Sample Category Title

Forex Analysis: USDJPY And AUDJPY

The Japanese Yen (JPY) could strengthen as trade related uncertainty has created risk aversion in global markets. The uncertainty is caused by the Trump administration sending mixed signals regarding foreign investment in American companies. First the US Treasury Secretary Steven Mnuchin stated that a “Statement will be out not specific to China, but to all countries that are trying to steal our technology”. Then later on Monday, Peter Novarro tried to downplay the remarks in an interview on CNBC saying that the market is overreacting. With little in the way of economic or political developments in Japan, the JPY is trading in relation to risk appetite. During risk off, the JPY tends to strengthen given its safe haven characteristics.

USDJPY

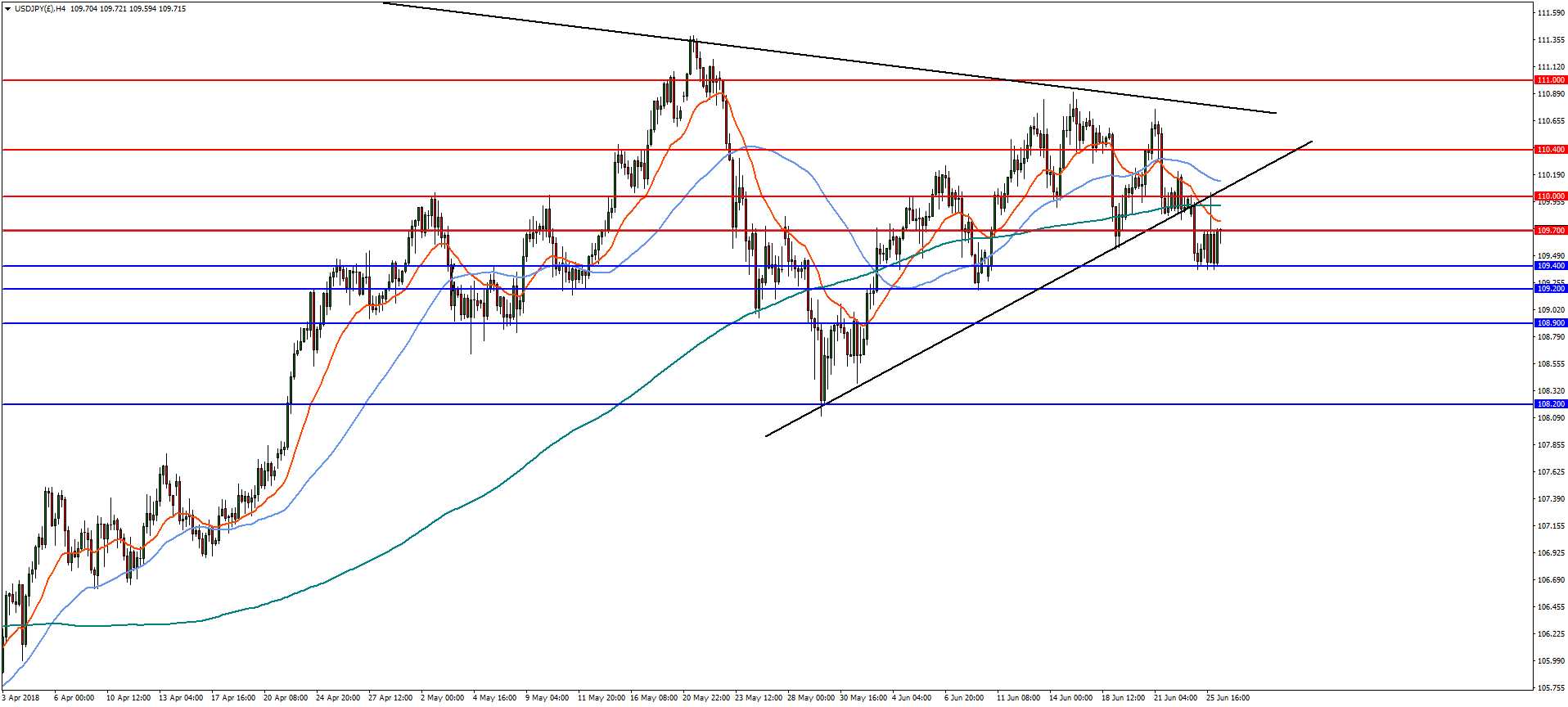

On the 4-hourly chart USDJPY failed to break the December 2017 resistance trend line and appears to be moving lower after breaking below the support trend line at 110.00. The pair needs to break near term support at 109.40 to continue to the downside with further support near the 61.8% retracement at 109.20 and then 108.90. However, a reversal above 109.70 will find horizontal and trend line resistance at 110.00.

