Sample Category Title

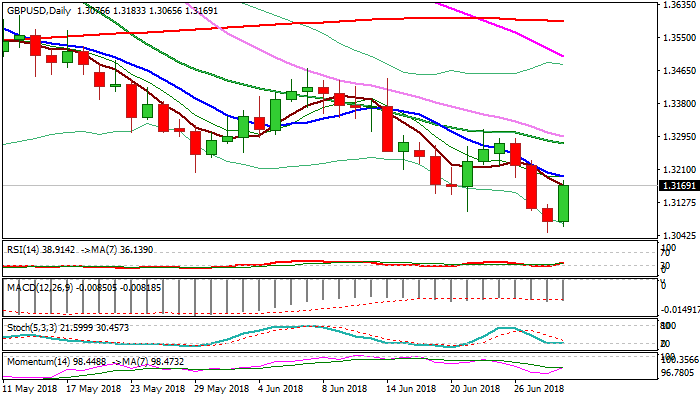

Pound Keeps Firm Tone after Upbeat UK Data, Bulls Pressure 10SMA Pivot

Cable remains firm in early US trading on Friday and regaining traction after pulling back from European session high at 1.3183, posted on acceleration on better than expected UK data.

Current account gap narrowed to 17.7 billion pounds in Q1, beating forecast for 18 billion gap as previous release was revised lower to -19.5 billion from initial -18.4 billion pounds.

GDP rose 0.2% in Q1, beating forecast / previous release at 0.1%.

Fresh bulls emerged above weekly cloud top (1.3254) and pressure descending 10SMA (1.3193) which marks pivotal barrier and close above it is needed to generate fresh bullish signal.

North-heading RSI and momentum support the advance which could extend towards 1.3277 (falling 20SMA) and key 1.33 resistance zone on sustained break above 10SMA.

Res: 1.3193; 1.3233; 1.3277; 1.3300

Sup: 1.3133; 1.3101; 1.3065; 1.3049

GBPUSD: Rallies, Backs Off Lower Prices

GBPUSD: The pair faces further price strength after it rejected lower prices to press higher on Friday. Support lies at the 1.3150 level where a break will turn attention to the 1.3100 level. Further down, support lies at the 1.3050 level. Below here will set the stage for more weakness towards the 1.3000 level. Conversely, resistance stands at the 1.3250 levels with a turn above here allowing more strength to build up towards the 1.3300 level. Further out, resistance resides at the 1.3350 level followed by the 1.3400 level. On the whole, GBPUSD remains biased to upside on correction.

Sunset Market Commentary

Markets

Today, the swings in core US and German bond yields were moderate. Both EMU and US (core PCE) inflation data were close to expectations and had no decisive impact on intraday yields’ trends. The US yield curve bear flattens slightly with 2 & 5 year yields rising 1.5bp while the 30-y yield trades little changed. German bunds slightly outperform with the very long end also outperforming (30-y -2.9 bp). During the morning session, the bund showed a more volatile trading pattern. The moves were probably linked a Reuters article. The article suggested that the ECB is considering buying more long-dated bonds when reinvesting maturing bonds from the APP purchases. It could help to keep a potential rise in LT European yields in check. The article also suggested that ECB, to some extent, could deviate from the capital key when reinvesting in bonds. The bund initially declined after the quotes, but soon reversed the initial losses. The Bund future contract trades little changed (162.50 area). Intra-EMU spreads versus Germany narrowed up to 8 bp with Italy (-6 bp) and Greece (-8 bp) outperforming.

After the EUR/USD short squeeze following the EU-summit migration deal, the pair lost a few ticks before hovering back to its intraday-top (around 1.1660/65 area). The improved in global risk sentiment caps the rise of the dollar against the likes of the euro. The trade-weighted dollar is drifting further south of the important technical 95-barrier, possibly suggesting some easing EM-tensions. USD/JPY remains the exception to the rule. The pair is set for a 4-day winning streak as a moderate risk-on weighs on the yen. EMU inflation matched estimates of 1.0% YoY core inflation and 2.0% YoY headline inflation and had little impact on euro trading. Core PCE inflation in the US came in at an expected 0.2% MoM but was slightly higher than anticipated on a yearly basis (2.0% YoY vs. 1.9% expected). The impact on the dollar was very limited.

