Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.81; (P) 110.15; (R1) 110.61; More...

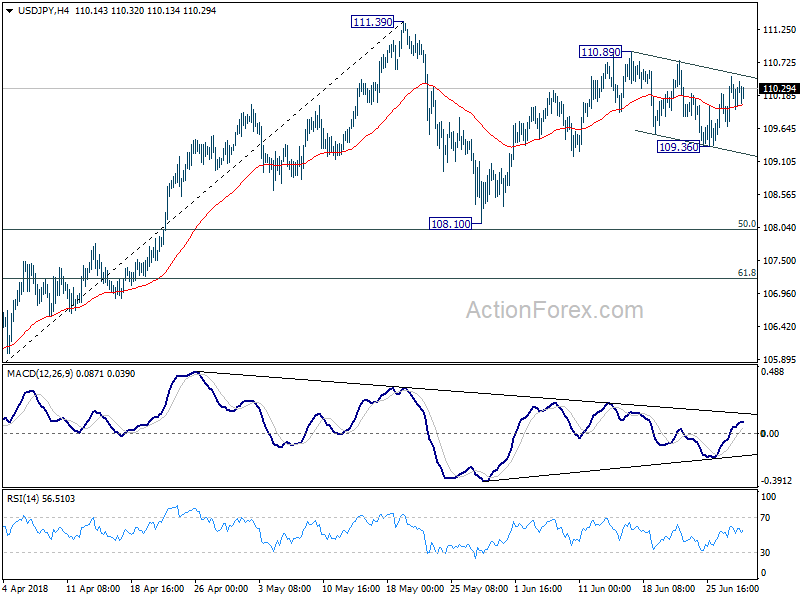

USD/JPY is staying in the sideway pattern from 110.89 and intraday bias remains neutral first. On the upside, break of 110.89 will resume the rise from 108.10 and target 111.39. Firm break there will resume the rally from 104.62 and target 114.73 key resistance. On the downside, below 109.36 will resume the fall from 110.89. In that case, as price actions from 111.39 are seen as a corrective pattern, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound.

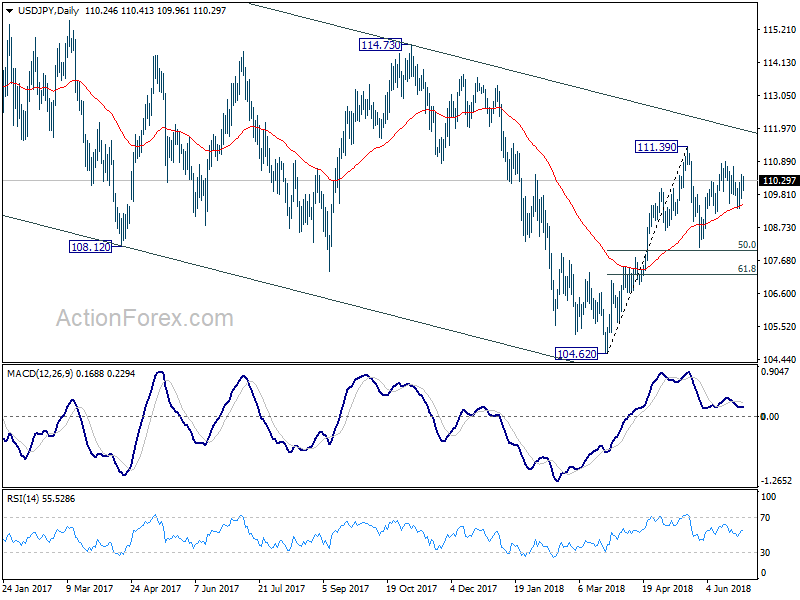

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1505; (P) 1.1590 (R1) 1.1638; More.....

