Sample Category Title

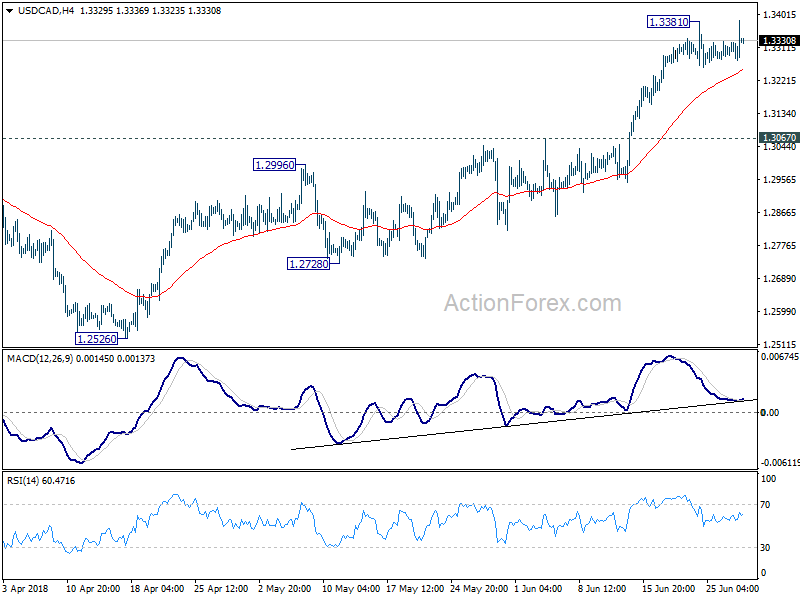

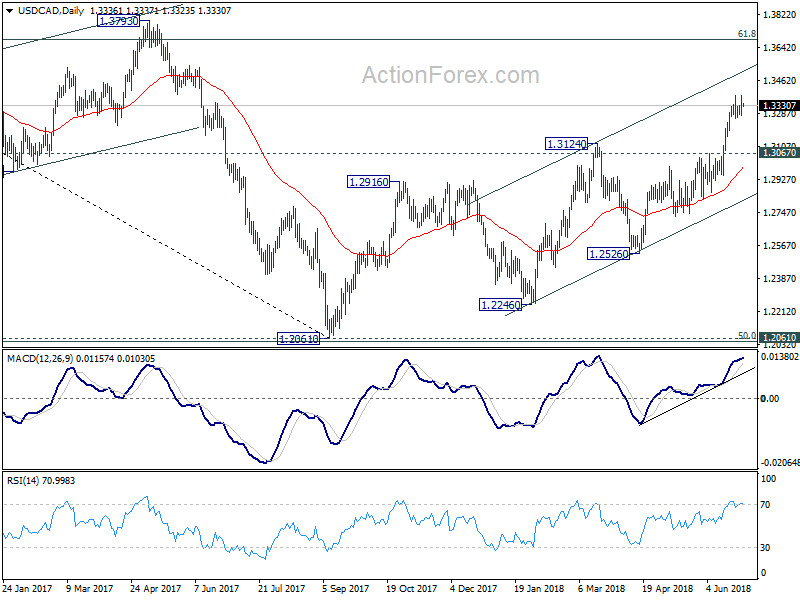

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3283; (P) 1.3334; (R1) 1.3394; More...

Despite breaching 1.3381 to 1.3385, USD/CAD quickly retreated back to established range. Intraday bias remains neutral as consolidation could extend. In case of deeper pull back, downside should be contained above 1.3067 resistance turned support to bring rise resumption. On the upside, firm break of 1.3381 will resume recent rally for 1.3685 medium term fibonacci level next.

In the bigger picture, current development solidify the view of bullish trend reversal. That is fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. This will now be the preferred case as long as 1.2916 resistance turned support holds, even in case of deep pull back.

