Sample Category Title

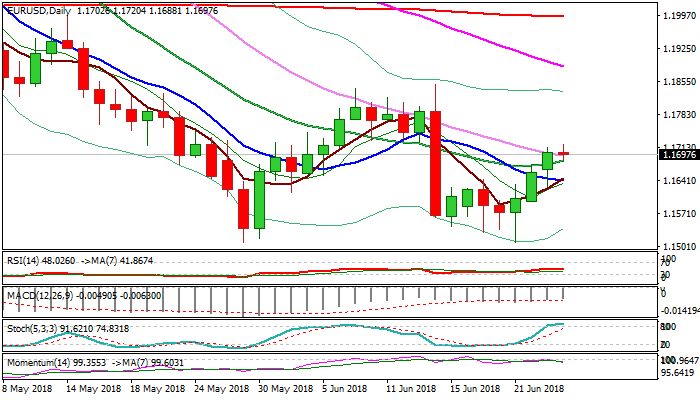

EURUSD Outlook: Consolidation May Precede Fresh Upside, Broken 20SMA To Ideally Contain

The Euro maintains firm tone and cracked pivotal barrier at 1.1718 (Fibo 61.8% of 1.1848/1.1508 bear-leg) in early Tuesday's trading after generating bullish signal on Monday's close above previous pivot, marked by 20SMA and converged daily Tenkan./Kijun-sen (1.1677).

Risk aversion on concerns about trade war continues to support Euro, but stronger hesitation at 1.1718 Fibo barrier could be anticipated.

Consolidation was so far held by strong support provided by broken 20SMA/4-hr cloud top (1.1685) which should ideally keep the downside protected and keep bulls intact.

Eventual break above 1.1718 would expose next key barrier at 1.1746 (weekly cloud top), violation of which would generate another strong bullish signal. Extended dips below 1.1685 need to be contained by strong supports at 1.1640 zone (converged 5/10SMA's / 4-hr cloud base) to maintain bullish near-term bias.

Res: 1.1720, 1.1746, 1.1767, 1.1800

Sup: 1.1685, 1.1670, 1.1640, 1.1591

China drops tariffs on soybeans, soybean cake and fishmeal from Asian neighbors

China announced to drop tariffs on some animal feed ingredients from five Asian neighbor countries. The products include soybeans, soybean cake and fishmeal. There are currently 3%, 5% and 2% tariffs on these products currently. And, tariffs on these products originating from Bangladesh, India, Laos, South Korea and Sri Lanka will be dropped effective July 1.

The move is seen as a preparation for US initiated trade war. China announced to retaliate to US section 301 tariffs. Soybean is on the list of US goods to be imposed 25 tariffs, effective July 6.

UK And US Central Bank Representatives Will Be Speaking Today

At 09:00 GMT, MPC Member Haskel is due to testify on his appointment before the Treasury Select Committee, in London. GBP pairs can move in reaction to comments made during this event.

At 09:30 GMT, MPC Member McCafferty is due to speak about monetary policy at the Official Monetary and Financial Institutions Forum, in London. Audience questions are expected to follow. GBP crosses may be moved by the comments made during this event.

At 12:00 GMT, US S&P/Case Schiller Home Price Index (YoY) (Apr) is expected to come in at 6.8% from a prior 6.8%. This measure has been holding a steady improvement since the late 2014 low, with today’s data expected to be largely in line with expectations.USD crosses may be heavily traded as a result of this data.

At 17:00 GMT, FOMC Member Bostic is due to speak at the Birmingham Civil Rights Institute, in Alabama. Audience questions are expected after the speech. USD pairs can move as a result of comments made during this event.

At 17:45 GMT, FOMC Member Kaplan is due to speak at a scheduled event today. USD pairs can be impacted as a result of comments made during this time.

At 21:45 GMT, New Zealand Trade Balance (MoM) (May) numbers will be released and is expected to be $100M (MoM) and $-3.74B (YoY) with a prior number of $-1,193M (MoM) and $-3.76B (YoY). Imports (May) are expected to be $5.10B against $4.79B previously. Exports (May) are expected to be $5.25B against $5.05B previously. This data can cause a move in the NZD crosses.

Equities And USD Extend Losses In Risk Adverse Markets

Stock markets fell hard yesterday as trade tensions deepened and the consequences of such action has investors worried. US Company Harley Davidson has announced plans to shift some production out of the US in order to avoid paying tariffs when exporting its products into the EU. This is a blow for Presidents Trumps trade policy and is a bell weather for the extraordinary measures businesses are having to explore in order to weather the storm as trade relations break down.

Harley Davidson shares dropped 5.97% yesterday with the US 500 down to 2717.00 and the Nasdaq down 2.17% to 7044.50 as it continues to fall since the US Supreme Court ruled to allow internet sales taxes last week. The JPY is strong today with the USD weak as risk off sentiment persists as we close the half year this weak and traders pare losing positions.