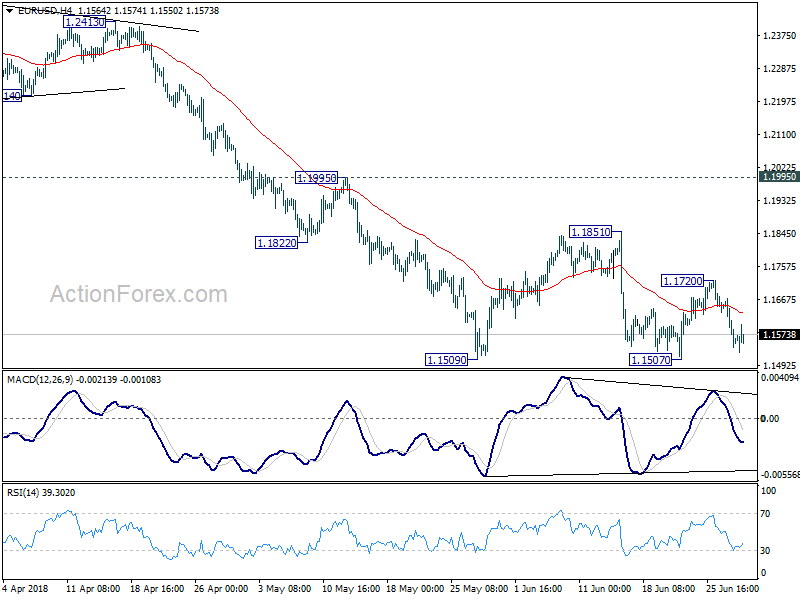

Intraday bias in EUR/USD is turned neutral as it just recovered ahead of 1.1507 low. More consolidations could be seen but upside of recovery should be limited by 1.1851 resistance. On the downside, firm break of 1.1507 will resume whole fall from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

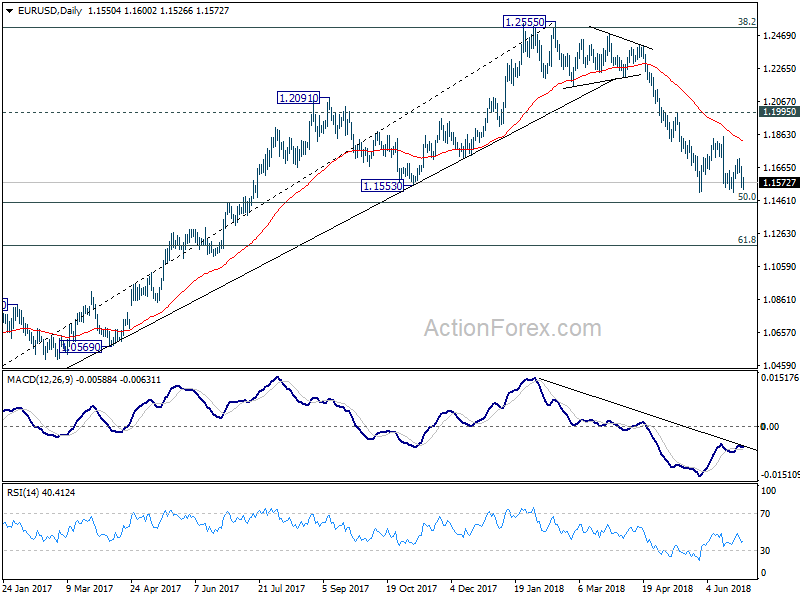

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

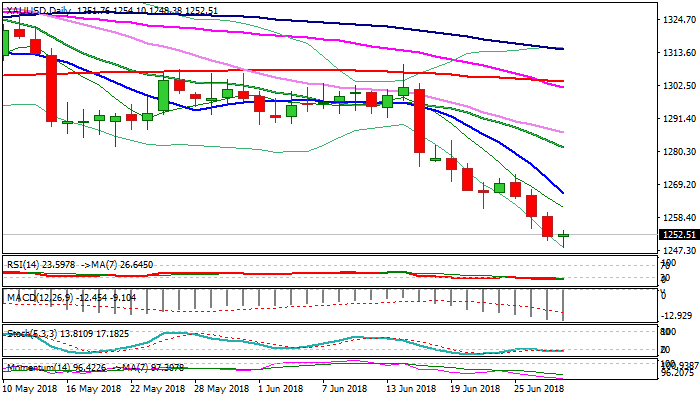

XAUUSD Outlook: Profit-Taking May Delay Bears for Final Push Towards $1236 Target

Spot Gold is holding within tight consolidation above new over six-month low at $1248 posted today, with oversold daily studies suggesting gold price may enter consolidative / corrective phase in coming sessions.

