Sample Category Title

Trump backs down on tough Chinese investment curb, revert to CFIUS

The markets are responding positive to news that Trump is backing away from the rumored harsh measure on curbing Chinese investments in US technology companies. Instead, his administration will revert to existing laws, with an upgrade. Trump himself told reports that "it's not just Chinese". Treasury Secretary Steven Mnuchin also said that "we are not singling out China, but we will protect technology transfer to China as we will to other important areas." Mnuchin also pledged that "we will have the necessary tools to protect investments, whether it's China or anybody else."

The administration will relay on the newly strengthened Committee on Foreign Investment in the United States (CFIUS) to deal with the issue. The legislation to be used is called the Foreign Investment Risk Review Modernization Act. Trump said the upgraded CFIUS"will enhance our ability to protect the United States from new and evolving threats posed by foreign investment while also sustaining the strong, open investment environment to which our country is committed and which benefits our economy and our people." And, "I have concluded that such legislation will provide additional tools to combat the predatory investment practices that threaten our critical technology leadership, national security, and future economic prosperity."

Trump originally considered invoking executive authority to impose and much tougher crackdown on Chinese investments. And there have been conflicting messages from White House trade adviser Peter Navarro and Mnuchin. But such an idea appeared to have drawn severe complaints from US businesses and Republicans, on the potential economic fallout.

US stocks futures reversed initial losses and now point to flat open. In particular, NASDAQ will be an index to watch today for its tech compositions. Dollar also jumps on the news, ignoring mixed economic data.

Dollar Bounces Up on Trade Relief News; Kiwi Holds onto Losses Ahead of RBNZ Rate Decision

Here are the latest developments in global markets:

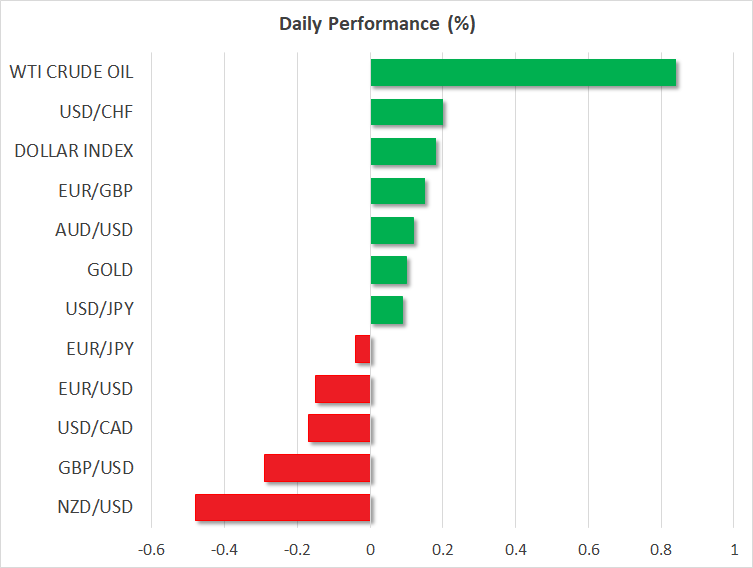

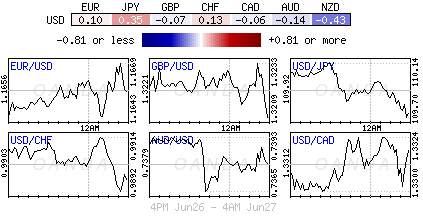

FOREX: Dollar/yen managed to recover earlier losses to climb back to 110.14 (+0.08%) as a US official messaged on Wednesday that Washington will not use stricter trade frictions against China but monitor Chinese investments through an existing national security review system. The dollar index also advanced to touch 94.79 (+0.14%), while investors were preparing their positions ahead of the durable goods orders later in the day and preliminary PCE inflation numbers on Friday. On the other hand, the euro was heading downwards as trade risks and political conditions in Germany continued to hang in the background. Euro/dollar moved lower to 1.1626 (-0.15%) before the EU summit kicks off on Thursday although Italy’s eurosceptic Senate, Alberto Bagnai said today that the government will not act against the euro. Pound/dollar remained in the negative ground, dropping below the 1.3200 handle (-0.10%) after the BOE Governor Carney highlighted risks from Brexit at his financial stability review presentation. He also argued that rising trade uncertainties could pull world interest rates back. Dollar/loonie was slightly up at 1.3310. Aussie/dollar held below its opening level around 0.7386 (-0.14%), while kiwi/dollar declined to 0.6820 (-0.61%) ahead of the RBNZ policy meeting overnight