German IFO – Current Assessment (Jun) was 105.1 against an expected 105.5 from 106.0 previously which was revised to 106.1. IFO – Expectations (Jun) were 98.6 against an expected 98.5 from 98.5 prior which was revised to 98.6. IFO – Business Climate (Jun) was 101.8 against an expected 101.7 from 102.2 previously which was revised to 102.3. The data showed a weakening business climate in Germany following on from the fall in the March data. This data cannot be ignored as it surveys 7,000 businesses and is a leading indicator of economic direction. EURUSD moved higher from 1.16398 to 1.16708 after the release of this data.

Chicago Fed National Activity Index (May) came in at -0.15 against an expected 0.09 from a previous 0.34 which was revised up to 0.42. This data has now dropped below the zero level for 2018 with a high set at 0.88 in the February reading. A slip under zero can cause a market reaction but is not a worry in itself with the normal range being re-established. GBPUSD fell from 1.32869 to 1.32703 following the data release.

US New Home Sales (MoM) (Apr) were 0.689M against an expected 0.666M from 0.662M previously which was revised down to 0.646M. The data gained some ground on last month and is holding steady between 0.600M and 0.700M. Further improvement in these figures shows a pickup in confidence in the US housing market. EURUSD fell from 1.32800 to 1.32557 after this data release.

EURUSD is up 0.06% overnight, trading around 1.17098.

USDJPY is down -0.14% in the early session, trading at around 109.588

GBPUSD is up 0.04% this morning trading around 1.32820

Gold is down -0.13% in early morning trading at around $1,263.70

WTI is down -0.07% this morning, trading around $67.93

Currencies: Euro Holding Fairly Strong Even As Trade Tensions Persist

Rates: Risk sentiment shows signs of improvement

Asian stock markets show reliance after a weak opening while other markets also suggest that yesterday's risk aversion won't continue. It could slow/halt the slide in core bonds since mid-June. The start of the US supply operation could cause underperformance vs the German Bund. The eco/event calendar is rather uninspiring.

Currencies: Euro holding fairly strong even as trade tensions persist

Yesterday, USD/JPY and EUR/USD were only little affected by the risk-off correction due to raising trade fears. EUR/USD is even trending higher in the 1.1510/1.1851 range. The market apparently already reduced substantial euro long exposure after the ECB meeting. We remain cautious on further sustained euro gains.

The Sunrise Headlines

- US equity markets were hit hard yesterday, with the NASDAQ (-2.09%) underperforming the rest. Asian stock markets continue the trend this morning with all major markets opening in red, but in recovery since.

- Following positive remarks from Moody's, Standard & Poor has reviewed Greece's rating from B to B+. They believe the final debt relief deal with the European Stability Mechanism significantly reduces sovereign debt risks.

- The Irish Central bank is leaning toward increasing the so-called counter cyclical capital buffer as the economy strengthens. With this move, it would follow other European nations, such as France, the UK and Sweden.

- BMW has signalled that Brexit could force them to close UK plants. The German car manufacturer said it saw no other option if the company cannot quickly and reliably import components from mainland Europe.

- Despite the deal struck by OPEC+ to increase oil output, what normally would put bearish pressure on oil prices, “price risk is still very much to the upside” according to analysts with supply side problems in Venezuela, Iran and Libya.

- ECB Executive Board member Benoit Coeure has confirmed the ECB will continue to reinvest the principal payments from maturing securities in 2019, which amount to around €15 billion per month.

- Several prominent BOE officials speak at appointment Hearings in London today and Fed's Bostic and Kaplan will give a speech in the US tonight. US consumer confidence is the sole eco release while the US and Italy tap the market

Currencies: Euro Holding Fairly Strong Even As Trade Tensions Persist

Euro not affected by risk-off correction

On Monday, global equities tumbled as investors feared more fall-out from the trade war. Still, the risk off had only modest impact on the major FX cross rates. EUR/USD even rebounded. US-German interest rate differential narrowed slightly, but we doubt this was the driver. A decent German IFO maybe helped the euro. Market positioning was probably the main factor as investors already scaled back euro longs after the ECB meeting. EUR/USD closed at 1.1704. USD/JPY reversed most intraday losses as White House advisor Navarro downplayed the risk of investment restrictions later in the session. Overnight, Asian equities also trade with modest losses, but the damage remains contained given the sell-off in the US. A tentative sign that the impact of trade tensions might ease a bit, at least for now? USD/JPY remains under moderate downside pressure (at 109.55). EUR/USD extends its gradual rebound and is changing hands north of the 1.17 barrier.

