Sample Category Title

Minneapolis Fed Kashkari doubts long term impact of tax cut

Minneapolis Fed President Neel Kashkari expressed his doubts on the long term effect of Trump's USD 1.5T package of corporate and individual tax cuts. In an event at African Development Center of Minnesota, he said "we know if you cut taxes on the margin that should boost economic growth in the short term." However, "the question is when that short term is over, does it actually lead to longer-term, higher sustained economic growth? That's unclear right now."

He also points to the information he got from businesses. Kashkari said while business leaders "are more optimistic than I had expected," they are also saying that lower tax rates have not led them to make new investments, at least not yet. He added "I am asking businesses 'are you actually investing more?' And so far the answer that I've heard is 'we're waiting to see.'"

https://www.youtube.com/watch?v=ze8kjcWw6kk

Japanese Yen Higher, Japan Inflation Data Next

The Japanese yen has posted gains in the Thursday session. In the North American trade, USD/JPY is trading at 110.01, down 0.31% on the day. On the release front, key U.S indicators were mixed. The Philly Fed Manufacturing Index slid to 19.9 points, its lowest level since August. There was better news on the employment front, as unemployment claims remained unchanged at 218 thousand, beating the estimate of 220 thousand. In Japan, National Core CPI is expected to remain at 0.7%, and PMI Flash Manufacturing is forecast to tick up to 52.6 points. On Friday, OPEC members meet in Vienna.

The Bank of Japan plans to hold the course on monetary policy, according to the minutes of the BoJ’s April policy meeting. At the meeting, policymakers maintained interest rates at -0.10%. As well, the bank also dropped the timeframe for achieving its inflation target of 2 percent, a signal that the bank has no plans to increase stimulus. The minutes indicated that most members wanted to maintain current monetary policy, holding rates at -0.10% and the 10-year bond yield around zero percent. BoJ policymakers appear resigned to the fact that the inflation target will not be reached anytime soon, but the BoJ nevertheless is sticking to its 2 percent target.

The escalating trade spat between the U.S and its trading partners has shaken up the markets, as unnerved investors monitor developments. The Japanese yen is traditionally a safe-haven asset in times of trouble, the currency has recorded limited gains against the U.S dollar. Although President Trump has not imposed import tariffs on Japan, the Japanese economy depends heavily on exports, and a rash of tariffs would take a toll on growth. In the latest salvo in the trade war rhetoric, Trump has threatened China with a 10 percent tariff on some $200 billion in Chinese goods.

Emerging Market and Risk Sensitive Currencies Take a Hit from Rising Trade Tensions

The United States and China came one step closer to an all-out trade war this week after the Trump administration announced counter tariffs to China’s retaliation to the US’s 25% tariffs on $50 billion of Chinese goods, when they matched it with similar levies. Until now, the growing rift in trade policy between the world’s two largest economies had been met by only modest responses in financial markets. However, following the latest exchange of heated rhetoric, market participants may have gotten a taste of what could come if the dispute was to escalate to a wider trade conflict.

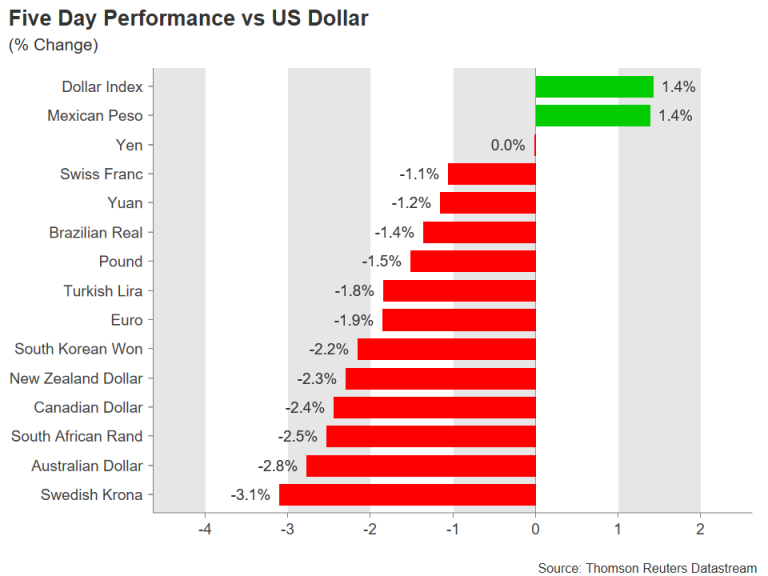

With the US economy in strong shape and imports far outstripping exports, traders don’t appear too concerned about the possible impact of higher tariffs on the American economy. The US dollar has risen sharply against most of its peers this week, with the exception of the safe-haven yen. The dollar index, which measures the greenback against a basket of six major currencies, scaled an 11-month high of 95.53 on Thursday.

In contrast, countries that are heavily reliant on trade have seen their currencies tumble in recent days on concerns that increased protectionism would harm global trade and therefore, economic growth. The risk sensitive Australian dollar has been one of the worst hit among advanced economies, falling by 2.8% over the past week, as Australian exports stand to lose considerably if a trade war was to badly hurt the Chinese economy. Aussie/dollar fell to a 13-month low of $0.7342 this week on the back of an increase in risk aversion. The aussie has already lost significant appeal amid a widening yield differential between US and Australian government bond yields.

