Sample Category Title

Canada retail sales dropped -1.2%, ex-auto sales dropped -0.1%, core CPI moderated

Canadian Dollar drops sharply after very weak retail sales data. Headline sales dropped -1.2% mom in April versus expectation of 0.0% mom. Ex-auto sales dropped -0.1% mom versus expectation of 0.2% mom.

Inflation data is not helping neither. CPI rose 0.1% mom, 2.2% yoy in May, below expectation of 0.4% mom, 2.6% yoy. CPI core common was unchanged at 1.9% yoy. CPI core median dropped to 1.9% yoy, down from 2.1% yoy. CPI core Trim dropped to 1.9% yoy, down from 2.1% yoy.

USD/CAD resumes recent rally after brief retreat, and is on course for 1.3404 projection level.

Oil Stays Bullish as OPEC Seen Near Agreement; Euro Cheers on Upbeat PMIs

Here are the latest developments in global markets:

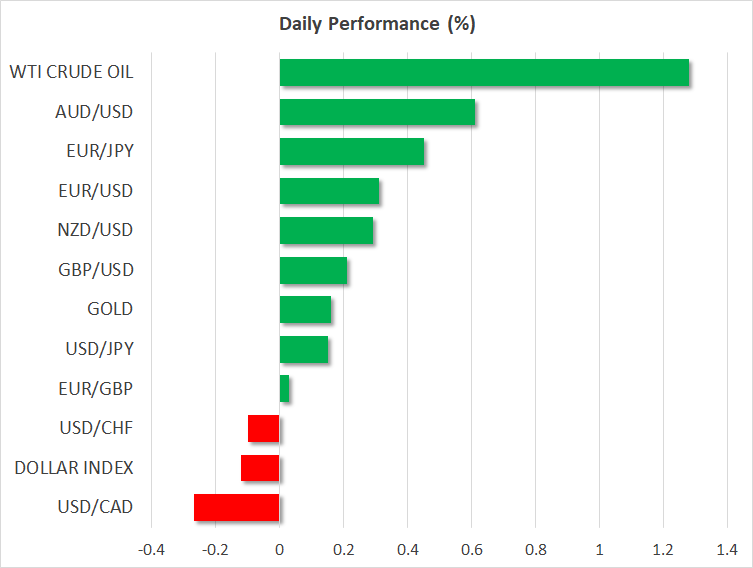

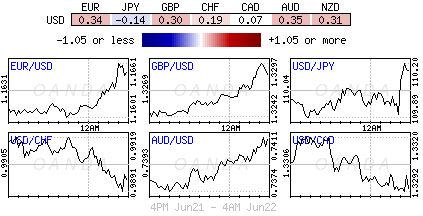

FOREX: Dollar/yen was posting moderate gains on Friday, inching up to 110.14 (+0.14%) as uncertainties around US-Chinese trade relations were still high. The two giant world exporting economies exchanged additional threats of import tariff measures this week, with the Chinese Ministry of Commerce characterizing US trade protectionism on Friday as “self-defeating and a symptom of paranoid delusions”. The dollar index was down for the second day, last seen at 94.62 (-0.12%) as the euro and the pound remained in bullish mode. Euro/dollar jumped to a one-week high of 1.1675 before it slid to 1.1637 (+0.31%) as preliminary Manufacturing and Services PMI figures of the Eurozone surprised to the upside. Meanwhile, in Germany, sources stated that Merkel’s coalition party, the SPD, was discussing the prospect of new elections last week. Euro/yen printed a stronger rally, breaking the 128 key-level to hit a session high of 128.58 (+0.44%). Demand for the pound continued to increase as well following an unexpected shift in BoE rate votes yesterday, with three out of nine policymakers backing a rate rise compared to two back in May. The move increased speculation that policymakers could feel more confident to push borrowing costs up in August. Euro/pound edged to 0.8755 (-0.05%). In antipodean currencies, aussie/dollar and kiwi/dollar were recovering, with the former bouncing up to 0.7426 (+0.65%) and the latter heading up to 0.6895 (+0.31%). The commodity-linked dollar/loonie retreated to $1.3275 ahead of the release of Canadian CPI data later today, weighed on by increasing oil prices.

STOCKS: Stronger-than-expected PMI data out of the eurozone helped European stocks to move higher on Friday at 1100 GMT, with the pan-European STOXX 600 and the blue-chip STOXX 50 both being up by 0.77% and 0.87% repsectively, led by financials. The German DAX 30 gained 42%, the French CAC 40 climbed by 0.85%, while the Italian FTSE MIB surged by 1.11%. The Spanish IBEX 35 and UK’s FTSE 100 rose by 0.82% and by 0.98% respectively. In Asia, equities closed mixed, while in the US, futures tracking the major indices were in the green, pointing to a positive open.

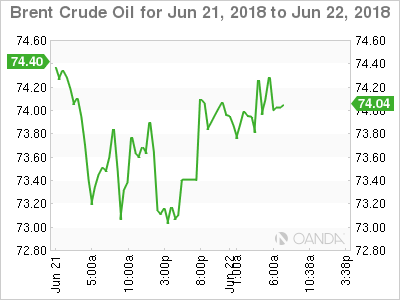

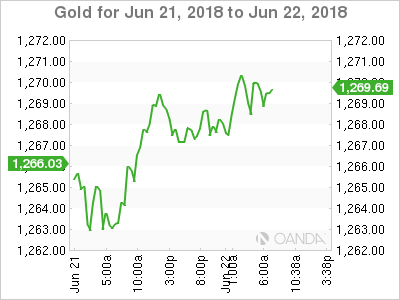

COMMODITIES: Oil prices stretched higher on Friday after OPEC and its allies were said to have cooked a deal of a 1 million output hike at the early stage of the meeting which concludes on Saturday. Speaking from Vienna, the Saudi Arabian oil minister, Khalid al-Falih messaged that the majority of his colleagues are supporting a gradual and a pro-rata output increase. WTI crude and Brent were last trading at $66.46/barrel (+1.40%) and at $74.09 (+1.46%) respectively. In precious metals, gold was higher at $1,269/ounce (+0.24%).

