Sample Category Title

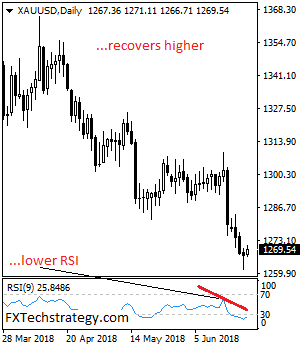

GOLD: Backs Off Lower Prices, Sees Correction

GOLD: The pair has backed off lower prices to face corrective recovery. On the downside, support comes in at the 1,260.00 level where a break will turn attention to the 1,250.00 level. Further down, a cut through here will open the door for a move lower towards the 1,240.00 level. Below here if seen could trigger further downside pressure targeting the 1,230.00 level. Conversely, resistance resides at the 1,280.00 level where a break will aim at the 1,290.00 level. A turn above there will expose the 1,300.00 level. Further out, resistance stands at the 1,310.00 level. All in all, GOLD looks to recover higher.

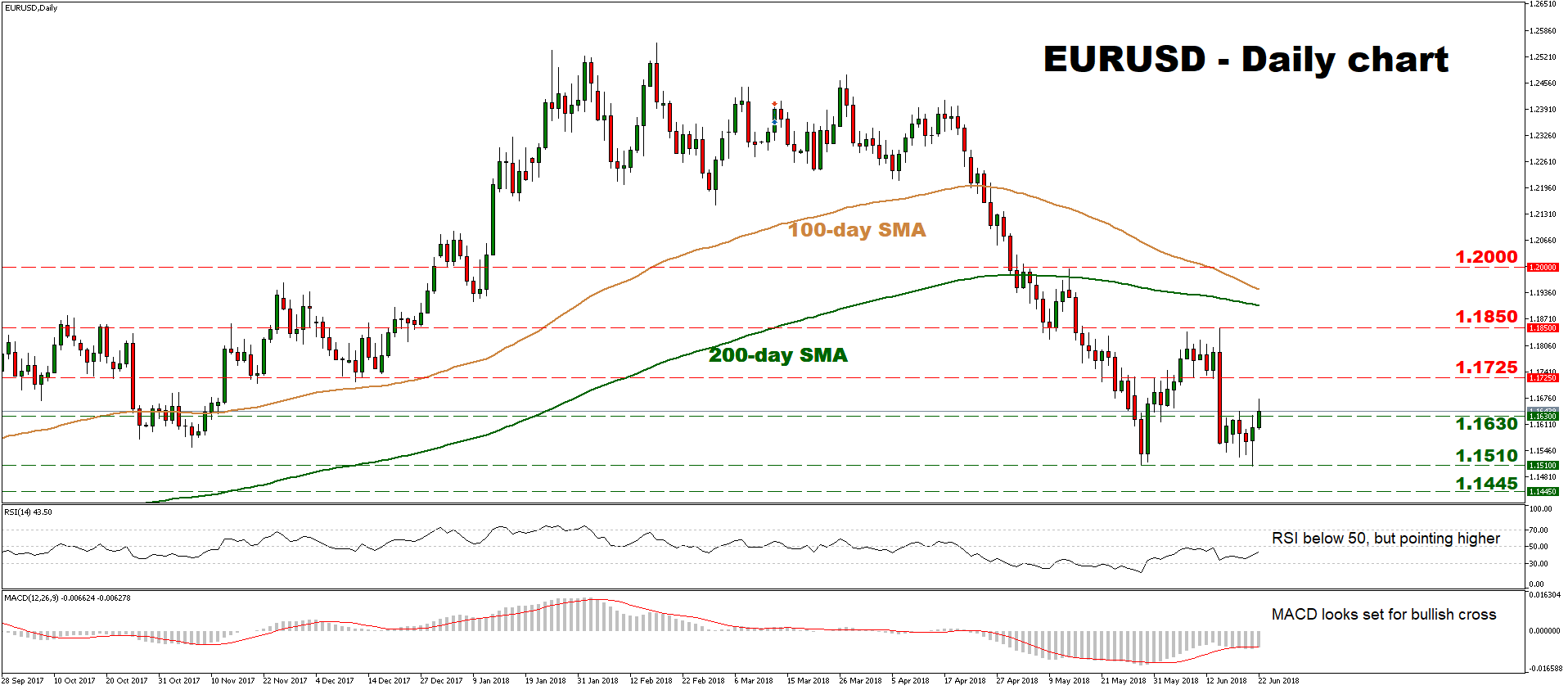

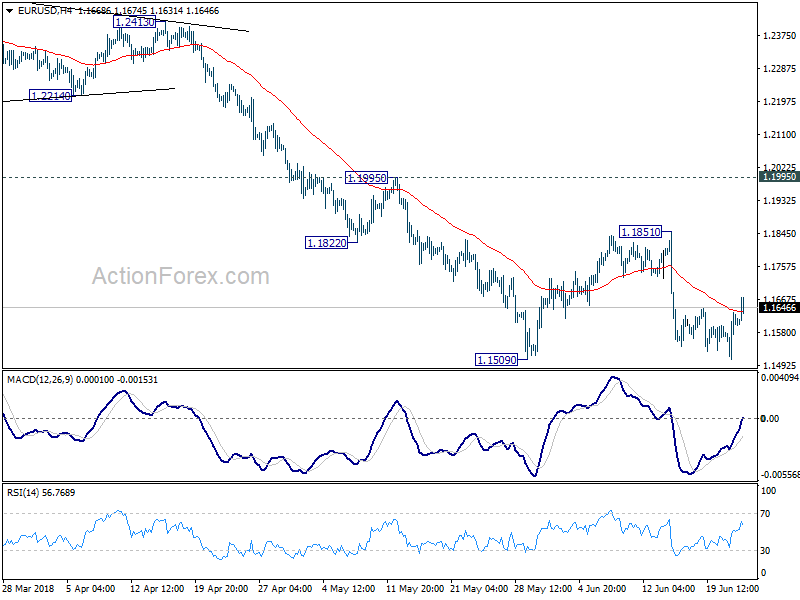

EURUSD Posts Eleven-Month Low, But a Double-Bottom May be Forming

EURUSD reached an eleven-month low of 1.1510 on May 29, subsequently rebounded, but came back down to test that area again on June 21. However, the bears were unable to pierce that level, and now, a double-bottom formation looks to be in the works. A break above 1.1850 is needed to confirm such a pattern, in which case the odds for further recovery in the pair would increase substantially from a technical standpoint.

Momentum oscillators in the daily timeframe support the case for further recovery in the near-term. The RSI – although below its neutral 50 line – is currently pointing higher, while the MACD looks set to post a bullish cross above its trigger line. Both suggest that negative momentum is fading.

