Sample Category Title

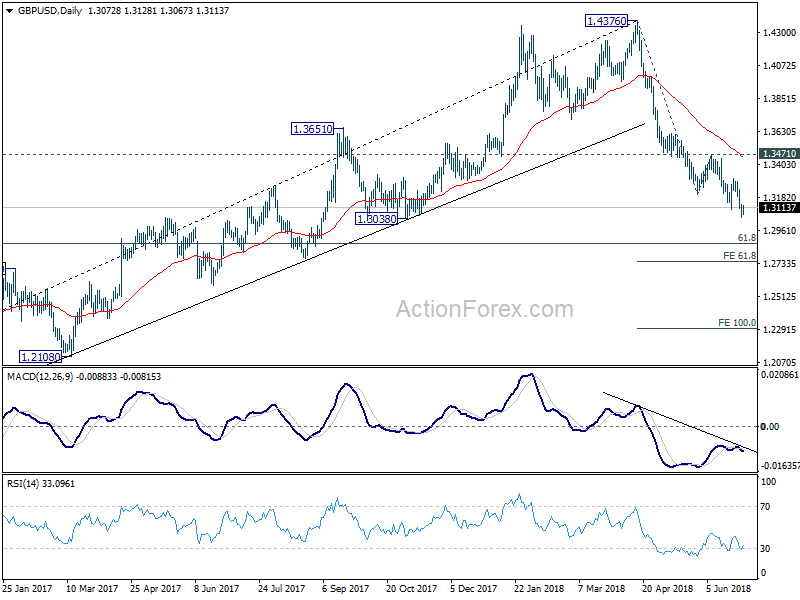

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3043; (P) 1.3085; (R1) 1.3119; More...

Intraday bias in GBP/USD remains on the downside. Current fall from 1.4376 should target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. Break there will target 61.8% projection of 1.4376 to 1.3101 from 1.3471 at 1.2683 next. On the upside, break of 1.3314 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

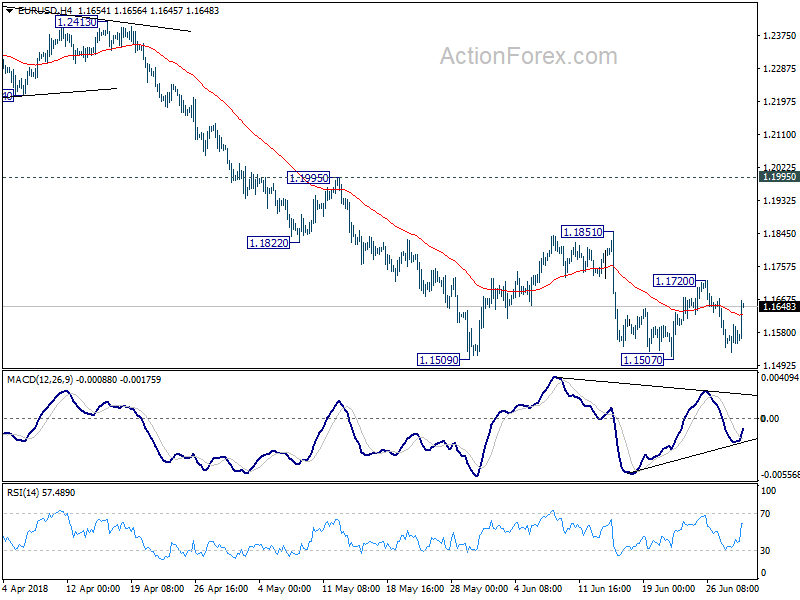

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1566 (R1) 1.1604; More.....

EUR/USD rebounds strongly today but after all, it's staying in range of 1.1507/1851. Outlook remains unchanged. Further recovery could be seen but we'd expect strong resistance by 1.1851 to limit upside. Larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro Cheers EU Agreement on Migration, Yen Dives as Chinese Stocks Rebound

Euro surges broadly today as traders cheer the agreement by EU leaders on migration. Australian Dollar follows as the second strongest as Chinese stocks lead a strong rebound in Asian equities. At the time of writing the Shanghai composite is up 1.2%, Hong Kong HSI is up 1.15% while Singapore Strait Times is up 0.7%. With that, Yen is sold off broadly and is trading as the weakest for today so far. Dollar follow as the second weakest. In other markets, Spot Gold dipped to as low as 1246.11 but regains 1250, follow Dollar's pull back. WTI crude oil stays strong and extends this week's rally to as high as 73.42.