Steep fall from lower top at $1309 (16 Jun) may take a breather before final push towards target at $1236 (12 Dec low).

Stronger dollar on renewed risk-on mode keeps gold price under pressure, but profit-taking and oversold studies may push the price higher before bears resume.

Bullish divergence on daily slow stochastic supports the notion, however, strong bearish momentum suggests limited corrective action.

Solid barriers provided by falling 10SMA ($1266) and top of weekly cloud ($1276) are expected to cap.

Only return above descending 20SMA ($1281) would sideline bears and risk stronger correction.

Res: 1254; 1260; 1266; 1272

Sup: 1248; 1240; 1236; 1231

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3066; (P) 1.3154; (R1) 1.3203; More...

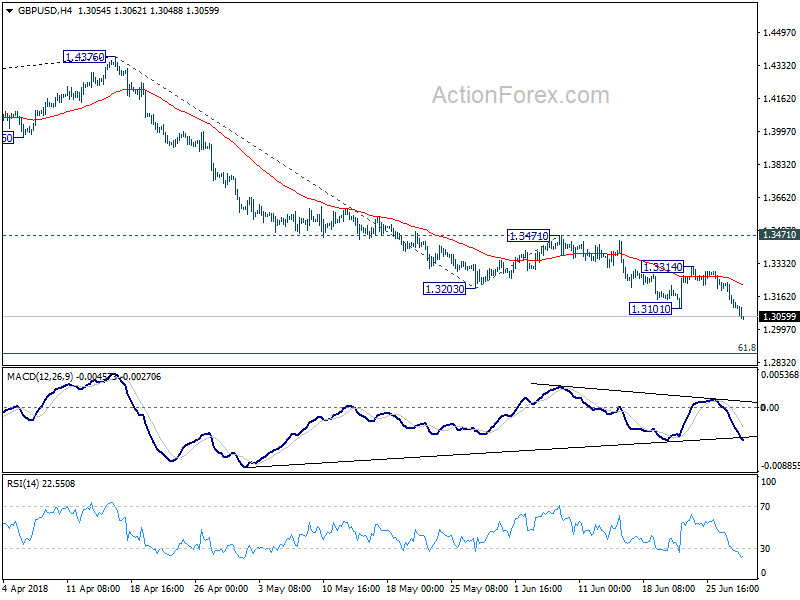

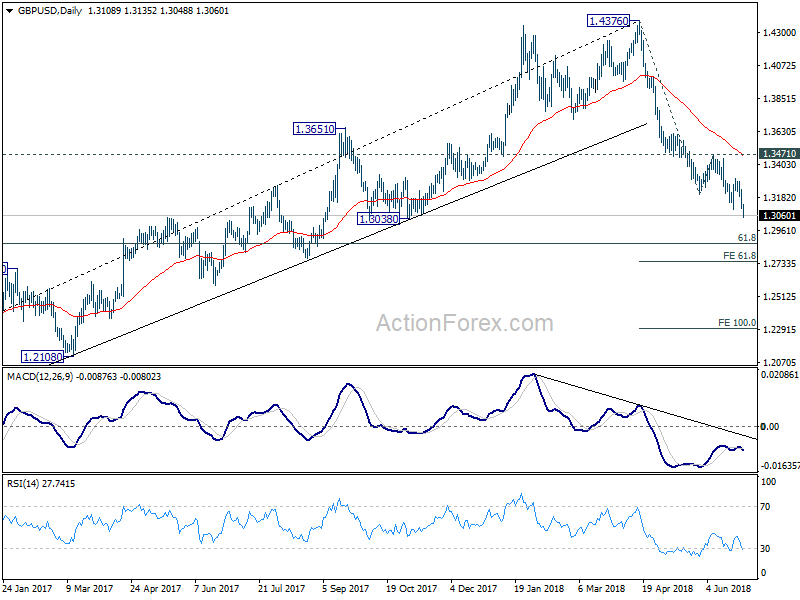

GBP/USD drops to as low as 1.3048 so far today. Solid break of 1.3101 indicates resumption of larger decline from 1.4376. Intraday bias stays on the downside for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. Break there will target 61.8% projection of 1.4376 to 1.3101 from 1.3471 at 1.2683 next. On the upside, break of 1.3314 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Sterling Downside Breakout Against Dollar and Euro, Risk Aversion Stays

Risk aversion continue to be a main theme in the markets, ahead of quarter end. At the time of writing, major European indices are trading in red. DAX leads again by losing -1.27%, CAC down -0.76% and FTSE down -0.44%. DOW futures also point to more losses. Oil prices continue recent rally after making four year high. WTI crude is currently at 72.5 after marginally missing 73 handle. Spot gold is trying to defend 1250 but strengthen is non-existing so far.

In the currency markets, Canadian Dollar is trading broadly higher today, with help from oil price. The Loonie is followed by Euro as EUR/USD recovers ahead of 1.15 support. EUR/GBP also finally breaks out of month long range. New Zealand Dollar is trading as the weakest one for today after dovish RBNZ, followed by Sterling. For the week, though, Dollar remains the strongest one, followed by Yen. Nonetheless, at the other hand, Kiwi and the Pound are still the weakest.

Technically, GBP/USD's solid break of 1.3101 support confirm resumption of recent decline from 1.4375. It should now head to 1.2875 fibonacci level. EUR/GBP's break of 0.8844 also indicate resumption of rise from 0.8620 and should target 0.8697 resistance next. While EUR/USD recovered ahead of 1.1507, there is no follow through buying. Focus will remain on this support, and break could trigger more broad based rally in the greenback. USD/CHF's 0.9989 minor resistance will also be watched.

