Sample Category Title

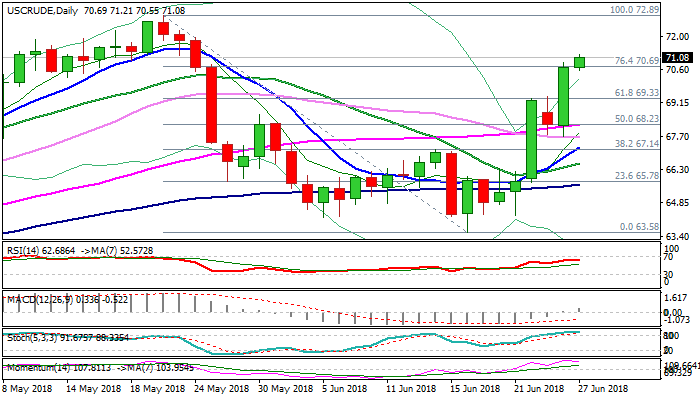

WTI Oil Outlook: Bulls May Extend To Key Barrier At $72.89 On Upbeat Crude Stocks Report Today

WTI oil price broke above $71 per barrel on Wednesday, extending strong rally of the previous day's 3.7% advance.

Oil prices are in steep ascend which extends into second consecutive week and supported by several factors.

Initial boost came from OPEC's decision lower increase of global oil production than market initially expected, which sparked strong rally last Friday.

Supply disruption in Canada, uncertainty over oil exports from Libya further supported oil prices which accelerated after much stronger than expected draw in US crude stocks on Tuesday (API report showed draw of 9.22 million barrels vs 2.5 million barrels draw forecasted).

Tuesday's strong rally generated bullish signals on close above psychological $70 barrier as well as daily cloud top ($70.39).

Today's extension above $71.00 opens way towards key resistance at $72.89 (22 May recovery high, the highest since Nov 2014).

Bullish setup of daily techs supports the notion, along with strong bullish sentiment, with focus turning towards release of US EIA crude oil stocks report, due later today, which is forecasted for 2.57 million barrels draw vs previous week's draw of 5.91 million barrels.

Any surprise at the upside could spark fresh acceleration of oil price.

Conversely, bulls may take a breather on downbeat crude inventories results, with overbought studies expected to support action.

Res: 71.21, 71.86, 72.28, 72.89

Sup: 70.39, 70.00, 69.33, 68.21

BoE Carney warns of financial stability risks originating beyond the UK shores

The Bank of England published the latest Financial Stability Report today. In the opening remarks of the press conference, BoE Governor Mark Carney warned that "events of the past few months are a reminder that many of the most important risks to financial stability in the United Kingdom originate beyond our shores."

The risks include "recent tightening in global financial conditions" that could be a "'precursor to a much more substantial snapback in world interest rates". There could be "more challenging bank, corporate and sovereign funding conditions."

Besides, "Rising protectionist sentiment could sap some of the current strength of the global economy and reduce the size of sustainable external imbalances."

In addition, "the complete set of mitigants to the risks of a cliff-edge Brexit also rely on the efforts of EU authorities". Lastly, "cyber risks to UK financial services could originate from anywhere on the planet."

Below is the press conference.

https://www.youtube.com/watch?v=AMggL6LOpds

EUR/USD – Euro Subdued, Investors Await US Durable Goods Data

EUR/USD has ticked lower the Wednesday session. Currently, the pair is trading at 1.1640, down 0.07% on the day. In economic news, there are no major eurozone events. In the U.S, the focus is on durable goods orders. Core durable goods orders are expected to drop to 0.5%, while durable goods orders is forecast to drop -0.9%, which would mark a second straight decline. On Thursday, EU leaders meet for a two-day summit in Brussels. The U.S will release Final GDP for the first quarter and unemployment claims.