For the week, Canadian Dollar remains the strongest one, followed by the greenback. But the positions could change before close with the number of key events scheduled, including Eurozone CPI, US PCE and Canada GDP. New Zealand Dollar remains the weakest one and there is little hope on a come back.

Technically, USD/CAD's pull back accelerated on oil and an repricing of BoC July hike odds. Deeper fall could be seen today in case of upside surprise in Canadian GDP. But we'd not expect a break of 1.3067 support. EUR/USD is staying in range above 1.1507. While further rebound could be seen, we don't expect a break of 1.1851 resistance. And, as EUR/GBP's rally continues, we'd expect Sterling to stay pressured broadly.

Euro surges as EU leaders agreed on migration

Euro jumps broadly today on news that the 28 EU leaders have agreed on the conclusions of the EU summit, including migration. There were some concerns earlier as Italy threatened to block all agreement if they requests on migration were not met. German Chancellor Angela Merkel, who's under political pressure domestically, said that "overall, after an intensive discussion on the most challenging theme for the European Union, namely migration, it is a good signal that we agreed a common text."

In short, on migration, European Council pledged to reinforce polices that " prevent a return to the uncontrolled flows of 2015" in immigrants. And it will further "stem illegal migration on all existing and emerging routes." EU also pledged to "stand by" Italy and other Central Mediterranean nations, "step up its support for the Sahel region, the Libyan Coastguard, coastal and Southern communities, humane reception conditions, voluntary humanitarian returns, cooperation with other countries of origin and transit, as well as voluntary resettlement

EU pledged to guard against all protectionist actions

Regarding trade tension with the US, EU leaders reiterated that the US steel and aluminium tariffs "cannot be justified on the grounds of national security". And European Council " fully supports the rebalancing measures, potential safeguard measures to protect our own markets, and the legal proceedings at the WTO, as decided on the initiative of the Commission". EU also pledged to "respond to all actions of a clear protectionist nature".

European Council also "underlines the importance of preserving and deepening the rules-based multilateral system." And it invites the European Commission to "propose a comprehensive approach to improving, together with like-minded partners, the functioning of the WTO in crucial areas such as (i) more flexible negotiations, (ii) new rules that address current challenges, including in the field of industrial subsidies, intellectual property and forced technology transfers, (iii) reduction of trade costs, (iv) a new approach to development, (v) more effective and transparent dispute settlement, including the Appellate Body, with a view to ensuring a level playing field, and (vi) strengthening the WTO as an institution, including in its transparency and surveillance function."

China signals shift in monetary policy stance

While quarter end position adjustment could be a factor, a main trigger for the rebound in Asian stocks is the shift in the policy stance of China's central bank PBoC. With that, the process of deleveraging could be slowed to ensure sufficient liquidity in the markets.

In the statement released after Q2 regular meeting, PBoC noted challenges and uncertainties in international developments. And it emphasized the need in "anticipation and forward-looking pre-adjustment fine-tuning" on monetary policy. While being neutral, monetary policy has to "maintain adequate liquidity, and guide the reasonable scale of monetary credit and social financing."

Also, PBoC noted the need to use a variety of tools to "grasp the strength and rhythm of structural deleveraging". The aims were to promote "promote stable and healthy economic development, stabilize market expectations, and guard against systemic financial risks."

St. Louis Fed Bullard hearing full-throated angst about trade disputes

St. Louis Fed President James Bullard said he's "hearing full-throated angst" regarding escalating trade disputes across his district. He added that "all aspects of the economy are affected, but agriculture is certainly" being hit.

He pointed to some suppliers using threat of new tariffs to raise prices, even though their businesses are not directly targeted. And to Bullard, "that shows you how uncertainty over trade policy can feed back" into business decision-making."

Minneapolis Fed Kashkari comfortable to move interest rate to neutral

Minneapolis Fed President Neel Kashkari said he's "comfortable" with interest rate moving back to a "neutral rate". That is, a level that's "not stimulating the economy, but not also constraining the economy". After that, Kashkari would prefer to " just wait and see how inflation evolves." And, Fed could the observe whether wage growth, inflation data support moving to a contractionary policy. But so far, according to Kashkari, the data "does not" support moving into contractionary policy.