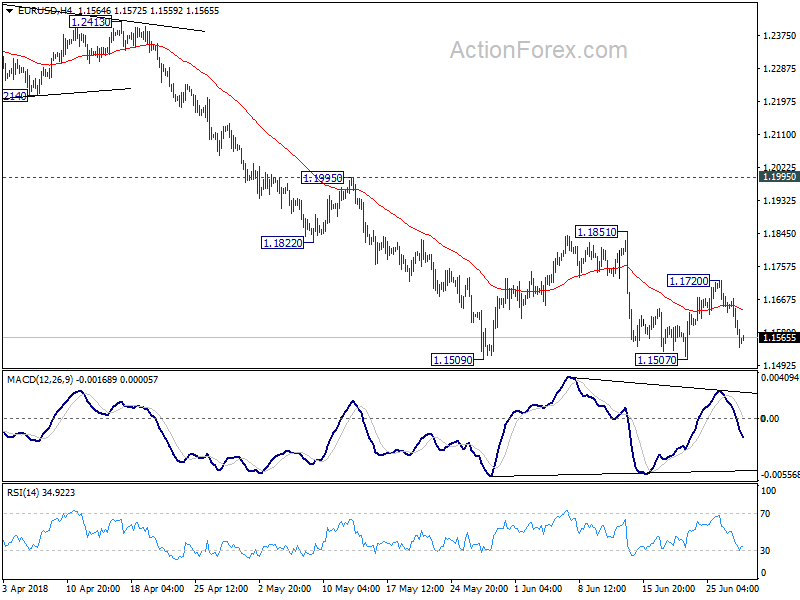

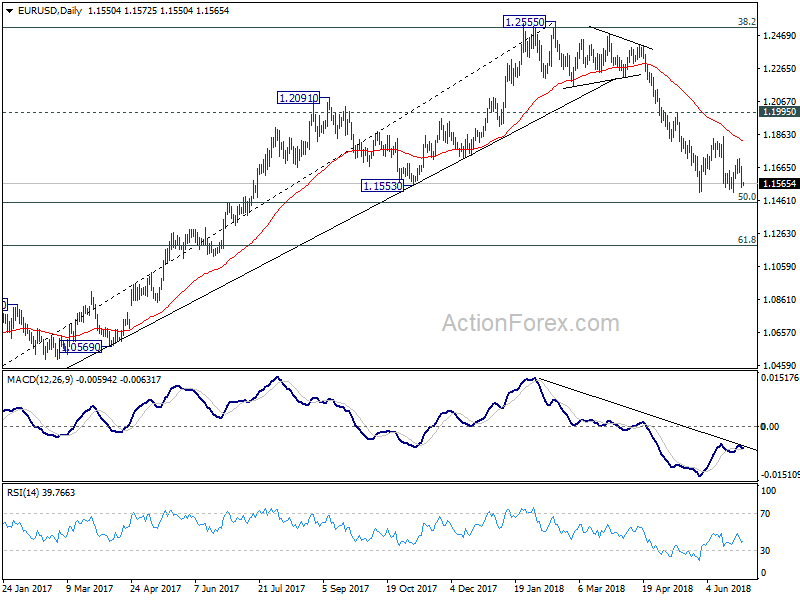

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1505; (P) 1.1590 (R1) 1.1638; More.....

Intraday bias in EUR/USD remains mildly on the downside for 1.1507 low. Break will resume whole fall from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186. On the upside, above 1.1720 will bring another recovery. But still, upside should be limited by 1.1851 resistance to bring fall resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

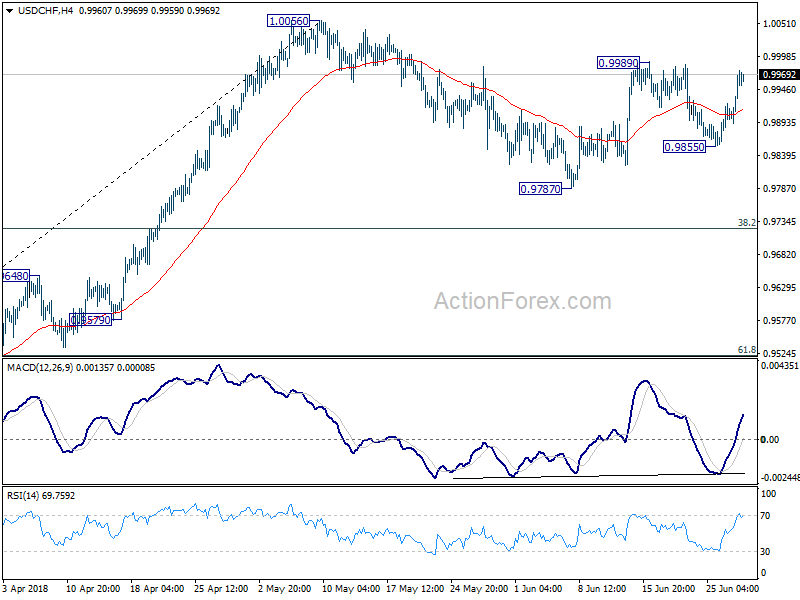

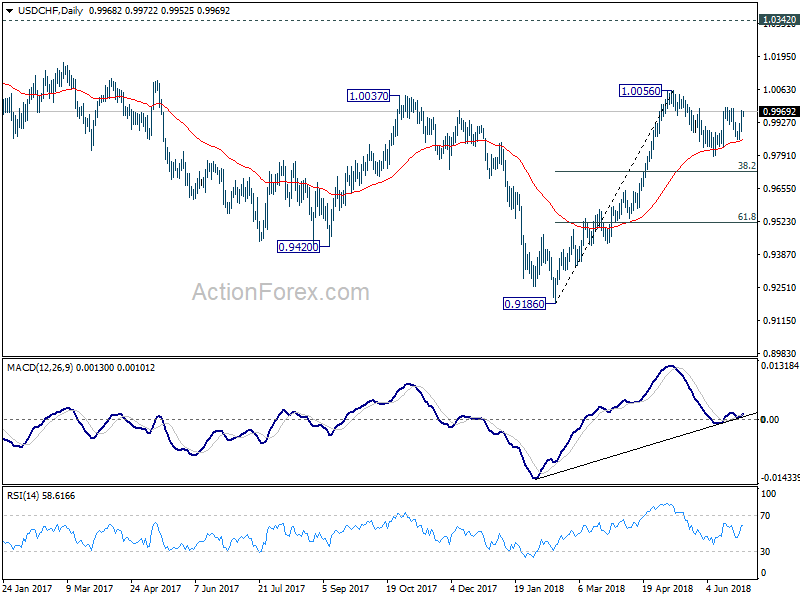

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9916; (P) 0.9946; (R1) 1.0002; More...

