Sample Category Title

Boston Fed Rosengren: Don’t let the economy run above capacity

Boston Fed President Eric Rosengren delivered a speech titled Ethics and Economics Making Cyclical Downturns Less Severe yesterday. There he argued that Fed shouldn't let the economy "run above capacity" and "fall far below the sustainable unemployment rate". He noted it's the path that will "increase the probability of a longer recession-free period".

It should be noted that unemployment rate, currently at 3.8% in May, is already quite far below Fed's longer run rate at 4.5%. But where the real natural rate is, it's still up for debate.

Also, Rosengren repeated his push for inflation range target. He said "one might allow the inflation target to rise within the range during periods of low real rates, thus providing more room for the funds rate to fall during an economic downturn."

https://www.youtube.com/watch?v=D0oDy5pKels

NASDAQ could be starting a medium term correction

NASDAQ suffered most among major US indices on Trump's intention to curb foreign investments in US tech industry. This week's downside acceleration is starting to argue that it's in a medium term correction. For the near term, outlook will stay bearish as long as 7610.67 resistance holds. Focus is on 55 day EMA (now at 7460.17). Sustained trading below this EMA will add more weight to this bearish case.

Looking at the bigger picture, outlook isn't too good neither with bearish divergence condition seen in weekly MACD and RSI. Long term trend line support at around 7125 is another line of defence. Firm break there would confirm that fall from 7806.60 is correcting whole up trend from 4209.76. In that case, we'll likely see more downside to 38.2% retracement of 4209.76 to 7806.60 at 6432.60) before forming a bottom.

DOW reversed initial rebound as Kudlow spoiled the party

US stocks reversed early gains and closed broadly lower overnight as White House economic advisor Larry Kudlow spoiled the party. NASDAQ led the losses again, dropping -116.55 pts or -1.54 % to close at 7445.08. DOW lost -165.52 pts or -0.69% to 24117.59 while S&P 500 decline -23.43 pts or -0.86% to 2699.63.

The initial rebound was fueled by lessened worries on US-China trade relationship. Trump announced to use a a strengthened national security review panel — the Committee on Foreign Investment in the United States (CFIUS) to guard against threats from Chinese investments in US technology companies. That's a blanket measure that doesn't single out China as the target, as confirmed by Trump's own words, and comments by Treasury Secretary Steven Mnuchin.

The markets generally see that as Trump backing down to a softened approach on China. But such notion was rejected by Kudlow. In an interview, Kudlow said "the idea of softer or harder is really beside the point". And, "That's really not the intent. We're not driving there." Kudlow added that "it's not meant to be harder or softer," and "it's going to be very comprehensive and very effective at protecting our technological family jewels in the United States."

DOW's rejection by 55 H EMA is clearly as sign of near term bearishness. It looked like trades had indeed made use of yesterday's rebound to sell, rather than revering their position. There won't be any bottoming as long as 24569.02 minor resistance holds.

Meanwhile, the close below 24247.84 support affirmed our bearish view on DOW. That is, rise from 23344.52 has completed at 25402.83 already. Deeper fall should be seen back to 23444.52. There is prospect of dropping beyond this support as the decline from 25402.83 could be the third leg of the corrective pattern fro 26616.71 high.

BoC Poloz Focuses on Data Dependency as Uncertainty Mounts

Bank of Canada Governor Stephen Poloz spoke in Victoria today. His remarks focused on how the Bank of Canada communicates its thinking to market participants and the public more broadly.

Regarding Canadians at large, Bank research suggests that more can be done to improve the readability and interpretation of the Bank's work. The Bank will be making changes to help its message reach a broader audience, including a new publication "The Economy Plain and Simple". Governor Poloz also discussed the importance of two-way conversation, notably in the context of the Business Outlook Survey.

When it comes to market signals, Mr. Poloz expressed comfort in the current process, noting that explicit forward guidance is best used in crisis situations (such as 2009 and not currently), as it can lull markets into a sense of complacency otherwise, unnecessarily constraining the Bank's actions.