Today, several ECB members will speak. We don't expect them to question the ECB guidance on interest rates. Even so, their assessment remains interesting. In the US, the Richmond Fed manufacturing index and Consumer confidence from the Conference Board will be released. The consumer confidence is expected stable at a strong 128. This indicator will probably be little affected by the trade conflict. The report might be slightly USD supportive. Yesterday, the flaring-up off trade fear didn't cause the ‘usual' risk-off correction in the major FX crosses (several small, less liquid currencies were affected more). Markets will continue to keep a close eye at the trade developments. In a day-to-dayperspective, we have the impression that tensions might ease. This might help to put a bottom for USD/JPY. The picture for EUR/USD is less clear. For now, we assume further consolidation in the 1.1510/1.1851 trading range. There is still plenty of euro event risk to come starting with the EU summit later this week.

Yesterday, sterling remained in the defensive. EUR/GBP was also supported by the EUR/USD rebound. Today, the CBI retail data wil be published. Jonathan Haskel will appear before Parliament for its appointment hearing. Markets will look for its position (hawk-dove) within the MPC. For now, we don't expect a big reaction of sterling. A better sentiment on risk might be slightly supportive for the UK currency

EUR/USD: extends gradual rebound

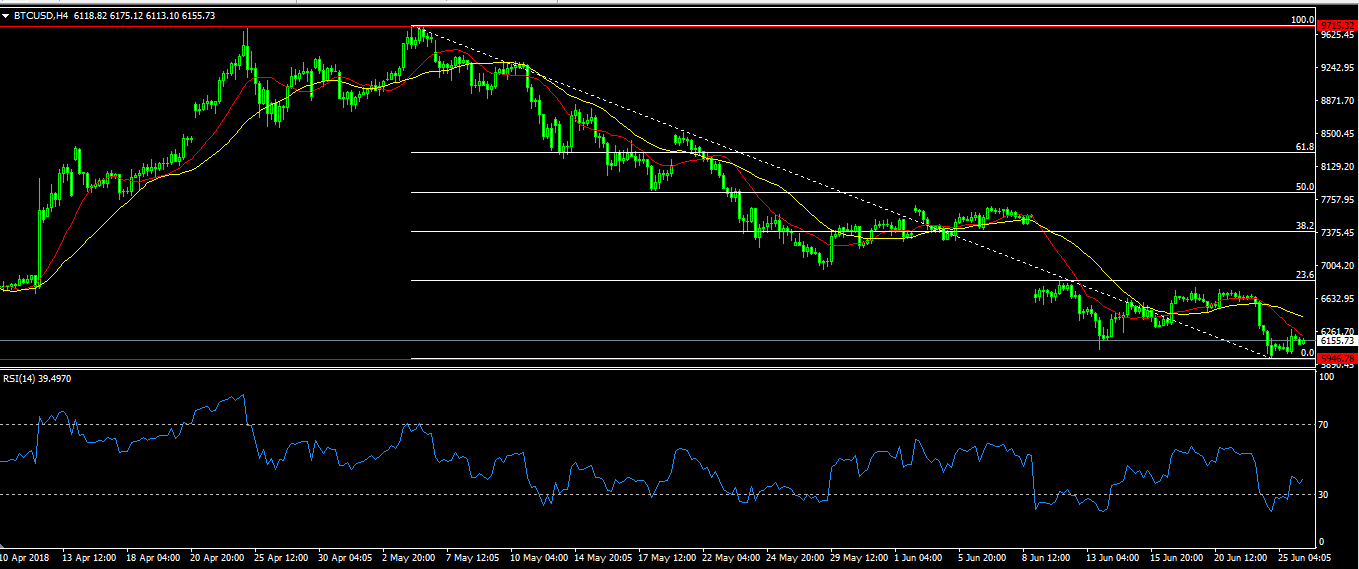

Bitcoin Bounces Back After Weekend Sell-Off

Two weeks ago, the price of bitcoin dropped sharply from $7580 to $6730 after a South Korean cryptocurrency exchange was hacked. Since then, the price of bitcoin has remained at these low levels and this weekend, the price dropped to below $6,000. This was the lowest level since February this year. The sharp decline came as traders started worrying about regulations and the security of their holdings.

After the hackings that happened in the past two weeks, regulators around the world grew concerned and initiated talks on how to regulate the sector. Traders view these regulations as being counterproductive to the whole idea of blockchain which is ultimately designed to be transparent, unregulated and not governed by any third party.

Crypto security has always been an area of concern. Critics of digital tokens believe that the decentralized system makes it possible for people with bad intentions to gain access. Moreover, most of the crypto exchanges have been accused of manipulating the price of cryptocurrencies. For example, in December, Coinbase – one of the largest exchanges – announced that an insider trading investigation was underway. Last month, Upbit – the fourth largest exchange in the world – announced that it was being investigated for deceiving investors.

Today, the BTC/USD pair is trading at $6150, which is a bit higher than the pair’s weekend low of $5945. The current price is also lower than the previous support level of $6450 which the pair reached in April. The price is also below the short and longer-term moving averages. Its RSI has moved from 19 during the weekend and is currently at 39. There is a likelihood that the pair will continue moving up as traders pick the bottom. If this happens, traders should pay attention to the $7,400 and $7800 which are the 38.2% and 50% Fibonacci retracement levels.

