Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1566 (R1) 1.1604; More.....

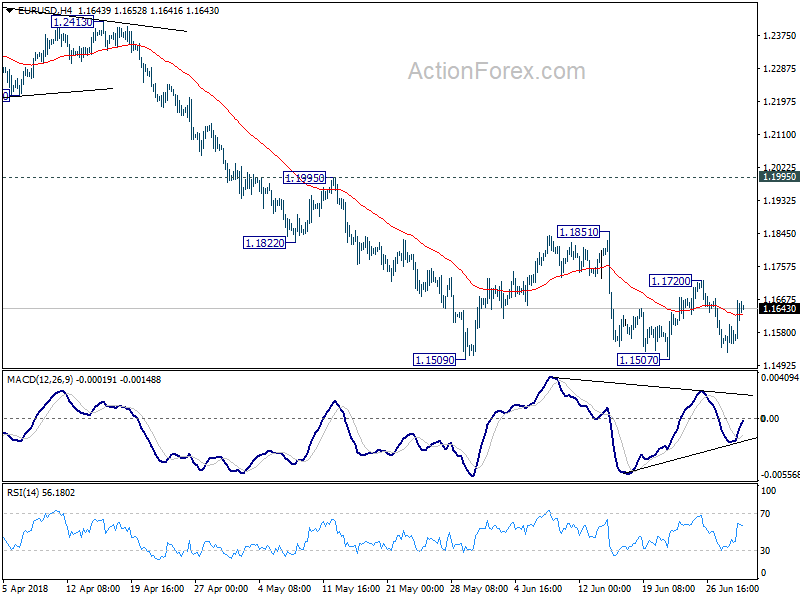

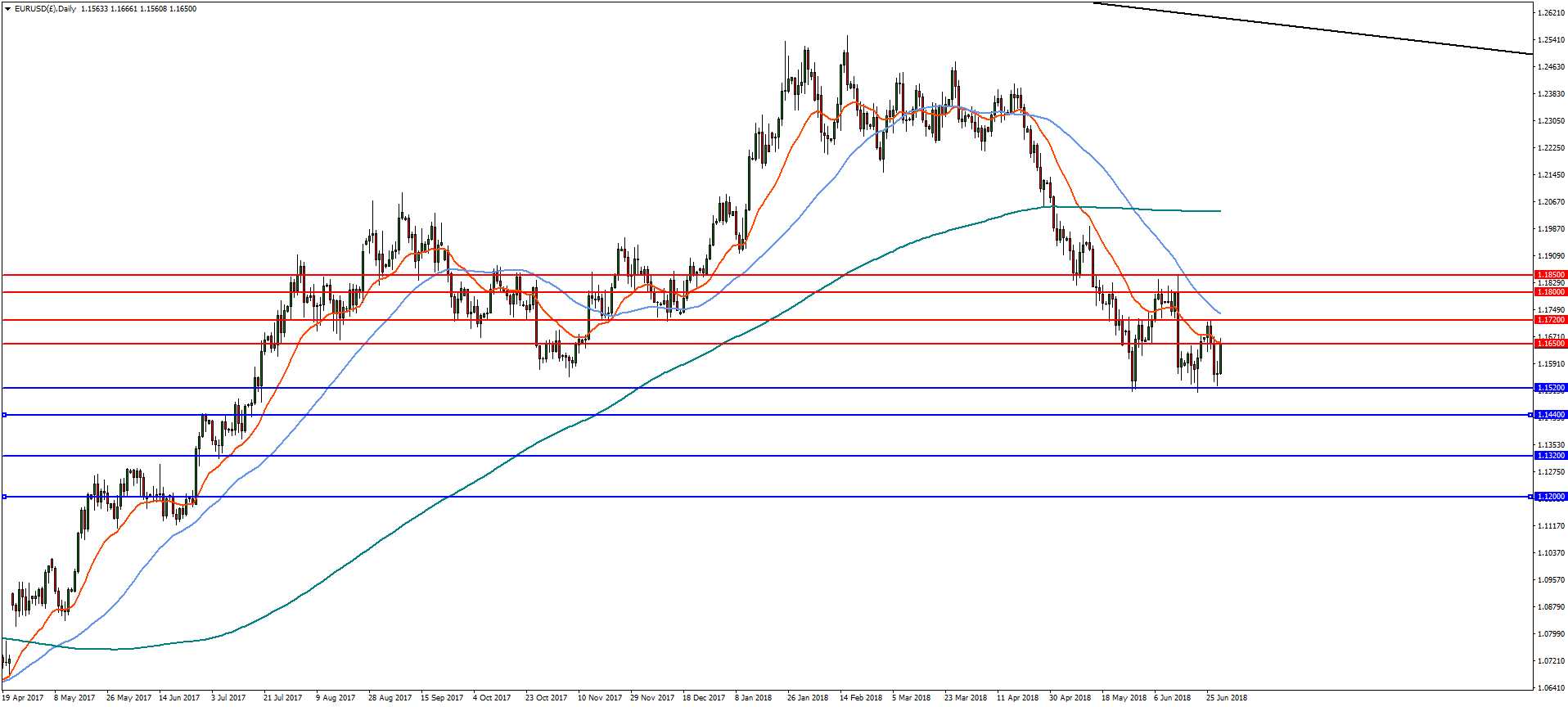

At this point, EUR/USD is staying in range of 1.1507/1851 and intraday bias remains neutral. Outlook remains unchanged too. Further recovery could be seen but we'd expect strong resistance by 1.1851 to limit upside. Larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

