Sample Category Title

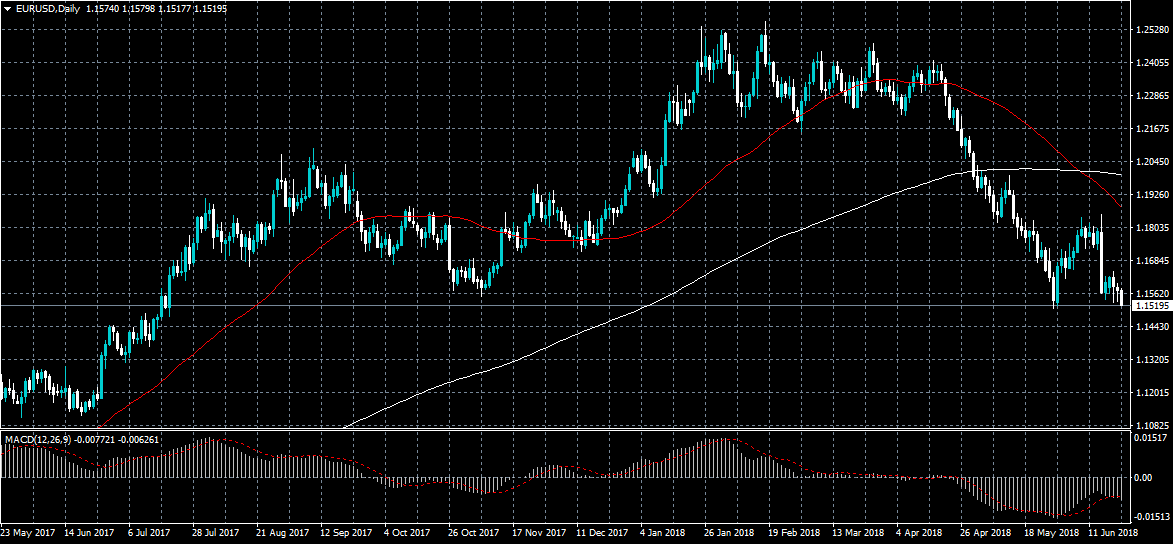

EURUSD Further Bearish Below 1.1510 Level

The euro is falling towards the lowest trading levels of the year against the greenback, as Italian political woes resurface and the US dollar index surges to levels not seen since July 2017. The EURUSD pair is currently trading around the 1.1520 level, with price fast approaching the May monthly trading-low, at 1.1509. The euro risks heavy trading losses below the 1.1500 level, with technical selling likely to increase a traders stop-losses are triggered.

The EURUSD pair is strongly bearish while trading below the 1.1510 level, key technical support is now located at the 1.1480 and 1.1430 levels

If the EURUSD pair moves above the 1.1554 level, intraday technical resistance can be found at the 1.1575 and 1.1600 levels.

DAX Under Pressure As Investors Fret Over Trade Tensions

The DAX index has posted gains in the Thursday session. Currently, the DAX is at 12,614, down 0.65% on the day. On the release front, the sole eurozone indicator is consumer confidence, which is expected to remain pegged at zero for a fifth straight month. On Friday, Germany and the eurozone will release services and manufacturing PMI reports.

The U.S-China trade war has been dominating the headlines, overshadowing escalating trade tensions between the U.S and the European Union. President Trump recently slapped import tariffs on steel and aluminum imports from the European Union, triggering retaliatory tariffs from Brussels. The eurozone economy is performing relatively well, so much so that the ECB has announced it is winding up its asset-purchase program at the end of the year. The eurozone can ill-afford a trade war with the United States, which would hurt exports, particularly from Germany. Investors are increasingly nervous about the trade war rhetoric, which is weighing on global equity markets. The DAX index has declined 2.6% this week and is at its lowest level since May 31.

Mario Draghi preached a lesson on prudence and patience from the ECB Forum on Tuesday. Last week, the ECB announced that it was winding up its asset-purchase plan by the end of the year, but added that it would not raise interest rates before next summer. This dovish message sent the euro sharply lower. Draghi said that the ECB will be “patient in determining the timing of the first rate rise”. Draghi also made reference to inflation, saying that “inflation expectations remain well anchored”. However, analysts were quick to note that eurozone inflation has fallen short of the bank’s target of just below 2 percent for five years. Draghi acknowledged that there were external factors which could weigh on inflation, including the threat of global protectionism and higher oil prices. There is also the vexing problem that higher wages have failed to translate into increased inflation.

Pound Posts Fresh Lows Ahead Of BoE Rate Decision, Oil Tumbles

Here are the latest developments in global markets:

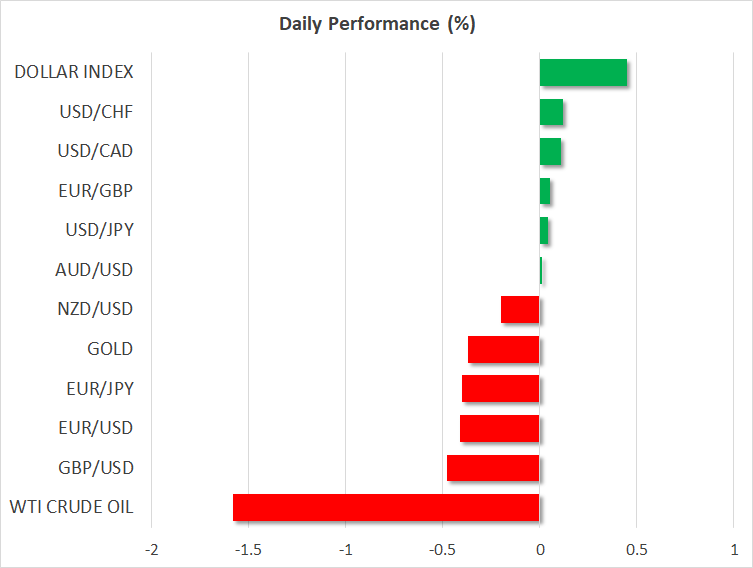

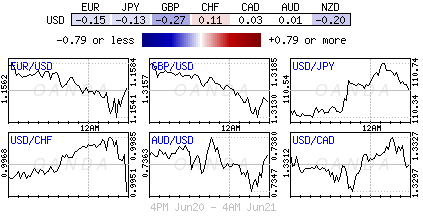

FOREX: Dollar/yen lacked direction for a third day, moving sideways around 110.40 (+0.05%), while the dollar index hit a fresh 11-month high at 95.52 (%?), advancing on the back of a weaker euro and pound. Earlier in the day, US 10-year government bond yields had spiked to a 1-week high of 2.95% but they soon returned to 2.91%. Euro/dollar was in pain as trade uncertainties remained in the air, while in Italy, Eurosceptic Alberto Bagnai, was appointed as the new head of the Senate finance committee, with the pair dropping further to a 3-week low of 1.1507 (-0.40%). Pound/dollar extended its downtrend marginally below 1.31 for the first time since mid-November ahead of the BoE policy decision today. Yesterday, Theresa May’s Brexit bill, was approved by theParliament, easing risks to May’s leadership and bringing a no-deal Brexit deal back on the table in case of no progress in Brexit talks. In antipodean currencies, kiwi/dollar crawled down to a 6-month low of 0.6823 (-0.28%) as economic growth in New Zealand slowed down, as expected, in the face of a weaker consumer spending.Aussie/dollar held steady today at 0.7366. The commodity-linked dollar/loonie reached a new 1-year peak at 1.3329 (+0.09%).

STOCKS: European stocks were mixed at 0830 with the British FTSE 100 being the best performer (+0.32%) and the Italian FTSE MIB being the worst one (-0.80%) as the Italian 10-year bond yields jumped higher. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 inched up by 0.05% and by 0.18% respectively, with consumer non-cyclicals and healthcare sectors leading the gains. The German DAX 30 fell by 0.40% after the German carmaker Daimler signaled that US import tariffs on Chinese products are a threat to its profits. France’s Peugeot and the auto supplier Valeo faced headwinds, as well as trade risks, were looming in the background, sending the French CAC 40 down by 0.19%. In Asia, benchmark stock indices closed in negative territory, while in the US, futures tracking the major indices were flashing red as well, pointing to a negative open.

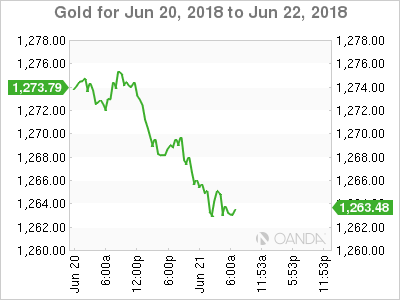

COMMODITIES: Oil prices were under pressure a day before OPEC members and their allies including Russia meet in Vienna to review the supply cut agreement signed in December 2016. Saudi Arabia and Russia continued to support that a supply hike is necessary, with the Saudi Arabian energy minister saying on Thursday that demand could heighten in the second half of this year and OPEC would negotiate how much to increase output, noting that 1 mb/d is a good target. On the other hand, Iran, remained in the opposite side, arguing that OPEC should reject US proposals to raise supply – though the nation did show some willingness to compromise on a supply increase. Meanwhile, Russia’s Rosneft, one of the world’s biggest oil producers, said that a 1.5 mb/d rise in global production is needed to offset global shortages. WTI crude and the London-based crude were last seen at $64.56/barrel (-1.75%) and at $73.23/barrel (-2.02%) respectively. In precious metals, gold extended losses for the fifth day, retreating to a six-month low of $1,261.36 (-0.38%).

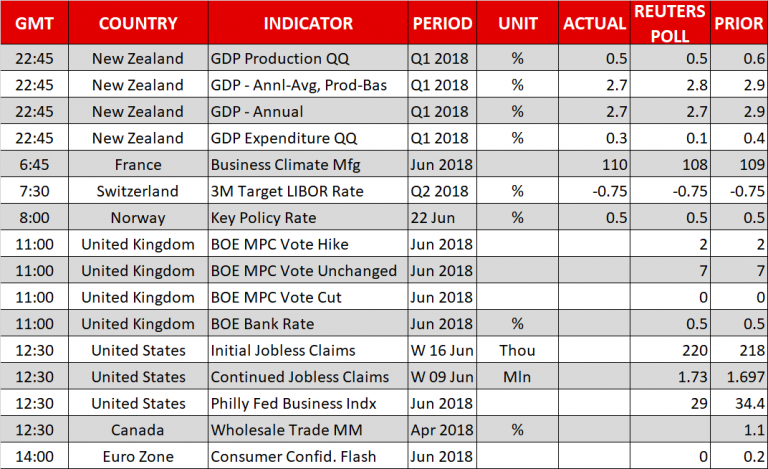

Day Ahead: Bank of England decides on rates; US initial jobless claims pending

The main event of the day is the Bank of England (BOE) interest rate decision at 1100 GMT, where no change in the 0.5% benchmark rate or QE are widely anticipated. Investors will turn their attention to the statement and minutes for guidance, which will be of interest following a run of overall disappointing data so far in Q2 from April and May. Moreover, traders will be watching for any notable changes to the Monetary Policy Committee’s (MPC) members’ in the statement for any clues as to whether a rate hike is possible in August.

Out of the US, weekly jobless claims – initial and continued – due at 1230 GMT will be gathering attention. The number of initial benefits claimants for the week ending June 16 is anticipated to be 220k, little changed from the preceding week’s 218k.

