Sample Category Title

XAUUSD Intraday Analysis

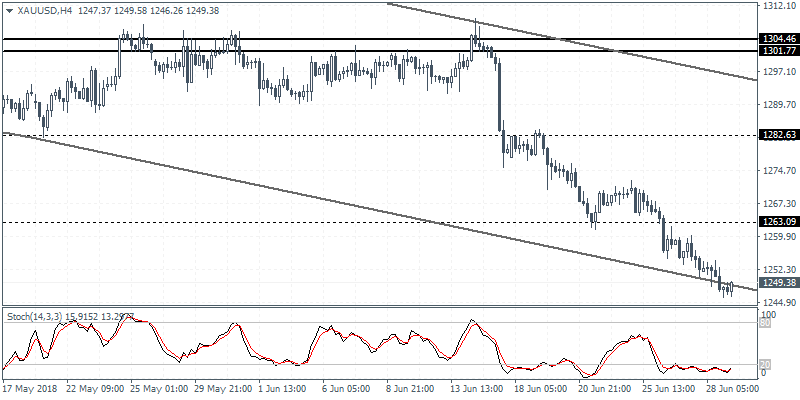

XAUUSD (1249.38): Gold prices continued to post the declines as price action was seen briefly falling below the 1250 handle in the near term. This also coincides with price action testing the lower trend line of the falling price channel. In the event of a rebound, gold prices could be seen extending the gains back to the 1263 level where resistance is most likely to be formed. The Stochastics on the 4-hour chart remains a bit overstretched into the oversold levels currently.

USDJPY Intraday Analysis

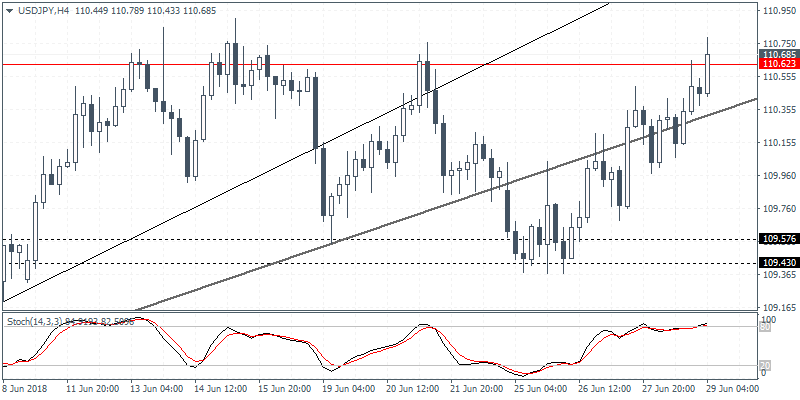

USDJPY (110.68): The USDJPY currency pair was seen slowing inching higher as price action was seen testing the resistance level of 110.62 once again. A convincing breakout above this level could trigger further gains to the upside. However, we expect to see price action mostly consolidating near the resistance level. While there is scope for the USDJPY to pull back, this could potentially lead to an evolving inverse head and shoulders pattern that could turn bullish for the currency pair. The support at 109.57 - 109.43 remains a key level of interest in the near term.