The Canadian dollar has also taken quite a beating this week, slumping to a one-year low of C$1.3334 per US dollar. With US-Canadian relations currently at a low point, the prospect that the two nations would be able to resolve their differences over NAFTA is looking grimmer after the US responded angrily to China’s countermeasures and announced an additional $200 billion worth of tariffs. Canada sells more than half of its exports to the US and could face an economic crisis if the US decided to extend the tough line to NAFTA and pull out of the trilateral accord. A further potential blow for the loonie could come from lower oil prices if a trade conflict was to dent global demand for oil.

Another casualty has been the Swedish krona. The Nordic currency is perhaps a more unlikely victim of the heightened trade tensions and has plunged by about 3% over the past week, falling to a 3-week low of 8.9499 kronor per dollar. Like Germany, Sweden’s economy is also highly dependent on exports to drive growth and is a major producer of machinery, vehicles and electrical equipment. If President Trump decided to turn his focus on the German car industry as his next target, Swedish exporters would suffer too as any new auto duties would apply for the whole of the European Union.

Among emerging markets, the South African rand, the Turkish Lira and the South Korean won are the biggest losers from the latest market panic about a possible trade war. Although EM economies are not in the direct firing line of Trump’s trade policy, a decline in world trade as a result of higher import duties in the big trading blocs would inevitably spill over to emerging markets. However, the EM currencies coming under most pressure are those with existing weaknesses and so their sell-off is being exasperated by trade concerns rather than being entirely driven by them.

For example, the rand has been reeling from a large shock contraction in South African GDP in the first quarter, following the data released earlier in June. In Turkey, the lira has only just managed to stabilize from a freefall after the country’s central bank finally took firm action to prevent capital outflows. The Turkish lira, along with the Argentine peso was the worst hit from the emerging market outflow set off by rising US rates and treasury yields back in May. Investor angst ahead of Turkish presidential elections on Sunday are also weighing on the lira.

The South Korean won meanwhile has fallen mainly on worries that lower Chinese exports to the US would have a knock-on effect on Korean manufacturers. South Korea is one of the largest exporters of intermediate goods to China, which are then used in finished products to be sold to the US. If the US went ahead with its threat and imposed tariffs on an additional $200 billion of Chinese products, that could have a more far-reaching impact on Chinese exports than the existing levies and hurt not just China but the regional economy in Southeast Asia as well.

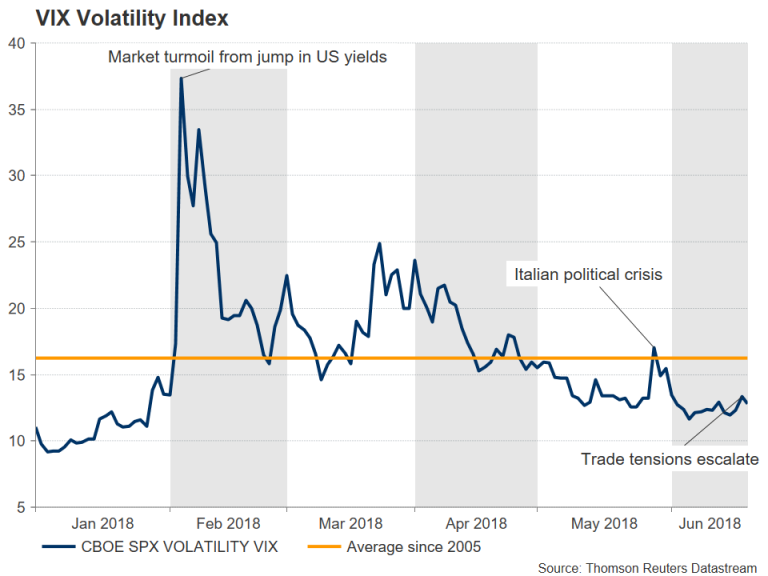

Looking at the broader markets, the fallout of the growing trade spat remains fairly contained. The VIX volatility index briefly spiked to a 2½-week high of 14.68 on Tuesday as the trade row started brewing again. However, this is far below the peak of 50.30 seen at the height of the turmoil in early February when soaring US yields triggered a sell-off in bonds and equities. And while the tariffs have had a notable drag on certain stock sectors, equities in general have held up reasonably well against the protectionist backdrop. The only exception are Chinese stocks, which have plunged to one-year lows on worries about restricted access to the US market for Chinese firms.

It can be concluded therefore that trade frictions have so far only managed to dampen risk sentiment and there’s no signs yet of economic growth forecasts being revised lower. Most investors are still holding the view that the latest US actions are part of a negotiating strategy and President Trump will back down once he secures better trade deals with other nations.

However, even if a trade war is averted, prolonged uncertainty about the trade outlook and higher tariffs in the interim could start to take their toll on the US economy. If these were to raise fears of a slower pace of rate increases by the Fed and at worst, a US downturn, the market fallout would be far greater than what has been seen already as this would go against the dominant theme that has prevailed since the start of the year, which is that the US economy is the only one that’s outperforming, leaving the Fed as the sole central bank that can repeatedly raise borrowing costs.