STOCKS: European equities were in the green at 1200 GMT, with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 rising by 0.54% and by 0.65% repsectively. The German DAX 30 jumped by 0.97%, the French CAC 40 gained 0.74%%, while the Italian FTSE MIB moved up 0.66%. The UK’s FTSE 100 advanced by 0.81%. In Asia, equity markets closed in the negative territory with the exception of the Japanese Topix, while in the US, futures tracking the major stock indices were pointing to a positive open.

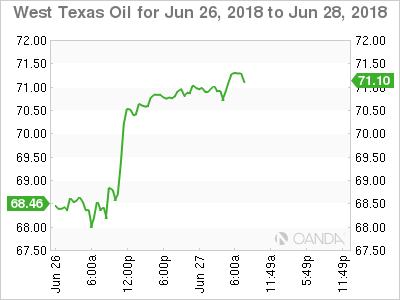

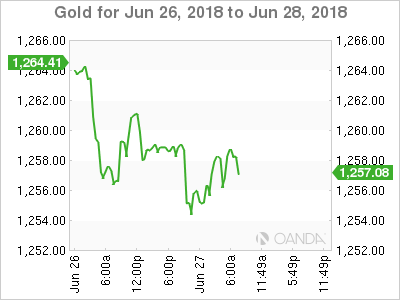

COMMODITIES: Oil prices had a significant winning day after yesterday’s API readings printed a much bigger inventory drawdown than analysts expected. Concerns over US sanctions on Iran were also supporting the market today. .West Texas Intermediate (WTI) oil surpassed $71 per barrel, posting a new one-month high and adding 0.78% to its daily performance. London-based Brent crude climbed by 0.48% to $76.68 per barrel. In precious metals, gold retreated by 0.21% to $1,257.43 per ounce, hitting a fresh six-month low of $1,253 early today.

Day ahead: US durable goods attract attention; RBNZ to hold rates steady but eyes on outlook

Durable goods orders and pending home sales out of the US will highlight the economic calendar later on Wednesday, while trade developments will continue to be closely monitored, with investors waiting eagerly to see whether the US will soften its protectionist stance against China.

At 1230 GMT, the US Census Bureau is expected to say that US durable goods orders have dropped by 1.0% m/m in May, by less than the 1.6% fall in the previous month, while in the absence of transport products the gauge is projected to record a growth of 0.5% m/m compared to 0.9% expansion in April. The non-defense core measure which excludes aircraft is also expected to slow down, easing from 1.0% m/m to 0.5%. Should the numbers surprise to the upside, calming concerns that the US trade frictions could cut back investments in the business sector, the dollar could attract some buying interest.

Separately, pending home sales due 1400 GMT are anticipated to increase by 0.5% m/m in May after a decline of 1.3% in the prior month.

Still, any deterioration or improvement in the trade situation could offset the impact of the above data.

Meanwhile, in oil markets, the EIA weekly report on US oil inventories could move prices at 1430 GMT. Recall that the API figures indicated a sharp downfall of 9.2mn barrels in US crude stocks in the week ending June 22, with crude prices hitting fresh highs in the wake of the data. In case the EIA figures unexpectedly show a bigger decrease than the 2.5mn decline currently priced in, then the market could post additional gains.

On the monetary policy front, the Reserve Bank of New Zealand will announce its decision on interest rates early on Thursday (Wednesday 2100 GMT). Analysts, though, are highly expecting policymakers to keep borrowing costs unchanged at 1.75% for the eleventh consecutive time as GDP growth in the first quarter weakened as expected, hinting that the economy is not ready yet to welcome a rate hike at times when risks around global trade are flashing red thanks to the US trade policy. Earlier today, New Zealand’s ANZ business confidence stats missed forecasts, retreating from -27.2% to -39.0%, the lowest since November. Therefore, given the data weakness, investors will turn their attention to the rate statement submitted along the rate decision to identify the RBNZ’s outlook on the economy. If the Bank turns more worried about the economy’s prospects (to avoid outlook twice), sending messages that a rate cut could still be on the cards, the kiwi could extend losses. Alternatively, if policymakers use a more hawkish tone, suggesting that the slowdown could be temporary, the local currency could reverse to the upside.