Of particular note, the Governor referred to the new approach of starting from a blank page for policy decisions, using the previous statement (in May) as an example. He noted that the change to 'gradual' in characterizing the approach to rates represented increased confidence that the economy was meeting expectations, and that financial markets understood the message. Continuing in this vein during the press conference, recent market pricing (which sees a July hike as a coin flip) was characterized as a reasonable reflection of recent data.

The speech was wrapped with a reminder that economic models only provide a starting point for rate decisions. Uncertainty also plays a role, notably in terms of trade policy uncertainty and housing market developments. This uncertainty and resulting data dependence underscores Poloz's view that forward guidance in the current context would put the Bank's credibility at risk.

Key Implications

With the Bank of Canada's next interest rate decision less than two weeks away, this was a closely watched speech. As it turned out, Governor Poloz was a bit on the cagey side. Coming on the heels of generally disappointing April data, the focus on data dependence and references to the impact of trade policies and housing developments are clearly dovish signals. At the same time, the statement that "Financial markets understood our message" is in reference to a statement that drove market odds of a July rate hike from 60% to 80% in a single day.

That current risks around trade and housing/debt will factor into the Bank's decision-making is a given. Developments since Deputy Governor Lane's speech (which fell on the same day as the announcement of U.S. steel and aluminum tariffs, and after the hawkish May statement) have certainly been less than encouraging.

All told, today's statements reduces our conviction in a July rate hike. Monetary policy isn't set in response to monthly noise, but uncertainty is undoubtedly elevated which will be taken into account in the rate decision (see Poloz's discussion paper from shortly after his appointment). The broader economic outlook may be developing in line with the Bank's expectations, but this uncertainty will temper the implications.

So, it is back to data dependency. Friday's GDP report and Business Outlook Survey will be key to watch, as will the May credit data early next week. In light of today's remarks, the burden of proof, and thus the likelihood of a July move hinges on seeing upside surprises.

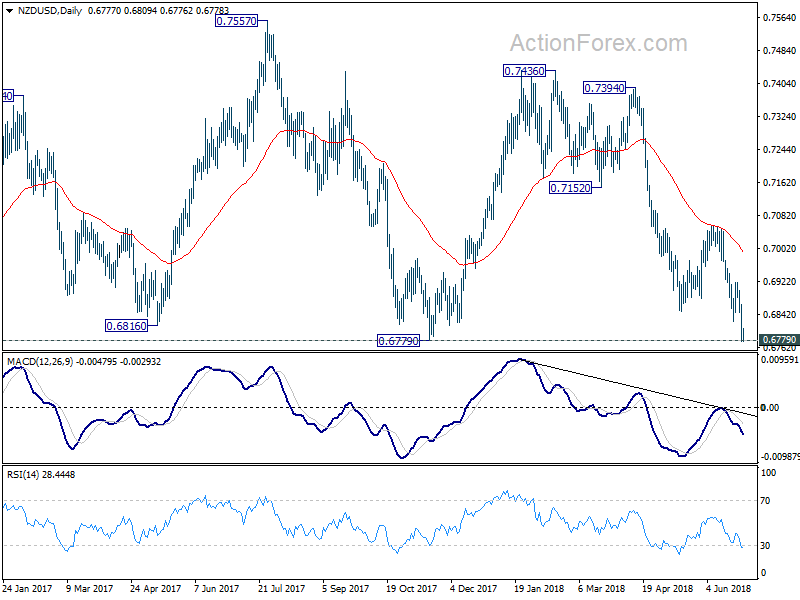

RBNZ ketp OCR unchanged at 1.75%, can move up or down after considerable period

RBNZ kept the Official Cash Rate unchanged at 1.75% at widely expected.It reiterated to "ensure the OCR is at an expansionary level for a considerable period." Bias is neutral as it's "well positioned to manage change in either direction – up or down – as necessary."