A question that Fed policymakers are facing the the lack on acceleration in inflation even though unemployment rate dropped to as low as 3.8% last month. It's commonly believed that inflation would surge to pull unemployment rate back up to the natural rate level. Kashkari pointed out that "in a recession, economists tend to raise the natural rate of unemployment". However, during recovery, we're so reluctant to then lower it, and we end up being late lowering it in recovery." Nonetheless, Kashkari said he's not ready to believe that natural unemployment rate to be as low as 3.5% as that's a big departure from historical data.

BoE Haldane: The vote for hike last week was hardly either surprising or radical

BoE chief economist Andy Haldane said yesterday that his vote for rate hike last week was "hardly either surprising or radical". He pointed out it was a "a full decade after monetary policy was first placed on an emergency setting". Even with a 25bps hike in the Bank Rate to 0.75%, monetary conditions in the UK would remain " extraordinarily accommodative by any historical metric". And the aim for a hike was to "lower the risk of needing to tighten policy less gradually in future and cause a sharper adjustment in the economy." He also noted he would even have voted for a hike back in May "had data on the economy held firm".

On the economy, he said "data on the consumer since the May MPC meeting has, virtually without exception, bounced back strongly". And that includes "measures of retail spending, consumer confidence and consumer credit". The underlying picture now appears to be one of "gently rising household spending". This is being supported by highly accommodative credit conditions and "now-positive growth in inflation-adjusted wages".

In addition, Haldane also said that there may could still be data disappointments. But he added that "waiting for something to turn up is not a prudent strategy in life. And waiting for everything to turn up is certainly not a prudent strategy for monetary policy."

Busy data ahead - Eurozone CPI, US PCE and Canada GDP watched

On the data front, New Zealand building permits rose 7.1% mom in May. UK Gfk consumer confidence dropped to -9 in June. Japan unemployment rate dropped to fresh 25 year low at 2.2%, down from 2.5%. Tokyo CPI accelerated more than expected to 0.7% yoy in June. Industrial production dropped -0.2% mom in May. Housing starts rose 1.3% yoy in May. Consumer confidence dropped to 43.7 in June.

Looking ahead, it's a pretty busy day. Swiss KOF, German unemployment, UK mortgage approvals, current account and Q1 GDP final will be featured in European session. But main focus is Eurozone CPI, which is expected to finally meet ECB target of 2% in June.

Later in the day, US will release personal income and spending, PCE inflation, Chicago PMI. Canada will release GDP, IPPI and RMPI, as well as BoC business outlook survey.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1566 (R1) 1.1604; More.....

EUR/USD rebounds strongly today but after all, it's staying in range of 1.1507/1851. Outlook remains unchanged. Further recovery could be seen but we'd expect strong resistance by 1.1851 to limit upside. Larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | 7.10% | -3.70% | -3.60% | |

| 23:01 | GBP | GfK Consumer Confidence Jun | -9 | -7 | -7 | |

| 23:30 | JPY | Jobless Rate May | 2.20% | 2.50% | 2.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 0.70% | 0.60% | 0.50% | |

| 23:50 | JPY | Industrial Production M/M May P | -0.20% | -1.10% | 0.50% | |

| 5:00 | JPY | Housing Starts Y/Y May | 1.30% | -6.00% | 0.30% | |

| 5:00 | JPY | Consumer Confidence Jun | 43.7 | 43.9 | 43.8 | |

| 7:00 | CHF | KOF Leading Indicator Jun | 101 | 100 | ||

| 7:55 | EUR | German Unemployment Change (000's) Jun | -8K | -11k | ||

| 7:55 | EUR | German Unemployment Claims Rate Jun | 5.20% | 5.20% | ||

| 8:30 | GBP | Mortgage Approvals May | 62K | 62K | ||

| 8:30 | GBP | Money Supply M4 M/M May | 0.30% | 0.20% | ||

| 8:30 | GBP | Current Account Balance (1Q) | -18.2B | -18.4B | ||

| 8:30 | GBP | Index of Services 3M/3M Apr | 0.00% | 0.30% | ||

| 8:30 | GBP | GDP Q/Q Q1 F | 0.10% | 0.10% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Jun | 2.00% | 1.90% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Jun A | 1.00% | 1.10% | ||

| 12:30 | CAD | Industrial Product Price M/M May | -0.50% | 0.50% | ||

| 12:30 | CAD | Raw Materials Price Index M/M May | -0.60% | 0.70% | ||

| 12:30 | CAD | GDP M/M Apr | 0.30% | |||

| 12:30 | USD | Personal Income May | 0.40% | 0.30% | ||

| 12:30 | USD | Personal Spending May | 0.40% | 0.60% | ||

| 12:30 | USD | PCE Deflator M/M May | 0.10% | 0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y May | 2.00% | 2.00% | ||