Intraday bias in USD/CHF remains neutral with focus on 0.9989 minor resistance. Break there will resume the rebound from 0.9787 and target 1.0056 high. Break will resume whole rally from 0.9186. On the downside, below 0.9855 will likely resume the correction from 1.0056 through 0.9787 support. But downside should be contained by 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

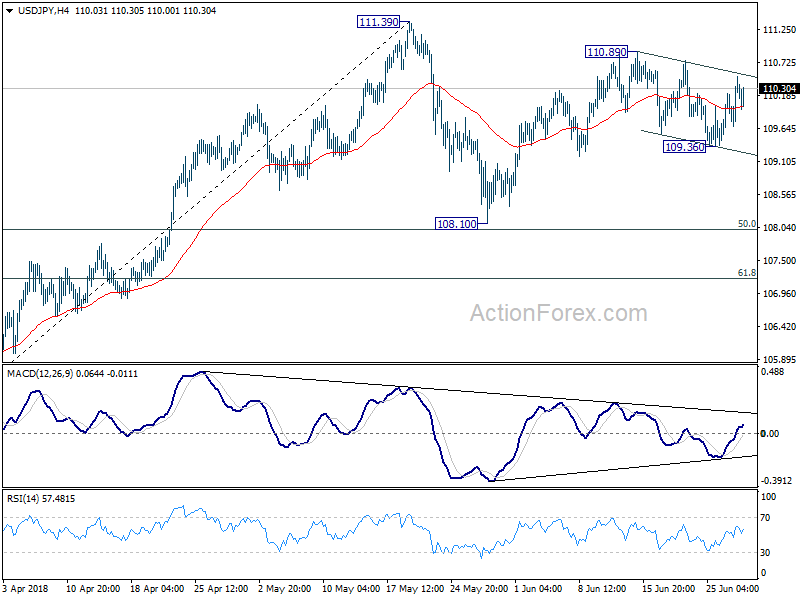

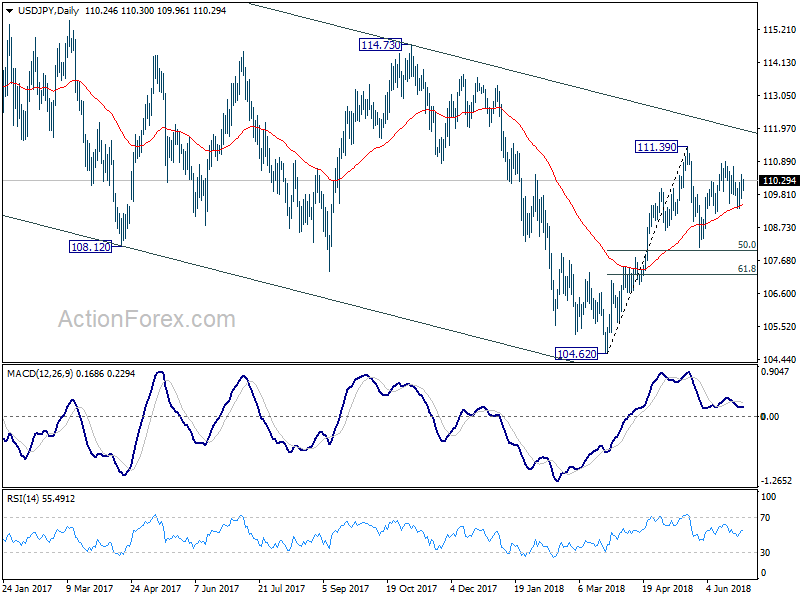

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.81; (P) 110.15; (R1) 110.61; More...

Intraday bias in USD/JPY remains neutral for the moment. Despite the strong rebound from 109.36, it's staying in range below 110.89. On the upside, break of 110.89 will resume the rise from 108.10 and target 111.39. Firm break there will resume the rally from 104.62 and target 114.73 key resistance. On the downside, below 109.36 will resume the fall from 110.89. In that case, as price actions from 111.39 are seen as a corrective pattern, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

