Sample Category Title

BoC Governor, Stephen Poloz, Keeps Markets Guessing On July Rate Move

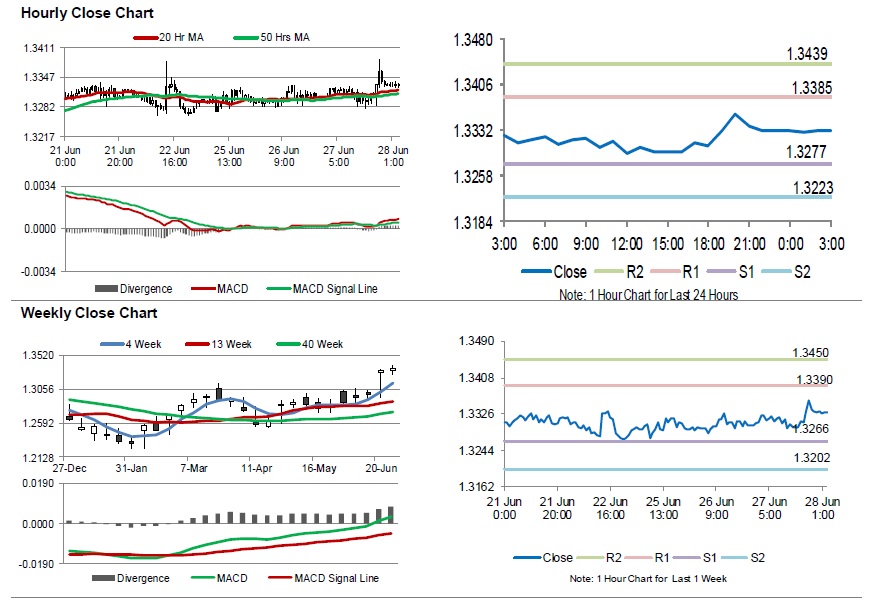

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the CAD and closed at 1.3331.

Yesterday, the Bank of Canada Governor, Stephen Poloz, stated that the impact of US trade fight and tighter mortgage rules will “figure prominently” in the Central Bank’s July’s interest rate decision.

In the Asian session, at GMT0300, the pair is trading at 1.3330, with the USD trading slightly lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3277, and a fall through could take it to the next support level of 1.3223. The pair is expected to find its first resistance at 1.3385, and a rise through could take it to the next resistance level of 1.3439.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Aussie Trading On A Stronger Footing This Morning

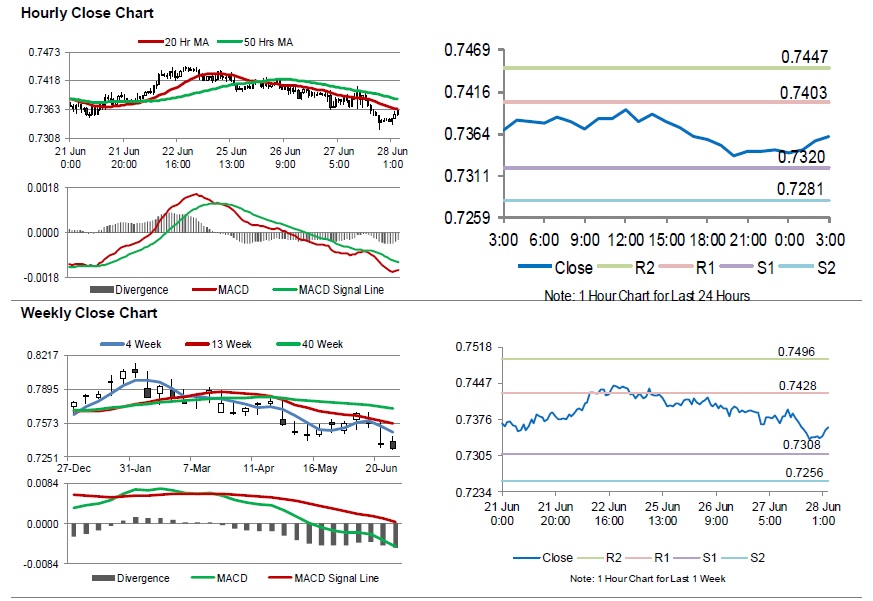

For the 24 hours to 23:00 GMT, the AUD declined 0.66% against the USD and closed at 0.7343.

