Sample Category Title

USDX Elliott Wave Analysis: Bullish Sequence Calling Higher

USDX short-term Elliott Wave view suggests that the decline to 94.18 on 6/25 low has ended correction to the cycle from 6/7/2018 low as Intermediate wave (X). The internals of that pullback unfolded as a Flat correction where Minor wave A ended in 3 swings at 94.53, Minor wave B ended in 3 swings at 95.52 and Minor wave C of (X) ended at 94.18 low.

Above from there, the rally is unfolded in 5 waves structure which ended Minor wave A of a Zigzag structure. Up from 94.18, Minute wave ((i)) ended at 94.77. Minute wave ((ii)) ended at 94.52, Minute wave ((iii)) ended at 95.41. Minute wave ((iv)) ended at 95.20, and Minute wave ((v)) of A ended at 95.53 high. The Index made a marginal new high above the previous irregular Minor wave B of (X) at 95.52, suggesting that the next extension higher in intermediate wave (Y) has started.

Down from 95.53 high, the index is pulling back in shorter cycles to correct cycle from 6/25 (94.18) within Minor wave B pullback. Near-term focus remains towards 94.68-94.85 100%-123.6% Fibonacci extension area of a Minute wave ((a))-((b)) to find buyers in the index either for new highs or for 3 wave reaction higher at least. We don’t like selling the index and expect buyers to appear in Minor wave B pullback in 3, 7 or 11 swings at the extreme area provided the pivot at 94.18 low stays intact.

USDX 1 Hour Elliott Wave Chart

The Eco Calendar Is Moderately Interesting

Markets

Yesterday, US and German bonds initially remained well bid as investors pondered the consequences of recent correction on emerging markets. Later, risk sentiment improved. US equities rebounded and US bonds closed the day with modest losses. US yields rose up to 1.9 bp (5y) with the long end outperforming (30y, -0.1bp). German yields (earlier close) finished mixed with the long end also doing best (30y -1.6bp). This morning, Asian equities are joining the risk rebound for the US. Pressure on Asian markets eases as the dollar rally did run into resistance. The rebound in Chinese equities was supported by Chinese authorities easing some foreign investment restrictions. Late today, global sentiment on risk (including the performance of EM) will remain a key factor for core bond trading. Regarding the data, the EMU June headline inflation is expected to rise further from 1.9% Y/Y to 2.0%, but core inflation might ease from 1.1% to 1.0%. A big upward surprise is probably needed for the inflation data to have a big impact on European bonds as the ECB committed to keep rates unchanged through the Summer of 2019. In the US, May personal spending and income, the Chicago PMI and the final Michigan consumer confidence will be released. Especially the PCE deflators are interesting. The headline index is expected to rise from 2.0% to 2.2%. The core measure is seen at 1.9% (from 1.8%). In a positive risk context, the PCE deflators coming closer to/rising above 2.0% might put some additional pressure on US bonds. In longer term perspective, EM tensions probably have to move further to the background first, for core yields to start a more protracted upleg.

Yesterday, the USD rally did run into resistance as the US currency neared/reached important technical barriers. (95.15/50 for the DXY trade-weighted dollar, low 1.15 area for EUR/USD). A gradual easing in global risk aversion (especially in the US) also helped to prevent further USD gains (except for USD/JPY). This morning, the dollar is losing further ground against most majors, including the CNY. Remarkably, the USD correction was for an important part the result of a short squeeze in EUR/USD after EU leaders signalled they had reached an agreement on EU immigration policy. This EUR/USD rise also spilled over to other USD cross rates. This USD correction on the EU migration story suggests that the market had probably become positioned a bit too much long USD. Question is whether a USD move mainly based on this trigger (EU immigration agreement) can be sustained further down the road. We remain cautious on further USD losses (EUR/USD rise) for now. In this respect, we keep an eye on the dollar reaction in case of a further rise in the US PCE deflators. Yesterday, EUR/GBP finally broke out of the 0.87/0.8850 consolidation pattern. Ongoing poor progress in the Brexit process (Brexit was only a ‘secondary item’ at the EU summit) and end of month repositioning finally helped the break above 0.8850. Overnight GFK consumer confidence disappointed. EUR/GBP was also propelled by the euro rise after the announcement on an EU migration deal. Next resistance comes in at 0.8968 (March correction top).

