Sample Category Title

Elliott Wave View: USDJPY Support Around The Corner?

USDJPY short-term Elliott wave view suggests that the rally to 110.91 high ended Minor wave 1 & also the cycle from 5/29 low. The internals of that rally higher unfolded as Elliott wave leading diagonalwhere Minute wave ((i)) ended at 110.27 high in 5 waves, Minute wave ((ii)) pullback ended at 109.17, and Minute wave ((iii)) ended at 110.85 in 5 waves structure.

Down from there, Minute wave ((iv)) pullback ended at 109.89 and Minute wave ((v)) of 1 ended at 110.90 high in another 5 waves structure. Below from 110.9 high, pair is doing a Minor wave 2 pullback to correct cycle from 5/29 low in 3, 7 or 11 swings. So far the pullback looks to be unfolding as Elliott wave double three structure where Minute wave ((w)) ended at 109.53 with internals subdivision as zigzag correction. Up from there, Minute wave ((x)) bounce ended at 110.76 with internal subdivision of a double three. Near-term focus remains towards 109.36-109.04, which is 100%-123.6% Fibonacci extension area of Minute ((w))-((x)) to end the Minute wave ((y)) & also the Minor wave 2 pullback. Afterwards, the pair is expected to resume higher provided the pivot from 5/29 low (108.10) stays intact or should do a 3 wave bounce at least. We don’t like selling the proposed pullback.

USDJPY 1 Hour Elliott Wave Chart

Equity Markets Have Been Under Pressure Both In Europe And In The US

Market movers today

It is time for flash euro area PMI for June. It will be interesting to see if there is any effect of the recent deterioration on the trade front. The data is typically collected from the 12-21 in the month. Manufacturing PMI has fallen for five consecutive months and after peaking at 60.6 in December 2017, it fell to 55.5 in May 2018. We expect a further fall to 54.8 in June. Service PMI has seen a similar development, declining from 58.0 in January to 53.8 in May. We expect service PMI to fall to 53.7 in June from 53.8 in May.

Markit PMI for the US is also due to be released. The manufacturing index has moved up since mid-2017. However, we look for some moderation as hard data on exports, investment orders and consumption has been soft. We expect a decline from 56.4 in May to 56.0 in June.

Selected market news

Focus returned to Italy yesterday as the new government appointed two very eurosceptic lawmakers to influential parliamentary committees that deal with economic policy. Alberto Bagnai, who in two books has advocated for a dismantling of the monetary union, was appointed to head the financial committee and Claudio Borghi was appointed to head the budget committee in the lower house. The latter has been arguing strongly for so-called mini-BOTs, which could be seen as a parallel currency. 2Y and 10Y BTP yields widened 30bp and 22bp, respectively, to Germany.

The pressure on Italy might very well continue today after the IMF s Christine Lagarde said last night that financial markets could react violently to any fiscal easing or reversal of reforms. An IMF team is due to visit Italy in two weeks to deliver the scheduled assessment of the Italian economy.

While things are heating up in Italy once again, a deal between Greece and its euro area creditors was reached overnight. Maturities on the EUR96.6bn Greece received in its second bailout will be pushed out for 10 years and Greece will receive a grace period also of 10 years in respect of coupons and interest rates. The deal should clear the way for Greece to exit its bail-out programme in August.

Equity markets have been under pressure both in Europe and in the US. The combination of the Italian political crisis flaring up and a profit warning from Daimler weighed on sentiment in Europe. Especially the latter fuelled fears that the global trade war is now having a real impact on growth and profits. The negative sentiment was carried over to the US and the major indices all ended the day lower. Nikkei is also in the red this morning.

OPEC is set to meet today to review current production cuts that are due to expire by the end of the year. Tonight, a preliminary deal to hike oil production by 1mb/d was reached though the actual production rise will probably be somewhat lower around 600,000 barrels a day. But it might be difficult to reach a formal agreement today, as Iran that walked out of the meeting overnight. Iran does not want a hike in production. Without Iran and possibly Venezuela, a formal communique might not be send out. Note that non-OPEC member Russia is part of the current deal. The disagreement among OPEC members has pushed oil up by a dollar overnight.