LME Copper prices declined 0.4% or $24.0/MT to $6688.0/MT. Aluminium prices rose 2.4% or $52.5/MT to $2204.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7360, with the AUD trading 0.23% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7320, and a fall through could take it to the next support level of 0.7281. The pair is expected to find its first resistance at 0.7403, and a rise through could take it to the next resistance level of 0.7447.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Gold: Yellow Metal Trading A Tad Higher In The Morning Session

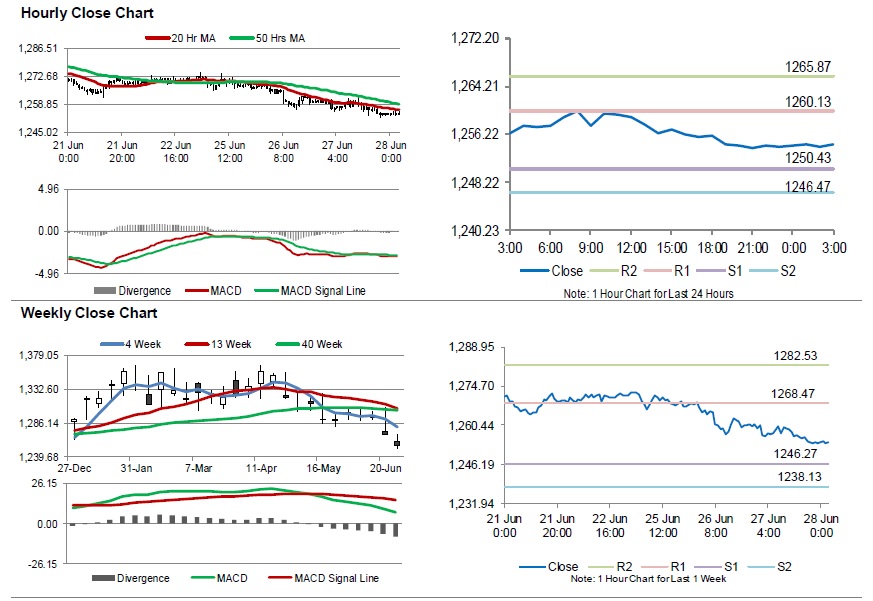

For the 24 hours to 23:00 GMT, Gold declined 0.52% against the USD and closed at USD1254.30 per ounce, as strength in the greenback dampened demand for the safe haven asset.

In the Asian session, at GMT0300, the pair is trading at 1254.40, with gold trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1250.43, and a fall through could take it to the next support level of 1246.47. The pair is expected to find its first resistance at 1260.13, and a rise through could take it to the next resistance level of 1265.87.

The yellow metal is trading below its 20 Hr and 50 Hr moving averages.

