Sample Category Title

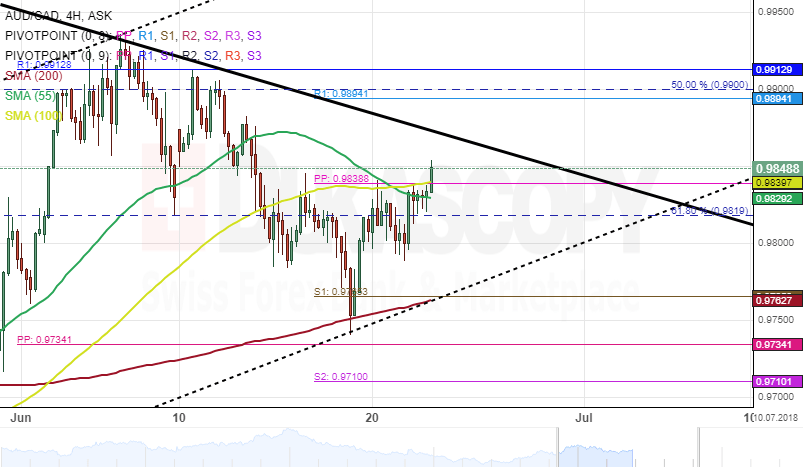

AUD/CAD 4H Chart: Pair Expected To Appreciate

The price movement of the AUD/CAD currency pair has been constrained by a medium-term ascending channel. The exchange rate re-tested the lower boundary of the channel on June 19 and followed by 100-pips gain.

By Friday's session, the currency pair was stranded between the 55-,100-hour SMAs and combination of the weekly pivot point and the 61.80% Fibonacci retracement level near the 0.9829 mark.

As for near future, it is likely that bulls could gather enough strength to dash through the resistance cluster. Meanwhile, technical indicators demonstrate that bulls are likely to grow stronger during the following trading sessions.

AUD/JPY 4H Chart: Several Channels At Play

The Australian Dollar has been moving in several channel down against the Japanese Yen. The most important of which is the medium-term descending channel form on June 7 and has guided the currency pair lower.

During the past few days, the exchange rate has been trading sideways within the range of 81.73 and 80.77.

Given that the AUD/JPY currency exchange rate has breached the upper boundary of the descending channel, the nearest target for the pair could be a strong resistance level near 82.62 set by the combination of the 55-,100-,200-hour SMAs and the monthly and weekly PPs.

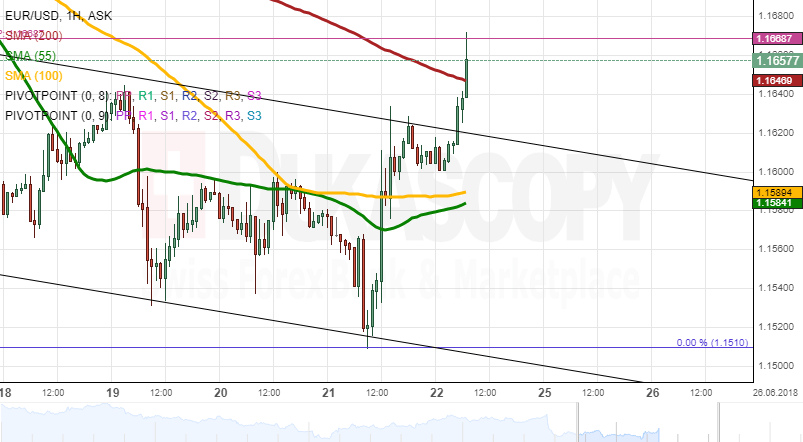

EURUSD Analysis: Trades Between Strong Barriers

EUR/USD was pressured lower on Thursday morning by the combined resistance of the 55– and 100-hour SMAs. This allowed the pair to re-test its one-year low of 1.15 prior to gaining strong bullish momentum and dashing through these lines later in the session.

The pair might still edge slightly higher during the first part of the day; however, it does face a significant resistance cluster formed by the 200-hour, 55– and 100-period (4H) SMAs and the weekly PP at 1.1670. This area is likely to halt the pair today, thus letting bears to re-gain some of the lost positions.

Given the strength of the aforementioned support and resistance levels, the Euro might remain stranded in between these barriers until early Monday.