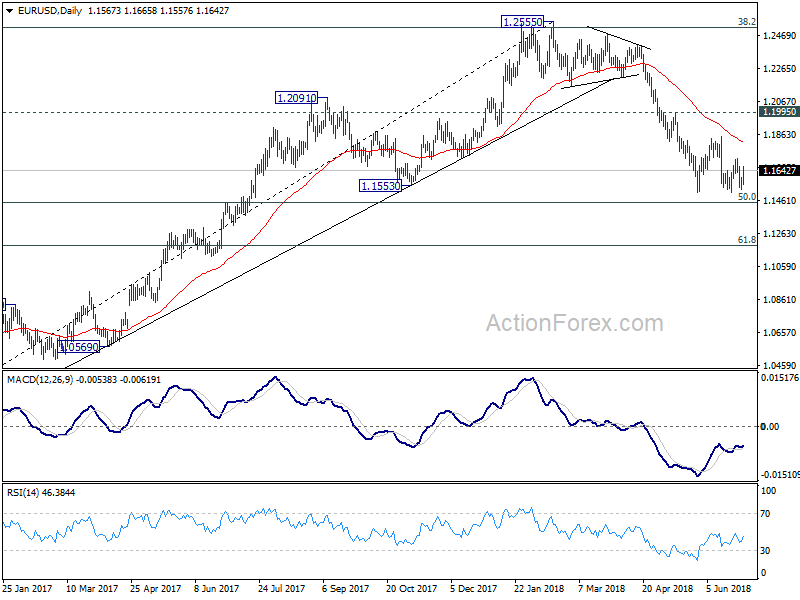

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro to End the Month on a Strong Note, Inflation Data Couldn’t Help Dollar

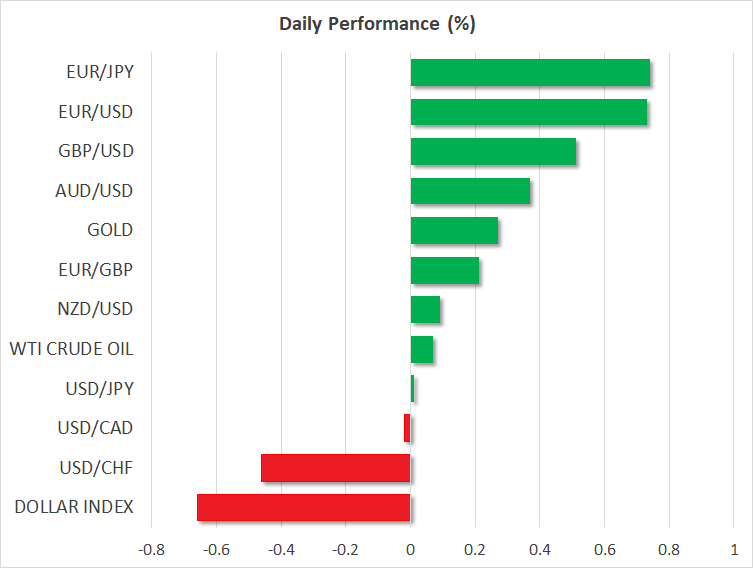

Euro continues to trade as the strongest one for today as boosted by the EU leader's agreement on immigration. While the common hasn't been the star this month, it's indeed up against all but Dollar. European stocks investors are also happy with the result. At the time of writing, DAX and CAC are trading up more than 1% while FTSE is up around 0.6%. Additional support is seen for the common currency as Eurozone headline inflation accelerated to ECB's target of 2%. Sterling, is trading as the second strongest one, with help from upward revision in the final Q1 GDP reading.

Dollar, on the other hand, is not getting much support from stronger than expected inflation data. It's trading as the second weakest one for today, following Yen. The pre-quarter-end rebound in global stocks is set to continue into US session as DOW futures suggest. In other markets, WTI crude oil is holding firm above 73 handle. Gold continues to defend 1250 handle, with help of retreat in Dollar.

US core inflation accelerated to 2.3%, Canada GDP beat expectations

Inflation data released from the US are rather solid. Headline PCE accelerated to 2.3% yoy in May, up from 2.0% yoy and beat expectation of 2.0% yoy. Core PCE also jumped to 2.0% yoy, up from 1.8% yoy and beat expectation of 1.8% yoy. Personal income rose 0.4% in May, matched expectation. Personal spending, though rose 0.2%, below expectation of 0.4%. The data support Fed's projection of two more rate hike this year, in September and December.