EURUSD Intraday Analysis

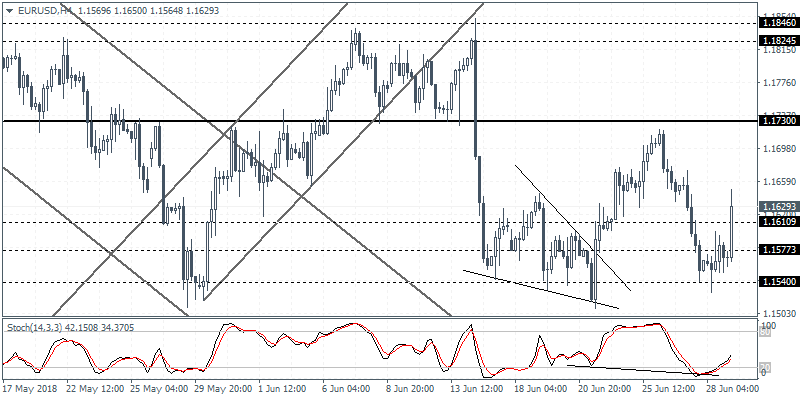

EURUSD (1.1629): The EURUSD currency pair was seen trading subdued on Thursday but price action quickly gained momentum into the early Asian trading session today. The rebound off the 1.1540 support is expected to see some upside prevailing in the currency pair. In the near term, the EURUSD currency pair is expected to struggle near the resistance level of 1.1730. A breakout above this resistance is required for price action to test the next main resistance level at 1.1846 - 1.1824. To the downside, as long as the current support holds, we expect the currency pair to either trade sideways or biased to the upside.

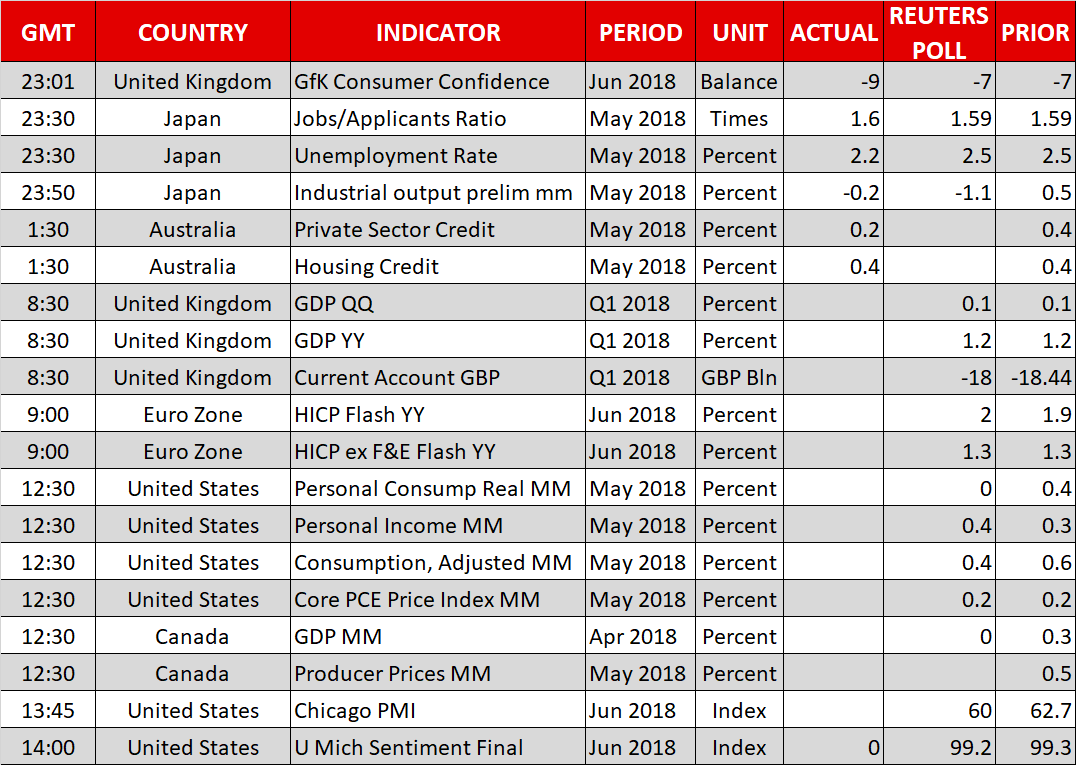

UK Final GDP Revision To Stay Unchanged

The U.S. dollar was seen holding its ground across some of the currency pairs despite the U.S. first quarter GDP report showing a downside revision. Data from the Commerce department showed that the first quarter GDP in the U.S. increased at a pace of 2.0% compared to the previous estimates that suggested the economy increased at a pace of 2.2%.

The greenback shed some losses but quickly recovered on the day.

The economic calendar is somewhat busy today with the data from the Eurozone covering the French consumer spending and the preliminary inflation reports. This is later followed by the preliminary inflation figures for the Eurozone.

In the UK, the current account figures are expected followed by the final revised GDP for the first quarter of the year.