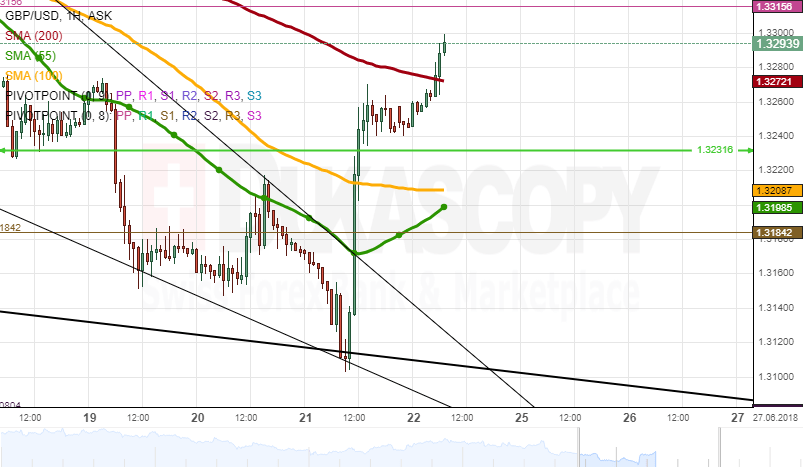

GBPUSD Analysis: Tests 200-Hour SMA

The Pound remained rather steady against the US Dollar on Thursday morning due to traders awaiting the BOE Monetary Policy Statement released mid-session.

Despite the benchmark rate being left on hold, the market was surprised by the hawkish undertone of the statement, thus causing the Sterling to fall 1.12% within a couple of hours. This strong appreciation resulted in a reversal from the senior channel and a breakout from the 55– and 100-hour SMAs and a historic resistance/support level at 1.3232.

Given that technical indicators are located in the overbought territory and the pair has approached an important resistance cluster set by the 55– and 100-period (4H) and the 200-hour SMAs near 1.33, its general direction is more likely to be to the downside today.

Strong support is likewise ahead at 1.3180.

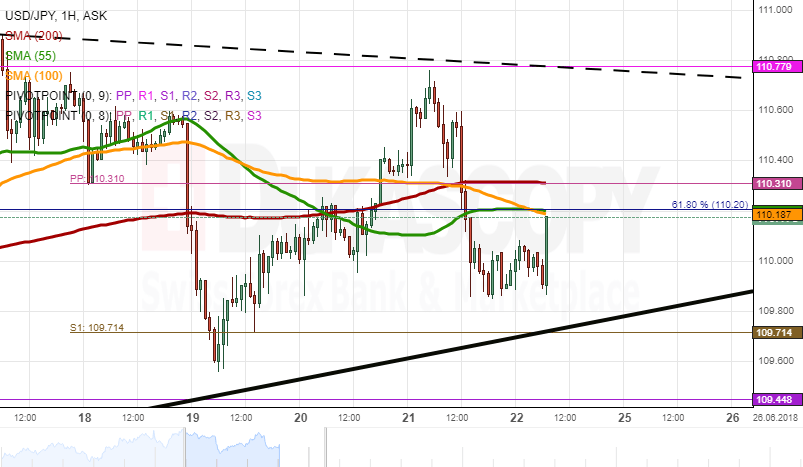

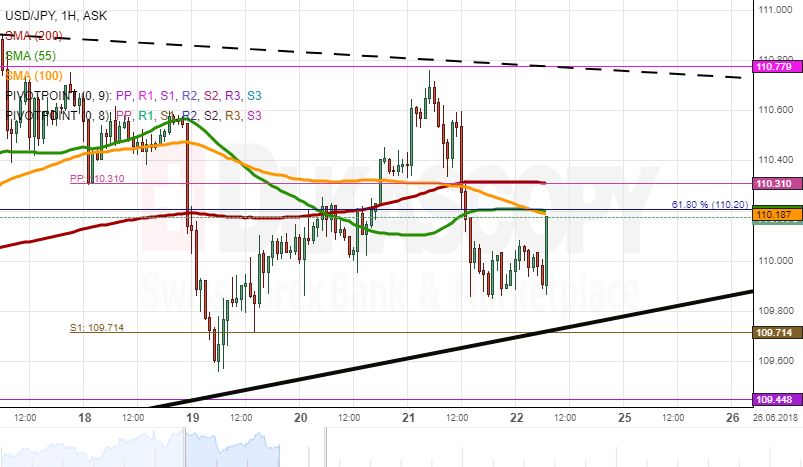

USDJPY Analysis: Breaches Strong Support

As apparent on the chart, the US Dollar respected the dashed trend-line and the monthly R1 at 111.00 yesterday. This allowed bears to take the dominant hand in the market and consequently breach the 55-, 100– and 200-hour SMAs and the 61.80% Fibonacci retracement near 110.20. The remaining part of the session was spent trading sideways.

