Sample Category Title

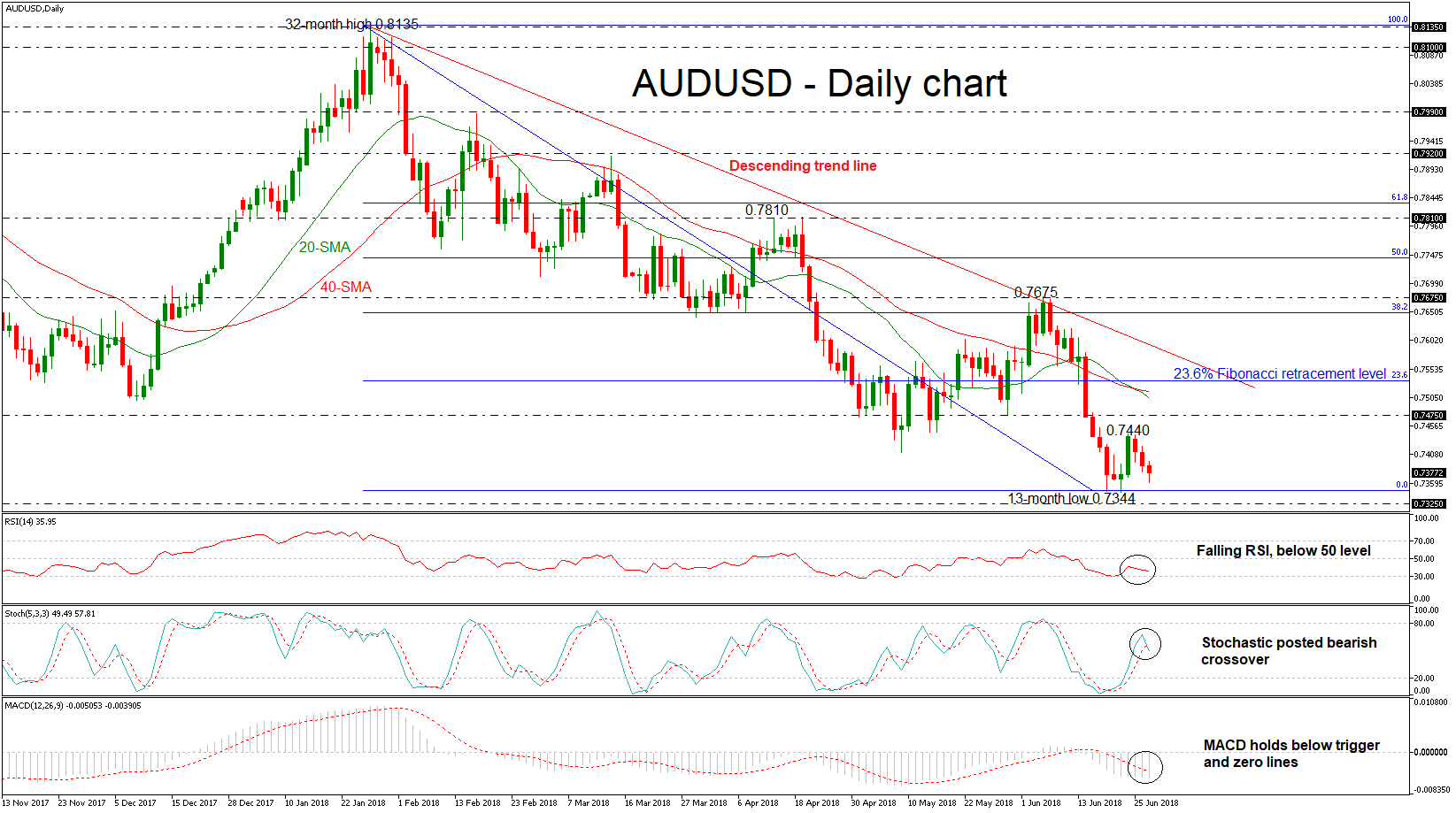

AUDUSD Bears Hold Control, Hovers Near 13-Month Low

AUDUSD is set to post the third consecutive bearish day as it remains under strong downside pressure after the bounce off the 0.7440 high, reached last Friday. The sharp sell-off especially this month endorses the scenario for further declines in the medium-term.

In the daily timeframe, the momentum indicators are supportive of the bearish picture, with the RSI falling into negative territory below 50 and approaching the 30 oversold mark. Also, the %K line of the stochastic oscillator created a negative cross with the %D line and is moving towards the oversold zone. The MACD oscillator lies below its trigger and zero line, suggesting further losses.

Currently, the price is developing slightly above the 13-month low of 0.7344 that hit on June 21. Immediate support below this level is being provided by the 0.7325 barrier, taken from the low on May 2017. Should prices dip lower again could open the way towards the 0.7160 hurdle, identified by the trough on December 2016.

In case of an upward attempt, the next resistance for investors to have in mind is the 0.7475 level, taken from the bottom on May 31. A jump above this level, the price could challenge the 20- and 40-simple moving averages (SMAs) around 0.7510. Slightly above this region the 23.6% Fibonacci retracement level of 0.7533 of the downleg from 0.8135 to 0.7325, could provide strong resistance for the bulls.