AUDJPY

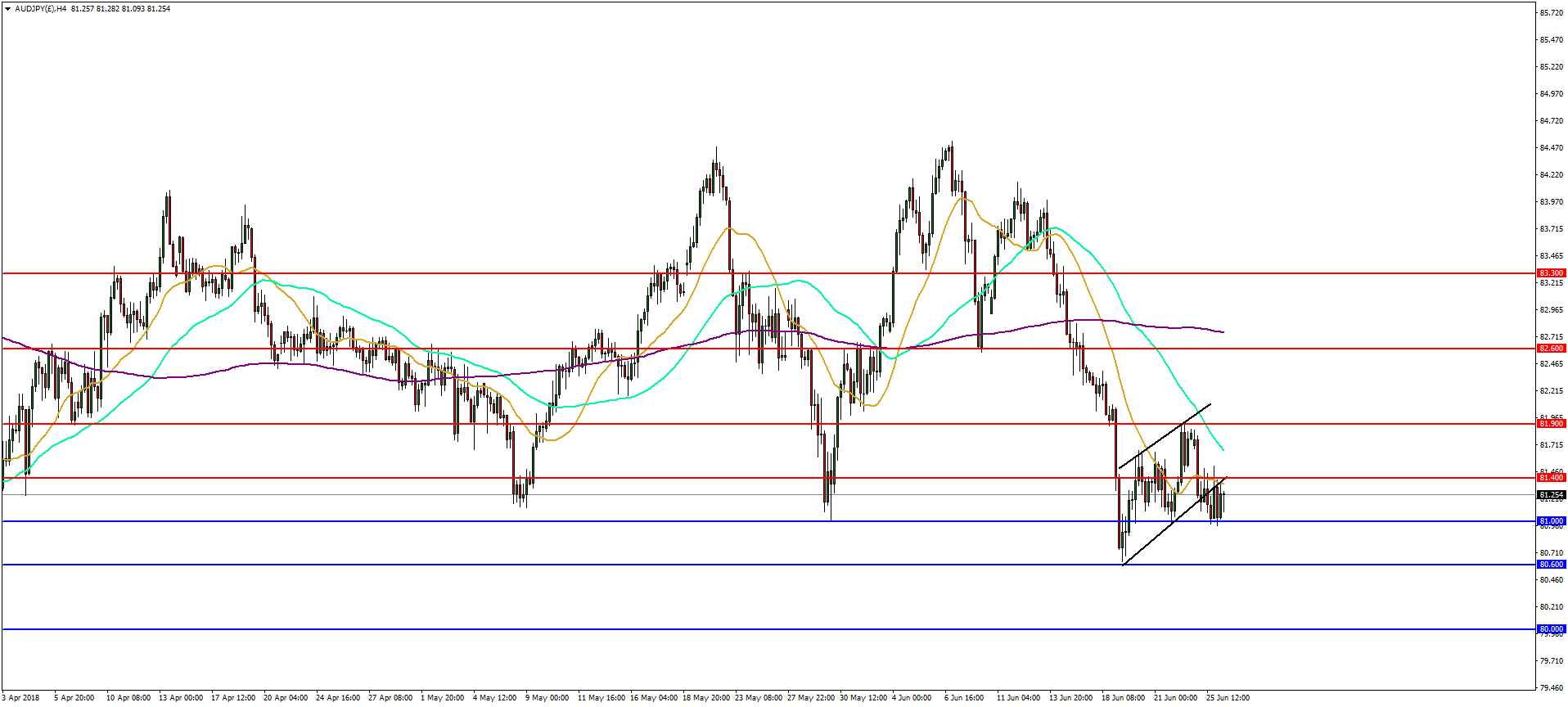

In the 4-hourly timeframe, the AUDJPY appears to have broken a bear flag with a measured target at 78.50. A break of 81.00 is needed to open the way to declines to last week’s low at 80.60 before continuing towards the psychologically important 80.00. A reversal and break of 81.40 would negate the outlook with any upside move finding resistance at 81.90.

Copper Outlook: Bears Look For Test Of Key Supports At $2.9425/$2.9370

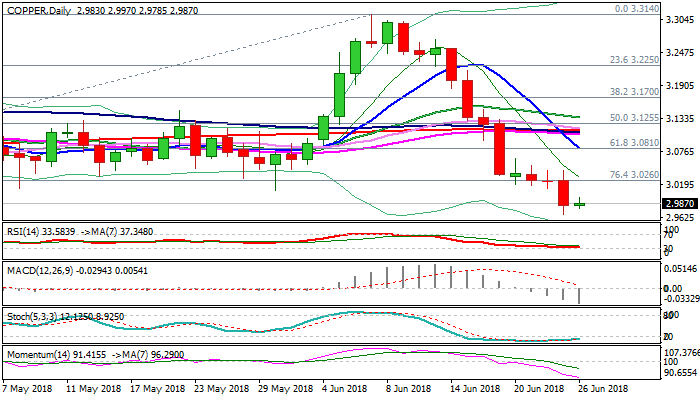

Copper holds firmly in red for the third straight week and broke below psychological $3.00 support on Monday’s extension of steep downtrend from $3.3140 peak (07 Jun).

Pullback from $3.3140 has nearly fully retraced $2.9370/$3.3140 (Mar/Jun rally) and pressuring key supports at $2.9425 (05 Dec 2017) and $2.9370 (26 Mar) which form a higher base on weekly chart.

Fears of escalation of trade conflict between major economies, continues to heavily weigh on copper price.

Firm break below $2.9425/$2.9370 pivot would confirm double-top ($3.3200/$3.3140) and generate major reversal signal.

Negative daily techs support scenario but hesitation on approach to key $2.9425/$2.9370 supports could be expected as slow stochastic is reversing in deep oversold territory.

Limited recovery is expected to precede fresh weakness, with upticks to be ideally capped by weekly 55SMA ($3.0408) and base of thin daily cloud ($3.0652).

Res: 3.0000, 3.0130, 3.0408, 3.0652

Sup: 2.9670, 2.9425, 2.9370, 2.9000

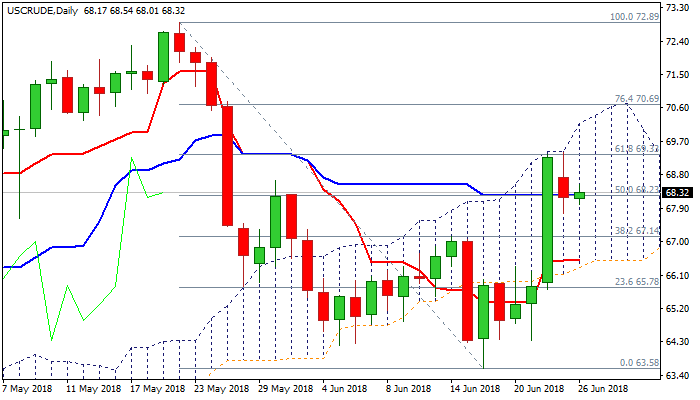

Crude Oil Outlook: Limited Correction Keeps Bullish Sentiment Remains In Play For Fresh Attempts Higher

WTI oil price rose on Tuesday, as uncertainty over Libyan exports partially offset negative impact from OPEC decision to increase output and fears of escalation of trade conflict between the US and other world major economies.

Oil price dipped on Monday after being repeatedly capped by top of daily cloud, on profit-taking after Friday's surge, but pullback was contained by 55SMA.

Positive sentiment exists on concerns about trade war and supply shortage from Libya, supported by bullish techs.

Also, Friday's long bullish daily candle continues to underpin, keeping near-term focus at the upside, while 55SMA holds.

Bulls need sustained break above key barrier at $69.33 (Fibo 61.8% of $72.89/$63.58 fall) to generate bullish signal for attack at psychological $70 barrier and daily cloud top at $70.18, break of which is needed to confirm bullish continuation.

Conversely, increased downside risk could be expected on close below 55SMA ($68.09), with break below $67.15 (Fibo 61.8% of $63.58/$69.36 upleg) needed to confirm reversal.