News Headlines

At the gathering in Brussels, EU leaders this morning reached a deal on the migration topic. Rescued migrants on EU territory should be sent to “controlled centres” in the bloc. For those in need of international protection, the principle of solidarity would apply (an Italian demand) but on a voluntary basis (a central European demand).

Facing mounting complaints by the US, Germany and other trading partners, China eased limits on foreign ownership in several sectors (including car manufacturing and insurance). The move comes after US president Donald Trump softened his stance in regard to restrictions on Chinese investments in the US.

The eco calendar is moderately interesting. The Chicago PMI (US) is likely to drop from 62.7 to 60.0. US personal income and spending data will also be published. The US core PCE deflator is expected to edge up from 1.8% YoY to 1.9%. EMU headline inflation might touch the 2% mark. Core inflation is expected to ease to 1.0% (from 1.1%).

Euro Trading On A Stronger Footing, After EU Leaders Reach A Deal On Migration

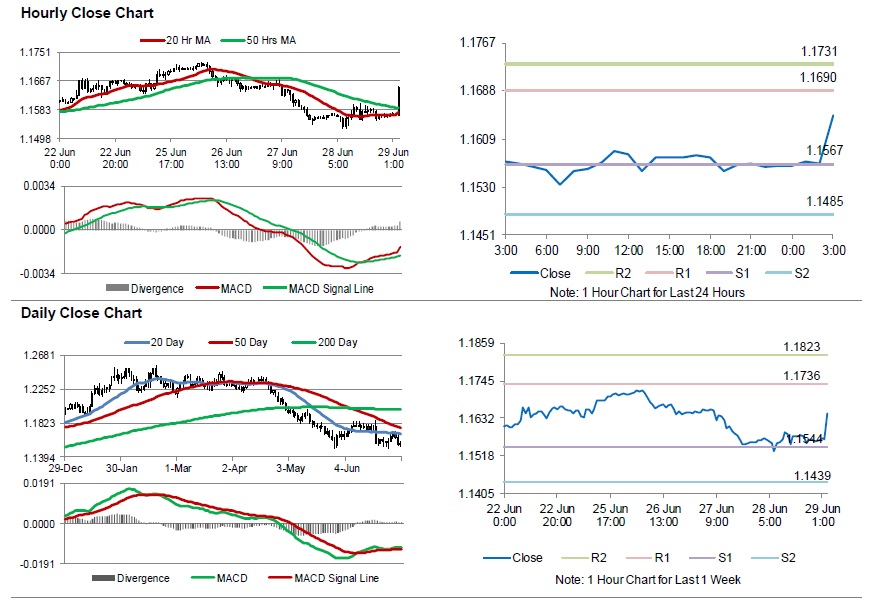

For the 24 hours to 23:00 GMT, the EUR rose 0.03% against the USD and closed at 1.1564.

The ECB, in its economic bulletin, signalled downside risks to the global growth and confirmed the end of asset purchases.

Macroeconomic data indicated that Euro-zone's final consumer confidence index eased to its lowest level since October 2017 to -0.5 in June, confirming the preliminary print and in line with market expectations. In the prior month, the index recorded a level of 0.2. Additionally, the region's business climate indicator declined to a level of 1.39 in June, following a revised reading of 1.44 in the previous month. Market had anticipated for a fall to a level of 1.4.

Moreover, nation's economic sentiment indicator fell to a 10-month low level of 112.3 in June, higher than market expectations of a fall to a level of 112.0. The indicator had recorded a reading of 112.5 in the preceding month.

Separately, Germany's Gfk consumer confidence remained unchanged at 10.7 in July, compared to market expectations for a drop to a level of 10.6. Meanwhile, the nation's flash consumer price index (CPI) recorded a rise of 2.1% on an annual basis in June, less than market expectations for an advance of 2.2%. In the prior month, the CPI had advanced 2.2%.

In the US, data showed that the final annualised gross domestic product (GDP) was revised down to 2.0% in the first quarter of 2018, oppressed by weakest consumer spending in last 5-years, while markets had envisaged for a rise of 2.2%. The GDP had registered a rise of 2.9% in the previous quarter.

On the contrary, the nation's seasonally adjusted initial jobless claims jumped to a level of 227.0K in the week ended 23 June, higher than market expectations of a rise to 220.0 K. In the previous week, initial jobless claims had recorded a reading of 218.0K.