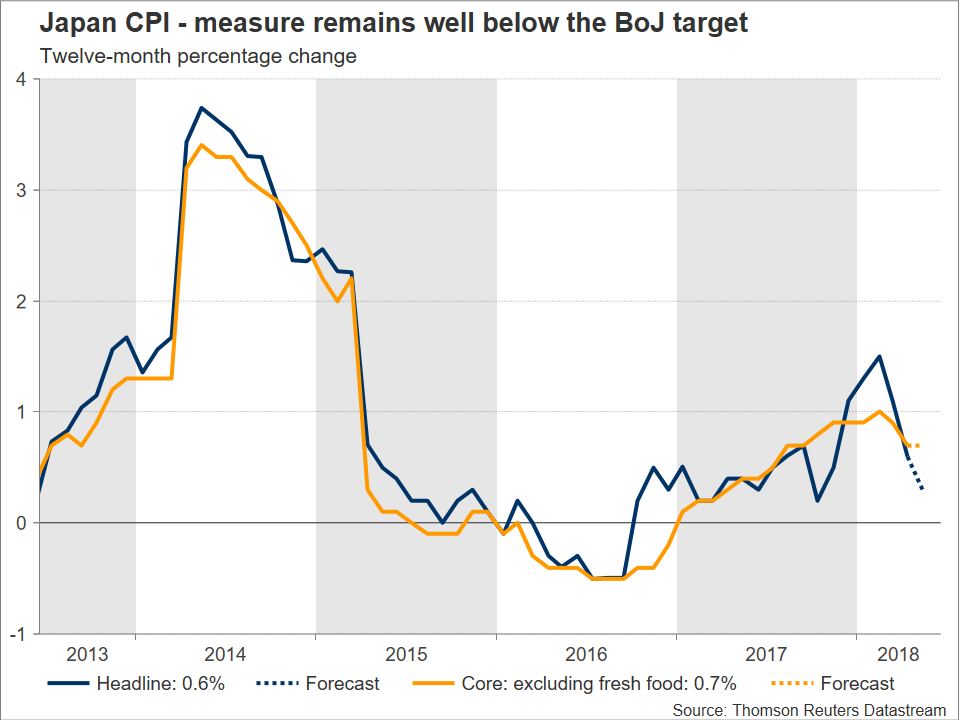

Japanese Inflation to Confirm Bank of Japan Remains Long Way from Policy Normalization

Japanese inflation data for May are scheduled for release on Thursday at 2330 GMT. Overall, the numbers are expected to confirm that the Bank of Japan remains far off from its inflation target. Consequently, further monetary policy divergence between the Japanese and US central banks is to be anticipated moving forward, something which favors a stronger dollar/yen pair.

Thursday’s figures out of Japan are projected to show headline inflation as gauged by the consumer price index (CPI) falling to 0.3% y/y in May from April’s 0.6%. Meanwhile, core CPI is forecast to grow at 0.7% y/y for the second straight month; this is the measure that excludes fresh food items but includes energy and which is targeted by the BoJ in its policymaking. This compares to the central bank’s target for inflation of 2% on an annual basis.

Up to (and including) February, price pressures were on the rise in Japan – headline and core CPI grew by 1.5% and 1.0% during the month –, spurring speculation that the country’s central bank was edging closer to entering a path of policy normalization after years of ultra-loose monetary policies. However, the “excitement” was relatively short-lived, with the measures of inflation being in retreat mode ever since. As a consequence, during last week’s meeting on monetary policy, the BoJ downgraded its assessment on inflation, saying it expects consumer price growth to remain in a range of “0.5-1.0%”, from “around 1.0%” which was the view held during April’s meeting; the BoJ seems “locked” into ultra-accommodative policies for the foreseeable future.

Contrast this with the US central bank which remains firmly on policy-tightening mode, having recently delivered its seventh quarter percentage point interest rate increase since it began hiking rates in late 2015, and is projecting a steeper rate path in 2018 than previously thought. All these are pointing to policy divergence between the US and Japan reaching new heights, translating into higher yield differentials (in the US’ favor of course) and being supportive of a stronger USDJPY moving forward.

