Sample Category Title

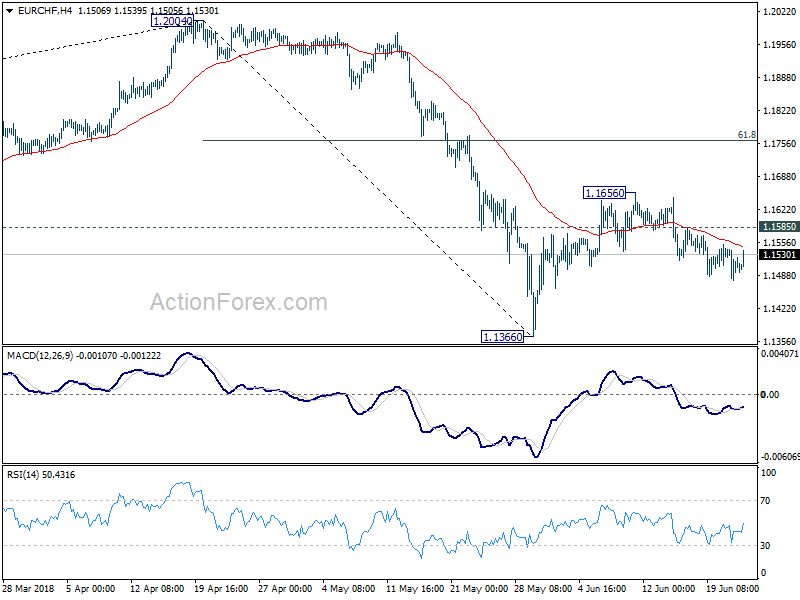

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1477; (P) 1.1512; (R1) 1.1543; More....

No change in EUR/CHF's outlook. With 1.1585 minor resistance intact, deeper fall is in favor for 1.1366 support. Break there will resume the corrective fall from 1.2004. On the upside, though, above 1.1585 will likely extend the rebound from 1.1366 through 1.1656. But in that case, upside should be limited by 61.8% retracement of 1.2004 to 1.1366 at 1.1760.

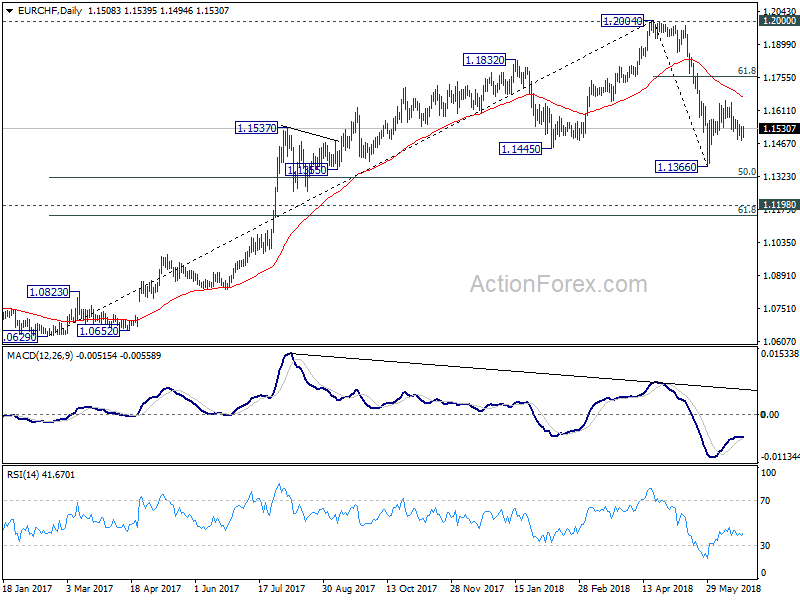

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

Strategy: The Implications Of A Global Trade War

Todays key points

- A further escalation of the trade tensions has become our baseline scenario ahead of 6 July.

- The escalation will weigh on global economic growth.

- Equity volatility will be high, with downside risks for equities near term.

- Industrial and agricultural commodities are primarily at risk.