Economists polled expect to see no change which could confirm that the UK's economy grew at one of the slowest paces of just 0.1%.

In the U.S. trading session, the core PCE price index is expected to show a 0.2% increase on the month while personal spending and income are expected to rise 0.4% each.

Sterling jumps as UK Q1 GDP revised up to 0.2%

Sterling jumps notably after GDP upward revision. Q1 GDP growth is finalized at 0.2% qoq, revised up from 0.1% qoq. Services made the largest contribution by growing 0.2%. The 0.1% growth in production was offset by the -0.1% contraction in construction.

Among services, business and finance services jumped 0.6%, government and other services rose 0.3%. Distribution, hotels and restaurants increased by 0.1%. Transport, storage and communication increased by 0.1%

Also from the UK, mortgage approvals rose to 64.5k in May. M4 dropped -0.4% mom in May. Index of services rose 0.2% 3mo3m in April. Current account deficit narrowed to GBP -17.7B in Q1.

Chinese Equities Rise Amid Rebound In Property Shares, Comments By PBoC And Sovereign Wealth Fund

General Trend:

- Asian equity markets trade generally higher after gains in the US

- Nike rises over 9% in the afterhours, raised sales guidance; US banks disclose capital return plans

- China and Hong Kong equities rise, Property shares advance

- China sovereign wealth fund official said A-shares are attractive after recent drop

- Xiaomi IPO said to price at lower end of range

- Sharp rallies over 10% after canceling stock offering; cited US/China trade spat

- Osaka Gas announces investment in US shale gas project

- Aussie rises amid equity gains in China, Japanese quarter-end flows in focus

- Euro rises on EU migration agreement

- US Treasury Dept. said to plan to release report related to China later on Friday

- China issued list related to foreign investment access

- PBoC discussed deleveraging measures in Q2 monetary policy report

- China 10-yr bond Futures trade at highest level since April 2017

- BoJ may later today announce bond purchase schedule for July

- Bank of Japan (BoJ) cut purchases of 5-10 yr JGBs at daily operation

- Japan jobless rate hits over 25-year low in May

- Tokyo June core CPI rises more than expected, headline inflation unexpectedly rose

- New Zealand consumer confidence hits lowest level since Aug 2016

- Indonesia 10-yr bond yield rises ahead of central bank decision, rate hike expected

- BoJ Tankan survey due for release next week (Monday, July 2nd)

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 Utilities index +1.4%, REIT +1%, Resources +0.3%, Consumer Discretionary +0.2%, Financials flat; Telecom -0.4%

- (AU) Australia May Private Sector Credit M/M: 0.2% v 0.4%e (matches Jan 2017 low) ; Y/Y: 4.8% v 5.0%e

- (NZ) NEW ZEALAND JUN ANZ CONSUMER CONFIDENCE INDEX: 120.0 V 121.0 PRIOR (lowest level since Aug 2016); M/M: -0.8% V +0.4% PRIOR

- (NZ) New Zealand May Building Permits M/M: +7.1% v -3.6% prior

China/Hong Kong

- Shanghai Composite opened +0.1%, Hang Seng -0.1%

- Hang Seng Consumer Goods index +2.8%, Info Tech +2.7%, Industrial Goods +2.4%, Property/Construction +2.2%, Services +1.8%, Materials +1.3%, Financials +1.3%

- (CN) China PBOC Quarterly (Q2) Monetary Policy Committee: Reiterates stance to maintain prudent and neutral monetary policy; To control intensity and pace of structural deleveraging

- (CN) For the week, the PBoC drained a net of CNY370B in its open market operations v CNY140B net injection w/w

- (CN) China PBoC set yuan reference rate at 6.6166 v 6.5960 prior (weakest yuan fix since Dec 13 2017)

- (US) US Ambassador to China Branstad: The Trump Administration is not convinced China is willing to make enough progress soon enough on trade issues

- (CN) Zinc smelters in China said to propose 10% output cut - US financial press

- (CN) China State Researcher sees GDP growth of ~6.5% in H2 2018 and 2019 - US financial press

- (CN) China state planner issued special management measures list for foreign investment access, effective July 28th - press