NZD/USD stays pressured after the release, partly also due to Dollar strength. NZD/USD is preassure 0.6779 key support level and there is no sign of bottoming so far.

Full statement below.

Statement by Reserve Bank Governor Adrian Orr:

Tena koutou katoa, welcome all.

The Official Cash Rate (OCR) will remain at 1.75 percent for now. However, we are well positioned to manage change in either direction – up or down – as necessary.

Our outlook for the New Zealand economy, as detailed in the May Monetary Policy Statement, remains intact. Employment is around its sustainable level and consumer price inflation remains below the 2 percent mid-point of our target, necessitating continued supportive monetary policy for some time to come.

Global economic growth is expected to support demand for our products and services. Global inflationary pressure is also expected to be higher but remain modest. This outlook has been tempered slightly by trade tensions in some major economies. Ongoing volatility in some emerging market economies continues.

Domestically, ongoing spending and investment, by both households and government, is expected to support growth. However, the recent weaker GDP outturn implies marginally more spare capacity in the economy than we anticipated. The Government's projected spending impulse is also slightly lower and later than anticipated.

CPI inflation is likely to increase in the near term due to higher fuel prices. Beyond that, inflation is expected to gradually rise to our 2 percent annual target, resulting from capacity pressures.

The best contribution we can make to maximising sustainable employment, and maintaining low and stable inflation, is to ensure the OCR is at an expansionary level for a considerable period.

Meitaki, thanks.

(RBNZ) Official Cash Rate unchanged at 1.75 percent

Statement by Reserve Bank Governor Adrian Orr:

Tena koutou katoa, welcome all.

The Official Cash Rate (OCR) will remain at 1.75 percent for now. However, we are well positioned to manage change in either direction – up or down – as necessary.

Our outlook for the New Zealand economy, as detailed in the May Monetary Policy Statement, remains intact. Employment is around its sustainable level and consumer price inflation remains below the 2 percent mid-point of our target, necessitating continued supportive monetary policy for some time to come.

Global economic growth is expected to support demand for our products and services. Global inflationary pressure is also expected to be higher but remain modest. This outlook has been tempered slightly by trade tensions in some major economies. Ongoing volatility in some emerging market economies continues.

Domestically, ongoing spending and investment, by both households and government, is expected to support growth. However, the recent weaker GDP outturn implies marginally more spare capacity in the economy than we anticipated. The Government's projected spending impulse is also slightly lower and later than anticipated.

CPI inflation is likely to increase in the near term due to higher fuel prices. Beyond that, inflation is expected to gradually rise to our 2 percent annual target, resulting from capacity pressures.

The best contribution we can make to maximising sustainable employment, and maintaining low and stable inflation, is to ensure the OCR is at an expansionary level for a considerable period.

Meitaki, thanks.

Eco Data 6/28/18

[php_everywhere instance="1"]