- The prospects of a stronger USD, lower commodity prices and weaker global growth weigh on emerging markets

Rising risk of a full-blown trade war

Rising risk of a full-blown trade war This week saw a dramatic escalation of the trade dispute between the US and China. The US administration upped the rhetoric against China by saying that if China retaliates against the new US tariffs on 6 July, the US is prepared to slap additional 10% tariffs on up to USD400bn of Chinese exports to the US. The Chinese side has clearly signalled a readiness to respond with equal measures ). With no negotiations in sight at the moment, our base case is shifting to a further escalation of the trade conflict between the two countries. There is a risk of deterioration in relations between the two sides already on 30 June when the US is due to announce its plan to restrict Chinese investments into the US and to limit exports of US tech products to China.

Can such an escalation be avoided? We remain sceptical. Firstly, there appears to be little trust between the two sides, notably on the Chinese side, after the US turned its back on the negotiated trade deal last month. Secondly, Trump is increasingly leaning towards trade and China hawks such as Peter Navarro, US Trade Representative Robert Lighthizer and National Security Advisor, John Bolton. However, Trump has previously made sudden changes in tactics (think of North Korea and this week on immigration), but we still only assign a 10-20% probability for new negotiations and a possible defusing of the trade tensions between the two sides.

Trade tensions between Europe and the US are also at risk of escalating. The EU has adopted a 25% tariff on EUR2.8bn of US goods (jeans, motorcycles, Bourbon whisky and several commodities) today in response to the US tariffs on steel and aluminium import from EU countries. This may well trigger countermeasures from Trump as with China, which could include tariffs on European car exports (read: from Germany) causing another retaliation from the EU and so on. Several emerging market countries such as Turkey, India and Russia have recently adopted countermeasures to US steel and aluminium tariffs.

Downside risks to global growth from escalation of trade tensions

We think global growth is likely to take a sizable hit from an escalation of the trade war between the US and China (and possible other countries). In the event of US tariffs on USD450bn of Chinese goods and China retaliation with measures of equal size, both exports between the two countries as well as business confidence will be hit, hampering investments and consumer spending, also globally. The impact of a more restrictive global trade regime will be felt most acutely in surplus countries (i.e. China, manufacturing Emerging Markets and Germany). We see the risk of a fall in global growth of between 0.25-0.50% (assuming central banks weather part of the shock).

Indeed, central banks are starting to sound concern about the economic outlook in face of the risk of an escalation in trade tensions. This became clear at this week’s gathering of global central bankers at the Sintra conference in Portugal. Fed Chair Jerome Powell said that trade tensions “could cause us to have to question the outlook”, while the ECB’s Mario Draghi said that “for the first time we are hearing (from business leaders) about decisions to postpone investment, postpone hiring, postpone making decisions.” The Chinese central bank signalled this week a possible monetary policy easing perhaps already this weekend in response to the possible hit from the trade frictions with the US. In our view, other large central banks could take similar steps should growth weaken materially in the wake of trade restrictions. With uncertainty on the trade relations between major economies, we think volatility in equity markets will be markedly higher. There would be downside risk for equities in the event of an escalation of trade tensions.

Industrial and agricultural commodities are primarily at risk

An escalation of the trade war creates a downside risk to commodity prices. Prices on industrial commodities, e.g. aluminium and steel, and agricultural commodities, e.g. soybean, will suffer directly from the imposed tariffs, which will reduce global demand for these commodities. If an escalation leads to a significant setback in the total volume of global trade, then oil prices are also at risk as fuel demand in shipping would take a hit.

Emerging markets vulnerable to trade tensions

Emerging markets were already on the back foot before this week’s growing trade war concerns. Investors had become more cautious in the wake of higher US rates and USD especially the more vulnerable EMs like Turkey, Brazil and Argentina. And this week’s rising risk of global trade war certainly hasn’t helped. We think sentiment toward EMs will remain fragile until 6 July, when the trade war between the US and China could escalate. If the trade war indeed broadens, manufacturing EMs with high export exposure would suffer the most (Eastern Europe and Asian countries in particular). Poland has a bigger domestic market than other CEE economies, which will ease the trade war impact on PLN. It should, however, be noted that the macro situation in emerging markets is generally stronger than ten years ago, boasting lower inflation, less FX exposure, advanced adjustment to Fed tightening, more independent central banks and a larger share of multilateral trade with other EM partners. Should the chance of negotiations between the US and China re-appear, the EM could see a significant relief rally.