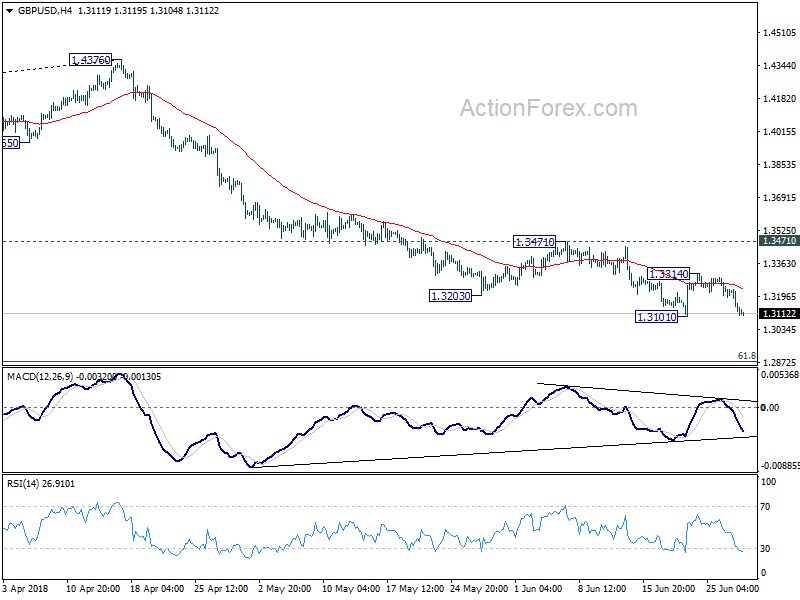

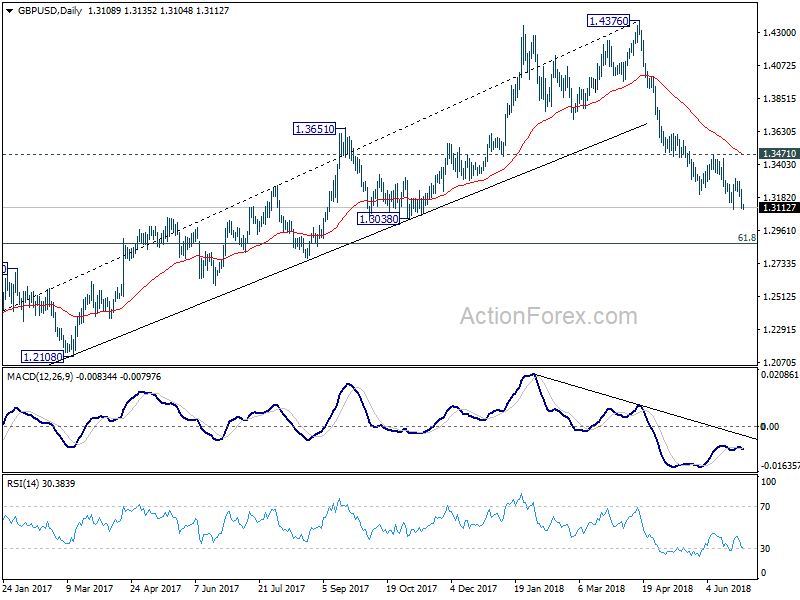

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3066; (P) 1.3154; (R1) 1.3203; More...

GBP/USD drops to as low as 1.3104 so far and focus is now on 1.3101 support. Break will resume fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next. In case of another recovery, we'd continue to expect upside to be limited by 1.3471 resistance to bring decline resumption.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Dollar Stays Strong after Roller Coaster Ride in Stocks

It was a roller coaster ride in US stocks overnight. The markets cheered Trump's backing down on the hard-line position on curbing Chinese investments in US companies. But White House economic advisor Larry Kudlow spoiled the party said the plan is neither harder nor softer. NASDAQ led the losses again, dropping -116.55 pts or -1.54 % to close at 7445.08. DOW lost -165.52 pts or -0.69% to 24117.59 while S&P 500 decline -23.43 pts or -0.86% to 2699.63. Notable strength was also seen in treasuries as 10 year yield dropped -0.053 to 2.827, breaking last week's low. WTI crude oil surged through 72.83 key resistance. Gold stays pressured after diving to 1251.

In the currency markets, Dollar swam against the tide of falling yield and stocks. While the greenback retreats mildly in Asian session, it's staying as the strongest one for the week. Yen follows as the second strongest for the week on risk aversion. Canadian Dollar is trading as the third strongest for the week, helped by oil strength but capped by trade and BoC uncertainties. On the other hand, New Zealand Dollar remains the weakest one after some dovish tweaks in RBNZ statement. Sterling and Aussie are the next weakest ones.

Technically, for now, EUR/USD is still holding above 1.1507 support and this will be the level to watch today. GBP/USD is catching up on Sterling weakness and could break equivalent support at 1.3101 earlier than EUR/USD. GBP/JPY's break of 144.37 support should now bring deeper decline to 143.18. AUD/USD breached 0.7328 key cluster support level as recent fall resumed. But there is no follow through buying yet. This will also be a level to watch today too. USD/CAD's rally looks ready to resume but 1.3381 must be overcome decisively first.

DOW reversed initial rebound as Kudlow spoiled the party

The initial rebound in stocks was fueled by lessened worries on US-China trade relationship. Trump announced to use a a strengthened national security review panel — the Committee on Foreign Investment in the United States (CFIUS) to guard against threats from Chinese investments in US technology companies. That's a blanket measure that doesn't single out China as the target, as confirmed by Trump's own words, and comments by Treasury Secretary Steven Mnuchin.

