Sample Category Title

Markets Buoyed By EU Immigration Deal

- Italy and Merkel the big winners from EU deal;

- GBP rallies as GDP data increases chance of August hike;

- Plenty of US data to come today.

It’s been a more positive start to trading on Friday, with investors apparently buoyed by the news that EU leaders reached an agreement on immigration.

While something like this would not necessarily be a market moving event, the fragile political environment in the euro area right now means no agreement could have had serious and worrying consequences. Not only could a failure to reach an agreement have increased the divisions that are growing between Italy’s new populist government and others, it could have led to the collapse of the German coalition government.

This all sounds very dramatic but immigration has been a very divisive issue for Europe for some time now and has contributed to the rise of populist parties, many of which don’t share the same affinity for the single currency as the current establishments. Angela Merkel has also long been the only strong and stabilising factor in the region and the collapse of her government over the issue could be seen as a very worrying sign of things to come.

Investors are clearly pleased with the outcome, with European indices up around 1% and that feeling is being seen throughout the markets with risk appetite having returned following a period of trade-related worry. US futures are currently pointing to gains of around half a percent for the major indices, while the euro is also rallying in response to the news.

The pound is also making decent gains this morning, benefiting from a combination of improved risk appetite but also the small upward revision to first quarter GDP – up from 0.1% to 0.2% on a quarterly basis - which triggered a decent rally in the currency. The upward revision goes some way to confirming the view of the Bank of England that the first quarter wasn’t as bad as it initially appeared and gives further reason to follow through on plans to raise rates even if that may come a few months after initially intended.

The data comes on top of improvements to other economic indicators for the UK and the meeting last week in which Andy Haldane became the third policy maker to vote in favour of a hike. Markets are currently pricing in a 56% chance of a rate hike at the next meeting in August, something that should increase if we continue to see these improvements in the data before then.

Today there’s a number of data releases that traders will be aware of. US income, spending and inflation data will be of particular interest as the Federal Reserve continues on the path to four rate hikes in 2018, as will the UoM consumer sentiment and Chicago PMI surveys.

Constructive Events Seen For Europe During The Session

Notes/Observations

- EU leaders reach agreement on migration on a voluntary basis; centers will determine genuine migrants, and irregular migrants whom would be turned back.

- German unemployment remains at record low level

- UK Final Q1 GDP data revised slightly higher but overall annual pace the slowest in 4 years

- EU Jun inflation data continued to prove constructive for the ECB game plan

- Indonesia Central Bank delivered an aggressive rate hike to help guard the IDR currency (Rupiah)

Asia:

- PBOC sets USD/ CNY mid-point today at 6.6166 for its weakest onshore fixing since December 13th 2017

- China NDRC said it would properly control the amount of foreign debt, as it noted that some companies overseas borrowing amounts were too large.

- Japan May Jobless Rate: 2.2% v 2.5%e (over 25-year low)

Europe:

- EU leaders said to reach deal on migration with accord including clauses on voluntary hosting of migrants in the EU and reform of asylum system by consensus.

- Italy PM Conte stated that his country was no longer alone after EU summit that reached deal on migration. Italy would decide later whether to set up migrant centers in the country.

- UK PM May reiterated view that she wanted a deal that works for both the UK and EU and sought to accelerate Brexit talks after London published white paper on futures ties with EU in July

Americas:

- Fed Banking Sector Stress test (part 2): 34 out of 35 banks had capital planning processes that met Fed’s expectations. Fed failed Deutsche Bank citing “widespread and critical deficiencies”

Economic Data:

- (ID) Indonesia Central Bank (BI) raised the 7-Day Reverse Repo Rate by 50bps to 5.25% (more than expected

- (DE) Germany May Retail Sales M/M: -2.1% v -0.5%e; Y/Y: -1.6% v +1.9%e

- (DE) Germany May Import Price Index M/M: 1.6% v 0.9%e; Y/Y: 3.2% v 2.4%e

- (DK) Denmark Q1 Final GDP Q/Q: 0.4% v 0.4%e; Y/Y: -0.6% v -0.5% prelim

- (DK) Denmark May Gross Unemployment Rate: 4.0% v 4.0%e; Unemployment Rate (seasonally adj): 3.2% v 3.3%e