Euro susceptible to an escalation in trade tensions.

With the risk of a more wide-raging trade war rising lately, the risk of its FX implications shifting has risen. At the start of the year the trade dispute was largely associated with a political push for a weaker dollar – and if anything helped to add to the ‘America first’ risk premium, which Trump has in our view introduced on USD. But as the risk of a bigger hit to confidence and activity globally is looming, the open euro-area economy may be up for a bigger hit growth-wise than the US, which could in turn weigh on EUR/USD (even if the ECB has been arguing the opposite, see speech by Benoît Coeuré, a April 2018). We still think the cross is capped largely at 1.15 but a possible global trade war (especially if the US decides to impose further tariffs on EU goods this weekend), uncertainty about Italy and higher USD carry remain downside risks.

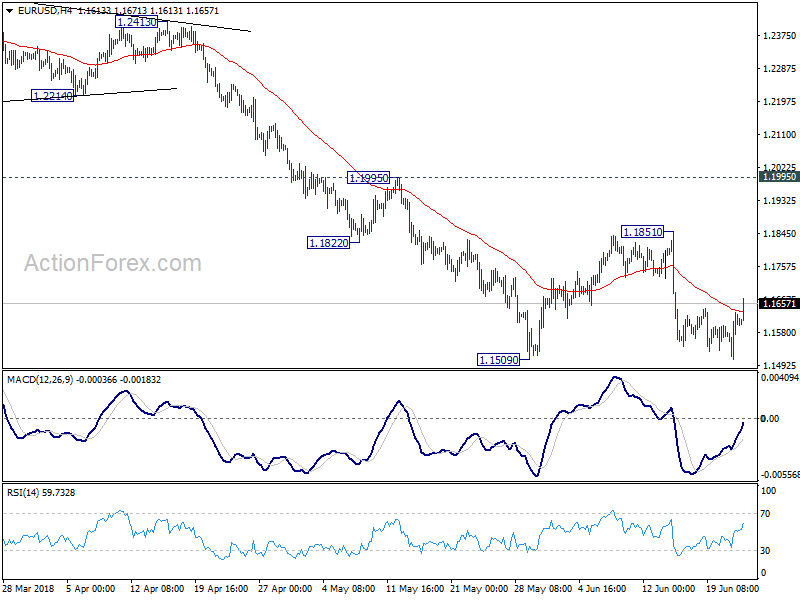

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1531; (P) 1.1582 (R1) 1.1655; More.....

EUR/USD rebounds further today as consolidation pattern from 1.1509 is extending. While further rise cannot be ruled out, upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