Canadian wholesale trade data for the month of April are scheduled for release at 1230 GMT.

A survey from the European Commission’s Directorate General for Economic and Financial Affairs covering the whole of the euro area will release June’s flash consumer confidence. It is scheduled for release at 1200 GMT and projections are for a dip in consumer confidence to 0.0 from 0.2 before.

In terms of public speeches, the Governor of the Bank of England, Mark Carney will give a speech at the Lord Mayor’s Bankers and Merchants Dinner, at Mansion House, London.

Overnight, Japan will release its CPI figures for May. Expectations are for the inflation rate is to fall to 0.3% in yearly terms, from 0.6% in the preceding month.

Sterling surges as BoE chief economist Haldane joined hawks to vote for rate hike

Sterling surges BoE kept bank rate unchanged 0.50% with 6-3 vote. The usual suspects Ian McCafferty and Michael Saunders voted for a hike to 0.75%. And to many's surprise, chief economist Andrew Haldane voted for a hike too. His vote carries much significance.

On growth, BoE noted the judgement that the dip in Q1 was temporary "appears broadly on track". It pointed to the rebound in household consumption and sentiments as evidence while "employment growth has remained solid". Despite decline in manufacturing output in April, surveys of business activity have been stable. And overall, the data "point to growth in the second quarter in line with the Committee's May projections.

On inflation, BoE expects CPI to "pick up by slightly more than projected" in the near term. That reflects " higher dollar oil prices and a weaker sterling exchange rate." And, indicators of wage growth also picked up with labor markets remains tight. "Domestic cost pressures will continue to firm gradually, as expected."

On forward guidance, BoE expects to maintain the size of assets purchased at GBP 435B and use the Bank Rate as "primary instrument" for momentary policy for now. And BoE will NOT reduce the size of the assets until Bank Rate reaches around 1.50%, lowered from prior guidance of around 2.00%.

Full statement below.

Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted by a majority of 6-3 to maintain Bank Rate at 0.5%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 20 June 2018, the MPC voted by a majority of 6-3 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

In the MPC's most recent projections, set out in the May Inflation Report, GDP was expected to grow by around 1¾% per year on average over the forecast, conditioned on the gently rising path of Bank Rate implied by market yields at the time. In those projections, growth continued to rotate towards net trade and business investment and away from consumption. While modest by historical standards, the projected pace of GDP growth over the forecast was nevertheless slightly faster than the diminished rate of supply growth, which averaged around 1½% per year. As a result, a small margin of excess demand was projected to emerge by early 2020, feeding through into higher rates of pay growth and domestic cost pressures. Nevertheless, CPI inflation continued to fall back gradually as the effects of sterling's past depreciation faded, reaching the 2% target in two years.

A key assumption in the MPC's May projections was that the dip in output growth in the first quarter would prove temporary, with momentum recovering in the second quarter. This judgement appears broadly on track. A number of indicators of household spending and sentiment have bounced back strongly from what appeared to be erratic weakness in Q1, in part related to the adverse weather. Employment growth has remained solid. Although manufacturing output recorded a decline in April, and this was accompanied by a fall in goods exports, surveys of business activity have been stable and, as a whole, point to growth in the second quarter in line with the Committee's May projections.

Internationally, activity data have been mixed. Indicators suggest that US growth bounced back strongly in Q2 from the softness in Q1. Euro-area growth has been weaker than expected, and downside risks have increased in some emerging markets, in part reflecting tighter financial conditions. More broadly, the prospects for global GDP growth remain strong, and while financial conditions have tightened somewhat, they continue to be accommodative.

CPI inflation was 2.4% in May, unchanged from April. Inflation is expected to pick up by slightly more than projected in May in the near term, reflecting higher dollar oil prices and a weaker sterling exchange rate. Most indicators of pay growth have picked up over the past year and the labour market remains tight, suggesting that domestic cost pressures will continue to firm gradually, as expected.

The Committee's best collective judgement remains that, were the economy to develop broadly in line with the May Inflation Report projections, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to its target at a conventional horizon. For the majority of members, an increase in Bank Rate was not required at this meeting. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

In addition to its discussion of the immediate policy decision, the Committee reviewed its previous guidance on the level of Bank Rate at which the MPC will consider whether to start to reduce the stock of purchased assets. The MPC continues to expect to maintain the stock of purchased assets until Bank Rate reaches a level from which it can be cut materially, reflecting the Committee's preference to use Bank Rate as the primary instrument for monetary policy. Since the previous guidance, the Committee has reduced Bank Rate from 0.5% to 0.25% in August 2016 and has noted that it could lower it further if required. Reflecting this, the MPC now intends not to reduce the stock of purchased assets until Bank Rate reaches around 1.5%, compared to the previous guidance of around 2%. Any reduction in the stock of purchased assets will be conducted at a gradual and predictable pace. Decisions on Bank Rate will take into account any impact of changes in the stock of purchased assets on overall monetary conditions, in order to achieve the inflation target. In the event that potential movements in Bank Rate are judged insufficient to achieve the inflation target, the reduction in the stock of assets could be amended or reversed.

(BOE) Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted by a majority of 6-3 to maintain Bank Rate at 0.5%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 20 June 2018, the MPC voted by a majority of 6-3 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

In the MPC's most recent projections, set out in the May Inflation Report, GDP was expected to grow by around 1¾% per year on average over the forecast, conditioned on the gently rising path of Bank Rate implied by market yields at the time. In those projections, growth continued to rotate towards net trade and business investment and away from consumption. While modest by historical standards, the projected pace of GDP growth over the forecast was nevertheless slightly faster than the diminished rate of supply growth, which averaged around 1½% per year. As a result, a small margin of excess demand was projected to emerge by early 2020, feeding through into higher rates of pay growth and domestic cost pressures. Nevertheless, CPI inflation continued to fall back gradually as the effects of sterling's past depreciation faded, reaching the 2% target in two years.