- (FI) Finland Apr Final Trade Balance: €0.1B v €0.1B prelim

- (NO) Norway May Retail Sales W/Auto Fuel M/M: 1.8% v 0.3%e

- (ZA) South Africa May M3 Money Supply Y/Y: 5.7% v 6.2%e; Private Sector Credit Y/Y: 4.6% v 4.9%e

- (FR) France Jun Preliminary CPI M/M: 0.1% v 0.1%e; Y/Y: 2.1% v 2.1%e

- (FR) France Jun Preliminary CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 2.4% v 2.4%e

- (FR) France May PPI M/M: +0.6% v -0.7% prior; Y/Y: 2.9% v 2.3% prior

- (FR) France May Consumer Spending M/M: 0.9% v 0.8%e; Y/Y: -0.2% v +0.1%e

- (CH) Swiss Jun KOF Leading Indicator: 101.7 v 99.7e

- (AT) Austria May PPI M/M: 0.6% v 0.3% prior; Y/Y: 2.4% v 1.4% prior

- (CZ) Czech Q1 Final GDP (3rd reading) Q/Q: 0.5% v 0.4%e; Y/Y: 4.2% v 4.4%e

- (HU) Hungary May PPI M/M: +1.9% v -0.3% prior; Y/Y: 5.3% v 2.7% prior

- (TR) Turkey May Trade Balance: -$7.8B v -$7.7Be

- (CN) Weekly Shanghai copper inventories (SHFE): 264.0K v 255.4K tons prior

- (SE) Sweden May Household Lending Y/Y: 6.6% v 6.7%e

- (SE) Sweden Apr Non-Manual Workers Wages Y/Y: 1.7% v 2.5% prior

- (TH) Thailand May Current Account: $1.0B v $1.5Be; Overall Balance of Payments (BOP): $0.0B v $0.9Be; Trade Account Balance: $2.7B v $0.2B prior; Exports Y/Y: 13.1% v 14.6% prior; Imports Y/Y: 12.7% v 22.7% prior

- (DE) Germany Jun Unemployment Change: -15K v -8K); Unemployment Claims Rate: 5.2% v 5.2%e (rate matches record low)

- (CZ) Czech May M2 Money Supply Y/Y: 5.2% v 4.4% prior

- (NO) Norway Jun Unemployment Rate: 2.2% v 2.2%e

- (NO) Norway Central Bank (Norges) July Daily FX Purchases (NOK): -600M v -750M prior

- (RU) Russia Narrow Money Supply w/e Jun 22nd: 10.16T v 10.18T prior

- (ES) Spain Apr Current Account: -€1.5B v +€0.9B prior

- (UK) Q1 Final GDP (3rd reading) Q/Q: 0.2% v 0.1%e; Y/Y: 1.2% v 1.2%e (slowest annual pace since 2012)

- (UK) Q1 Final Total Business Investment Q/Q: -0.4% v -0.2%e; Y/Y: 2.0% v 2.0%e

- (UK) Q1 Current Account: -£17.7B v -£17.9Be

- (UK) May Mortgage Approvals: 64.5K v 62.3Ke

- (UK) May Net Consumer Credit: £1.4B v £1.5Be; Net Lending: £3.9B v £3.7Be

- (UK) May M4 Money Supply M/M: 0.4% v 0.1% prior; Y/Y: 1.8% v 1.2% prior; M4 ex-IOFC 3-month Annualized: +3.4% v -0.8% prior

- (UK) Apr Index of Services M/M: 0.3% v 0.3%e; 3M/3M: 0.2% v 0.0%e

- (PT) Portugal Jun Preliminary CPI M/M: 0.1% v 0.4% prior; Y/Y: 1.6% v 1.0% prior

- (PT) Portugal Jun Preliminary CPI EU Harmonized M/M: 0.1% v 0.8% prior; Y/Y: 2.0% v 1.4% prior

- (EU) Euro Zone Jun Advance CPI Estimate Y/Y: 2.0% v 2.0%e; CPI Core Y/Y: 1.0% v 1.0%e

- (GR) Greece Apr Retail Sales Value Y/Y: 1.3% v 1.5% prior; Retail Sales Volume Y/Y: 0.8% v 1.2% prior

- 05:00 - (IS) Iceland May Final Trade Balance (ISK): -17.3B v -12.8B prelim

Fixed Income Issuance:

- (IN) India sold total INR120B vs. INR120B indicated in 2022, 2028, 2035 and 2055 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +1.6% at 3,413, FTSE +0.7% at 7,671, DAX +1.5% at 12,354, CAC-40 +1.3% at 5,343; IBEX-35 +1.2% at 9,702, FTSE MIB +1.6% at 21,775, SMI +1.2% at 8,564 , S&P 500 Futures +0.6%]

- Market Focal Points/Key Themes: European indices open higher across the board; risk sentiment supported following agreement with EU28 leaders; Malta and Ukraine closed for holiday; with light earnings news flow, focus is on heavy macro schedule; materials and technology sectors lead gainers; consumer discretionary underperforming; Peru closed for holiday; earnings releases expected in the upcoming US session include Greenbrier and Constellation Brands; European Medicines Agency expected to results of latest CHMP meeting

Equities

- Consumer discretionary: Assystem ASY.FR -5.9%(outlook), Casino Guichard-Perrachon +4.2% CO.FR (analyst action)

- Financials: Caixabank CABK.ES +5.4% (aset sale), Serco SRP.UK -4.9% (outlook)

- Healthcare: Galapagos GLPG.BE -9.1% (study results)

- Industrials: Air Liquide +1.8% AI.FR (acquisition)

- Materials: Clariant +2.2% (SABIC considerign stake boost), DSM +2.5% DSM.NL (analyst action), Eramet ERA.FR +2.8% (facility for MDL holders)

- Technology: Schneider Electric SU.FR +2.0% (partnership)

- Telecom: Claranova CLA.FR +7.9% (buyback), Mediaset MS.IT -4.0% (analyst action)

Speakers

- ECB reportedly considers buying more longer-term bonds from 2019 as part of QE reinvestments to maintain portfolio duration

- EU chief Brexit negotiator Barnier: Progress made on Brexit; huge divergence over Ireland border issue remain

- Spain govt said to seek to raise €6.5B through higher taxes. New govt looked to raise income tax on the highest earners and sought a minimum 15% on corporate tax for multinationals. Also looking to raise tax on diesel fuel

- German CSU official Michelbach: EU leader agreement on migration was a positive signal. Added that the alliance with CDU party in govt had absolute priority (**Note: German Chancellor Merkel had been under pressure to reach a deal on migration issue from Interior Minister Seehofer (head of her Bavarian coalition partner the CSU)

- EU's Brexit negotiating team said to reject any Brexit deal which allowed the UK to remain in the single market for goods

- Reportedly employees at dozens of leading banks to face a German tax-evasion probe

- Turkey President Chief Adviser Ertem: Central bank is independent; treasury policies to be optimized with the new govt structure. Inflation targeting remained intact

- Indonesia Central Bank Gov Warjiyo pre-rate decision press conference noted that it would keep a front loaded, preemptive monetary policy. Reiterated view to guard IDR currency (Rupiah) to be in line with fundamentals and saw Q2 economic growth improving. Reiterated to continue supporting the market with duel interventions of FX and bonds

- India interim Fin Min Goyal: INR currency (Rupee) volatility due to external factors; no need for knee-jerk response

- Thailand Central Bank: Jun CPI to accelerate due to oil prices and weak THB currency (Baht)

- China PBoC Xu reiterated view that the domestic economy was capable to face external shocks. The deleveraging pressure was mostly on government and state-owned enterprises (SOEs) and that Rapid rise in household leverage 'preliminarily controlled'.

- Hong Kong Chief Executive Lam: To revise pricing mechanism of subsidized housing

- Russia Energy Min Novak: Could increase oil production in July by 200K bpd in the post OPEC+ agreement

Currencies

- Positive events in Europe caused the USD to move away from recent cycle highs. Focus will turn back to trade as the US prepares to present a list to help remedy the trade environment

- Euro was firmer in the aftermath of the EU leaders finding common ground on a migration plan. The EUR/USD was in the mid-1.16 area as a result with the Euro having its best trading day in a month. The pair has repeatedly held psychological support at the 1.15 handle and remained well contained in the 1.15-1.20 quarterly trading range. Constructive European inflation data also providing some tailwinds for the Euro

- A slight upward revision in UK Q1 GDP QoQ reading helped the GBP currency move away from recent 7-month lows. GBP/USD edging back towards the 1.32 area after probing 1.30 earlier in the week

- Indonesia delivered an aggressive rate hike to help guard the IDR currency and moved its monetary policy stance to tight from neutral. USD/IDR firmer by 0.4% just ahead of the NY morning.

