Sample Category Title

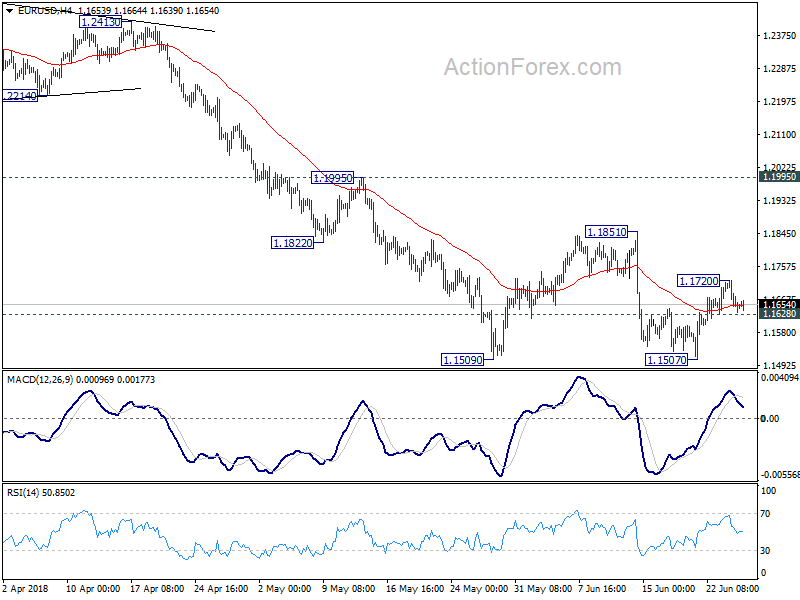

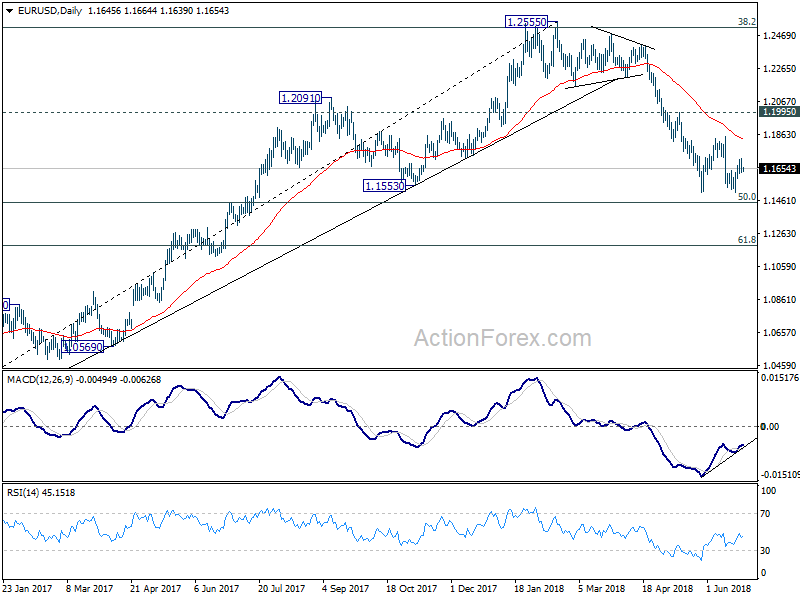

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1616; (P) 1.1668 (R1) 1.1702; More.....