Chinese PMIs Due amid Ongoing Concerns Over Global Trade and a Weakening Yuan

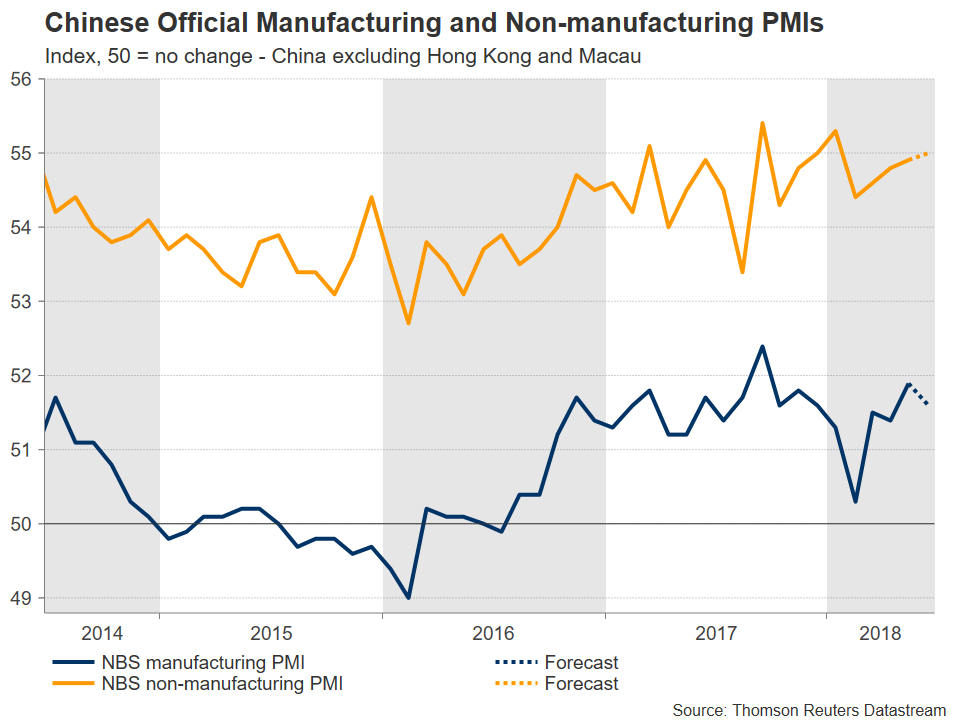

Chinese official PMI data for June are scheduled to be made public on Saturday at 0100 GMT. Manufacturing activity, which is expected to attract the lion’s share of attention, is projected to slightly ease though to still remain in expansionary territory. Beyond the releases, the ongoing spat between the US and China over trade and investment issues remains in the background, having the potential to move markets. Meanwhile, yuan weakness is attracting interest with some linking it to trade developments.

Official manufacturing PMI data out of China are anticipated to show the measure standing at 51.6 in June. This compares to May’s 51.9, which surpassed expectations to reach its highest since September 2017. Last month’s manufacturing PMI also constituted the 22nd consecutive month that the reading remained above the 50 level that distinguishes sectoral expansion from contraction. In the meantime, the respective non-manufacturing (services) PMI print is forecast to edge higher for the fourth straight month, specifically to stand at 55.0, from May’s 54.9. The Chinese services sector has gained greater prominence over the last number of years. This came on the back of government efforts to rebalance as well as diversify the economy by making it more dependent on services and spending, as opposed to relying almost entirely on investments and exports. Still, the figures on manufacturing activity are expected to be gathering more interest than those on services.

Overall, if the numbers come in line with projections, they would paint a relatively healthy picture, especially if one considers the continuing efforts by the Communist party to curb industrial pollution and limit the financial risks posed by excessive credit availability in the economy; both of these are factors that are weighing on economic activity, though at the same time they are contributing to more sustainable, higher quality growth moving forward.

Still, downside risks remain on the horizon that span beyond environmental considerations and high debt levels. Those relate to “differences” over trade – these include potential investment restrictions as well – between the US and China, the world’s two largest economies, which are seen as increasing the odds for a trade war that would act to the detriment of their respective economies as well as global growth.