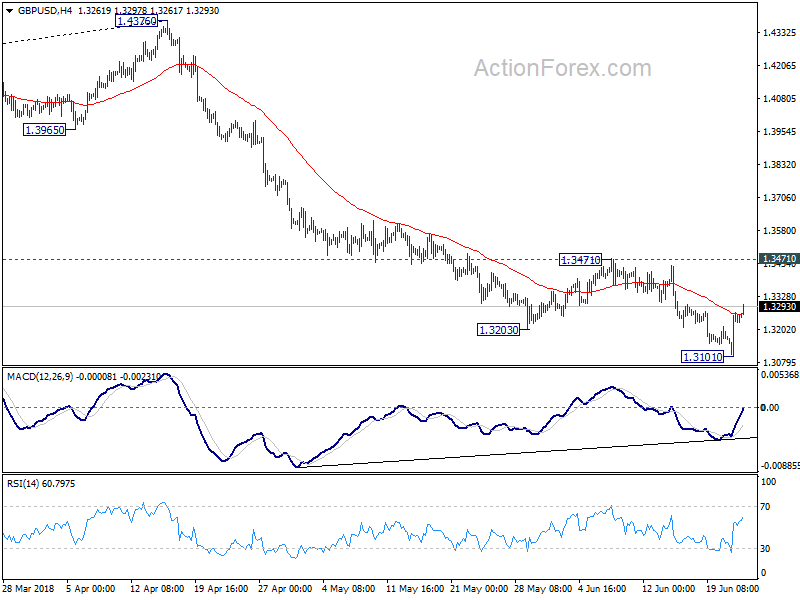

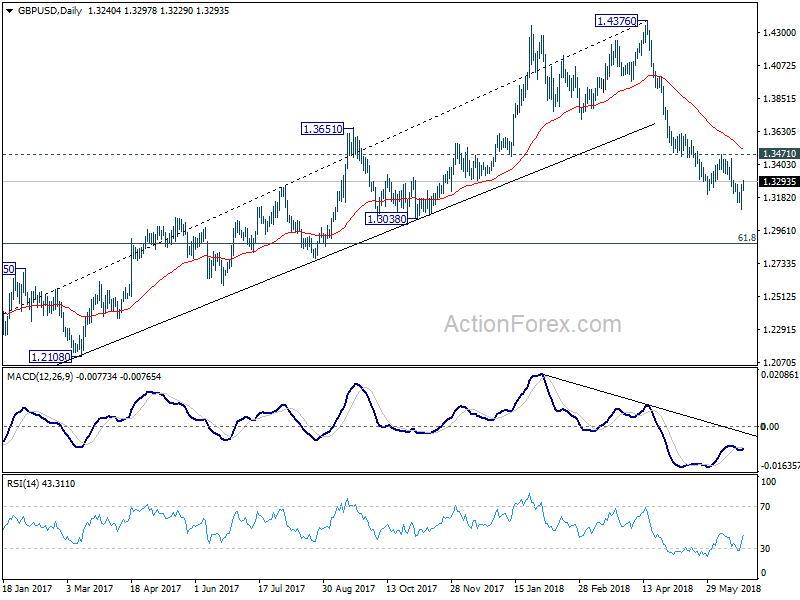

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3139; (P) 1.3205; (R1) 1.3308; More...

GBP/USD's rebound from 1.3101 temporary low is in progress and could extend higher. Still, near term outlook will remain bearish as long as 1.3471 resistance holds. And larger decline is expected to continue. On the downside, break of 1.3101 will resume the fall from 1.4376 for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