Advances in prices could encounter immediate resistance near 1.1725, a level defined by the inside swing low on June 8. An upside break would bring the June 14 high of 1.1850 into focus. Further advances from there would confirm a double bottom pattern, potentially opening the way for the psychological territory of 1.2000.

On the downside, further declines could find preliminary support near 1.1630, a level that halted several advances between June 15 and 21. A break below it could see scope for another test of the eleven-month low of 1.1510, with even steeper declines aiming for 1.1445, a level seen back in June 29, 2017.

Overall, the broader outlook for EURUSD remains bearish, but in the near-term, the latest rebound could continue. Should prices power above 1.1850, however, that could confirm a double bottom and signal a potential trend reversal.

Inflation Steady at 2.2% in Canada, But Core Price Growth Softens

Consumer prices were up 2.2% year-on-year in Canada in May, unchanged from April and well below market expectations for an acceleration to 2.6%. Adjusted for seasonal patterns, prices rose 0.1% month-on-month.

Steadying the headline rate, energy prices were up 11.6% year-on-year, led by gasoline (+22.9%), but offset by falling electricity prices (-0.8%). Excluding energy, inflation decelerated to 1.6% (from 1.9% previously). Statistics Canada notes decline in telephone service index (down 7.1% year-on-year) as weighing on inflation in the month.

Indeed, outside of energy, price growth was fairly soft across the board. Price growth decelerated (year-on-year) for five of eight major categories. Leading declines on a month-on-month basis (seasonally adjusted) were household operations (-1.0%, seasonally adjusted), and clothing and footwear (-0.2%). The only category to see a significant increase was recreation, education and reading (+1.7%), following a 1.5% decline in April.