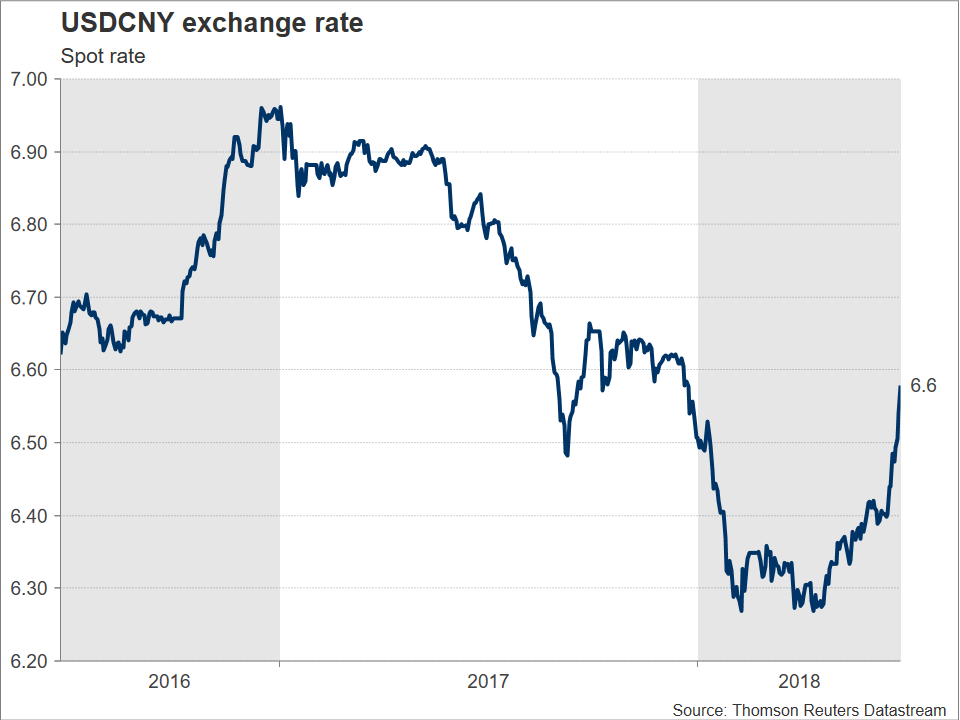

USDCNH, this referring to the US dollar versus the offshore-traded yuan, hit its highest since around mid-December earlier on Wednesday, with the onshore yuan (USDCNY – depicted in the chart below) also coming under pressure against the US currency. Some are attributing the slide in the yuan as coming on the back of Chinese policymakers purposefully devaluing the currency in response to US tariff threats. The fact that not too long ago, Chinese officials were struggling to limit accelerating capital outflows due to currency weakness discredits this view though, at least to an extent. Perhaps more likely “culprits” for the fall in the renminbi are increasing doubts on whether the nation can survive a trade war with the US, softer-than-expected Chinese economic data – for example May’s fixed asset investments, industrial production and retail sales – and divergent monetary policies between the Federal Reserve and the People’s Bank of China. Furthermore, it should be kept in mind that the dollar is not just stronger versus the Chinese currency in 2018, but also against most emerging market currencies, as well as versus the majors.