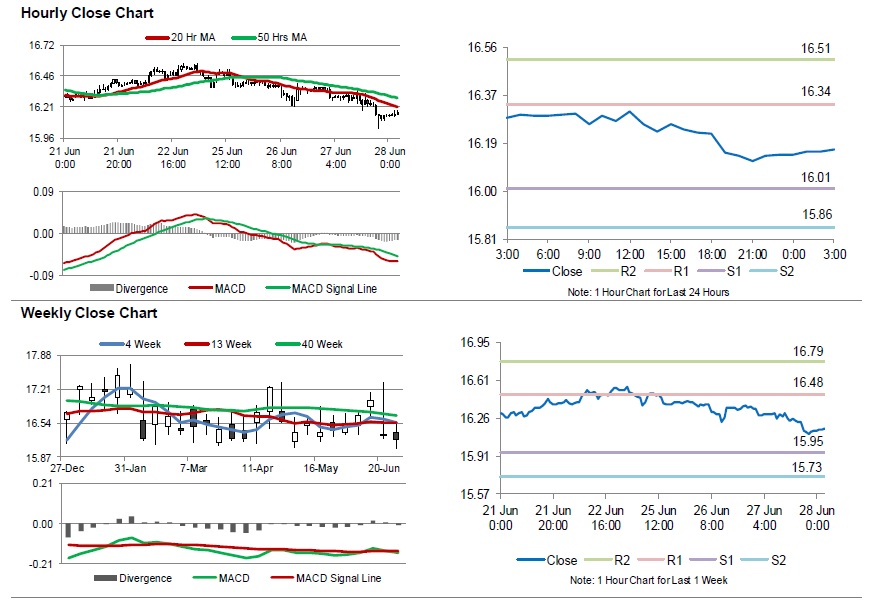

Silver: White Metal Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Silver declined 1.37% against the USD and closed at USD16.15 per ounce, tracking losses in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.17, with silver trading 0.12% higher against the USD from yesterday’s close.

The pair is expected to find support at 16.01, and a fall through could take it to the next support level of 15.86. The pair is expected to find its first resistance at 16.34, and a rise through could take it to the next resistance level of 16.51.

The white metal is trading below its 20 Hr and 50 Hr moving averages.

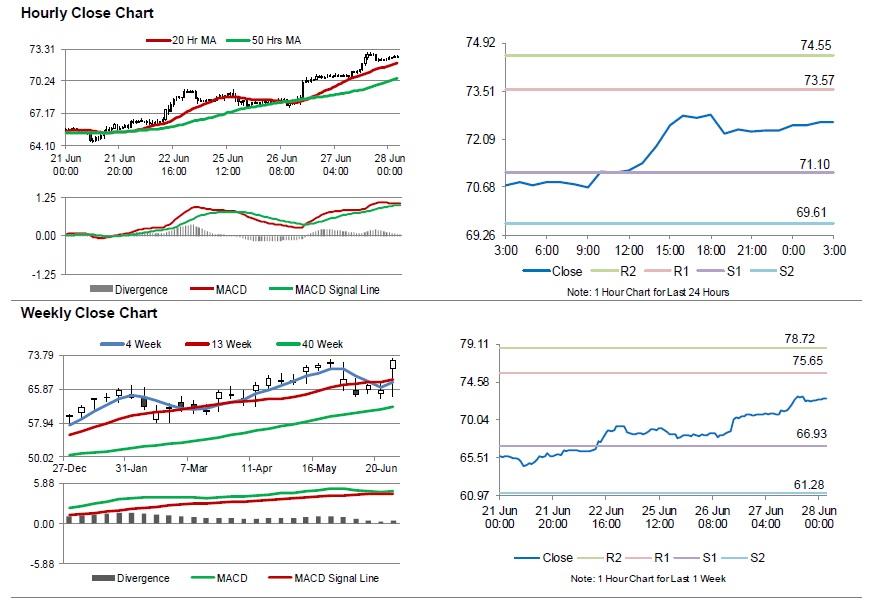

Crude Oil: Oil Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, Crude Oil rose 2.42% against the USD and closed at USD72.33 per barrel, after the Energy Information Administration (EIA) report indicated a massive drop in US crude oil stockpiles. The agency reported that crude supplies declined by 9.9 million barrels to 416.64 million barrels in the week ended 22 June, marking its largest weekly decline this year.

In the Asian session, at GMT0300, the pair is trading at 72.59, with oil trading 0.36% higher against the USD from yesterday’s close.

The pair is expected to find support at 71.10, and a fall through could take it to the next support level of 69.61. The pair is expected to find its first resistance at 73.57, and a rise through could take it to the next resistance level of 74.55.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

Today, The Two-Day European Council Meeting Starts

Market movers today

Today, the two-day European Council meeting starts. Several topics will be in focus: migration, Brexit, security and eurozone reforms are on the agenda (European Council Agenda Highlights). Migration will be one of the hottest topics, especially following the pressure on Merkel from her CSU coalition partner to find an EU-wide solution to migration problems. We will also closely follow what stance the new Italian government will take on the topics. We are likely to see a very split EU, where only France's Macron seems to be a strong advocate for closer EU cooperation in terms of economics, security and migration. Trade will also be discussed in light of recent global and growing trade tensions. The European Council is expected to underline the importance of the multilateral rules-based system, call for improvements to the functioning of the World Trade Organisation and emphasise the EU's positive trade agenda.