A key assumption in the MPC's May projections was that the dip in output growth in the first quarter would prove temporary, with momentum recovering in the second quarter. This judgement appears broadly on track. A number of indicators of household spending and sentiment have bounced back strongly from what appeared to be erratic weakness in Q1, in part related to the adverse weather. Employment growth has remained solid. Although manufacturing output recorded a decline in April, and this was accompanied by a fall in goods exports, surveys of business activity have been stable and, as a whole, point to growth in the second quarter in line with the Committee's May projections.

Internationally, activity data have been mixed. Indicators suggest that US growth bounced back strongly in Q2 from the softness in Q1. Euro-area growth has been weaker than expected, and downside risks have increased in some emerging markets, in part reflecting tighter financial conditions. More broadly, the prospects for global GDP growth remain strong, and while financial conditions have tightened somewhat, they continue to be accommodative.

CPI inflation was 2.4% in May, unchanged from April. Inflation is expected to pick up by slightly more than projected in May in the near term, reflecting higher dollar oil prices and a weaker sterling exchange rate. Most indicators of pay growth have picked up over the past year and the labour market remains tight, suggesting that domestic cost pressures will continue to firm gradually, as expected.

The Committee's best collective judgement remains that, were the economy to develop broadly in line with the May Inflation Report projections, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to its target at a conventional horizon. For the majority of members, an increase in Bank Rate was not required at this meeting. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

In addition to its discussion of the immediate policy decision, the Committee reviewed its previous guidance on the level of Bank Rate at which the MPC will consider whether to start to reduce the stock of purchased assets. The MPC continues to expect to maintain the stock of purchased assets until Bank Rate reaches a level from which it can be cut materially, reflecting the Committee's preference to use Bank Rate as the primary instrument for monetary policy. Since the previous guidance, the Committee has reduced Bank Rate from 0.5% to 0.25% in August 2016 and has noted that it could lower it further if required. Reflecting this, the MPC now intends not to reduce the stock of purchased assets until Bank Rate reaches around 1.5%, compared to the previous guidance of around 2%. Any reduction in the stock of purchased assets will be conducted at a gradual and predictable pace. Decisions on Bank Rate will take into account any impact of changes in the stock of purchased assets on overall monetary conditions, in order to achieve the inflation target. In the event that potential movements in Bank Rate are judged insufficient to achieve the inflation target, the reduction in the stock of assets could be amended or reversed.

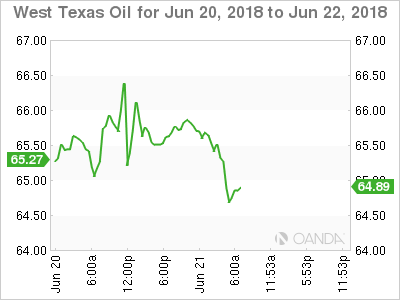

Oil Falls -2% As OPEC Nears Deal To Raise Production

Thursday June 21: Five things the markets are talking about

Currently, there are many moving parts that are keeping capital market players on their toes. President Trump and Chancellor Merkel continue to deal with immigration policy worries, while trade and tariffs tops most central bankers and other leaders’ agendas.

Overnight, the U.S dollar remains better bid, again encroaching on its 12-month highs against G10 currency pairs, supported by interest yield differentials, as U.S Treasury yields back up from yesterday’s session highs.

This morning, European stocks have gained alongside U.S futures, while emerging-market stocks slid. The pound has come under some pressure ahead of the Bank of England (BoE) rate decision in a few hours while West Texas oil (WTI) has slipped below +$66 a barrel ahead of tomorrow’s crucial OPEC meeting that will decide on output.

With trade concern, majority of investors are looking for surety, and with the U.S ‘bullish’ on growth and the Fed raising rates, U.S assets continue to look appealing and reason enough why the U.S dollar remains so bid.

On tap: Bank of England (BoE) monetary policy decision (07:00 am EDT)

1. Stocks mixed results

In Japan overnight, the Nikkei share average rallied as concerns over Sino-U.S trade issues appeared to recede, while technology stocks rallied on the back of U.S tech stocks strong performance Wednesday. The Nikkei index rose +0.61%, while the broader Topix fell -0.12%.

Note: The market is also being supported by expectations that June dividend payouts would be reinvested. Estimated dividend payout over the next fortnight is +$41B.

Down-under, Aussie shares rallied overnight with financials and materials stocks leading the gains – a weaker AUD is supporting foreign interest. The S&P/ASX 200 index rose about +1%. In S. Korea, the Kospi fell -1.1%.

In Hong Kong, stocks closed out atop of their six-month low, as Sino-U.S trade conflict fears continue to curb risk appetite. The Hang Seng index ended -1.4% lower, while the China Enterprises Index closed lower by -1.2%.

In China, equities shed early gains to end lower, with the benchmark Shanghai index closing at a two-year low on lingering trade worries. The blue-chip CSI300 index closed down -1.2%, while the Shanghai Composite Index ended -1.4% lower.

In Europe, regional bourses are off the highs ahead of the U.S open, lead by the DAX, which is weighed, lower by automakers – Daimler profit warning citing potential auto-tariffs and clamp down on diesel emission cars.

U.S stocks are set to open in the ‘red’ (-0.2%).

Indices: Stoxx600 flat at 384.2, FTSE +0.2% at 7643, DAX -0.5% at 12634, CAC-40 -0.2% at 5363, IBEX-35 -0.7% at 9723, FTSE MIB -1.0% at 21891, SMI +0.1% at 8562, S&P 500 Futures -0.2%

2. Oil falls -2% as OPEC nears deal to raise production

Oil prices remain under pressure, as OPEC crude exporters appear to be nearing a deal to increase production.

