Sample Category Title

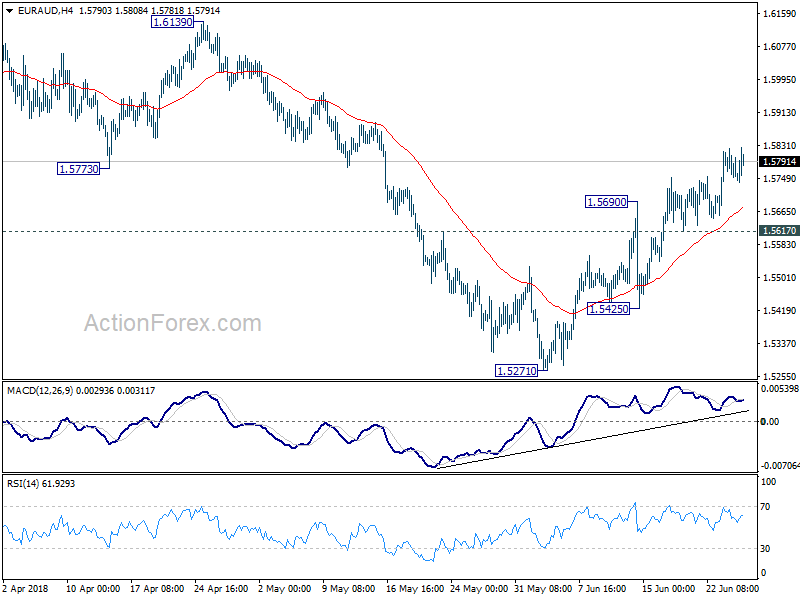

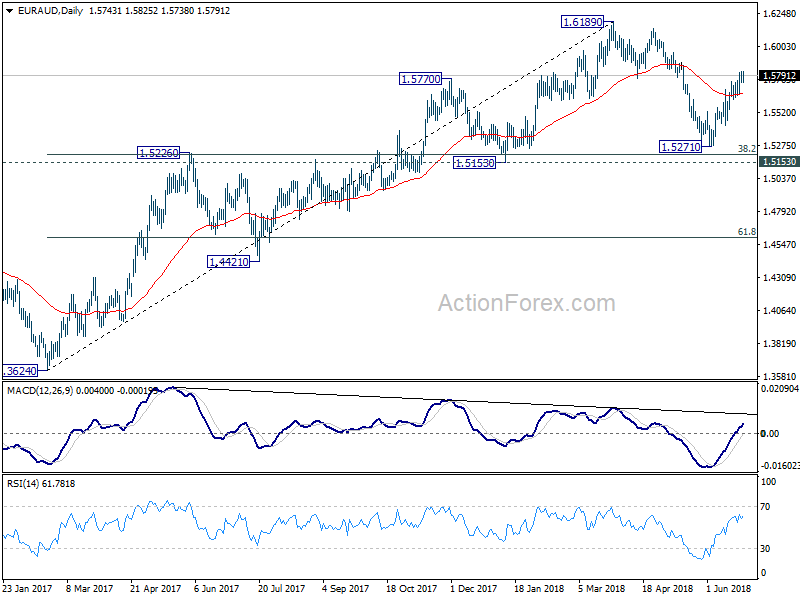

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5725; (P) 1.5775; (R1) 1.5809; More....

Intraday bias in EUR/AUD remains on the upside. Current rise from 1.5271 is target a test on 1.6189 high. On the downside, break of 1.5617 support is needed to indicate completion of the rise from 1.5271. Otherwise, outlook will now remain cautiously bullish in case of retreat.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And rise medium term rise from 1.3624 (2017 low) is not completed yet. Break of 1.6189 will target 1.6587 key resistance (2015 high).

AUD/USD Capped By A Negative Trend Line

Pivot (invalidation): 0.7400

Our preference Short positions below 0.7400 with targets at 0.7360 & 0.7345 in extension.

Alternative scenario Above 0.7400 look for further upside with 0.7420 & 0.7435 as targets.

Comment A break below 0.7360 would trigger a drop towards 0.7345.