Day Ahead: Spotlight events of the day are OPEC meeting & Canadian CPI

All eyes today will be on Vienna, where the Organization of the Petroleum Exporting Countries (OPEC) and major non-OPEC oil producers including Russia are gathering to review a supply cut agreement signed in December 2016. OPEC, Russia, and several other non-OPEC producers agreed to cut output by 1.8 million bpd starting from January 2017, to support oil prices, which had more than halved by that time, notably due to global oversupply and increasing US shale production. Now, the media reports suggest supports that the meeting is close to delivering a supply hike of 1mn barrels per day (bpd), probably persuading Iran, who recently warned to veto any output increase, to collaborate.

Also, another main event will be in Canada, where data on inflation and retail sales are scheduled to be published at 1230 GMT. The headline inflation rate for May is forecasted to rise by 2.5% y/y versus 2.2% previously, however, month-on-month the rate is expected to remain steady at 0.3%. April’s retail sales are expected to tick down to 0.0% m/m versus 0.6% in the prior month, the lowest since December 2017. Core retail sales, which exclude automobiles, are projected to grow by 0.5% m/m from -0.2% before. If the stats beat expectations, then the Canadian dollar could extend today’s gains even further.

Out of the US, at 1345 GMT, Markit’s preliminary PMIs for the month of June might also attract some attention. Analysts are expecting the Manufacturing PMI to tick lower to 56.5 compared to 56.4 before, while the service index is anticipated to inch lower by 0.4 points to 56.4. The composite flash reading is forecasted to decline to 55.1 versus 56.6 previously.

In energy markets, the US Baker Hughes oil rig count is due at 1700 GMT, however, the most important event for investors is the OPEC two-day meeting.

Canadian Dollar Edges Higher ahead of CPI, Retail Sales

The Canadian dollar is showing slight gains in the Friday session. Currently, USD/CAD is trading at 1.3279, down 0.28% on the day. On the release front, Canada will publish key consumer data. CPI, the primary gauge of consumer spending, is expected to edge up to 0.4%. The markets are expecting mixed signals from retail sales reports. Core retail sales are expected to rebound to 0.5%, but retail sales is forecast to slip to 0.0%. There are no major events in the U.S.

The Canadian dollar is struggling, and June is likely to be the currency’s worst month since February. USD/CAD has gained 2.5% this month, as fears of a global trade war have soured investor appetite for minor currencies like the Canadian dollar. Canada is particularly vulnerable to protectionist moves by the United States, as some 80% of Canadian exports go to the U.S. A tight trading relationship between Canada and the U.S, anchored by the NAFTA agreement, hasn’t prevented President Trump from imposing tariffs on Canadian steel and aluminum. With the NAFTA talks showing little sign of progress, Trump has threatened to impose tariffs of 25 percent on Canadian-built vehicles. Such a move would be disastrous for the Canadian automotive sector, which is worth some C$80 billion to the economy every year. The Trudeau government has promised to help sectors hit with US tariffs, but bailing out the auto industry would cost billions. Canada may have to provide the U.S with more concessions in the NAFTA negotiations, in order to stave off tariffs against Canadian vehicles, which could have a disastrous effect on economic growth.