The markets generally see that as Trump backing down to a softened approach on China. But such notion was rejected by Kudlow. In an interview, Kudlow said "the idea of softer or harder is really beside the point". And, "That's really not the intent. We're not driving there." Kudlow added that "it's not meant to be harder or softer," and "it's going to be very comprehensive and very effective at protecting our technological family jewels in the United States."

Two auto groups blast Trump's auto tariffs

The Association of Global Automakers issued a statement titled "International Automakers Are Not A National Security Threat" today in objection to Trump's intention to impose tariffs on import cars. The group warned that "these tariffs will harm today's U.S. auto industry, which is comprised of fourteen auto manufacturers, all of which are global and 10 of which are international automakers." And, "each of these companies employ American workers to produce cars in the United States, and tariffs will substantially increase prices for consumers."

Further it criticized that "there is no national security justification for taxing imports of vehicles and parts or discriminating between global companies headquartered here or in allied countries." The group noted that "every U.S. production facility in the industry could be made available in a national emergency, and the 130,000 Americans who work directly for international automakers are no less patriotic or willing to serve their country in a time of crisis than any other American."

Finally, it warned that "if this investigation leads to tariffs, retaliation against U.S. exports is inevitable." And, "substantial tariffs against major US auto exports have in fact already been announced, placing American auto workers on the front lines of this trade conflict."

Another group Alliance of Automobile Manufacturers also object to the tariff. It said in a statement that "tariffs are not the right approach" to achieve a level playing field. And, it urge reduction in trade barriers across the board and achieve "fairness" through "facilitating rather than inhibiting trade." And, economic security of the auto industry and country would be strengthened through modernizing NAFTA and concluding a U.S.-EU Trade Pact.

The statement also listed the bad effects of auto tariffs. There will be USD 45B in additional tax for consumers. a 25% tariffs would result in 1.5% decline in production and cause USD 195k works to lose jobs over 1-3 years or possibly longer. Job losses could surge further to 624k on retaliation by other countries. Auto sales will fall 1-2m units. It will cancel out tax reform benefits, reduce auto exports and harm other vital sectors of the economy. Besides, it will cede US leadership on future vehicle technologies.

Boston Fed Rosengren: Don't let the economy run above capacity

Boston Fed President Eric Rosengren delivered a speech titled Ethics and Economics Making Cyclical Downturns Less Severe yesterday. There he argued that Fed shouldn't let the economy "run above capacity" and "fall far below the sustainable unemployment rate". He noted it's the path that will "increase the probability of a longer recession-free period".

It should be noted that unemployment rate, currently at 3.8% in May, is already quite far below Fed's longer run rate at 4.5%. But where the real natural rate is, it's still up for debate.

Also, Rosengren repeated his push for inflation range target. He said "one might allow the inflation target to rise within the range during periods of low real rates, thus providing more room for the funds rate to fall during an economic downturn."

BoC Poloz sent mixed messages on July hike

BoC Governor Stephen Poloz's speech yesterday caught much attention given that the central bank is due to meet again on July 11, just two weeks away. Expectations on a July hike was built up after the statement in May. But such expectations were put in doubt after a string of weaker than expected data. Escalation on trade tension with US also cloud the economic outlook. Overall, Poloz gave little hint on the chance of a July move with mixed messages with the post speech press conference.

On the hawkish side, Poloz said the shift in the language in May's statement showed "increased confidence that the economy was performing as we expected, and that higher interest rates will indeed be warranted." He also down played recent disappointing data. He said, "having the occasional data point that didn't fit market expectations is not the sort of thing that throws that entire narrative off course. We are data dependent, not headline dependent."

However, Poloz also emphasized that policy makers "cannot mechanically follow the rate path provided by our models because there is simply too much uncertainty in the world." He pointed out that " the degree to which uncertainty about trade policy is holding back business investment" is one of the certainties. And, the impact of new lending guidelines on housing markets is another one.

Poloz added that "as we approach our next interest rate decision, we are working to incorporate in our projections the effects of the recently announced US steel and aluminum tariffs, along with retaliatory measures, both in Canada and globally." Also, BoC will analyze how the new lending guidelines are affecting the housing markets. These issues will " figure prominently in our upcoming deliberations." This is seen as the dovish side of the messages.

The upcoming data, April GDP and Business Outlook Survey will be highly critical on July BoC rate decision. In our view, should they disappoint, a July hike would be ruled out. Otherwise, it could be a 50/50 for BoC policy makers.

RBNZ to stay on hold longer as dovish statement indicates

New Zealand Dollar stays pressured after RBNZ left OCR unchanged at 1.75% as widely expected. The central bank reiterated in the statement that the best contribution it could make is "to ensure the OCR is at an expansionary level for a considerable period." Also, the next move could come in "either direction - up or down".

Nonetheless, there are some dovish tweaks in the statement too. Firstly, the global economic outlook has been "tempered slightly by trade tensions in some major economies" and "ongoing volatility in some emerging market economies continues." Secondly, "recent weaker GDP outturn implies marginally more spare capacity in the economy than we anticipated." And thirdly, "the Government's projected spending impulse is also slightly lower and later than anticipated."