There is still some downside potential until the senior channel line that could be realised during the following hours. However, considering that the 100– and 200-period (4H) SMAs are located at 109.95, this channel line might actually be reached only in the evening with the pair trading sideways.

In terms of resistance, this session should not mark big fundamental leaps; thus, the strong 110.20 area is unlikely to be breached.

Gold Analysis: Reaches New Low

The yellow metal continues to weaken against the US Dollar for the fifth consecutive session. This movement has been guided mainly by the 55– and 100-hour SMAs; thus, these moving averages might still lead the pair lower today until the bottom line of a three-month channel and the monthly S2 located near 1.255.00.

The 1,263.00 level which was reached mid-Friday is also the pair's lowest position since late December, 2017.

It seems that technical indicators are gradually starting to recover on the longer time-frames, as well. This could be an early indication of a possible change in sentiment. Even if bulls do not manage to push the yellow metal considerably higher today, they are expected to lead the pair next week.

Today's trading range is 1,255.00/1,285.00.

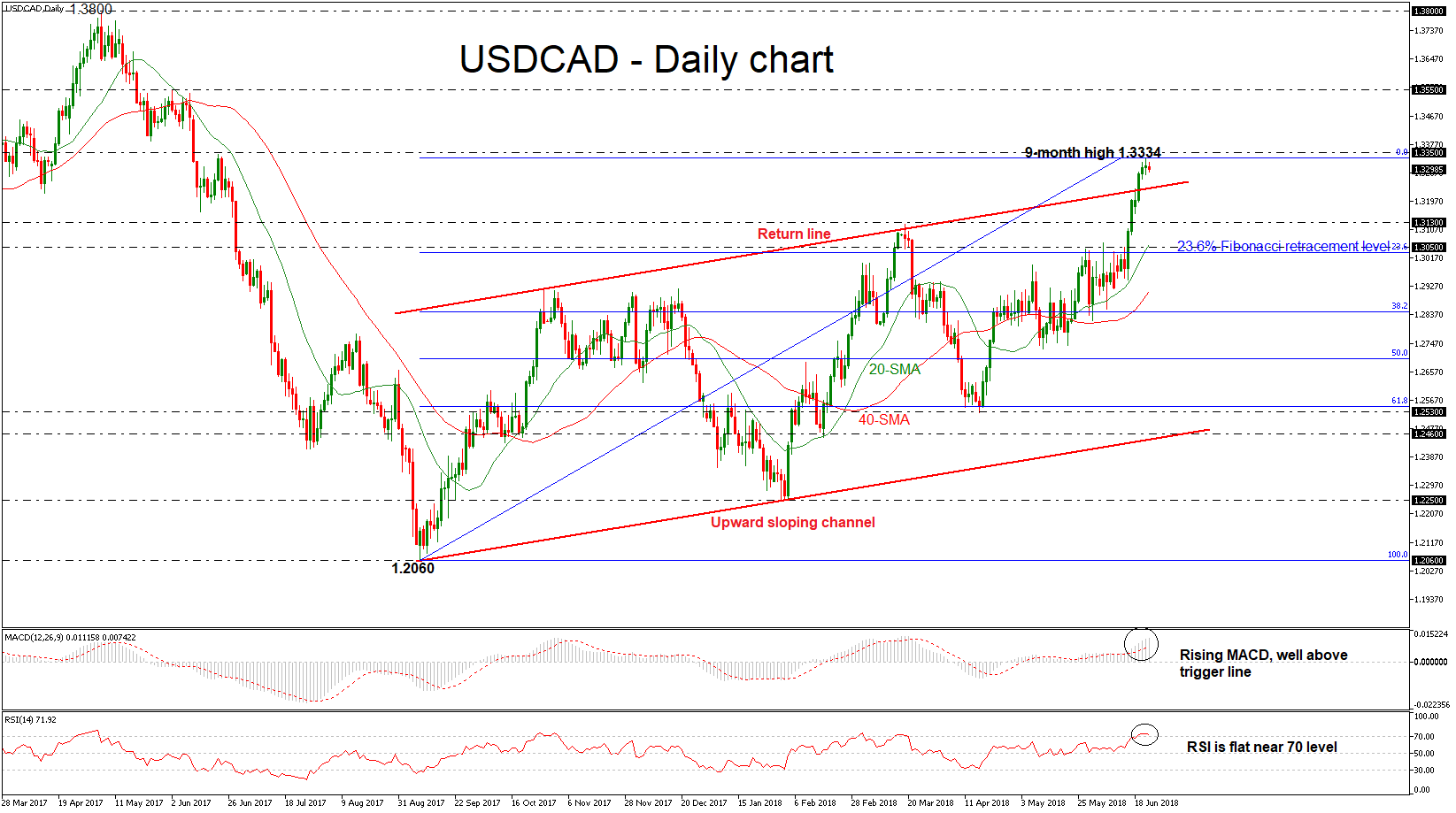

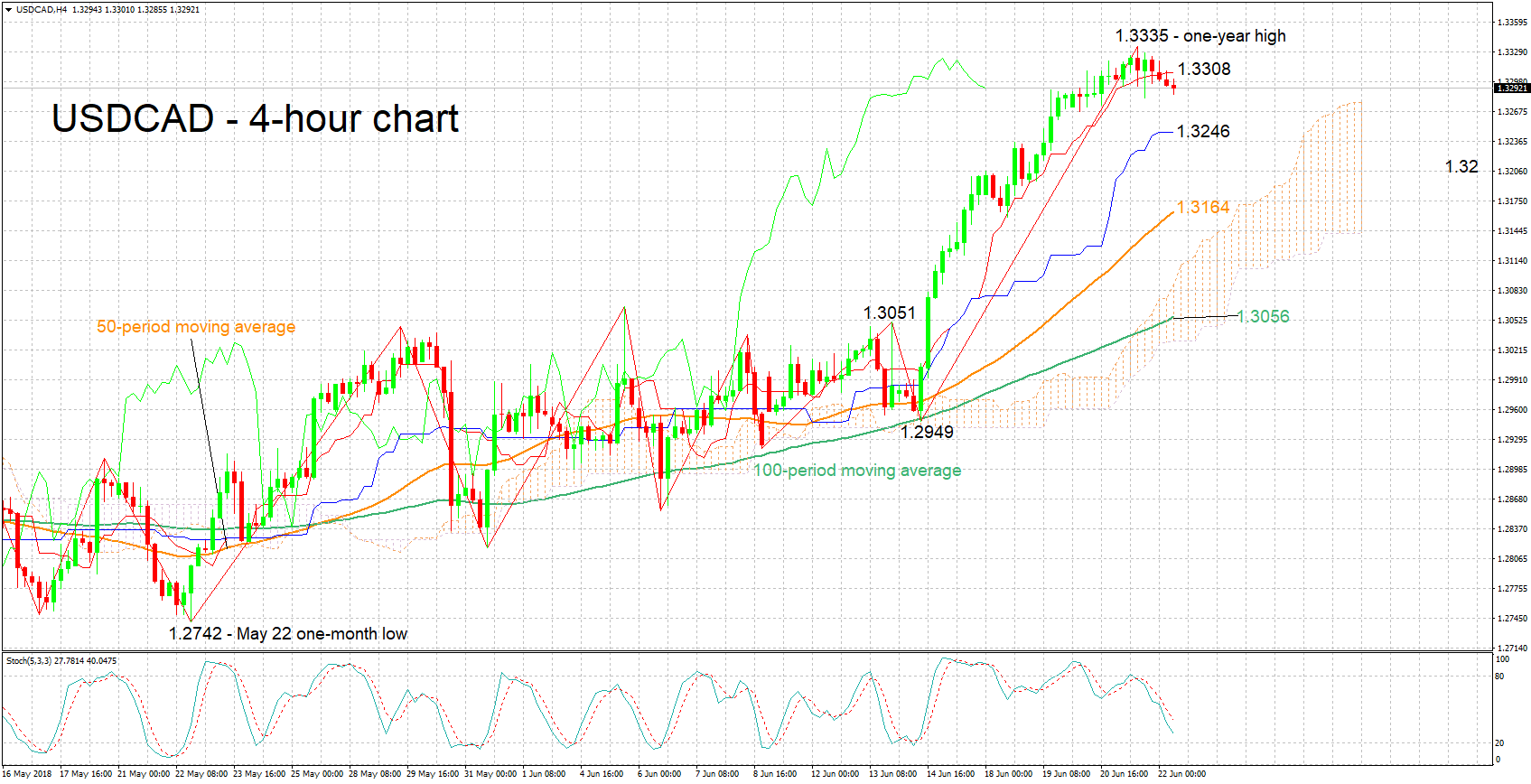

USDCAD Advances Above Upper Channel, Trades Near 9-Month High