US initial jobless claims rose 9k to 227k. Q1 GDP revised down to 2.0%

US initial jobless claims rose 9k to 227k in the week ended June 23, above expectation of 220k. Four week moving of initial claims rose 1k to 221k. Continuing claims dropped -21k to 1.705m in the week ended June 16. Four week moving average of continuing claims dropped -3.75k to 1.7195. This is the lowest level since December 1973.

Q1 GDP growth was finalized at 2.0%, revised own from 2.2% and missed expectation of 2.2%. GDP price index was revised up to 2.2%, from 1.9%.

EU Malmstrom: To take provisional safeguard measures for steel industry starting mid-July

EU Trade Commissioner Cecilia Malmstrom said there could be provisional safeguard measures for the steel industry starting mid-July. The European Commission is still in process of investigation the measures needed after US steel and aluminum tariffs.

Malmstrom said "this is an investigation that will probably take until the end of the year before we can get the full picture." But she emphasized that "we are seriously contemplating to have provisional measures in place, I would say mid-July could be some provisional measures. Exactly what form that will take is still under discussion."

Separately, UK International Trade Minister Liam Fox said separately in the parliament that "we are looking to see what impact there may be from any diversion and whether we need to introduce safeguards to protect UK steel producers." And,

"the earliest time that is likely to happen would be early to mid-July. We are already seeing some movements that I think may justify that." He added that "as soon as we have the evidence to be able to justify such a decision, we would take it."

ECB: Rise in protectionism could be significant risks to global activity

In its monthly bulletin, ECB noted that "euro area economic expansion remains solid and broad-based across countries and sectors, despite recent weaker than expected data and indicators." In the June Eurosystem macroeconomic projections, annual real GDP growth is projected to be at 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020.. HICP inflation is projected to be at 1.7% in 2018, 2019 and 2020.

On the global scale, ECB noted, that "following a year of strong and highly synchronised growth, global momentum slowed somewhat in the early part of 2018." While, growth is expected to rebound in near term, it warned that "the implementation of higher trade tariffs, amid ongoing discussions of further protectionist measures, represents a risk to the global economic outlook."