- (CN) China to revise rules related to public-private partnerships - Chinese Press

Japan

- Nikkei 225 opened +0.2%

- TOPIX Iron & Steel index +0.5%, Securities +0.4%; Real Estate -0.3%

- (JP) JAPAN MAY JOBLESS RATE: 2.2% V 2.5%E (over 25-year low)

- (JP) JAPAN MAY PRELIM INDUSTRIAL PRODUCTION M/M: -0.2% V -1.0%E; Y/Y: 4.2% V 3.4%E

- (JP) Japan June Tokyo CPI Y/Y: 0.6% v 0.4%e; Ex-Fresh Food (Core) Y/Y: 0.7% v 0.6%e

- (JP) JAPAN JUN CONSUMER CONFIDENCE: 43.7 V 43.8E

- (JP) JAPAN MAY ANNUALIZED HOUSING STARTS: 996K V 930KE; Y/Y: +1.3% V -5.7%E

- (JP) Newsprint companies in Japan said to seek first price increase in many years - US financial press

Korea

- Kospi opened +0.5%

- (KR) South Korea May Industrial Production m/m: 1.1% v 0.2%e; y/y 0.9% v 0.9%e

- (KR) South Korea May Cyclical Leading Index Change: -0.1 v -0.3 prior

- (KR) South Korea July Business Survey: Manufacturing: 80 v 79 prior; Non-Manufacturing: 80 v 85 prior

North America

- US equity markets ended higher: Dow +0.4%, S&P500 +0.6%, Nasdaq +0.8%, Russell 2000 +0.3%

- S&P500 Technology +1.2%, Telecom +1%

- Nike [NKE]: Raised forecast for annual sales growth to high single digits (prior mid to high single digits)

Europe

- (EU) EU leaders said to reach deal on migration - US financial press

- Deutsche Bank [DBK.DE]: Fed objects to capital plan for Deutsche Bank US unit due to qualitative

Levels as of 01:30ET

- Nikkei 225, +0.1%, ASX 200 flat, Hang Seng +1.2%; Shanghai Composite +1.5%; Kospi +0.4%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.3%, Dax +0.1%; FTSE100 flat

- EUR 1.1558-1.1667; JPY 110.37-110.80 ; AUD 0.7334-0.7393 ;NZD 0.6736-0.6784

- Aug Gold +0.1% at $1,252/oz; Aug Crude Oil -0.4% at $73.17/brl; Jul Copper +0.6% at $2.987/lb

GOLD Descending Trend Line At Weekly Support

Gold has made a big drop that is marked by a descending trend line. However, today is Friday and we could see some profit taking in the market before the next move. The POC zone stands exactly where the trend line is and where the W L5 level supports the price. Below 1245.70, further weakness is expected towards 1239.65. Above D H3 1250.29 we could see 1256.34. Ideally for bears, the price should stay capped below 1260-63 – strong resistance.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