Fixed Income

- Bund Futures trade 8 ticks lower at 162.22 as the curve flattened following the ECB sources report. Upside targets 162.75 followed by 163.25, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.00 lower by 17 ticks after QoQ GDP was revised higher. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Friday's liquidity report showed Thursday's excess liquidity declined from €1.801T to €1.793T. Use of the marginal lending facility fell from €97M to €30M.

- Corporate issuance saw Charter Communications raise $1.5B secured debt in the primary market

Looking Ahead

- (US) Treasury Dept to release report related to China trade issues

- (BR) Brazil May CNI Capacity Utilization: No est v 78.1% prior

- (MX) Mexico May YTD Budget Balance (MXN): No est v 5.8B prior

- 05:30 (SL) Sri Lanka Jun CPI Y/Y: No est v 4.0% prior

- 05:30 (ZA) South Africa to sell ZAR600M in I/L 2029, 2033 and 2050 bonds

- 06:00 (PT) Portugal May Industrial Production M/M: No est v -3.1% prior; Y/Y: No est v 3.8% prior

- 06:00 (PT) Portugal May Retail Sales M/M: No est v -4.2% prior; Y/Y: No est v 0.7% prior

- 06:00 (UK) DMO to sell combined £4.5B in 1-month, 6-month and 12-month Bills £1.5B, £1.5B and £1.5B respectively)

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 07:30 (IN) India Apr Eight Infrastructure (key industries) Y/Y: % v 4.7% prior

- 08:00 (BR) Brazil May National Unemployment Rate: 12.6%e v 12.9% prior

- 08:00 (ZA) South Africa May Budget Balance (ZAR): No est v -43.7B prior

- 08:00 (ZA) South Africa May Trade Balance (ZAR): 5.8Be v 1.1B prior

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) May Personal Income: 0.4%e v 0.3% prior; Personal Spending: 0.4%e v 0.6% prior; Real Personal Spending (PCE): 0.2%e v 0.4% prior

- 08:30 (US) May PCE Core M/M: 0.2%e v 0.2% prior; Y/Y: 1.9%e v 1.8% prior

- 08:30 (US) May PCE Deflator M/M: 0.2%e v 0.2% prior; Y/Y: 2.2%e v 2.0% prior

- 08:30 (CA) Canada Apr GDP M/M: 0.0%e v 0.3% prior; Y/Y: 2.4%e v 2.9% prior

- 08:30 (CA) Canada May Industrial Product Price M/M: 0.9%e v 0.5% prior; Raw Materials Price Index M/M: No est v 0.7% prior

- 09:00 (CL) Chile May Industrial Production Y/Y: 2.4%e v 7.6% prior; Manufacturing Production Y/Y: 2.2%e v 11.8% prior

- 09:00 (CL) Chile May Unemployment Rate: 6.9%e v 6.7% prior

- 09:00 (RU) Russia Q1 Final Current Account: No est v $28.8B prelim

- 09:30 (BR) Brazil May Nominal Budget Balance (BRL): -43.5Be v -26.8B prior; Primary Budget Balance: -12.4Be v 2.9B prior; Net Debt to GDP ratio: 51.4%e v 51.9% prior

- 09:45 (US) Jun Chicago Purchasing Manager: 60.0e v 62.7 prior

- 10:00 (US) Jun Final University of Michigan Confidence: 99.0e v 99.3 prelim

- 10:00 (MX) Mexico May Net Outstanding Loans (MXN): No est v 4.13T prior

- 10:30 (CA) Bank of Canada (BOC) Q2 Senior Loan Officer Survey: No est v -5.2 prior

- 11:00 (CO) Colombia May National Unemployment Rate: No est v 9.5% prior, Urban Unemployment Rate: 10.2%e v 10.7% prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 15:00 (AR) Argentina May Industrial Production Y/Y: -2.0%e v +3.4% prior

- 15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to leave Overnight Lending Rate unchanged at 4.25%