The Bank of Canada's core measures were similarly unexciting. CPI-trim fell to 1.9% (from 2.1% previously), while CPI-median and CPI-common remained unchanged at 1.9%.

Key Implications

This was a soft report. Coming alongside a disappointing retail sales report, the data flow this week suggests little need for urgency from the Bank of Canada to raise interest rates. This is in line with our thinking. We expect just one more hike from the Bank of Canada this year, before it pauses to assess the state of a Canadian economy in the midst of a slowing housing market and ongoing trade uncertainty.

The weaker Canadian dollar, which has fallen to its lowest level in a year, will eventually show up in the inflation report, helping to pull up both core and headline measures. However, this is unlikely to be a game changer for the Bank of Canada, which will look through its impact.

CAC Jumps on Strong French Services PMI

The CAC index has posted sharp gains in the Friday session. Currently, the CAC is at 5368, up 0.97% on the day. On the release front, French PMIs were mixed. The services PMI improved to 56.4, beating the estimate of 54.3 points. However, the manufacturing PMI slipped to 53.1, shy of the estimate of 54.0 points. Eurozone PMIs also showed continuing expansion in the services and manufacturing sectors.

French PMI reports in June showed a similar trend to their Geman and eurozone counterparts. The good news is that services and manufacturing PMIs continue to indicate expansion in France, the eurozone and Germany. However, this is not the entire story, as manufacturing in the eurozone and Germany continue to drop from month to month. In France, manufacturing PMI fell to 53.1, its lowest level since February 2017. With global protectionism on the rise as the trade war worsens, the French export sector could suffer, which in turn would have a negative impact on manufacturers. If upcoming PMIs continue to weaken, investor confidence in the eurozone could wane and weigh down the already fragile European equity markets.

Although the CAC index is in green territory on Friday, it hasn’t been immune to investors’ concerns over the escalating global trade war, and has declined 2.2% this week. Nervous markets had a chance to listen in on the heads of the U.S and EU central banks, who met at the ECB forum this week. Mario Draghi and Jerome Powell sounded gloomy about the recent protectionist moves, which were triggered by the U.S imposing tariffs on China, the EU and other trading partners. Powell saying that the changes in trade policy would have a negative effect on business hirings and investment, and could force the Fed to question its economic outlook. Mario Draghi said that the trade spat could have negative consequences on monetary policy. Although both central bankers didn’t provide any specifics, their apprehension over the rash of new tariffs is unmistakable. If the trade spat worsens and forces central banks to alter their monetary policy, this could have a significant impact on equity markets.

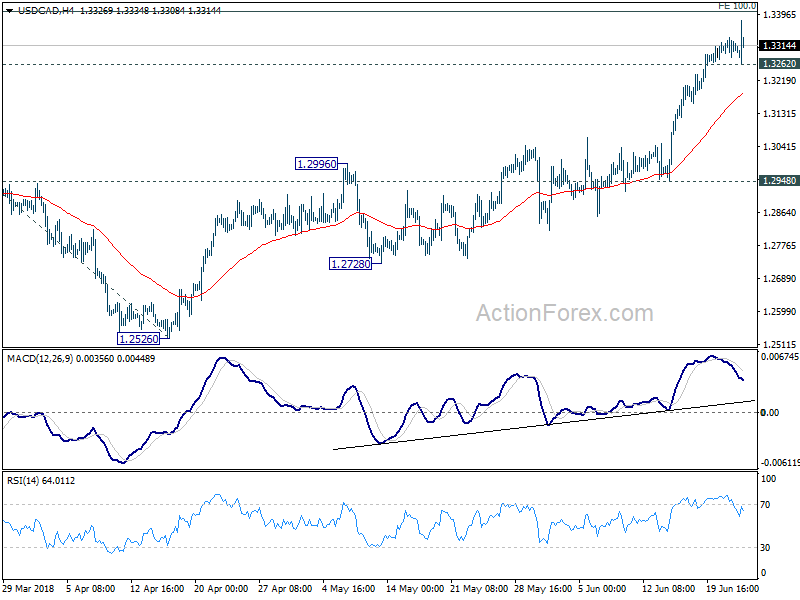

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3291; (P) 1.3315; (R1) 1.3345; More...