Initially, sterling lost further ground against a stronger euro. However, the pound soon pared losses after the ONS increased Q1 growth from 0.1% QoQ to 0.2% QoQ, suggesting the growth slowdown in the first quarter was not as sharp as feared. Chances for an august rate hike rose, and so did sterling. However, EUR/GBP gained back a few ticks, possibly the result of some EU Brexit negotiator Barnier squawking. The pair is currently trading 0.8850 area. So, the jury is still out whether the break of the 0.87/0.8850 consolidation pattern will be confirmed. Cable profited from the EUR/USD short squeeze in the early trading hours and enjoyed a second boost from the GDP upgrade. The pair is currently changing hands at around 1.3150.

News Headlines

At the European Council top in Brussels, Michel Barnier, EU Brexit negotiator, warned that “huge and serious” differences still had to be overcome. He also said the EU would not accept any move to keep Britain in the single market for the goods sector only. Meanwhile, rating agency Moody’s sees the UK-EU negotiations momentum waning, suggesting Brexit uncertainty could “persist for longer than anticipated”.

Larry Kudlow “hopes the Fed understands” that faster economic growth and rising employment don’t cause inflation. Instead, Trump’s pro-business measures have expanded the economy’s potential to grow, according to the president’s top economic adviser.

US Treasury Mnuchin said it’s fake news about Trump push for WTO exit

US Treasury Steven Mnuchin calls the report about Trump wants to exit WTO "fake news" and an "exaggeration."

Mnuchin added that "the president has been clear, with us and with others, he has concerns about the WTO, he thinks there's aspects of it that are not fair, he thinks that China and others have used it to their own advantage, but we are focused on free trade. That's what we're focused on - breaking down barriers."

Earlier today, Axios reported, quoting unnamed source" that Trump also said "I don't know why we're in it. The WTO is designed by the rest of the world to screw the United States." The reported added that "sources with knowledge of the situation say the Trump administration will continue to call attention to various ways in which the U.S. encounters what some Trump advisers perceive is unfair and unbalanced treatment within framework of the WTO."

Canadian April GDP Rises Modestly

Highlights:

- Canadian April GDP came in slightly stronger than anticipated rising 0.1% relative to expectations of unchanged activity with manufacturing unexpectedly rising 0.8% in the month.

- Service-producing industries showed unchanged activity in the month after rising 0.2% in March.

Our Take:

GDP growth in April rose 0.1% following solid gains of 0.3% and 0.4% in March and February, respectively. Much of the slowing was due to transitory factors that are expected to reverse in May. For Q2 as a whole we are assuming annualized GDP growth of 2.2% up from the 1.3% recorded in Q1. The pace of growth over the second half of 2018 is expected to be buffeted by a complete shutdown of a major oil sands production facility in July due to a transformer malfunction. This could send Q3 growth back down closer to the Q1 growth rate though Q4 activity will likely bounce back with growth rising around 2 1/2%. Annual 2018 growth will be little changed from our current forecast of 2%. The projected growth this year will be down from the 3.0% recorded in 2017. However, with the economy at capacity a slowing closer to the economy’s potential rate of 1.8% is not undesired. Given monetary conditions remain highly stimulative, our expectation is that the Bank of Canada will continue to withdraw stimulus from the system to maintain this lower pace of growth. We expect another 25 basis point hike in the overnight rate in July followed by similar-sized moves the following three quarters raising the overnight rate 100 basis points to 2.25% by mid-2019. The risk of trade protectionism could stall this tightening though recent comments by the Bank of Canada imply material impacts would need to emerge either in terms of specific tariffs or evidence of weakening confidence weighing on business investment.