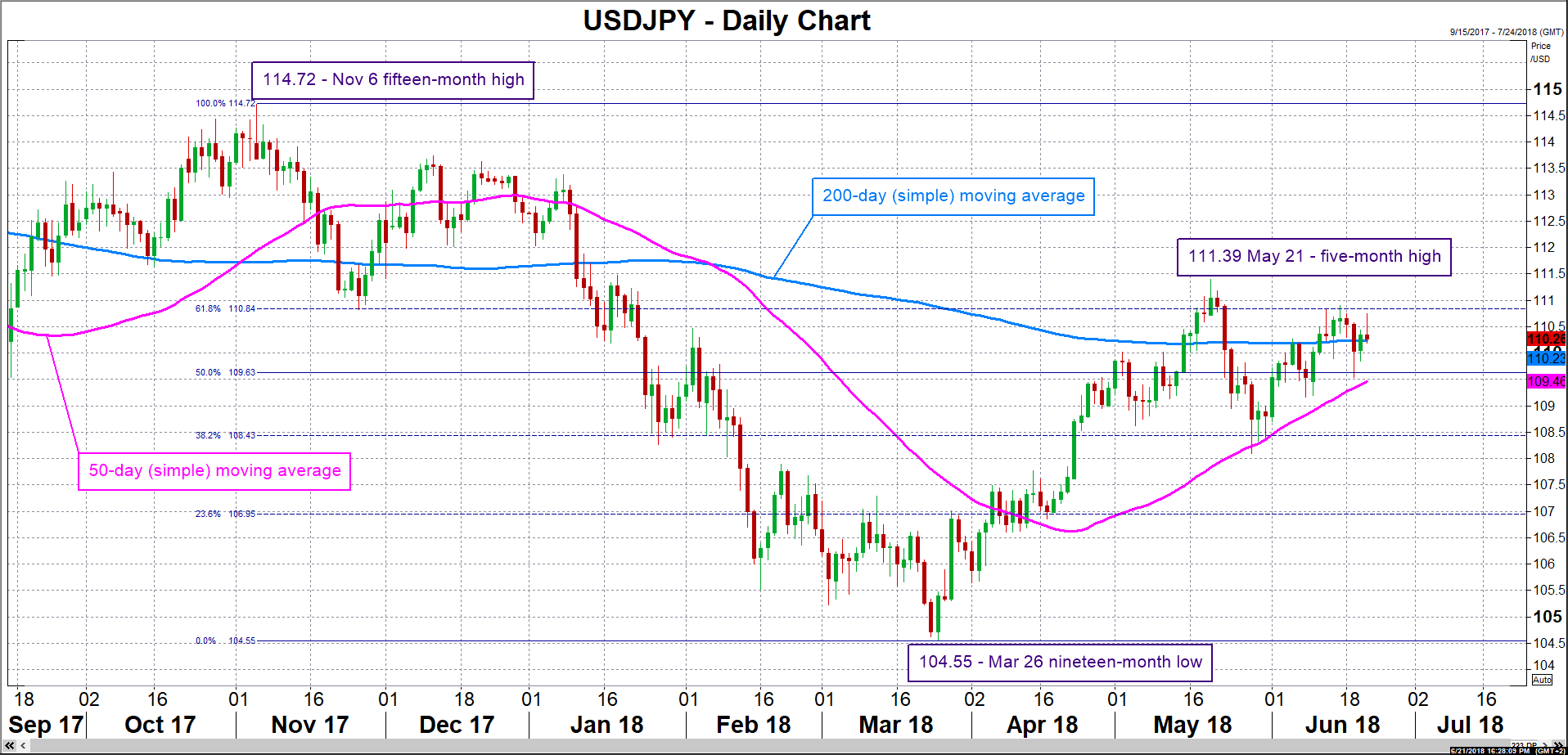

Turning to FX markets and focusing on dollar/yen, an advancing pair may meet resistance around the 61.8% Fibonacci retracement level of the November 6 to March 26 downleg at 110.84, with the region around this point encapsulating the 111 round figure as well. Stronger bullish movement would turn the attention to the May 21 five-month high of 111.39 and then to the 112 handle. On the downside, immediate support seems to be coming around the current level of the 200-day moving average at 110.23, including the 110 handle. Further below, the area around the 50.0% Fibonacci mark at 109.63, which also includes the 50-day MA at 109.46, would be eyed next.

Lastly, although a CPI beat has the capacity to boost the yen (of course the opposite holds true for a data miss) and bring into scope the abovementioned technical levels, it should be noted that the Japanese currency hasn’t been that sensitive to data releases lately. Instead, safe-haven inflows (or outflows) have been the name of the game for the yen. In this respect, the US-China trade spat has acted as a catalyst driving funds into the safe-haven perceived yen (thus weighing on dollar/yen) over the last number of months – whenever tensions are on the rise that is. Therefore, further escalation of tensions is likely to be met with a depreciating USDJPY, with easing concerns having the opposite effect.