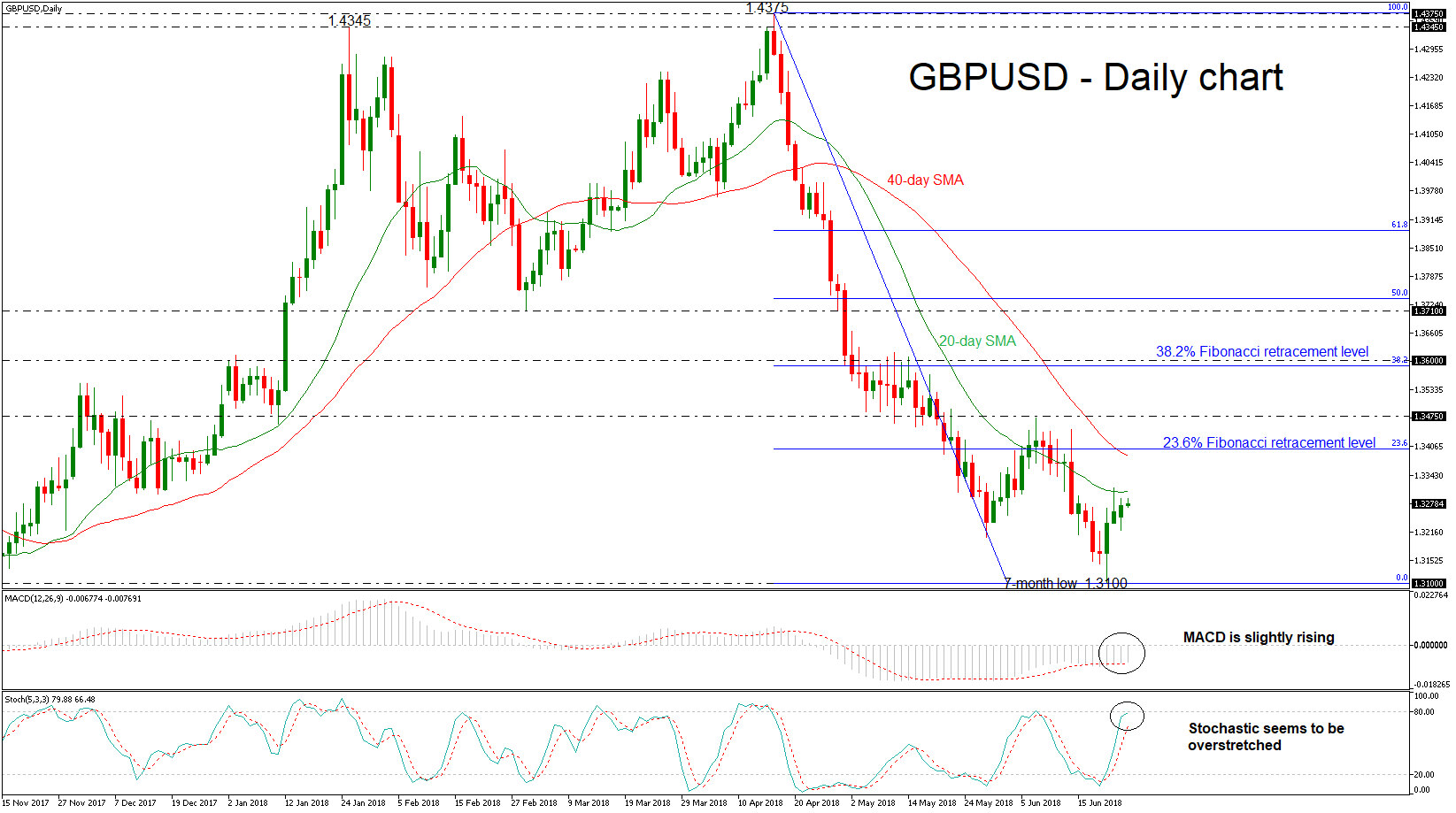

GBPUSD Bounces Off 7-Month Low Of 1.3100, Finds Obstacle On 20-Day SMA

GBPUSD has been trading higher following the rebound on the seven-month low near the 1.3100 psychological level. The price is set to complete the fourth bullish day in a row, however, the 20-day simple moving average is acting as major resistance barrier for the bulls. The neutral to the bearish picture over the past month looks to last for a while longer as the technical indicators fail to have clear directional movement.

In the daily timeframe, the MACD oscillator is moving slightly above its trigger line but still holds in the negative territory. On the other hand, the %K line of the stochastic oscillator is approaching the overbought zone but is losing its strong momentum, while the %D line is following the price action.

If prices continue to head higher, resistance should come from the 23.6% Fibonacci retracement level of the downleg from 1.4375 to 1.3100, around the 1.3400 handle. This level is also holding near the 40-day SMA. A jump above these levels would strengthen the short-term bullish view and open the way towards the 1.3475 hurdle. Clearing this key level as well, the next stop could come at 1.3600.