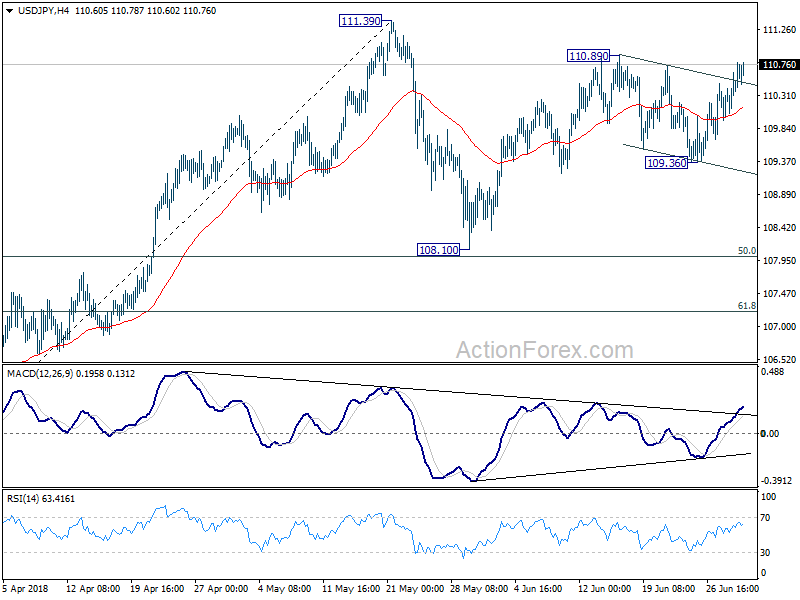

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.09; (P) 110.38; (R1) 110.80; More...

Intraday bias in USD/JPY remains neutral with focus on 110.89. Break there will resume the rise from 108.10 and target 111.39. Firm break there will resume the rally from 104.62 and target 114.73 key resistance. On the downside, below 109.36 will extend the consolidation from 111.39 with another decline. But we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

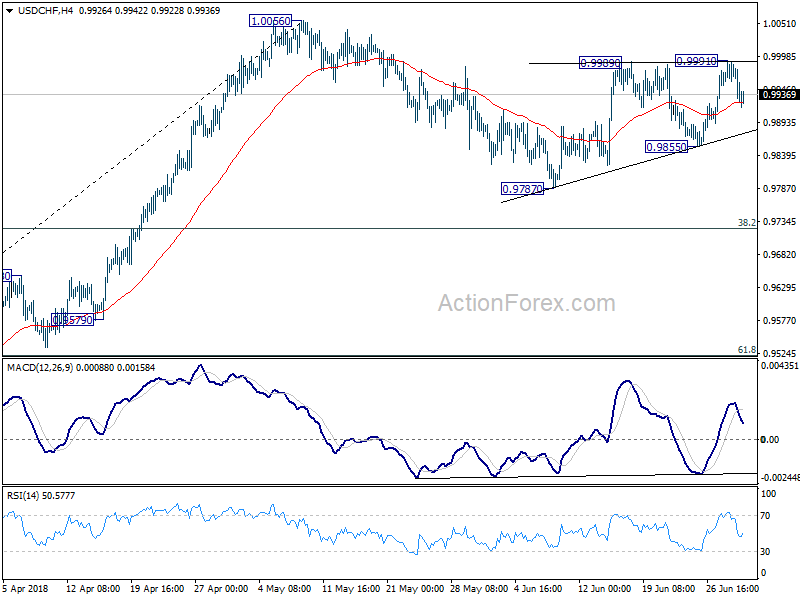

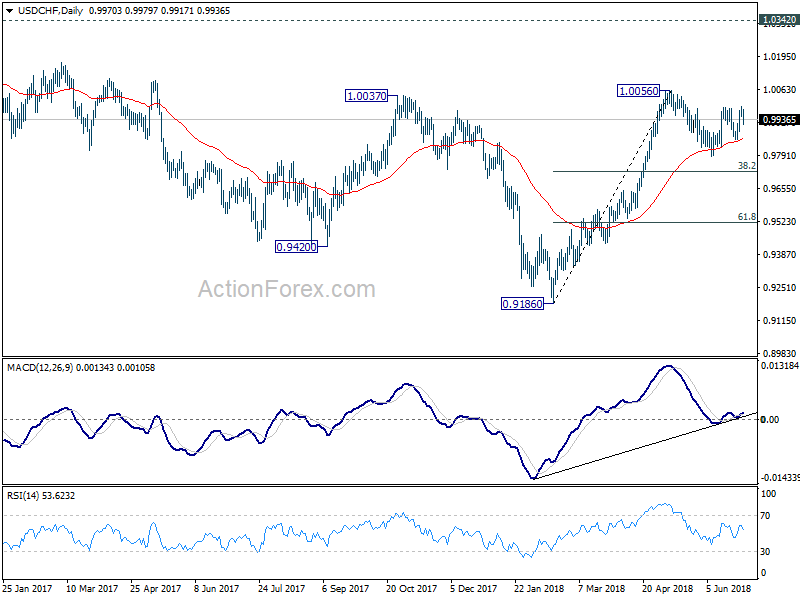

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9954; (P) 0.9973; (R1) 0.9996; More...