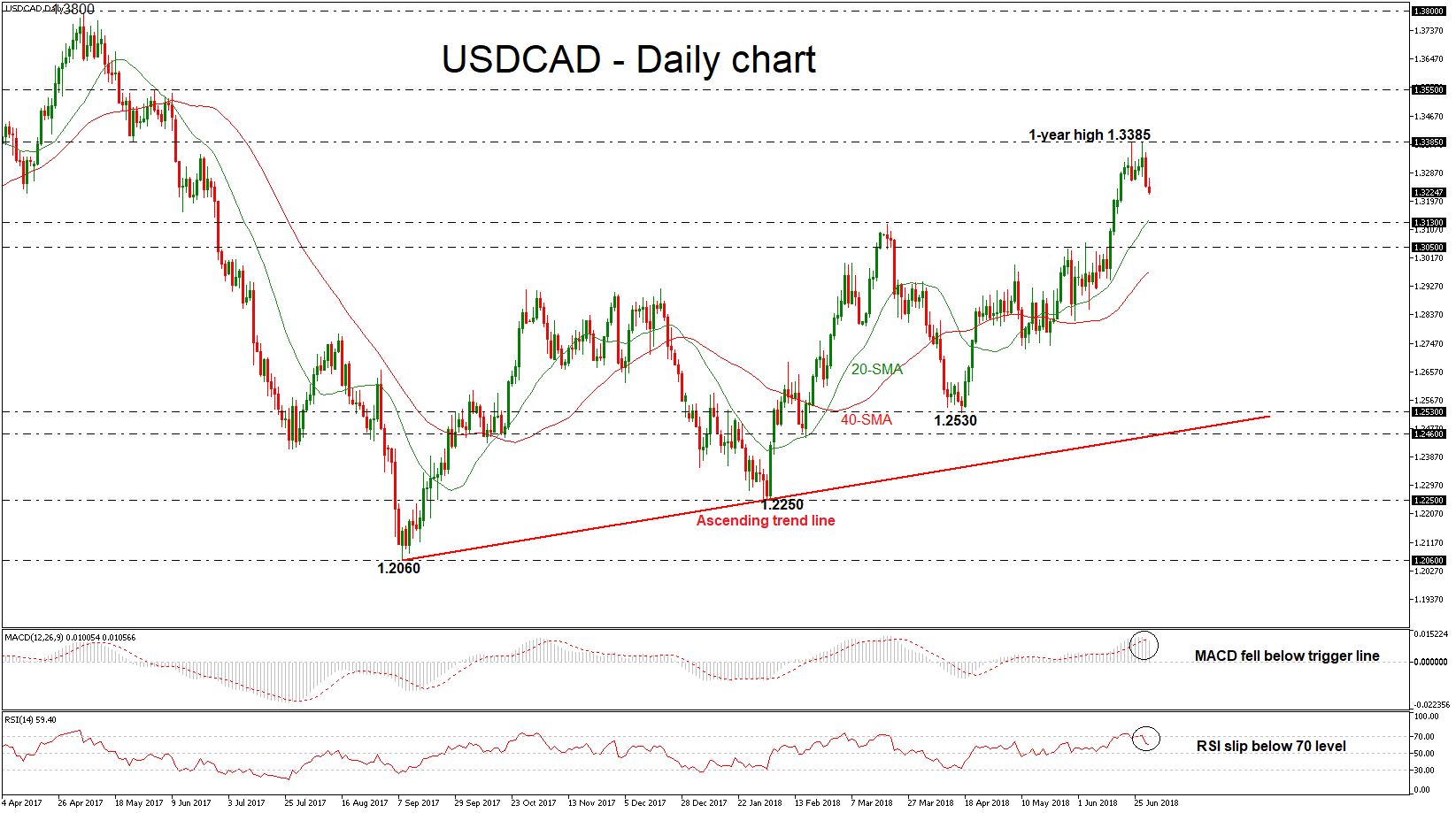

USDCAD Erases Rally, Set To Post Red Week After Two Positive Sessions

USDCAD reversed back some of the previous week's gains, creating a significant red day on Thursday after the bounce off the one-year high of 1.3385. The sharp sell-off has not shifted yet the positive medium-term outlook to negative as it is still developing above the ascending trend line. The technical indicators, though are sending bearish signals in the near-term, suggesting that the strong bullish bias is over.

Looking at momentum oscillators on the daily chart, they suggest further declines may be on the cards in the short-term. The RSI is below the 70 line, detecting negative momentum, and is also pointing downwards. The MACD, already negative, lies below its trigger line.

In case of further declines in the pair, immediate support may be found at 1.3130, an area that also encapsulates the 20-day simple moving average (SMA). If sellers manage to push below that hurdle that would mark a touch of the 1.3050 support, increasing the probability for further bearish extensions.

On the flip side, if the bulls retake control, price advance may stall initially near the latest highs at 1.3385. A potential upside violation of this zone would drive the price until the 1.3550 resistance barrier, identified by the June 2017 highs.

Overall, USDCAD seems to be in a strong upward movement as long as it is trading above the moving averages in the longer-term timeframes, suggesting that the bullish outlook holds.