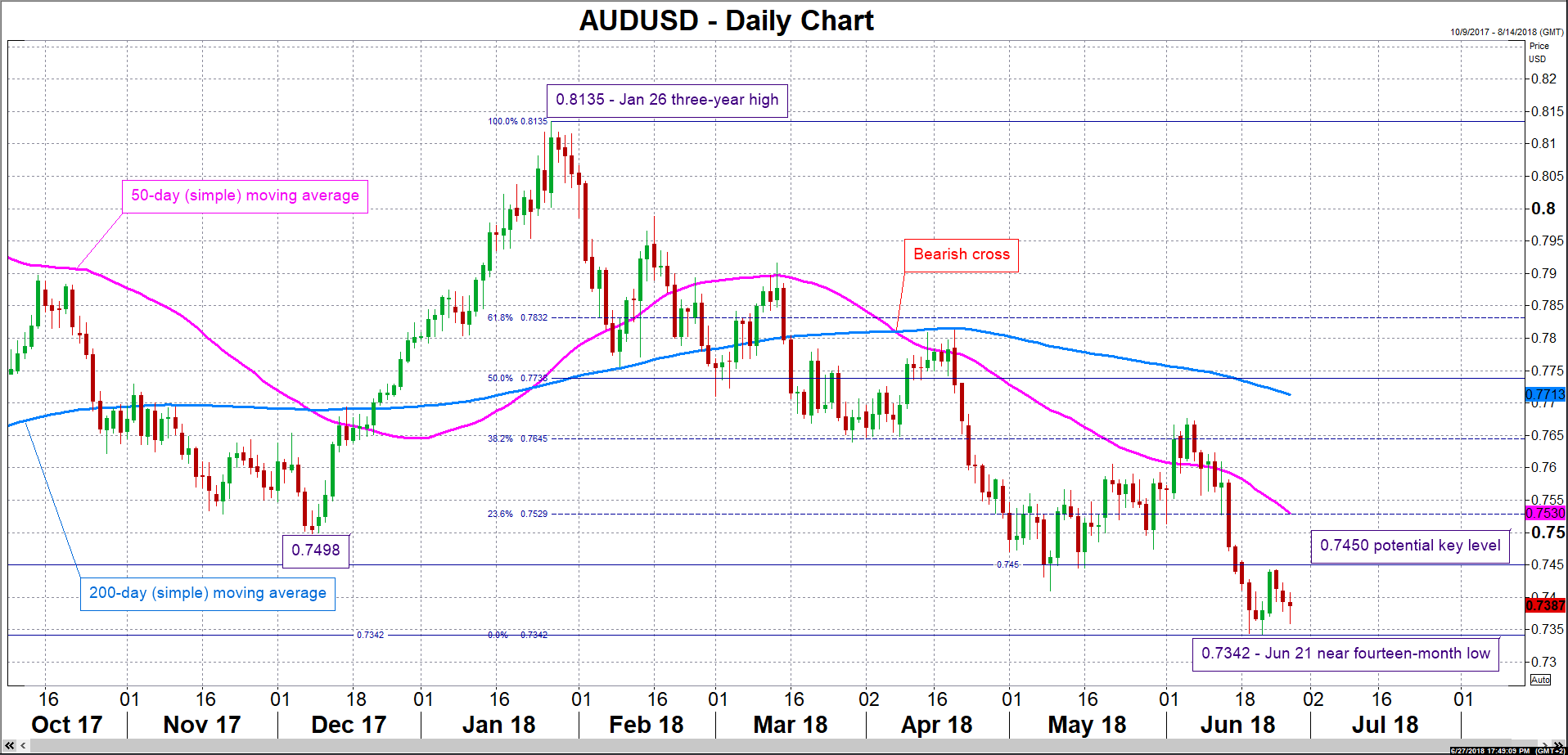

Besides the yuan, the Australian dollar is also attracting interest on the back of trade jitters and has been on the decline in recent weeks, falling to multi-month low levels versus the greenback. This has to do with the fact the Australian economy heavily relies on commodity exports and is thus seen as losing out considerably in the event of the imposition of barriers to trade. Moreover, Australia shares close economic ties with China – a strong Chinese economy is seen as aussie-positive and vice versa – which have rendered the aussie as a liquid proxy for China’s economy in investors’ minds.

Technically, a rising AUDUSD could meet a barrier around the 0.7450 mark that may have held some significance in the past, managing to resist a successful close below it a few times during May; in other words, this is a point that acted as support in the past and may now provide resistance. A successful break above would turn the attention to the area around the 23.6% Fibonacci retracement level of the January 26 to June 21 downleg at 0.7529, with the current level of the 50-day moving average roughly coinciding with this level. On the downside, support might come around the near 14-month low of 0.7342 from June 21, with steeper losses potentially meeting additional support around the 0.73 round figure.

Although Saturday’s releases may spur some positioning on the aussie on Monday when markets reopen for trading – a data beat is seen as aussie-positive and vice versa – still the Australian dollar seems more sensitive at the moment to the ongoing concerns over trade. Receding fears for a trade war will likely boost the aussie, with escalating tensions having the capacity to push it further down.

Lastly, Caixin’s manufacturing and non-manufacturing PMI figures, which focus on small and medium size Chinese businesses, as opposed to the official data which are broader in nature, are due out next week (on Monday and Wednesday correspondingly).