Canada GDP rose 0.1% mom in April, above expectation of 0.0% mom. IPPI rose 1.0% mom in May while RMPI rose 3.8% mom. BoC Governor Stephen Poloz has made himself very clear this week. Economic models suggested that there should be a rate hike soon. But models are just part of the equation for the decision. Trade tensions and impacts of higher interest rates on household are factors to consider too. To us, it's 50/50 for BoC to hike in July.

Euro stays strong on EU migration deal and inflation data

Euro jumps broadly today on news that the 28 EU leaders have agreed on the conclusions of the EU summit, including migration. There were some concerns earlier as Italy threatened to block all agreement if they requests on migration were not met. German Chancellor Angela Merkel, who's under political pressure domestically, said that "overall, after an intensive discussion on the most challenging theme for the European Union, namely migration, it is a good signal that we agreed a common text."

Italy's Interior Minister Matteo Salvini, a known anti immigrant leader of the League, said he's pleased with EU's agreement on immigration. He said today that "I'm satisfied and proud of our government's results in Brussels." And, "finally Europe has been forced to discuss an Italian proposal… (and) finally Italy is no longer isolated and has returned to being a protagonist."

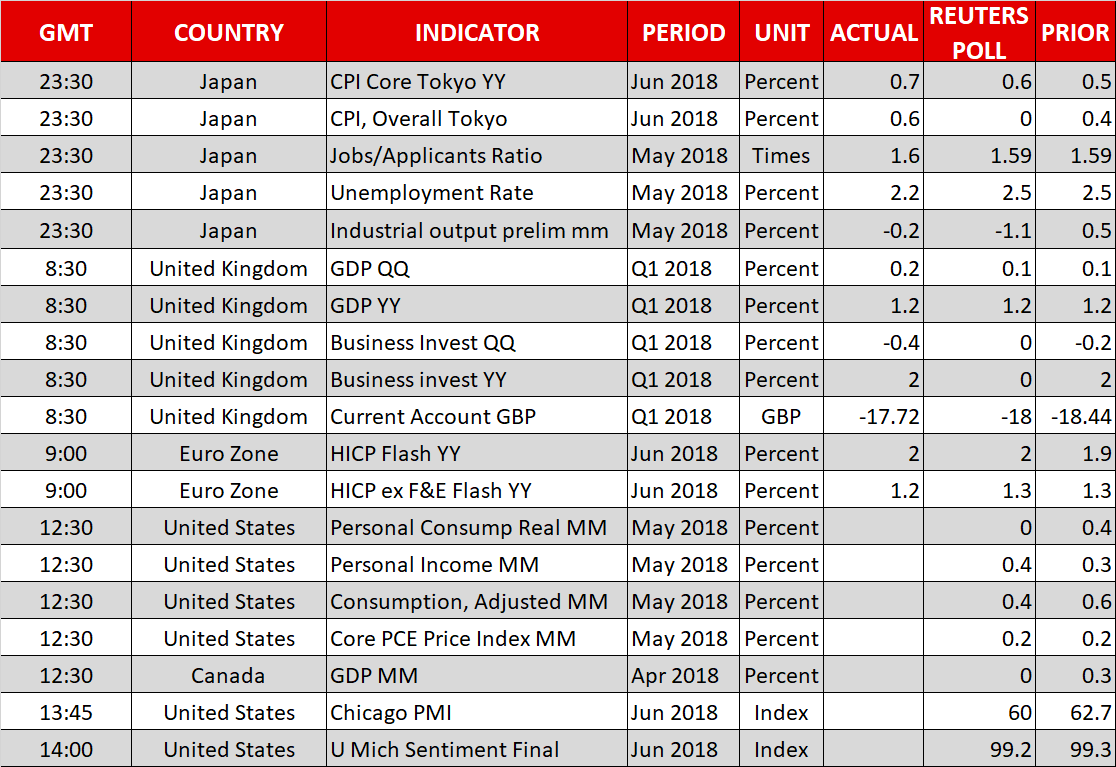

Eurozone CPI rose to 2.0% yoy in June, up from 1.9% yoy and met expectation. CPI core, slowed to 1.0% yoy, down from 1.1% yoy, matched expectation. German unemployment dropped -15k in June. German unemployment rate was unchanged at 5.2% in June.

Sterling lifted by GDP upward revision.

Sterling jumps notably after GDP upward revision. Q1 GDP growth is finalized at 0.2% qoq, revised up from 0.1% qoq. Services made the largest contribution by growing 0.2%. The 0.1% growth in production was offset by the -0.1% contraction in construction. Among services, business and finance services jumped 0.6%, government and other services rose 0.3%. Distribution, hotels and restaurants increased by 0.1%. Transport, storage and communication increased by 0.1%

Also from the UK, mortgage approvals rose to 64.5k in May. M4 dropped -0.4% mom in May. Index of services rose 0.2% 3mo3m in April. Current account deficit narrowed to GBP -17.7B in Q1.GFK consumer confidence dropped to -9 in June.

Swiss KOF Economic Barometer to 101.7, clear contribution from exports

Swiss KOF Economic Barometer rose 1.7 to 101.7 in June, above expectation of 101.0. It's also back above long-term average at 100.0. KOF said it indicates a "slightly above-average development" in Switzerland. But still, the "tailwind for the Swiss economy is no longer as strong as during winter."