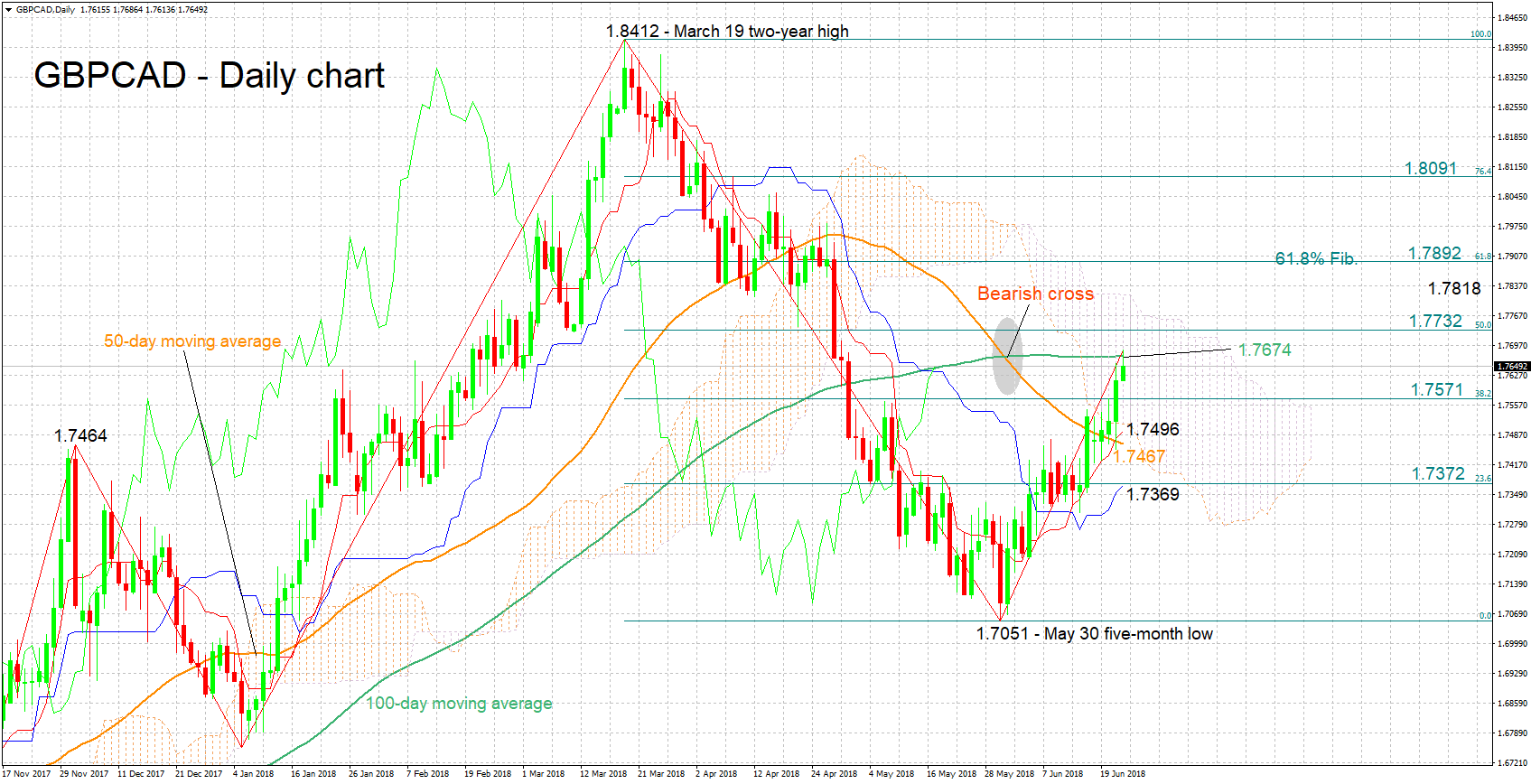

GBPCAD Hits 8-Week High, Looking Neutral In The Medium-Term

GBPCAD has been on the rise since effectively late May, after touching a five-month low of 1.7051 on May 30. Earlier on Friday, the pair reached an eight-week peak of 1.7686.

The positively-aligned Tenkan- and Kijun-sen lines are confirming the view for the existence of a bullish bias in the short-term. In addition, the fact that the two lines are steeply heading higher suggests that bullish movement in the near-term has still room to run.

The area around the current level of the 100-day moving average at 1.7674 seems to be acting as an immediate barrier to price advances; note that the 100-day MA was momentarily violated earlier in the day. An upside break off this region, would turn the attention to the area around the 50% Fibonacci retracement level of the March 19 to May 30 downleg at 1.7732, and then to the Ichimoku cloud top at 1.7818.

On the downside, support could come around the 38.2% Fibonacci mark at 1.7571, and further below from the zone around the current level of the Kijun-sen at 1.7496, which also encapsulates the Ichimoku cloud bottom at 1.7514 (and consequently the 1.75 round figure).

In terms of the medium-term picture, the price action over roughly the last three weeks has defied the negative signal given by the bearish cross recorded in late May, when the 50-day MA moved below the 100-day one. Instead, the outlook is looking predominantly neutral, with trading activity taking place inside the Ichimoku cloud. If the positive movement continues though, with the price moving above the 100-day MA and subsequently breaking above the cloud, then that would mark a bullish tilt in terms of the medium-term outlook.

Overall, the short-term picture is bullish at the moment, and the medium-term one is looking mostly neutral.