Brent crude futures have fallen -$1.76 a barrel – or more than -2% – to trade at a low of +$72.98. U.S light crude (WTI) is -$1.00 lower at +$64.71.

Note: Brent reached a four-year high above +$80 a barrel in May, but has fallen steadily in recent weeks as Saudi Arabia has signalled it intends to raise production to stabilize prices.

OPEC is holding its biannual two-day meeting in Vienna starting tomorrow and is widely expected to agree to pump more, possibly supported by some other producers outside OPEC, including Russia. Iran had been expected to oppose any rise in crude output, but it has now indicated it may support a small increase.

Currently, market expectations are looking for an aggregate increase in production for OPEC of between +500k to +1M bpd.

Ahead of the U.S open, gold prices have fallen to a new six-month low as investors sold holdings in the physical market and the dollar climbed on interest rate differentials. Spot gold is down -0.4% at +$1,262.78 an ounce, its lowest print since Dec. 20. U.S. gold futures are down -0.8% at +$1,264.50 an ounce.

Note: the ‘yellow’ metal has lost more than -7% since the April high above +$1,365 an ounce.

3. SNB stands pat on key rate despite upbeat economy

Earlier this morning, there were no surprises by the Swiss National Bank (SNB) who remains constrained by the actions of the ECB. The Swiss policy makers kept their key policy rate in ‘deeply negative territory’ despite signs of healthy economic activity and slowly rising inflation.

It left its deposit rate at -0.75% as widely expected, where it has been for the past three-years. In the adjoining statement, the central bank said the CHF ($0.9972) is “highly valued” and that it was willing to intervene in currency markets, if necessary, should the franc strengthen too much.

The situation in currency markets “remains fragile,” the SNB said, “and the negative interest rate and our willingness to intervene in the foreign exchange market as necessary therefore remain essential.”

Elsewhere, U.S Treasury bond prices remain under pressure after Fed Chair Jerome Powell ‘bullish’ comments yesterday saying that falling U.S unemployment and faster inflation support additional interest rate increases.

The yield on the benchmark 10-year note has backed up +1 bps to +2.921%, while the yield on the two-year Treasury note has rallied to +2.555%.

Note: The Fed raised rates in March and June, and at it’s meeting last week, officials penciled in two more increases for the remainder of 2018, or a total four for the year. Their forecasts at the December and March meetings were for three increases in 2018.

Nevertheless, global trade conflicts could hinder the Fed from meeting its goals – Fed-funds futures indicate that the odds the Fed will raise interest rates four or more times this year are at +48%, down from +55% Monday.

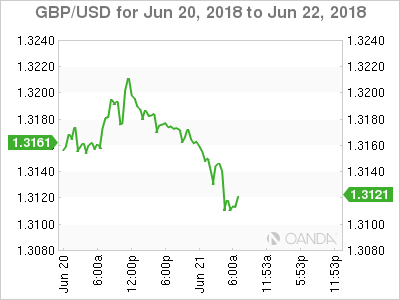

4. Pound falls before BoE decision

Sterling (£1.3116) trades lower ahead of this morning’s Bank of England monetary policy decision (07:00 am). It is largely expected the central bank will keep interest rates unchanged this month, with focus on whether it gives any hint on the timing of any rate rise in the foreseeable future. The fixed income market is forecasting a +50% chance of an increase in August.

The EUR/USD (€1.1525) is probing the lower end of its overnight range after reports circulated that Italy has appointed a Euro-sceptic to head its Senate Finance Committee. Italian bond yields have also backed up.

USD/JPY (¥110.40) remains in the middle of its current range supported by comments yesterday by U.S Secretary of Commerce Ross who stated that he did not think the Chinese want a trade war any more than U.S did.

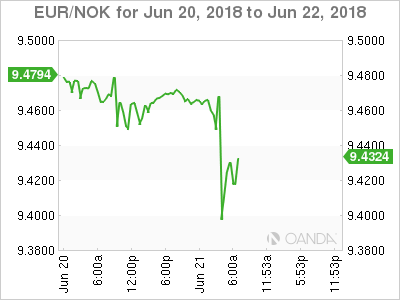

EUR/NOK (€9.4292) is lower by -0.7% after Norges Bank left its key interest rate unchanged at +0.5% and said it would most likely raise the rate “in September 2018.”

5. U.K borrowing fell in May

U.K data this morning showed that U.K government borrowing declined on the year in May as higher taxes offset a small rise in spending.

The ONS said borrowing in May was +£5B compared with +£7B a year earlier. The office also stated that borrowing for the fiscal year to the end of March was the lowest in eleven-years, at a revised +£39.5B.

Note: The U.K government has been running a small surplus on day-to-day spending, which ex-investment.

Earlier this week, PM Theresa May said her government intends to increase borrowing and raise taxes to help finance a spending boost for the NHS.