In terms of Brexit, the summit has become less important as the clashes between the EU and UK are likely to be postponed to the October EU summit. However, Brexit remains a key driver for the pound and thus very sensitive to Brexit-related comments from the Summit.

The German flash inflation print for June is due to be released, which together with similar releases in Italy and Spain may be an important gauge for the eurozone inflation release tomorrow. The market is expecting inflation to fall back modestly in Germany from 2.2% in May to 2.1% in June, due primarily to base effects.

Selected market news

Retail sales in Japan covering May published overnight disappointed consensus. Retail sales grew 0.6% y/y down from 1.5% y/y in April and below the consensus estimate of 1.2% y/y.

The Reserve Bank of New Zealand kept its key policy rate unchanged at 1.75% at its meeting overnight. It further struck a somewhat dovish tone by noting that it is well positioned to manage a change in the policy rate both up and down.

The Chinese Ministry of Commerce commented on recent protectionist measures from the US overnight, saying it is becoming a major drag on global investment and that China is in cooperation with the EU on market access. The Chinese equity market stabilised overnight following significant underperformance over the past couple of weeks.

Oil prices continued to rise yesterday, shrugging off sour risk sentiment and a stronger dollar. Tighter supply remains a focal point for the market. Yesterday, the market reacted partly to the weekly EIA inventory report, which showed a large draw on inventories. The price on Brent crude briefly touched USD78/bbl - the highest level in a month.

The US 10Y government bond yield continued to drop yesterday, falling to 2.83% and down about 16bp since the start of the month.

Huge Decline US Oil Inventory Sent WTI Crude to Highest Level since 2014

Both oil benchmarks rallied for two days in a row. The front-month WTI crude contract has obviously outperformed, accumulating gains of 6.7% over the past two days. The Brent contract added +3.8% during the period. WTI's rally was driven by the sharp decline in US oil inventory.

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks fell -4.56 mmb to 1203.6 mmb in the week ended June 22. Crude oil inventory slumped -9.89 mmb (consensus: -2.57 mmb) to 416.64 mmb, as inventories decreased in 3 out of 5 PADDs. PADD III saw inventory draw of -5.17 mmb Cushing stock slipped -2.71 mmb to 29.89 mmb. Utilization rate added +0.8% to 97.5%. Meanwhile, crude production steadied at 10.9M bpd for the week.

Refined oil product inventories increased further. Gasoline inventory added +1.16 mmb to 241.2 mmb although demand jumped +4.34% to 9.73M bpd. The market had anticipated a +1.31 mmb increase in stockpile. Production added +0.43% to 10.14M bpd while imports soared +16.24% to 0.99M bpd during the week.

Distillate inventory increased +0.02 mmb to 117.42 mmb. The market had anticipated a +0.77 mmb gain. This came in as a result of a -5.57% decline in demand to 3.61M bpd. Production slipped -1.32% to 5.4M bpd while imports rose +10.2% to 0.05M bpd during the week.

Released after market close on Tuesday, the industry- sponsored API estimated that crude oil inventory dropped -9.23 mmb during the week. For refined oil products, gasoline stockpile rose +1.15 mmb while distillate added +1.79 mmb.