Res: 68.54, 69.00, 69.33, 70.00

Sup: 68.09, 67.77, 67.15, 66.56

Trade Spats Continue To Weigh

- Investors remain concerned about trade war prospects;

- USD rallying as risk aversion drives safe havens higher.

US futures are in the red again ahead of the open on Tuesday, with the ongoing trade spats between the US and others continuing to weigh.

While there haven't been any major developments in the last 24 hours, nothing we've heard recently fills investors with any confidence that we're going to see a de-escalation any time soon. With tariffs already being implemented and US President Donald Trump promising more in retaliation against the European Union and China, it seems the situation is going to get much worse before it improves.

As it stands, it's difficult to determine just what impact recent events will have on the economies of those involved, not to mention just how much worse the situation is going to get. What's clear though is that it's weighing heavily on risk appetite and if Trump keeps doubling down on his threats against the US trade partners, it could seriously take its toll. Given how closely Trump watches the markets, it will be interesting to see whether he changes his approach if the recent declines continue.

The dollar is continuing to be one of the biggest beneficiaries of the safe haven shift, with US 10-year Treasury yields creeping back below 2.9%. The greenback had pared its gains over the last week but it appears to be back on the ascent, with the euro having run into resistance around 1.17 against it. The pair has run into significant support around 1.15 on a couple of occasions over the last month, so could be a decent test of it should we slip back to those levels again.

The pound is also coming under pressure again today, having rotated off the 1.33 level. While the dollar appears to be the main driver here, it is also seeing weakness against other safe haven currencies, such as the yen. Moreover, with Brexit negotiations seemingly making little progress, the recent boost from the Bank of England's hawkish turn has proved to be short-lived.

The economic calendar is looking a little thin again on Tuesday, with US consumer confidence and API crude inventories the only notable releases. We will also hear from a number of central bankers throughout the day including Federal Reserve officials Raphael Bostic and Robert Kaplan.

Listless Session In Terms Of Positioning

Notes/Observations

- Incoming BOE MPC member Haskel touts the majority view in Parliamentary testimony

- Treasury Secretary Mnuchin and trade advisor Navarro walk-back hawkish views of investment-restriction plans for China in effort to calm markets

Asia:

- China PBoC may further reduce the Reserve Ratio Requirement (RRR) in H2 by 50-100bps

- China PBoC sets yuan reference rate at 6.5180 v 6.4893 prior (weakest yuan setting since January). China's sudden currency slide sparks rumors of an anti-Trump policy move

- China President Xi said to have told various CEOs last week that Beijing planned to strike back against punitive American tariffs. "In our culture we punch back"

- RBNZ announces Statement of Intent for July 2018 to June 2021: NZD currency (Kiwi) remains at an elevated level; reiterated policy to remain accommodative for some time - Japan PM Abe: Wants to secure US understanding of reason for BoJ policy; reiterates BoJ monetary policy not aimed at weakening JPY currency (Yen)

Europe:

- ECB's Couere (France): Expect rates to remain unchanged through the summer 2019 (in-line with Draghi press conference). Confident that inflation would return to close to 2%

- German Chancellor Merkel’s coalition troubles deepen over refugee crisis. Bavaria’s conservatives ramped up pressure on Merkel's open-door refugee policy

- Britain to announce more details on UK vision for future relationship in a white paper after the June EU Leader Summit

- UK: Parliament voted 415 to 119 in favor of building a new runway at London Heathrow

- SNB's Maechler: CHF currency remains highly valued; conditions remain fragile

- S&P raised Greece sovereign rating one notch to B+ from B; outlook Stable from Positive

Americas:

- White House Trade Adviser Navarro: we have no plans to impose investment restrictions; recent market selloff was a large overreaction

- Treasury Sec Mnuchin: Statement would be out not specific to China, but to all countries that are trying to steal our technology

Energy:

- CME raised NYMEX Crude Oil Futures maintenance margins by 7.8% to $2,750/contract (effective for Aug), gasoline futures maintenance margins by 3.2% to $3,200/contract (effective for Sept)

Economic Data:

- (DK) Denmark May Retail Sales M/M: 0.9% v 0.4%e; Y/Y: +3.9 v -0.7% prior

- (FI) Finland May Unemployment Rate: 9.3 v 8.6% prior

- (ZA) South Africa Apr Leading Indicator: 105.9 v 106.2 prior

- (SE) Sweden May PPI M/M: 1.4% v 0.6% prior; Y/Y: 6.3% v 4.9% prior

- (UK) May BBA Loans for House Purchases: 39.2K v 38.2Ke

- (HK) Hong Kong May Trade Balance (HKD): -43.2B v -49.1Be; Exports Y/Y: 15.9% v 8.5%e; Imports Y/Y: 16.5% v 11.3%e

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) opened its book to sell EUR-denominated 10-year bond via syndicate; Guidance revised to +55bps to mid-swaps with order book over €20.5B

- (FR) France Debt Agency (AFT) opened its book to sell EUR-denominated 1.75% Jun 2039 green bond; guidance seen +17bps to French Treasuries

- (ID) Indonesia sold total IDR5.16T in 6-month Islamic Bills, 2-year,4-year,7-year and 15-year Sukuk

- (CH) Switzerland sold CHF355M in 3-month Bills; Yield: -0.864% v -0.861% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.4% at 3,377, FTSE +0.6% at 7,480, DAX +0.3% at 12,308, CAC-40 +0.5% at 5,306; IBEX-35 +0.6% at 9,622, FTSE MIB +0.6% at 21,442, SMI +0.1% at 8,440, S&P 500 Futures flat]

- Market Focal Points/Key Themes: European markets open generally higher but moderated gains though maintaining positive; US talking down trade concerns support equities; light corporate news in the final week of trading before end of second quarter; construction and materials best performing sectors; travel & leisure worst performers; most indices trading higher; Eutelsat announces not interested in takeover of Inmarsat; UK Parliament votes to expand Heathrow; focus on German coalition talks; earnings expected in the upcoming US session include Lennar and Schnitzer Steel

Equities

- Consumer discretionary: Carnival CCL.UK -7.9% (earnings), Carpetright CPR.UK -0.3% (earnings), Elior ELIOR.FR -4.1% (new strategy), Ingenico ING.FR +5.3% (reportedly receives takeover interest), JC Decaux DEC.FR -1.0% (acquisition)