Overall, both the short- and medium-term outlooks are currently looking bearish, though caution is warranted in the near-term as there are signs of a possible new multi-month low. In addition, AUDUSD has been developing within a descending move since January 26.

Markets Bounce As Trade Tensions Ease For Now

Here are the latest developments in global markets:

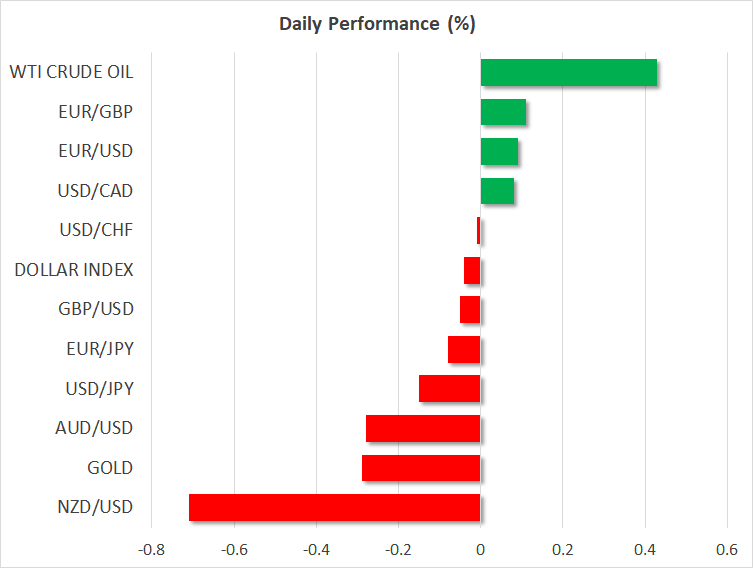

FOREX: The US dollar index is down on Wednesday, but by less than 0.1%. It managed to rebound yesterday, recovering some losses from the previous three sessions. The euro was on the back foot yesterday, perhaps amid jitters ahead of the EU summit tomorrow, while the pound retreated as well following some dovish-perceived signals from the BoE.

STOCKS: Concerns around an imminent trade war took a back seat yesterday, after the Trump administration hinted it may opt for less-aggressive measures to curb Chinese investments into US technology firms. The tech-heavy Nasdaq Composite rose by 0.39%, while the S&P 500 and Dow Jones edged higher by 0.22% and 0.12% respectively. However, the rebound may be short-lived, as futures tracking the Nasdaq 100, S&P, and the Dow are pointing to a notably lower open today. In Asia, most major indices were in the red. In Japan, the Nikkei 225 fell 0.31% but the Topix managed to gain 0.02%, while in Hong Kong, the Hang Seng dropped by 1.07%. Meanwhile, Europe looks undecided, as futures following the major benchmarks are mixed and close to neutral territory.

COMMODITIES: Oil prices raced higher on Tuesday, amid headlines that the US will press its allies to halt their Iranian oil imports altogether by November, something that would tighten global supply. Some news that militants have taken control of oil ports in Libya, and a larger-than-anticipated drawdown in the private API inventory data released yesterday may have helped as well. WTI and Brent crude are up by 0.4% and 0.6% respectively on Wednesday as well. In precious metals, gold prices are down by 0.3% today, posting a new low for 2018 of $1,253. The dollar-denominated metal continues to be battered by a strong US dollar, and has displayed a very limited response to mounting trade tensions over the past weeks.

Major movers: Markets take a breather as Trump extends “olive branch”; dollar rebounds, euro and pound tumble

The US dollar index edged higher on Tuesday, recovering some of the losses it posted in the previous three sessions. The move came as concerns around an escalating US-China trade confrontation eased somewhat, following “peace” signals from US President Trump. He said his nation may not restrict all Chinese investments into high-tech US firms, but instead may rely on a committee to scrutinize foreign acquisitions for national security risks, on a case-by-case basis.

The fact that the US administration seems to have extended an “olive branch” to China likely dampened concerns around further escalation, for now at least. As a result, the safe-haven Japanese yen retreated against the dollar, while major stock indices like the S&P 500 rose a little. Risk sentiment remains very fragile, with markets switching from gains to losses almost daily, and any new signals on the trade front will be closely watched.

In the UK, the pound came under renewed selling interest yesterday, after two BoE policymakers struck different chords. BoE MPC member Ian McCafferty – who will leave the Bank at the end of August – and his incoming replacement Jonathan Haskel were both on the wires, and appeared to be at the two extreme ends of the hawk-dove spectrum. McCafferty called for hikes without delay, while Haskel kept the option of further rate cuts on the table. The difference in views was so striking that it likely dampened expectations for rate increases beyond August, amid speculation that one of the most hawkish voices in the BoE would be replaced with a dovish one.

The euro tumbled against its major peers on Tuesday, without any clear catalyst behind the move. Its underperformance may reflect market jitters ahead of tomorrow’s EU summit, where it increasingly appears that unless Angela Merkel can secure a deal on immigration, then her job as German Chancellor may be in jeopardy.