Euro Rebounds On EU Migration Deal, US Core PCE Price Index Awaited

Here are the latest developments in global markets:

FOREX: The US dollar index is down by 0.5% on Friday, as the currency with the biggest weight in that index – the euro – is advancing after EU leaders reached a deal on immigration overnight, dispelling some political uncertainty. The safe-haven Japanese yen is on the retreat, as the positive tones from the EU summit and the lack of any concerning trade news boosted risk appetite.

STOCKS: US markets closed in the green on Thursday in the absence of a fresh escalation in trade tensions, with technology and financial shares leading the way higher. The tech-heavy Nasdaq Composite advanced 0.79%, while the S&P 500 and the Dow Jones climbed by 0.62% and 0.41% respectively. The rebound looks set to continue, as futures tracking the Dow, S&P, and Nasdaq 100 are pointing to a significantly higher open today, something likely owed to the positive outcome of the EU summit. The bullish sentiment rolled over into Asia too, with Japan's Nikkei 225 and Topix gaining 0.15% and 0.23% correspondingly. In Hong Kong, the Hang Seng surged by 1.58%. Europe was even more encouraging. Futures suggest all the major European indices are set to open more than 1.0% higher today.

COMMODITIES: Oil prices corrected lower on Friday, after posting notable gains in the previous session. WTI is down by 0.2%, after it touched a fresh three-and-a-half year high yesterday of $74.03, while Brent is 0.1% lower, trading just below a one-month high. Without any fresh news on the supply front, the gains appear to be owed mostly to the correction lower in the dollar, as well as the broader risk-on sentiment in markets. In precious metals, gold is up by 0.3% on Friday. It is currently trading near the $1250/troy ounce level, attempting to post its first day of advances this week amid a dip in the US dollar, which makes the dollar-denominated metal more attractive for investors using foreign currencies.

Major movers: Euro recovers, yen retreats as EU reaches migration deal; loonie rebounds too

After marathonlike talks that dragged on until the early hours of Friday, EU leaders finally reached an agreement on migration. They agreed to take more steps towards restricting the movement of asylum seekers between member states, and also to set up new centers that process migrants to determine whether they are genuine refugees or not. The accord strengthens the position of German Chancellor Merkel, who was under pressure to return home with a deal or face the potential collapse of her fragile coalition government.

The euro spiked higher on the news, recovering ground against all its major counterparts as the likelihood for early elections in Germany diminished and political uncertainty faded. Euro/dollar is up by 0.6% on Thursday, while euro/sterling is 0.4% higher, touching a fresh three-month high. Sterling will probably remain watchful of Brexit developments – remember the EU summit continues today and the leaders could highlight the lack of meaningful progress in those talks lately.

Euro/yen was the biggest winner, gaining 0.7% as the EU deal boosted risk appetite in general, diverting funds out of safe-haven assets like the yen and into high-yielding currencies like the Australian dollar. Besides the migrant deal, the yen seems to be on the defensive amid a lack of fresh escalation in the trade saga. In fact, China said overnight it will allow more foreign investment in its economy after July 28, in sectors such as banking and automotive, helping to ease concerns of further tensions. Dollar/yen is up by 0.1%, and looks set to post a green candle for the fourth consecutive session.

Elsewhere, rising oil prices breathed some life back into the Canadian dollar yesterday. The loonie surged as WTI crude prices touched fresh three-and-a-half year highs; recall Canada is a major oil-exporting economy. Besides oil, monetary policy will likely be a major driver for the currency in the coming days. The BoC meets again on July 11 and a rate hike is priced in with a 64% probability, according to Canada's OIS. Should today's GDP data and next week's jobs figures confirm the economy continues to operate on all cylinders, markets could push that probability closer to 100% and the loonie may stay in demand – absent any worrisome NAFTA headlines, of course.

Day ahead: US core PCE index, personal income & consumption under the spotlight; EU CPI in focus as well

Friday's economic calendar will keep investors busy in terms of key data releases, while trade developments may continue to dictate changes in risk sentiment.