- Consumer staples: Eurofins Scientific ERF.FR +4.6% (outlook)

- Industrials: Andritz ANDR.AT +2.8% (analyst action), Renault RNO.FR +0.9% (analyst action)

- Telecom: Eutelsat ETL.FR +2.9% (not interested in Intelsat), Inmarsat ISAT.UK -7.9% (Eutelsat not interested in takeover)

- Utilities: Engie ENGI.FR +1.2% (not decided on EDP Renovaveis takeover)

Speakers

- ECB’s Hansson (Estonia) reiterated Council view that policy to remain rather expansionary

- BOE appointee Haskel (incoming MPC in Sept): Opportunities for adjusting interest rates appear to be growing but saw risks if raised too quickly . Would be ill-advised to change the inflation target

- Italy Fin Min Tria: Global cooperation was key for the world economy

- Italy Interior Min Salvini (also Dep PM): Govt to seek to reduce taxes for small business

- France Fin Min Le Maire: Cheap nuclear power was a considerable advantage; key to France's competitiveness

- EU authorized negotiations with WTO on Brexit-related adjustment

- Germany CSU official Dobrindt: Not looking to break up CDU-CSU alliance

- Taiwan Central Bank reiterated its view of its commitment to keep FX market in order and that t FX rate determined by market forces

- India PM Modi stated that saw 2018 GDP at 7.4%. Had taken a number of steps to increase investments. Govt committed to path of fiscal consolidation. Inflation had stayed within target despite rise in oil prices

- Iran President Rouhani reiterated view that would not give into pressure from President Trump. Country to defend its independence and values

Currencies

- Risk aversion tried to subside as US officials talk down trade restrictions on China and this helped the USD to stabilize against the major pairs.

- EUR/USD stalled just above the 1.17 for now as dealers’ noted the monetary policy divergence between the FED and ECB. The pair drifted lower as the session progressed in subdued trade. ECB’s Hansson helped to put some headwinds into the Euro after he noted that its policy would remain rather expansionary

- GBP/USD slightly lower at 1.3260 while USD/JPY was hovering just under the 109.70 area

Fixed Income

- Bund Futures trade 15 ticks lower at 161.98 as yields edge higher as Merkel fights for political future. Upside targets 162.75 followed by 163.25, while a return lower targets the 159.75 level.

- Gilt futures trade at 122.66 lower by 23 ticks after better than expected BBA loans for house purchases data. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Tuesday's liquidity report showed Monday's excess liquidity declined from €1.829T to €1.803T. Use of the marginal lending facility fell from €77M to €74M.

- Corporate issuance saw no deals priced in the primary market

Looking Ahead

- (BR) Brazil Jun CNI Consumer Confidence: No est v 102.2 prior

- 05:30 (ZA) South Africa Q1 Non-Farm Payrolls Q/Q: No est v 0.8% prior; Y/Y: No est v 0.2% prior

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (UK) BOE’s McCafferty (dissenter) in London

- 05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender (MRO)

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (UK) DMO to sell £2.25B in 1.75% Sept 2037 Gilts

- 05:30 (ZA) South Africa announces to sell combined ZAR2.4B in 2030, 2040 and 2044 bonds

- 06:00 (UK) Jun CBI Retailing Reported Sales: 10e v 11 prior; Total Distribution: No est v 17 prior - 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Jun FGV Construction Costs M/M: 0.6%e v 0.3% prior

- 07:00 (BR) Brazil Jun FGV Consumer Confidence: No est v 86.9 prior

- 07:00 (BR) Brazil Central Bank (BCB) COPOM Minutes

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (ES) ECB’s De Guindos (Spain) in Frankfurt

- 08:00 (RU) Russia announces weekly OFZ bond auction (held on Wed)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:55 (US) Weekly Redbook Sales

- 09:00 (US) Apr S&P/ Case-Shiller 20-City M/M: 0.40%e v 0.53% prior; Y/Y: 6.80%e v 6.79% prior; House Price Index (HPI): No est v 208.62 prior

- 09:00 (US) Apr S&P Case-Shiller (overall) HPI Y/Y: No est v 6.53% prior, Overall HPI Index: No est v 198.94 prior

- 09:00 (MX) Mexico May Unemployment Rate: 3.4%e v 3.4% prior; Unemployment Rate (Seasonally adj): 3.4%e v 3.4% prior

- 09:00 (EU) Weekly ECB Forex Reserves

- 10:00 (US) Jun Consumer Confidence: 128.0e v 128.0 prior

- 10:00 (US) Jun Richmond Fed Manufacturing Index: 15e v 16 prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 13:00(US) Treasury to sell 2-Year Notes

- 13:00 (US) Fed’s Bostic (voter, dove) in Alabama

- 13:45 (US) Fed’s Kaplan (dove, non-voter) in Houston

- 15:00 (AR) Argentina Apr Economic Activity Index (monthly GDP) M/M: No est v -0.1% prior; Y/Y: 2.1%e v 1.4% prior