However, should a downside reversal take form, immediate support will likely come from the seven-month low of 1.3100. A slip below this level could shift the bias back to bearish one, with the next support coming from the 1.3040 level, taken from the low on October 2017.

To sum up, GBPUSD has been developing within a downtrend since April 17 that reached the 1.4375 resistance barrier and started an aggressive bearish rollercoaster. The medium-term picture remains negative as the price is still moving below the moving averages.

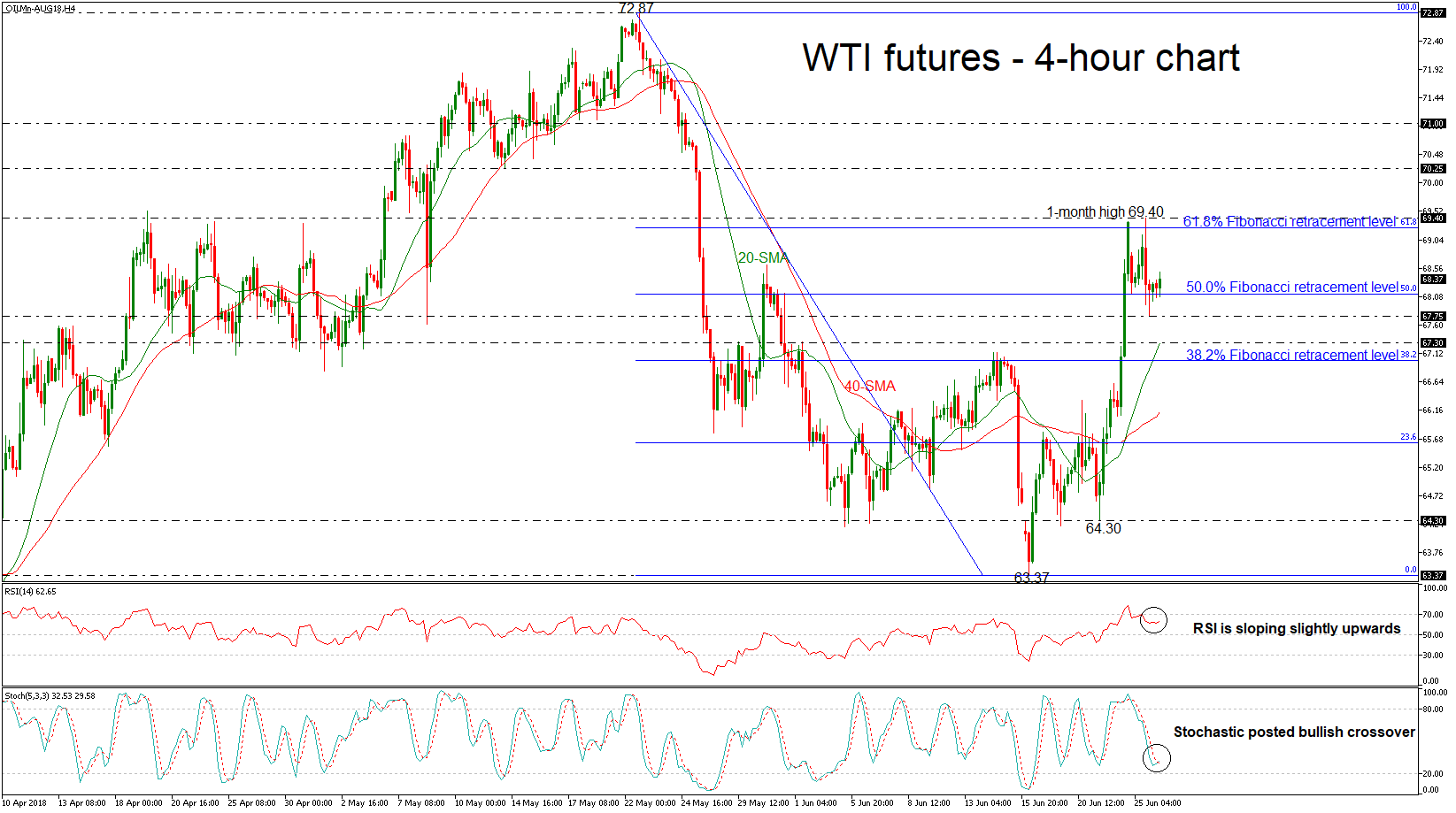

WTI Futures Remains Bullish As It Stands Above 50.0% Fibonacci

West Texas Intermediate (WTI) futures posted a negative day after they reached a new one-month high of 69.40 yesterday, while on Friday the price created sharp bullish extensions. The price eased and tested the 67.75 support level on Monday before the jump above the 50.0% Fibonacci retracement level of the downleg from 72.87 to 63.37, near 68.12, once again.

In the 4-hour chart, the RSI stands in the bullish area and is sloping slightly north, while the %K line of the stochastic oscillator posted a positive crossover with the %D line near the oversold zone, suggesting that the market would continue the upside momentum.

