Sample Category Title

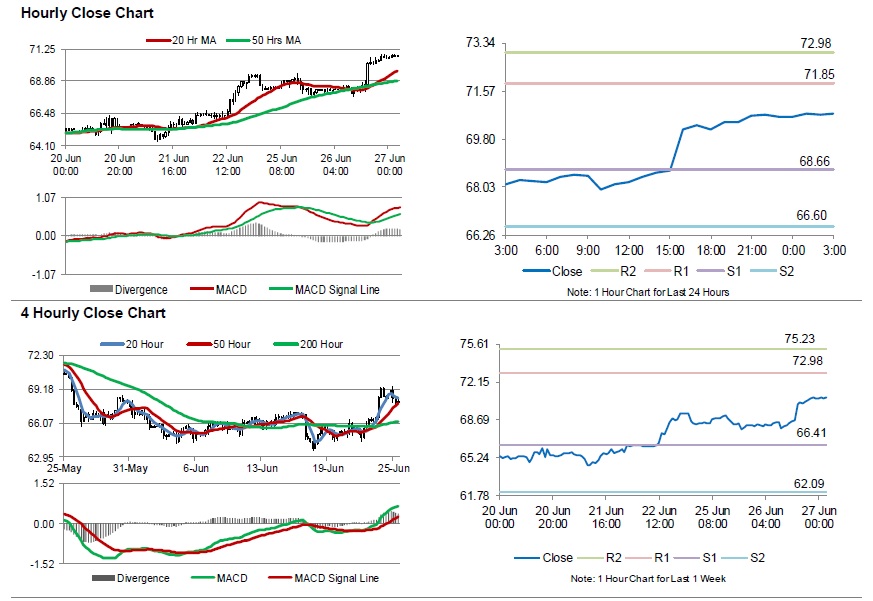

Crude Oil: Oil Trading Higher, Ahead Of EIA’s Weekly Crude Oil Stockpiles Data

For the 24 hours to 23:00 GMT, Crude Oil rose 3.55% against the USD and closed at USD70.62 per barrel, amid news that the US demanded all countries cut imports of Iranian oil to zero by November. Moreover, the American Petroleum Institute (API) reported that US crude oil inventories fell 9.2 million barrels to 421.4 million barrels in the week ended 22 June.

In the Asian session, at GMT0300, the pair is trading at 70.73, with oil trading 0.16% higher against the USD from yesterday's close.

The pair is expected to find support at 68.66, and a fall through could take it to the next support level of 66.60. The pair is expected to find its first resistance at 71.85, and a rise through could take it to the next resistance level of 72.98.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

New Zealand business confidence deteriorated, trade surplus widened

New Zealand ANZ Business Confidence deteriorated again in June and dropped to -39.0, down from -27.2. The Own Activity index also dropped from 14 to 9. ANZ noted in the release that the GDP growth growth indicator remained expansionary but "the economy may continue gently losing steam over coming months, despite the support coming from fiscal stimulus and high commodity prices."

And, "tailwinds in the form of fiscal stimulus and strong terms of trade will see the economy continue to grow at about par. However, cost, credit and capacity headwinds have strengthened, and firms have noticed."

New Zealand trade surplus widened to NZD 294m in May, beat expectation of NZD 100m. Goods exports rose 10% to NZD 5.4B, hitting a new high for total exports in a May month, and the second largest for any month. Goods imports rose 5.7% to 5.1B, also a new high for total imports in a May month.

BoJ Amamiya: Don’t change public perceptions with a shock blow

BoJ Deputy Governor Masayoshi Amamiya said Japan is having "steady progress" towards 2% inflation even though that could take time. And he emphasized that "instead of trying to change public perceptions with a shock blow, we should guide inflation toward our target through steady improvements in the output gap and inflation expectations."

He added that BoJ will "scrutinise factors that are preventing inflation from accelerating" and "look very carefully into what is happening." He doesn't rule out fine-tuning of the ultra-loose monetary policy and "an adjustment could happen if that's necessary to stably achieve our price target.

USTR Lighthizer on EU’s complete hypocrisy and distortion of WTO rules

US Trade Representative Robert Lighthizer condemns retaliatory tariffs from EU and other WTO members in a statement released overnight. He claimed that the US actions on steel and aluminum tariffs were "wholly legitimate and fully justified". But the EU has concocted a groundless legal theory to justify immediate tariffs on U.S. exports.