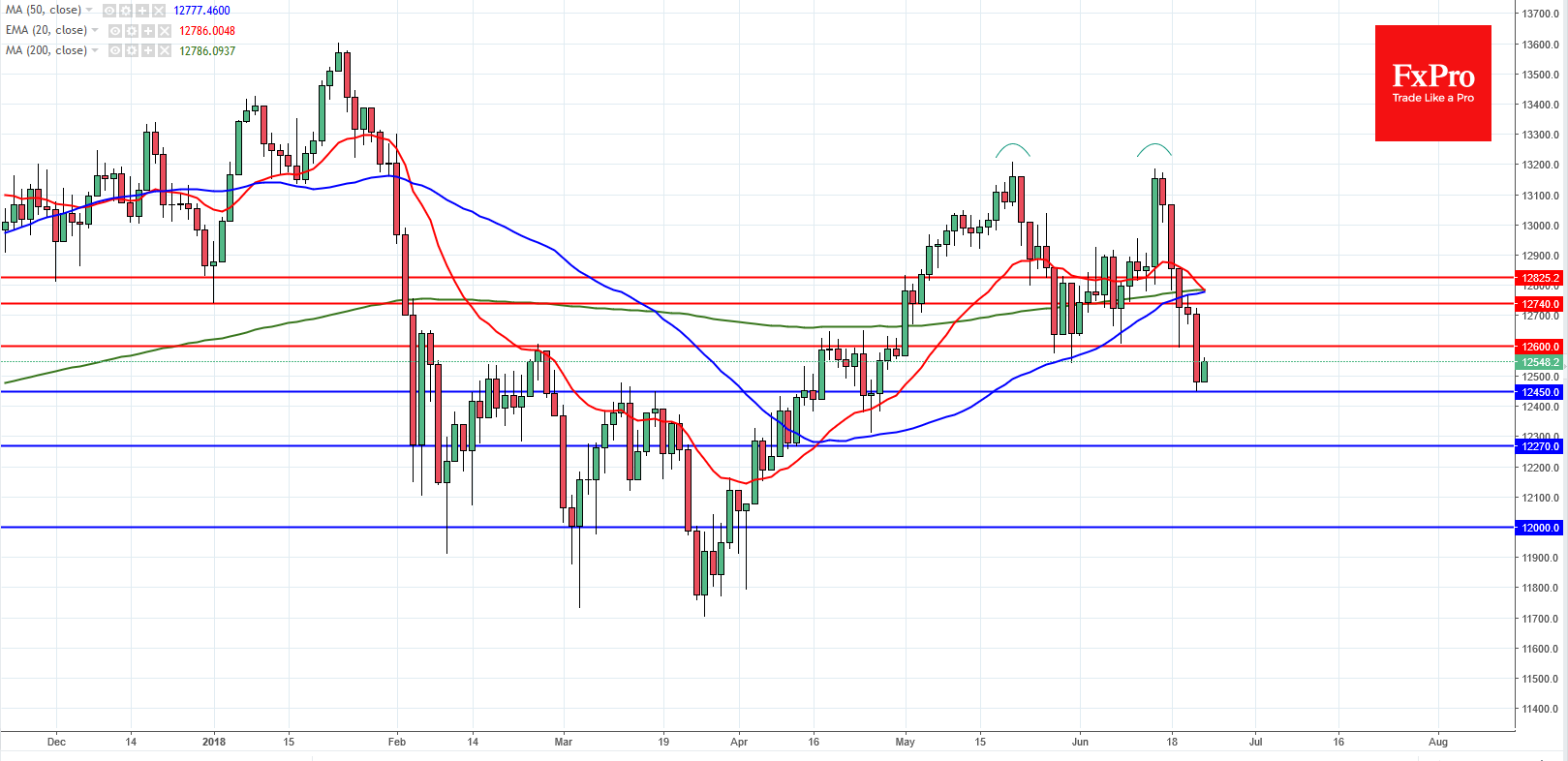

DAX Steady, But Trade War Fears Hang Over Markets

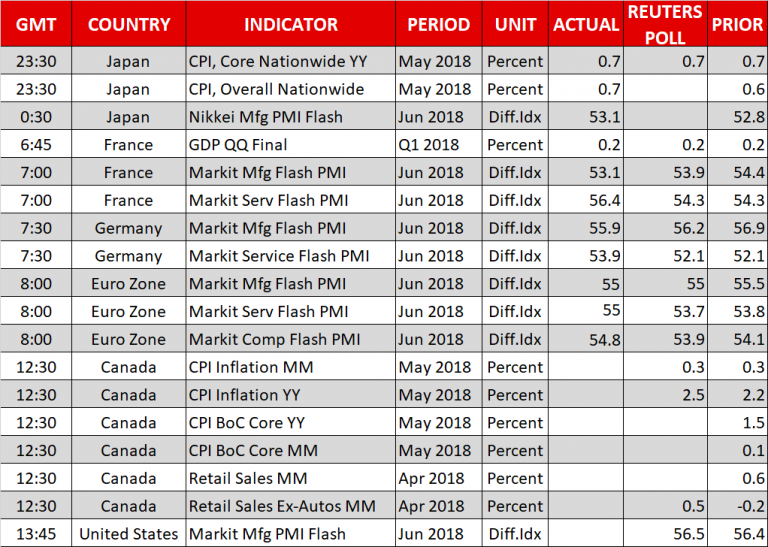

The DAX index has posted gains in the Friday session, after sharp losses on Thursday. Currently, the DAX is at 12,567, up 0.45% on the day. On the release front, the markets are digesting June PMI reports. Germany and the eurozone posted Services PMIs of 53.9 and 55.0, respectively, both of which beat the estimates. On the manufacturing front, German Manufacturing PMI dropped to 55.9, missing the estimate of 56.3 points. Eurozone Manufacturing PMI softened to 55.0, matching the estimate. Later in the day, OPEC members meet in Vienna to discuss a proposal to raise oil production.

The eurozone economy continues to perform fairly well, led by the robust German economy. PMI indicators are important barometers of the health of the economy. The good news is that services and manufacturing PMIs continue to indicate expansion in both the eurozone and Germany. However, this is not the entire story, as both manufacturing PMIs slowed for a sixth straight month, and the German release was the weakest since December 2016. With global protectionism on the rise as the trade war worsens, German and eurozone exports could suffer, which in turn would have a negative impact on manufacturers. If upcoming PMIs continue to weaken, investor confidence in the eurozone could wane and weigh down the already fragile European equity markets.

The escalating global trade war has taken a toll on the stock markets, and nervous investors had a chance to listen in on the heads of the U.S and EU central banks, who met at the ECB forum this week. Mario Draghi and Jerome Powell sounded gloomy about the recent protectionist moves, which were triggered by the U.S imposing tariffs on China, the EU and other trading partners. Powell saying that the changes in trade policy would have a negative effect on business hirings and investment, and could force the Fed to question its economic outlook. Mario Draghi said that the trade spat could have negative consequences on monetary policy. Although both central bankers didn’t provide any specifics, their apprehension over the rash of new tariffs is unmistakable. If the trade spat worsens and forces central banks to alter their monetary policy, this could have a significant impact on equity markets.