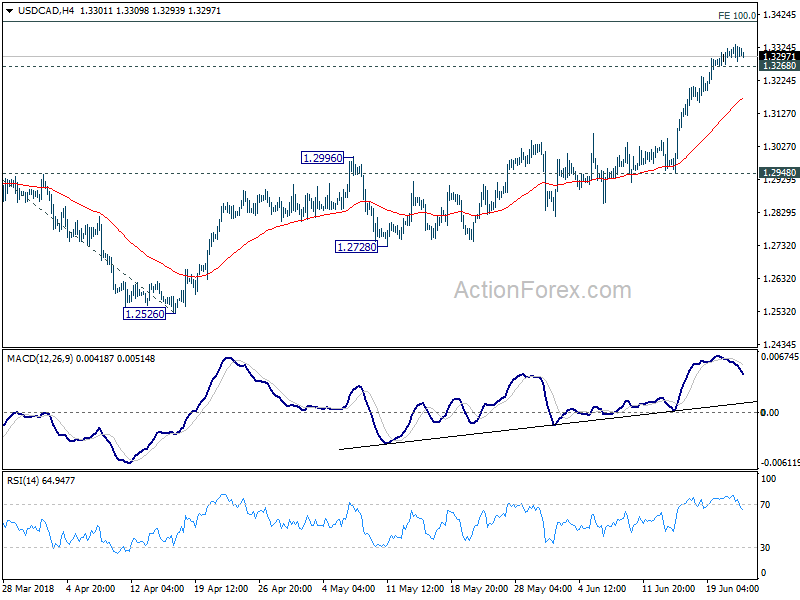

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3291; (P) 1.3315; (R1) 1.3345; More...

USD/CAD continues to lose upside momentum as seen in 4 hour MACD. But with 1.3268 minor support intact, further rise is still expected to the upside for 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. Nonetheless, break of 1.3268 will indicate short term topping. In that case, intraday bias will be turned to the downside for pull back to 4 hour 55 EMA (now at 1.3169) or below. But we'd expect strong support above 1.2948 to bring rally resumption.

In the bigger picture, current development solidify the view of bullish trend reversal. That is fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. This will now be the preferred case as long as 1.2526 support holds, even in case of deep pull back.

Sterling Rebound Short-Lived, Risk Aversion Regained Spotlight

The BoE triggered rebound in Sterling was relatively brief. Risk aversion quickly regained the spotlight in the markets. DOW extended its losing streak for the eight day and closed down -196.10 pts or -0.80% at 24461.70. S&P 500 and NASDAQ were down -0.63% and -0.88% respectively. Asian markets follow, with Nikkei losing -1% at the time of writing. Yen retreats mildly today but remains the second strongest one for the week, next to Swiss Franc. Gold extended recent slump to as low as 1261.52 yesterday and 1260 looks vulnerable. WTI crude oil continues to struggle in range ahead of meeting of oil producers on production raise.

Technically, USD/CHF's dip yesterday puts 0.9894 minor support back into focus. Break there could resume recent correction from 1.0056 through 0.9787 low before completion. USD/JPY is also heading back to 109.54 temporary low and break could finally build up some downside momentum for 108.10 support. USD/CAD could be an interesting one to watch too as recent rally is losing momentum despite hitting 1.3334. A break of 1.3268 minor support, triggered by oil or Canadian data, could mark short term topping and bring deeper pull back.

No follow through buying in Sterling after strong but brief BoE rebound

The BoE triggered rebound in Sterling yesterday was initially rather strong, but lacked follow through buying. GBP/USD is kept well below key near term resistance at 1.3471. EUR/GBP is still hovering around mid-point of range of 0.8693/8844. Even GBP/JPY is held below 146.46 minor support. For the week, Sterling is staying in red against Dollar, Euro, Swiss and Yen. It's just up against the risk aversion hit Canadian, Australian and New Zealand Dollar.

Yesterday's more hawkish than expected BoE announcement just revived the chance of an August hike. That was indeed the base case as presented in the May Inflation Report. Remember that during the most Sterling bullish time earlier this year, markets were expecting a hike in May and speculating for another one in November. The BoE announce just solidify the case for a hike in the second half of the year, that is either in August or November, possibly in August. And it sort of ruled out the possibility of BoE standing pat for the rest of the year.