In terms of public appearances, Fed Vice Chair for Supervision Randal Quarles (1500 GMT – permanent FOMC voting member), Boston Fed President Eric Rosengren (1430 GMT – non-voter in 2018) and Bank of Canada Governor Stephen Poloz (1915 GMT) are some of the policymakers to deliver speeches later today.

UK Hammond to China: We’re a firm supporter of trade liberalization and your long-term trusted partner

UK Chancellor of Exchequer Philip Hammond wrote in an article in China's financial magazine Caixin, saying the the globalized UK is China's long term partner. Hammond is visiting Beijing this week and he pledges to "convey a message to the outside world - as a firm supporter of trade liberalization and a free market, the United Kingdom is China's long-term trusted partner."

Also, he wrote "Britain is committed to promoting free and open trade, and as Britain and its European cooperation partners form a new relationship, we will deepen our relations with other regions around the world." And, there was "enormous development space" with cooperation with Chinese financial services businesses. Hammond also hailed that UK is an "ideal cooperation partner" to the Belt and Road initiative, and they would likely to " grasp the unlimited opportunities" and "take a lead in its financing work."

This is Hammond's article in simplified Chinese (gated). We've yet to find the English version.

Canadian Dollar Steady, US Durable Goods Reports Next

The Canadian dollar continues to have an uneventful week. In the Wednesday session, USD/CAD is trading at 1.3316, up 0.10% on the day. On the release front, the sole Canadian event is a speech from BoC Governor Stephen Poloz. In the U.S, the focus is on durable goods orders. Core durable goods orders are expected to drop to 0.5%, while durable goods orders is forecast to drop -0.9%, which would mark a second straight decline. On Thursday, the U.S will publish Final GDP for the first quarter and unemployment claims.

As the second quarter draws to a close, the U.S economy continues to perform well. Economic growth has been strong and the labor market is close to capacity. However, the trade war between the U.S and its major partners could be the dark cloud on the horizon. The Federal Reserve now plans to raise rates four times in 2018 (up from three), but a global trade war could force the Fed to revise its forecast back to three hikes. On Tuesday, Atlanta Fed bank president Raphael Bostic said that if the trade war intensified, he would vote against a fourth rate hike, due to downside risks to the economy. Fed Chair Jerome Powell sounded pessimistic about the economic effects of trade tensions at an ECB forum earlier in June, and if other Fed members express concerns, the Fed could delay a fourth hike until 2019.

The Bank of Canada has dropped hints that it is ready to raise rates in the second half of 2018, but policymakers have concerns both internally and on the global stage. The escalating trade war between the U.S and China could have serious repercussions for the Canadian economy. President Trump hasn’t spared Canada from tariffs, and with 80% of Canadian exports headed to the U.S, Canada can ill-afford a trade spat with its giant southern neighbor. On the domestic front, Canadian consumer inflation and spending data was softer than expected. Retail Sales was dismal, with a sharp drop of 1.2 percent. Despite these soft numbers, the BoC remains confident about the economy, and a July rate hike remains a reasonable possibility. Inflation is still above the target of 2.0%, and in its May policy statement the BoC removed its reference to “cautious”, replacing it with “gradual” describing its approach to rate adjustments. The markets viewed this as a signal that the bank is preparing to press the rate trigger. A rate hike would likely boost the Canadian dollar, as it makes the currency more attractive to investors.

Forex Analysis: USDMXN

The rise in the USD against the MXN has been halted with a push down from resistance ahead of 21.00000 to the 50 DMA at 19.77420. Today the price is holding under 20.00000 after bouncing from the 50 DMA yesterday. This could be the start of a pattern but it is too early to tell and more data is needed to see whether the uptrend resumes or the selloff deepens. A breakdown of the 50 DMA or yesterday’s low could see selling continue. This would point to a retest of lower levels with the 19.4400 area being supported by the 100 DMA at 19.38127. A slip under this point would bring attention to the 19.14250 level with the 200 DMA close by at 19.08163.