Exports made a "particularly clear contribution" to the improvement. There were also "positive developments in domestic demand, with increase in "propensity to consume". In manufacturing and construction, the indicators for order backlogs, inventory reserves and intermediate goods purchasing point to a more positive development. Within manufacturing, however, "signs of developments in the near future are mixed."

Released earlier

On the data front, New Zealand building permits rose 7.1% mom in May. Japan unemployment rate dropped to fresh 25 year low at 2.2%, down from 2.5%. Tokyo CPI accelerated more than expected to 0.7% yoy in June. Industrial production dropped -0.2% mom in May. Housing starts rose 1.3% yoy in May. Consumer confidence dropped to 43.7 in June.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1566 (R1) 1.1604; More.....

At this point, EUR/USD is staying in range of 1.1507/1851 and intraday bias remains neutral. Outlook remains unchanged too. Further recovery could be seen but we'd expect strong resistance by 1.1851 to limit upside. Larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will send EUR/USD through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | 7.10% | -3.70% | -3.60% | |

| 23:01 | GBP | GfK Consumer Confidence Jun | -9 | -7 | -7 | |

| 23:30 | JPY | Jobless Rate May | 2.20% | 2.50% | 2.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 0.70% | 0.60% | 0.50% | |

| 23:50 | JPY | Industrial Production M/M May P | -0.20% | -1.10% | 0.50% | |

| 05:00 | JPY | Housing Starts Y/Y May | 1.30% | -6.00% | 0.30% | |

| 05:00 | JPY | Consumer Confidence Jun | 43.7 | 43.9 | 43.8 | |

| 07:00 | CHF | KOF Leading Indicator Jun | 101.7 | 101 | 100 | |

| 07:55 | EUR | German Unemployment Change (000's) Jun | -15K | -8K | -11k | |

| 07:55 | EUR | German Unemployment Claims Rate Jun | 5.20% | 5.20% | 5.20% | |

| 08:30 | GBP | Mortgage Approvals May | 64.5K | 62K | 62K | |

| 08:30 | GBP | Money Supply M4 M/M May | -0.40% | 0.30% | 0.20% | |

| 08:30 | GBP | Current Account Balance (1Q) | -17.7B | -18.2B | -18.4B | |

| 08:30 | GBP | Index of Services 3M/3M Apr | 0.20% | 0.00% | 0.30% | |

| 08:30 | GBP | GDP Q/Q Q1 F | 0.20% | 0.10% | 0.10% | |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y Jun | 2.00% | 2.00% | 1.90% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun A | 1.00% | 1.00% | 1.10% | |

| 12:30 | CAD | Industrial Product Price M/M May | 1.00% | -0.50% | 0.50% | 0.40% |

| 12:30 | CAD | Raw Materials Price Index M/M May | 3.80% | -0.60% | 0.70% | 0.80% |

| 12:30 | CAD | GDP M/M Apr | 0.10% | 0.00% | 0.30% | |

| 12:30 | USD | Personal Income May | 0.40% | 0.40% | 0.30% | 0.20% |

| 12:30 | USD | Personal Spending May | 0.20% | 0.40% | 0.60% | 0.50% |

| 12:30 | USD | PCE Deflator M/M May | 0.20% | 0.10% | 0.20% | |

| 12:30 | USD | PCE Deflator Y/Y May | 2.30% | 2.00% | 2.00% | |

| 12:30 | USD | PCE Core M/M May | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | PCE Core Y/Y May | 2.00% | 1.80% | 1.80% | |

| 13:45 | USD | Chicago PMI Jun | 60.1 | 62.7 | ||

| 14:00 | USD | U. of Mich. Sentiment Jun F | 99.2 | 99.3 | ||

| 14:30 | CAD | BOC Business Outlook Survey | ||||

| 14:30 | CAD | BOC Business Outlook Survey |

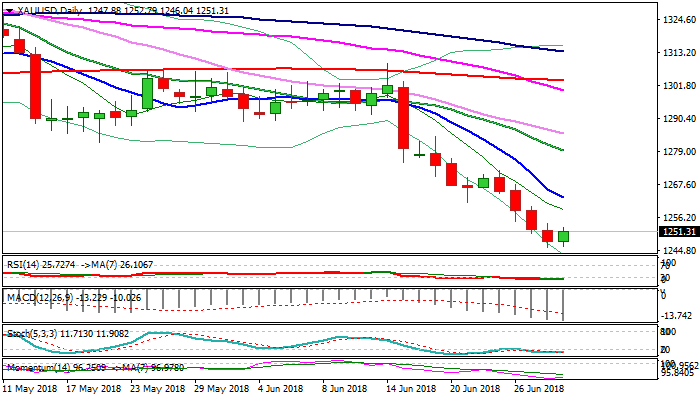

Spot Gold Outlook – Consolidation to Precede Final Push towards $1236 Target

Spot Gold moved higher on Friday but stays near new low at $1245 (the lowest since mid-Dec 2017) posted on Thursday.