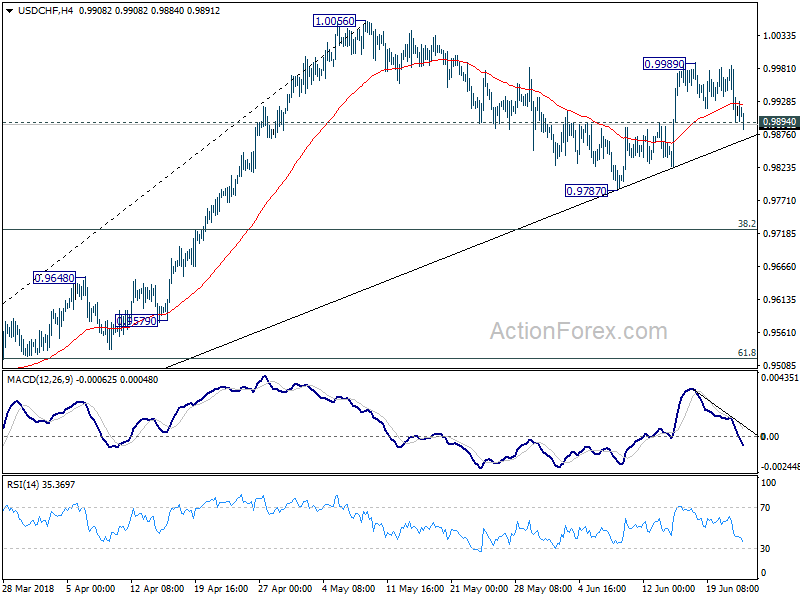

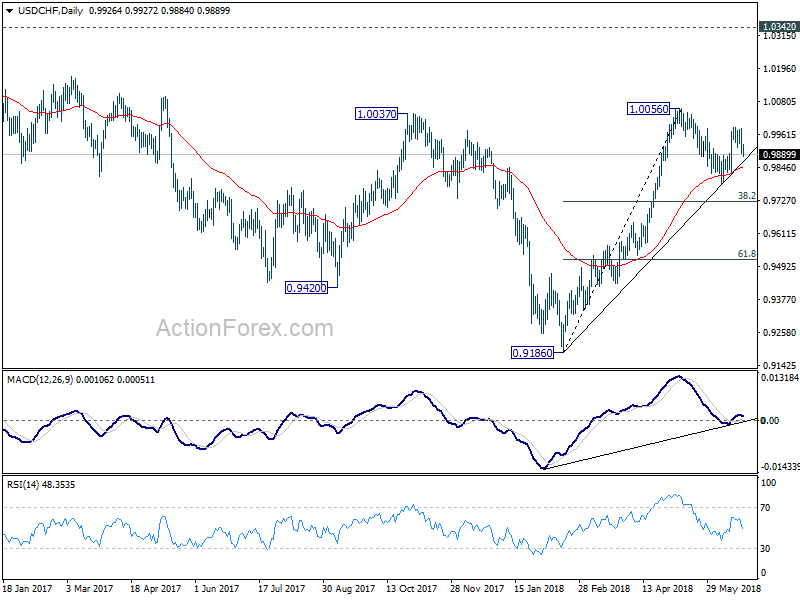

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9882; (P) 0.9934; (R1) 0.9971; More...

USD/CHF's break of 0.9894 minor support suggests that rebound from 0.9787 is completed at 0.9989. And, correction from 1.0056 is extending. Intraday bias is turned back to the downside for 0.9787 support and possibly below. But we'd expect strong support from 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to contain downside to bring rebound. On the upside, break of 0.9989 will target a test on 1.0056 first. Break will resume whole rise from 0.9186.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

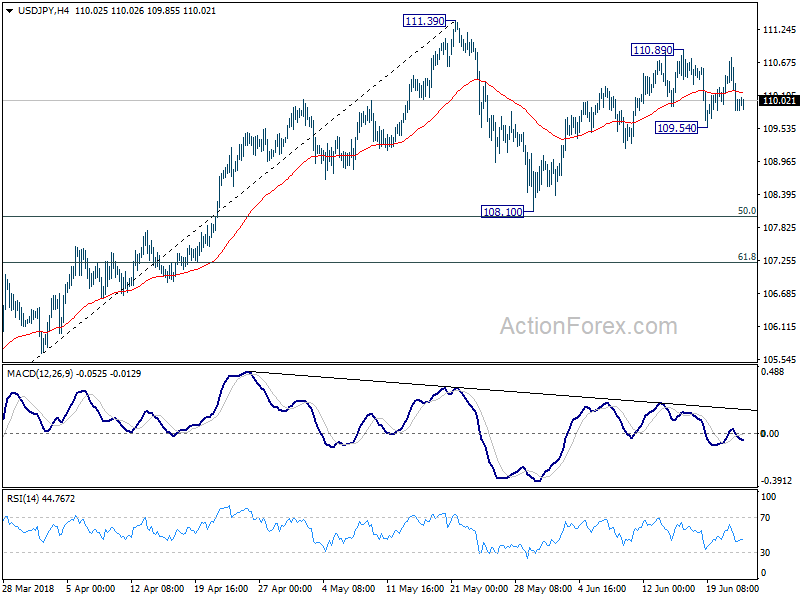

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.62; (P) 110.19; (R1) 110.55; More...