In the Asian session, at GMT0300, the pair is trading at 1.1648, with the EUR trading 0.73% higher against the USD from yesterday's close, after the European leaders clinched a deal on migration.

The pair is expected to find support at 1.1567, and a fall through could take it to the next support level of 1.1485. The pair is expected to find its first resistance at 1.1690, and a rise through could take it to the next resistance level of 1.1731.

Moving forward, investors would await the release of Euro-zone's consumer price index for June along with Germany's retail sales for May and unemployment rate for June, slated to release in a few hours. Also, the US personal spending and personal income for May as well as the Chicago PMI and the Michigan consumer sentiment index both for June, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Sterling Trading Higher, Ahead Of Final GDP Data

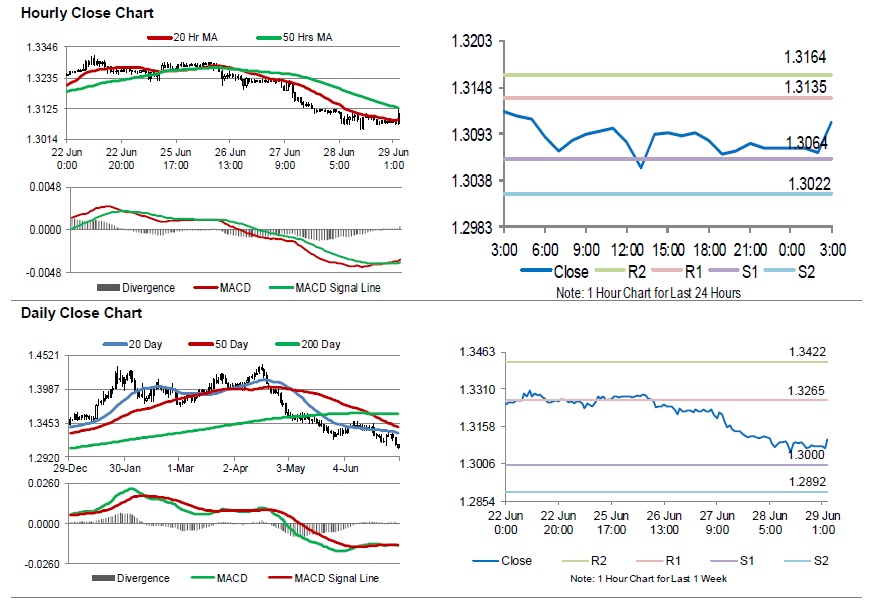

For the 24 hours to 23:00 GMT, the GBP declined 0.31% against the USD and closed at 1.3077.

In the Asian session, at GMT0300, the pair is trading at 1.3107, with the GBP trading 0.23% higher against the USD from yesterday’s close.

On the data front, UK’s Gfk consumer confidence unexpectedly slid to -9.0 in June, amid increasing pessimism among investors and defying market expectations for a steady reading. The index had recorded a reading of -7.0 in the previous month.

Further, the nation’s Lloyds business sentiment index dropped to 29.0 in June, posting its lowest level in this year and compared to a reading of 35.0 in the prior month.

The pair is expected to find support at 1.3064, and a fall through could take it to the next support level of 1.3022. The pair is expected to find its first resistance at 1.3135, and a rise through could take it to the next resistance level of 1.3164.

Looking ahead, investors will keep an eye on UK’s final 1Q GDP data, net consumer credit and mortgage approvals for May, set to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japan’s Jobless Rate Hits A 26 Year Low Level In May