Out of the Eurozone, the German unemployment rate will come into view at 0800 GMT to show that the jobless rate remained unchanged at the record low of 5.2% in June according to analysts, with the number of unemployed people decreasing by 8k, less than the 11k reduction in May. Eurozone flash inflation readings for the aforementioned month, however, will be of greater interest as these could affect the ECB's view on monetary policy and therefore bring greater volatility to the euro if the data deviate from expectations. Forecasters are now supporting that the headline CPI has inched up to 2.0% y/y in June compared to 1.9% in May, while the core equivalent which excludes food and energy is seen unchanged at 1.3% y/y. Should inflation data register a higher increase than expected, the euro could extend today's rally on speculation ECB policymakers could feel more confident to raise interest rates after the termination of the asset purchasing program at the end of this year. Still, investors will likely continue to monitor the political situation in Germany despite EU leaders finding a solution to the migration puzzle at the EU summit today. Particularly, it would be interesting to see whether Merkel's coalition partners, who oppose the Chancellor's refugee policy, will raise their thumbs up, saving the coalition government and Merkel's political career.

Meanwhile, in the UK, the Office for National Statistics will be publishing its final GDP growth estimates for the first quarter at 0830 GMT, with expectations being for an expansion of 1.2% y/y and 0.1% m/m as first and second estimates indicated. At 1230, Canada will also see its monthly GDP growth stats but no growth is expected to have been recorded in April. In March, Canadian GDP increased by 0.3% m/m.

In the US, all eyes will turn to the calendar at 1230 GMT when the Bureau of Economic analysis is scheduled to update the Fed's favorite inflation measure, the core Personal Consumption Expenditure Index, as well as its personal income and personal consumption gauges. The report is projected to show that inflation has risen by 0.2% m/m in May, the same as in April, pushing the yearly gauge from 1.8% to 1.9%, just below the Fed's inflation target of 2.0%. Investors, though, will look at the consumption and income figures to clarify whether higher interest rates and inflation are pressuring consumers. While consumption could have eased to 0.4% m/m from 0.6% seen previously, personal income is projected to edge up by 0.1 percentage points to 0.4% m/m. In case the numbers – especially the consumption gauge – beat expectations, amplifying the case for a more hawkish rate path by the Fed, then the dollar could attract additional buying interest.

A little bit later, Chicago PMI and University of Michigan Consumer Sentiment will come under review as well at 1345 and at 1400 GMT respectively.

In oil markets, Baker Hughes will report the number of active US oil drills at 1700 GMT.

As for today's public appearances, the French President Emmanuel Macron, the Chairman of the EU summit Donald Tusk, and the head of the European Commission Jean-Claude Juncker will be giving a news conference after a two-day European leaders' summit at 1130 GMT. Comments on Brexit and eurozone economic integration will be in focus.