- 19:00 (NZ) RBNZ Dep Gov Bascand

- 21:00 (CN) China Jun Official Govt Manufacturing PMI: 51.7e v 51.9 prior; Non-manufacturing PMI: 54.8e v 54.9 prior, Composite PMI: No est v 54.6 prior

- 21:20 (FR) ECB’s Couere (France) in Singapore

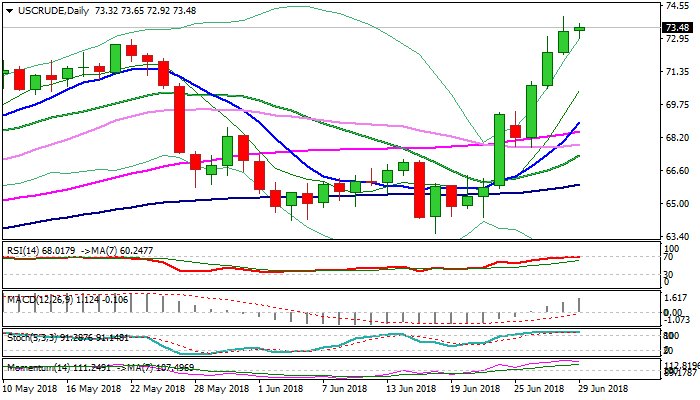

WTI Oil Outlook: Limited Downside On Consolidation Under New High But Deeper Correction Could Be Anticipated

WTI oil holds firm on Friday after pullback from new 3 1/2 year high at $74.01 (posted on Friday) found footstep at $72.92 before the price moved higher again. Expectations were for deeper pullback on profit-taking at the end of the week, which was marked by strong rally of oil price, but dip could be so far described as minor and bulls remain firmly in play. Investors continue to take advantage of strong bullish sentiment, helped by output reduction from Libya and Canada and sanctions on Iran, as well as lower than expected production increase from major oil producers, which was designed to prevent shortage in oil market and upbeat crude inventories data. WTI oil is on track for the second straight strong bullish weekly close which would underpin for further advance and weekly close above previous top at $72.89 is needed to confirm and signal extension of two-week rally from $63.58 trough. Bulls eye next significant barrier at $76.35 (Fibo 61.8% of $107.45/$26.04, Jun 2014 / Feb 2016 fall) violation of which would unmask psychological $80 barrier. Daily tech are bullish and maintain strong momentum, ignoring for now overbought conditions, however, corrective action could be anticipated in coming sessions.

Res: 73.65, 74.01, 75.09, 76.45

Sup: 72.92, 72.19, 71.55, 70.55

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

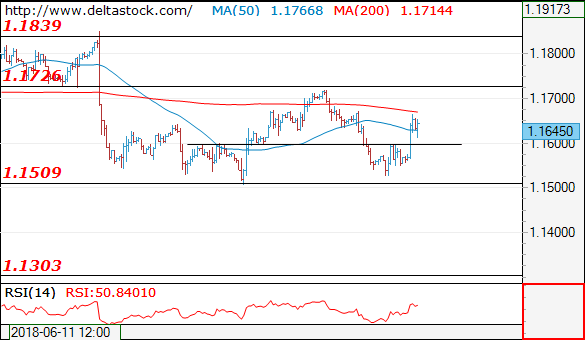

EUR/USD

Current level - 1.1645

The intraday bias is still positive above 1.1600, as the pair currently struggled below 1.1670 dynamic resistance. An eventual break through the latter will challenge 1.1720 area. My outlook on the senior frames remains bearish, for a violation of 1.1510 lows, towards 1.1300.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1670 | 1.1730 | 1.1600 | 1.1510 |

| 1.1730 | 1.1830 | 1.1510 | 1.1300 |

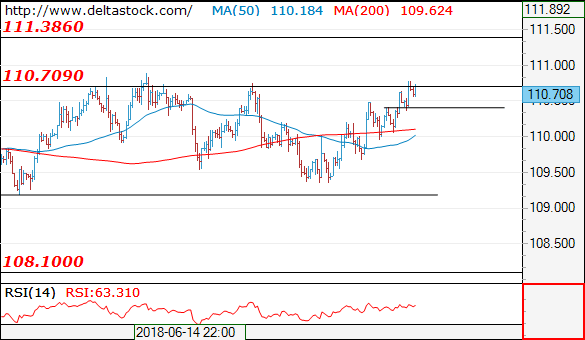

USD/JPY

USD/JPY

Current level - 110.78

There is still no sign of a reversal and the intraday bias is positive, for a rise towards 111.40 area. Initial support is projected at 110.40, followed by 110.00.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 110.80 | 111.40 | 110.40 | 107.80 |