USD/CAD dipped briefly to 1.3262 but quickly resumed recent rise to 1.3318. Further rise is expected to 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. Nonetheless, break of 1.3262 will indicate short term topping. In that case, intraday bias will be turned to the downside for pull back to 4 hour 55 EMA (now at 1.3187) or below. But we'd expect strong support above 1.2948 to bring rally resumption.

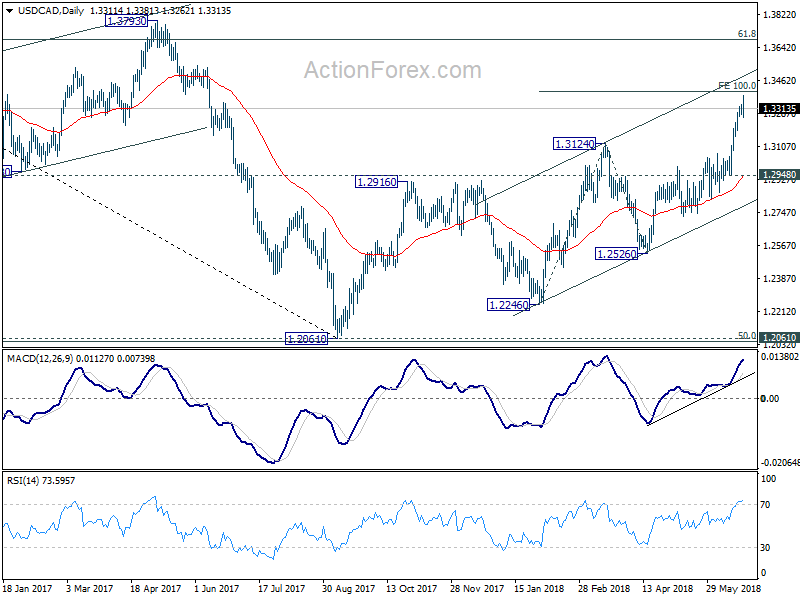

In the bigger picture, current development solidify the view of bullish trend reversal. That is fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. This will now be the preferred case as long as 1.2526 support holds, even in case of deep pull back.