With a lack of major eurozone indicators this week, the markets will have plenty of time to focus on this week’s EU economic summit. High on the agenda will be the escalating trade war, which has been marked by the U.S and China imposing tariffs on each other’s goods. The EU and the U.S have also been involved in a tariff spat, with the EU firing the latest salvo when it slapped tariffs of 25% on $3.3 billion of U.S products. This move was in response to U.S tariffs on EU steel and aluminum imports. With President Trump not showing any intent to blink first, all eyes will be on the summit, as the markets wait for a response (olive branch?) from EU leaders. Another key issue will be Brexit, as the sides remain far apart on a number of issues, with Britain scheduled to leave the club in March 2019. The EU had said that it wanted issues such as the Irish border to be resolved by the June summit, but this won’t happen, and the EU will now have to set another deadline, with time running out. There have been various suggestions for a type of customs union arrangement between Ireland and Northern Ireland, but the May government is split on the issue, much to the frustration of EU leaders. If EU leaders do little more than bash the British over Brexit, the euro could lose more ground to the U.S dollar.

The U.S economy continues to perform well, buoyed by steady expansion and a labor market that is close to capacity. However, the trade war between the U.S and its major partners could be the dark cloud on the horizon. The Federal Reserve now plans to raise rates four times in 2018 (up from three), but a global trade war could force the Fed to revise its forecast back to three hikes. On Tuesday, Atlanta Fed bank president Raphael Bostic said that if the trade war intensified, he would vote against a fourth rate hike, due to downside risks to the economy. Fed Chair Jerome Powell sounded pessimistic about the economic effects of trade tensions at an ECB forum earlier in June, and if other Fed members express concerns, the Fed could delay a fourth hike until 2019.

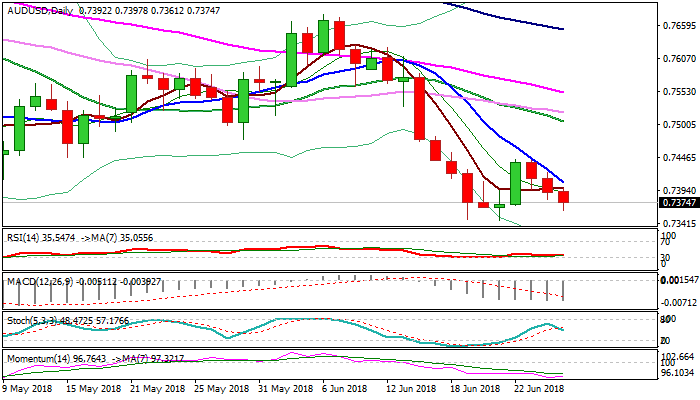

AUDUSD Outlook: Bears Eye Key Supports At 0.7345/25 As Trade War Fears Keep Aussie Under Pressure

The Aussie dollar holds in red for the third consecutive day and threatens of retesting 0.7345 base, as persisting fears about trade war escalation keep Aussie under pressure.

Fresh weakness from 0.7443 double top (22/25 Jun) where recovery from 0.7345 stalled, retraced the biggest part of 0.7345/0.7443 recovery leg and focus key supports at 0.7345 (19/21 Jun lows) and 0.7325 (Fibo 61.8% of 0.6825/0.8135 2016/2018 ascend).

Break here would generate strong bearish signal for continuation of larger fall from 0.8156 (2018 high).

Daily techs in full bearish setup maintain scenario, with broken 5SMA offering initial barrier at 0.7397 and falling 10SMA (which tracks descend since mid-June and currently at 0.7407) expected to cap upticks.