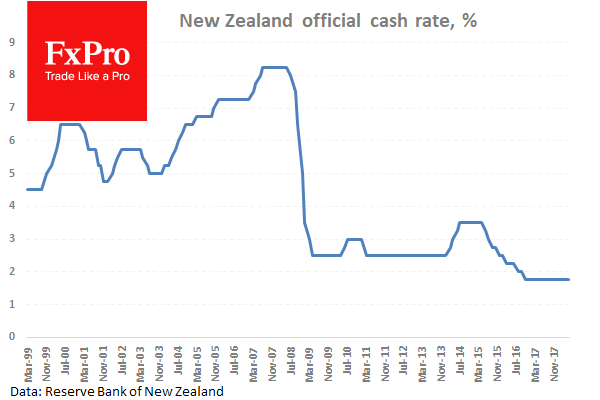

Elsewhere, kiwi/dollar is down by 0.7% today, touching a fresh seven-month low, after the ANZ business survey for June revealed another notable drop in business sentiment. While typically not a major market mover, the decline may have generated speculation for a more cautious bias by the RBNZ today, which will announce its rate decision at 2100 GMT; rates are expected to be maintained at the historic low of 1.75%.

Day ahead: US durable goods and pending home sales due; global trade developments remain in focus

The main release out of Wednesday’s calendar are capital goods orders out of the US. Beyond releases, any updates on the front of global trade will be closely watched.

The European Central Bank will be releasing monthly data on lending and money supply at 0800 GMT, while the Bank of England’s Financial Stability Report for June is due at 0930 GMT.

At 1000 GMT, the Confederation of British Industry’s distributive trades balance relating to retail sales growth is projected to stand at +11 in June, matching May’s reading which was the highest since January.

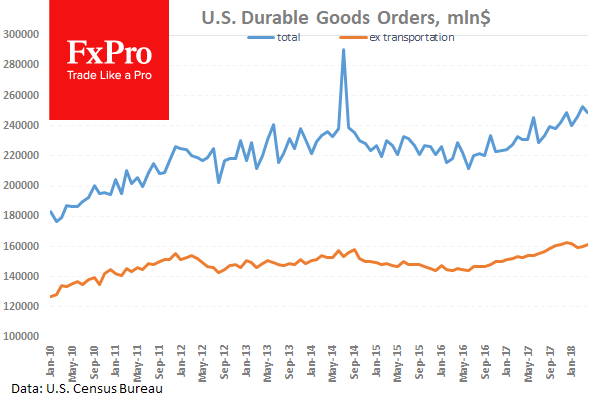

The attention will next turn to the US which will see the release of durable goods orders data – that give an indication on business spending – for May at 1230 GMT. The headline measure of orders is forecast to record its second straight monthly decline, specifically to fall by 1% m/m after contracting by 1.6% in April. The core measures of capital goods orders will also be watched. Projections for those are mixed, with orders that exclude defense expected to decline by 1.0% m/m, and those that exclude transportation anticipated to increase by 0.5% m/m. It would be interesting to see if the releases offer any clues as regards whether rising trade tensions are starting to weigh on business activity in the world’s largest economy.

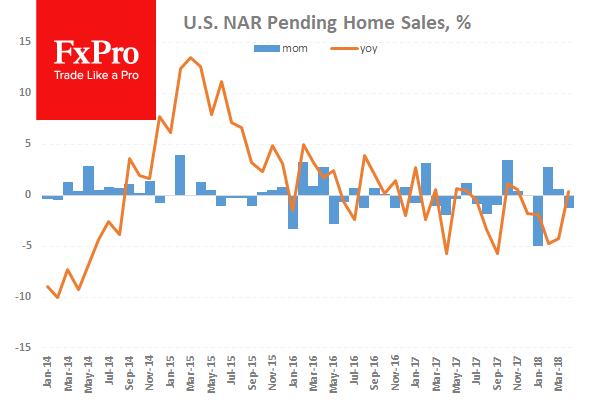

US pending home sales data for May are due at 1400 GMT. Sales are expected to increase by 0.5% m/m in May after contracting by 1.3% in April.

Once again, trade developments which have implications not just for FX markets but other asset classes as well, will be closely monitored.

Fed Vice Chair for Supervision Randal Quarles (1500 GMT – permanent FOMC voting member), Boston Fed President Eric Rosengren (1430 GMT – non-voter in 2018) and Bank of Canada Governor Stephen Poloz (1915 GMT) are some of the policymakers making appearances today.

EIA data on crude oil inventories due at 1430 GMT might offer some short-term direction to oil prices. Crude stocks are forecast to have declined by around 2.6 million barrels during the week ending June 22, after falling by around 5.9m in the previously tracked week.