The dovish tweaks argue that RBNZ would stay on hold for longer even though they don't warrant a cut yet.

On the data front

Elsewhere, Japan retail sales rose less than expected by 0.6% yoy in May. Germany will release Gfk consumer sentiment and CPI in European session. Eurozone will release confidence indicators. Later in the day, US will release Q1 GDP final and jobless claims.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3066; (P) 1.3154; (R1) 1.3203; More...

GBP/USD drops to as low as 1.3104 so far and focus is now on 1.3101 support. Break will resume fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next. In case of another recovery, we'd continue to expect upside to be limited by 1.3471 resistance to bring decline resumption.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | Retail Trade Y/Y May | 0.60% | 1.20% | 1.60% | 1.50% |

| 06:00 | EUR | German GfK Consumer Confidence Jul | 10.6 | 10.7 | ||

| 08:00 | EUR | ECB Monthly Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Business Climate Indicator Jun | 1.2 | 1.45 | ||

| 09:00 | EUR | Eurozone Economic Confidence Jun | 112.1 | 112.5 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jun | 6.5 | 6.8 | ||

| 09:00 | EUR | Eurozone Services Confidence Jun | 15.9 | 14.3 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -0.1 | -0.5 | ||

| 12:00 | EUR | German CPI M/M Jun P | 0.50% | |||

| 12:00 | EUR | German CPI Y/Y Jun P | 2.20% | |||

| 12:30 | USD | GDP Annualized Q/Q Q1 T | 2.20% | 2.20% | ||

| 12:30 | USD | GDP Price Index Q1 T | 1.90% | 1.90% | ||

| 12:30 | USD | Initial Jobless Claims (JUN 23) | 220K | 218K | ||

| 14:30 | USD | Natural Gas Storage | 91B |

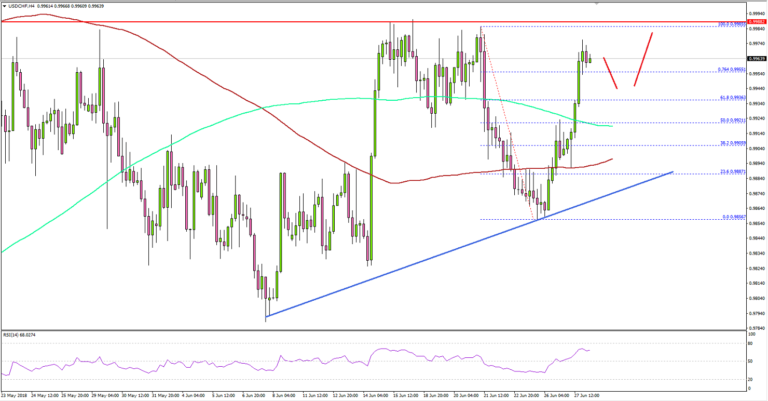

USD/CHF Remains Supported Ahead Of USD GDP

Key Highlights

- The US Dollar is trading in a bullish zone above the 0.9880 support against the Swiss Franc.

- There is a crucial bullish trend line formed with support at 0.9880 on the 4-hours chart of USD/CHF.

- The US durable goods orders decreased 0.6% in May 2018 (MoM), less than the forecast of -1.0%.

- Today in the US, the GDP figure for Q1 2018 will be released, which is forecasted to grow 2.2%.

USDCHF Technical Analysis

The US Dollar found a strong support near the 0.9855 level against the Swiss Franc. The USD/CHF pair started a fresh upside wave and traded above the 0.9900 and 0.9910 resistance levels.

During the upside move, the pair broke the 50% Fib retracement level of the last drop from the 0.9985 high to 0.9855 low. It also moved above the 0.9920 resistance and the 100 simple moving average (red, 4-hours).

More importantly, there was a close above the 61.8% Fib retracement level of the last drop from the 0.9985 high to 0.9855 low. It seems like the pair is placed nicely in a bullish trend and it could trade towards the 0.9980 level in the near term.

On the downside, the 0.9920 support and the 200 simple moving average (green, 4-hours) are likely to act as a supports. There is also a crucial bullish trend line formed with support at 0.9880 on the 4-hours chart.

Therefore, dips remains supported above 0.9900 and 0.9880. On the upside, resistances are at 0.9985 and 1.0000.

Recently in the US, the durable goods orders report for May 2018 was released by the US Census Bureau. The market was looking for a decline in orders by 1% in May 2018 compared with the previous month.

However, the actual result was a bit better as the decline was 0.6%. Looking at the durable goods orders ex transportation, there was a decline of 0.3%, whereas the market was looking for a rise of 0.5%.

The overall market sentiment still supports the US Dollar, and there are chances of more declines in EUR/USD and GBP/USD in the near term.

Economic Releases to Watch Today

- Germany’s GfK Consumer Confidence for July 2018 – Forecast 10.6, versus 10.7 previous.