Eurozone’s PMIs Expected to Lose More Steam, Keeping Euro Under Pressure

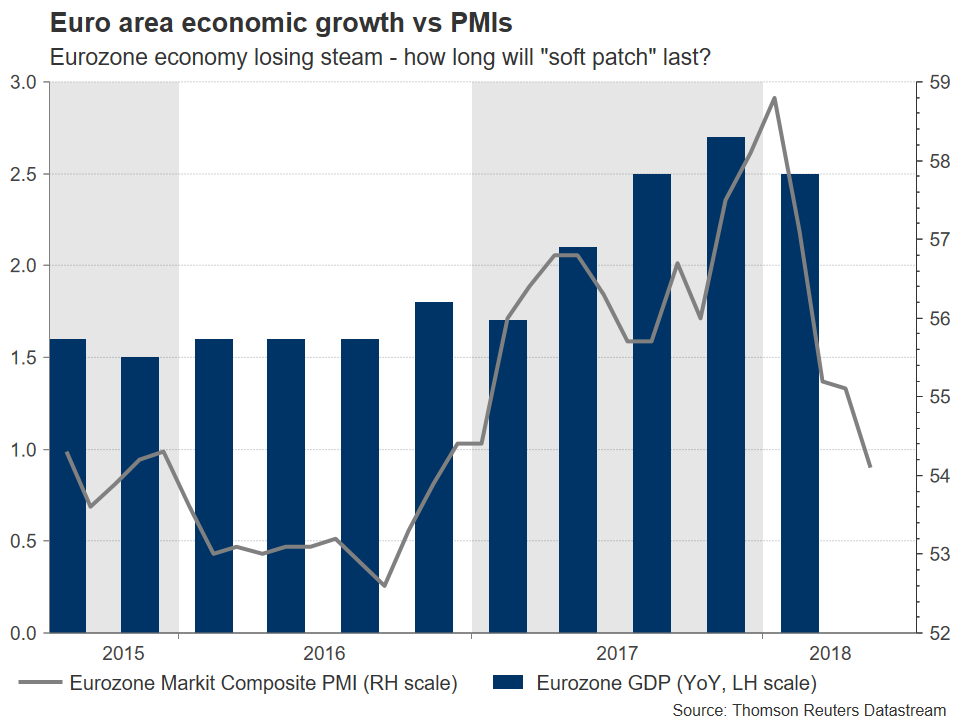

The Eurozone will see the release of its preliminary PMI figures for June on Friday, at 0800 GMT. Forecasts suggest the surveys may signal a further slowdown in the Eurozone’s growth momentum, and although that may not be much of a surprise for ECB policymakers, it may be another factor weighing on the already-battered euro.

It’s no secret the Eurozone’s economy has lost momentum since the beginning of the year. While growth rates are still decent, the currency bloc has clearly shifted down gears, a development the European Central Bank (ECB) has dubbed as a “soft patch” that it expects will fade soon. As such, investors will keep a close eye on the bloc’s Purchasing Managers Indices (PMIs) by HIS Markit for June, to determine whether the slowdown subsided, or intensified further at the end of Q2.

In June, the Eurozone’s preliminary manufacturing PMI is forecast to edge lower to 55.0 – from 55.5 in May, touching an 18-month low. Meanwhile, the services print is expected to tick lower to 53.7 from 53.8 previously, dragging the Composite index – that blends the two measures – down to 53.9, from 54.1 in May.

Besides a moderating economic outlook, business sentiment is likely to have been hit by a combination of trade and political risks. As Germany’s ZEW survey for June pointed out, financial experts are spooked by a potential trade dispute with the US, and the new Italian government pursuing destabilizing policies; concerns likely to be echoed in the PMIs too.

While a further decline in the PMIs may not come as a shock to ECB officials, given that President Draghi recently noted the soft patch may last longer than expected, it would still be a factor arguing for the first ECB rate increase to come later rather than sooner. Market pricing currently suggests the Bank will touch the rate-hike button only in Q4 2019, when it is anticipated to hike rates by a modest 10bps. Anything that pushes that timing back – for instance another set of soft PMIs – could work to the detriment of the common currency.