The highs of February and March could see buyers step in around 18.96400/18.96900. A consolidation in this area down to 18.0000 could see a trading range develop further with a move back towards 20.50000 on the horizon. A break out higher above 21.00000 would target the 2017 high just above 22.00000. In the shorter term a turn higher from current levels would test 20.20390 followed by 20.50000 and 20.64170. The recent high remains in place at 20.94630.

DAX Halts Slide, Markets Eye EU Summit

The DAX index has reversed directions on Wednesday and is in red territory. In Tuesday’s North American session, the DAX is at 12,268, up 0.17% on the day. In economic news, there are no major eurozone events. On Thursday, EU leaders meet for a two-day summit in Brussels. Germany will release GfK Consumer Confidence and Preliminary CPI.

European equity markets remain under pressure, as investors cast a nervous eye on the escalating trade tariff between the U.S and its major trading partners. The DAX has lost 2.0% so far this week, and there is more downside if trade tensions worsen. On Friday, the EU slapped retaliatory tariffs of some 25% on $3.3 billion of U.S goods. This move was in response to U.S tariffs on EU steel and aluminum imports. President Trump didn’t blink and has threatened to impose 20% tariffs on EU vehicles. This threat sent automobile stocks on the DAX sharply lower on this week, as Daimler and BMW recorded steep declines. BMW exports cars from the U.S to China and Europe, so the trade battles could have a negative impact on the company’s revenues.

The markets are keeping a close eye on the EU summit. Key issues include EU immigration policy, the simmering trade dispute with the U.S, and the stalled Brexit negotiations. Investors will want to see some progress on these issues rather than the leaders highlighting their differences or bashing the Brits. Will EU leaders stick to their guns on the tariffs or offer Trump an olive branch? U.S tariffs will take a toll on the European export sector, and many EU members will want to lower the tensions with the Trump administration. On the Brexit front, the EU had said that it wanted issues such as the Irish border to be resolved by the June summit, but this won’t happen, and the EU will now have to set another deadline, with time running out. There have been various suggestions for a type of customs union arrangement between Ireland and Northern Ireland, but the May government is split on the issue, much to the frustration of EU leaders.

Stocks Decline On Trade Worries, Oil Rallies

Wednesday June 27: Five things the markets are talking about

Lingering concerns about trade is keeping global equities muted, although gains in oil prices have been supporting stocks of oil-and-gas companies.

Crude prices have built on yesterday's gains after the U.S. stepped up its pressure on Iran. West Texas Intermediate crude is trading atop of a one-month high, as Washington demanded that Iran's customers halt imports.

In currencies, China's yuan appears to have found a temporary floor after its rapid decline this week, while Japan's yen is again attempting to outperform it G10 counterparts, while sovereign bonds are found wanting.

On tap: RBNZ monetary policy decisions is this afternoon (05:00 pm EDT), while U.S personal spending is expected to have increased for a third consecutive month on Friday. On Saturday, China manufacturing and non-manufacturing PMI are due.

1. Stocks see red

Asian stocks closed lower across the board after Chinese equities fell into a ‘bear' market yesterday.

In Japan, the Nikkei share average dropped overnight after higher oil prices hurt rubber products makers, airlines and shippers, while companies' going ex-dividend added to the market's broader weakness. The benchmark Nikkei closed down -0.3%, while the broader Topix eked out a small gain of +0.02%.

Down-under, Aussie stocks faded late and left the S&P/ASX 200 with a fourth-straight decline of -0.03%. S Korea, both the Kospi and won collapsed overnight as the escalating U.S-China trade conflict dented investor sentiment. The index was down -0.38%.

In Hong Kong and China, stocks also fell to trade atop of their seven-month lows as the Yuan's slide adds to China growth fears. In Hong Kong, the Hang Seng index fell -1.8%, while the China Enterprises Index lost -2.2%.

In China, the CSI300 index fell -1.2%, while the Shanghai Composite Index lost -0.5%.

Note: China's yuan weakened beyond the psychologically $6.600 level and bets are growing for further downside amid the escalating Sino-U.S trade row.

In Europe, regional bourses remain under pressure as concerns over trade remain the theme of the risk off sentiment in markets.

U.S stocks are set to open in the ‘red' (-0.7%).