Weaker dollar gave a breather to gold bears, but bearish techs and sentiment limit recovery attempts and keep strong bearish stance intact.

Extended recovery attempts are expected to hold below falling 10SMA ($1263) before final push towards target at $1236 (12 Dec low, reinforced by weekly 200SMA).

The notion is supported by the third straight long bearish weekly candle.

Only weekly close above 10SMA would ease existing pressure and open way for stronger recovery.

Res: 1252; 1254; 1260; 1263

Sup: 1245; 1240; 1236; 1231

US core inflation accelerated to 2.3%, Canada GDP beat expectations

Inflation data released from the US are rather solid. Headline PCE accelerated to 2.3% yoy in May, up from 2.0% yoy and beat expectation of 2.0% yoy. Core PCE also jumped to 2.0% yoy, up from 1.8% yoy and beat expectation of 1.8% yoy. Personal income rose 0.4% in May, matched expectation. Personal spending, though rose 0.2%, below expectation of 0.4%.

The data support Fed's projection of two more rate hike this year, in September and December.

Canada GDP rose 0.1% mom in April, above expectation of 0.0% mom. IPPI rose 1.0% mom in May while RMPI rose 3.8% mom.

BoC Governor Stephen Poloz has made himself very clear this week. Economic models suggested that there should be a rate hike soon. But models are just part of the equation for the decision. Trade tensions and impacts of higher interest rates on household are factors to consider too. To us, it's 50/50 for BoC to hike in July.

Germany’s Political Future at Stake after EU Summit

EU summit: main results so far

Migration

- Establishment of 'controlled centres' across the bloc for processing migrants.

- Increased development funding for Africa.

- Curb secondary movements of asylum seekers.

- Reform of EU asylum rules.

Defence

- Strengthen European defence through enhancing investment, capability development and operational readiness.

Trade

- Need to preserve and deepen rules-based multilateral system.

As the European Council meeting draws into its second day, where notably eurozone reforms and Brexit are on the agenda, EU leaders struck a hard-fought deal yesterday on migration already. Apart from strengthening the EU's external borders, they also agreed in a 12-point plan – in a concession to Italy – to establish regional disembarkation platforms for people saved at sea. Migrants should be shared across the EU territory on a voluntary basis and transferred to 'controlled centres' across the bloc for rapid and secure processing of asylum claims. A distinction would be made between irregular/economic migrants earmarked for return and those in need of international protection, for whom the principle of solidarity would apply.

Although the deal is a first step in the right direction and even Italy's Prime Minister Giuseppe Conte signalled satisfaction with it, open questions abound: how many countries would actually be willing to establish these 'controlled centres' on a voluntary basis? Where would successful and failed asylum claimants be sent afterwards? How will the reform of the Dublin Regulation and establishment of a new Common European Asylum System be spelled out? Austria – which has an anti-immigrant government already – will take over the presidency of the EU Council from 1 July. Focus on asylum and migration issues and protection of external borders will remain a hot topic in the meantime.

A viable European solution to migration was particularly important for German chancellor Angela Merkel, who is approaching a weekend ultimatum set by her CSU coalition partner. The agreement includes only a small paragraph on the issue of secondary movements of asylum seekers, calling on members to take all necessary 'internal legislative and administrative measures' to counter movements of asylum seekers across borders.

The key question is whether this vague formulation will be enough for the CSU to relinquish its plan of sending back already-registered asylum seekers at the German border, triggering repercussions for other EU countries such as Austria and Italy. If it does not satisfy the CSU, Interior Minister Horst Seehofer has the power to move ahead unilaterally with his plan of turning away migrants at the border. This would put Merkel in a tight position, where she might feel pressured to relieve Seehofer of his duties for his open defiance. In this case, it is difficult to imagine the CSU remaining part of the German governing coalition. This would leave the CDU/SPD coalition two seats short of a majority in parliament.

A breakdown of the German government is clearly not in the CSU's interest, but it has also manoeuvred itself into a tight corner. Budging from its flagship migration policy would cost it dearly in the upcoming Bavarian state election in October, where the anti-immigrant AfD party is its biggest rival. The CSU is on track to suffer a significant decline in the vote in October, compared with the 47.7% it won in the last state election five years ago, and it may lose its absolute majority of seats. That said, the CSU's ultimatum approach is not without risks: according to an Infratest Dimap poll, 75% of Germans favour a European solution to migration, compared to 22% for a national one. Should the CSU steer Germany into a political crisis, it could also result in a strong voter backlash in the state election.

The next key date to look out for is Sunday 1 July, when CDU/CSU party officials will meet again to discuss immigration, and Seehofer is expected to announce his verdict on Merkel's migration deal. So far, a de-escalation and eventual resolution of the German government crisis remains our base case, as all involved parties have an interest in some kind of compromise solution. That said, we should not underestimate the risk of the German government breaking apart and the toppling of Merkel over the coming months (see scenarios below). Should she be replaced by a more hard-line/conservative candidate, this could also have grave repercussions for the stability and resilience of the EU and bring the European political risk premium back into markets.

Impact fixed income markets

As the EU continues the 'kicking the can down the road' approach with the recent migration deal, it is supportive for the peripheral markets relative to the core EU (Germany).