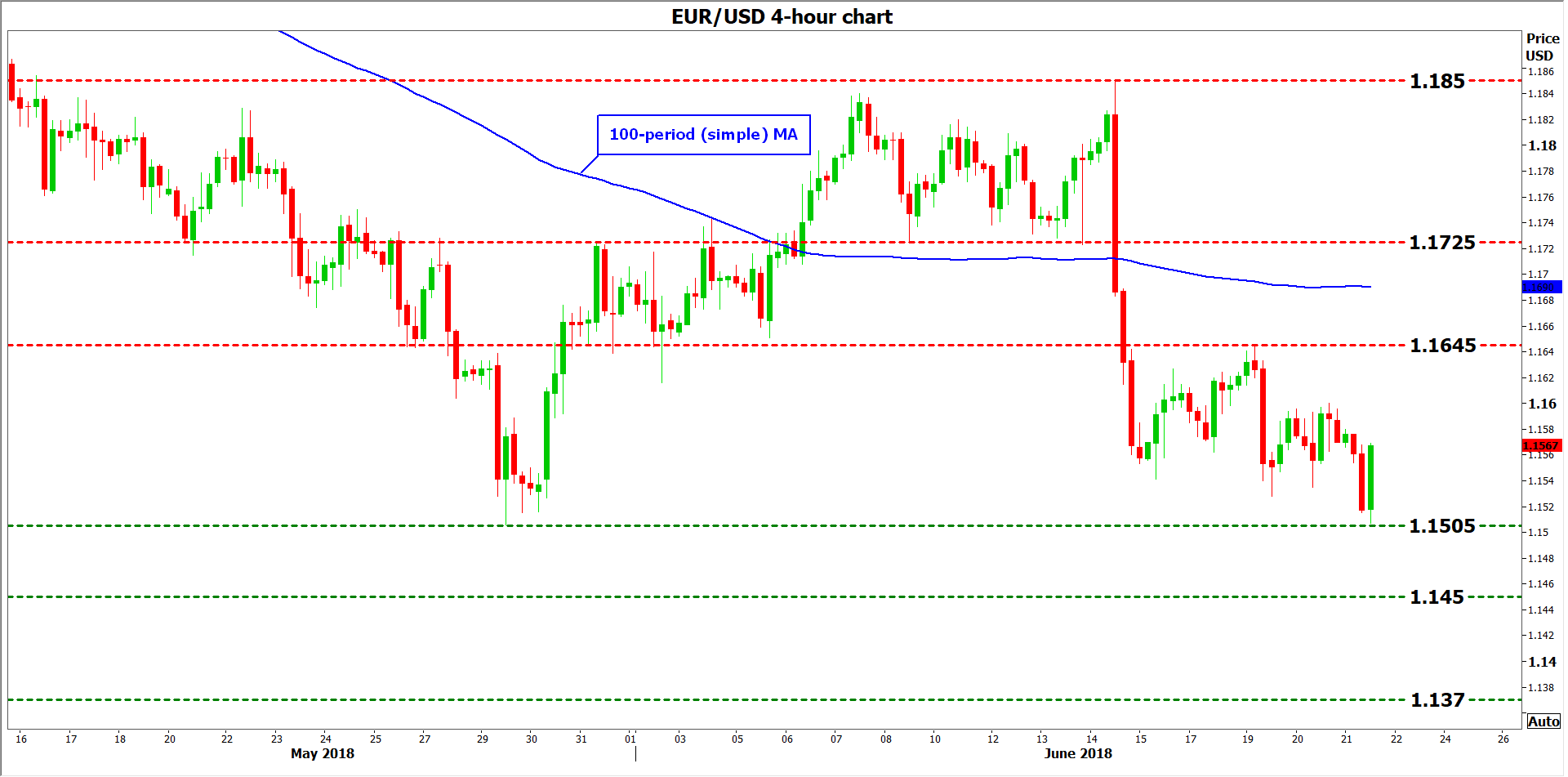

Technically, looking at euro/dollar, declines in the pair could encounter immediate support near the 11-month low of 1.1505, reached on May 29. A downside break would mark a lower low on the daily chart –and could open the way for the 1.1450 zone, defined by the peaks of 29 June, 2017. Even lower, attention would increasingly shift to the 1.1370 territory, the low of 13 July, 2017.

On the upside, immediate resistance to advances may come at 1.1645, the peak from June 19. If the bulls manage to power through it, then sell orders may be found near 1.1725 initially and at 1.1850 thereafter, these being the inside swing low on June 8 and the top of June 14 respectively.

Finally, note that the French and German PMIs will be released a few minutes earlier, at 0700 and 0730 GMT respectively, and have the capacity to impact price action ahead of the bloc’s prints.

Sunset Market Commentary

Markets:

Global core bond trading was volatile today. The first move of the day was a leap higher in which the Bund outperformed. The move was the mirror image of a setback in Italian BTP’s after two Eurosceptic Legia lawmakers were tapped to lead key Italian parliamentary committees that deal with economic policy. Italian FM Tria repeated Italy’s commitment to the euro today. Tuesday night’s German-Franco deal, which includes a vague proposal to make it easier to restrict EMU bonds from troubled countries, gradually gains traction as well and might have negative implications for EMU sovereigns. Today’ weakness in BTP’s was probably again exaggerated by overall low volumes. Once the move burned out, core bonds stabilized. The second significant directive move was a down leg, inspired by a sell-off in UK Gilts following a hawkish BoE meeting (see below). The Bund and US Note future managed to hold on to some of the early gains though and received a new in push in the back following the release of a disappointing June Philly Fed Business Outlook (19.9 from 34.4 vs 29.0 exp.). US weekly jobless claims, which continue to hover near all-time lows, couldn’t cushion the blow. The US yield curve bull flattens at the time of writing with yields 1.7 bps (2-yr) to 2.8 bps (30-yr) lower. Changes on the German yield curve vary between -2.1 bps (2-yr) and -3.4 bps (5-yr). 10-yr yield spread changes vs Germany widen by 10 bps for Portugal/Spain and by 19 bps for Italy.

EUR-USD. This morning, the euro remained in the defensive with Italy again in the forefront. Italian assets underperformed again after two euroskeptics were chosen at key places in the Italian parliament. EUR/USD tested the 1.1510 correction low but a break didn’t occur. Later, tensions on the euro eased. Early in US dealings, the dollar faced some headwinds too as the Philly Fed business outlook printed substantially softer than expected. Of late, markets were quite confident that the trade war didn’t have much negative impact on the US economy yet. It is premature to change that view on the basis of the Philly Fed release. Even so, it was enough to push some USD longs out of their position. At the same time, the market probably also felt itself to short euro positioned and EUR/USD was squeezed higher to the 1.16 area after the Philly Fed. USD/JPY also dropped back to the 110.30 area (compared to an intraday top near 110.75 before the start in Europe this morning). Is the USD rally losing some momentum?

GBP. The focus for sterling trading turned to the BoE policy decision. Sterling traded with a cautious bias going into the policy announcement. EUR/GBP hovered in a tight range close too, slightly below 0.88. The BoE, as expected, kept its policy rate unchanged at 0.50%. However, the vote was 3-6 (2-7 in May) as BoE Chief economist Haldane joined to camp for an immediate rate hike. The MPC also changed its guidance on when to start the reduction of the stock of asset purchases. The Bank will consider to reduce its balance sheet when the policy rate reaches 1.5% instead of 2% announced previously. The Bank sounded rather positive on recent economic developments and signaled some upward inflation risks. Even so, the BoE gave no clear hint on the timing of a next rate hike. Still, markets concluded that chances have risen for monetary policy to normalize sooner than expected. The market implied probability for an August rate hike rose from just below 50% to 68%. Sterling jumped higher. EUR/GBP trades currently in the 0.8730 area. Cable rebounded to trade well north of 1.32.