Forex Analysis: DAX And FTSE 100

European stock indices are under pressure due to the threat of euro-sceptic policies in Italy and the impact of protectionism on a global economy. Trade tension remained in focus as the heads of several major central banks expressed concern over the impact it may have on the global economy. German car maker Daimler in a profit warning on Thursday said that sales of its Mercedes-Benz SUVs would suffer from fresh tariffs on cars exported from the U.S. to China. That prompted shares of other German automakers to fall as well.

DAX

On the daily chart, the DAX (Germany30) index broke a major horizontal support at the 38.2% retracement from the lows of March at 12600. There is now a possible double top with a measured target of 12000. The index will find support at 12450 and the 12270. The DAX needs to close back above 12600 to change the outlook with resistance at 12740 and 12825.

FTSE

On the daily chart, the FTSE 100 (UK100) was driven lower by the strength in the British Pound after the Bank of England interest rate announcement yesterday. The index has now found support at 7550 and a break could lead to more downside with support at the 38.2% retracement 7500 and then 7340. A reversal above 7630 is needed for a move back to the June highs near 7770.

Markets Brace For OPEC Showdown In Vienna

There seems to be a growing sense of uncertainty over what to expect from today’s OPEC meeting in Vienna, given the disagreements among major Oil producers around whether to boost output.

While Saudi Arabia and Russia have proposed to ease supply curbs, other members including Iran, Iraq, Algeria and Venezuela are against such a move. With Iran already storming out of preparatory discussions yesterday, investors should fasten their seat belts in preparation for potential fireworks today. If Iran continues to reject the deal to raise output and gathers support from other cartel members, talks are at risk of ending in an impasse. Such an undesirable outcome is likely to create uncertainty and will spark fears over the future of OPEC’s 18-month agreement with Russia to limit production. A market-friendly outcome could be a scenario where Iran makes a last-minute U-turn to cooperate, consequently allowing Saudi Arabia and Russia to move forward with a gradual production increase.

Will OPEC manage to agree on a production increase? This remains a recurrent question on the minds of most investors. Whatever the outcome of the OPEC meeting in Vienna, it will most likely leave a lasting impact on Oil prices.

Currency spotlight – Dollar

The Dollar has extended losses against a basket of major currencies today, easing from an 11month peak as investors engaged in a bout of profit taking. There is a suspicion that the disappointing Philly Fed manufacturing index, which fell to a 19-month low, also played a role in the Dollar decline with prices trading marginally below 94.50 at the time of writing. While the Dollar has scope to venture lower in the short term as bears exploit the weaker economic data to drag prices lower, losses may be limited by US rate hike expectations.

Moving the focus away from the fundamentals, the technical picture remains heavily bullish on the daily charts despite the recent declines. A technical correction could be in play with the next key level of interest on the Dollar Index around the 94.00 region. If bulls are able to defend 94.00, then the Dollar Index has scope to rebound back towards 95.00 and 95.35, respectively.

Commodity spotlight – Gold

Gold is poised to conclude this trading week negatively, as a broadly stronger Dollar and the prospect of higher US interest rates continue to erode appetite for the precious metal.

Although prices have attempted to rebound higher today, this has less to do with a change of sentiment towards Gold and more to do with Dollar weakness amid profit taking. While the safehaven asset could receive some support as uncertainty mounts ahead of the OPEC meeting this afternoon, gains could be capped below $1280 resistance level. With the fundamental drivers behind Gold's depreciation still in place, further weakness could be seen in the medium to longer term.

Euro Area PMI Data Suggest That Q2 GDP Growth Will Rebound

Notes/Observations

- Major European Jun PMI data mixed but remaining in expansion territory to help paint a picture that Q2 activity has rebounded (Manufacturing missing for France, Germany while Services and Composite beat across the board)

- OPEC bi-annual meeting expected to be the most contentious in years; official start delayed as Saudi-Iran minister meet privately

Asia:

- Japan Jun Preliminary Manufacturing PMI: 53.1 v 52.8 prior; first time since August 2016, new export orders declined

- Japan May National CPI Y/Y: 0.7% v 0.6%e; CPI (ex-fresh food (Core) Y/Y: 0.7% v 0.7%e

- Japan ruling LDP party said to plan leadership election on Sept 20th

Europe:

- BOE Gov Carney’s annual Mansion House speech: preparing for new global financial system

- Greece creditors agree on debt relief package (as speculated). Agreement said to include 10-year extension of EFSF loan and a 10-year deferral on interest and amortization. Greece to receive €15B as its final bailout disbursement leaving the country with €24.1B cash buffer as its exit bailout program. Greece to have independence form market borrowing for some 22 month

- IMF Lagarde: Debt relief measures announced today to improve Greece's medium-term debt prospects, mitigate refinancing risks. IMF to examine the sustainability of Greece's debt starting next week (Jun 25th) and remain 'fully engaged' in supporting Greece. IMF fund will not join the expiring €86B bailout as the time “has run out”,

- Germany BDI Industry Body: UK is heading for a 'disorderly exit' from the EU

Americas:

- Fed Bank Stress Test Results: All 36 banks exceed minimum capital requirements. most severe hypothetical scenario projects $578B in total losses for the 35 participating bank holding companies during the nine quarters tested.