Indices: Stoxx50 -0.9% at 3,344, FTSE -0.3% at 7,520, DAX -0.6% at 12,158, CAC-40 -0.6% at 5,249; IBEX-35 -1.2% at 9,521, FTSE MIB -1.0% at 21,195, SMI -1.2% at 8,376, S&P 500 Futures -0.7%

2. Oil rises on supply losses and on U.S. push to isolate Iran

Oil prices are better bid on a supply disruption in Canada, falling U.S crude stocks, uncertainty over Libyan exports and after the Trump administration telling importers to stop buying Iranian crude from November.

Brent crude is up +30c a barrel at +$76.61, while U.S light crude is +25c higher at +$70.78.

A supply outage at Syncrude in Canada has locked in +350K bpd of crude, with repairs expected to last at least through the end of next month.

Note: The fall in Canadian exports has helped drain supplies of heavy crude across North America and contributed to a major draw in U.S. crude oil inventories according to Analysts.

U.S API data yesterday reported a much-higher-than-expected -9.2M barrel reduction in U.S crude inventories in the week to June 22 to +421.4M barrels.

Also keeping markets on edge was the risk of a disruption to oil supplies from the Africa and the Middle East.

Ahead of the U.S open, gold prices have hit a seven-month low as the U.S dollar steadied and investors turned to other safe-haven assets amid expectations of more interest rate hikes by the Fed. Spot gold fell for a third straight session and is down -0.3% at +$1,255.51 an ounce. U.S gold futures for August delivery are -0.2% lower at +$1,257.30 per ounce.

3. Sovereign yields fall on risk aversion trading

Global sovereign yields remain under pressure, mostly on trade tensions.

The yield on Germany's 10-year Bund remains under pressure after E.U leaders failed to reach a deal on a new approach to immigration. The 10-year Bund yield fell -2 bps to +0.31%.

For further directional cues, dealers will now look to the E.U summit on immigration this Thursday and Friday as well as Friday's release of eurozone inflation numbers, which could see core inflation, drop to +1%.

Elsewhere, the yield on 10-year Treasuries fell -2 bps to +2.86%, the lowest in more than three-weeks, while in the 10-year Gilt yield fell -3 bps to +1.273%.

There is only one central bank meeting this week and its today's RBNZ monetary policy announcement (05:00 am EDT) where they are expected to deliver a ‘dovish' tone and signal again that the next move could be “up or down.”

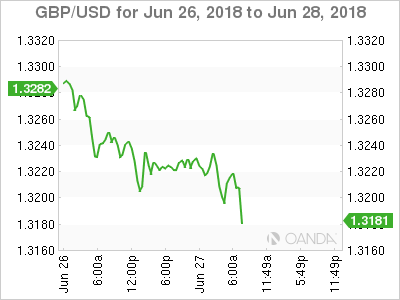

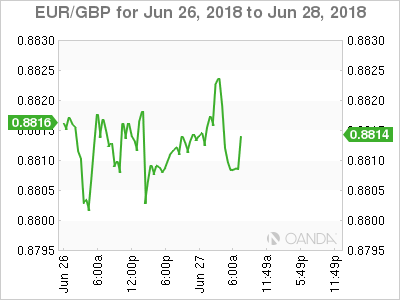

4. Sterling falls as uncertainty grows over BoE outlook

Sterling remains under pressure (£1.3210), remaining weak after yesterday's testimony from incoming BoE policymaker Jonathan Haskel was taken as a suggestion that he is not inclined to raise interest rates. The intraday low overnight was £1.3196. EUR/GBP is up +0.1% to €0.8811

Note: He is set to replace Ian McCafferty, who has consistently voted to increase rates in recent months. Many expect the BoE to hike rates in August, though many investors are nervous given economic and Brexit-related uncertainties.

The People's Bank of China (PBoC) set the dollar's reference rate at ¥6.5569 yuan, which meant the yuan was -0.6% lower than the previous session. The “fix” put the yuan at its weakest level since Dec. 25, 2017.

EUR/USD (€1.1642) remains confined to a tight range in quiet trading. Focus will now turn to key Euro inflation data – German CPI on Thursday and E.U Flash CPI on Friday.