Suggested readings on BoE

- BOE Recap: Beaten-Down GBP/USD Grows Hawkish Wings

- BoE Leaves Door Open for August Hike

- BOE Voted 6-3 to Keep Rate at 0.5%, QE Tapering Might Come Sooner

Minneapolis Fed Kashkari doubts long term impact of tax cut

Minneapolis Fed President Neel Kashkari expressed his doubts on the long term effect of Trump's USD 1.5T package of corporate and individual tax cuts. In an event at African Development Center of Minnesota, he said "we know if you cut taxes on the margin that should boost economic growth in the short term." However, "the question is when that short term is over, does it actually lead to longer-term, higher sustained economic growth? That's unclear right now."

He also points to the information he got from businesses. Kashkari said while business leaders "are more optimistic than I had expected," they are also saying that lower tax rates have not led them to make new investments, at least not yet. He added "I am asking businesses 'are you actually investing more?' And so far the answer that I've heard is 'we're waiting to see.'"

Japan CPI Core unchanged, PMI manufacturing improved

Released from Japan, all items CPI rose to 0.7% yoy in May, up from 0.6% yoy. Core CPI, less fresh food, was unchanged at 0.7% yoy. Core core CPI, less fresh food and energy even slowed to 0.3% yoy, down from 0.4% yoy. The data highlighted BoJ's inability to lift inflation and inflation expectation even with the ultra-loose monetary policy. And the central bank is still a long way from stimulus exit.

PMI manufacturing rose to 53.1 in June, up from 52.8, beat expectation of 52.6. Joe Hayes, Economist at IHS Markit note in the release that "the final PMI reading of the second quarter revealed a quickened pace of growth across the Japanese manufacturing economy. "The sector has sustained a relatively solid upward trend across 2018," and "there appears to be further legs in the manufacturing growth cycle."

Oil price in range ahead of pivotal OPEC meeting

Oil price is staying in range between 63.6/66.9 as markets await the pivotal meeting in Austria. Delegations of OPEC and non-OPEC oil producing countries are meeting today in Vienna. The producers are trying to reach a consensus on easing the output cap, that is raising production, to cool oil prices.

Saudi Arabia's Energy Minister Khalid Al-Falih, the defacto leader of OPEC, said yesterday that he was "optimistic" on a deal as there was a "spirit of cooperation" among the group. And they would discuss how to raise production by around 1 million barrels per day.

The United Arab Emirates' minister of energy and industry, and OPEC president, Suhail Al- Mazrouei emphasized that OPEC is "not a political organization" but a "commercial organization". Iraq's Oil Minister Jabbar Ali al-Luaibi also said he's "confident that we will reach some sort of agreement".

However, Iran, Iraq and Venezuela are known to oppose the relaxation of production cut. Iranian Oil Minister Bijan Zanganeh said he doubted OPEC could reach a deal this week and he was feeling "very good" about the current production levels.

Russian Energy Minister Alexander Novak warned that "Oil demand usually grows at the steepest pace in the third quarter ... We could face a deficit if we don't take measures." And, "this could lead to market overheating." Russia is pushing up to 1.5 million barrels per day of output raise, OPEC and non-OPEC countries together.

Looking ahead

Eurozone PMIs will be the major focus in European session. Canada will release retail sales in CPI later in the day. US will release Markit PMIs too.

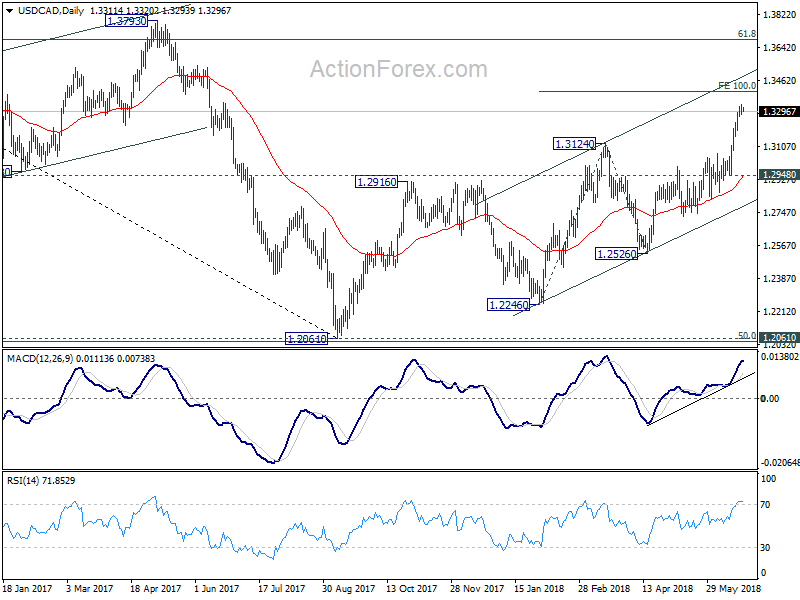

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3291; (P) 1.3315; (R1) 1.3345; More...