Intraday bias in EUR/USD remains neutral for the moment. In case the rebound from 1.1507 extends, upside should be limited by 1.1851 resistance to bring fall resumption eventually. On the downside, below 1.1628 will bring retest of 1.1507 first. Break will resume the whole fall from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

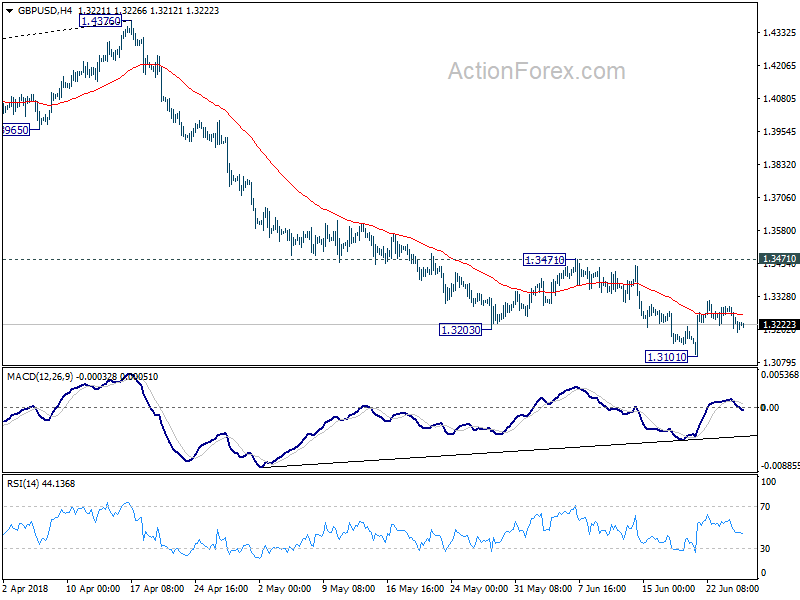

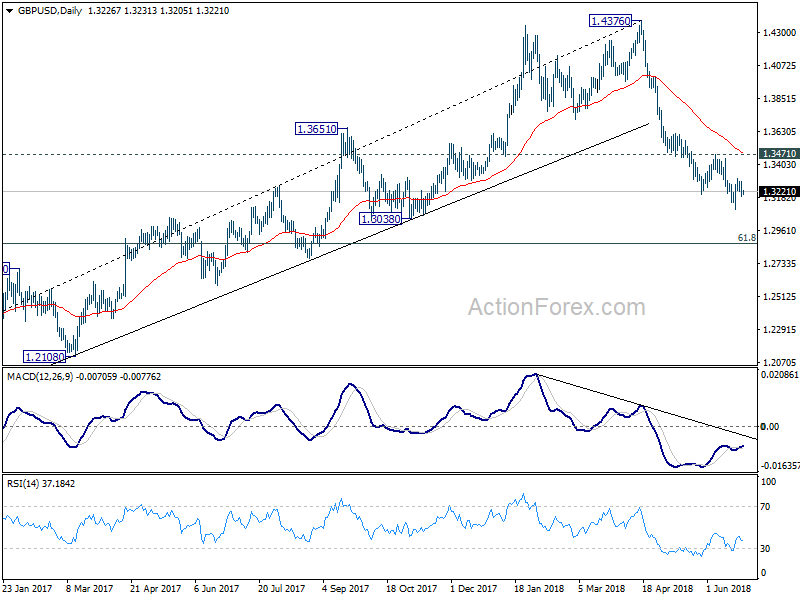

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3176; (P) 1.3240; (R1) 1.3287; More...

Intraday bias in GBP/USD remains neutral at this point. Correction from 1.3101 could extend with another rise. But we'd expect strong resistance from 1.3471 to limit upside. On the downside, break of 1.3101 will resume fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3490) holds, even in case of strong rebound.

China Beige Book Positive On The Economy

General Trend:

- Asian equity markets trade mixed

- Property shares in China and Hong Kong extend losses

- China Commerce Ministry responds to speculated investment restrictions by the US

- New Zealand May trade surplus above ests, lamb exports hit record high

- New Zealand June business confidence declines, Kiwi (NZD) hits 2018 low

- RBNZ due to hold policy decision on Thursday

- Chinese yuan (CNY) declines for 10th straight session

- Offshore yuan (CNH) declines past 6.60/USD for first time since Dec 2017 , and -6% from March highs

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%

- TOPIX Marine Transportation index -1.1%, Real Estate -0.7%, Iron & Steel -0.5%; Retail Trade +0.8%, Info & Communications +0.7%