- Euro Zone Consumer Confidence June 2018 – Forecast -0.5, versus -0.5 previous.

- Euro Zone Services Sentiment June 2018 – Forecast 14.2, versus 14.3 previous.

- German Consumer Price Index for June 2018 (YoY) (Prelim) – Forecast +2.1%, versus +2.2% previous.

- German Consumer Price Index for June 2018 (MoM) (Prelim) – Forecast +0.1%, versus +0.5% previous.

- US Initial Jobless Claims – Forecast 220K, versus 218K previous.

- US Gross Domestic Product Q1 2018 – Forecast 2.2% versus previous 2.2%.

Market Morning Briefing: Pound Has Moved Lower Towards Support Near 1.31

STOCKS

Dow (24117.59, -0.68%) rose to levels above 24500 but then came off sharply to close lower. As mentioned in the past few editions, 24000 is an near term support which could hold and push back prices to higher levels. Break below 24000 would open up chances of testing 23600-23500 on the downside.

The weekly support on Dax (12348.61, +0.93%) seems to have held and while that holds, the index could move up targeting

13000 in the medium term.

Nikkei (22177.58, -0.42%) has been gradually moving lower and could pause for some sessions near 22000. Failure to see a short bounce from 22000 would take it lower towards 21800-21500 in the longer run.

2800 on Shanghai (2814.45, +0.045%) 3-day candles is an immediate support and if that holds some short term rise is possible towards 2850-2900. Overall in the longer rub 2800 may not act as a strong support and an eventual break below 2800 is likely.

Nifty (10671.40, -0.91%) came off sharply yesterday to make an intra-day low of 10652. But unless a sharp and sustained fall below 10650 is seen, we may still have some hopes of bullishness for the near to medium term. A break below 10650, on the other hand would initiate medium term fall towards 10400 or even lower. The 2-remaining sessions this week would be crucial to watch.

COMMODITIES

Trump’s demands that the allies including India should stop importing Crude from Iran by November 4 this year could impact India as India and China fall under the major importers of Iranian Oil. Crude prices are trading higher just now and is likely to move up in the near term.

Very sharp rise seen in Brent (77.58) and WTI (72.59) after the recent dip and consolidation. Brent has enough room on the upside towards 80-82 on the 3-day candles; while WTI could face some resistance near 76. Overall near term looks bullish.

Gold (1254.40) is on its way to test 1250-1240 where a pause could be seen in the early sessions of next week. While below 1270, Gold prices may remain bearish.

Copper (2.9995) could possibly trade above 2.95 for now. A break below 2.90 would be necessary to turn the sentiment to bearish in the medium term.

FOREX

Euro (1.1567): Euro broke below support near 1.16 on daily line chart to see a low near 1.154 yesterday. It could see a rise till 1.158-1.160 in today’s session before falling again towards its previous low of 1.1508. The likelihood of a break below 1.15 to target support near 1.145 (on 3 day line chart) has increased and might happen next week. The trigger for the same could be political instability in Germany in the coming week.

Dollar Index (95.24): As per expectation, Dollar Index saw a high near 95.4 yesterday and could test resistance near 95.6 on 3 day line chart in this week. Next week could see a breach of this resistance and a further rise towards 96, as the Euro moves below 1.15.

Dollar Yen (110.11): Dollar Yen saw a high of 110.49 yesterday and could come down towards 110.0-109.8 today. Ranging between 110.75-109.75 could continue into next week; after which it could turn bearish (preferred) or bullish (less preferred). Resistance near 110.5-111.0 is a very strong long term resistance and hence we are expecting it to hold.

Euro Yen (127.38): Against expectation, Euro Yen has broken below support on daily candles near 127.5. With our projection for Euro being bearish and for Dollar Yen being ranged for next week, Euro Yen could dip lower towards 126.5-126.0. We have been saying that a gradual fall towards support near 124 on weekly candles is on the cards in July.

Pound (1.3114): Pound has moved lower towards support near 1.31 on daily and 3 day candles and could move even lower towards horizontal support near 1.30 (weekly candles) in the coming week. A break of 1.30 would be very bearish.

Dollar Rupee (68.61): Chances of Dollar Rupee opening gap up near 68.90 today. The market might be quite Overbought at levels near 68.90 and might be ripe for profit-taking.

INTEREST RATES

US and German yields dropped further as the risk aversion sentiment gets stronger.

German 10 year bond yield (0.32%) is very close to support near 0.3% and could break the support to test previous lows near 0.18% in the weeks ahead.

US 10 year (2.835%), 30 Year (2.976%), 5 Year (2.707%), 2 Year (2.496%) : US yields saw a significant dip with the 10 Year yield seeing lows near 2.82% yesterday:

The US 10 Year yield’s gradual downtrend could target support near 2.70%-2.65% on medium term chart.

Similarly, the 30 Year yield also looks like it could move towards 2.90%.