Japanese Industrial Output and Retail Sales to Deteriorate; Employment to Stay Firm

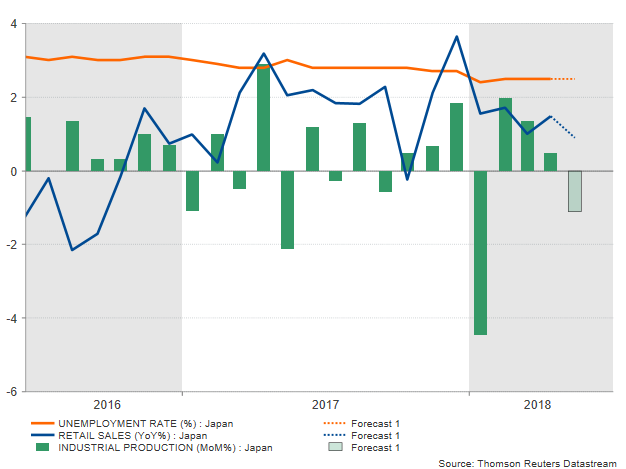

While the safe-haven Japanese yen tends to be less sensitive compared to other currencies when data releases come out of the calendar, updates on economic measures out of Japan can improve or deteriorate investors’ sentiment on the economy. On Thursday, Japan will issue readings on retail sales, while late on Friday employment and industrial production figures will also come under the spotlight. However, the numbers are not expected to show improvement, with labor stats projected to remain unchanged, while retail sales and flash industrial production forecasted to ease.

On Friday (Thursday at 2330 GMT), the Statistics Bureau is expected to say that its labour survey for the month of May was no different to April’s report as analysts believe that the unemployment rate stood flat at 2.5% for the third consecutive month, the lowest in 25 years, while the jobs-to-application ratio held at 1.59, at the highest since 1974. While both figures indicate that the Japanese labor market remained tight despite GDP growth estimates for the first quarter of the year falling to negative territory, recent evidence on wages showed that growth in cash earnings in April narrowed sharply. In fact, payments almost halved, easing from a multi-year high of 2.0% expansion to 0.8% over the year to hint that inflationary pressures are nowhere near to heating up. Household spending supported this view as well when April’s numbers dropped surprisingly by 1.3% y/y, recording the second straight month of losses. Retail sales – a proxy for consumer spending – due on Thursday (Wednesday at 2350 GMT) are anticipated to continue this narrative, showing that sales at the retail level have expanded by 0.9% y/y in May compared to 1.5% in the preceding month.

Meanwhile, on the supply side, production in the industrial sector, where export activities are mostly concentrated, is forecasted to have weakened even further in May according to initial monthly estimates. Particularly, forecasters anticipate the gauge to post a strong pullback of 1.1% m/m after inching up by 0.5% in April. This would be the first decline since the 6.8% sharp downfall in March.

In the meantime, inside the Bank of Japan, policymakers believe that the economy which contracted by 0.6% on an annualized basis in the first quarter of the year, will return to positive territory, attributing the weakness to temporary factors such as the unusually bad weather according to June’s BoJ summary of opinions. Having said that, they still insist that monetary policy should remain accommodative with interest rates remaining below zero, in hopes inflation will continue its broken uptrend towards the BoJ price target of 2.0% despite removing the timeframe for achieving its price goal at April’s policy meeting and downgrading their view on inflation earlier this month. However, with Japanese factories, especially in the growth-driving automobile sectors, facing threats from the US import tariffs on steel (25%) and aluminium (10%) in effect since June 1, the BoJ will likely hold off from winding down its stimulus even if its US and UK counterparts continue to deliver higher rates and its EU peers announcing the termination of their asset purchases program this year. Risks are also stemming from the escalating US-China trade war given that China is Japan’s biggest export destination and any trade restrictions weakening Chinese purchasing power could limit demand for Japanese products. Nevertheless, Japan might face a smaller negative impact than other tariff-affected countries due to their high-quality products which export partners might face difficulty to replace.