- (JP) BoJ Q1 Flow of Funds Report: Central bank held 41.8% of the JGB market as of the end of March v 41.1% q/q

- (JP) BOJ Dep Gov Amamiya: paying close attention to the downside of stimulus, not ruling out the possibility of policy adjustments if circumstances warrant

- (JP) Fitch Report: Pace of asset purchases by Bank of Japan (BoJ) has continued to slow sharply in 2018 to an annual rate of ~¥45T ($410B)

- (JP) Japan Fin Min Aso: Cautious about changing how capital gains on cryptocurrencies is taxed - press

Korea

- Kospi opened -0.1%

- (KR) Experts on North Korea shared views that overheated expectations of inter-Korean economic cooperation should be moderated, as companies may have to wait a long time before seeing the benefits of economic ties - Korean press

China/Hong Kong

- Hang Seng opened +0.3%, Shanghai Composite -0.1%

- Hang Seng Property/Construction index -2.1%, Materials -1.9%, Financials -0.9%, Consumer Goods -0.6%; Energy +1.8%

- Shanghai Property index extends losses, drops over 1.5%

- (CN) China President Xi: Warned leaders to be ready for a full scale trade war with the US; also noted PBOC will refrain from buying US treasuries and will seek to reduce them "appropriately" - press citing Xi in meeting with other leaders - ZeroHedge

- (CN) China researcher urging more proactive fiscal policy in H2 - China Daily

- (CN) China looking at rules that could curb implicit debt - Chinese press

- (CN) China insurance regulator CIRC said to increase on-site checks of insurance companies - China Securities News

- (CN) China Beige Book: Economy is doing better than official data shows

- (US) President Trump has suggested he would not go ahead with new curbs on investment from China in the US and instead rely mainly on existing tools – press

- 763.HK US Senators said to be considering trading restrictions for lifting ban on ZTE – SCMP

- (CN) China removes imports tariffs on soybean imports from India, South Korea, Bangladesh, Laos and Sri Lanka from the prior 3%

- (CN) China Global Times calls on Govt to increase efforts to support industries affected by US tariffs, including subsidies

- (CN) China PBoC Open Market Operation (OMO): Injects CNY60B in 7-day reverse repos v injects CNY80B in 7-day reverse repos prior; Net: drains CNY150B v CNY90B drains prior

- (CN) China PBoC sets yuan reference rate at 6.5569 v 6.5180 prior

- (CN) China May Industrial Profits y/y: 21.1% v 21.9% prior

- (CN) China Commerce Ministry (MOFCOM) Notices US possible restriction measures on investment, will closely watch possible measures

- (HK) According to Nomura, mortgage rates may be increased in Hong Kong amid rising domestic interest rates - US financial press

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 Energy index +1.3%, Consumer Discretionary +1%, Resources +1%; Telecom -1.3%, Financials -0.2%

- (NZ) NEW ZEALAND MAY TRADE BALANCE (NZ$): +294M V +100ME; 12-MONTH YTD: -3.59B V -3.74BE

- (AU) Australia May YTD underlying cash deficit A$10.0B v A$14.9B prior

- (NZ) RBNZ to defer bank liquidity policy review after priority rethink

- (NZ) New Zealand Jun ANZ Activity Outlook: 9.4 v 13.6 prior; Confidence: -39.0 v -27.2 prior

- (AU) Australia sells A$1.0B v A$1.0B indicated in 2.50% May 21 2030 bonds, avg yield 2.7083% v 0.7029% prior, bid to cover 3.48x v 3.36x

- (AU) Australia Stats Bureau said to examine the whether it is feasible to issue monthly CPI reports

Other Asia

- Philippine Peso (PHP) hits lowest level since 2006; Government official denied Presidential interference regarding central bank