The US steel and aluminium tariffs so far "affect only a small proportion of global trade and are expected to have only a small global macroeconomic effect". However, "the risks of further protectionist steps have risen". Firstly, US "threatened to increase tariffs on USD 50 billion of Chinese goods, to which China pledged to retaliate. Secondly, "the United States launched an investigation into the national security implications of automobile imports."

ECB added that "expectations of an escalation in the dispute could affect investment decisions, with potential effects on global growth". And, "risks to global activity from a widespread rise in protectionism could be significant."

Eurozone economic sentiment dropped sligthly by -0.2

Eurozone economic sentiment index (ESI) dropped a mere -0.2 to 112.3 in June, slightly above expectation of 112.1. Among the Eurozone countries, ESI rose 1.2 in Italy and 1.0 in France. however, there was a notable -1.8 decline in the Netherlands and -0.8 in Germany.

Eurozone industrial confidence was unchanged at 6.9, above expectation of 6.5. Services confidence was unchanged at 14.4, below expectation of 14.3. Consumer confidence was finalized at -0.5. The business climate indicator dropped -0.05 to 1.39, above expectation of 1.2.

ECB: Rise in protectionism could be significant risks to global activity

German Gfk consumer sentiment unchanged at 10.7. Economic expectations tumbled on protectionist Trump

German Gfk consumer climate for July (in June) was unchanged at 10.7, slightly above expectation of 10.6. Among the components, there is notable 14.1pts drop in economic expectations from 37.4 to 23.3. GFK blamed US trade policy as the driver of the decline. It said in the statement that "the American President's protectionist trade policy, which affects both Germany and other export-oriented countries such as China, casts further gloom over the economic forecast." As a result, "economic experts are currently predicting that the economic dynamics of the global economy will decline."

As an export nation, Germany is affected "naturally". Gfk pointed to the study of German Institute for Economic Research (DIW) and the ifo Institute, which projected the German economy will "drop down a gear" this year. These two institutes lowered GDP forecasts by around half a percent to 1.9% and 1.8% respectively.

Nonetheless, income expectations improved from 54.2 to 57.6. Propensity to buy also rose from 55.9 to 56.3. The improvements offset deterioration in economic expectations.

Also from Germany, CPI slowed to 2.1% yoy in June, down from 2.2% yoy and met expectation.

RBNZ More Dovish in June Meeting

RBNZ left the OCR unchanged at 1.75%. While the central bank reiterated its "neutral" monetary policy stance, the accompanying statement revealed that policymakers have turned slightly more dovish than previous months. The members were concerned about global trade tensions and the resulting financial market volatility. They also acknowledged more spare capacity at home as driven by the weaker than expected first quarter GDP growth. The members are ready to leave the policy rate at the current low level and get prepared to lower it, when necessary.

More in RBNZ More Dovish in June Meeting.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3066; (P) 1.3154; (R1) 1.3203; More...

GBP/USD drops to as low as 1.3048 so far today. Solid break of 1.3101 indicates resumption of larger decline from 1.4376. Intraday bias stays on the downside for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. Break there will target 61.8% projection of 1.4376 to 1.3101 from 1.3471 at 1.2683 next. On the upside, break of 1.3314 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | Retail Trade Y/Y May | 0.60% | 1.20% | 1.60% | 1.50% |

| 06:00 | EUR | German GfK Consumer Confidence Jul | 10.7 | 10.6 | 10.7 | |

| 08:00 | EUR | ECB Monthly Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Business Climate Indicator Jun | 1.39 | 1.2 | 1.45 | 1.44 |

| 09:00 | EUR | Eurozone Economic Confidence Jun | 112.3 | 112.1 | 112.5 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | 6.9 | 6.5 | 6.8 | 6.9 |

| 09:00 | EUR | Eurozone Services Confidence Jun | 14.4 | 15.9 | 14.3 | 14.4 |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -0.5 | -0.1 | -0.5 | -0.2 |