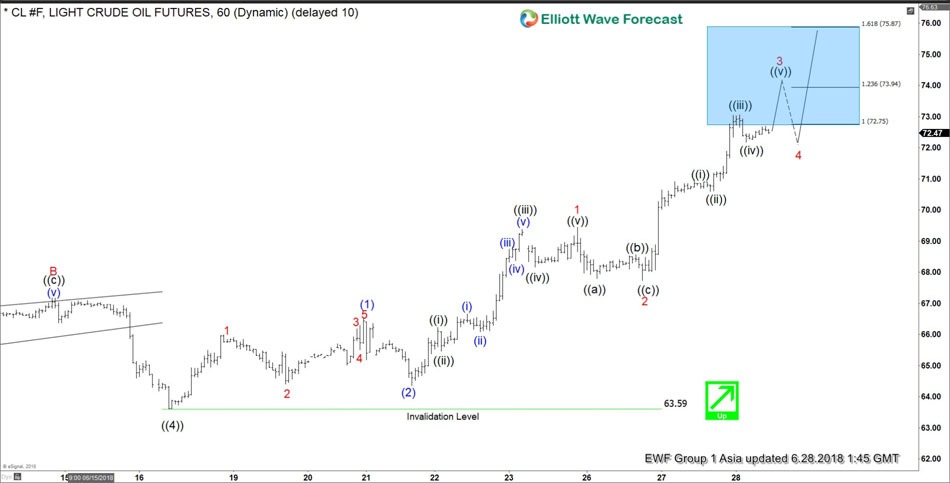

Oil Elliott Wave Impulse Structure Calling For More Upside

OIL short-term Elliott Wave view suggests that the decline to $63.59 on 6/18/2018 low ended primary wave ((4)) pullback. Above from there, the instrument has rallied to new highs already. And confirming the next extension higher taking place in primary wave ((5)). The rally higher from $63.59 low is taking the form of Elliott wave impulse structure with extension favoring more upside in the instrument.

Up from $63.59 low, the rally to $66.53 high ended intermediate wave (1) in lesser degree 5 waves structure. Down from there, intermediate wave (2) ended at $64.34 low. Then up from there, intermediate wave (3) remains in progress in another 5 waves structure within lesser degree cycles. And expected to show sub-division of 5 waves structure in each leg higher i.e Minor wave 1, 3 & 5. Above from $64.34 low, Minor wave 1 of (3) ended in 5 waves at $69.44. Minor wave 2 of (3) ended at 67.72 low. Minor wave 3 of (3) is expected to complete soon in-between 123.6%-161.8% Fibonacci extension area of Minor wave 1-2 at 72.75 – 73.94 area. Afterwards, the instrument is expected to do a pullback in Minor wave 4 of (3) before further upside extension is seen. We don’t like selling it into a proposed pullback.

OIL 1 Hour Elliott Wave Chart

RBNZ More Dovish in June Meeting

RBNZ left the OCR unchanged at 1.75%. While the central bank reiterated its “neutral” monetary policy stance, the accompanying statement revealed that policymakers have turned slightly more dovish than previous months. The members were concerned about global trade tensions and the resulting financial market volatility. They also acknowledged more spare capacity at home as driven by the weaker than expected first quarter GDP growth. The members are ready to leave the policy rate at the current low level and get prepared to lower it, when necessary

On the global economic developments, RBNZ forecast that inflation would continue to improve but remain “modest”. This appears more upbeat that May’s reference that global inflationary pressure would “rise” but remain “contained”. However, the additional comments in June that the inflationary outlook “has been tempered slightly by trade tensions in some major economies” and “ongoing volatility in some emerging market economies continues” indicate that the members are cautious about the global developments, especially the US-induced trade tensions.

At home, RBNZ judged that the outlook from May “remains intact”, but that there was “marginally more spare capacity in the economy” than anticipated given the “recent weaker GDP outturn”. It added that the government’s spending impulse is “slightly lower and later than anticipated” and this would pose downside risk to the medium-term outlook. On inflation RBNZ noted that it is still “expected to gradually rise to our 2%, resulting from capacity pressures”. While recent weakness in NZD should help boosting the price level, the members might not necessarily be relieved as the depreciation come at a time when domestic data softened.

On the monetary policy outlook, the central bank noted that it is “well positioned to manage change in either direction – up or down – as necessary”. This is compared with May’s reference that “the direction of our next move is equally balanced, up or down. Only time and events will tell”. Meanwhile, it noted that the current policy rate would remain unchanged “for now”. When compared with May’s reference that the current level of policy rate would remain for “some time to come”, it appears that the members are determined to keep the rates at low levels for a more extended period of time.