USD/CAD continues to lose upside momentum as seen in 4 hour MACD. But with 1.3268 minor support intact, further rise is still expected to the upside for 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. Nonetheless, break of 1.3268 will indicate short term topping. In that case, intraday bias will be turned to the downside for pull back to 4 hour 55 EMA (now at 1.3169) or below. But we'd expect strong support above 1.2948 to bring rally resumption.

In the bigger picture, current development solidify the view of bullish trend reversal. That is fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. This will now be the preferred case as long as 1.2526 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y May | 0.70% | 0.70% | 0.70% | |

| 00:30 | JPY | Flash Manufacturing PMI Jun | 53.1 | 52.6 | 52.8 | |

| 04:30 | JPY | All Industry Activity Index M/M Apr | 0.90% | 0.00% | ||

| 07:00 | EUR | France Manufacturing PMI Jun P | 54 | 54.4 | ||

| 07:00 | EUR | France Services PMI Jun P | 54.3 | 54.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 56.3 | 56.9 | ||

| 07:30 | EUR | Germany Services PMI Jun P | 52.2 | 52.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 55 | 55.5 | ||

| 08:00 | EUR | Eurozone Services PMI Jun P | 53.7 | 53.8 | ||

| 08:00 | EUR | Eurozone Composite PMI Jun P | 54.1 | |||

| 12:30 | CAD | Retail Sales M/M Apr | 0.00% | 0.60% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Apr | 0.20% | -0.20% | ||

| 12:30 | CAD | CPI M/M May | 0.10% | 0.30% | ||

| 12:30 | CAD | CPI Y/Y May | 2.10% | 2.20% | ||

| 12:30 | CAD | CPI Core - Common Y/Y May | 1.90% | |||

| 12:30 | CAD | CPI Core- Median Y/Y May | 2.10% | |||

| 12:30 | CAD | CPI Core- Trim Y/Y May | 2.10% | |||

| 13:45 | USD | US Manufacturing PMI Jun P | 56.2 | 56.4 | ||

| 13:45 | USD | US Services PMI Jun P | 54.9 | 56.8 |

No follow through buying in Sterling after strong but brief BoE rebound

The BoE triggered rebound in Sterling yesterday was initially rather strong, but lacked follow through buying. GBP/USD is kept well below key near term resistance at 1.3471. EUR/GBP is still hovering around mid-point of range of 0.8693/8844. Even GBP/JPY is held below 146.46 minor support. For the week, Sterling is staying in red against Dollar, Euro, Swiss and Yen. It's just up against the risk aversion hit Canadian, Australian and New Zealand Dollar.

GBP action bias table also reveals no notable momentum in the Sterling pairs.

Yesterday's more hawkish than expected BoE announcement just revived the chance of an August hike. That was indeed the base case as presented in the May Inflation Report. Remember that during the most Sterling bullish time earlier this year, markets were expecting a hike in May and speculating for another one in November. The BoE announce just solidify the case for a hike in the second half of the year, that is either in August or November, possibly in August. And it sort of ruled out the possibility of BoE standing pat for the rest of the year.

Suggested readings on BoE

DOW extends losing streak on trade war, 24247 support in focus

DOW closed down -196.10 pts or -0.8% overnight to 24461.70. Trade war fears extended the losing streak to eight days, longest in more than a year.

Technically, the break of near term trend line support this week, and the failure to regain 55 day EMA argues that rise from 23344.52 has completed earlier that expected at 25402.83. It couldn't reach 25800.35/26616.71 resistance zone. Immediate focus will be on 24247.84 today and next week. Break there could accelerate the selloff to 23344.52 support.

Overall, there there are a few interpretations of the price actions from 26616.71 high, they all point to the case that it's a correction that's not completed. That is, fall from 25402.83 could be a falling leg of the whole medium term correction pattern that could break through 23344.52 low. We'd maintain our view that the correction from 26616.71 should at least extend to 38.2% retracement of 15450.56 to 26616.71 at 22351.24 before completion.