- 15:00 (AR) Argentina Q1 Current Account: -$8.6Be v -$8.7B prior

- 15:00 (AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 40.00%

- 16:30 (US) Weekly API Oil Inventories

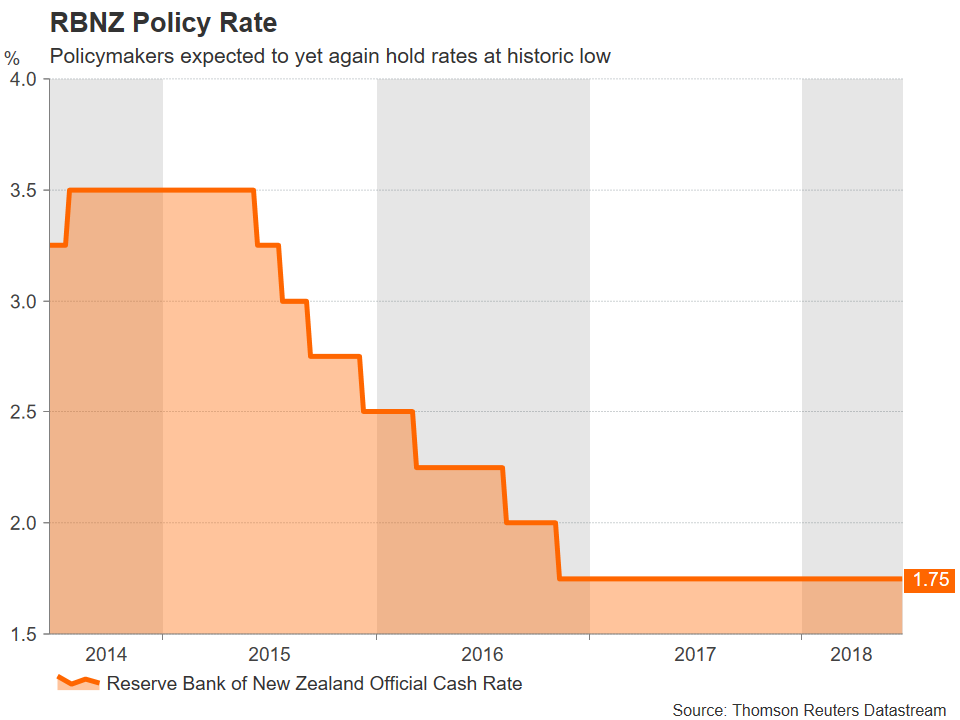

RBNZ Expected To Stand Pat, Policymakers’ Assessment To Move The Kiwi

The Reserve Bank of New Zealand will be deciding on rates on Wednesday at 2100 GMT. The central bank is anticipated to hold rates unchanged, with the focus falling on the Bank's communication regarding future policy as well as New Zealand's economic outlook.

New Zealand's central bank is widely expected to maintain its official cash rate at the historic low of 1.75% for the eleventh straight meeting. Thus, positioning on the kiwi will be dependent on policymakers' assessment of the economy as reflected in the statement accompanying the rate decision.

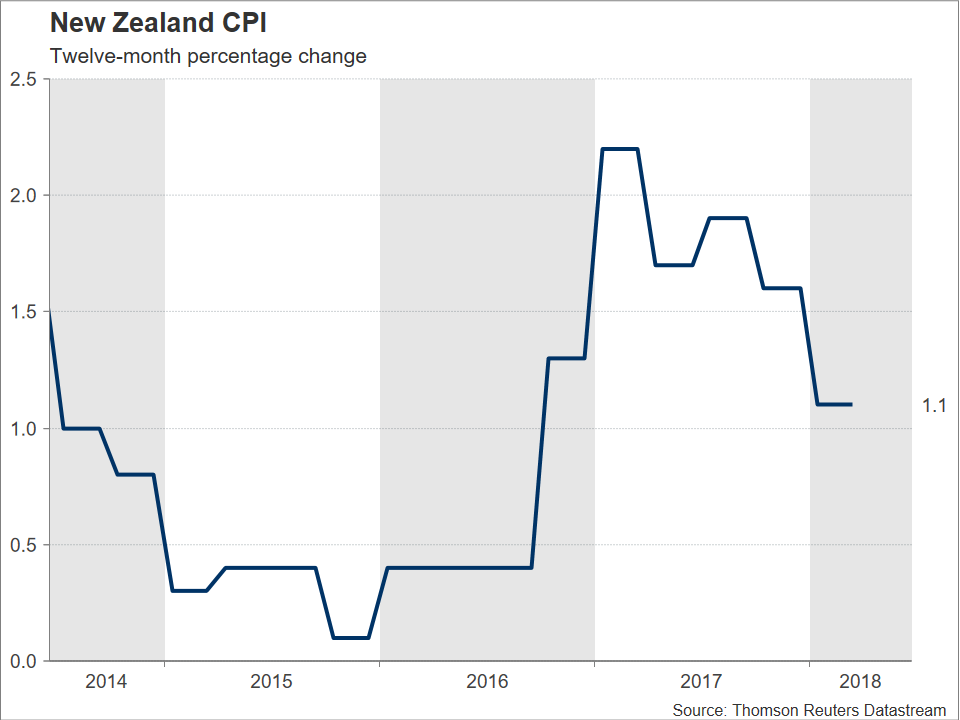

Last week's GDP figures showed a slowdown in the country's quarterly growth rate in Q1 relative to Q4 2017 – specifically, the rate of expansion stood at 0.5% q/q, its weakest since Q4 2016. Moreover, headline inflation fell in Q1, barely remaining within the lower bound of the bank's medium-term target range of 1-3% on an annual basis. Meanwhile, the risk of protectionism on the back of the Trump administration's latest actions looms large, having the capacity to weigh on global trade and consequently on New Zealand's economy which is heavily dependent on commodity exports. All these are supporting the case for a neutral stance by the RBNZ, the implication being that a hike or an interest rate cut remain on the table as the Bank's next move.

Nevertheless, despite an overall neutral stance as the most likely outcome, still policymakers' relative views about the economy can move the kiwi.