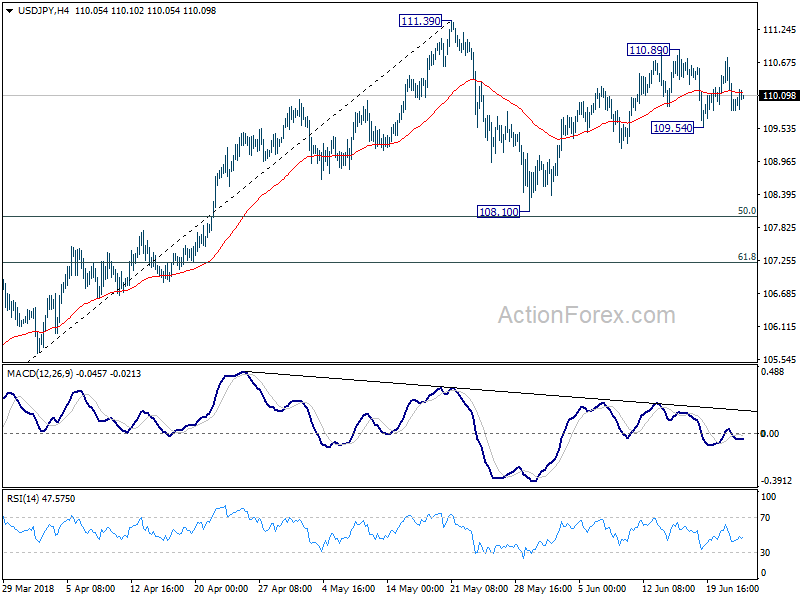

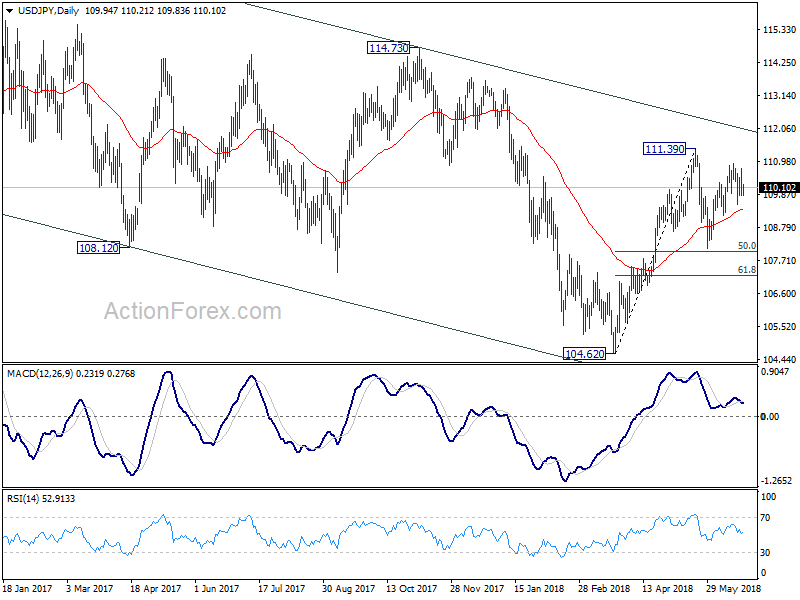

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.62; (P) 110.19; (R1) 110.55; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, below 109.54 will extend the corrective pattern from 111.39 with another falling leg to 108.10 and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39. But we'd be cautious on strong resistance from there to limit upside.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

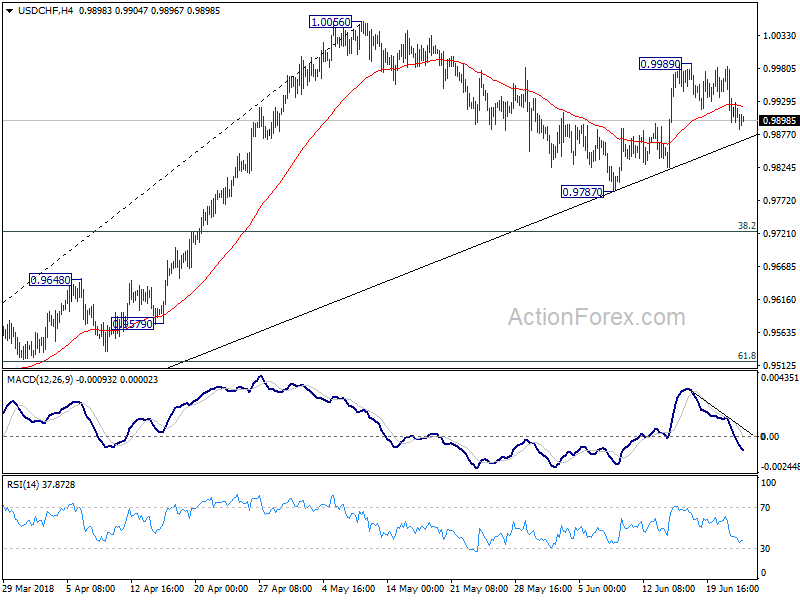

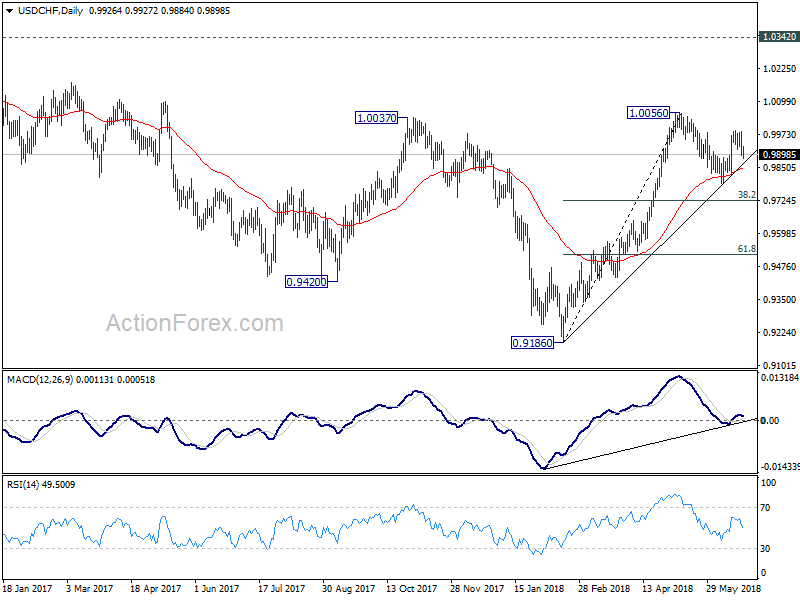

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9882; (P) 0.9934; (R1) 0.9971; More...