USD/JPY is staying in range of 109.54/110.89 and intraday bias remains neutral first. On the downside, below 109.54 will extend the corrective pattern from 111.39 with another falling leg to 108.10 and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39. But we'd be cautious on strong resistance from there to limit upside.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

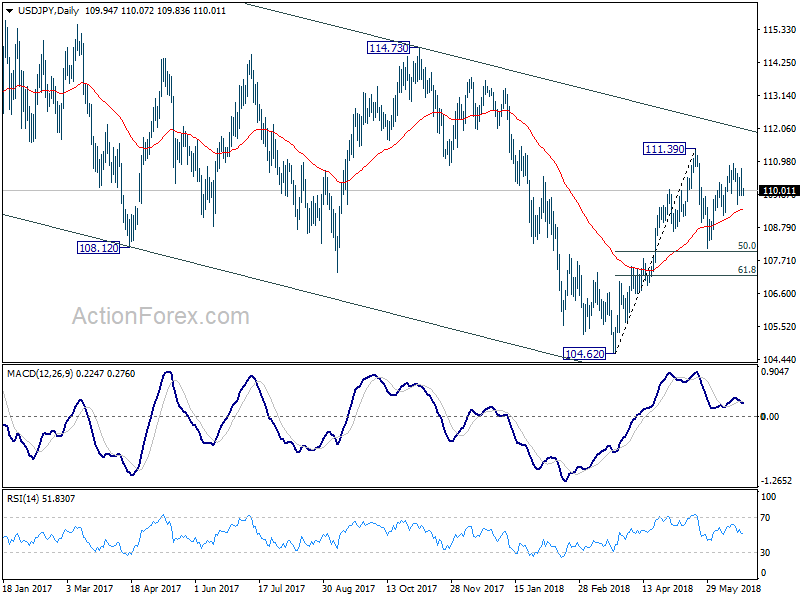

Eurozone Consumer Confidence Drops To Lowest Reading Since October

For the 24 hours to 23:00 GMT, the EUR rose 0.28% against the USD and closed at 1.1608

On the macro front, the Euro-zone's preliminary consumer confidence index unexpectedly declined to a level of -0.5 in June, amid trade war fears, Italian political crisis and marking its lowest reading since October 2017. The PMI had registered a rise of 0.2 in the prior month, while market participants had envisaged for a flat reading.

Macroeconomic data showed that the number of Americans filing for fresh unemployment benefits dropped more-than-anticipated to a level of 218.0K in the week ended 16 June, compared to market expectations for a drop to a level of 220.0K. Initial jobless claims had registered a revised level of 221.0K in the prior week. Meanwhile, the nation's Philadelphia Fed manufacturing index fell higher-than-expected to a level of 19.9 in June, weighed down by a sharp drop by the new orders index and defying market consensus for a fall to a level of 29.0. The index had registered a reading of 34.4 in the prior month. Other data showed that, the leading index rose less-than-expected 0.2% on a monthly basis in May. The index had registered a rise of 0.4% in the prior month, while markets had envisaged the index to rise by 0.4%.

In the Asian session, at GMT0300, the pair is trading at 1.1605, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.1531, and a fall through could take it to the next support level of 1.1458. The pair is expected to find its first resistance at 1.1656, and a rise through could take it to the next resistance level of 1.1708.

Going ahead, market participants would keep a close watch on the release of flash Markit manufacturing and services PMI, for June, across the Euro-zone. Additionally, the US flash manufacturing and services PMI for June, set to release later in the day, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