North America

- US equity market ended higher: Dow +0.1%, S&P500 +0.2%, Nasdaq +0.4%, Russell 2000 +0.7%

- S&P500 Energy +1.3%, Consumer Discretionary +0.7%

- (US) Weekly API Oil Inventories: Crude: -9.2M v -3M prior

- (US) S&P affirms United States sovereign rating at AA+: Outlook stable

- (US) US Trade Rep Lighthizer: Retaliatory tariffs show trading hypocrisy, US will take all necessary actions to protect its interests

Europe

- (UK) UK Chancellor Hammond: Hopes UK can seize unlimited opportunities brought by China Belt and Road Initiative - Chinese Press

- (DE) CDU's Kauder (Merkel ally): Agreement on migrant policy between German coalition parties was not expected in talks Tues night; migration disagreement will not hinder coalition work

Levels as of 01:30ET

- Hang Seng -0.9%; Shanghai Composite -1.0%; Kospi +0.0%; Nikkei225 -0.2%; ASX 200 +0.1%

- Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax +0.0%; FTSE100 +0.0%

- EUR 1.1640-1.1664; JPY 109.37-110.20; AUD 0.7361-0.7398;NZD 0.6812-0.6866

- Aug Gold -0.3% at $1,256/oz; Aug Crude Oil +0.3% at $70.72/brl; Sept Copper -0.6% at $2.99/lb