Confusion Reigns Supreme

Confusion reigns supreme

Uncertainty and confusion around trade war are slowly but surely leading the markets down the road to financial horror. Global equity markets continue to fray at the edges on the streams of negative headlines and none more so damning than a report from a Chinese government think tank. The leaked note warned a further escalation could lead to ” financial panic ” on the mainland and of course the fear is that contagion could spill over from the world’s second-largest economy at a time when significant economies outside of the US are struggling on the economic front and raises the spectre more dynamic Pboc policy adjustments. All the while the market is voting that China will be the ultimate loser in this protracted game of high stakes poker.

On the US markets, stocks closed lower as confusion reigns over the US administration trade policy. Wall Street started in positive territory as President Donald Trump walked back a previously announced plan to impose limits on Chinese investment in American technology companies only to see gains evaporate after Larry Kudlow, director of the National Economic Council, said in an interview that the Trump administration wasn’t softening its stance on imposing limits on Chinese investments. If the administration doesn’t understand what the President is trying to achieve from his trade policy, that is hardly a sign of confidence for investors. It would be entirely natural if investors were a bit confused as indeed confusion reigns supreme. And for traders hoping to take a summer vacation, there is no rest for the weary.

Oil market

The US benchmark settled as its highest prices since 2014 after fuelled too by a considerable plunge in US inventories. Oil production was flat at 10.9 million barrels per day last week, according to the Energy Information Administration. US crude oil exports jumped 626,000 bpd to an eye-watering 3.00 mmbpd. Indeed, the massive $11 Brent-WTI spread in early June was probably a significant factor in the jump in exports.

This data comes on the back of a bullish spike after the US called on their allies to adhere to a zero tolerance on Iran imports. The US administration is wielding a huge stick on the trade war front, and its expect this compliance will stick for fear for of more US corporate reprisals.

All the while supplies will continue to run tight in North America as the shutdowns of the essential Syncrude oil sand facility will keep 350,000 barrels per day offline at least until the end of July. And without question, the markets are bedevilled again by enormous supply uncertainties.

The Oil bulls are back in charge!

Gold Market

Gold prices went in the tank again as investors continue to pile into the haven US dollar to buy US Bonds, and the surging greenback is tarnishing golds appeal. The Yield on 10-year treasures fell to 2.83% as investor view US government debt as the place to ride out escalating trade disputes which continue to send jitters through global capital markets. While shaky global markets make gold look attractive there is no escaping the massive bearish risk for a stronger USD.

Currency Market

EUR: Political fissures around migration sees the EUR trading on shaky ground. Continue to view Political risk and negative differentials to the EUR should see the EURO move. Short EURJPY should continue to look fruitful especially if we get a severe case of the risk wobbles which could trigger some JPY buying on safe-haven demand.

AUD: Even if the China markets have a mild case of the sniffles, AUD trader will take notice but if the China markets are indeed on the cusp of “financial panic “, it should be all in short on G-10 primary China proxy

MYR: With the USDCNH breaching fresh highs the USD the USMYR continues trading higher in sympathy with the Yuan weakness. The overnight headlines of the Chinese Thinktank have local investors extremely concerned. And with the USD dollar reasserting itself as the unquestionable hedge against escalating trade war, there’s no escaping the wrath of a stronger USD. The surging USD and prospect of escalating trade war, indeed the path of least resistance appears higher with the next key focus on 4.05 USDMYR.

BoC Poloz sent mixed messages on July hike

BoC Governor Stephen Poloz's speech yesterday caught much attention given that the central bank is due to meet again on July 11, just two weeks away. Expectations on a July hike was built up after the statement in May. But such expectations were put in doubt after a string of weaker than expected data. Escalation on trade tension with US also cloud the economic outlook. Overall, Poloz gave little hint on the chance of a July move with mixed messages with the post speech press conference.

On the hawkish side, Poloz said the shift in the language in May's statement showed "increased confidence that the economy was performing as we expected, and that higher interest rates will indeed be warranted." He also down played recent disappointing data. He said, "having the occasional data point that didn't fit market expectations is not the sort of thing that throws that entire narrative off course. We are data dependent, not headline dependent."

However, Poloz also emphasized that policy makers "cannot mechanically follow the rate path provided by our models because there is simply too much uncertainty in the world." He pointed out that " the degree to which uncertainty about trade policy is holding back business investment" is one of the certainties. And, the impact of new lending guidelines on housing markets is another one.

Poloz added that "as we approach our next interest rate decision, we are working to incorporate in our projections the effects of the recently announced US steel and aluminum tariffs, along with retaliatory measures, both in Canada and globally." Also, BoC will analyze how the new lending guidelines are affecting the housing markets. These issues will " figure prominently in our upcoming deliberations." This is seen as the dovish side of the messages.

The upcoming data, April GDP and Business Outlook Survey will be highly critical on July BoC rate decision. In our view, should they disappoint, a July hike would be ruled out. Otherwise, it could be a 50/50 for BoC policy makers.

Here is the speech Let Me Be Clear: From Transparency to Trust and Understanding

Video of the speech:

https://www.youtube.com/watch?v=otQcSXREuBI

Video of the press conference:

https://www.youtube.com/watch?v=zcYfN-v3TI0