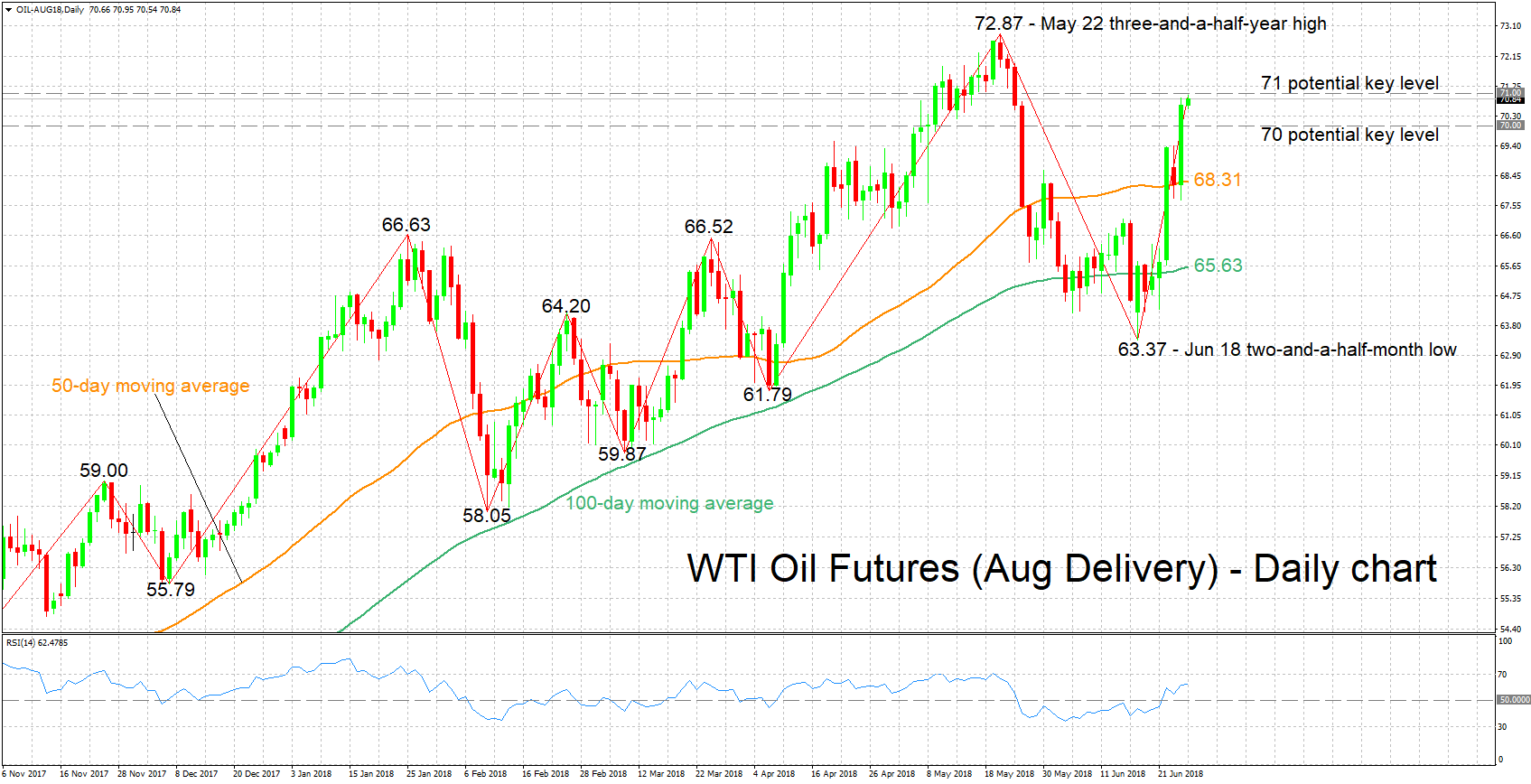

Technical Analysis: WTI oil futures bullish at one-month high

WTI oil futures (August delivery) have risen considerably over roughly the last ten days and they touched a one-month high of 70.95 earlier on Wednesday. The RSI remains on the rise in bullish territory, projecting a positive picture in the short-term. Notice though that the indicator has eased somewhat, indicating a partial loss of positive steam.

If today’s EIA report shows a larger-than-anticipated drawdown in crude inventories, then prices could move higher. Immediate resistance seems to be taking place around the 71 round figure which may carry psychological significance. An upside break would increasingly bring into scope the three-and-a-half-year high of 72.87 from May 22.

On the downside and in case of a smaller-than-expected drawdown in crude stocks (or a buildup) that pushes prices down, support could come around the 70 handle which may also be of psychological importance. Steeper losses would shift the focus to the region around the current level of the 50-day moving average line at 68.31.