If the market manages to pick up speed, the 61.8% Fibonacci mark of 69.24 could offer nearby resistance. Then a leg above that level, the oil could meet the one-month high of 69.40, which stands marginally above the aforementioned barrier.

Should prices decline and drop below the 50.0% Fibonacci support could be found around 67.75, an area which provided strong resistance on Monday. Then a leg below that level, the oil could meet 67.30, which overlaps with the 20-SMA in the 4-hour chart, before the focus shifts to the 38.2% Fibonacci near the 67.00 handle.

In the medium-term, the outlook remains bullish since prices hold above all the moving average lines and the bullish cross between the 20- and the 40-SMAs stays in place.

Dollar Around 2-Week Lows Versus Yen As Trade Worries Keep Risk Appetite Suppressed

Here are the latest developments in global markets:

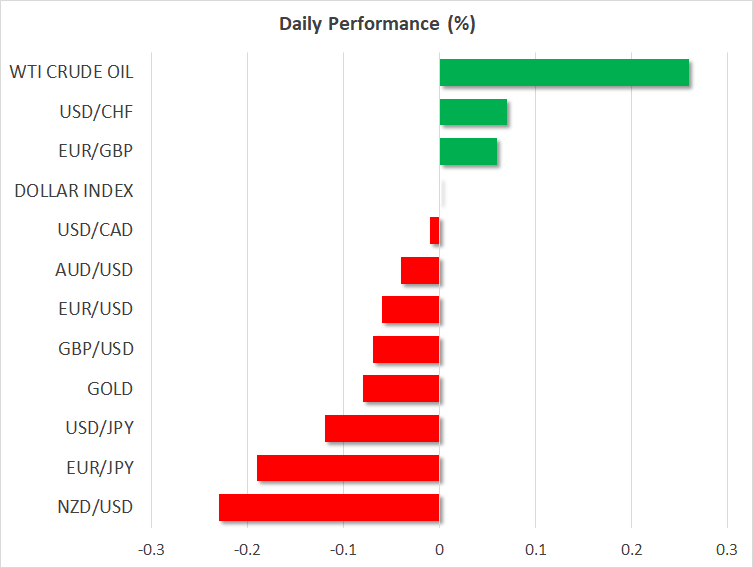

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – is practically unchanged on Tuesday, after posting losses in the previous session. Meanwhile, the Japanese yen continued to enjoy some haven demand as trade frictions remained front and center.

STOCKS:Trade concerns triggered another selloff in US stocks on Monday. The Nasdaq Composite led the way lower (-2.09%), while the S&P 500 (-1.37%) and the Dow Jones (-1.33%) followed in its footsteps. US Treasury Secretary Mnuchin hinted that the upcoming investment restrictions against China may be applied to other countries as well, while Harley Davidson (-5.97%) said it would move some production overseas to avoid retaliatory EU tariffs. Asian equities, on the other hand, were mixed. Japan’s Nikkei 225 and Topix indices rose by 0.02% and 0.16% respectively. In Hong Kong, the Hang Seng was nearly unchanged (-0.01%), while in China, the CSI 300 fell 0.83%. In Europe, futures tracking all the major benchmarks are pointing to a positive open today. The same applies for US equity futures; the Dow, S&P, and Nasdaq are expected to open a little higher.

COMMODITIES: Oil prices are higher on Tuesday, recovering some of the losses from the previous session. WTI and Brent crude are higher by 0.3% and 0.2% respectively today, buoyed by supply disruptions in Canada and Libya. On the other hand, though, the escalating trade conflict between the US and China was casting a shadow on the robust forecasts for oil demand over the coming years, dragging prices lower yesterday. In precious metals, gold is down by nearly 0.1%, currently trading just above $1,264. The yellow metal continued to decline yesterday even despite the risk-off sentiment seen in other assets and a pullback in the US dollar; two factors that typically support gold.

Major movers: Risk aversion dominates as trade fears linger

Concerns regarding global trade remained the dominant market theme on Monday, diverting money flows away from riskier assets such as stocks and into perceived safe-havens, like the Japanese yen and US bonds. Major US stock indices closed the day notably lower, while dollar/yen touched a fresh two-week low of 109.35 and longer-term US Treasury yields declined somewhat.

The moves followed some conflicting signals from the White House. First came US Treasury Secretary Mnuchin, who ignited the first wave of risk aversion after saying via a tweet that any investment restrictions into the US will not be specific to China, but would apply to all countries “trying to steal our technology”. However, White House trade advisor Navarro soon told CNBC that there are “no plans to impose investment restrictions on any countries” and that “all we’re doing…is trying to defend our technology when it may be threatened”. He also characterized the negative market reaction as a “large overreaction”. Navarro’s remarks triggered a rebound in risk-sentiment, helping dollar/yen and US stock indices to spike higher on the news, though his optimism was not enough to calm investors as the recovery quickly faded and markets resumed their slide.