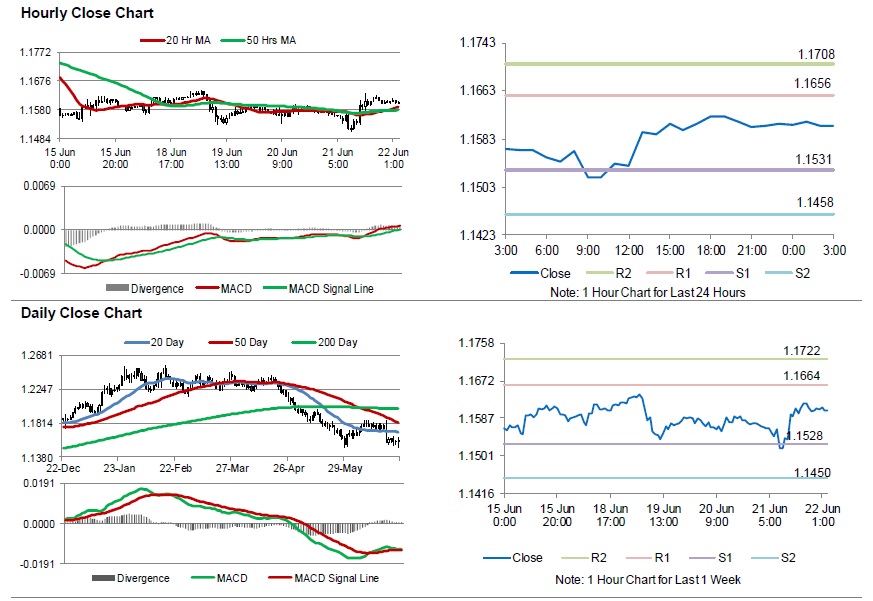

BoE Leaves Benchmark Interest Rates Unchanged, BoE, Chief Economist Raises Prospects Of August Rate Hike

For the 24 hours to 23:00 GMT, the GBP rose 0.57% against the USD and closed at 1.3247.

Yesterday, the Bank of England (BoE), at its June monetary policy meeting, opted to keep its key interest rates unchanged at 0.50%, in a split vote while all nine officials voted to maintain its asset purchase facility at £435.0 billion. Meanwhile, the Bank of England’s Chief Economist, Andy Haldane unexpectedly supported the hawks calling for an immediate interest-rate increase, defying the majority of policymakers who voted to keep the rate unchanged. The minutes of the meeting revealed that policymakers expect that any future increases in the rate are likely to be at a gradual pace and to a limited extent.

Data released showed that UK’s public sector net borrowing has recorded a deficit of £3.4 billion in May, while markets had envisaged for a deficit of £5.0 billion. In the previous month public sector borrowings registered a revised deficit of £5.3 billion.

In the Asian session, at GMT0300, the pair is trading at 1.3257, with the GBP trading 0.08% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3149, and a fall through could take it to the next support level of 1.3042. The pair is expected to find its first resistance at 1.3317, and a rise through could take it to the next resistance level of 1.3378.

Going forward, investors would await Britain’s final GDP and consumer confidence data, slated to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

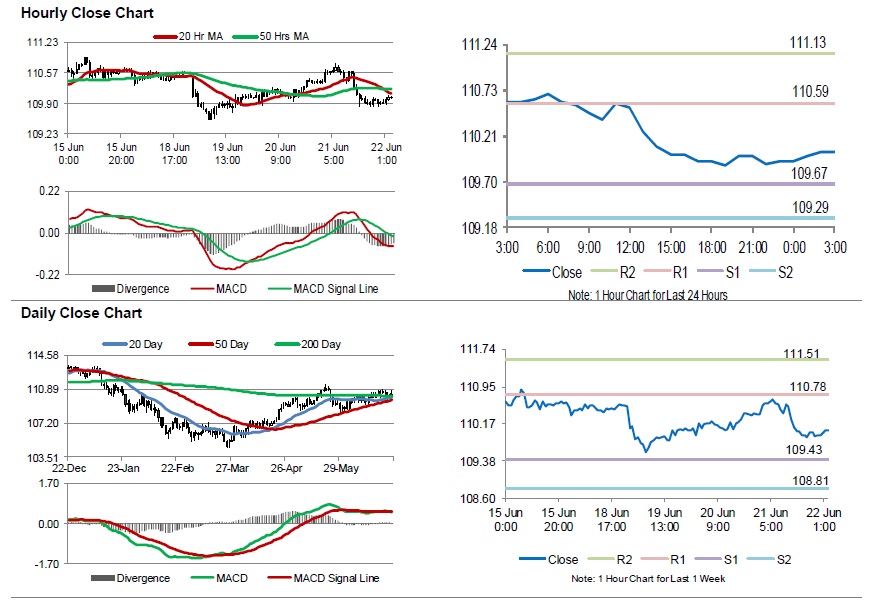

Japanese Yen Trading A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.42% against the JPY and closed at 109.92.