| 12:00 | EUR | German CPI M/M Jun P | 0.10% | 0.10% | 0.50% | |

| 12:00 | EUR | German CPI Y/Y Jun P | 2.10% | 2.10% | 2.20% | |

| 12:30 | USD | GDP Annualized Q/Q Q1 T | 2.00% | 2.20% | 2.20% | |

| 12:30 | USD | GDP Price Index Q1 T | 2.20% | 1.90% | 1.90% | |

| 12:30 | USD | Initial Jobless Claims (JUN 23) | 227K | 220K | 218K | |

| 14:30 | USD | Natural Gas Storage | 73B | 91B |

US initial jobless claims rose 9k to 227k. Q1 GDP revised down to 2.0%

US initial jobless claims rose 9k to 227k in the week ended June 23, above expectation of 220k. Four week moving of initial claims rose 1k to 221k.

Continuing claims dropped -21k to 1.705m in the week ended June 16. Four week moving average of continuing claims dropped -3.75k to 1.7195. This is the lowest level since December 1973.

Q1 GDP growth was finalized at 2.0%, revised own from 2.2% and missed expectation of 2.2%. GDP price index was revised up to 2.2%, from 1.9%.

Canadian dollar Gains Ground, U.S GDP Next

The Canadian dollar has posted losses in the Thursday session. Currently, USD/CAD is trading at 1.3289, down 0.40% on the day. On the release front, there are no Canadian events. In the U.S, Final GDP is forecast at 2.2%, identical to the reading of Preliminary GDP in May. As well, unemployment claims is expected to edge up to 220 thousand. On Friday, Germany releases retail sales and the eurozone publishes CPI reports. The U.S will publish consumer spending and inflation data, as well as consumer confidence.

Will he or won’t he? Investors are keeping a close eye on the Bank of Canada, which holds a policy meeting on July 11. The bank has strongly hinted that a rate hike could be coming soon. On Wednesday, BoC Governor Stephen Poloz had a hawkish message for the markets, noting that inflation was on target and the domestic economy was performing well. However, Poloz also mentioned that the trade war between Canada and the U.S was hurting business investment. Currently, the likelihood of a rate hike in July is 55 percent. Canadian economic data in the next two weeks will likely be the determining factor as to whether the BoC presses the rate trigger, or opts to wait until later in the year.

As the second quarter draws to a close, the U.S economy continues to perform well. Economic growth has been strong and the labor market is close to capacity. However, the trade war between the U.S and its major partners could be the dark cloud on the horizon. The Federal Reserve now plans to raise rates four times in 2018 (up from three), but a global trade war could force the Fed to revise its forecast back to three hikes. On Tuesday, Atlanta Fed bank president Raphael Bostic said that if the trade war intensified, he would vote against a fourth rate hike, due to downside risks to the economy. Fed Chair Jerome Powell sounded pessimistic about the economic effects of trade tensions at an ECB forum earlier in June, and if other Fed members express concerns, the Fed could delay a fourth hike until 2019.