The negative sentiment was likely amplified by reports that trade fears are already starting to disrupt supply chains, after Harley Davidson said it would move production for European customers overseas to evade retaliatory tariffs on its products from the EU. Moving forward, trade developments could continue to dictate market action in the coming days. The next major announcement is likely to come on June 30, when the US is due to announce the specifics of its investment restrictions against China. Of utmost importance will be the extent of these restrictions, as well as how China chooses to respond.

Sterling/dollar was down by nearly 0.1%, while euro/sterling was up by roughly the same percentage, ahead of a crucial EU summit on Brexit that commences Thursday.

Elsewhere, the commodity-linked currencies reacted as one would expect amid boiling trade tensions; by moving lower. Kiwi/dollar is down by 0.2% and aussie/dollar by 0.05%, both extending losses from yesterday.

Day ahead: Trade and politics in focus; CaseShiller house price data and consumer confidence figures due out of the US

Tuesday’s economic calendar does not feature much in terms of releases, with some data on house prices and consumer confidence being due out of the US. It appears that developments on the trade front, as well as political deliberations in Germany, have greater potential to move the markets rather than any of today’s releases.

The CaseShiller indices gauging house prices in the US during the month of April will be made public at 1300 GMT, while the Conference Board will be releasing data on June’s consumer confidence at 1400 GMT. Consumer sentiment as measured by the relevant index is anticipated to stand at 128.0, remaining unchanged relative to May’s print.

Trade tensions continue to rank high in terms of investor focus, with market participants turning their attention to the Trump administration’s trade and investment restrictions, as well as any retaliatory actions by trading partners of the US that could further escalate the situation, triggering a flight to safety at the expense of riskier assets such as stocks. Among others, a US Treasury release relating to technology investment restrictions will be closely watched.

Meanwhile, German Chancellor Angela Merkel will be holding talks with the leaders of the other parties in her coalition government, touching on euro-area reforms and immigration policy; the latter is seen as posing threats to her government.

Among policymakers making appearances on Tuesday are Dallas Fed President Robert Kaplan (1745 GMT – non-voting FOMC member in 2018), Atlanta Fed President Raphael Bostic (1715 GMT – voting FOMC member in 2018) and ECB Vice President Luis de Guindos (1200 GMT).

In energy markets, weekly API data on crude oil stocks are due at 2030 GMT.