Intraday bias in USD/CHF remains mildly on the downside. As noted before, correction from 1.0056 is possibly resuming through 0.9787 support. But, we'd expect strong support from 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to contain downside to bring rebound. On the upside, break of 0.9989 will target a test on 1.0056 first. Break will resume whole rise from 0.9186.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

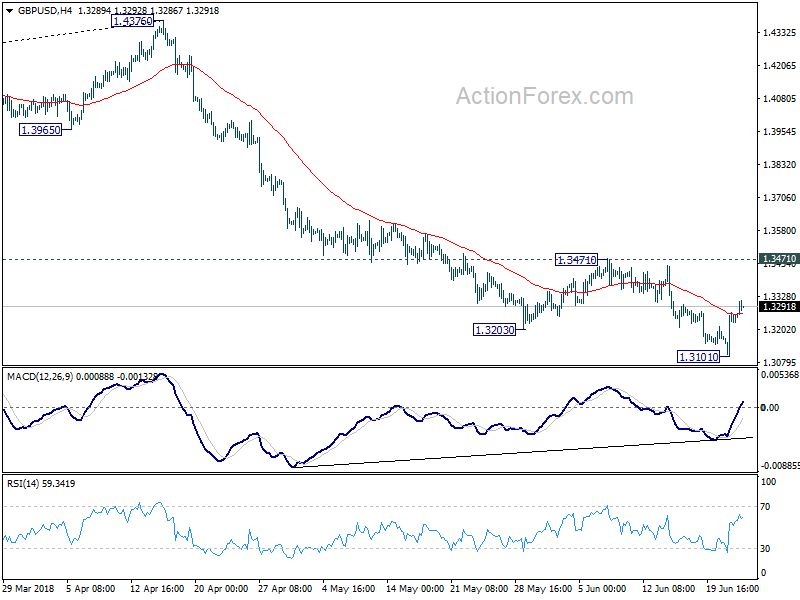

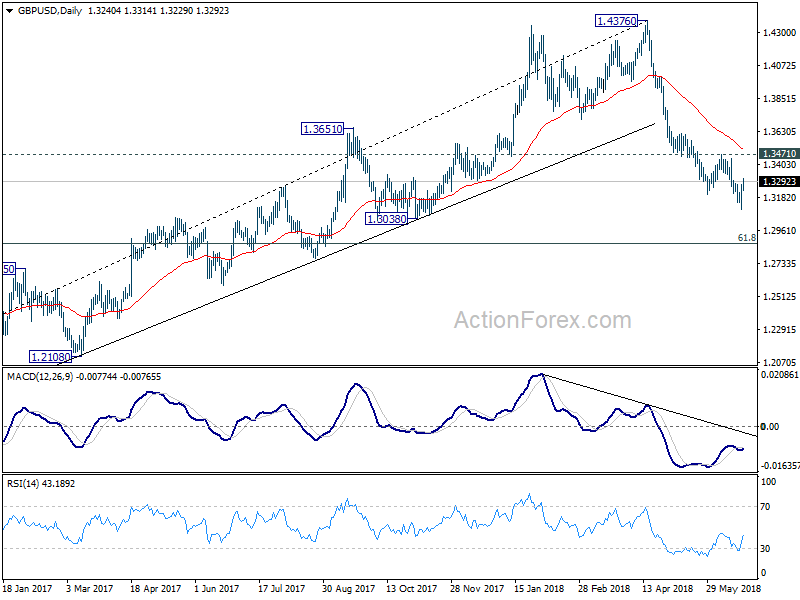

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3139; (P) 1.3205; (R1) 1.3308; More...

GBP/USD's rebound from 1.3101 extends to as high as 1.3314 so far. While further rise cannot be ruled out, outlook is unchanged. With 1.3471 resistance intact, outlook remains bearish for another decline. Break of 1.3101 will resume the fall from 1.4376 for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1582 (R1) 1.1655; More.....