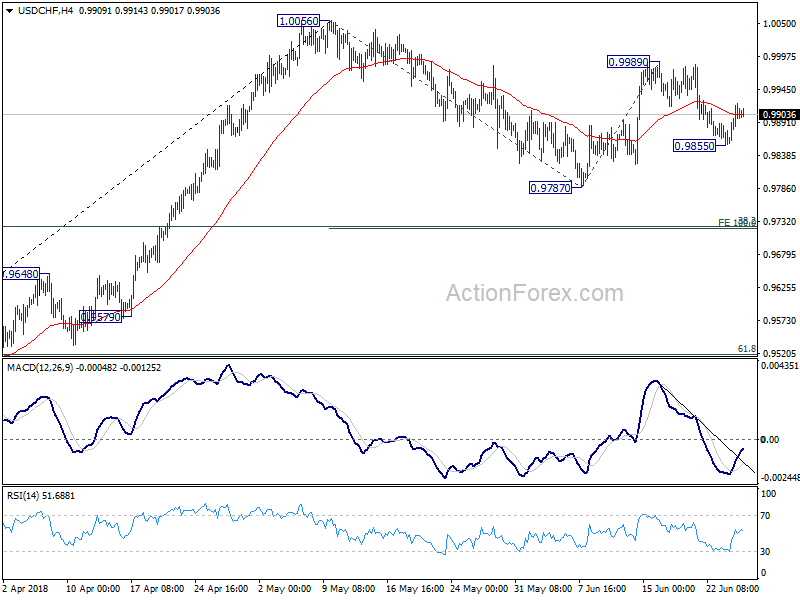

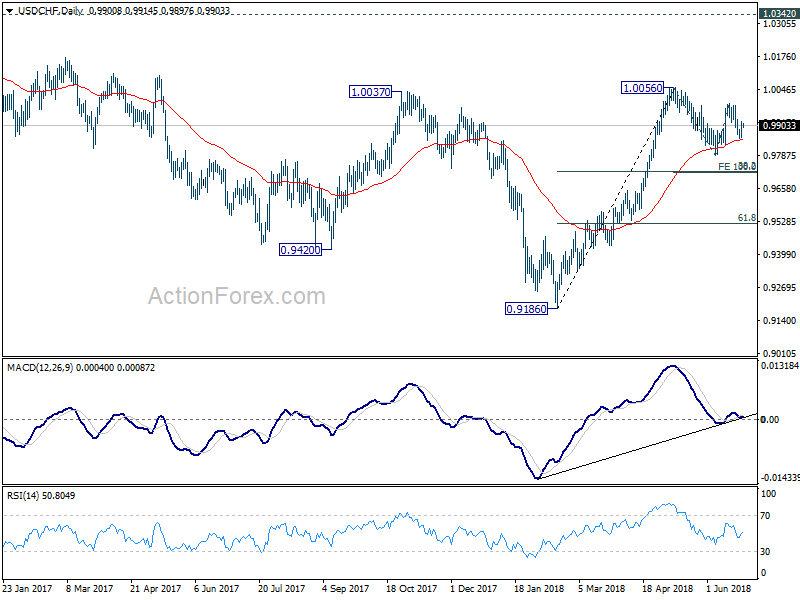

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9868; (P) 0.9896; (R1) 0.9933; More...

Intraday bias in USD/CHF remains neutral for the moment. The consolidation pattern from 1.0056 could extend with another fall. Below 0.9855 will target 0.9787 support and below. But we'd expect strong support from 0.9720/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9989 at 0.9720) to bring rebound. On the upside, above 0.9989 will bring retest of 1.0056 high first.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

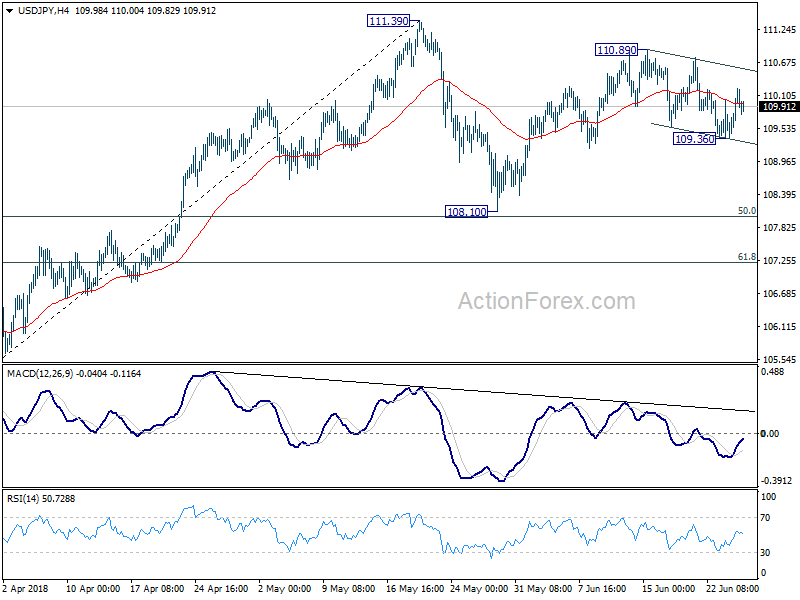

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.39; (P) 109.74; (R1) 110.11; More...

Intraday bias in USD/JPY is turned neutral with the current recovery. On the downside, below 109.36 will resume the fall from 110.89 to 108.10 and possibly below. But as price actions from 111.39 are seen as a corrective pattern, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will resume the rise from 108.10 towards 111.39.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