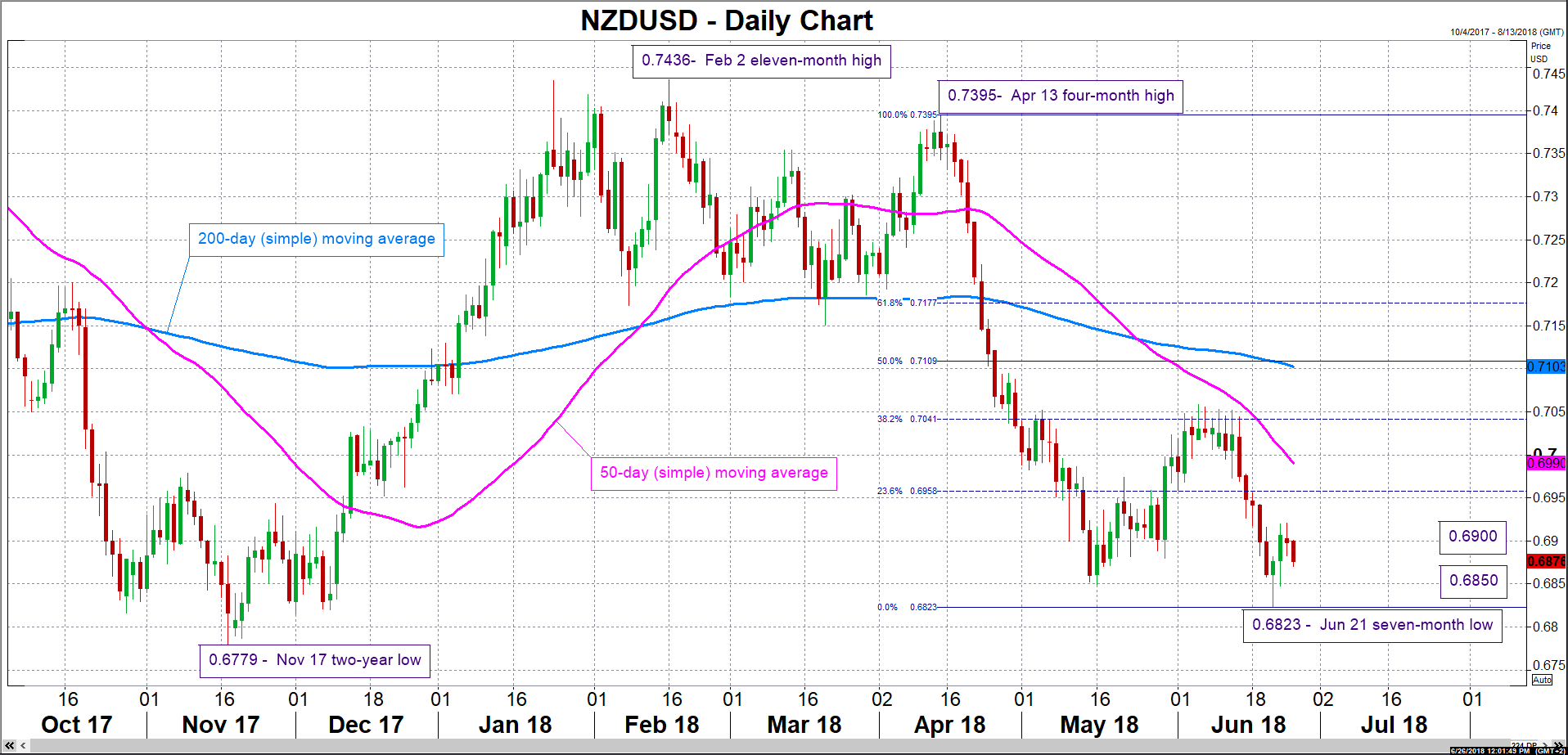

An upbeat take on the economic outlook is likely to boost NZDUSD, with resistance to advances possibly coming around the 23.6% Fibonacci retracement level of the April 13 to June 21 downleg at 0.6958, given that first the region around the 0.69 round figure is conclusively broken. More bullish movement would turn the attention to the current level of the 50-day moving average at 0.6990, with the area around this also encapsulating the 0.70 handle. On the downside, and in case of a cautious RBNZ that expresses concerns about the growth outlook, kiwi/dollar is expected to lose ground. Initial support to declines could come from the zone around 0.6850, this being a level that successful resisted a close below it from mid-May onwards. The seven-month low of 0.6823 from June 21 lies not far below and would be eyed in case of steeper declines; the region around this point also includes the 0.68 mark.

Commodity currencies, such as the kiwi and the aussie, have been suffering lately on the back of trade jitters instigated by President Trump's trade rhetoric. In this respect, comments on trade in the RBNZ's statement will be of particular interest. Also related to the statement, it is perhaps worth mentioning that Governor Adrian Orr, who took on the role in March, pledged to simplify the Bank's communication; the upcoming meeting might offer markets a taste of what he meant.

Ahead of the RBNZ policy decision and having the potential to lead to positioning on the kiwi will be May's trade figures due out on Tuesday at 2245 GMT. Of course, any updates on global trade and the trade spat between the US and China, as well as countries/blocks that were traditionally considered as US allies, such as the EU and Canada, will also be closely watched by market participants.

For the record, most economists polled by Reuters project a rate hike by the RBNZ materializing in H2 2019. Lastly, weighing on the kiwi on Monday were some remarks by New Zealand's acting Prime Minister Winston Peters, who said he does not expect the RBNZ to raise rates “any time soon”. He added though that “I could be wrong.”

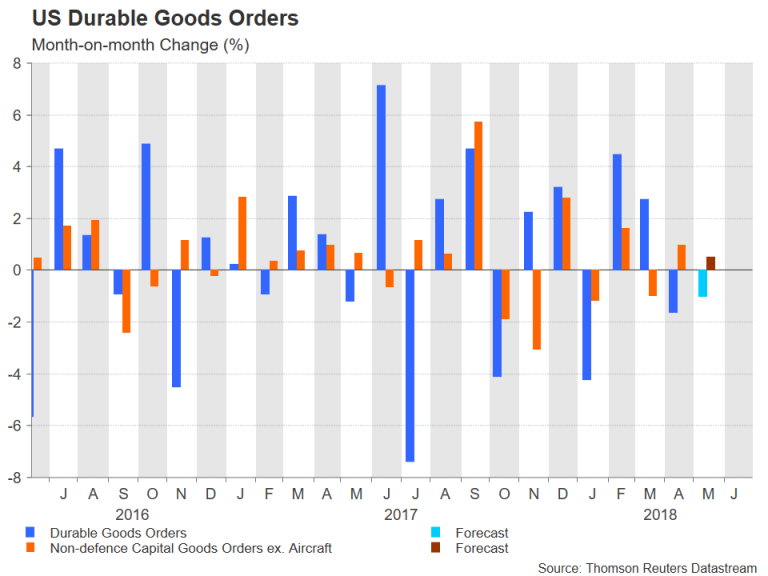

US Capital Goods Orders To Rise Further In May But Trade Policy Clouds Outlook

Data on durable goods orders will be watched out of the United States this week for an indication of business spending amid a worsening trade row between the world’s biggest trading powers. The report will be published by the US Census Bureau on Wednesday at 12:30 GMT and is expected to show another drop in the headline figure but increases in the more relevant core measures. The US dollar, which has been in retreat since the end of last week, could suffer further losses if the numbers suggest trade tensions are starting to bite into business sentiment.

Orders of durable goods, consisting of all manufactured goods designed to last at least three years, are forecast to decline by 1% month-on-month in May, adding to the 1.6% drop seen in April. However, the core measures of durable goods are expected to rise in May, which would point to a positive contribution to GDP growth in the second quarter.

When excluding for transportation, durable goods orders are projected to increase by 0.5% m/m in May, easing from the prior rate of 0.9%. The more closely-watched core measure, the non-defence capital goods orders excluding aircraft, are also forecast to rise by 0.5%, though this is half the rate of 1% enjoyed in April.