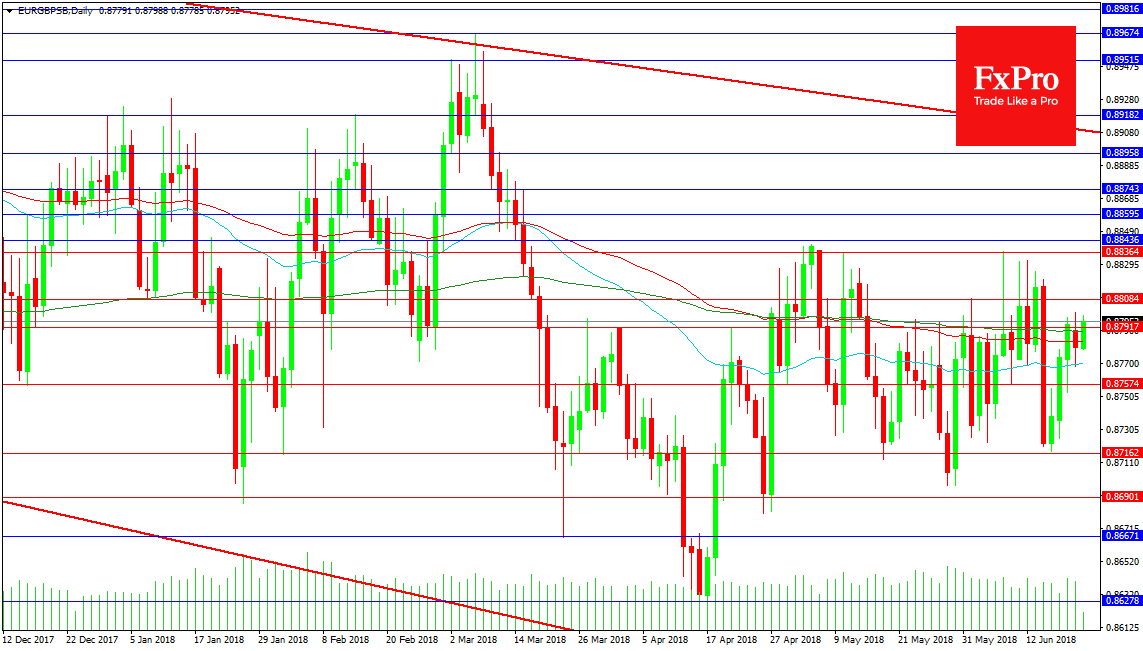

Forex Analysis: EURGBP

This pair is reversing the drop lower after the ECB announcement. The pair has traded above 0.88000 yesterday and was using its 50 period 4 hour moving averages as support in an attempt to eke out gains. This market has been in a sideways range for many months so traders are watching for a breakout above 0.90000 with this week's price action restoring their hopes. The retracement this morning has gotten to 0.87988, close to the 0.88000 target. A break higher hopes to test the recent high at 0.88364 and then push to the falling red trend line at 0.89000. A break above this line would see 0.89674 tested with support built at the 0.89000 zone.

Support can be seen on the chart at the moving averages around 0.87900 and 0.87700. Further support is located at 0.87574 and the low of last week at 0.87162 followed by the 0.87000 level. A move under the end of May lows can target 0.86900 followed by 0.86671 and the important swing low at 0.86200. From there buyers would look to enter the market as far down as 0.85700 but a loss of 0.85500 may result in a shakeout of positions and a drive to 0.84000 and beyond.

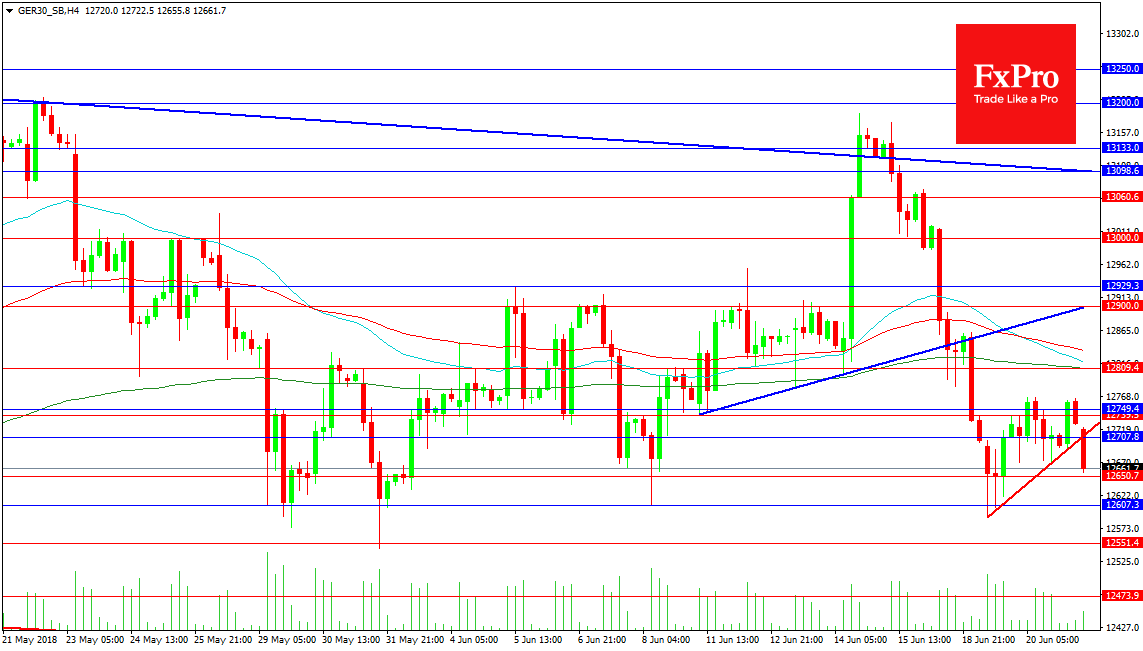

Forex Analysis: German 30

The German 30 Index is under pressure again today after last week’s rally faded. The index broke above resistance at 12950.00 and 13000.00 before falling short of the 13200.00 level. The selloff has broken supports and the index is trading in the lower portion of the trading range. The outlook remains bearish with a recovery of yesterday’s highs needed for bulls to attempt 12900.00 again. Traders will be watching for a break of the 12770.00 area which points to a moved back to the moving averages above 12809.40, followed by a retest of trend line resistance at 13098.00.

Support below comes in at 12600.00 followed by 12544.00. A drop under this level would signal a reversal of the rally last week and a swing towards a more bearish outlook. Support under 12500.00 comes in at 12474.00. The 12375.00 level represents a zone of support down to 12335.00 and falling trend line support. A move down out of this range can point to further declines as the summer progresses towards.