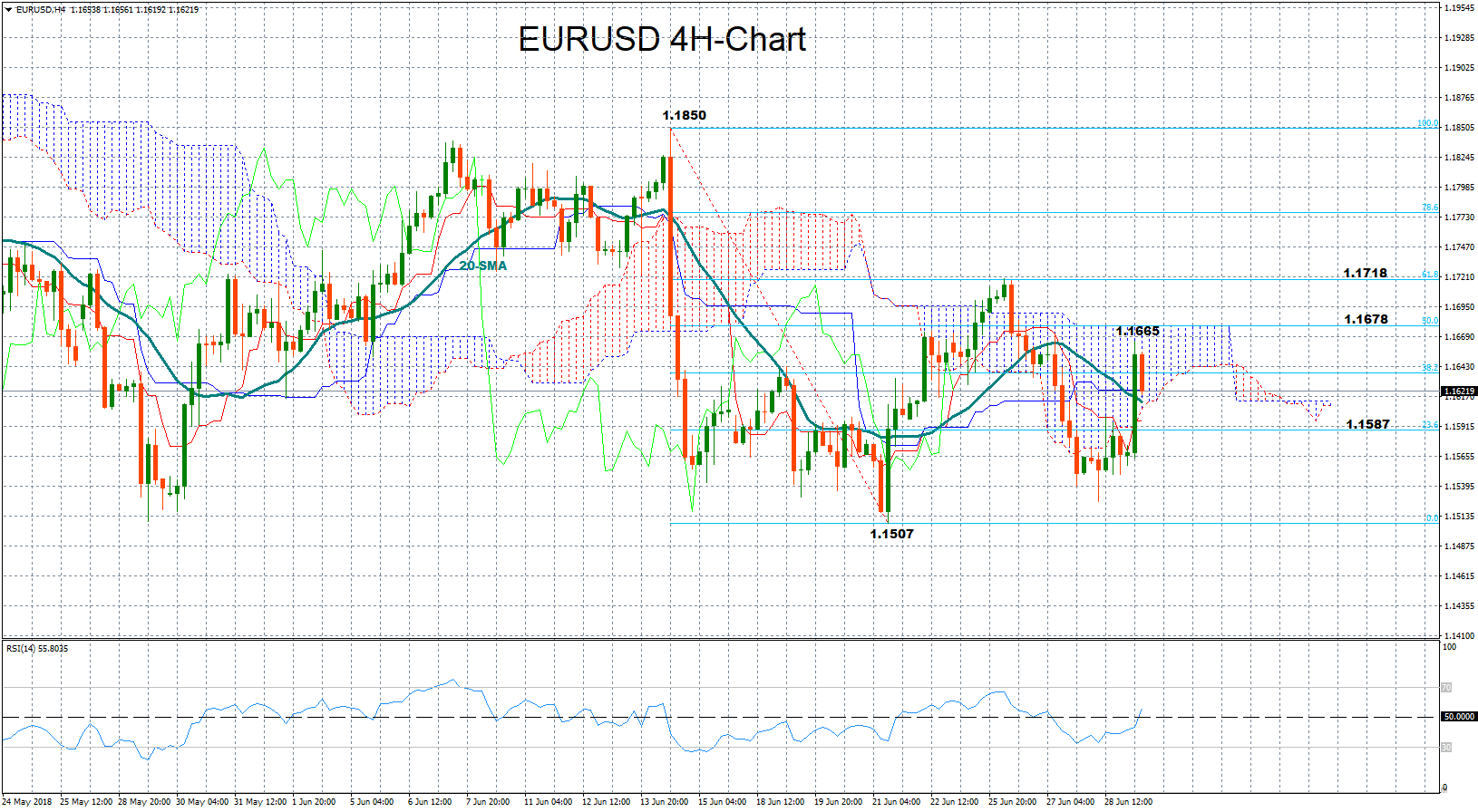

Technical Analysis: EURUSD breaks 1.1600 but momentum indicators are still neutral

The announcement of a migration deal in the Eurozone, woke up euro bulls early today, driving EURUSD above the 1.1600 level and back into the Ichimoku cloud in the four-hour chart. The Ichimoku indicators, however, continue to support that the pair is likely to trade neutral, maintaining the downtrend from 1.1719 as the red Tenkan-sen line has flattened below the blue Kijun-sen line. The RSI has improved further but is currently moving around its neutral threshold of 50, sending additional neutral signals at the moment.

Still, the pair could gain more ground today if Eurozone inflation figures surpass forecasts, with traders looking for resistance probably at today's high of 1.1665 before eyes turn to 1.1678, the 50% Fibonacci retracement of the downleg from 1.1850 to 1.1507. A break of this point could then shift focus to the 61.8% Fibonacci retracement of 1.1718, where the market stopped upside corrections on Tuesday.

On the other hand, disappointing prints could immediately lead the market down to the 20-period moving average which currently stands at 1.1613 before steeper declines eye the 23.6% Fibonacci of 1.1587. The area around 1.1550, though, could be a stronger support since it has provided some floor to the market over the past two weeks.

Swiss KOF Economic Barometer to 101.7, clear contribution from exports

Swiss KOF Economic Barometer rose 1.7 to 101.7 in June, above expectation of 101.0. It's also back above long-term average at 100.0. KOF said it indicates a "slightly above-average development" in Switzerland. But still, the "tailwind for the Swiss economy is no longer as strong as during winter."

Exports made a "particularly clear contribution" to the improvement. There were also "positive developments in domestic demand, with increase in "propensity to consume". In manufacturing and construction, the indicators for order backlogs, inventory reserves and intermediate goods purchasing point to a more positive development. Within manufacturing, however, "signs of developments in the near future are mixed."