Res: 0.7397, 0.7407, 0.7423, 0.7443

Sup: 0.7361, 0.7345, 0.7325, 0.7283

After PMI Boost, Euro Eyes Economic Sentiment Indicator

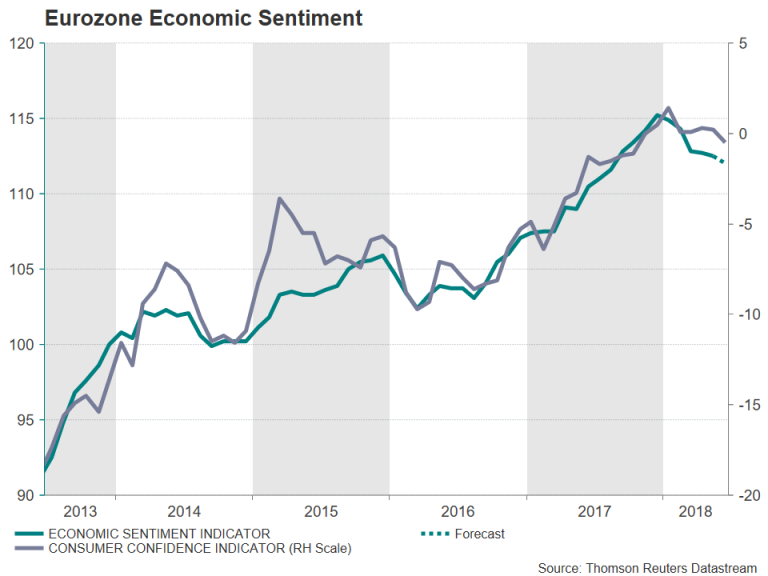

The European Commission will publish its economic sentiment indicator (ESI) on Thursday at 09:00 GMT, which comes hot on the heels of last week's much better-than-expected Eurozone services PMI from IHS Markit. The flash PMI readings for June raised hopes that the Eurozone soft patch is coming to an end, boosting the euro. However, consensus forecasts for the ESI are for another drop in the indicator in June.

Sentiment across the euro area hit the highest since 2000 in December, with the index rising to 115.2, as the growth momentum peaked. However, following the slowdown since the start of 2018, the gauge has retreated to 112.5. Expectations are for the ESI to continue to trend lower in June, falling to 112.0. While the pullback in the economic sentiment index hasn't been as large as the more closely-watched manufacturing and services PMIs, it's reinforced the view that business morale has been dampened notably since the beginning of the year.

Looking at the ESI's sub-indices, the weakening sentiment over the past few months is visible across all sectors. The industry, services, consumer, retail trade and construction sectors which make up the ESI have all come off their highs achieved in December/January. European consumers have also been feeling less optimistic. The European Commission's consumer confidence indicator fell back into negative territory in June, declining to -0.5 in the flash reading and retracting from the 17½-year high of 1.4 reached in January. It is expected to remain unrevised in Thursday's final print.