Lighthizer went further to say that "these retaliatory tariffs underscore the complete hypocrisy that governs so much of the global trading system." According to him, the EU and others claimed to champion the WTO but "their recent tariffs prove that they simply ignore WTO rules whenever doing so is convenient."

Also, "when the EU and others falsely assert the U.S. steel and aluminum duties are safeguard measures, and impose retaliatory duties under this pretense, they do great damage to the multilateral trading system. Indeed, they show that they are willing to distort WTO rules to mean whatever they want, whenever they want."

In short, the US is ready to go for auto tariffs.

Dallas Fed Kaplan: Let’s fight the big threat China, not others

Dallas Fed President Robert Kaplan trade with Canada and Mexico boosts US employment and competitiveness. And he warned that the US risks losing such competitiveness as the trade spat continues. He emphasized that the real threats come from China. Kaplan noted that "intellectual property rights and technology transfer are very big issues, where China is using the joint ventures to get technology and then compete globally" And, "let's fight what I think is actually a very big threat, which is the relationship with China."

Regarding monetary policy, he reiterated the view that neutral rate is between 2.50-2.75%. And Fed is "still accommodative" at the current 1.75-2.00%. Kaplan also felt reluctant to dismiss the yield curve signal on recession as it reflections expectations of future growth. Flattening yield curve can also affect behavior of businessmen.

Market Morning Briefing: Euro Yen Is Respecting Support Near 127.5

STOCKS

Almost all stock indices look bearish for the near term and may continue to trade sideways or dip a bit in the coming sessions.

Dow (24283.11, +0.12%) moved up slightly but is overall stable for now. Crucial support to watch are 24000 and lower at 23600 which if hold may bring in another fresh up move in the medium term; else the index could continue to remain bearish for at least the next 5-6 weeks.

Dax (12234.34, -0.29%) dipped further yesterday and is indicative of a fall towards 12000 in the near term. View is bearish for this week and the next with little chances of seeing a sharp bounce to higher levels.

Nikkei (22225.44, -0.52%) was almost stable with no major movement. 21800 on the downside looks possible in the coming sessions before a bounce from there is seen.

Shanghai (2849.65, +0.18%) is also somewhat stable without any major movement just now. Chances of gradually testing 2750 on the downside is possible in the medium term.

Sensex (35490.04, +0.056%) and Nifty (10769.15, +0.062%) may look bullish only as long as they trade above 35250 and 10650 respectively. Narrow and small movements just now does not give much clarity on further direction.

COMMODITIES

Crude prices have risen sharply. Brent (76.53) and WTI (70.74) moved up sharply and may continue to rise towards 80 and 72 respectively from where a short dip is possible. Near term looks bullish.

Gold (1256.40) has dipped in line with our expectations and may test 1240 on the downside before stopping there. Near term looks bearish.

Copper (2.9780) has important support near 2.90/95 region which could possibly push back the price to above 3.0 in the near term.

FOREX

Euro (1.1655) : As per our expectation, Euro came down from just below the 1.1720-50 Resistance region yesterday. It could see a break below support near 1.1650-30 in this week, which would make it very bearish. In case it moves up again from here and breaks past 1.1750, it could be headed up towards 1.185 (previous high).

Dollar Index (94.62): As we had expected, support for Dollar Index near 94.1-94.2 held well yesterday and it is now bouncing again towards previous highs near 95.0-95.5. A break below 1.15 for the Euro in the next 1-2 weeks should correspond with a breach above 95.5 for Dollar Index.

Dollar Yen (109.94): Contrary to our expectation, Dollar Yen rose towards 110 once again, thereby negating it's previous break of support on daily candles. Maybe a final test of levels near 110.50-110.75 is due before it becomes decisively bearish.

Euro Yen (128.14): Euro Yen is respecting support near 127.5 on daily candles and resistance near 129.5-130.0. With Dollar Yen looking like it could rise to test 110.50-110.75 in the next few sessions, a break below 1.15 (Euro) would be required for Euro Yen to break below 127.5.

Pound (1.3226): Pound is trading exactly midway in the downward channel on daily and 3 day candles. There are equal chances of it moving up to test resistance near 1.335 or moving lower towards 1.31. It's target for the next 1-2 weeks could be horizontal support near 1.30 on weekly candles.

Dollar Rupee (68.245):Dollar Rupee could possibly open with a gap up today near 68.35/40 with some possibility of testing 68.50 on the upside. Note that 68.50 is an important level and we do not expect a break above this just now. Rather it could come off from 68.50 to again test levels near 68.30-25 by early next week.