| 111.40 | 114.40 | 110.00 | 106.70 |

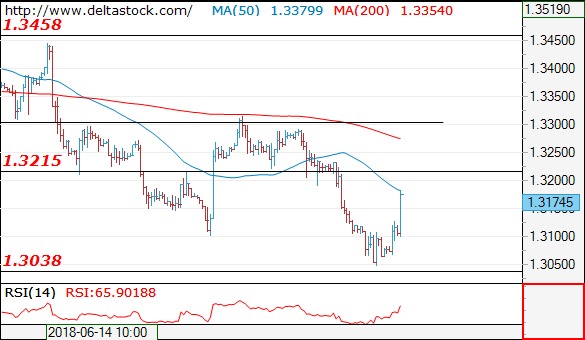

GBP/USD

Current level - 1.3174

The intraday rise should be capped at 1.3200 resistance, for another downswing towards 1.3040. Minor intraday support lies at 1.3120.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3200 | 1.3618 | 1.3120 | 1.3040 |

| 1.3310 | 1.3990 | 1.3040 | 1.2770 |

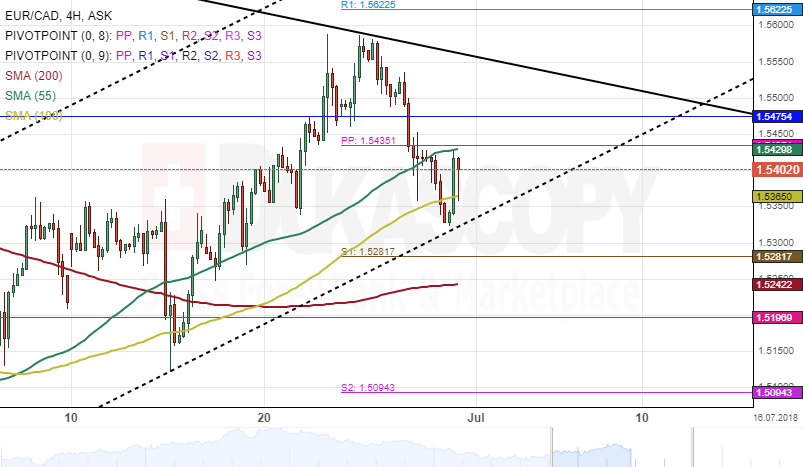

EUR/CAD 4H Chart: Bulls Expected To Prevail

The price movement for the EUR/CAD exchange rate has been constrained by several channels. The most important of which for swing traders is the junior ascending pattern in line with the dominant uptrend channel. Its bottom boundary was tested late May when the pair made a U-turn from the Monthly S1 at 1.4987.

The currency pair is likely to continue appreciating within the following trading sessions as it maintains the junior pattern. The rate could dash through a resistance cluster formed by the weekly and the monthly PPs near the 1.5435 mark today.

On the 4H time frame, technical indicators flash bearish signals. This could suggest a decline for the pair is likely in the short-term.

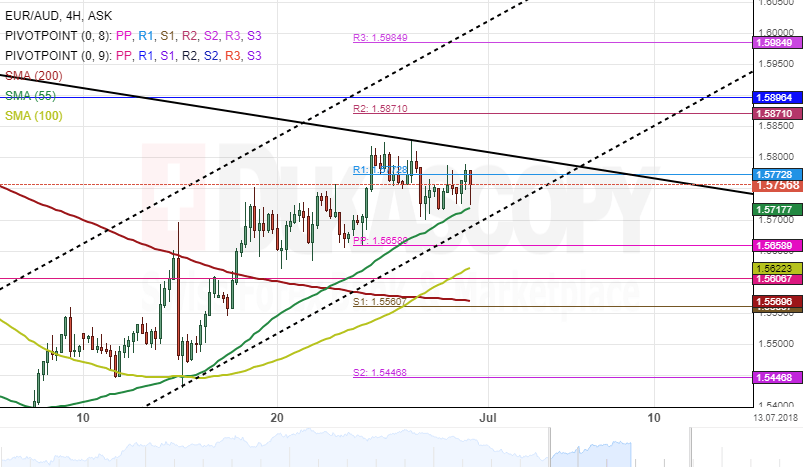

EUR/AUD 4H Chart: Awaits Breakout

The common European currency has been bound in several long and short-term patterns against the Australian Dollar which have guided the price up since early June.