- Mexico Central Bank (Banxico) raised its Overnight Rate by 25bps to 7.75% (as expected)

- Some Trump administration officials reportedly pushing to resume trade talks ahead of China implementing tariffs on July 6th; advisers still at odds over strategy

Energy:

- OPEC and its allies said to have reached a preliminary agreement in the face of strong opposition from Iran. OPEC and its allies look to increase oil output by 1.0M barrels a day, (analysts estimates that the actual increase would be lower (more likely in a range between 600-800K bpd).

Economic Data:

- (NL) Netherlands Q1 Final GDP Q/Q: 0.6% v 0.5%e; Y/Y: 2.8% v 2.8%e

- (FR) France Q1 Final GDP Q/Q: 0.2% v 0.2%e; Y/Y: 2.2% v 2.2%e

- (FR) France Q1 Final Wages Q/Q: 0.7% v 0.7% prelim

- (FR) France Jun Preliminary Manufacturing PMI: 53.1# v 54.0e (21st month of expansion), Services PMI: 56.4 v 54.3e, Composite PMI: 55.6 v 54.2e

- (DE) Germany Jun Preliminary Manufacturing PMI: 55.9 v 56.3e (42nd month of expansion and lowest since Dec 2016), Services PMI: 53.9 v 52.2e, Composite PMI: 54.2 v 53.4e

- (CN) Weekly Shanghai copper inventories (SHFE): 255.4K v 253.0K tons prior

- (EU) Euro Zone Jun Preliminary Manufacturing PMI: 55.0 v 55.0e (59th straight month of growth but lowest since Dec 2016), Services PMI: 55.0 v 53.8e, Composite PMI: 54.8 v 53.9e

- (RU) Russia Narrow Money Supply w/e Jun 15th: 10.18T v10.06 T prior

- (TW) Taiwan May Unemployment Rate: 3.7% v 3.7%e

- (HK) Hong Kong Q1 Current Account: $16.3B v $16.0B prior; Overall Balance of Payments (BoP): $73.8B v $73.5B prior

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.5% at 382.8, FTSE +0.5% at 7597, DAX +0.4% at 12556, CAC-40 +0.7% at 5353, IBEX-35 +0.8% at 9781, FTSE MIB +1.0% at 21891, SMI +0.8% at 8523, S&P 500 Futures +0.5%]

- Market Focal Points/Key Themes: European Indices trade higher across the board following prelim PMI data out of Europe, ahead of the OPEC meeting in Vienna. News flow has been light, with Hornbach trading lower after lower y/y profit, while Airbus trades higher after providing commentary regarding Brexit. In the M&A BPER trading higher after Unipol acquired a further stake in the company, NN Group sold its Dutch residential real estate portfolio for €1.5B, while Hispania Activos Inmobiliaros trades higher after Alzette raised its offer for the company. In the Healthcare space Nanobiotix rises sharply after positive topline data in soft tissue sarcoma. Looking ahead notable earners include Blackberry and Carmax.

Movers

- Consumer Discretionary Hornbach [HBH.DE] -2.4% (Earnings)

- Financials Deutsche Beteiligungs [DBAN.DE] -2.0% (Bafin tax probe), Hispania Activos [HIS.ES] +3.2% (Raised bid from Alzette), BPER [BPE.IT] +7% (Unipol raises stake)

- Healthcare Nonobiotix [NANO.FR] +47% ( positive phase II/III topline data in soft tissue sarcoma with NBTXR3), Santhera Pharma [SANN.CH] +4.0% (UK's MHRA renews Early Access to Medicines Scheme Scientific Opinion for Santhera's Raxone)

Speakers

- Italy League party official Borghi (league, budget committee): Euro exit plan is not part of govt policy but did noted that monetary sovereignty would solve many of Italy's problems

- EU's Dombrovskis: Greece debt relief agreement ensures the country return to financial stability

- South Africa Fin Min Nene: have little fiscal room to maneuver. Needed to build fiscal buffers to deal with any potential crisis

- Saudi and Iran oil ministers said to have held private talks before today's closed-door OPEC session

- China Stats Bureau Official Ning reiterated view that domestic economy still faces uncertainties

Currencies

- USD continued to move off the recent cycle highs against the European pairs

- EUR/USD high higher by almost 0.5% to test 1.1670 area as the Major European PMI survey helped to dispel concerns of a prolong slowdown in the region and paint a picture of Q2 activity after the weakness in Q1.

- GBP built upon Thursday’s hawkish hold to teat its highest level in over a week around the 1.33 area. GBP benefited as three out of nine BOE policymakers, including its chief economist, voted to increase rates

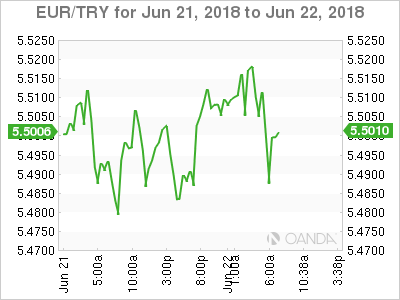

- On the emerging market front analysts noted that it was difficult to predict how the lira and local assets may react after Turkey's parliamentary and presidential elections on Sunday.

Fixed Income

- Bund Futures trade 34 ticks lower at 161.88 as Euro Zone PMIs offer further stabilization for the euro. Upside targets 162.25 followed by 162.75, while a return lower targets the 158.75 level.

- Gilt futures trade at 122.75 lower as the British pound extends the post-BOE rally to erase this week’s loss. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Friday's liquidity report showed Thursday's excess liquidity fell from €1.840T to €1.820T. Use of the marginal lending facility rose from €83M to €97M.