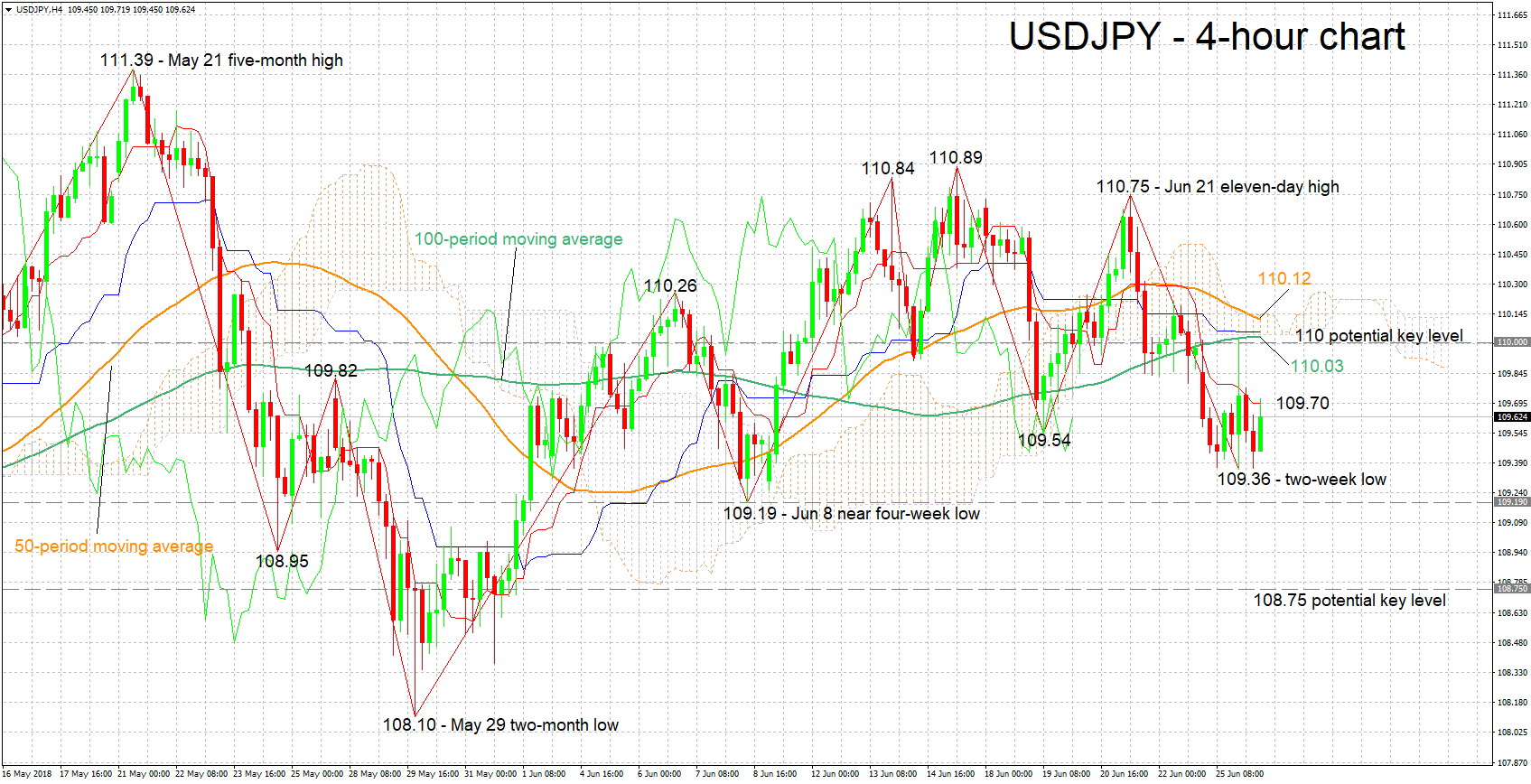

Technical Analysis: USDJPY bearish bias eases

USDJPY has gained some ground after reaching a two-week low of 109.36 during Monday’s trading. The bias remains to the downside as indicated by the negatively-aligned Tenkan- and Kijun-sen lines, though bearish momentum appears to have eased – this is also signaled by the flat Kijun-sen.

Intensifying trade tensions are likely to see the yen attracting safe-haven flows, thus weighing on USDJPY. Yesterday’s two week low of 109.36 may provide support to declines, with the near four-week low of 109.19 from June 8 lying not far below. Sharper declines will turn the attention to the region around 108.75 which experienced some congestion between late May and early June.

Easing tensions on the other hand are likely to boost USDJPY. Immediate resistance seems to be taking place around the current level of the Tenkan-sen at 109.70, with the focus next turning to the zone around the 110 round figure, which includes the current levels of the 50- and 100- period moving average lines (at 110. 12 and 110.03 respectively), as well as the Kijun-sen (110.06), and the Ichimoku cloud bottom (110.04) and top (110.14).

Consumer confidence data due out of the US can also lead to positioning on the pair.

Yuan Weakness Accelerates As Trade War Retaliation Concerns Support Japanese Yen

Concerns over the possibility of an upcoming trade war are expected to remain front and center of investor focus once again today. Although the trading atmosphere is not quite as negative as it was yesterday, clear indications of risk aversion in the financial markets remain. Global stocks are likely to remain pressured after a negative session on Monday, with emerging market currencies still feeling the brunt from a lack of risk appetite from traders. The Chinese Yuan, Malaysian Ringgit, Thai Baht, Indian Rupee and Indonesian Rupiah are once again trading lower against the Dollar, while the Japanese Yen is still outperforming as a result of investor reluctance to take on risk during an atmosphere of market uncertainty.

There have been some improvements in the Asian trading session, namely that some stocks have pared their losses in the region and both the Singapore Dollar and Korean Won are attempting to recover losses against the Dollar. Both of these currencies were negatively impacted by the spillover of trade war concerns from the end of last week. Of course, this sentiment could change very fast if there are any defensive comments made by either President Trump, Beijing or even the European Union about retaliating against trade tariffs. President Trump already warned on Sunday through Twitter that all countries need to remove their barriers and tariffs or 'be met with more than reciprocity by the U.S.A'.

Anxiety over how others might retaliate against the protectionist nature of Trump’s policies is likely to lead market sentiment throughout the week. The news that Harley-Davidson is planning to shift production away from the US in order to avoid European Union tariffs provides an indication over how major corporations are taking the trade war fears very seriously.

The Yuan has weakened once again on Tuesday, with the currency having now lost 3% in the last two weeks. There has been a noticeable acceleration in the speed of Yuan weakness in recent days, which is mounting speculation that the PBoC might be weakening the Yuan to offset some of the concerns over how the China economy could be impacted if a trade war does break out. The Chinese Yuan is now overall trading at its weakest level since December 2017.

What is most fascinating about the recent performance of the Chinese Yuan is how the currency has quickly transformed from one of the best performing emerging market currencies across the globe, to now trading over 0.7% lower year-to-date.

While it does appear coincidental that the momentum in the Chinese Yuan has taken a turn for the worse at the same time that trade war concerns have intensified, we also shouldn’t discount away the fact that there has been a broad-based USD rally across the FX markets over the second quarter. It is just as possible that the Yuan is playing catch up to the losses most global currencies have faced and following the same momentum of its emerging market counterparts, as it is that the weaknesses in the Yuan is a deliberate measure from authorities.