The exchange rate is likely to continue moving in the ascending channel within the following session in line with the dominant ascending pattern. The currency pair is currently trading near the border of a medium-term downtrend channel and could breach the upper boundary today.

If and when this scenario occurs, the currency exchange rate is likely to encounter a resistance cluster formed by the weekly and the monthly PPs near the 1.58 mark.

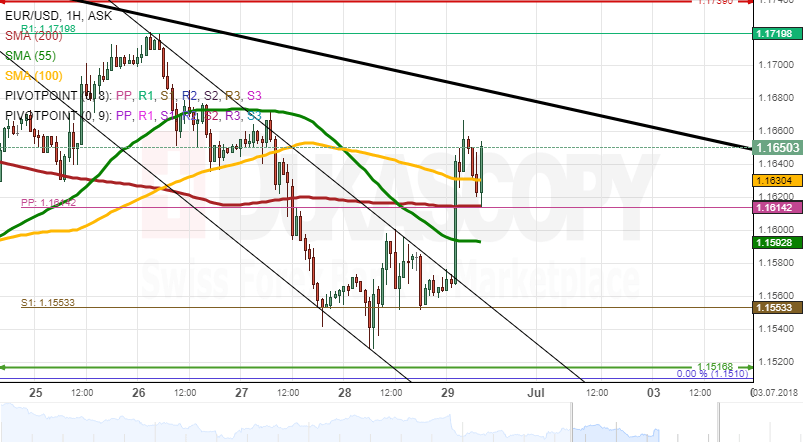

EURUSD Analysis: Euro Boosted By Fundamentals

Following the strong depreciation of EUR/USD on Wednesday, the pair stabilised and was trading slightly above the weekly S1 at 1.1553 yesterday. A fall down to the one-year low at 1.1520 did not follow.

This lack of direction stopped early on Friday when the pair, boosted by successful talks in the EU Economic Summit, surged 74 pips in one hour and consequently breached the weekly PP and the 55-, 200– and 100-hour SMAs.

It seems that this bullish sentiment could still guide the pair in this session, supported by hourly SMAs. However, traders should consider the 100– and 200-period (4H) moving averages that are located at the upper channel line near 1.1680.

Bulls might be reluctant to breach this cluster, thus leaving the rate ranging in between hourly and four-hour SMAs.

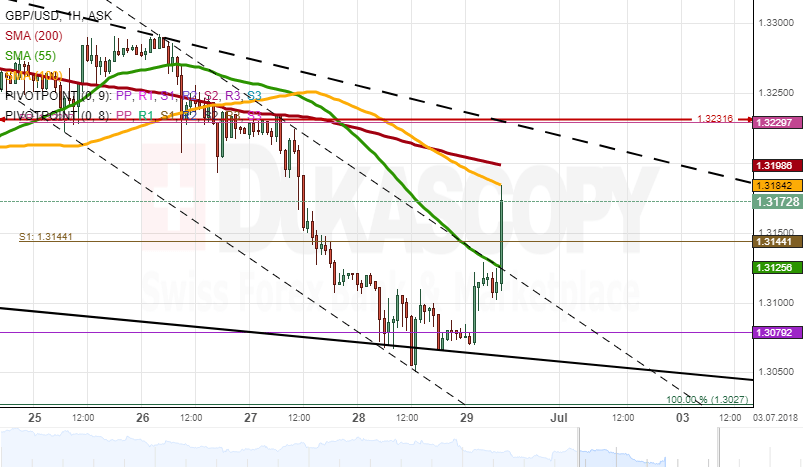

GBPUSD Analysis: Hits Channel Line

The GBP/USD exchange rate showed no changes to its positioning on Thursday, thus trading near the monthly S1 and the bottom channel line circa 1.3080 for the whole session.