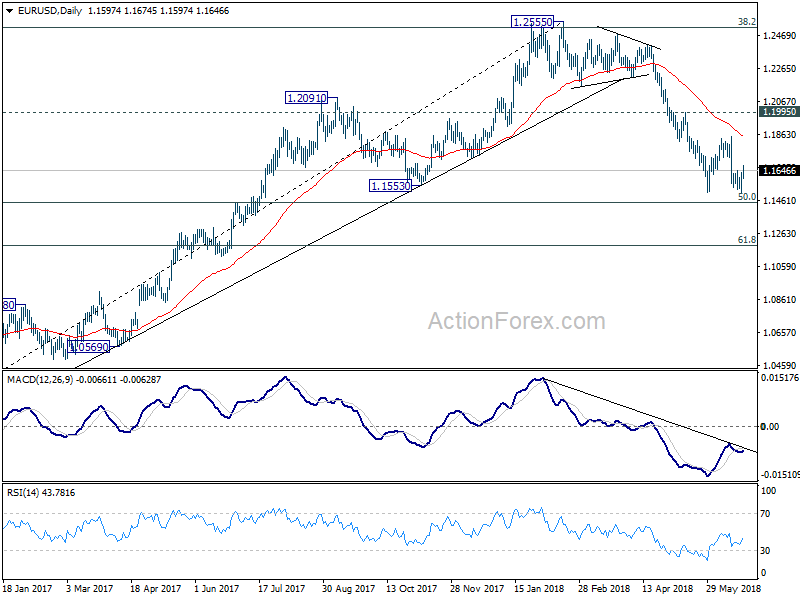

EUR/USD rebounds to as high as 1.1674 so far today but outlook is unchanged. While further rise cannot be ruled out, upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 low will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro Jumps on Solid PMI, Canadian Dollar Hammered by Retail Sales and CPI

Economic data and improving sentiments are the main drivers in the markets. Australian Dollar and New Zealand Dollar are so far the strongest ones today as European stocks rally. At this time of writing, FTSE is up 1.33%, DAX up 0.42% and CAC is up 0.97%. US futures also point to higher open. However, as the rebound in stocks is ... just a rebound. Major global indices are still on track to close the week lower. Aussie and Kiwi are the second and third weakest ones for the week too. We won't call that a "risk-on" market. Investors are squaring their positions, taking profits, ahead of the weekend. In particular, there are reports on White House split over the hardline response to trade war with China. Based on the erratic nature of Trump and his administration, we'll neve know if there will be some surprises before next week.

Meanwhile, Canadian dollar suffers steep selling today after weaker than expected retail sales and CPI data. It's also trading as the weakest one for the week. There are reports that OPEC is reaching an agreement in principle to raise output by 600k barrels a day, much lower than the worst case of 1-1.5m barrels a day. That could give oil prices a lift, but may not help the Loonie too much. Euro rises broadly today, except versus Aussie and Kiwi. PMIs show strong rebound in services which offset the slowdown in manufacturing.

Yen is trading broadly lower today, but it will still likely end the week as two of the strongest, along with Swiss Franc. Sterling, despite the BoE boost, is still down against Dollar, Euro, Yen and Swiss for the week.

Euro surges as PMIs point to solid 0.5% GDP growth, price pressures on the rise

Eurozone PMI manufacturing dropped to 55.0 in June, down from 55.5 and met expectation. PMI services rose to 55.0, up from 53.8 and beat expectation of 53.7. PMI composite rose to 54.8, up from 54.1 and beat expectation of 53.9. PMI composite is at a 2 month high while PMI services is at at 4-month high. However, PMI manufacturing is at an 18-month low. Overall, the data point to 0.5% GDP growth in Q2.

Markit Chief Business Economist Chris Williamson noted in the release that "an improved service sector performance helped offset an increasing drag from the manufacturing sector in June, lifting Eurozone growth off the 18- month low seen in May. With growth kicking higher in June, the surveys are commensurate with GDP rising 0.5% in the second quarter." In addition, "price pressures are also on the rise again, running close to seven-year highs. Increased oil and raw material prices are driving up costs, but wages are also lifting higher, in part reflecting tighter labour markets in some parts of the region."