Note: Chancellor Merkel's German coalition failed to find an agreement of the migrant issue ahead of the upcoming E.U leader summit beginning tomorrow.

5. Eurozone bank lending picks up

The recovery in eurozone bank lending continued in May.

Data from the European Central Bank (ECB) saw lending to non-financial corporations grow at an annual rate of +3.6% in May, which marks the highest rate in nine-years. In April it was +3.3%.

Digging deeper, lending to eurozone households was also robust. It grew at an annual rate of +2.9% in May, the same rate as in April, according to the ECB.

Nevertheless, despite the pick up in lending across sectors, lending rates remain well below pre-crisis levels. In 2007, bank lending to businesses was running at rates well above +12%.

The ECB's key indicator of the money supply, meanwhile, picked up unexpectedly, with the annual growth rate of M3 rising to +4.0% from +3.8% in April.

USDJPY Selling Preferred Below 110.00

The US dollar continues to trade in an increasingly narrow trading range against the Japanese yen currency, as investors await key US economic data. The USD/JPY pair remains weak while trading below the 110.00 level, as trade tariff tension between the United States and China linger. Buyers need to once again move price above the 110.00 level, while sellers will need to keep price below the 109.54 level.

The USDJPY pair is intraday bearish while trading below the 110.00 level, further downside towards the 109.54 and 109.00 seems possible.

If the USDJPY pair moves above the 110.00 level, buyers will likely test towards the 110.25 and 110.40 resistance levels.

EURUSD Further Bearish Below 1.1628 Level

The euro has fallen to a fresh weekly trading-low against the greenback, after a strong technical rejection from the key 1.1674 resistance level earlier today. The EUR/USD pair is also under pressure from intraday strength in the US dollar Index, as it approaches the 95.00 level once again. Sellers now look to further losses below the 1.1628 level, while buyers need to move price back towards the 1.1674 level.

The EURUSD pair is further bearish while trading below the 1.1628 level, key support is located at the 1.1600 and 1.1540 levels.

If EURUSD buyers can move price back above the 1.1674 level, key resistance is found at the 1.1700 and 1.1724 levels.

Risk Aversion Continues, Oil Climbs Ahead Of Inventories

- Trade war fears remain;

- Oil edges higher ahead of EIA release.

Financial markets are once again in risk aversion mode on Wednesday, as investors continue to take shelter from the ongoing trade spat.

There hasn’t been much progress – positive or negative – in recent days although US Treasury Secretary Steve Mnuchin did deny reports that the country is looking to block investment from China in US tech, instead claiming there will be a statement aimed at all countries trying to steal technology. Given related comments from the Trump administration, it would be safe to assume this primarily targets China but clearly there is a desire to involve others as well.

While this appears to neither escalate nor de-escalate the trade dispute the US is raising with a number of countries, it is yet another reminder that Trump is not softening his stance and instead continuing to double down on efforts to pressure countries into submission, something that does not appear to be working yet. There is clearly still a long way to go so traders should get used to the hostile and potentially risky environment we now find ourselves in.

The question is whether markets will respond as they often do, which is to be very sensitive to early exchanges before becoming less susceptible to verbal threats and tit-for-tat exchanges. With US futures in the red and European markets trading with a slightly negative tone, we’re clearly not there yet, although the Dow is still just under 4% from this year’s low, the S&P 500 just under 8% and the Nasdaq only a week ago hit a new record high.

Oil is continuing to climb in European trade after a US state department official claimed they are pushing allies to cut oil imports from Iran to zero. This comes at a time when supply disruptions in some countries such including Venezuela is already weighing on output. Last week, OPEC and some non-OPEC producers that participated in the 1.8 million barrel a day output cut in recent years agreed to pump an extra million barrels a day, something traders appear to feel will be difficult to achieve.

API also reported a 9.228 million barrel draw down in inventories on Tuesday which is the biggest drop since January and, if confirmed by EIA today, would far exceed expectations and be the biggest decline we’ve seen since September 2016. This could provide further support to Brent and WTI crude which are once again quite elevated and not trading far from their recent highs, despite the agreement last week.

Also being released today is durable goods orders and pending home sales. There’s also appearances from more Federal Reserve officials, including Randal Quarles – a permanent voter on the FOMC – and Eric Rosengren – a voter next year