News Headlines:

Norway’s central bank kept its policy rate unchanged today, but stated that it expects to hike in September. The Norges Banks argued that the upturn in Norwegian economy is continuing, while inflation pressure is building. The news strengthened the Norwegian krone against the euro at a current EUR/NOK of 9.43.

Philly Fed index dropped sharply to 19.9, initial claims stayed low at 218k

Here is a summary of US data released today.

Philly Fed Manufacturing index dropped sharply to 19.9 in June, down from 34.4 and missed expectation of 25. 6-month expectation dropped to 34.8, down from 38.7. From the release, it's said that "Responses to the June Manufacturing Business Outlook Survey indicate continued expansion for the region's manufacturing sector, although indicators for general activity and new orders fell notably from last month. The firms reported continued increases in employment, and the indexes for prices paid and received continued to reflect widespread price pressures. Looking ahead six months, the firms remain optimistic overall, but the survey's future indicators continued to moderate."

Initial jobless claims dropped -3k to 218k in the week ended June 16, below expectation of 220k. Four-week moving average of initial claims dropped -4k to 221k. Continuing claims rose 22k to 1.723m in the week ended June 9. Four-week moving average of continuing claims dropped -4.75k to 1.7225m. This is the lowest level since December 8, 1973.

House price index rose 0.1% mom in April versus expectation of 0.3% mom. Leading index rose 0.2% in May versus expectation of 0.4%.

BOE Voted 6-3 to Keep Rate at 0.5%, QE Tapering Might Come Sooner

Surprisingly, BOE voted 6-3 to leave the Bank rate on hold at 0.50%. Chief economist Andy Haldane joined Ian McCafferty and Michael Saunders in opting for a +25bps rate hike. The outcome is more hawkish than consensus of a 7-2 vote. The more split committee was resulted from the dividing views over the economic outlook. Another surprise is that the Committee has changed its guidance about when it might start unwinding its asset purchase program which currently stands at 435B pound. BOE now believes that it might start to sell the government bonds when the policy rates have reached around 1.5%, compared with 2% previously. British pound has got the biggest bounce in more than 2 week after slumping to 1.3099, the lowest level over 7 years, before the announcement. The chance of an August rate hike has immediately increased to 67% from about 50% before the meeting.

In the preview, we noted that the members need more data points to determine whether the growth slowdown in the first quarter was driven by temporary factors or would persist for a longer period of time. The June meeting revealed that the members so far still judged that “the softness of activity in the first quarter had been largely temporary”. The noted that household consumption had “recovered strongly from their subdued levels at the time of the previous meeting”. However, the division lies here: The majority preferred to stand on the sideline in June, given the softer global growth outlook and weak manufacturing output and goods exports in April. These members preferred to see more data in these areas before adopting for a rate hike.

On the other hand, the dissenters “had a higher degree of confidence that the slowdown in Q1 was temporary or erratic and would largely be unwound”. The minutes added that these members saw the labor and pay settlement indicators as contain “upside risks to the expected pickup in average weekly earnings and unit wage costs”. They judged that “a modest tightening of monetary policy at this meeting could mitigate the risks of a more sustained period of above-target inflation that might ultimately necessitate a less gradual subsequent change in policy and hence a sharper adjustment in growth and employment”.

BOE has adjusted its forward guidance on QE, noting that it might start to sell the government bonds when the policy rates have reached around 1.5%, compared with 2% previously. While this appears a hawkish shift in first glance, the fact that the SONIA market is not pricing Bank rate at 1.5% until 2027 signals that the QE program would stay unchanged for an extended period of time.

GBP Rallies on Hawkish BoE

Risk aversion remains on trade fears

We’re continuing to see risk aversion in the markets on Thursday, as the trade spats between the US and others ramp up.

The week started with the US and China announcing tariffs against one another which will come into effect on 6 July, and it will end with the European Union announcing counter-tariffs against the world’s largest economy in response to those already imposed. While much of what has been announced this week was already anticipated, the rhetoric between these huge trading partners is heating up and that’s a major concern for investors.

While China and the EU appear to be targeting politically important products and regions ahead of the mid-term elections, Donald Trump is instead threatening significant escalation with another $200 billion of tariffs on China and $200 billion more if they respond. China and the EU are clearly hoping the harm suffered at the polling stations will hurt more than the economic impact of just matching what the US does, which will have the added benefit of hurting their own economy as little as possible.

Oil slipping ahead of OPEC meeting

Oil prices are coming under a little pressure once again as we near the outcome of the meeting in Vienna between OPEC and some non-OPEC countries where producers are due to discuss whether and how to increase output following their success in significantly reducing global inventories. It is believed there is some dispute between members on how much to increase output by, with Iran reportedly opposed to bowing to pressure from the US.