USDCAD edged sharply higher over the previous six days successfully penetrating the nine-month ascending sloping channel to the upside. The price recorded a fresh one-year high of 1.3334 during yesterday’s session, however, today it started the day in negative territory.

Short-term momentum indicators are also pointing to a continuation of the bullish bias. However, the RSI is above the 70-overbought level and is looking overstretched. The MACD oscillator is rising well above the trigger line in the positive area. Also, the moving averages are following the price action to the upside.

If price action remains above the upward sloping channel, there is scope to test the next immediate resistance of 1.3350. Rising above it would see prices re-test the 1.3550 key level, taken from the peak on June 2017, creating a significant resumption of the uptrend.

In case of a bearish correction and a slip below the return line, then the focus would shift to the downside towards the 1.3130 support. More downside movement could increase the negative pressure and challenge the 23.6% Fibonacci retracement level of the upleg from 1.2060 to 1.3334, which holds near the 1.3050 support hurdle.

When looking at the bigger picture, the pair has a clear rising trend as it exited from the channel in the previous days and the medium-term strong momentum is expected to remain.

Pound Soars After BoE, OPEC Meeting And Key Data Eyed

Here are the latest developments in global markets:

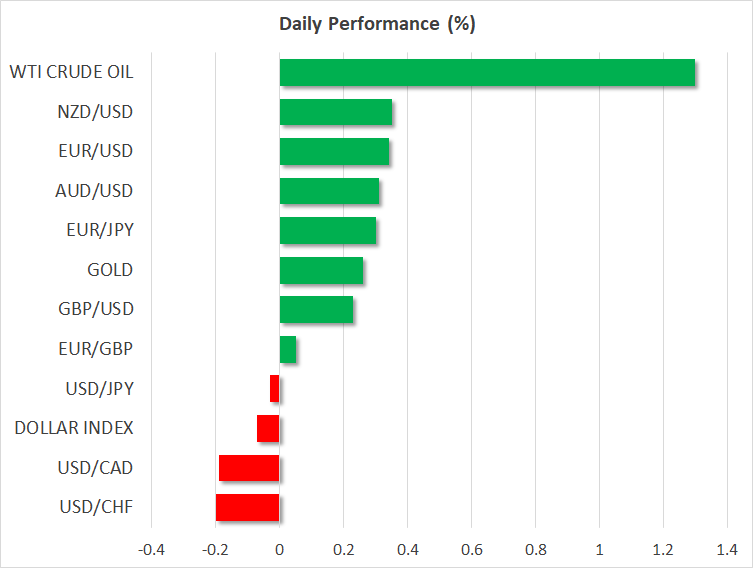

FOREX: The US dollar index – which tracks the greenback's performance against a basket of six major currencies – is lower on Friday, though by less than 0.1%. The index closed lower on Thursday, after touching its best levels in 11 months. In the UK, the pound soared after the BoE kept rates unchanged, but adopted a more hawkish tone, stoking expectations for a rate increase at the August meeting.

STOCKS: US markets closed lower on Thursday, amid concerns the recent trade spat is weighing on business sentiment. Also, e-commerce stocks took a hit after the US Supreme Court ruled that states can force online retailers to collect sales taxes, eroding an advantage that titans like Amazon (-1.13%) and Ebay (-3.18%) had enjoyed so far. As such, the tech-heavy Nasdaq Composite underperformed, declining by 0.88%, while the Dow Jones and S&P 500 fell by 0.80% and 0.63% respectively. That said, futures tracking the S&P, Dow, and Nasdaq 100 are currently flashing green, pointing to a higher open today. Asia was mixed, with Japan's Nikkei 225 and Topix edging lower by 0.78% and 0.33% correspondingly, but Hong Kong's Hang Seng index gaining 0.18%. Europe was a more cheerful story, as all major benchmarks are expected to open higher today, according to futures markets.