| 12:30 | USD | PCE Core M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | PCE Core Y/Y May | 1.80% | 1.80% | ||

| 13:45 | USD | Chicago PMI Jun | 60.1 | 62.7 | ||

| 14:00 | USD | U. of Mich. Sentiment Jun F | 99.2 | 99.3 | ||

| 14:30 | CAD | BOC Business Outlook Survey |

Asian markets jump, Yen dives as China signals shift in monetary policy stance

Asian markets are staging a strong rebound today. At the time of writing, Chines Shanghai Composite is up 1.2%, Hong Kong HSI is up 1.15%, Singapore Strait Times is up 0.7%. Nikkei lags behind, though, and is up 0.14% only. Yen is sold off broadly.

A main trigger for the rebound is the shift in the policy stance of China's central bank PBoC. The process of deleveraging could be slowed to ensure sufficient liquidity in the markets.

In the statement released after Q2 regular meeting, PBoC noted challenges and uncertainties in international developments. And it emphasized the need in "anticipation and forward-looking pre-adjustment fine-tuning" on monetary policy. While being neutral, monetary policy has to "maintain adequate liquidity, and guide the reasonable scale of monetary credit and social financing."

Also, PBoC noted the need to use a variety of tools to "grasp the strength and rhythm of structural deleveraging". The aims were to promote "promote stable and healthy economic development, stabilize market expectations, and guard against systemic financial risks."

EU pledged to guard against all protecionist actions

Regarding trade tension with the US, EU leaders reiterated that the US steel and aluminium tariffs "cannot be justified on the grounds of national security". And European Council " fully supports the rebalancing measures, potential safeguard measures to protect our own markets, and the legal proceedings at the WTO, as decided on the initiative of the Commission". EU also pledged to "respond to all actions of a clear protectionist nature".

European Council also "underlines the importance of preserving and deepening the rules-based multilateral system." And it invites the European Commission to "propose a comprehensive approach to improving, together with like-minded partners, the functioning of the WTO in crucial areas such as (i) more flexible negotiations, (ii) new rules that address current challenges, including in the field of industrial subsidies, intellectual property and forced technology transfers, (iii) reduction of trade costs, (iv) a new approach to development, (v) more effective and transparent dispute settlement, including the Appellate Body, with a view to ensuring a level playing field, and (vi) strengthening the WTO as an institution, including in its transparency and surveillance function."

Euro surges as EU leaders agreed on migration

Euro jumps broadly today on news that the 28 EU leaders have agreed on the conclusions of the EU summit, including migration. There were some concerns earlier as Italy threatened to block all agreement if they requests on migration were not met. German Chancellor Angela Merkel, who's under political pressure domestically, said that "overall, after an intensive discussion on the most challenging theme for the European Union, namely migration, it is a good signal that we agreed a common text."

In the summit conclusion, it's written that "the European Council reconfirms that a precondition for a functioning EU policy relies on a comprehensive approach to migration which combines more effective control of the EU's external borders, increased external action and the internal aspects, in line with our principles and values."

It noted that the measures since 2015 has brought down detected illegal border crossings into EU by 95%. And European Council pledged to "continue and reinforce this policy to prevent a return to the uncontrolled flows of 2015 and to further stem illegal migration on all existing and emerging routes."

Regarding the "Central Mediterranean Route", EU pledged to "stand by Italy and other frontline Member States in this respect. It will step up its support for the Sahel region, the Libyan Coastguard, coastal and Southern communities, humane reception conditions, voluntary humanitarian returns, cooperation with other countries of origin and transit, as well as voluntary resettlement. All vessels operating in the Mediterranean must respect the applicable laws and not obstruct operations of the Libyan Coastguard."

Market Morning Briefing: Dollar Index Could Probably See A Dip To 95.00-94.75 Levels

STOCKS

Worries of trade tariff between US and its major trading partners seems to be taking the stocks lower. Imposition of 20% tariffs on EU vehicles as stated by Trump took down the automobile stocks on the Dax this week, while the EU posed retailitory tariffs of about 25% on $3.3bln of US goods in response to the US tariffs on EU steel and aluminium imports.

Dax (12177.23, -1.39%) looks bearish in the near term towards 11800.