USD/CAD Target 1.3330

Pivot (invalidation): 1.3290

Our preference Long positions above 1.3290 with targets at 1.3330 & 1.3345 in extension.

Alternative scenario Below 1.3290 look for further downside with 1.3275 & 1.3255 as targets.

Comment Technically the RSI is above its neutrality area at 50.

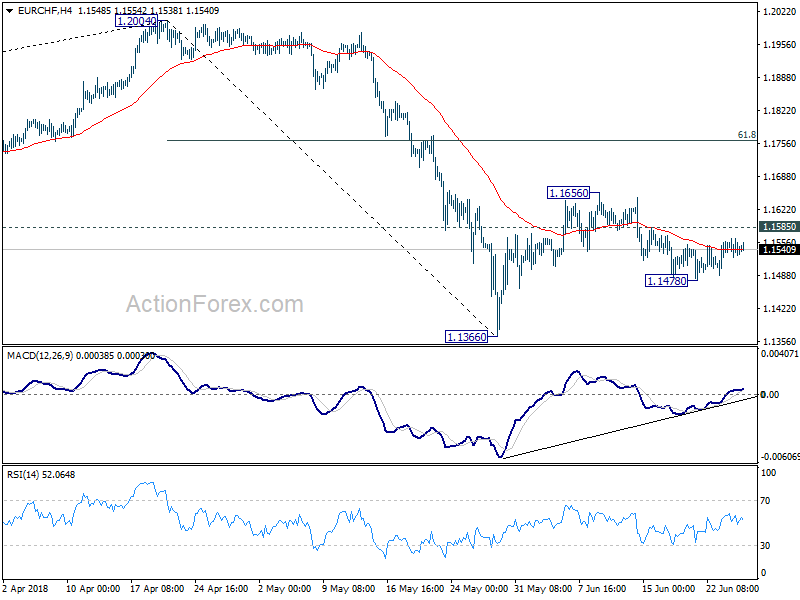

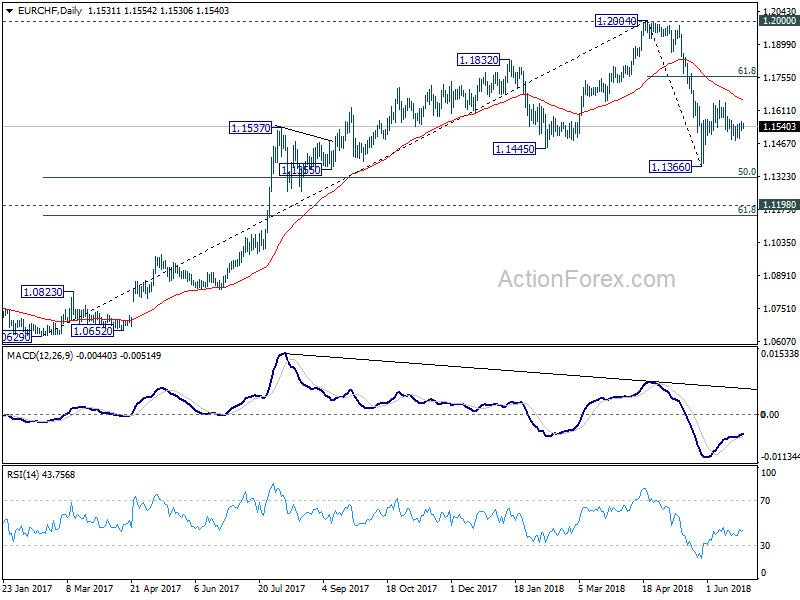

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1521; (P) 1.1543; (R1) 1.1561; More....

Intraday bias in EUR/CHF remains neutral at this point. Another fall is mildly in favor with 1.1585 minor resistance intact. Below 1.1478 will target 1.1366 first. Break will resume the larger corrective decline from 1.2004. On the upside, above 1.1585 will likely extend the rebound from 1.1366 through 1.1656. But in that case, upside should be limited by 61.8% retracement of 1.2004 to 1.1366 at 1.1760.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

USD/CHF Bullish Bias Above 0.9880

Pivot (invalidation): 0.9880

Our preference Long positions above 0.9880 with targets at 0.9925 & 0.9950 in extension.