COMMODITIES: Oil prices edged up on Thursday and are trading higher on Friday as well, with WTI and Brent crude gaining 1.3% and 1.5% respectively. The gains came amid a plethora of OPEC-related comments ahead of the cartel's bi-annual meeting today. The latest comments suggest the producers may deliver an output increase of the magnitude of 600k – 1 million barrels per day (bpd), though Iran has continued to voice disagreement with a large production hike, a factor that has likely been supporting prices up until now. A sizeable output hike, closer to 1 milliion bdp could weigh on oil prices , whereas a more modest increase closer to 600k (or perhaps no increase at all) could boost prices further. In precious metals, gold is up by 0.2% on Friday, and is currently hovering near the $1,269 per troy ounce level. Buyers remain scarce for the yellow metal, which closed the session lower yesterday even despite a weaker US dollar and declines in stock markets.

Major movers: BoE holds, pound jumps as Haldane turns hawkish; Dollar softens

Major movers: BoE holds, pound jumps as Haldane turns hawkish; Dollar softens

The Bank of England (BoE) kept its policy unchanged yesterday, as was widely anticipated, though the vote count was more hawkish than expected. Three out of the nine policymakers voted in favor of an immediate rate increase, up from just two back in May, as the Bank's chief economist Andy Haldane joined the hawks. Haldane is considered neither dovish nor hawkish, so his dissent may have carried extra weight in signaling that a rate increase at the next meeting in August may be on the cards. Moreover, the minutes maintained a broadly upbeat tone, revealing that all members are more confident the slowdown in Q1 was only a transitory phenomenon, and noting that household spending has “bounced back strongly”.

Given these relatively hawkish signals, the implied probability for a rate increase in August jumped to 47% according to the UK OIS. By extent, the British pound rallied on the news, erasing the hefty losses it had posted up to that point in the session to trade much higher. Moving forth, considering that investors still view an August hike as a coin toss, incoming UK data could attract even more attention than usual. Their quality could shape market expectations around how the Bank will act and hence, dictate the pound's forthcoming direction – absent any major developments on the Brexit front, of course.

Even though the dollar index touched a fresh 11-month high on Thursday, it did not manage to hold onto its gains, ending the session lower overall. The correction followed a disappointment in the Philadelphia Fed business activity index. Although this is considered a “soft” data point, its unexpected tumble on an otherwise quiet calendar day probably cast doubt on the narrative the US economy grew at 4.7% in Q2 – as signaled by the Atlanta Fed GDPNow model –, thereby triggering some profit-taking in the dollar.

Euro/dollar was on the back foot early on Thursday, as the appointment of two Eurosceptic voices in the Italian parliament reignited political concerns, sending Italian yields higher. However, it rebounded later in the session on the back of a softer dollar. Technically, it appears the world's most traded currency pair is in the process of forming a double bottom near 1.1510. A break above the 1.1840 barrier is needed to confirm such a pattern.