Though, he also warned that "manufacturing is looking especially prone to a further slowdown in coming months, with companies citing trade worries and political uncertainty as their biggest concerns." And, "risks remained tilted towards a further slowdown in the second half of the year."

Also released, Germany PMI manufacturing dropped to 55.9 in June, down from 56.9 and missed expectation of 56.3. PMI services rose to 53.9, up from 52.1 and beat expectation of 52.2. PMI composite rose to 54.2, up from 53.4, and hit a 2-month high.

French PMI manufacturing dropped to 53.1 in June, down from 54.4 and missed expectation of 54.0. But PMI services rose to 56.4, up from 54.3 and beat expectation of 54.3. PMI composite rose to 55.6, up from 54.2, and hit a 2 month high.

Canada retail sales dropped -1.2%, ex-auto sales dropped -0.1%, core CPI moderated

Canadian Dollar drops sharply after very weak retail sales data. Headline sales dropped -1.2% mom in April versus expectation of 0.0% mom. Ex-auto sales dropped -0.1% mom versus expectation of 0.2% mom.

Inflation data is not helping neither. CPI rose 0.1% mom, 2.2% yoy in May, below expectation of 0.4% mom, 2.6% yoy. CPI core common was unchanged at 1.9% yoy. CPI core median dropped to 1.9% yoy, down from 2.1% yoy. CPI core Trim dropped to 1.9% yoy, down from 2.1% yoy.

Japan CPI Core unchanged, PMI manufacturing improved

Released from Japan, all items CPI rose to 0.7% yoy in May, up from 0.6% yoy. Core CPI, less fresh food, was unchanged at 0.7% yoy. Core core CPI, less fresh food and energy even slowed to 0.3% yoy, down from 0.4% yoy. The data highlighted BoJ's inability to lift inflation and inflation expectation even with the ultra-loose monetary policy. And the central bank is still a long way from stimulus exit.

PMI manufacturing rose to 53.1 in June, up from 52.8, beat expectation of 52.6. Joe Hayes, Economist at IHS Markit note in the release that "the final PMI reading of the second quarter revealed a quickened pace of growth across the Japanese manufacturing economy. "The sector has sustained a relatively solid upward trend across 2018," and "there appears to be further legs in the manufacturing growth cycle."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1582 (R1) 1.1655; More.....

EUR/USD rebounds to as high as 1.1674 so far today but outlook is unchanged. While further rise cannot be ruled out, upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 low will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y May | 0.70% | 0.70% | 0.70% | |

| 00:30 | JPY | Flash Manufacturing PMI Jun | 53.1 | 52.6 | 52.8 | |

| 04:30 | JPY | All Industry Activity Index M/M Apr | 1.00% | 0.90% | 0.00% | |

| 07:00 | EUR | France Manufacturing PMI Jun P | 53.1 | 54 | 54.4 | |

| 07:00 | EUR | France Services PMI Jun P | 56.4 | 54.3 | 54.3 | |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 55.9 | 56.3 | 56.9 | |

| 07:30 | EUR | Germany Services PMI Jun P | 53.9 | 52.2 | 52.1 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 55 | 55 | 55.5 | |

| 08:00 | EUR | Eurozone Services PMI Jun P | 55 | 53.7 | 53.8 | |

| 08:00 | EUR | Eurozone Composite PMI Jun P | 54.8 | 53.9 | 54.1 | |

| 12:30 | CAD | Retail Sales M/M Apr | -1.20% | 0.00% | 0.60% | 0.80% |

| 12:30 | CAD | Retail Sales Ex Auto M/M Apr | -0.10% | 0.20% | -0.20% | 0.00% |

| 12:30 | CAD | CPI M/M May | 0.10% | 0.40% | 0.30% | |

| 12:30 | CAD | CPI Y/Y May | 2.20% | 2.60% | 2.20% | |

| 12:30 | CAD | CPI Core - Common Y/Y May | 1.90% | 1.90% | ||

| 12:30 | CAD | CPI Core- Median Y/Y May | 1.90% | 2.10% | ||

| 12:30 | CAD | CPI Core- Trim Y/Y May | 1.90% | 2.10% | ||

| 13:45 | USD | US Manufacturing PMI Jun P | 56.2 | 56.4 | ||

| 13:45 | USD | US Services PMI Jun P | 54.9 | 56.8 |