Nevertheless, the positive figures in April, and if confirmed, in May too, would bode well for second quarter growth as core capital goods are a key component of GDP calculations and, moreover, are considered to be a good proxy for business spending.

With trade tensions showing no sign of abating anytime soon, any surprise weakness in the May durable goods report would raise concerns that businesses are cutting back on their investment plans due to the uncertainty created by the trade frictions and from the increased trading barriers already introduced.

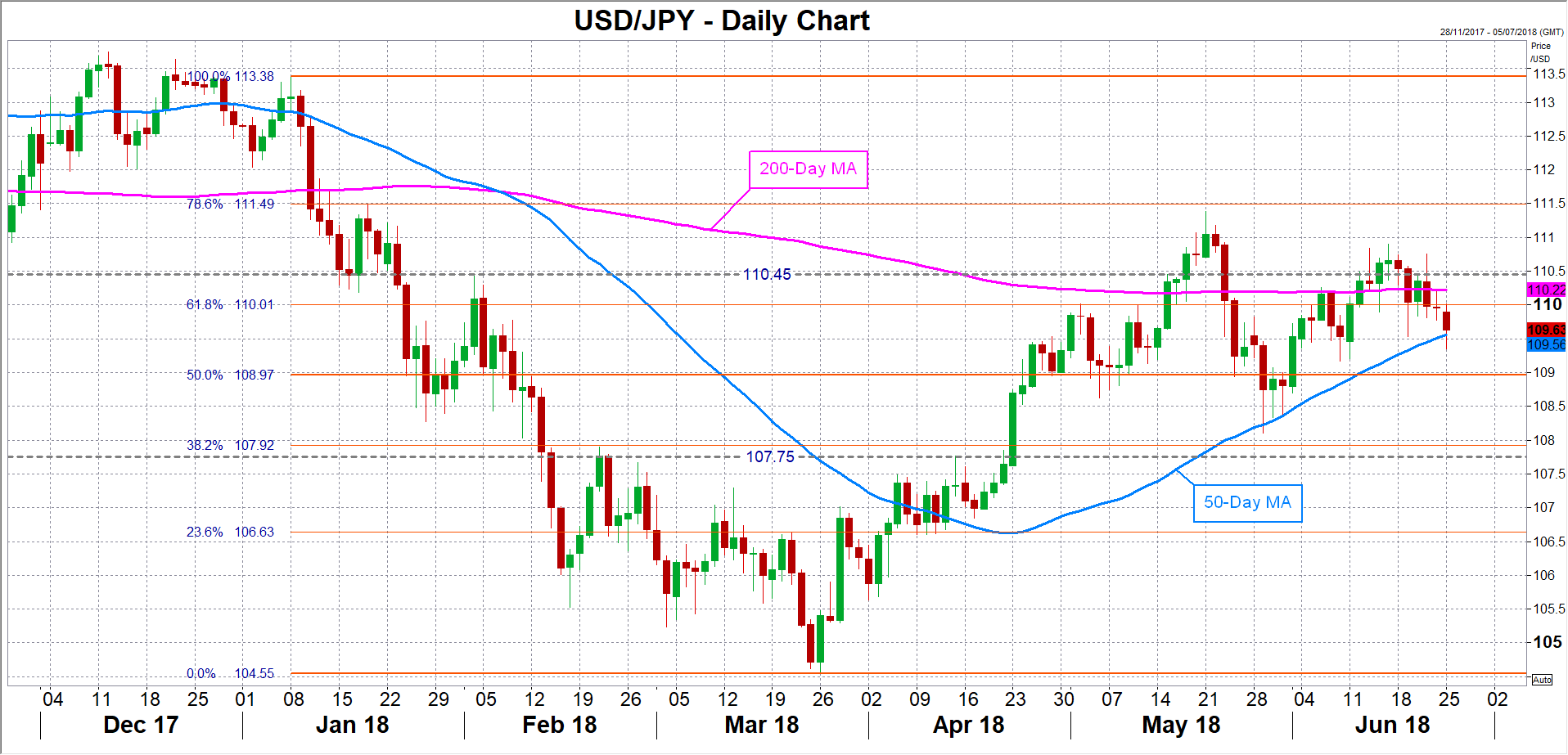

The dollar slipped to two-week lows versus the yen on Monday as President Trump threatened further protectionist actions against the EU and China. The pair is in danger of breaching the 109 level if the durable goods data disappoint. A drop below this key level, which is also the 50% Fibonacci mark of the downleg from 113.38 to 104.55, would open the way towards the next Fibonacci level at around 107.92.

However, better-than-expected numbers on Wednesday could help the greenback overcome nearby resistance at the 110 level. A break above the handle could help drive the pair towards the next resistance at 110.45. Higher up, the 78.6% Fibonacci at around 111.50 comes into view.

China Already Has Backup Plan If The US Bans Chinese Investments – ICOs

- The semiconductor space leads the tech sell-off

- ICOs attractive alternative investment in technology.

With the news of the Trump administration making a push to stop Chinese companies from investing in U.S. tech companies, many investors are wondering where the money will now flow? The ban is not only exclusive to China, the U.S. will plan on banning investment from any country that is planning on stealing U.S. Technology. News of the ban sent many tech stocks plunging with Micron Technology ($MU) dropping almost 7%. The semiconductor space leads the tech sell-off as trade war uncertainty and investment ban news intensified. Cryptocurrency caught a little bit of a break as many Altcoins posted double-digit percentage gains. Perhaps money that would once go into U.S. equities will now make its way into the cryptocurrency market, including ICO’s.

China and other nations affected by the U.S. ban may now see the cryptocurrency market including ICO’s as an attractive alternative investment in technology. China has been quick to support the development and use of crypto assets that emerge from within and work closely with its government. China is home to the 7th largest cryptocurrency, NEO that is currently trading near $32, down well over 50% from its all-time high of just over $162 at the height of the bull market. It is known that China and the United States are competing tirelessly to become the leader in technology. Perhaps cryptocurrency innovation is the vehicle that will give China the upper hand.