Technical indicators on the 1H and 4H time-frames demonstrate that the Pound might accelerate from this channel today, thus breaching the 55-hour SMA at 1.3131 and approaching the massive resistance cluster formed by the 100– and 200-hour and 55-period (4H) SMAs near 1.32. Given that this area has been historically significant resistance/support, a move above it is very unlikely.

In case the bearish sentiment takes over the market today, it is expected that the Sterling moves lower along the bottom channel line towards the weekly S1 and a nine-month low of 1.3025.

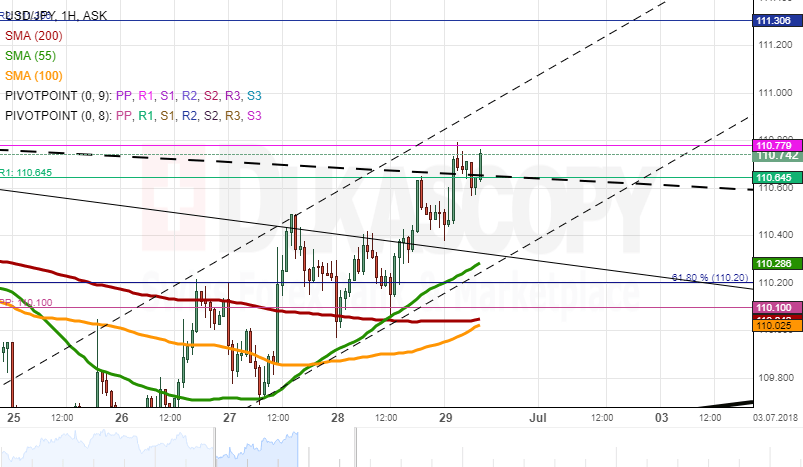

USDJPY Analysis: Reaches Trend-Line

The US Dollar was driven by slight upside momentum on Thursday. The pair found support at the weekly PP, the 61.80% Fibo retracement and the 55– and 200-hour SMAs circa 110.20 and thus had reached the weekly and monthly R1s and a downward-sloping trend-line near 110.75 by Friday morning.

It seems that the Greenback could be ready to breach this dashed trend-line that should result in a surge either today or early next week. A breakout above the monthly R1 would be followed by a test of the weekly R2 at 111.30.

In case this resistance is not breached, the rate should return back to the 110.20 area. This support is unlikely to be surpassed, as it is strengthened not only by technical indicators on the hourly but also on the 4H chart.

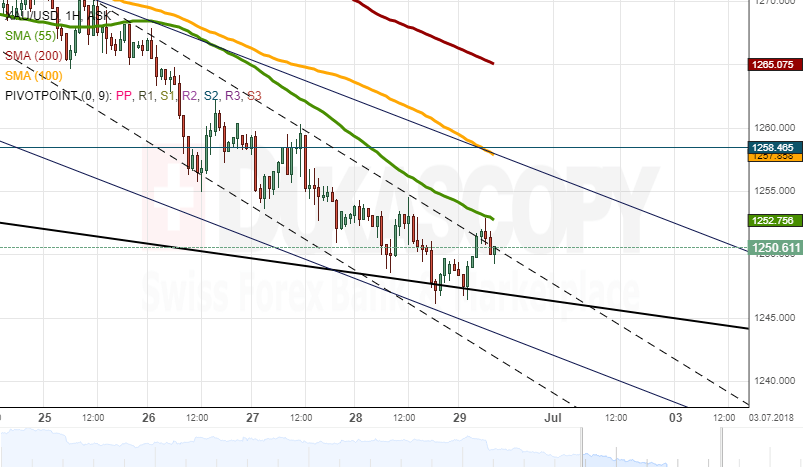

Gold Analysis: Pressured By 55-Hour SMA

Gold still shows some weakness against the US Dollar, as it is being pressured lower since mid-June. By Friday morning, the pair had fallen down to the bottom boundaries of two channels, the most senior of which was formed in March.

The yellow metal has likewise returned to test the 55-hour SMA at 1,253.00. In case this moving average is breached, the rate is likely to aim for the following resistance cluster set by the 55-period (4H) and the 100-hour SMAs and the monthly S2 at 1.260.00. A strong bullish sentiment could send it even higher gains towards 1,265.00.

In general, it is not expected that a massive fall occurs today. If the 55-hour SMA remains intact, Gold should continue gradually moving lower along this line