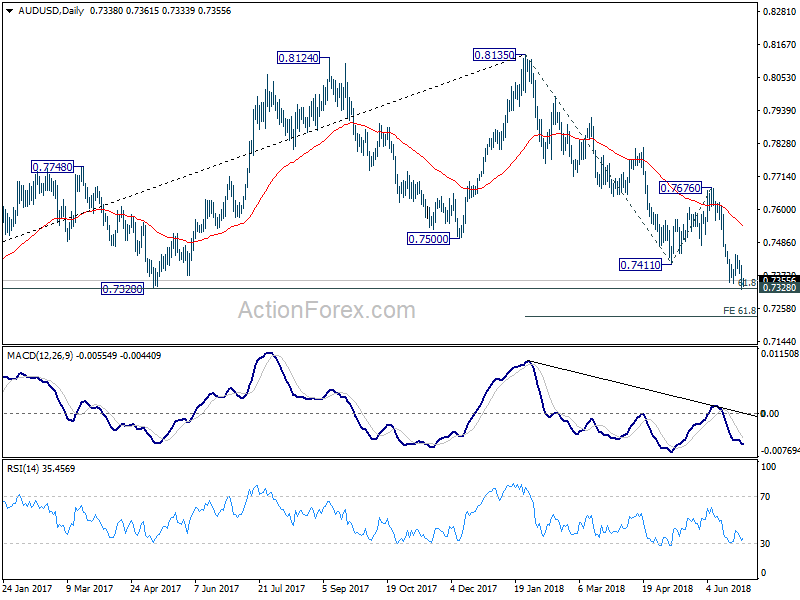

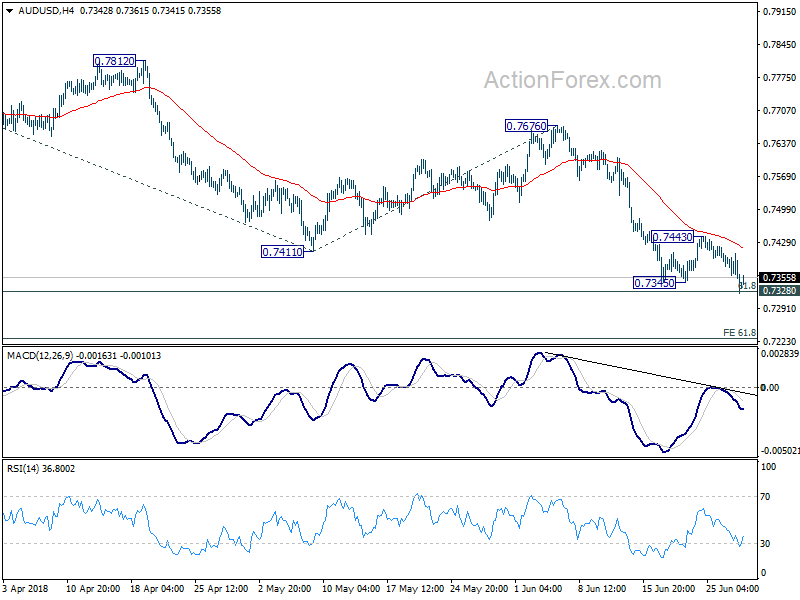

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7309; (P) 0.7358; (R1) 0.7390; More...

AUD/USD dipped to 0.7322 but quickly drew support from 7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). Intraday bias remains neutral first. Deeper fall is expected as long as 0.7443 resistance holds. Sustained break of 0.7326/8 will extend larger fall from 0.8315 to 61.8% projection of 0.8135 to 0.7411 from 0.7676 at 0.7229 next Though, break of 0.7443 resistance will suggest short term bottoming and bring lengthier consolidations.

In the bigger picture, medium term rebound from 0.6826 (2016 low) is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. Firm break there will resume the long term down trend from 1.1079 and take 0.6008 support next (2008 low). This will now remain the favored case as long as 0.7676 resistance holds.