Source – OANDA fxTrade Advanced Charting Platform

It’s generally believed that we’ll see some increase, particularly as both Saudi Arabia and Russia appear keen to start reversing the 1.5 million barrel a day output cut that has been so accurate at reducing stocks and lifting prices. An initial increase of between half a million and a million barrels is expected to be agreed which will be welcomed by Trump who has been targeting OPEC as of late.

GBP spikes on interest rate vote

The pound has been given a significant boost by the Bank of England after policy makers voted 6-3 in favour of leaving interest rates unchanged, with Andy Haldane joining Ian McCafferty and Michael Saunders in voting for a hike. Policy makers stuck to their view that first quarter weakness will prove temporary which given that this was primarily behind their decision not to raise rates last month suggests August is very much a live meeting.

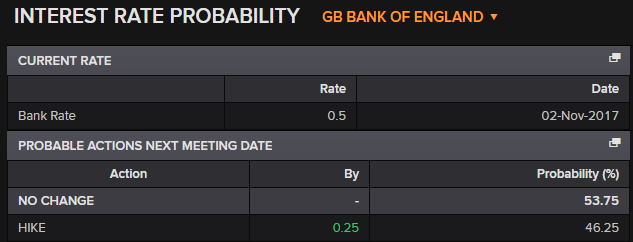

BoE Interest Rate Probability (August)

Source – Thomson Reuters Eikon

Prior to today’s meeting, investors were unconvinced by the prospect of a rate hike in August but I think today’s release will change that. Sterling rallied above 1.32 against the dollar from just above 1.31 prior to the release which suggests people’s expectations for August are being quickly revised. While a hike in November makes more sense as there’ll be more clarity – hopefully – by then, I wouldn’t be surprised if they go in August given the criticism they endured for holding off in May.

GBPUSD Daily Chart

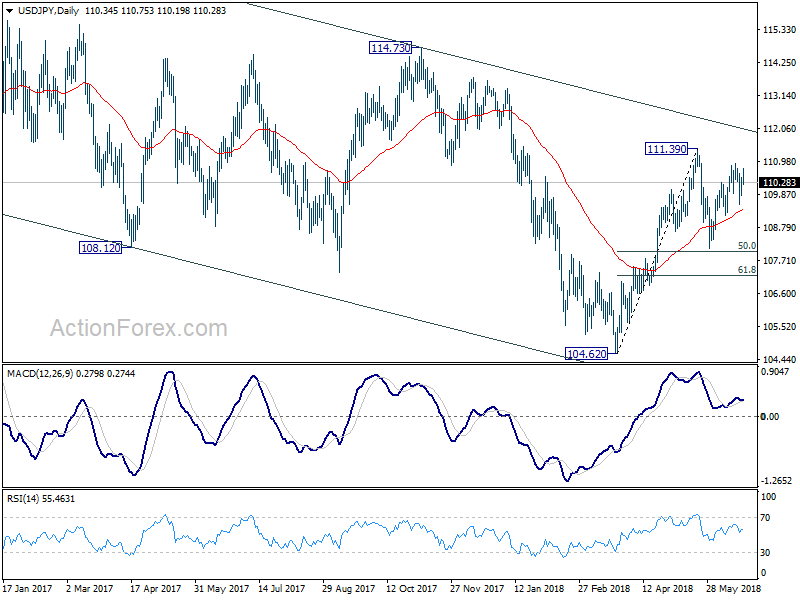

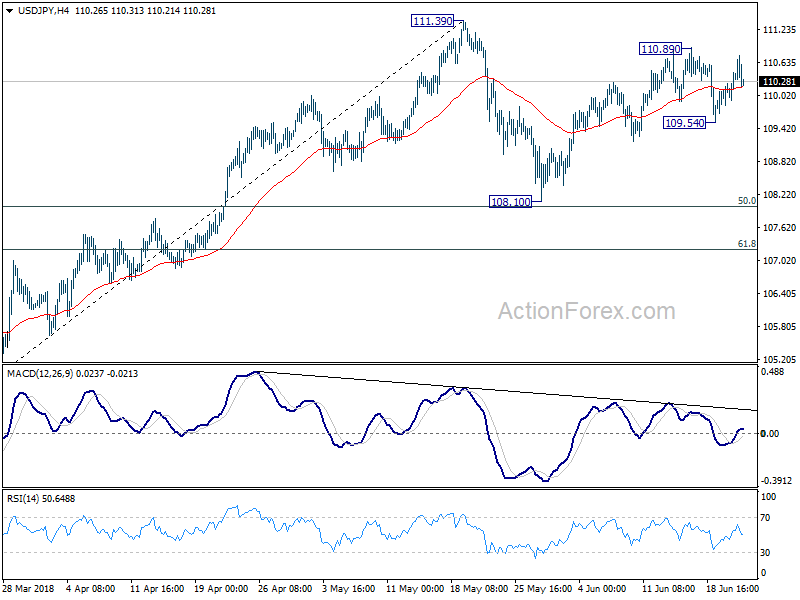

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.99; (P) 110.22; (R1) 110.59; More...

Intraday bias in USD/JPY remains neutral at this point. On the downside, below 109.54 will extend the corrective pattern from 111.39 with another falling leg to 108.10 and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39. But we'd be cautious on strong resistance from there to limit upside.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.