The migration 'deal' made by the EU is positive for peripheral markets, as it has shown that the EU can find a compromise even though there are several unknown factors in the deal. If Seehofer supports the deal (as in our base case), there is room for more performance in Italy (and Spain and Portugal) across the curve. We typically see a steepener of the Italian curve in this environment between 2Y and 10Y.

If the CSU and Seehofer choose not to support the deal and Germany is thrown into a political crisis, Italy will underperform and the curve will flatten. This is not our base case.

As noted above, we expect the CSU to support the deal and for Merkel to remain as Chancellor of Germany. However, we are still reluctant to buy Italy even though spreads are still at elevated levels. We have some hard budget negotiations coming up in Italy and there is plenty of issuance from the Italian Debt Office, so there is no need to rush in and buy Italian government bonds.

Italy’s Salvini pleased with the EU immigration deal

Italy's Interior Minister Matteo Salvini, a known anti immigrant leader of the League, said he's pleased with EU's agreement on immigration.

He said today that "I'm satisfied and proud of our government's results in Brussels." And, "finally Europe has been forced to discuss an Italian proposal... (and) finally Italy is no longer isolated and has returned to being a protagonist."

European markets are also generally happy with the news. At the time of writing, DAX and CAC are trading up around 1.4%. FTSE is up 0.8%.

Euro continues to trade as the strongest one today, followed by Sterling.

Canadian Dollar Steady Ahead Of Canadian GDP

The Canadian dollar is steady in the Friday session, after posting gains on Thursday. Currently, USD/CAD is trading at 1.3250, down 0.05% on the day. On the release front, Canada releases monthly GDP, which is expected to drop to 0.0%. On the inflation front, the Raw Materials Price Index is forecast to climb to 1.2%. In the US, Core PCE Price Index is expected to remain pegged at 0.2% for a fourth straight month, while Personal Spending is forecast to drop to 0.4%. We’ll also get a look at UoM Consumer Confidence, which is forecast to rise to 99.1 points.

Investors are keeping a close eye on the Bank of Canada, which holds a policy meeting on July 11. The bank has strongly hinted that a rate hike could be coming soon. On Wednesday, BoC Governor Stephen Poloz had a hawkish message for the markets, noting that inflation was on target and the domestic economy was performing well. However, Poloz also mentioned that the trade war between Canada and the U.S was hurting business investment. Currently, the likelihood of a rate hike in July is 55 percent. Canadian economic data in the next two weeks will likely be the determining factor as to whether the BoC presses the rate trigger, or opts to wait until later in the year.

The tariff showdown between the U.S and its major trading partners continues, and the crisis could affect U.S monetary policy. Currently, the Federal Reserve plans to raise rates four times in 2018 (up from three), but a global trade war could force the Fed to revise its forecast down to three hikes. There is a split among Fed policymakers with regard to the number of rate hikes in the second half of 2018. Earlier in the week, Atlanta Fed bank president Raphael Bostic said that if the trade war intensified, he would vote against a fourth rate hike, due to downside risks to the economy. Fed Chair Jerome Powell sounded pessimistic about the economic effects of trade tensions at an ECB forum earlier in June, and if other Fed members express similar concerns, the Fed could delay a fourth hike until 2019.

Stocks Post Relief Rally After EU Deal, US Inflation Data Still To Come

Here are the latest developments in global markets:

FOREX: The euro surged early on Friday following news that the 28 European Union leaders had agreed on migration overnight, driving euro/dollar towards an intraday high of 1.1666 (+0.68%). Also, in terms of economic data, on a yearly basis, the Eurozone preliminary CPI jumped to 2.0% in yearly terms as expected, from 1.9% previously. Euro/yen climbed by 0.68% to 128.66, posting a two-week high. Dollar/yen jumped to a two-week high as well of 110.78, adding 0.05% to its performance and is set to post the fourth consecutive green day, while the US dollar index dived by 0.63%. Sterling moved higher against the greenback (+0.59%) today, after an unexpected upward revision to UK’s Q1 GDP, which increased expectations of monetary policy tightening during the year. The antipodean currencies traded higher with aussie/dollar up by 0.48% to 0.7387, while kiwi/dollar was up by 0.013% after it recorded a one-year low of 0.6759.Dollar/loonie was last seen at 1.3225 (-0.14%).

STOCKS: European equities were in the green on Friday at 1030 GMT, with every single major blue-chip index being comfortably in positive territory as EU leaders reached a deal on migration. The UK’s FTSE 100, German DAX and French CAC 40 were up by 0.88%, 1.27% and 1.39% respectively after a sell-off earlier this week that saw them post multi-week lows. Even the Italian FTSE MIB, which underperformed, was up by a hefty 0.61%. The pan-European Stoxx 600 was up by 1.09% at 380.97 and at a relative distance to Wednesday’s more than two-month low. Meanwhile, the blue-chip Euro Stoxx 50 traded higher by 1.37% as well. Futures tracking the Dow and S&P 500 traded higher, pointing to a higher open on Wall Street.