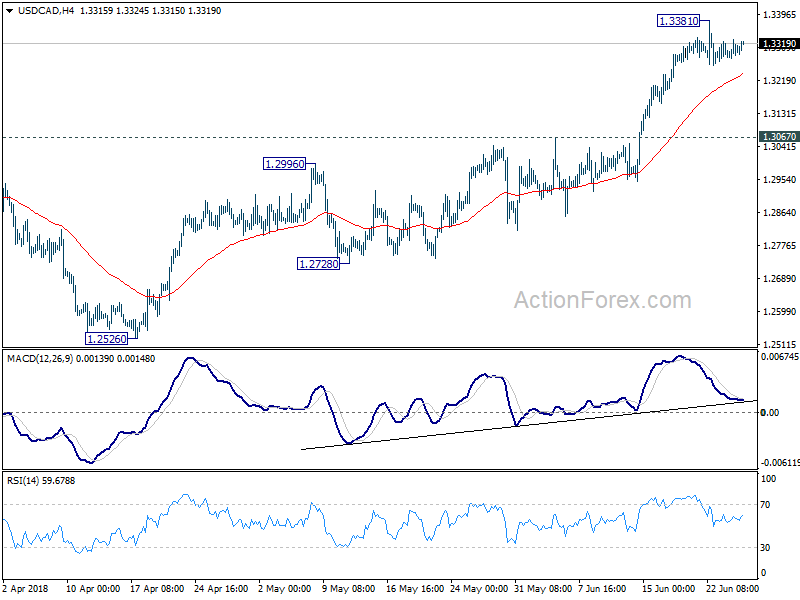

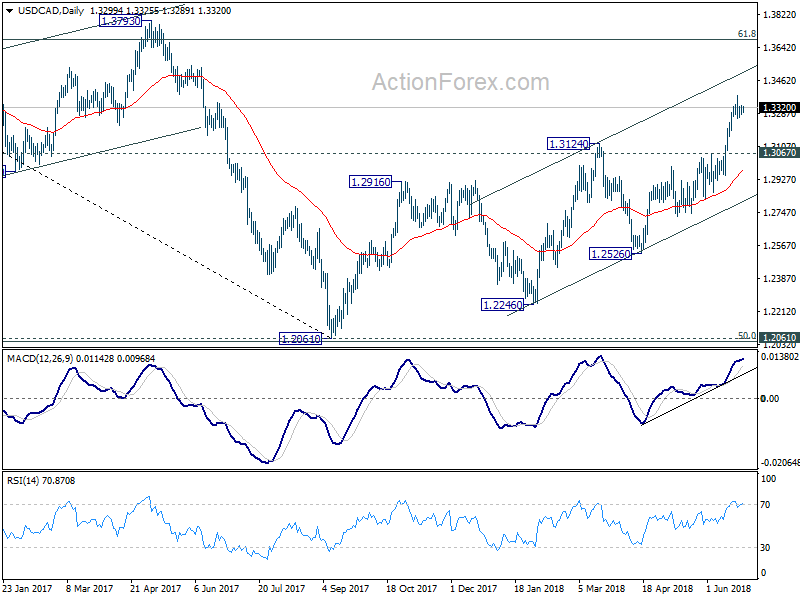

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3272; (P) 1.3304; (R1) 1.3334; More...

Intraday bias in USD/CAD remains neutral for consolidation below 1.3381. Deeper pull back cannot be ruled out. But downside should be contained above 1.3067 resistance turned support to bring rise resumption. On the upside, break of 1.3381 will resume recent rally for 1.3685 medium term fibonacci level next.

In the bigger picture, current development solidify the view of bullish trend reversal. That is fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. This will now be the preferred case as long as 1.2916 resistance turned support holds, even in case of deep pull back.