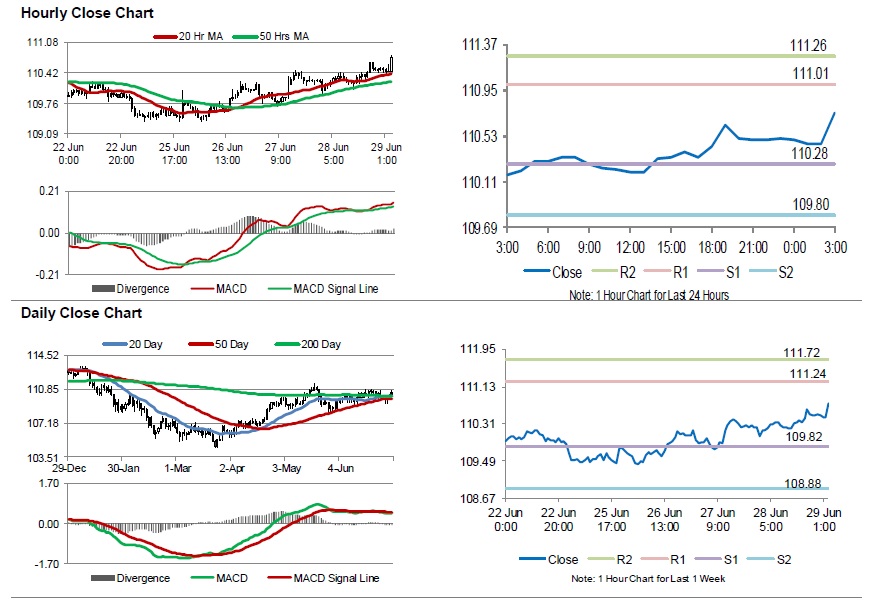

For the 24 hours to 23:00 GMT, the USD rose 0.24% against the JPY and closed at 110.51.

In the Asian session, at GMT0300, the pair is trading at 110.75, with the USD trading 0.22% higher against the JPY from yesterday's close.

Overnight data indicated that, Japan's flash industrial production retreated by 0.2% on a monthly basis in May, undershooting market expectations for a drop of 1.0%. In the prior month, industrial production had climbed 0.5%.

Moreover, the nation's unemployment rate dropped to 2.2% in May, hitting its lowest in 26-years and compared to 2.5% in the previous month.

The pair is expected to find support at 110.28, and a fall through could take it to the next support level of 109.80. The pair is expected to find its first resistance at 111.01, and a rise through could take it to the next resistance level of 111.26.

Going ahead, investors will keep an eye on Japan's housing starts for May and consumer confidence index for June, both set to release in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

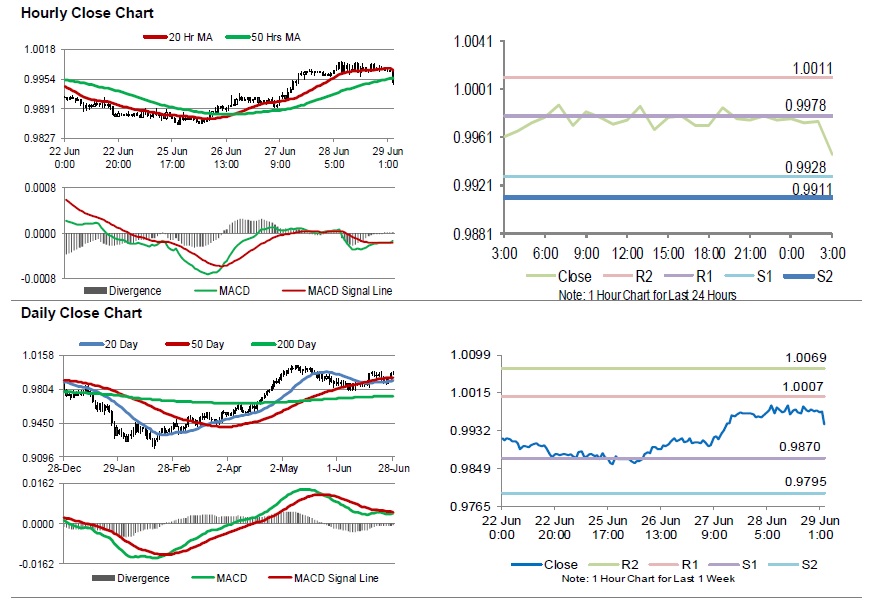

Swiss Franc Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.06% against the CHF and closed at 0.9975.

In the Asian session, at GMT0300, the pair is trading at 0.9946, with the USD trading 0.29% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9928, and a fall through could take it to the next support level of 0.9911. The pair is expected to find its first resistance at 0.9978, and a rise through could take it to the next resistance level of 1.0011.