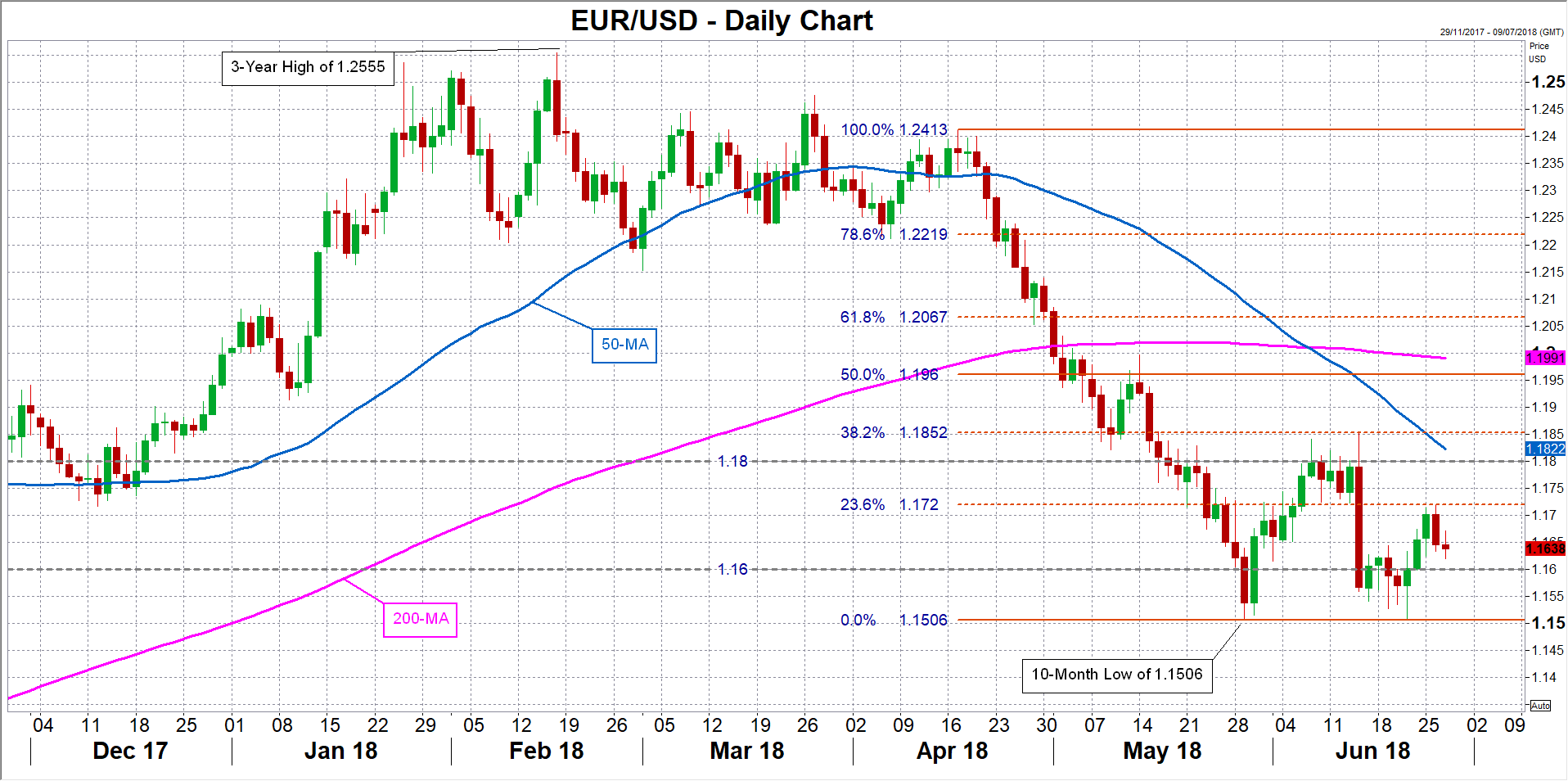

Having regained a positive footing after the unexpected jump in the services PMI on Friday, the euro could extend it gains versus the US dollar if the economic sentiment survey provides further evidence that business conditions are improving in the Eurozone. The single currency is currently facing immediate resistance at the 23.6% Fibonacci retracement of the April-June downslide, around $1.1720. A better-than-expected set of figures on Thursday could lift the euro above this barrier, bringing the $1.18 handle within reach.

However, a disappointing survey would cast doubt about a pick up in Eurozone growth and could cut short the euro's upside correction. Euro/dollar could re-test the $1.16 level on fresh selling pressure, with a break below it opening the way to May's 10-month low of $1.1506.

EURJPY In Neutral Bias After Climbing Above 23.6% Fibonacci Mark

EURJPY holds above the 23.6% Fibonacci retracement level of the downleg from 137.50 to 124.60, around 127.65 in the 4-hour chart but lost its strong momentum from yesterday.

From the technical point of view, the momentum indicators are supportive of the short-term neutral mode, with the RSI sloping slightly to the downside below the 50 level and the MACD oscillator holds near zero with weak movement.

If the price moves higher and jumps above the 20-simple moving average in the 4-hour chart, it could hit the 128.80 resistance level. However, should prices climb higher again they would challenge the 38.2% Fibonacci mark of 129.55, which stands near the descending trend line.