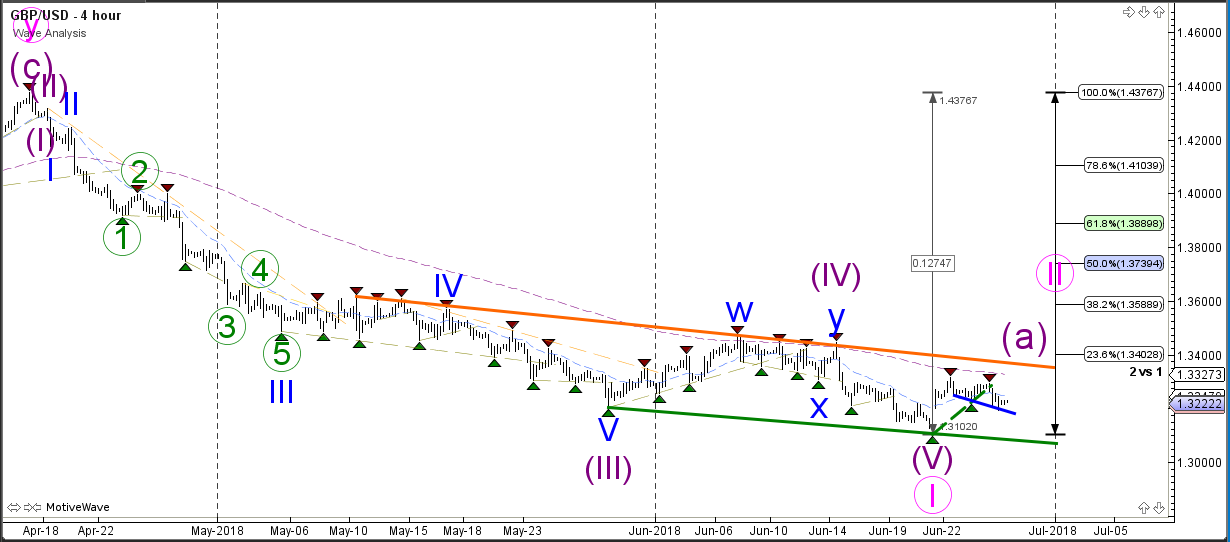

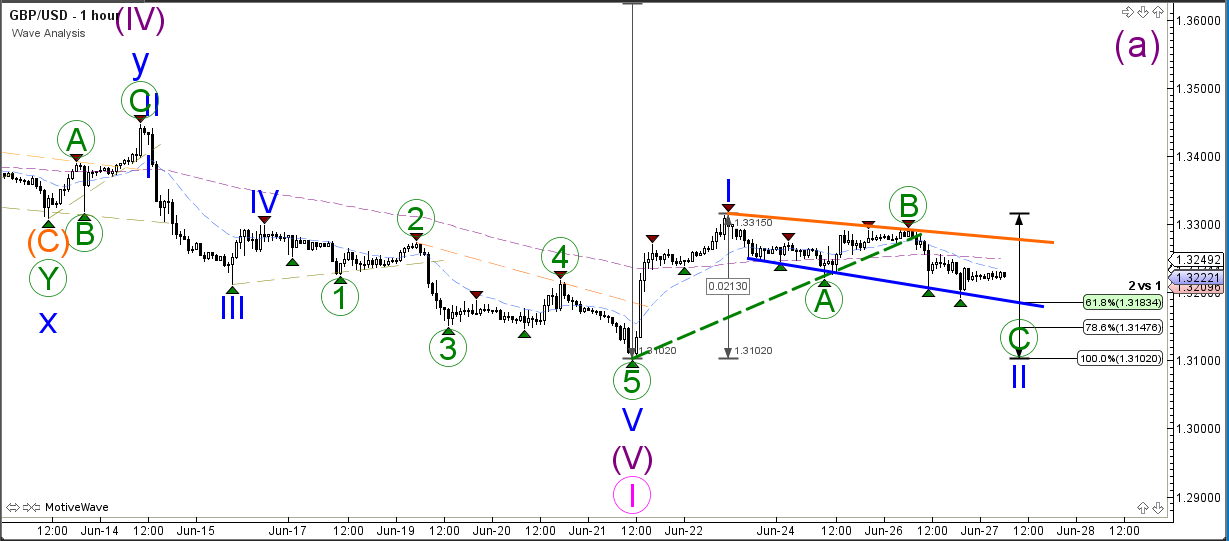

GBP/USD Challenges 61.8% Support Fib After ABC Correction

The GBP/USD remains in a downtrend channel but the bearish momentum is weakening. Price is in a difficult spot because both the bullish correction and downtrend continuation are equally likely. That said, the wave count is favouring a larger corrective zone back towards the Fibs of wave 2 (pink).

The GBP/USD seems to be building a bearish ABC correction (green), which has respected and stopped at the 61.8% Fibonacci level of wave 2. This wave pattern is invalidated if price breaks below the 100% Fib. Price could move up higher as part of a wave 3 or wave C if price breaks above the resistance trend line (orange).