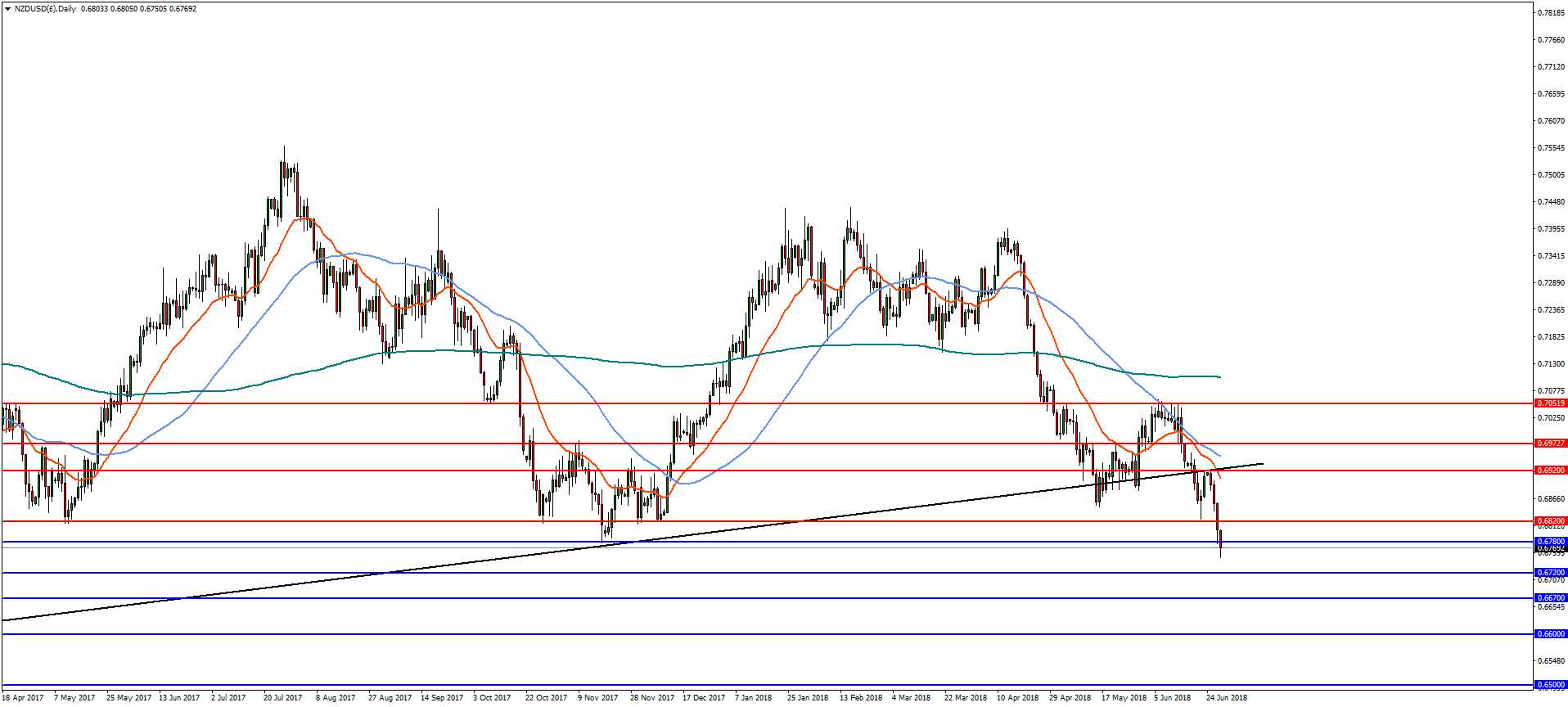

Forex Analysis: NZDUSD And NZDCAD

The New Zealand Dollar has extended losses after the Reserve Bank of New Zealand (RBNZ) kept rates steady at 1.75% yesterday. The accompanying RBNZ statement was dovish with suggestions that Kiwi interest rates will remain at record lows for “some time to come” and pointing out risks to both domestic and global economies. In May, RBNZ governor Adrian Orr left the door open to a rate cut by saying “the direction of our next move is equally balanced up or down, only time and events will tell”. This puts the RBNZ out of step with the Federal Reserve and the monitory policy differential will continue to put pressure on NZDUSD.

NZDUSD

On the daily chart, NZDUSD has declined to support at 0.6780 and break should see a continuation to the 61.8% Fibonacci expansion at 0.6720.Further downside support can be expected at 0.6670 and the psychologically important 0.6600. A reversal above 0.6920 is needed to change the bearish outlook with resistance at 0.6820.

NZDCAD

The Canadian Dollar (CAD) has been one of the stronger currencies of late so the NZDCAD pair may provide a short trading opportunity. In the 4-hourly time frame, NZDCAD has broken though 0.9030 and is trending to supports at 0.8970 and then 0.8910. Any pullback to 0.9030 is likely to be met with selling pressure. Only a sustained recovery back above 0.9030 changes the bearish scenario.

