seeing some movements that I think may justify that." He added that "as soon as we have the evidence to be able to justify such a decision, we would take it."

Dollar Rises To New Heights Against G10 And EM Pairs

Thursday June 28: Five things the markets are talking about

Global equities remain on the back foot as investors continue to come to terms with the U.S Whitehouse's strategy towards Chinese investments. After some confusion, the Trump administration has re-established its hardline stance on trade.

The U.S dollar has again found traction against its G10 peers, while EM currency pairs made a rough go of it in the overnight session.

U.S Treasuries have edged lower for their first drop in more than a week, while China's yuan fluctuated within a tighter range after its longest run of losses in years.

Note: Allowing the currency to fall is not only a sign that the PBoC is pursuing an easier policy stance but an admission of economic vulnerability.

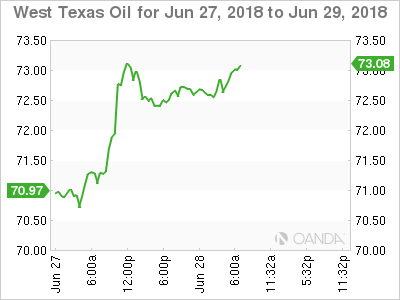

In commodities, West Texas Intermediate crude handed back some gains after yesterday hitting the highest in more than three-years.

On tap: The European economic summit begins today, while U.S personal spending is expected to have increased for a third consecutive month tomorrow. On Saturday, China manufacturing and non-manufacturing PMI are due.

1. Stocks see ‘red'

Japan's Nikkei closed little changed, but trades atop of its one-month low overnight, taking direction from the weakness stateside as a Sino-U.S trade row hurts investor risk appetite. The Nikkei eased -0.1%, its weakest close this month. Meanwhile, the broader Topix dropped -0.3%, the lowest closing level since mid-April.

Down-under, Aussie stocks faded late and left the S&P/ASX 200 with a fourth consecutive slight decline. It fell -0.01% overnight, falling a cumulative -0.6% during this down streak. Weighing overnight were the financial, industrial and telecom sectors. In S. Korea, the Kospi was down -1.19%.

In Hong Kong, stocks slid to a new seven-month low overnight, as a sharp fall in the yuan added to worries about China's economic growth amid escalating U.S.-China trade tensions. The Hang Seng index fell -1.8%, while the China Enterprises Index lost -2.2%.

In China and Hong Kong stocks again were pressured on lingering trade war fears and a depreciating yuan. The CSI300 index fell -1.2%, while the Shanghai Composite Index lost -0.5%. The Hang Seng index dropped -0.6%, while the Hong Kong China Enterprises Index lost -1.0%.

In Europe, regional bourses are under pressure ahead of the U.S open. Consumer discretionary leads performers, while materials are underperforming.

U.S stocks are set to open in the ‘black' (+0.2%).

2. U.S crude prices steady ahead of Iran sanctions, gold lower

U.S. oil prices steadied this morning, pulling back from their four-years highs, but supply remains tight with investors concerned by the prospect of a big fall in crude exports from Iran due to U.S sanctions.

U.S light crude (WTI) is -15c lower at +$72.61 per barrel, after hitting +$73.06 on Wednesday, its highest since November 2014, while the benchmark Brent was unchanged at +$77.62 a barrel.

The U.S this week demanded that all countries halt imports of Iranian oil from November, a hardline position the Trump administration hopes will cut off funding to Iran.

The move follows a decision by OPEC last week to increase production to try to moderate oil prices that have rallied more than +40% over the last year.

Note: Oil prices have rallied for much of this year on tightening market conditions due to record demand and voluntary supply cuts led by the Middle East dominated OPEC producer cartel. Unplanned supply disruptions from Canada to Libya and Venezuela have added to those cuts.

Gold prices hit their lowest in more than six months earlier this morning as the U.S dollar held near its one-year highs amid mounting Sino-U.S trade friction. Spot gold is down -0.2% an ounce.

Note: Earlier in the session, the bullion touched +$1,248.25, its lowest since mid-December. U.S gold futures for August delivery dropped -0.4% at +$1,251.20 an ounce.

3. Yields are flattening sovereign curves

Down-under yesterday, the Reserve Bank of New Zealand (RBNZ) left its Official Cash Rate unchanged at +1.75% (as expected). Policy makers reiterated their view that they “expected to keep rate at this expansionary level for a considerable period of time.” Monetary policy to be supportive for some time to come as CPI remains below target.

Elsewhere, the yield on 10-year Treasuries climbed +1 bps to +2.84%, the first advance in more than a week. In Germany, the 10-year Bund yield gained +1bps to +0.33%, while in the U.K 10-year Gilts Britain's 10-year yield increased +1 bps to +1.251%.

4. Dollar rises to a one-week high vs. EUR, EM currencies drop

The U.S dollar continues to rise this morning, reaching a one-week high against the EUR, taking EUR/USD to a low of +$1.1527, while emerging market currencies come under more selling pressure. Extracts of June inflation data for Germany and Spain showed CPI just above the ECB target level for the second consecutive month.

GBP/USD (£1.3100) remains within striking distance of its seven-month lows as E.U leaders began a 2-day summit with Brexit clarity as one of the main topics

USD/ZAR is up by +0.9% at $13.98, though the rand is also hit by domestic politics, with USD/ZAR having hit a seven-month high earlier.

USD/CNY continues to rise further, last up 0.2% at +6.6169.

5. Eurozone business confidence holds up

Eurozone businesses remained upbeat about their prospects in June, even as new tariffs were imposed on trade between the E.U and the U.S.

The E.C indicated that the measures of confidence among manufacturers and service providers was unchanged last month, while a drop in consumer sentiment led to a decline in its Economic Sentiment Indicator–an aggregate measure of consumer and business confidence – to 112.3 from 112.5 in May.

The ECB should be happy after expressing concerns that the threat of greater protectionism could make businesses more cautious in both their investment and hiring plans.

It also suggests that a period of slowing growth may be coming to an end.

The ECB's economists earlier this month cut their growth forecast for this year in response to a weak German Q1, but policy makers nevertheless said they expect to end QE in December.