Dow (24216.05, +0.41%) bounced a bit from levels just above 24000. While the daily trend support holds, there could be some upmove in Dow towards 24750. Else failure to remains above 24000 may take it lower to 23600 next week.

22000 is an important levels for Nikkei (22194.21, -0.34%). In case it breaks lower, it could be vulnerable to fall towards 21500 over the next couple of weeks. Watch price action near 22000.

Shanghai (2813.61, +0.96%) is likely to break below 2800 and head towards 2750 next week. The index looks bullish with some possibility of a bounce towards 2850.

Nifty (10589.10, -0.77%) finally broke below our expected 10650 levels and while the index trades lower, it could target 10400 in the near term. The index is bearish for the coming week.

COMMODITIES

Brent (77.39) may head towards 80 while above support near 76. Near term looks bullish. On the other hand, WTI (73.25) has resistance at 74 which if holds could bring in a small dip towards 72. 74-76 is a resistance zone for WTI which could prevent an immediate rise above current levels.

Gold (1249.70) is fast headed towards 1240 and may pause there. A short bounce from 1240 is possible before the price attempts to fall further. Overall Gold looks bearish for a few more sessions.

Copper (2.9730) could hold above immediate support near 2.95 and while that holds, the price could trade sideways in the 2.95-3.05 region.

FOREX

Euro (1.1570): Euro has seen a high near 1.1601-1.1617 over yesterday and today. There is resistance near 1.162 and higher up near 1.165 which it could test in today's session and then move down towards 1.15 again in the coming week.

Dollar Index (95.29): Dollar Index could probably see a dip to 95.00-94.75 levels in today's session. Next week, it could rise from support on daily candles (near 94.75) back towards 95.5 and beyond.

Dollar Yen (110.48): Dollar Yen's ranging continues and is now being restricted to a very narrow range between 110.7-110.0 on daily and 3 day candles. Next week could possibly see a break of this range on the downside (preferred). Long term crucial resistance near 110.5-111.0 is likely to hold.

Euro Yen (127.85): Euro Yen again rose above support on daily candles (127.75) as the Euro tested highs near 1.1617 and the Dollar Yen remained ranged. The horizontal support on weekly line chart near 127 is crucial and a break of the same would be required to confirm medium term bearishness towards 124.

Pound (1.3074): Pound tested support on daily and weekly candles near its low of 1.3050 yesterday. This support could hold for at least sometime in the next week, taking Pound towards 1.32 again. A break of this support (could happen eventually) would be very bearish.

Dollar Rupee (68.7925): Weakness in the Emerging Market currencies (specially, Chinese Yuan) are indicative of further weakness in Rupee. Immediate target on the upside could be 69.20, while above 68.60.

INTEREST RATES

US GDP data (released yesterday) for the 1st quarter fell short of previous estimates by 0.2%. This could moderate some of the enthusiasm in global markets regarding the US economy's growth and inflation prospects. It could also be a supporting factor for a further dip in US yields, which have already been falling due to the trade war worries.

US 10 year (2.84%), 30 Year (2.97%), 5 Year (2.72%), 2 Year (2.51%) :

Repeating yesterday's comments:

The US 10 Year yield's gradual downtrend could target support near 2.70%-2.65% on medium term chart.

Similarly, the 30 Year yield also looks like it could move towards 2.90%.

The German-US 10 Year spread (-2.52%) has risen slightly and is at resistance on medium term chart.. If it goes above this resistance, it could well target -2.48%. This might imply a further fall for US yields.

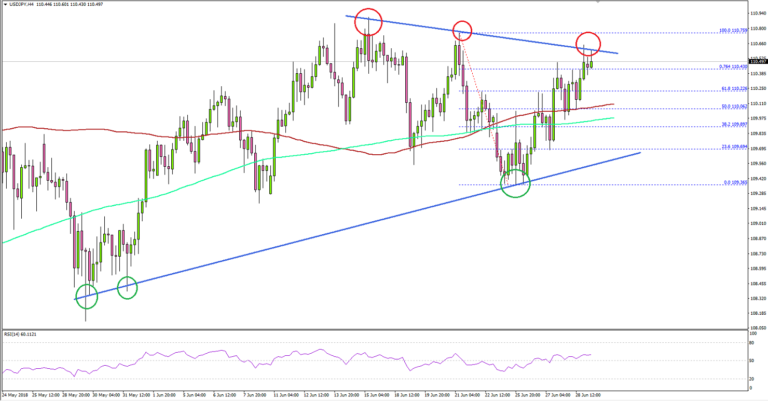

Can USD/JPY Break The 110.60 Resistance?