Looking forward, traders will focus on Switzerland’s KOF leading indicator for June, set to release in a few hours.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

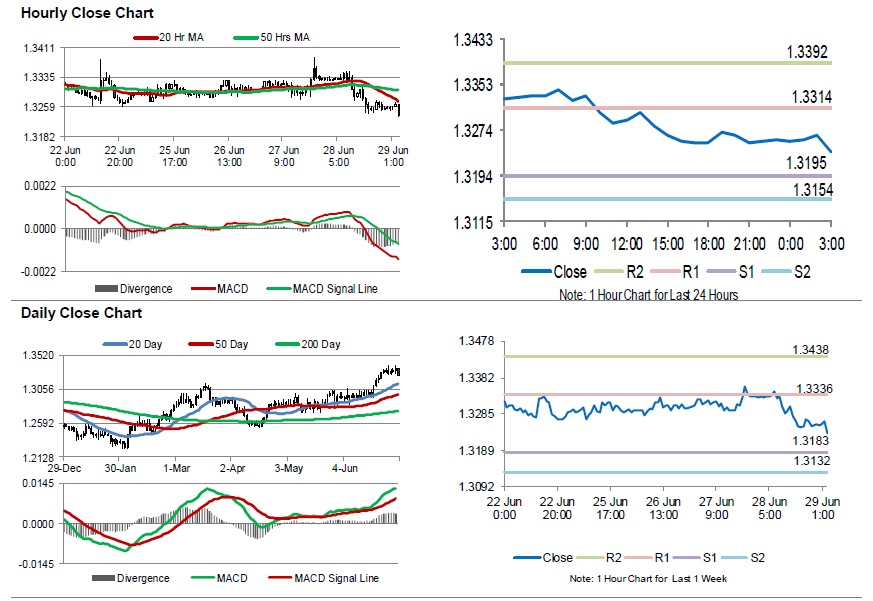

Loonie Trading Higher, Ahead Of GDP Data

For the 24 hours to 23:00 GMT, the USD declined 0.56% against the CAD and closed at 1.3257.

In the Asian session, at GMT0300, the pair is trading at 1.3235, with the USD trading 0.17% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3195, and a fall through could take it to the next support level of 1.3154. The pair is expected to find its first resistance at 1.3314, and a rise through could take it to the next resistance level of 1.3392.

Trading trend in the Loonie will be determined by Canada’s crucial GDP data for April, due to release later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

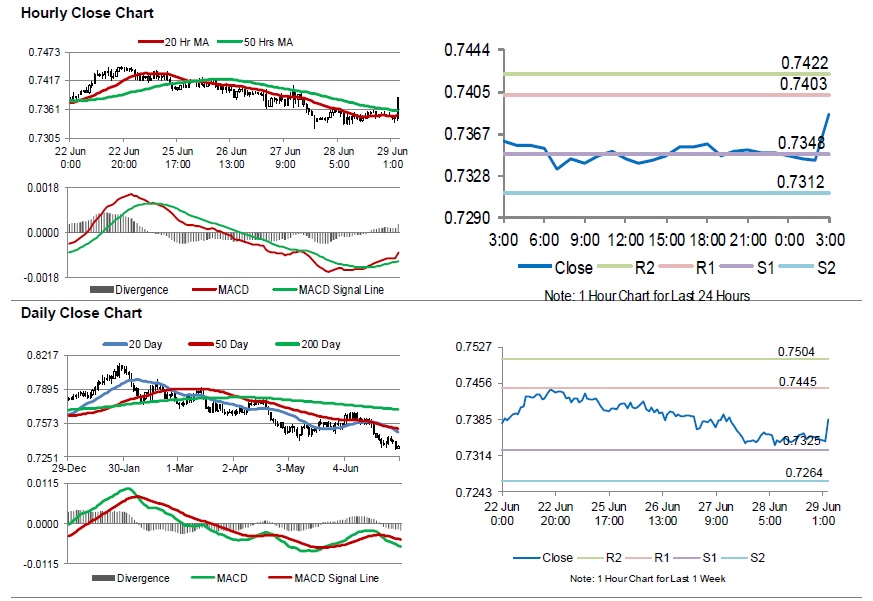

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.08% against the USD and closed at 0.7349.

LME Copper prices declined 0.6% or $38.0/MT to $6650.0/MT. Aluminium prices fell 1.4% or $31.5/MT to $2173.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7385, with the AUD trading 0.49% higher against the USD from yesterday’s close.

Earlier today, in Australia, the private sector credit recorded a slower-than-expected rise of 0.2% on a monthly basis in May, compared to an advance of 0.4% in the previous month.