INTEREST RATES

There seems to be no let up in the prevailing risk aversion sentiment as investors seem to be moving away from risky assets towards safer govt bonds, thereby keeping yields low.

US 10 year (2.88%), 30 Year (3.03%), 5 Year (2.75%), 2 Year (2.53%): US yields continue to remain stable around levels seen yesterday.

Repeating yesterday's view for the US 10 Year and 30 Year bond yields for the weeks ahead:

Having broken support on medium term chart near 2.9%, the target for the 10 year yield in July could be lower support near 2.65%-2.70%.

Similarly, the 30 Year yield’s break of support near 3.05% on short term chart could be the beginning of a downtrend towards 2.9%.

Atlanta Fed Bostic could move away from four hikes as trade spat worsens

While Fed is projecting four rate hikes in total this year, Atlanta Fed President Raphael Bostic said there is "some likelihood I will be moving away from four as a real possibility" due to the development of US trade policy. He commented on the "progresses the way it has been the last couple of days" regarding the trade threats of Trump's administration to trading partners. And Bostic noted that "the more it progresses in this more contentious way, the more it leads me to feel the risks are on the downside for the broader economy."

He added that "the disruption that comes from this type of trade war is not going to be good for the cost basis for businesses and it makes me a bit concerned how robust the economy will perform moving forward."

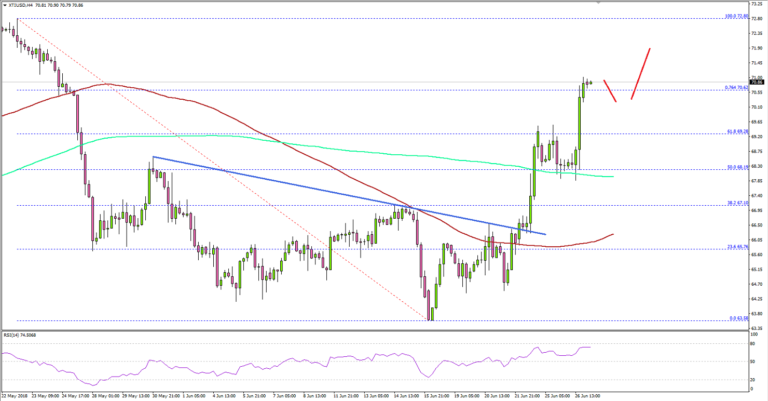

Can Crude Oil Price Trade Above $72?

Key Highlights

- Crude oil price stated a fresh upside wave from the $63.50 support area against the US dollar.

- There was a break above a key bearish trend line with resistance at $66.00 on the 4-hours chart of XTI/USD.

- The US S&P/Case-Shiller Home Price Indices in April 2018 increased 6.6%, less than the forecast of 6.8%.

- Today in the US, the Pending Home Sales for May 2018 will be released, which is forecasted to increase by 0.5% (MoM).

Crude Oil Price Technical Analysis

After trading below the $65.00 support, crude oil price found buyers around $63.50 against the US Dollar. The price traded as low as $63.58 and later it started an upside correction.

Looking at the 4-hours chart of XTI/USD, the price moved above the $65.00 resistance and broke the 23.6% Fib retracement level of the last decline from the $72.80 high to $63.58 low.

More importantly, there was a break above a key bearish trend line with resistance at $66.00 on the 4-hours chart of XTI/USD. The price climbed above the $68.00 level and the 100 (red) and 200 (green) simple moving averages (4-hours).

However, the upside move was slightly capped by the 76.4% Fib retracement level of the last decline from the $72.80 high to $63.58 low. The price is currently consolidating above the $70.00 support.

On the upside, the price must break the $72.00 resistance to gain traction. Above $72.00, the price may revisit the $75.00 zone. A failure to climb above $71.00 and $72.00 may perhaps result in a bearish reaction back towards $68.00.

Recently in the US, the S&P/Case-Shiller Home Price Indices figure for April 2018 was released by the Standard & Poor’s. The market was looking for a rise of 6.8% in April 2018 compared with the same month a year ago.

However, the actual result was below the market forecast since there was a change of 6.6%. Moreover, the last reading was revised down from 6.8% to 6.7%. There was no major impact on the US Dollar, but pairs like EUR/USD and GBP/USD still remains supported on the downside.

Economic Releases to Watch Today

- US Durable Goods Orders for May 2018 – Forecast -1.0% versus -1.6% previous.

- US Pending Home Sales for May 2018 (MoM) – Forecast +0.5%, versus -1.3% previous.