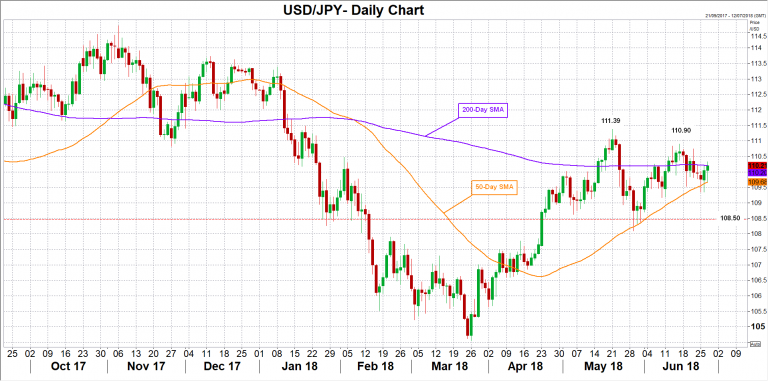

Turning to forex markets, the safe-haven yen, which tends to hardly respond to data releases, has been somewhat gaining on the back of rising tensions in the trade sphere over the past two weeks. In the wake of the above data the yen might not see big changes but a big positive surprise in the numbers – especially in the industrial production front – could increase optimism that economic growth could return to positive territory in the second quarter, increasing buying interest for the yen. In this case, dollar/yen could shift lower towards the 50-day MA at 109.68, which the market was unable to break since mid-April. Even lower, the 109 round-level could come into view, while in case of steeper declines, bears could also eye the area around 108.50, where the market stopped in previous months.

On the other hand, a deterioration in the measures could send dollar/yen towards June 15 peak of 110.90, while any step above this level could open the way towards May 21 high of 111.39.

On Friday (Thursday 2330 GMT) , Tokyo CPI readings for the month of June will attract some attention too as it will be another guide to inflation prospects after the more important to BoJ nationwide core CPI stood flat at 0.7% in May as expected.

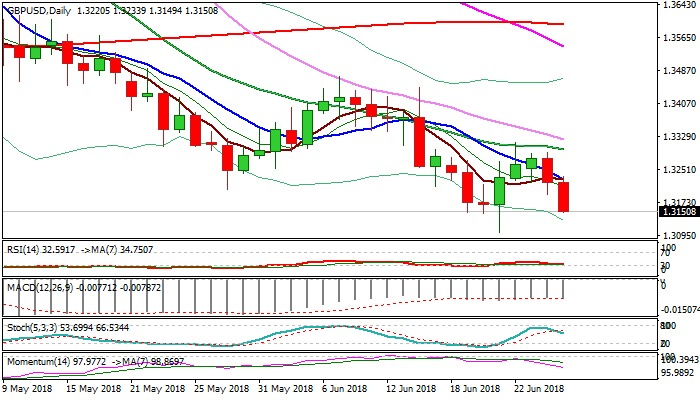

Weak Techs and Sentiment Keep Pound Under Pressure for Retest of Key 1.3101 Support

Cable stays in red for the second straight day and dipped to one-week low at 1.3150, retracing 76.4% of 1.3101/1.3315 recovery leg.

Tuesday’s bearish engulfing and daily techs in bearish setup weigh on near-term action, with negative sentiment being soured by expectations over Brexit’s impact on British economy, as well as doubts whether the BoE will raise interest rates this year.

Fresh weakness pushed the price back into weekly cloud after unsuccessful attempt to break above and pressures key near-term support at 1.3101 (21 Jun spike low).

Firm break here is needed to complete corrective phase and open way for test of psychological 1.30 support.

Falling 10SMA tracks descend and marks solid resistance at 1.3229.

Res: 1.3191; 1.3229; 1.3299; 1.3323

Sup: 1.3146; 1.3101; 1.3038; 1.3000