In case of a continuation of the medium-term downward movement and a breach of the 23.6% Fibonacci level, price action would likely meet support at the 127.00 handle. Slightly below this level, 126.60 acts as major support. A break below this hurdle as well would drive the pair until the next support of 126.30, taken from the low on May 31.

To sum up, the bearish outlook remains intact in the bigger picture, with the moving averages all pointing downwards in the daily chart and the price holding below the descending trend line since February 1. However, in the short-term, the pair seems to be neutral.

USD Holds Ground As Trade Uncertainty Prevails

Trade war remains main driver

The ongoing trade war is creating a lot of confusion on the FX market, as market participants struggle to guess out it would play out. So far, the US dollar has largely benefited from this uncertainty and extended gains against most of its peers, with the exception of safe haven currencies. Since mid-June, the speculators are long USD again. This is the first time since June last year. Traders are heavily against the Kiwie, the Aussie and the Swissie. However, regarding the latter, speculators started to reduce their short CHF exposure over the last few weeks amid escalating trade tensions.

Recently, Trump has been facing setbacks in the form of retaliatory measures and relocation announcement of certain US companies, which would suffer from upcoming tariffs. Against such a backdrop, it is reasonable to expect that Donald Trump would ease its stance and negotiate with its trade partners. Meanwhile, the market remains in risk-off mode by dumping currencies of export-oriented countries and favouring the Swissie and the yen. We see no reason for this trend to reverse anytime soon, at least as long as the uncertainty persists.

New Zealand: strong trade surplus

Numerous countries would envy New Zealand’s commercial situation. Despite trade tensions that globally create disorder in business transactions, it seems that the New Zealand economy continues to surprise, with a trade balance surplus for the month of May written at NZD 294.28 million (USD 206 million), its highest rate since December 2017.

With exports rising by NZD 454.30 million and imports maintained at a constant pace (NZD 5.12 billion), it appears that the New Zealand economy is more and more solicited by its commercial partners which require to find alternatives for their existing domestic demand in consumption goods. Indeed, increasing by 27%, 17%, and 0.5% for China, EU and Japan respectively due to a stronger demand in meat, lamb, fruit and aluminum, it seems that the New Zealand economy currently lies in a rather comfortable commercial situation from now, although business confidence continues to decline in June for the 4th month in a row according to the survey.

Expected to maintain its reference rate unchanged at 1.75% due to continued weakness in economic growth and inflation, the Bank of New Zealand will most probably maintain its dovish stance in today’s monetary policy meeting, a rather worrying situation for the kiwi. Currently trading at 0.6823, its lowest level since July 2017 (-4% year-to-date), the NZD/USD is expected to decline further, as a stronger greenback coupled with widening interest differentials will strengthen the downward tendency. The pair is expected to head along 0.6810 in the short-term.

ECB: Impacts of exchange rate on inflation are spread out over several quarters

ECB published an article today titled Monitoring the exchange rate pass-through to inflation. There it noted that exchange rate developments can play an "important role" in shaping the HICP inflation outlook, through "both direct and indirect channels". The impacts are "spread out over several quarters". And, the effect could be difficult to detect if it is "offset by a confluence of other factors". Among the components, "energy and food, non-energy industrial goods" are most sensitive to exchange rate movements.

As the background, Euro appreciated by about 8% in nominal effective terms and by about 10% against the US dollar, between April 2017 and May 2018. The impact of past euro exchange rate appreciation has been clearly visible in import price developments. The report pointed to import prices for non-food consumer goods, which dropped to 2.0% in April 2018, down from 1.3% in 2017. Over the same period, extra-euro area import price inflation for industry (excluding energy and construction), which also affect prices earlier in the domestic production chain, decreased from 3.1% to ‑1.7%.