Alternative scenario Below 0.9880 look for further downside with 0.9855 & 0.9830 as targets.

Comment Even though a continuation of the consolidation cannot be ruled out, its extent should be limited.

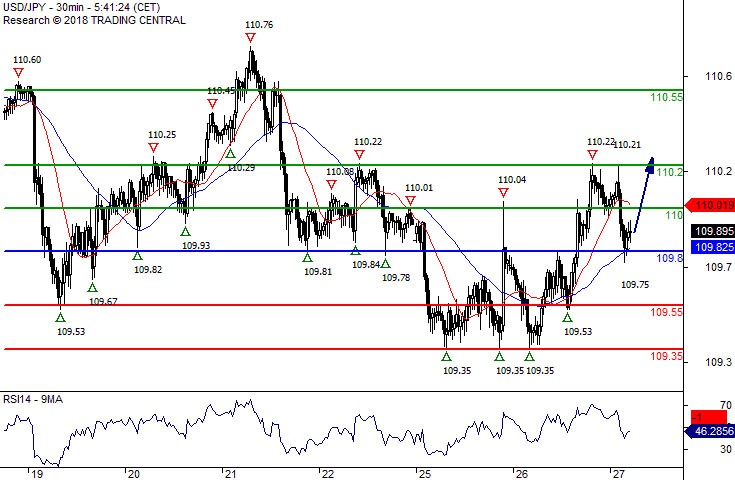

USD/JPY Caution

Pivot (invalidation): 109.80

Our preference Long positions above 109.80 with targets at 110.00 & 110.20 in extension.

Alternative scenario Below 109.80 look for further downside with 109.55 & 109.35 as targets.

Comment Intraday technical indicators are mixed and call for caution.

GBP/USD Under Pressure

Pivot (invalidation): 1.3255

Our preference Short positions below 1.3255 with targets at 1.3190 & 1.3145 in extension.

Alternative scenario Above 1.3255 look for further upside with 1.3290 & 1.3315 as targets.

Comment As Long as the resistance at 1.3255 is not surpassed, the risk of the break below 1.3190 remains high.

EUR/USD Under Pressure

Pivot (invalidation): 1.1685

Our preference Short positions below 1.1685 with targets at 1.1630 & 1.1600 in extension.

Alternative scenario Above 1.1685 look for further upside with 1.1720 & 1.1755 as targets.

Comment As Long as the resistance at 1.1685 is not surpassed, the risk of the break below 1.1630 remains high.

Bitcoin/Dollar The Downside Prevails As Long As 6206 Is Resistance

Our pivot (invalidation) point is at 6206.

Our preference The downside prevails as Long as 6206 is resistance.

Alternative scenario The upside breakout of 6206, would call for 6383 and 6488.

Comment The RSI is below its neutrality area at 50. The MACD is below its signal line and negative. The configuration is negative. Moreover, the pair is trading under both its 20 and 50 MAs (respectively at 6128 and 6177).

Potential U.S. Auto Import Tariffs: The View from Canada

The U.S. Commerce Department is considering imposing tariffs on U.S. auto imports, including from Canada. President Donald Trump is said to be eyeing tariffs in the 20% to 25% range. The ultimate decision on any tariffs (as well as the rate, countries targeted, etc.) will presumably depend on the findings of the Commerce Department's investigation. While the investigation could last up to nine months, the department is reportedly aiming to reach a conclusion sooner.

This latest trade threat could mostly disappear if a NAFTA resolution is reached. And it's hard to see any economic rationale for the U.S. imposing significant auto tariffs on Canada. Canada accounts for little of the U.S. auto trade imbalance and the tight integration of the North American auto sector means the U.S. auto industry would also be hurt. Nonetheless, if imposed, the U.S. tariffs would have a dramatic impact on the Canadian auto sector—and on Ontario, the centre of Canadian auto production—potentially lowering overall GDP in Canada by some 0.5%.