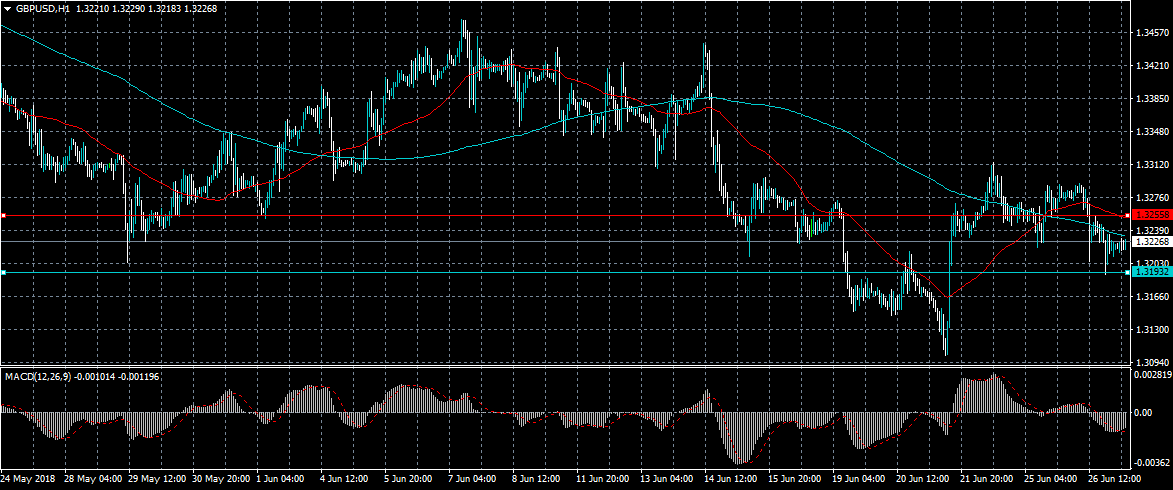

GBPUSD Strongly Bearish Below 1.3193 Level

The British pound has fallen sharply lower against the US dollar, after Bank of England member Jonathan Haskel delivered a dovish speech about future rate hikes from the BOE. The GBPUSD pair also came under pressure after repeated technical failure before the 1.3300 level and a reversal higher in the value of the US dollar index. A scheduled speech from Bank of England Governor Mark Carney this morning will likely set the intraday trading-tone for the GBPUSD pair.

The GBPUSD pair will turn strongly bearish below the 1.3193 level, key support is found at the 1.3144 and 1.3101 levels.

If the GBPUSD pair trades above the 1.3255 level, key technical resistance can be found at the 1.3291 and 1.3313 levels.

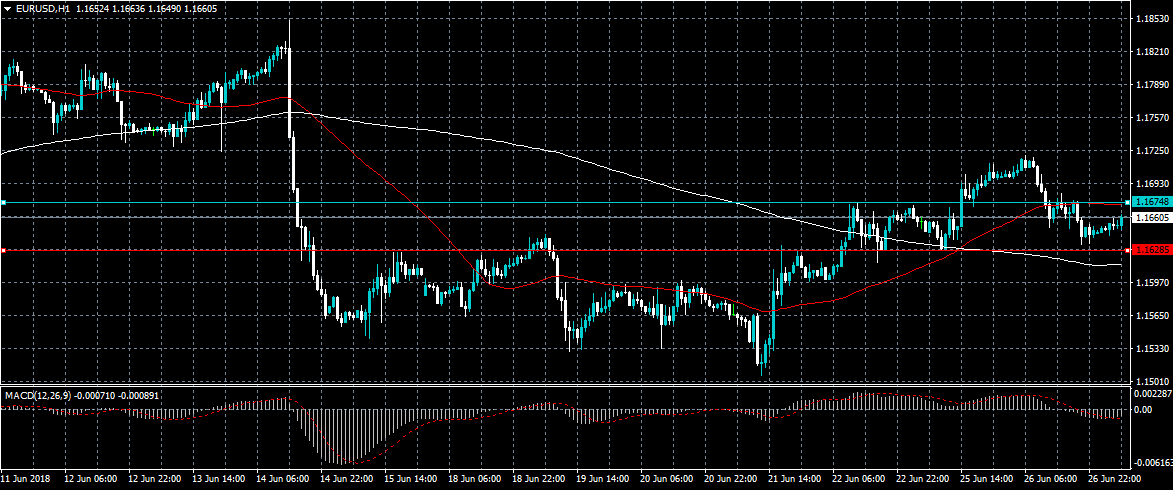

EURUSD Intraday Bearish Below 1.1674 Level

The euro is moving toward the lower end of its recent short-term trading range against the greenback, as the US dollar index starts to move higher. The EURUSD pair also came under selling pressure on Tuesday, as buyers failed to hold price above the 1.1700 level. Intraday sellers will attempt to breach the current weekly-low, at 1.1628, while buyers will try to maintain price back above the former weekly-high, at 1.1674.

The EURUSD pair is intraday bearish while trading below the 1.1674 level, key support is located at the 1.1628 and 1.1599 levels.

If EURUSD buyers move price back above the 1.1674 level, key resistance is then located at the 1.1700 and 1.1724 levels.

Postive Crypto News Does Little To Save Ethereum

The price of Ethereum declined overnight despite yesterday’s news that Andreessen Horowitz – one of the biggest venture capitalists in the world – had started a crypto fund. Horowitz is one of the most storied investors in Silicon Valley with his investment interests associated with companies like Facebook, Square, Cadre, and TransferWise among others. A few months ago, this news would have led to more demand on Ethereum and other related cryptocurrencies.

In addition to this, Facebook reversed its earlier policy on cryptocurrency-related advertisements. In an updated policy, Facebook announced that it would start accepting adverts from pre-approved cryptocurrency companies. However, according to Bloomberg, ICOs and other cryptocurrency startups had already found a way of advertising their products on social media using online influencers.

The ETH/USD pair is currently trading at $430, which is the lowest level since April this year. The price is slightly lower than the 200-day moving average. The current decline started in early May when the pair reached a high of $795. Since then, the pair has struggled to find a floor. It has continued to reach new lows every day and its attempt to recover have found a resistance. The pair’s RSI is currently at 27. During the decline, the oversold levels have done little to accelerate the recovery. Therefore, there is a high likelihood that the pair will continue falling, and possibly reach a low of $350 in the next few days.