On the data front, Japan’s final machine tool orders advanced 14.9% on an annual basis in May, confirming the preliminary print. In the previous month, machine tool orders had registered a rise of 22.0%.

In the Asian session, at GMT0300, the pair is trading at 110.04, with the USD trading 0.11% higher against the JPY from yesterday’s close.

Overnight data revealed that Japan’s national consumer price index (CPI) rose more-than-anticipated to 0.7% on an annual basis in May, compared to a gain of 0.6% in the prior month. Markets consensus was for the CPI to climb 0.6%.

Earlier in the session, the nation’s Nikkei flash manufacturing PMI advanced to a level of 53.1, compared to a reading of 52.8 in the previous month. Meanwhile, all industry activity index climbed 1.0% on a monthly basis in April, more than market expectations and compared to a flat reading in the previous month.

The pair is expected to find support at 109.67, and a fall through could take it to the next support level of 109.29. The pair is expected to find its first resistance at 110.59, and a rise through could take it to the next resistance level of 111.13.

Moving ahead, traders would closely monitor Japan’s jobless rate, industrial production and consumer confidence all set to release next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

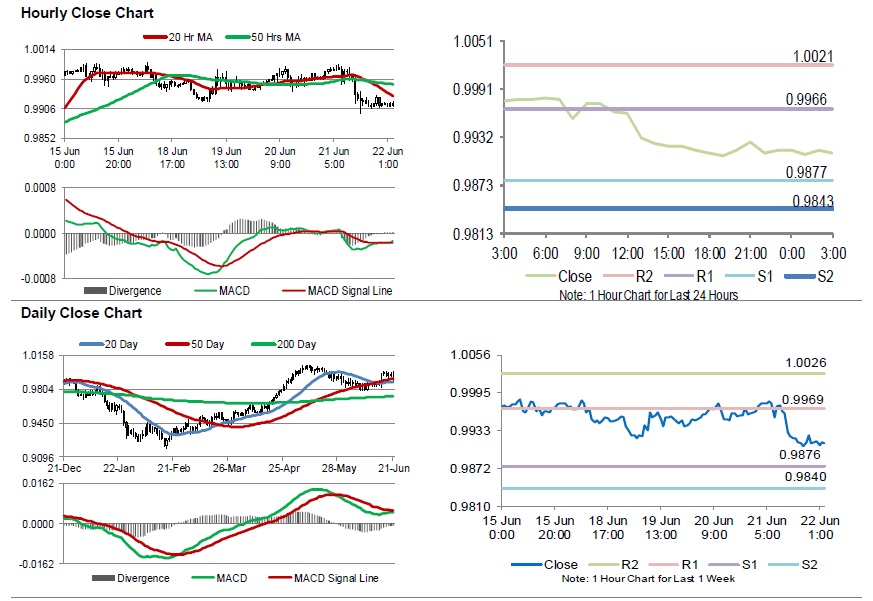

SNB Kept Key Interest Rates Unchanged At -0.75%

For the 24 hours to 23:00 GMT, the USD declined 0.46% against the CHF and closed at 0.9915.

Yesterday, the Swiss National Bank (SNB), at its March monetary policy meeting, held its benchmark interest rate unchanged at -0.75%, as widely expected. In its policy statement, the central bank pointed to loose policy over longer term. Meanwhile, the SNB lowered its medium-term forecast for Swiss inflation.

On the macro front, Switzerland’s trade surplus widened to a level of CHF2.76 billion in May. The nation had posted a revised surplus of CHF2.25 billion in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9912, with the USD trading a tad lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9877, and a fall through could take it to the next support level of 0.9843. The pair is expected to find its first resistance at 0.9966, and a rise through could take it to the next resistance level of 1.0021.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.