- Corporate issuance saw issuers face strong headwinds amid supply deluge; for the week ending Jun20th Lipper fund flows reported equity fund outflows of $1.3B vs outflows of $9.7B in the prior week

Looking Ahead

- OPEC bi-annual meeting in Vienna

- (UR) Ukraine May Industrial Production M/M: No est v -5.0% prior; Y/Y: No est v 3.0% prior

- 05:30 (ZA) South Africa to sell ZAR600M in I/L 2025, 2033 and 2050 bonds

- 06:00 (IE) Ireland May PPI M/M: No est v -0.8% prior; Y/Y: No est v -4.0% prior

- 06:00 (UK) DMO to sell combined £4.0B in 1-month, 6-month and 12-month Bills £1.0B, £1.5B and £1.5B respectively)

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (PL) Poland May M3 Money Supply M/M: 0.7%e v 0.2% prior; Y/Y: 5.9%e v 5.7% prior

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada May CPI M/M: 0.4%e v 0.3% prior; Y/Y: 2.6%e v 2.2% prior, CPI Core- Common Y/Y: 1.9%e v 1.9% prior, CPI Core- Median Y/Y: 2.1%e v 2.1% prior, CPI Core- Trim Y/Y: 2.1%e v 2.1% prior, Consumer Price Index: 133.9e v 133.3 prior

- 08:30 (CA) Canada Apr Retail Sales M/M: 0.0%e v 0.6% prior; Retail Sales Ex Auto M/M: +0.5%e v -0.2% prior

- 09:00 (BE) Belgium Jun Business Confidence: 0.0e v 0.2 prior

- 09:00 (CL) Chile May PPI M/M: No est v 0.2% prior

- 09:00 (MX) Mexico Apr IGAE Economic Activity Index (monthly GDP) Y/Y: +4.6%e v -0.8% prior

- 09:45 (US) Jun Preliminary Markit Manufacturing PMI: 56.1e v 56.4 prior, Service PMI: 56.5e v 56.8 prior, Composite PMI: No est v 56.6 prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 15:00 (CO) Colombia Apr Economic Activity Index (Monthly GDP) Y/Y: 2.7%e v % prior

Stocks, EUR Rally On Data, Oil Higher Ahead Of OPEC Meet

Friday June 22: Five things the markets are talking about

Euro equities are on the rise, along with U.S stock futures, as Euro manufacturing and services data this morning beat analysts’ expectations, dragging along with it the EUR (€1.1667).

Crude oil prices start Friday better bid, after OPEC and its allies are rumoured to have reached a preliminary agreement on output, an increase in production of +1M bpd (see below) and this despite calls from Iran to boost output further.

Even some risk appetite is seen returning to the foreign exchange market, as EM currencies see a small rebound and the dollar falls slightly, benefitting from reports that a number of U.S officials are trying to resurrect trade talks with China before Trump’s tariffs come into effect in July.

Fixed income dealers see U.S Treasury prices fall, backing up yields, while in Europe; Greece’s creditors have struck a deal to ease repayment terms on some of the nation’s loans. This is supporting Greek sovereign bonds, while Italian debt has also steadied after yesterday’s plunge.

On tap: CAD core-retail sales and CPI data (08:30 am EDT), OPEC two-day meeting begins in Vienna.

1. Stocks mixed reaction

In Japan, the Nikkei share average dropped overnight as shares of automakers fell after Germany’s Daimler cut its profit forecast citing tariff concerns yesterday, while weaker U.S data is dampening some investor enthusiasm. The Nikkei fell -0.78% and the index is down -1.46% on the week. The broader Topix shed -0.33%.

Down-under, Aussie financials rallied after ANZ Banking Group doubled its share-buyback programme, but the overall market remains under pressure from Sino-U.S trade tensions. The S&P/ASX 200 index fell -0.1%, but still posted its best weekly performance in nearly three-years with a gain of +2.2%. In S. Korea, the Kospi rallied +0.83%.

In Hong Kong, the benchmark stock index ended slightly higher overnight, but posted its biggest weekly loss in three-months amid escalating trade tensions. The Hang Seng index rose +0.2%, while the China Enterprises Index lost -0.2%. For the week, the Hang Seng lost -3.2%, its worst weekly performance since late March.

In China, stocks edged higher overnight, but posted their worst weekly loss since early February, on lingering worries over a full-blown trade war. The blue-chip CSI300 index closed up +0.5%, while the Shanghai Composite Index gained +0.5%. For the week, SSEC tumbled -4.4%, while CSI300 slid -3.8%.

In Europe, regional bourses trade higher across the board following the preliminary PMI data out of Europe (see below).

U.S stocks are set to open in the ‘black’ (+0.5%).

Indices: Stoxx600 +0.5% at 382.8, FTSE +0.5% at 7597, DAX +0.4% at 12556, CAC-40 +0.7% at 5353, IBEX-35 +0.8% at 9781, FTSE MIB +1.0% at 21891, SMI +0.8% at 8523, S&P 500 Futures +0.5%

2. Oil prices rise as OPEC meets, gold higher

Oil prices have rallied +1% this morning as OPEC struggles to agree a deal to increase output to compensate for losses in production.

OPEC begins its two-day meeting in Vienna today, together with non-OPEC oil producers to discuss output policy.

Benchmark Brent crude is up +75c a barrel at +$73.80, while U.S light crude is +60c higher at +$66.14.

Saudi Arabia and Russia want to raise output, but some other OPEC members, including Iran, have opposed this.