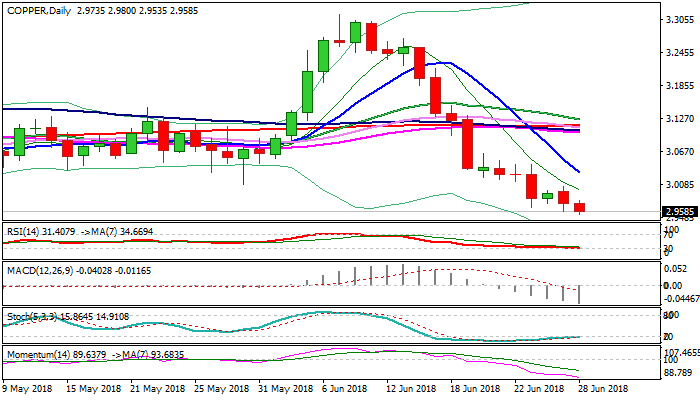

Copper Outlook: Violation Of Base At $2.94 Zone Could Trigger Further Extension Of Downtrend From 2018 High

Copper hit new over three-month low at $2.9535 on Thursday, in extension of steep fall from 2018 high at $3.3140 (posted on 07 Jun) which lasts almost three weeks.

Bears so far show no signs of fatigue despite oversold conditions and pressure key supports at $2.94 zone (higher base consisting of 05 Dec low at $2.9425 and 26 Mar low at $2.9370).

Supports also mark the lower boundary of multi-month consolidation as larger uptrend from Jan 2016 low at $1.9360 ran out of steam.

Sustained break lower would spark further weakness on completion of double-top on weekly chart for extension towards next strong support at $2.8960 (weekly cloud base).

Falling 10SMA continues to track descend (currently at $3.0292) and marks solid resistance which is expected to limit upticks and guard a cluster of MA barriers which lays in $3.1013/$3.1255 zone.

Res: 2.9800, 3.0000, 3.0292, 3.0645

Sup: 2.9535, 2.9435, 2.9370, 2.8960

DAX Slips As EU Summit, Trade Tensions Weigh On Investors

The DAX index has resumed its losing ways in the Thursday session, after the index posted gains on Wednesday. Currently, the DAX is at 12,259, down 0.73% on the day. In economic news, GfK Consumer Climate remained pegged at 10.7, edging above the estimate of 10.6 points. EU leaders are meeting in Brussels for a 2-day summit. Later in the day, Germany releases Preliminary CPI, with an estimate of 0.2%. In the U.S, Final GDP is forecast at 2.2%, identical to the reading of Preliminary GDP in May. Friday will be busy as well, as Germany releases retail sales and the eurozone publishes CPI reports.

European equity markets remain under pressure, as investors cast a nervous eye on the escalating trade tariff between the U.S and its major trading partners. The DAX has lost 2.0% so far this week, and there is more downside potential if trade tensions worsen. On Friday, the EU slapped retaliatory tariffs of some 25% on $3.3 billion of U.S goods. This move was in response to U.S tariffs on EU steel and aluminum imports. President Trump didn’t blink and has threatened to impose 20% tariffs on EU vehicles. This threat sent automobile stocks on the DAX sharply lower on this week, as Daimler and BMW recorded steep declines. BMW exports cars from the U.S to China and Europe, so the trade battles could have a negative impact on the company’s revenues.

All eyes are on the EU Summit, with a host of critical issues on the agenda. These include EU immigration policy, the simmering trade dispute with the U.S, and the stalled Brexit negotiations. Investors will want to see some progress on these issues rather than the leaders highlighting their differences or bashing the Brits. Will EU leaders stick to their guns on the tariffs or offer Trump an olive branch? U.S tariffs will take a toll on the European export sector, and many EU members will want to lower the tensions with the Trump administration. On the Brexit front, the EU had said that it wanted issues such as the Irish border to be resolved by the June summit, but this won’t happen, and the EU will now have to set another deadline, with time running out to resolve this thorny issue. There have been various suggestions for a type of customs union, but none that are to the liking of both sides. European leaders are exasperated with the lack of progress in the Brexit talks and could issue a tough statement warning that the EU and Britain without an agreement in place.