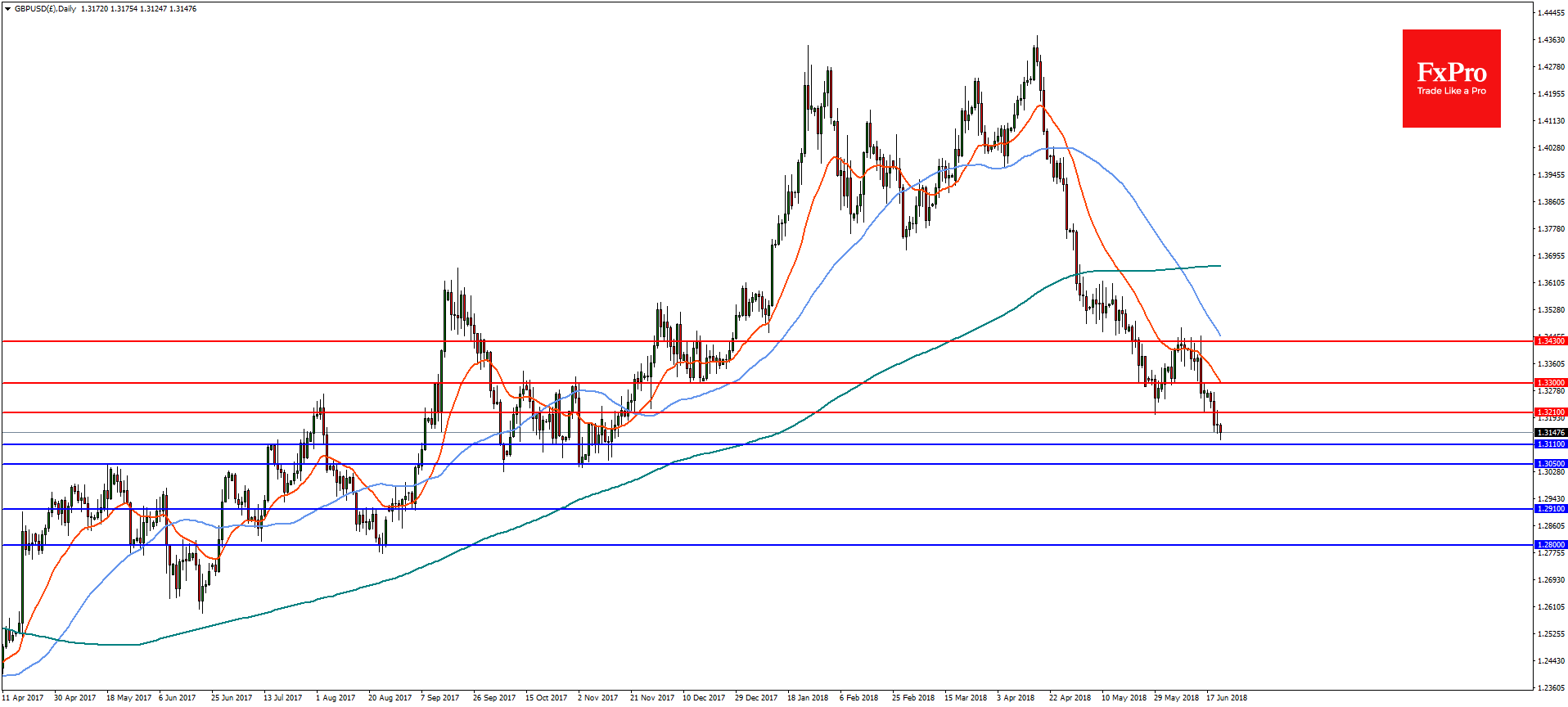

Forex Analysis: GBPUSD And GBPJPY

The major event for today is the Bank of England’s (BoE) interest rate decision and monetary policy statement. The most likely outcome is that the BoE keep rates on hold and the vote count remains the same but the focus will be on the possibility of a rate hike in August. The BoE wanted to see signs of stronger growth but data have been mixed with industrial output, construction and trade being weak, inflation unchanged in May and retail sales picking up. Wage growth, one of the most important indicators, has been muted and in line with expectations. If the monetary policy statement is dovish, the policy divergence with the US will drive the GBPUSD pair lower. However, a hawkish tone which revives hopes of rate hikes this year would give a lift to the British Pound. BoE Governor Mark Carney is also due to speak this evening so will have a chance to elaborate on the outlook.

GBPUSD

On the daily chart, GBPUSD is testing the 50% retracement of the lows of September 2016 near 1.3110. A break of that level will see the bearish trend continue to support at 1.3050, 1.2910 and then the 61.8% retracement at 1.2800. The pair needs to regain the 1.3300 level to change the outlook but faces near term resistance at 1.3210.