Intraday bias in USD/CHF remains neutral for the moment. On the upside, break of 0.9991 will resume the rebound from 0.9787 and target 1.0056 high. Break will resume whole rally from 0.9186. On the downside, below 0.9855 will likely resume the correction from 1.0056 through 0.9787 support. But downside should be contained by 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

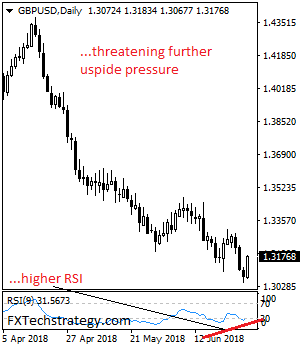

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3043; (P) 1.3085; (R1) 1.3119; More...

GBP/USD formed a temporary low at 1.3048 with today's recovery. Intraday bias is turned neutral for consolidation. Upside should be limited by 1.3314 resistance to bring fall resumption. Below 1.3048 will resume whole decline from 1.4376. Next target is 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. Break there will target 61.8% projection of 1.4376 to 1.3101 from 1.3471 at 1.2683.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Canadian Economy Ekes Out a Gain in April

Overall economic activity edged higher in April, up 0.1% month-on-month, beating expectations for a pause. Outsized declines in a few key sectors constrained the pace of expansion, which nevertheless showed decent breadth as 15 of the 20 major industries expanded output during the month.

Goods-producers led the way higher in April. Manufacturing rose 0.8% as the bulk of subsectors saw expansion, including, notably, a 2.8% gain in machinery manufacturing output. Utilities output was up 1.6%, reflecting colder-than-typical weather that included an ice storm in a number of provinces. Construction activity was also hit, down -0.5%.

Weather effects also appear to have hit the service sector. Overall output was up just a tick, still good to generate a 25th straight month of expansion. Activity was held back by retail trade (-1.3%), led, according to Statistics Canada, by declines at stores 'associated with springtime activities'. Weather was also seen as impacting accommodation and food services (-0.4%).

Statistics Canada reported an increase of activity at the offices of real estate agents and brokers (+0.5%), the first expansion of 2018 after mortgage rule changes slowed activity through the first three months.

Key Implications

Another pleasant surprise. With cold weather in much of the country, one-off factors hitting the mining and oil and gas industries, and some soft advance indicators, it was a welcome surprise to see a modest expansion of the Canadian economy in April.

What's more, to the extent that weather played a role in holding back growth, we should see an acceleration in May as this factor reverses. All told, we remain comfortable with our second quarter growth tracking of 2.4% (annualized) – a solidly above-trend figure that is welcome after the soft start to the year.

It is worth noting that our tracking isn't that far off the Bank of Canada's expectation in April of 2.5%. The details will probably be seen as encouraging, notably the expansion of machinery manufacturing and the return to growth at real estate agents and brokers offices. This is of course a backwards-looking report, and the Business Outlook Survey due at 10:30 this morning will likely be a significant factor in the Bank's deliberations ahead of the July 11th interest rate decision.

US: 2% Inflation Target Reached in May

As expected, personal income rose 0.4% in May, bang on market expectations. Adjusted for inflation and removing taxes, real disposable income was up 0.2% in the month.

Personal spending was slightly below market expectations, but still rose a respectable 0.2% in nominal terms in May. However, inflation meant that spending was flat in real terms. Real spending was held back by a decrease in spending for services, which was partially offset by spending on goods, particularly recreational goods and vehicles. A decline in outlays for household utilities held back services spending.

Perhaps most closely watched in this release these days is the inflation data. The PCE deflator rose 0.2% in May, right on expectations, as did the core metric, up a matching 0.2% on the month. On a year-on-year basis the core PCE deflator hit 2% in May, up from 1.8% in April. That puts the Fed’s preferred inflation gauge right on target

The personal saving rate rose by 0.2 percentage points to 3.2%.

Key Implications

Mission accomplished. After underperforming the Fed’s inflation target for many years, U.S. inflation has finally attained the elusive 2% pace. This supports our view that the Fed can continue to raise rates at a gradual pace. We expect two more 25 basis point hikes this year, as the Fed now shifts its focus from weaker-than-anticipated inflation, to containing upside risks.

May’s spending data confirms that consumers sprang back into action in Q2, but the rebound has a little less height than previously assumed. Consumer spending in real terms now looks to be tracking just shy 3%, rather than the 3.5% we had forecast in our recent QEF. Still, given widespread strength in other components we continue to expect the economy to grow by more than 4% annualized in the quarter.