US Data Fed Speakers In The Headlines On Wednesday

A combination of economic data and central bank speeches will be in the headlines on Wednesday, giving investors the latest insights into the health of the U.S. recovery and the potential path of monetary policy. Market participants can expect similar insights from the United Kingdom following the release of the Financial Stability Report.

The Bank of England (BOE) will publish its Financial Stability Report at 08:30 GMT. The biannual publication provides an assessment of the financial sector and its ability to withstand external shocks. At the time of its release, BOE Governor Mark Carney is expected to deliver a speech.

BOE officials voted last week to keep monetary policy unchanged, but the breakdown of the verdict suggests that a rate hike could be on the horizon.

In terms of Eurozone data, the Italian government at 10:00 GMT will report on the nation's trade balance for the month of May.

Shifting gears to North America, the US Department of Commerce will report on durable goods orders at 12:30 GMT. Orders for manufactured goods meant to last three years or more are projected to fall 1% in May following a 1.6% drop the month before. Excluding the volatile transportation category, sales are expected to rise 0.5%.

In a separate release, Commerce will report on the national goods trade balance for the month of May. Washington's deficit is forecast to have expanded to $68.9 billion from $67.34 billion the month before.

The National Association of Realtors (NAR) will report on pending home sales at 14:00 GMT. The forward-looking indicator of real estate transactions is forecast to rise 0.5% in May.

A pair of central bank officials are scheduled to deliver public commentary on Wednesday. They include Federal Reserve governor Randal Quarles and Eric Rosengren of the Boston Fed Bank.

EUR/USD

Europe's common currency lost momentum on Tuesday, falling roughly 70 pips against the dollar to reach 1.1650 US. EUR/USD is currently hovering right around that level. Immediate resistance is likely found at 1.1700, followed by the Tuesday high of 1.1720. On the flipside, a breakdown of current levels will expose the pair to the 1.1600 region.

GBP/USD

Cable experienced a similar breakdown to its euro counterpart Tuesday as the dollar regained momentum against a basket of currencies. GBP/USD fell from a high of 1.3291 all the way back down to 1.3204. The pair remains in a downtrend with immediate support located at Tuesday's low.

USD/JPY

It has been a volatile half day for the USD/JPY. The pair jumped to a high of 110.16 Tuesday before reversing course all the way back down to 109.78 at the start of Asian trading on Wednesday. USD/JPY now sits at the lower end of the range, with immediate resistance likely found at the psychological 110.00 level.

China In Focus As President Xi Warns Of Full Scale Trade War, The Yuan Is Devalued

Risk on sentiment returned briefly yesterday as markets retraced some of Monday’s selloff but sentiment in Asia has declined overnight. The PBOC cut the onshore reference rate for the Yuan as trade tensions escalate, in an effort to stay ahead of tariffs and a weakening currency due to trade concerns. The PBOC also said they will seek to reduce holdings of US Treasuries. President Xi warned the country to prepare for a full scale trade war. The Chinese are expecting further escalation from the US after earlier announcements this week that the US would limit foreign investment despite some row back from officials. The Shanghai Composite Index fell into bear market territory, which is a fall of 20% from its high with the Chinese A50 Index down -2.28% to 11471.44.

Oil rallied above $70.00 a barrel yesterday as Private Inventories data showed a bigger than expected draw in stocks. Today’s Inventory data will shed further light on the storage situation in the US with an expected draw of -2.481M expected from -5.914M last week. The USD gained as the tension eased yesterday and it is consolidating those gains for now.

US S&P/Case Schiller Home Price Index (YoY) (Apr) was 6.6% against an expected 6.8% from a prior reading of 6.8%. This measure has been holding a steady improvement since the late 2014 low, with today’s data largely in line with expectations. USDJPY fell from 109.686 to 109.553 as a result of this data.