Consensus expects OPEC to announce an increase in production of +500K to +600K bpd, which would help ease tightness in the market but not enough to create a glut.

A more relaxed policy will push Brent towards +$70 a barrel, while restrictive measures will support crude oil back towards +$80.

Ahead of the U.S open, gold prices have inched a tad higher after hitting a six-month trough Thursday, as the U.S dollar pulled back from its 11-month peak on profit taking. Spot gold is up +0.2% at +$1,269.46 an ounce. On Thursday, bullion touched +$1,260.84, its lowest since Dec. 19, 2017. U.S gold futures for August delivery are +0.1% higher at +$1,271.50 per ounce.

Note: The yellow metal is heading for a -0.7% decline for the week.

3. Italian bonds finds support

Borrowing costs in Europe’s third largest economy, Italy, are falling this morning after yesterday’s sharp bond selloff, although investor sentiment remains fragile.

News that Italy’s new anti-establishment government had appointed two-euro sceptics to head key finance committees in parliament resuscitated market concerns about the coalition’s commitment to the EUR.

Italy’s two-year bond yields are down -16 bps at +0.76%, while 10-year bond yields fell -8 bps to +2.67%.

Elsewhere, Mexico’s Central Bank (Banxico) raised its Overnight Rate by +25bps to +7.75% (as expected).

On Sunday June 24 is Turkey’s general election and it’s difficult to predict how the TRY and local assets may react after the vote.

Some investors will interpret Erodgan’s victory accompanied by a strong mandate obtained by his AKP as a source of political stability. Others will view such a result negatively, mainly due to concerns that the CPRT could be under political pressure to lower interest rates to maintain robust GDP growth.

Note: This comes at a time when the domestic economy is considered overheated – double digit inflation – and a wider current account deficit.

4. Dollar retreats from its 11-month highs

The USD continues to move away from its recent G10 currency price highs.

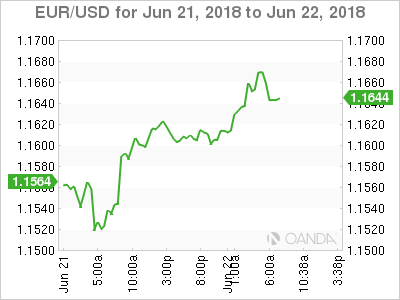

EUR/USD (€1.1667) is higher by almost +0.5% to again consider retesting the psychological €1.1680-00 level as this mornings Euro PMI surveys helped to dispel concerns of a prolong slowdown in the region and paint a stronger picture of Q2 activity after the weakness in Q1.

GBP (£1.3295) is building upon the BoE’s ‘hawkish’ hold yesterday. The pound benefitted as three out of nine BoE policymakers, including its chief economist, voted to increase rates.

In EM, investors eyes are on Sunday’s Turkey’s parliamentary and presidential elections. The governance system will switch over to an executive presidency – the market is waiting to find out how this will work in practice. Will the new president take control of the central bank and monetary policy? USD/TRY last trades flat at $4.7191, EUR/TRY is up +0.5% at €5.5052

5. Eurozone PMI’s pick up

Business activity in the eurozone picked up in June for the first month in five, which may suggest that the region is beginning to shake off a sluggish start to the year.

Euro data from Markit this morning showed that Eurozone manufacturing PMI and services PMI for June came in at 55.00 each, with services beating expectations of 53.6 and manufacturing in line – its composite PMI for the currency area rose to 54.8 from 54.1 in May.

ECB policy makers remain worried that the imposition of new tariffs on some items traded between the U.S and the EU could dampen confidence, making businesses wary of signing new deals and undertaking new investments.

Euro Gains Ground On Strong Services PMIs

EUR/USD has posted gains in the Friday session, continuing the upward trend we saw on Thursday. Currently, the pair is trading at 1.1639, up 0.32% on the day. On the release front, the focus is on manufacturing and services PMIs. Germany and the eurozone posted Services PMIs of 53.9 and 55.0, respectively, both of which beat the estimates. On the manufacturing front, German Manufacturing PMI dropped to 55.9, missing the estimate of 56.3 points. Eurozone Manufacturing PMI softened to 55.0, matching the estimate. Later in the day, OPEC members meet in Vienna to discuss a proposal to raise oil production.

Led by the German locomotive, the eurozone economy continues to grow, although there was a hiccup in the first quarter. The ECB has given the economy a vote of confidence, with a decision to finally wind up its asset-purchase program at the end of 2018. The June PMI reports pointed to continued expansion in the manufacturing and services sectors, but all may not be well. The eurozone and German Manufacturing PMIs both slowed for a sixth straight month, and the German release was the weakest since December 2016. With global protectionism on the rise as the trade war worsens, German and eurozone exports could suffer, which in turn would have a negative impact on manufacturers. If upcoming PMIs continue to weaken, investor confidence in the eurozone could wane and weigh on the euro.

Central bankers converged in Sintra, Portugal this week, and the trade war between the U.S and its trading partners was high on the agenda. The United States and the EU have slapped tariffs on each other, and President Trump shook up global equity markets when he threatened to impose a 10 percent tariff on some $200 billion worth of Chinese goods. The heads of the central banks from the U.S and the European Union were united in the gloomy view of the trade conflict, with Federal Reserve Chair Jerome Powell saying that the changes in trade policy could force the Fed to “question its outlook”. ECB President Mario Draghi said that the trade spat could have negative consequences on monetary policy. If these protectionist measures force central banks to alter their monetary policy, this could have a significant impact on exchange rates.