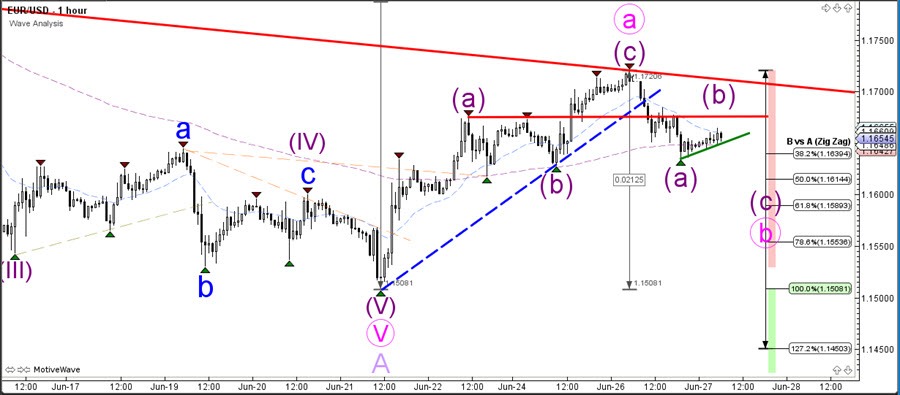

EUR/USD Bearish ABC Aims At 1.16 Support Zone

The EUR/USD broke below the support trend line (dotted blue) but overall price action remains choppy and indecisive. Furthermore, strong support and resistance levels could place a limit on any breakouts.

The EUR/USD could breakout to both directions but the wave count favours a larger bullish correction at the moment within wave B (purple).

USD/JPY Prepares Ascending Wedge Chart Pattern

The USD/JPY remains stuck in a large consolidation zone. A break above the resistance or below the support trend lines is needed before a larger breakout is likely.

The USD/JPY seems to have completed a wave C (blue) correction but price needs to break the triangle pattern (red/blue lines) before a new uptrend is possible.

The USD/JPY broke the resistance trend line (dotted orange) of the falling wedge chart pattern. It is now building an ascending wedge chart pattern. The trend lines are key and offer bounce and breakout spots but for the moment a bullish ABC seems slightly more likely.

The Latest News In The Trade Came From Canada Yesterday

Market movers today

We have another quiet day on the data front and instead the market will look for any new political statements in the trade dispute between the US and its major trading partners, the EU and China.

The only real important economic number is the preliminary core capex figures in the US. Overall, business investments have been increasing since summer 2016 but recently, they have stagnated - probably due to lower growth in the manufacturing sector. Figures for May will give us an impression of whether investments are heading higher again.

Selected market news

The latest news in the trade came from Canada yesterday, which is preparing to introduce tariffs and quotas on steel imports. The new measures should prevent global steel producers from dumping excess supply hit by US tariffs on the Canadian market.

S&P yesterday affirmed the US sovereign credit rating of AA+ and kept the outlook on stable. The rating further assumed that long-term fiscal challenges will be addressed over time.

The oil market traded on a series of supply-related stories yesterday. News out of Libya 6 that the militia has taken control of large oil ports threatening exports from Libya 6 initially pushed oil prices higher. Later in the day, Saudi Arabia was said to plan to boost oil output to a record high 10.8mb/d following the OPEC+ deal from last week. The news temporarily eased concerns over the potential supply risk from Libya and sent oil prices back down again before news broke that the US is pressing its allies to cut Iran oil imports to zero by November. If the US succeeds in the latter, it will tighten world oil supply and push prices higher.

In Denmark, the Systemic Risk Council yesterday recommended that the countercyclical buffer rate was kept unchanged at 0.5%. Due to the build-up of economic and financial risks the Council, however, said it expects to issue a recommendation during 2018 to raise the buffer rate by a minimum of 0.5 percentage point.