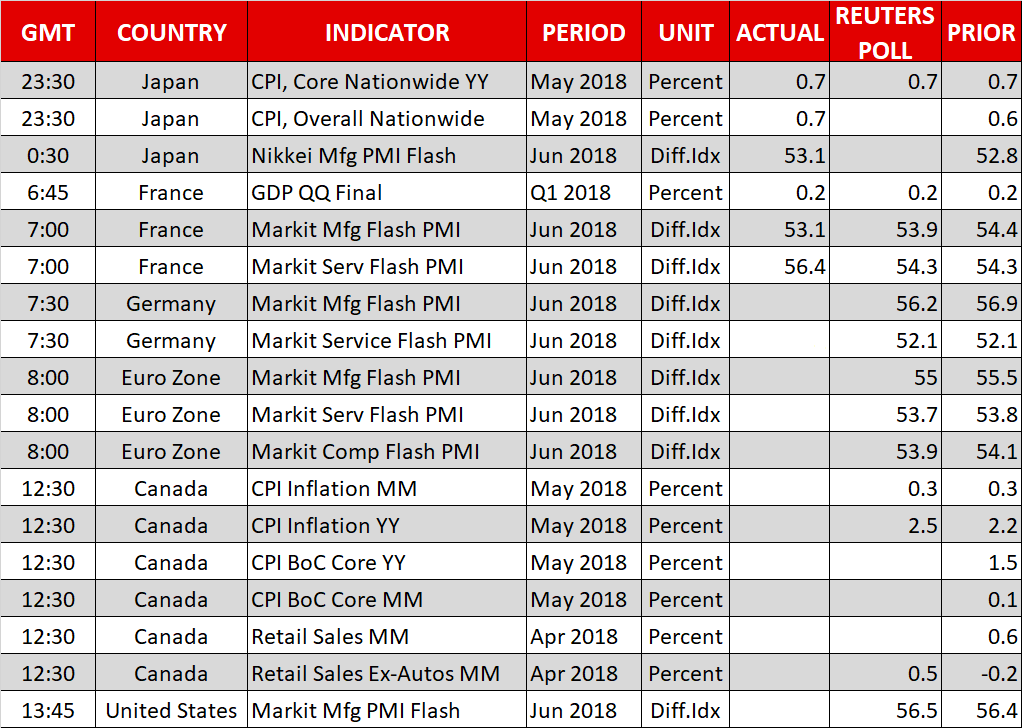

Day ahead: OPEC meeting takes place; eurozone flash PMIs in focus; Canadian CPI & retail sales also attract attention, with US on the receiving end of manufacturing activity data

Friday's calendar features numerous important releases, including June preliminary PMIs out of the eurozone and Canadian inflation & retail sales figures. Meanwhile, the OPEC meeting in Austria will also be firmly in focus, while updates on trade deliberations may also emerge.

The eurozone's flash manufacturing and services PMIs, as well as the composite measure that blends the two sectors, are due at 0800 GMT. All three indices are anticipated to further ease in June. Specifically, if the figures come in line or worse than forecasts, this would mark the sixth straight monthly decline for manufacturing activity and the fifth for services and the composite measure; the latter is viewed as a good overall growth indicator for eurozone economies. Such an outcome would confirm that slowing economic momentum in the euro area as we entered Q2 was not transitory after all. Still, all prints are expected above the 50 level, pointing to positive sectoral growth.

Germany, the eurozone's largest economy will see the release of its respective PMI readings at 0730 GMT, while France (the euro area's second largest economy) saw its corresponding numbers hitting the markets at 0700 GMT. Its manufacturing PMI came in below expectations and the figure for services was a beat; the euro/dollar pair gained after the release. Meanwhile, earlier in the day (0645 GMT), France's Q1 GDP growth was revised down to 0.2% on a quarterly basis, from the 0.3% in the preliminary reading.

At 1230 GMT, the attention will turn to Canada which will see the release of important data on inflation and retail sales. May's headline CPI is projected to grow by 2.5% y/y which would mark a six-year high and compares to April's 2.2%. On a monthly basis, it is forecast to rise by 0.3%. The Bank of Canada has a target band for annual inflation that ranges between 1 and 3%. The core measure of inflation that excludes volatile items and which stood at 1.5% y/y in April, as well as other gauges of price pressures monitored by the BoC – common, median and trimmed CPI – will also be attracting attention.

Regarding retail sales, those are expected to show no growth in April after expanding by 0.6% in March. The same does not hold true for the core measure of sales though, which is forecast to rise by 0.5%, following a contraction by 0.2% in March; core retail sales exclude automobiles.

The Bank of Canada next decides on rates on July 11. Market participants put the odds for a 25bps rate hike during that meeting at roughly 60% according to Canadian OIS. Upbeat data out of Canada today can boost those expectations, consequently supporting the loonie which has suffered considerable losses relative to its US counterpart as of late; the opposite holds true as well.

Markit's manufacturing PMI for the US due out at 1345 GMT is anticipated to slightly edge higher in June and match April's 56.5, this being the highest since late 2014.

The Baker Hughes report on active US oil rigs is due at 1700 GMT. Of far more importance for oil prices though, is expected to be OPEC's two-day meeting which commences today in Vienna; big oil producers that are not OPEC members, such as Russia, will also participate in the meeting. The cartel and its allies will decide on their oil supply policy moving forward.