COMMODITIES: In energy markets, West Texas Intermediate (WTI) crude oil corrected slightly lower, while London-based Brent crude oil moved significantly higher. WTI was down by 0.08% at $73.51 per barrel, however, it remains elevated near the three-and-a-half year high it reached on Thursday. Brent was up by 1.72% at $79.19 per barrel, creating a new one-month high. In precious metals, gold prices edged higher by 0.23% at $1,250.8 per ounce after touching a more than six-month low on Thursday.

Day ahead: US core PCE index awaited; EU summit eyed for Brexit clues

The most crucial releases left on Friday’s calendar are from the US. The core PCE price index, as well as personal consumption and income figures for May are all due for release at 1230 GMT. Beyond these figures, the conclusion of the EU summit in Brussels will be closely watched by sterling traders looking for fresh Brexit clues.

Kicking off with the data, the Fed’s preferred inflation measure – the core PCE price index – is expected to have risen by 1.9% in May on a yearly basis, from 1.8% previously. This would bring the rate within breathing distance of the Fed’s 2.0% inflation target. Meanwhile, expectations are mixed for the rest of the releases. In monthly terms, personal consumption is expected to have risen by 0.4% in May, a slower pace compared to April’s 0.6%, while personal income is forecast to have accelerated to 0.4%, from 0.3% previously.

Investors remain in doubt as to whether the Fed will deliver one, or two more rate increases this year. Whereas one more 25bps hike is already fully priced in, market pricing assigns just a 30% probability for a second one according to the Fed funds futures. A potential positive surprise in these data – especially in the core PCE and consumption figures – could make the prospect of two more rate increases more realistic, thereby bringing the dollar under renewed buying interest. The opposite holds true as well.

The Chicago PMI and final University of Michigan consumer sentiment index, both for June, are also due for release out of the US at 1345 and 1400 GMT respectively.

In Canada, monthly GDP figures will be in focus at 1230 GMT. The oil-exporting economy is expected to have recorded no growth in April, as opposed to the 0.3% seen in March.

In energy markets, the weekly Baker Hughes oil rig count is due at 1700 GMT.

Beyond economic data, the EU summit will wrap up later today, and any remarks on Brexit have the capacity to impact sterling. Following comments from EU chief Brexit negotiator Barnier earlier today that “big divergences” remain, it appears likely the EU leaders could express something along those lines too, highlighting the lack of progress on the Irish border issue.

As for the speakers, Donald Tusk and Jean-Claude Junker, the respective Presidents of the European Council and the European Commission, are expected to hold a press conference at 1130 GMT. Brexit and Eurozone reforms will be among the key topics.

Forex Analysis: EURUSD And DAX Analysis

The European Union leaders have come to an agreement at the EU Summit over immigration after marathon talks in Brussels. The deal appears to include the setting up of migrant centers within the EU and improving border controls. It remains to be seen if the agreement will be sufficient to keep the Merkel coalition government intact. The market reacted with a bounce in the EURUSD pair but the gains could be short-lived as the EU monitory policy differential with the Federal Reserve continues to put pressure on the Euro. However, market sentiment appears to be more optimistic over trade war issues as there have been no new developments over the last couple of days.

Traders should be aware that today is the end of the week, month and quarter so there may be choppy action as money managers adjust their portfolios.

EURUSD

On the daily chart, EURUSD continues to bounce from the 1.1500-1.1520 zone. A break of this support will open the way to continued declines to the 50% retracement from the November 2016 lows at 1.1440 and then 1.1320. To the upside, immediate resistance is at 1.1650 and a break will find strong resistance at the 23.6% and horizontal at 1.1720. A break of 1.1720 will be needed to change the bearish outlook.