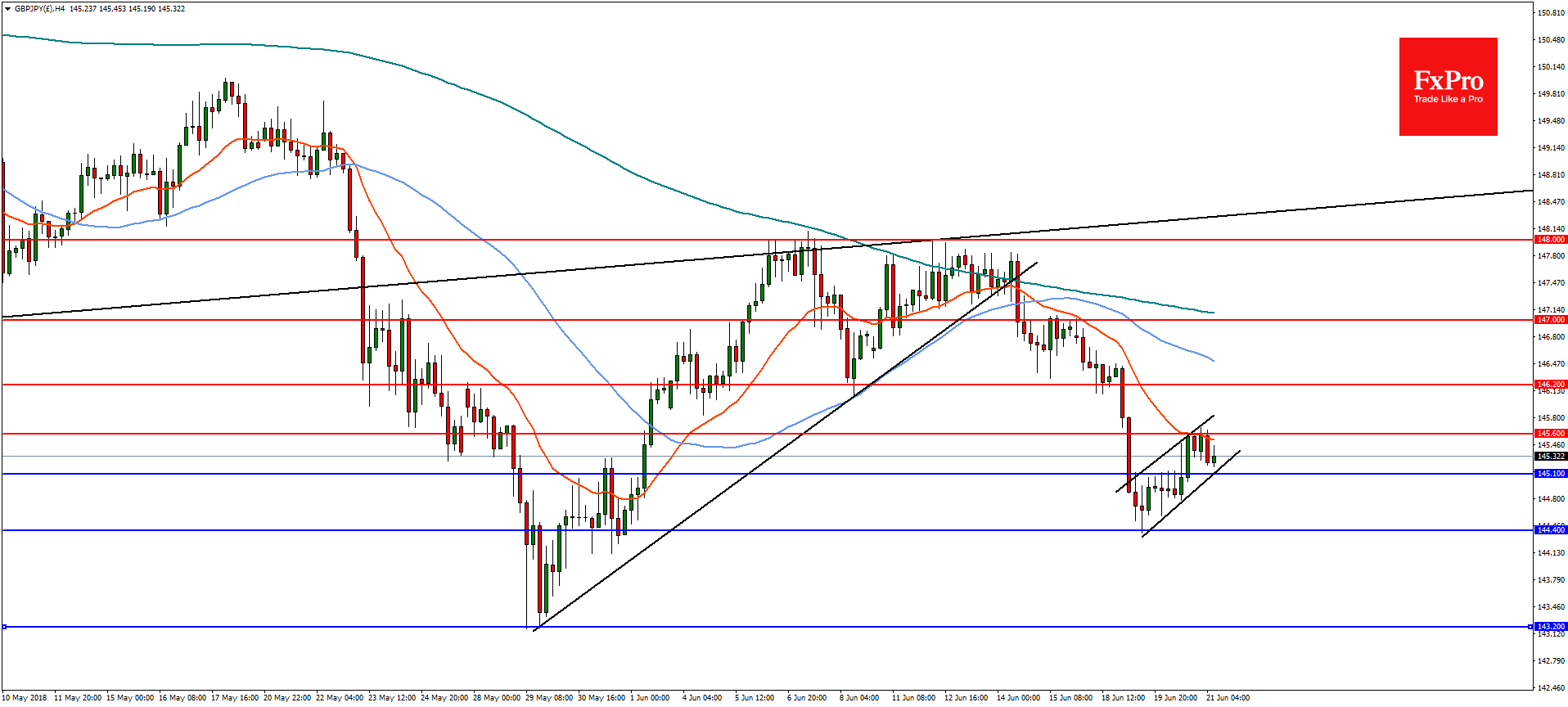

GBPJPY

In the 4-hourly timeframe, GBPJPY is forming a bear flag with a measured target of 142.20. The pair needs to break the 145.10 level to open the way to a downside move with supports at the 38.2% retracement of the September 2016 lows at 144.40 followed by 143.20. A reversal above 145.60 will find resistance at 146.20.

EUR/USD – Stumbling Euro Falls To 11-Month Low, U.S Jobless Claims Next

EUR/USD has posted losses in the Thursday session. Currently, the pair is trading at 1.1521, down 0.46% on the day. On the release front, the sole eurozone indicator is consumer confidence, which is expected to remain pegged at zero points for a fifth straight month. In the U.S, there are two key indicators. The Philly Fed Manufacturing Index is forecast to drop to 28.9 points. As well, unemployment claims are expected to edge up to 220 thousand. On Friday, Germany and the eurozone will release services and manufacturing PMI reports.

The headlines have been dominated by the U.S-China trade spat, which has shaken up the markets and sent the euro lower against the U. S dollar. Currently, EUR/USD is at its lowest level since July 2017. The U.S has also slapped tariffs on steel and aluminum exports from the European Union, setting off alarm bells in Brussels. The eurozone economy is performing relatively well, so much so that the ECB has announced it is winding up its asset-purchase program at the end of the year. The eurozone can ill-afford a trade war with the United States, which would hurt exports, particularly from Germany. The euro is at an 11-month low, as last week’s Federal Reserve rate hike and cautious remarks from Mario Draghi at the ECB Forum have helped propel the dollar higher.

Mario Draghi preached a lesson on prudence and patience from the ECB Forum on Tuesday. Last week, the ECB announced that it was winding up its asset-purchase plan by the end of the year, but added that it would not raise interest rates before next summer. This dovish message sent the euro sharply lower. Draghi said that the ECB will be “patient in determining the timing of the first rate rise”. Draghi also made reference to inflation, saying that “inflation expectations remain well anchored”. However, analysts were quick to note that eurozone inflation has fallen short of the bank’s target of just below 2 percent for five years. Draghi acknowledged that there were external factors which could weigh on inflation, including the threat of global protectionism and higher oil prices. There is also the vexing problem that higher wages have failed to translate into increased inflation. Draghi would like to get through the European Forum without shaking up the euro, and so far he has succeeded.

The headlines have been dominated by the U.S-China trade spat, which has shaken up the markets and sent the euro lower against the U. S dollar. Currently, EUR/USD is at its lowest level since July 2017. The U.S has also slapped tariffs on steel and aluminum exports from the European Union, setting off alarm bells in Brussels over the prospect of a trade battle with the U.S. The eurozone economy is performing relatively well, so much so that the ECB has announced it is winding up its asset-purchase program at the end of the year. The eurozone can ill-afford a trade war with the United States, which would hurt exports, particularly from Germany. The euro is at an 11-month low, as last week’s Federal Reserve rate hike and cautious remarks from Mario Draghi at the ECB Forum have helped propel the dollar higher.