Lastly, on the trade front, reports suggest some officials within the Trump administration are attempting to resume talks with China ahead of the initial round of tariffs on Chinese imports going into effect on July 6; the goal seems to be avoiding a tit-for-tat escalation that would increase the odds for a trade war. These efforts also exhibit a rift of some sorts within the White House between policy-hawks and those promoting a more moderate stance.

Technical Analysis: USDCAD bullish bias eases; stochastics give negative signal in very short-term

USDCAD has weakened a bit after reaching a one-year high of 1.3335 during Thursday's trading. The short-term bias remains to the upside as indicated by the positively-aligned Tenkan- and Kijun-sen lines, though the flat Kijun-sen points to an easing of momentum. Moreover, the stochastics are giving a bearish signal in the very short-term, with the %K line below the slow %D one and both lines heading lower.

Upbeat releases out of Canada can boost the loonie, weighing on USDCAD. Support to declines could come around the current level of the Kijun-sen at 1.3246, with the 1.32 round figure being eyed in case of steeper declines.

Worse-than-expected figures on the other hand are likely to push the pair higher. Immediate resistance may come around the Tenkan-sen at 1.3308 – including the 1.33 handle – which failed to hold on the way down earlier in the day. Further above, the attention would turn to yesterday's one-year high of 1.3335, with the 1.34 handle increasingly coming into view afterwards.

Eurozone PMI: Services improvement offsets manufacturing, points to 0.5% GDP growth in Q2

Eurozone PMI manufacturing dropped to 55.0 in June, down from 55.5 and met expectation. PMI services rose to 55.0, up from 53.8 and beat expectation of 53.7. PMI composite rose to 54.8, up from 54.1 and beat expectation of 53.9. PMI composite is at a 2 month high while PMI services is at at 4-month high. However, PMI manufacturing is at an 18-month low. Overall, the data point to 0.5% GDP growth in Q2.

Commenting on the flash PMI data, Chris Williamson, Chief Business Economist at IHS Markit said:

"An improved service sector performance helped offset an increasing drag from the manufacturing sector in June, lifting Eurozone growth off the 18- month low seen in May. With growth kicking higher in June, the surveys are commensurate with GDP rising 0.5% in the second quarter.

"Price pressures are also on the rise again, running close to seven-year highs. Increased oil and raw material prices are driving up costs, but wages are also lifting higher, in part reflecting tighter labour markets in some parts of the region. Service sector jobs are being created at the fastest rate seen over the past decade, underscoring the extent to which the job market is tightening.

"However, the details of the survey warn against any complacency. The June uptick could be at least in part explained by business returning to normal after an unusually high number of public holidays in May, suggesting that the underlying trend remains one of slower growth. Business expectations are running at one-and-a-half year lows, and output continues to increase at a faster rate than incoming new orders, all of which suggests that output and employment growth could weaken again in July unless demand picks up again.

"Manufacturing is looking especially prone to a further slowdown in coming months, with companies citing trade worries and political uncertainty as their biggest concerns. Sentiment about the year ahead in the factory sector has sunk to its lowest since 2015.

"While the June upturn provides some hope that the weakening of official data earlier in the year may have overstated the region's weakness, the risks remained tilted towards a further slowdown in the second half of the year."

Germany PMI composite hits 2 month high, clear divergence between manufacturing and services

Germany PMI manufacturing dropped to 55.9 in June, down from 56.9 and missed expectation of 56.3. PMI services rose to 53.9, up from 52.1 and beat expectation of 52.2. PMI composite rose to 54.2, up from 53.4, and hit a 2-month high.

Commenting on the flash PMI data, Phil Smith, Principal Economist at IHS Markit said:

"The headline PMI numbers for Germany make for slightly better reading in June thanks to a pick-up in the pace of expansion in the service sector, though the performance over the second quarter as a whole still looks to be one of only modest growth.

"The big disappoint was manufacturing, where the PMI fell further from last December's record high to the lowest in one-and-a-half years. A worrying slide in export order growth seen since the start of the year continued into June, with the latest survey's anecdotal evidence highlighting quieter client interest from the US and China.

"A clear divergence between manufacturing and services was also seen in the survey's gauge of business confidence. Services firms are in buoyant mood towards the outlook over the next 12 months, but manufacturers see growth continuing to cool and are their least optimistic for over three years."