- US Wholesale Inventories for May 2018 (preliminary) – Forecast +0.2%, versus +0.1% previous.

Apple Pie And Harley Davidson

Apple pie and Harley Davidson

US equity markets are slightly higher as Trade worries subsided despite a volley of tweets from President Trump threatening Harley Davidson’s with import taxes on any motorbikes built in Thailand. And the US dollar reasserted itself as the dollar bulls ran wild in the china shop overnight. While oil prices soared after State Department official indicated the US has no plan to issue oil waivers under Iran sanctions and calling for allies to cut Iran imports to zero tolerance. But without the oil gusher, markets would have closed lower as investors sentiment continues to wane as trade wars continue to percolate.

The only thing I can think of that is more iconic Americana than apple pie is Harley Davidson. So, after the President recent twitter trade tirade directed at the iconic motorcycle manufacturer, it cements the view that friend or foe, no one is safe from the wrath of the US administrations America first trade policy.

Equity markets are finding themselves in a real quandary. The US economy is healthy as it stands and earnings are significant, but investors are caught between a hammer and anvil on escalating trade wars. But one thing that is very consistent is the FANG performance as any trade induced thrashings gets quickly faded. Netflix aside which is dealing with internal issues, Apple was back on the move after bargain hunters snap up tech shares on masse.

Oil Market

Oil prices were flying higher overnight after catching an updraft from the US administration calling for allies to cut Iran imports to zero tolerance. While this shouldn’t be considered a huge surprise, the confirmation was enough to send prices surging.

But prices were firming after reports of a Libyan dispute over the control of oil production between the internationally recognised National Oil Corp. based in Tripoli and the competing National Oil Corp. based in Benghazi after Libya National Army militia leader Khalifa Haftar handed control to the Benghazi based organisation on Monday. Based on recent history, Lybia will continue to be a significant point of concern in the oil supply chain.

And the market continues to focus on Syncrude Canada where 350,000 bpd remain in limbo after a transformer blew and shut a critical oil sands upgrader on June 20. Still in damage assessment mode but it looks like the end of July estimate for repairs. This closure should lead to increased shortages in the North American supply and deplete vital inventory supplies in Cushing. And helping this view along nicely, API reports a major crude draw 9.228 million barrels of the United States crude oil inventories for the week ending June 22, well above analysts’ expectations.

Gold Market

All that glitter is indeed not gold, but rather the US dollar is the shining star. The stronger dollar continues to assert its presence as one of the primary safety nets as trade ware percolate. A stronger dollar coupled with relatively stable US equity markets overnight gold hedgers and long-term speculators pull off the bid as gold continues to melt lower. While trading off intraday lows speculators should continue selling into rallies with the break of the key 1261 has speculators now peeking the December lows of 1236.25

Currency Market

The China currency bears have finally woken from hibernation as deteriorating US-China trade relations, and concerns about China economy has untethered the dollar bulls who ran wild in the china shop overnight. And indeed, driving the broader dollar sentiment not only in Asia FX but G-10. If Yuan weakness continues, the spillover effects into the ASEAN basket could be a massive case for concern as there are hugely significant breakouts on EURCNH and CNHJPY. The big question remains with the SHCOMP down 20% Year to date and US-China economies diverging, will the markets get a more dovish response from the Pboc. But with no protests from the Pboc who are letting the market forces dictate the pace of play. Which get 2 thumbs up from this trader!

With the CNH and Gold trading at current levels, I can’t help but think the dollar should be trading at firmer levels however we still have the month end rebalancing act to get through so this will add to a bit of uncertainty into the decision matrix.

EUR: Political risk and negative EUR differentials to the USD should see the EURO move lower after a technical correction of sorts. But short EURJPY should be the best expression to capture escalating global trade war.

AUD: USDCNH, the domestic housing storyline, dovish RBA and economic slowdown in China suggest much lower levels to come. Positioning should be much cleaner after the technical correction last Friday which should see AUD test the .7350 standard sooner rather than later

MYR: With the USDCNH breaching fresh highs triggering waves stop losses Not too unexpectedly the USMYR is trading higher in sympathy with the Yuan weakness, but certainly higher WTI prices are buttressing a great deal of this negativity. But getting little support from foreign interest who are looking for a more significant fire sale, and with local markets under tremendous stress from capital outflow and the prospect of escalating trade war, indeed the path of least resistance appears higher with the next key focus on 4.05 USDMYR.

Eco Data 6/27/18

[php_everywhere instance="1"]