A U.S. auto import tax would hurt the sector it's meant to protect

The proposed auto tariffs differ from earlier actual tariffs the U.S. imposed on products including steel, aluminum, and softwood lumber in that there are no clear winners from the U.S. perspective. The criticism of those earlier tariffs (correctly) was that they would directly protect specific industries but raise costs for other manufacturers using these products as inputs, and ultimately hurt consumers. Imposing auto tariffs on Canada would have the same upward impact on U.S. prices but also would negatively impact the U.S. auto sector itself.

The North American auto sector is incredibly tightly integrated across national borders, more so than any of the industries that have faced a significant import tax so far under the Trump administration. As a result, a tax on U.S. auto imports would also quite directly act as a sizeable tax on U.S. exports. Consider that almost half of the value of Canada's finished motor vehicle exports to the U.S., and about a quarter of parts exports, are actually accounted for by the value of intermediate goods imported from the U.S. during the production process. OECD data show that the U.S. is actually one of its own largest auto import markets—bigger than Canada—once accounting for U.S. content in foreign country production chains.

U.S. auto factories don't have much room to expand

Even if highly integrated production chains could be disentangled—unlikely in the near term—the U.S. doesn't have much capacity to replace foreign-sourced vehicles with domestic production. Capacity utilization in the U.S. motor vehicle sector is already high, and with the U.S. unemployme nt rate sitting at multi-decade lows, labour is increasingly scarce. The most likely impact of auto tariffs would be higher costs to make motor vehicles and higher prices for North American auto buyers.

This still looks like a NAFTA negotiation tactic

Perhaps the only way the auto tariff investigation makes sense, at least in terms of potential tariffs on Canada, is to add pressure to reach a NAFTA deal favourable to the U.S. To be sure, U.S. anti-trade rhetoric has increased dramatically—and steel and aluminum If there is a problem with U.S. auto trade, it's not with Canada

Canada/US auto trade is roughly balanced. Using U.S. data, the total U.S. auto trade deficit last year was ~$US 190 billion. The deficit with Canada was 1% of that, or $US 2 billion. Canada is a large net importer of motor vehicles and parts overall. Canada's auto trade deficit was ~$C27 billion last year including non-U.S. trade partners. That partly reflects shifts in auto production and trade patterns within North America. Since the 2008/09 recession, Canada has lost share of final vehicle production to both the U.S. and Mexico. A decade ago, more than a quarter of U. S. auto imports came from Canada. Last year, it was less than 20%.

Canada's auto sector is not as big as it used to be

The Canadian auto sector accounted for about 14% of exports last year and 15% of manufacturing sales. The vast majority of Canadian auto exports go to the U.S. Those 'gross' flows, though, include the cost of imported intermediate inputs—and recall Canada runs a large auto trade deficit overall. Canadian 'value-added' production of motor vehicles and parts itself directly accounted for less than 1% of Canadian GDP and jobs last year. The share of GDP was closer to 2% in 1999/2000 but has been declining. In other words, any tariff impact could have a large impact on trade statistics but potentially a smaller, albeit still significant, impact on GDP/jobs numbers with a chunk of the total hit from reduced trade impacting U.S. rather than Canadian production.

For now, the risk is theoretical

What the U.S. investigation into auto tariffs will ultimately conclude remains very uncertain. There have been reports that the President wants to wrap up the investigation prior to the U.S. midterm elections in November but at this point nothing is imminent. An agreement on NAFTA—which still remains possible—would probably leave Canada exempt from any new auto tariffs.

In general, though, the auto sector is more vulnerable to a tariff hike than most other sectors. Tariffs are a tax on trade flows, not production, and the auto sector is the poster child for industrial integration across the Canada/U.S. border with intermediate goods crossing the border multiple times at different stages of production. A 2017 analysis from the CD Howe Institute found that Canada's automotive production would fall 5-10% in response to a theoretical across-the-board 10% U.S. tariff hike on all industries, depending on whether Canada were to retaliate or not. That's much larger than the 1% to 2% hit to the overall economy. On balance, we think it is reasonable to assume that significant auto tariff hikes could knock half a percent or so off of Canadian GDP relative to what otherwise might have been. That remains a theoretical risk at this point. But given the current climate on global trade, the threat won't help business investment spending in either Canada or the U.S.