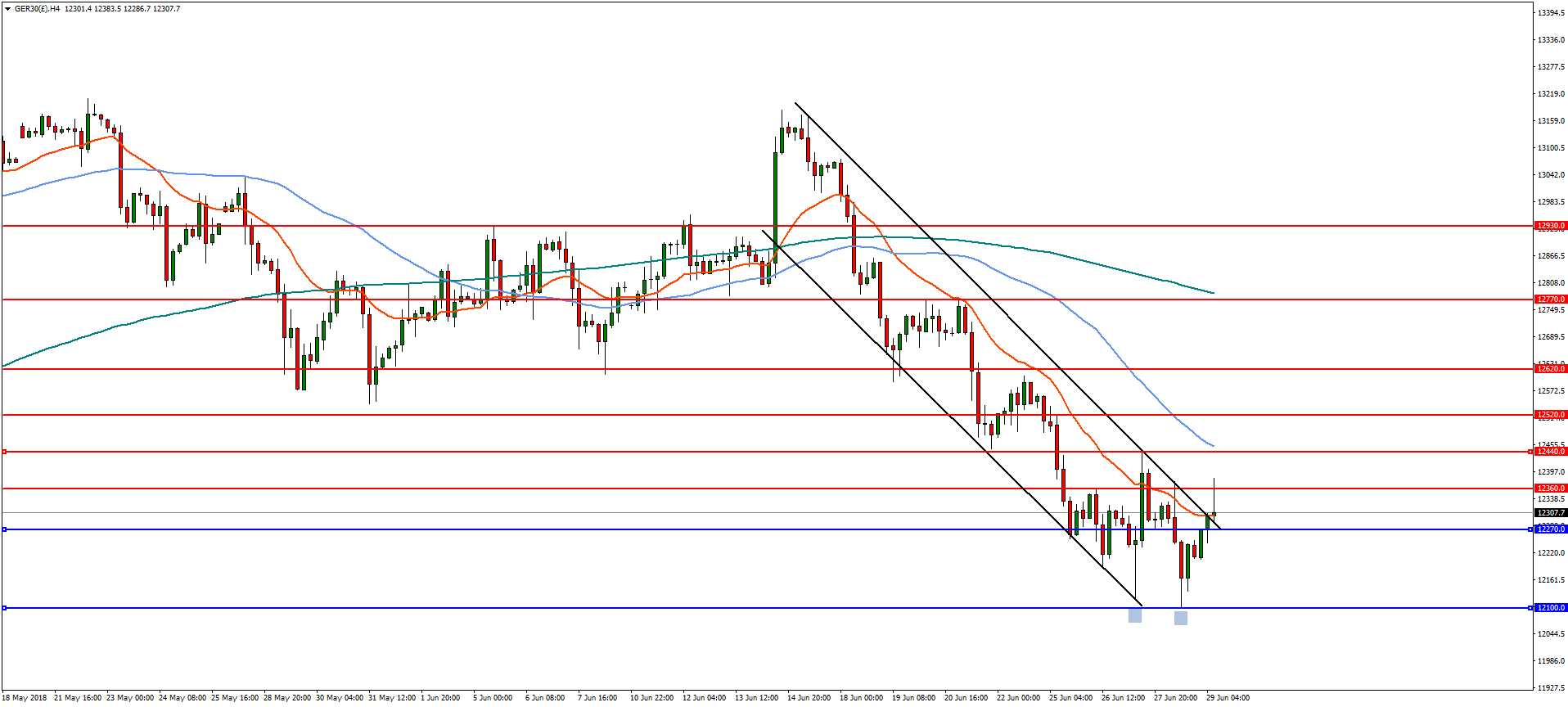

DAX

In the 4-hourly time frame, the DAX index has formed a possible double bottom and broken out of a bearish trading channel. A break of 12360 which is the 23.6% Fibonacci of the decline from the highs in June would indicate a potential upside target of 12620 with resistance at 12440 and 12520. On the flip-side, a reversal below 12270 would open the way for a return to the lows at 12100.

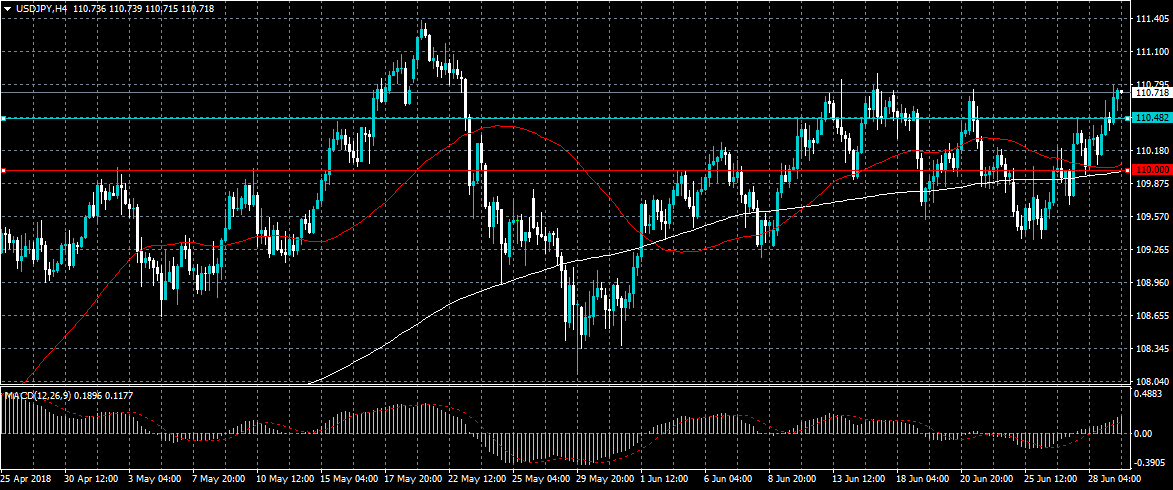

USDJPY Strongly Bullish Above 110.40

The US dollar continues to make gains above the 110.00 level against the Japanese yen, as the EU migrant deal boosts risk-on trading sentiment on Friday. The USDJPY pair has so far found technical resistance from the 110.80 level, and remains intraday bullish above the 110.40 level. Traders now look toward important Inflation and Wage data from the United States economy.

The USDJPY pair is strongly bullish while trading above the 110.40 level, further upside towards the 111.00 and 111.40 levels seems possible.

If the USDJPY pair moves below the 110.40 level, sellers will likely test towards the 110.20 and 110.00 support levels.