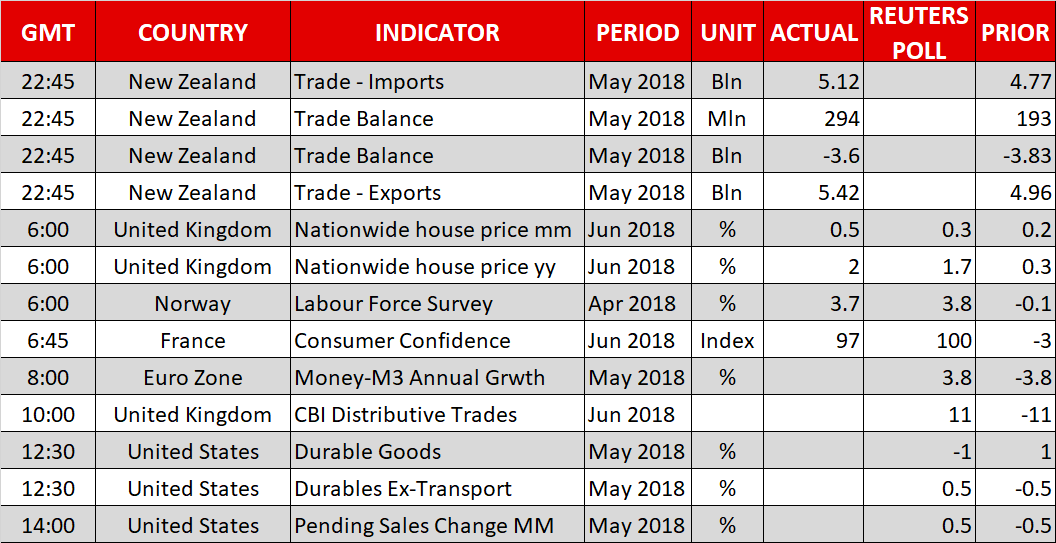

New Zealand Trade Balance (MoM) (May) numbers was released coming in at $294M (MoM) and $-3.60B (YoY) against an expected $100M (MoM) and $-3.74B (YoY) with prior numbers of $-1,193M (MoM) and $-3.76B (YoY) which were $193M (MoM) and $-3.83B (YoY). Imports (May) were $5.12B against an expected $5.10B from $4.79B previously which was revised down to $4.77B. Exports (May) were $5.12B against an expected $5.25B from $5.05B previously which was revised down to $4.96B. This data caused NZDUSD to move up from 0.68497 to 0.68588 before reversing and selling off to 0.68114.

EURUSD is up 0.09% overnight, trading around 1.16563.

USDJPY is down -0.15% in the early session, trading at around 109.848

GBPUSD is up 0.03% this morning trading around 1.32217

Gold is down -0.21% in early morning trading at around $1,256.10

WTI is down -0.16% this morning, trading around $70.24

Major Data Releases For 27 June

At 08:30 GMT, BOE Governor Mark Carney is due to hold a press conference about the Financial Stability Report, in London. The Report will be released at this time along with the FPC Statement. GBP pairs can move in reaction to comments made during this event.

At 12:30 GMT, US Durable Goods Orders ex Transportation (May) are expected to come in at 0.5% from 0.9% previously. Durable Goods Orders (May) is expected at -1.0% against -1.6% previously which was revised up from -1.7%. This data fell under 0% last month and is expected to stay below this mark but come in higher than the previous reading. The ex-transports data is also expected to be lower than the previous reading. This shows a slowing in quantity of orders placed. USD crosses can be moved by this data.

At 14:00 GMT, Pending Home Sales (MoM) (May) is expected to be 0.5% against a prior reading of -1.3%. These data points are expected to rebound after declining to the lowest level in four years In January at -4.7%. The New Year is usually the worst time for US home sales and there was a strong rebound in February. The data is expected to turn back above zero today. USD pairs can move due to this data release.

At 15:00 GMT, US Fed’s Quarles is due to speak about financial regulation at the Utah Bankers Association Annual Convention, in Idaho. USD pairs can be impacted as a result of comments made during this time.

At 20:00 GMT, BOC Governor Poloz is due to deliver a speech titled “Let Me Be Clear: From Transparency to Trust and Understanding” at the Greater Victoria Chamber of Commerce, in British Columbia. Audience questions are expected to follow. Comments made can result in moves in CAD pairs.

At 21:45 GMT, New Zealand Interest Rate Decision will be released and is expected to be left unchanged at 1.75%. The Rate Statement will also be released at the same time. This data can cause a move in the NZD crosses.

Currencies: Technical Trading Prevails In Major Dollar Cross Rates

Rates: Subdued core bond trading

Core bonds treaded water yesterday as risk tensions eased. Mixed US eco data, higher oil prices and comments by Atlanta Fed Bostic failed to inspire directional move. Trading settings remains the same today, suggesting more sideways range-bound action in core bonds.

Currencies: Technical trading prevails in major dollar

cross rates Yesterday, the dollar regained the benefit of the doubt. However, the moves in EUR/USD and USD/JPY were technically insignificant. Today, the eco data will probably only be of intraday significance. So more technical trading might be on the cards if there comes no important news on the trade sage. EUR/GBP is holding near the 0.88 mark

The Sunrise Headlines

- US equity markets got back on their feet after the hit on Monday, with all major indices gaining ground. Asian stock markets opened mixed this morning. Especially Chinese markets go deep in red.

- The renminbi continues to weaken, with USD/CNY passing the 6.6 level the first time since December. The PBoC is expected to want to avoid a '15-'16 scenario, when yuan weakness weighted on financial stability.

- US President Trump has softened his stance in regard to restrictions on Chinese investments in the US. In contrast to a full restriction, he now indicates the Committee on Foreign Investments can retain threats to US security.

- Germany will raise the minimum wage with 4%, following the earlier pay rises in the low-wage economy. The above-inflation increase is part of a two-year proposal and will be ratified by the government in the coming months.

- In New Zealand there was a significant drop in business confidence (39% of companies that are pessimistic, from 27.2% last month), signalling a slowing economy. The New Zealand dollar fell to its lowest level in 2018.

- Chinese Industrial profit growth remained strong with 21.1% (YoY) in May, a bit down from the 21.9% in April, supported by a raise in producer prices that were lifted by an increase in oil prices and metals.

- The Durable Goods Orders are released in the US today. In EMU, M3 Money Supply (YoY) for May is published. In Czech Republic and New Zealand, central banks hold policy meetings deciding on its rates

Currencies: Technical Trading Prevails In Major Dollar Cross Rates

Technical trading prevails in major USD crosses

On Tuesday, EUR/USD failed to extend the rebound from the previous days. The pair tried a lacklustre attempt to stay north of 1.17, but dollar strength soon prevailed again. There was little high profile news to guide trading. US data (Richmond Fed and consumer confidence) were mixed. The risk-off trade due to trade tensions eased, but uncertainty on next developments remains high. EUR/USD closed at 1.1648. USD/JPY also rebounded in US trading to close the day just north of 110.