Many new crypto projects are emerging from China and interestingly enough, many of them have very close ties to the Chinese government. This could be China’s strategy to promote and support crypto projects that are built at home. For example, THEKEY (TKY) is an identity verification crypto project that works closely with the Chinese government and is built on the NEO platform. China is making a push to work with THEKEY on research of Blockchain applications in social security service. This is huge news being that this is a push to use Blockchain and cryptocurrency to improve and replace an existing system for data identification and collection. TKY is currently trading for $0.008415 and has an overall market capitalization of $39,590,000. Currently, THEKEY is listed on lesser known smaller exchanges such as Kucoin and HitBTC. When the project gets more attention and is listed on larger exchanges with more volume we could see a significant price surge. That is usually the trend for newer coins that get listed on larger exchanges.

It is said that NEO is the Chinese Ethereum and the success of Ethereum came due to the large number of ICO’s that have been launched using the platform. As the U.S. tries to push China out of the competition, NEO seems to present itself as a saviour for Chinese technology innovation. If ICO’s begin to launch on the NEO platform at a similar rate to that of the Ethereum platform during 2017; it is possible that NEO can overtake some of the largest cryptocurrencies and be a top choice for developers that wish to build applications on the Blockchain. Thus driving a Chinese protocol to the forefront of the cryptocurrency ecosystem along with Ethereum and EOS. After all, Chinas government backed crypto rankings recently put EOS at the top spot. China may be able to get around U.S. obstacles by investing their time and money into becoming a leading cryptocurrency and Blockchain backed nation. China’s interest in Blockchain and Cryptocurrency is glowing, this is just another reason to be long-term bullish.

European Markets Shake Off Trade War Concerns | Gold Still Feeling The Heat

- Trump administration is further ranching up the tensions

- European car industry may face tariffs

Trade tariff trade is a funny one because if we have learned anything in the last few months since this trade tension issue has emerged is this that traders have bought the dips and sold it on top. Having said this, Trump administration is further ranching up the tensions around global trade war and investors have become increasingly nervous. The market action on Wall Street and in Asia was the evidence of this. However, investors over in Europe decided to shaken these concerns. It is highly likely that the dominant trend may remain skewed to the downside.

If the US stops Chinese investment in certain US sector, it will have a strong counteraction. Treasury secretary, Steven Mnuchin has said that more details on this would follow by the end of this week and this is going to keep investors even more nervous. On top of this, Trump administration is further adding to this uncertainty by keep sending conflicting statements; one person would say it is fake news and another would say more details on the topic would emerge sooner than later.

Looking at the biggest economy of the Eurozone, Germany, one can tell how much pain investors are feeling. Trump has shown initiatives to target the European car industry. The DAX index is at its two months low and the FTSE index is equally feeling the similar pain. If the trade tariffs on the European car industry become a reality, we will be set for another wild ride. The European markets would likely face a serious sell-off and the auto sector would be the focal point of this.

Back in the forex market, the British pound is still holding on to its most of its gains as investors continue to price in the possibility of another rate hike by the Bank of England.

Trade tensions aren’t helping gold at all, there is only one clear trend which is skewed to the downside. By looking at the chart, it appears that bulls have left the town. We think that the price would continue to move lower and it is likely that we test the support at $1250.

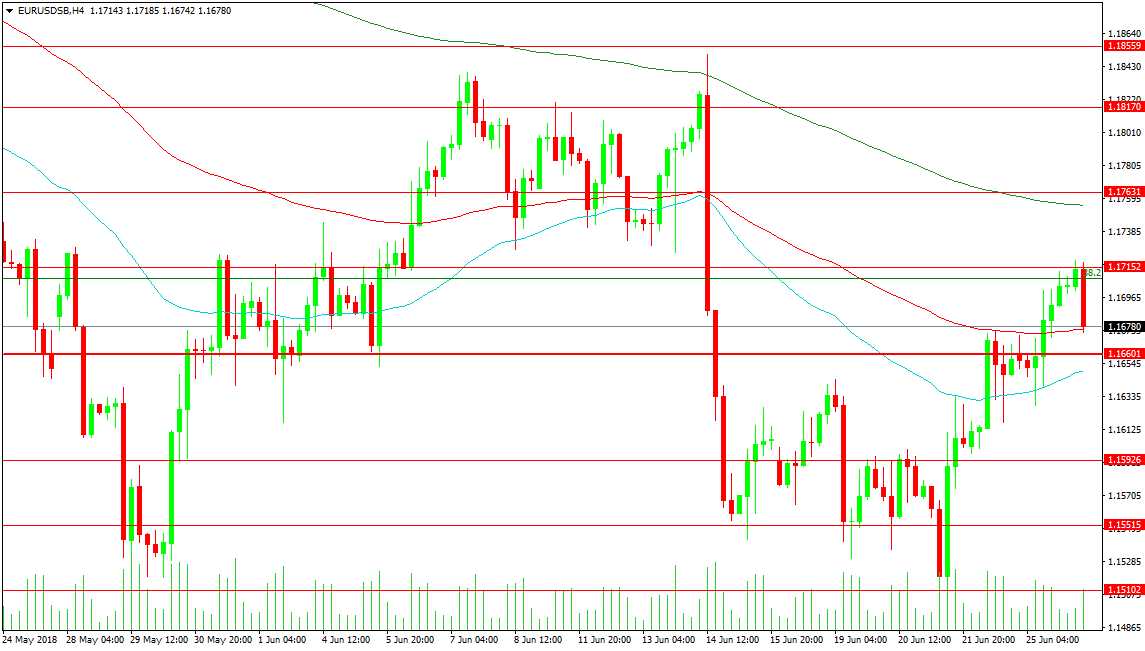

Forex Analysis: EURUSD

The EURUSD cross is currently testing its 100 period MA at 1.16760 as support while it retraces the selloff from the ECB on the 14th of June. Resistance for the pair comes in around the 1.17152 level and the 38.2% fib level of the 2016 low to the 2018 high. The 200 period MA is the next resistance and is found at 1.17547 with the 1.7631 level above. The 1.18000 level can see some profits taken with rallies this month sold above this area from 1.18170 to 1.18560. A break above the latter can signal a leg higher to test 1.20000.

The 1.16600 level remains a level of consolidation with price gathering strength here for the last leg higher. The 50 period MA was used as support on the recent touch and is located at 1.16495 today. A solid break under and retest of the MA can point to another push lower for the pair. This would target 1.16000 followed by 1.15926 and 1.15515. The recent lows have formed a double bottom on the 4 hour chart with the May low at 1.15100. This would require the high at 1.18500 to be broken and target 1.21900.