Key Highlights

- The US Dollar is trading in a positive zone above the 109.60 support against the Japanese Yen.

- There is a major contracting triangle formed with resistance near 110.50-60 on the 4-hours chart of USD/JPY.

- The US GDP in Q1 2018 grew 2%, less than the forecast of 2.2%.

- Tokyo's CPI in June increased 0.6% (YoY), compared with the forecast of 0.5%.

USDJPY Technical Analysis

The US Dollar started an upward move from the 109.36 swing low against the Japanese Yen. However, the USD/JPY pair must clear the 110.50-110.60 resistance zone to gain upside momentum.

After forming a low at 109.36, the pair moved higher and broke the 50% Fib retracement level of the last decline from the 110.75 high to 109.36 low. More importantly, the pair traded above the 110.00 level and the 100 simple moving average (red, 4-hours).

However, the upside move faced resistance near the 110.50 level and the 76.4% Fib retracement level of the last decline from the 110.75 high to 109.36 low. It seems like there is a major contracting triangle formed with resistance near 110.50-60 on the 4-hours chart of USD/JPY.

On the downside, there is a strong support formed around 109.50. Therefore, as long as the pair is above 109.50, it could move above 110.60 resistance. If not, there is a risk of a bearish break towards the 109.00 level.

Recently in the US, the Gross Domestic Product Annualized for Q1 2018 was released by the US Bureau of Economic Analysis. The market was looking for a growth of 2.2% in Q1 2018, but the actual was a bit lower since there the GDP came in at 2%.

The US GDP Price Index in Q1 2018 increased 2.2%, more than the forecast of 1.9%. The report stated that:

The increase in real GDP in the first quarter reflected positive contributions from nonresidential fixed investment, PCE, exports, federal government spending, and state and local government spending that were partly offset by negative contributions from residential fixed investment and private inventory investment. Imports, which are a subtraction in the calculation of GDP, increased.

The US Dollar corrected lower after the release, but it is still well supported on the downside. EUR/USD and GBP/USD may correct higher, but upsides are likely to be capped in the near term.

Economic Releases to Watch Today

- Germany's Unemployment Change for June 2018 – Forecast -8K, versus -11K previous.

- Germany's Unemployment Rate for June 2018 – Forecast 5.2%, versus 5.2% previous.

- UK GDP for Q1 2018 (QoQ) – Forecast +0.1% versus +0.1% previous.

- Euro Zone CPI for June 2018 (YoY, Preliminary) – Forecast +2.0%, versus +1.9% previous.

- Euro Zone Core CPI for June 2018 (YoY, Preliminary) – Forecast +1.0%, versus +1.1% previous.

- US Personal Income for May 2018 (MoM) – Forecast +0.4%, versus +0.3% previous.

- Canadian Gross Domestic Product for April 2018 (MoM) – Forecast 0.0%, versus +0.3% previous.

St. Louis Fed Bullard hearing full-throated angst about trade disputes

St. Louis Fed President James Bullard said he's "hearing full-throated angst" regarding escalating trade disputes across his district. He added that "all aspects of the economy are affected, but agriculture is certainly" being hit.

He pointed to some suppliers using threat of new tariffs to raise prices, even though their businesses are not directly targeted. And to Bullard, "that shows you how uncertainty over trade policy can feed back" into business decision-making."

Minneapolis Fed Kashkari comfortable to move interest rate to neutral

Minneapolis Fed President Neel Kashkari said he's "comfortable" with interest rate moving back to a "neutral rate". That is, a level that's "not stimulating the economy, but not also constraining the economy". After that, Kashkari would prefer to " just wait and see how inflation evolves." And, Fed could the observe whether wage growth, inflation data support moving to a contractionary policy. But so far, according to Kashkari, the data "does not" support moving into contractionary policy.

A question that Fed policymakers are facing the the lack on acceleration in inflation even though unemployment rate dropped to as low as 3.8% last month. It's commonly believed that inflation would surge to pull unemployment rate back up to the natural rate level. Kashkari pointed out that "in a recession, economists tend to raise the natural rate of unemployment". However, during recovery, we're so reluctant to then lower it, and we end up being late lowering it in recovery." Nonetheless, Kashkari said he's not ready to believe that natural unemployment rate to be as low as 3.5% as that's a big departure from historical data.