Overnight, Asian markets show agains a diffuse picture. Most markets are trading little changed. China continues to underperform. The yuan remains also under pressure even as the PBOC set a stronger daily fixing. The USD/JPY (110.00) and EUR/USD (1.1655) show no clear directional trend. Uncertainty on China also continues to weigh on the Aussie dollar (AUD/USD 0.7380). The kiwi dollar felt additional pressure from disappointing confidence indicators (NZD/USD 0.6820).

Today, the EMU money supply data will be published. In the US, the May advance trade balance and the durable goods orders will be published. The US trade deficit is expected to widen from $67.3 bln to 69 bln. Despite the ongoing trade war, the trade deficit data until now had only a limited impact on FX trading. We don't expect that to change in a profound way. Maybe there is a slight asymmetrical risk (more impact of a poor figure). Headline US durable orders are expected to decline for the second month in a row (-1.0% from -1.6% M/M) but core measures (ex-transportation) should paint a more constructive picture. We don't expect today's data to bring a game-changer for FX trading. If there are no important new developments in the trade war sage, more technical trading might be on the cards. Yesterday's price action suggests that any further euro gains are not that evident. The dollar retains the benefit of the doubt. EUR/USD might return lower in the 1.1510/1.1851 ST consolidation pattern. USD/JPY also shows no clear directional momentum at all.

Yesterday, EUR/GBP hovered close to, mostly slightly north of 0.88. In his appointment hearing, new MPC member Haskel warned on the risk of raising rate too early, suggesting he will join the dovish wing in the MPC. Today, the CBI retail data will be published. We don't expect the data to really change the picture in favour of sterling. More sideways trading might be on the cards. The 0.8843 resistance is coming with reach.

EUR/USD: going nowhere as visibility on trade developments stays low

Rising Rates Not Going to Derail Hong Kong Property Market, Weakening Chinese Economy Might

Although Hong Kong dollar (HKD) had approached the weak side (7.85) of the trading band against US dollar (USD) in May and June, after HKMA’s intervention in April, the gap between HIBOR and LIBOR has narrowed significantly since then. Through buying HKD and selling USD, HKMA’s numerous rounds of intervention in mid-April helped withdraw liquidity from the market, causing interbank rates to increase. As a result, the interbank liquidity has shrunk to about HKD 128B on April 23 from HK$ 180B before the intervention. Currently staying at HK$ 109B since mid- May, driven by further capital outflow, the interbank liquidity has been diminished to the lowest level since December 2008. Meanwhile, the 3-month LIBOR has risen almost +100 bps since the intervention. As a result, the HIBOR—LIBOR spread has narrowed to -0.25% as of June 26, compared with about -1.18% before the intervention. One-month HIBOR-LIBOR spread has narrowed more sharply to the level not seen since November 2015.

The questions we are facing now are: 1. Would further withdrawal of liquidity squeeze interest rates sharply higher? 2. The Fed is expected to raise the policy rate for two more times in 2H18. Would the catch-up in Hong Kong rates be so rapid that it leads to a fall in the property market?

The questions we are facing now are: 1. Would further withdrawal of liquidity squeeze interest rates sharply higher? 2. The Fed is expected to raise the policy rate for two more times in 2H18. Would the catch-up in Hong Kong rates be so rapid that it leads to a fall in the property market?

Although interbank liquidity has reached the lowest since December 2008, we have to emphasize that the current liquidity has remained ample by historical standard. Note that during Fed’s previous tightening cycle in 2004-2006, the interbank liquidity was hovering at a range of HK$ 1.3- 55B, or 1- 50% of the current level. Meanwhile, we believe that upcoming mega IPOs would help raise liquidity from the current level. As we mentioned above, HIBORs have soared over the past two months. This has increased the pressure for banks to raise the prime lending rates, which are currently at 5% or 5.25%. Indeed, prime lending rates have not been adjusted since December 2008, although the Fed has increased the policy rate for 7 times. We do not expect such a gradual increase in prime lending rate would roil the property market. We would like to emphasize that, despite recent pickup, the real rates in Hong Kong remain very low (about 0%), due to the improvement in inflation. Meanwhile, investors are relaxed that the rapid increase in property prices would more than offset the increase in interest costs.

There are comments that the current interest rate situation in Hong Kong is similar to the Fed’s previous tightening cycle during the period of 2004-2006. We would like to point out that the pace of increase rate increase is far slow than that time, when the Fed had hiked the policy rate by 425 bps. The Fed has to double the pace of rate hike if it wants to repeat the policy cycle back then. Yet, if history serves as a guide, it is noted that property price had risen for 3 more years after the first prime rate hike in 2005. We are not concerned that further interest rate increases would lead to a collapse in Hong Kong property prices. However, the downside risk to the property sector is the rapid slowdown in Chinese economy. The situation is aggravated by the heightening of US-China trade conflict and China’s elevated debts.