Producer price inflation, on the other hand, has remained resilient to downward pressure from the exchange rate appreciation. PPI for intermediate goods declined only moderately during the period. PPI of non-food consumer goods increased from 0.2% in April 2017 to 0.5% in April 2018.

Indirectly, euro exchange range can affect domestic price pressure through company profits, "albeit with a somewhat ambiguous overall sign." The

non-energy industrial goods inflation does not provide a clear sign for significant effects of the exchange rate appreciation.

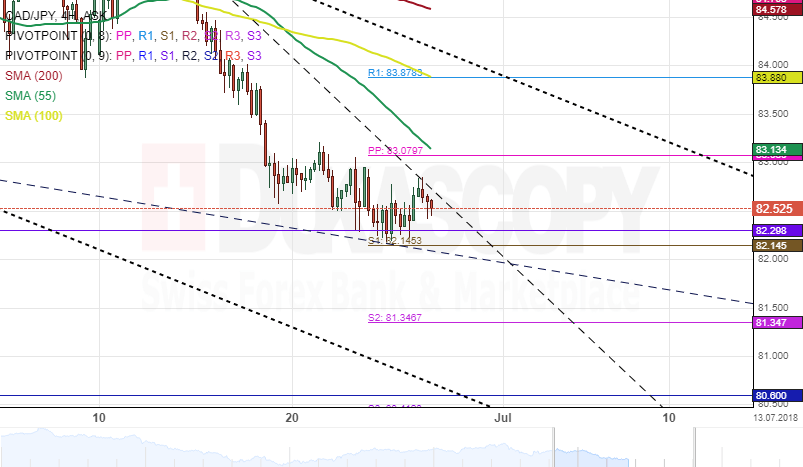

CAD/JPY 4H Chart: Falling Wedge

The CAD/JPY currency pair has shown no massive changes to its overall price movement during the past few weeks.

The exchange rate showed no significant changes to its price range. Moreover, the movement has been constrained by several descending patterns, the most recent of which, is a falling wedge pattern.

There is still downside potential that could drive the currency exchange rate lower toward the bottom border of the dotted downtrend channel during the following trading sessions.

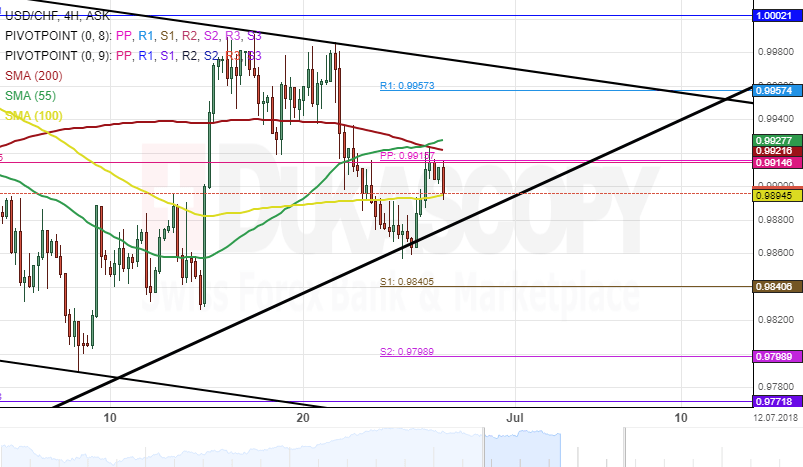

USD/CHF 4H Chart: Pair Bullish In Short-Term

Following a massive surge of 9.40% which happened beginning of February, the US Dollar has been trading in a junior descending pattern against the Swiss Franc. The currency pair tested the lower boundary of an ascending channel on June 26.

It seems that the exchange rate has bounced off the bottom border of the dominant pattern and this could follow by a subsequent surge for the USD/CHF currency pair.

As for near future, it is likely that the currency exchange rate breaks out from a strong resistance cluster formed by the combination of the weekly and the monthly PPs near 0.9921 during the following trading