The pair is expected to find support at 0.7348, and a fall through could take it to the next support level of 0.7312. The pair is expected to find its first resistance at 0.7403, and a rise through could take it to the next resistance level of 0.7422.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

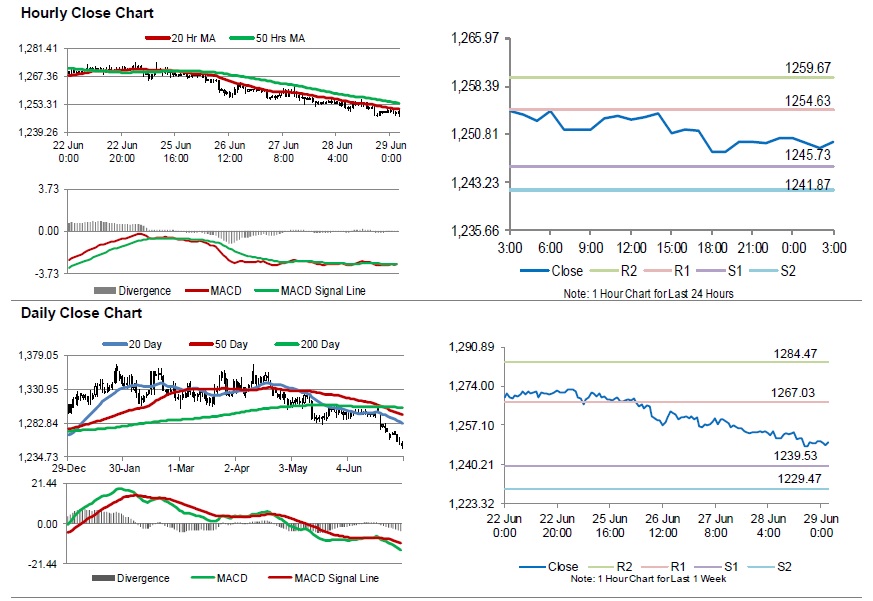

Gold: Yellow Metal Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.37% against the USD and closed at USD1249.30 per ounce, amid strength in the US equities.

In the Asian session, at GMT0300, the pair is trading at 1249.60, with gold trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1245.73, and a fall through could take it to the next support level of 1241.87. The pair is expected to find its first resistance at 1254.63, and a rise through could take it to the next resistance level of 1259.67.

The yellow metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

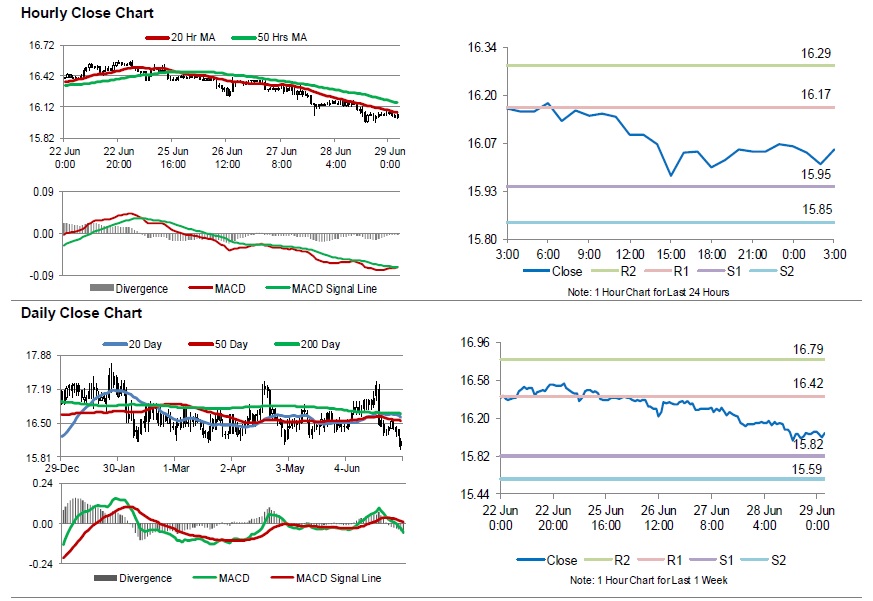

Silver: White Metal Extends Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, Silver declined 0.50% against the USD and closed at USD16.07 per ounce, tracking losses in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.05, with silver trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 15.95, and a fall through could take it to the next support level of 15.85. The pair is expected to find its first resistance at 16.17, and a rise through could take it to the next resistance level of 16.29.

The white metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.