Market Morning Briefing: Pound Tested Support In Downward Channel On Daily Candles Near 1.31

STOCKS

It seems that the global trade tensions continue to weigh on investor sentiments, leading to further fall in the Dow Jones. Dow (24461.70, -0.80%) may test 24250 in the coming sessions and look bearish for the near term.

Dax (12511.91, -1.44%) has possibility of testing 12300 while the index trades below 12800-12900. Near to medium term looks bearish for Dax too.

Nikkei (22520.97, -0.76%) tested 22800, in line with our expectation and may get some rejection from here towards 22200 or lower again. This is the third attempt to 22800 since May’18 and the index would find difficulty in breaking above 22800 just now. While the index trades below 22800, it could either be ranged in the 22000-22800 region or come off sharply in the longer run.

Shanghai (2861.89, -0.48%) tested 2950 on the upside before coming off from there. Support for the index could come from lower levels of 2800-2750 which would be gradually tested in the next couple of weeks. View remains bearish while below 3000.

Sensex (35432.39, -0.32%) is trading in the narrow 35300-35750 region and could soon move sharply on either side deciding the further course of movement. Nifty (10741.10, -0.29%) also trades just below 10850 and a break on the upside would be necessary to start a fresh upmove. Else a fall back to lower levels of 10600 would come into picture for the medium term.

COMMODITIES

News states that OPEC is likely to raise production by 0.5 mln barrels and while the markets wait for some decision from the OPEC meeting, crude prices could trade a bit higher. WTI (66.39) has moved up a bit and could test 67.0-67.5 levels in the near term. Brent (73.92) is also trading at slightly higher levels and has scope towards 75-76 just now.

Gold (1268.90) is almost stable. As mentioned earlier, we may look for an eventual fall towards 1250-1240 in the medium term.

Copper (3.0260) is trading lower as expected and it would be important to watch price action near 3.0. a break below 3, if seen would take the index towards 2.95-2.90 levels; else the index could bounce back from 3 to again rise to 3.10 and higher.

FOREX

Euro (1.1603) : Euro dipped to a more than 10 months low yesterday (1.1508) but then bounced from there towards 1.16. If it breaches 1.162, it could move up to 1.173 where the 34 days MA could provide crucial resistance. Inability to breach 1.162 would make it bearish towards 1.145 in the next week itself.

Dollar Index (94.86): Dollar Index has support near 94.5, which it could test next week. While above 94.5, it could again rise back towards 95.5.

Dollar Yen (110.01): As per our expectation at the beginning of the week, Dollar Yen has continued to oscillate between 111.0-109.5. As mentioned yesterday, Yen strength might resurface in the weeks ahead as markets get increasingly risk averse. A break below support on daily candles (near 109.5-110.0) sometime next week/week after that, is likely to make it bearish towards 107 in the medium term.

Euro Yen (127.65): If Euro moves past 1.162, Euro Yen might spend another week trading in the 127-130 zone above horizontal support on weekly line chart. However, likelihood of a gradual downtrend towards 1.24 (support on weekly candles) stays intact.

Pound (1.3257): Pound tested support in downward channel on daily candles near 1.31 yesterday and is now bouncing from there. It might see a rise towards 1.335 next week and then dip from there again, possibly targeting 1.30 in 2 weeks time.

Dollar Rupee (67.985): A dip into the 67.90-70 region could produce a strong bounce towards 68.50-65.

INTEREST RATES

Yields again dipped as global trade war worries continue to persist. Moreover, the Italian govt appointed 2 Euroskeptic lawmakers at the helm of important economic committees, thereby re-igniting fears of instability in the Euro zone.

German 10 year yield (0.335%) as per expectation, is tending towards support near 0.3% on the medium term chart and might test it next week.

US 10 year (2.9095%), 30 Year (3.052%), 5 Year (2.78%), 2 Year (2.55%) : US 10 Year yield is more or less stable around 2.9% currently as two opposing forces act on it:

1) the expectation of higher inflation in case the trade war intensifies (would be bullish for yields)

2) a sentiment of risk aversion due to the trade war (would be bearish for yields)

We might have to wait for a break below 2.85% before we can say that the 2nd factor is stronger.

Oil price in range ahead of pivotal OPEC meeting

WTI oil price is staying in range between 63.6/66.9 as markets await the pivotal meeting in Austria. Delegations of OPEC and non-OPEC oil producing countries are meeting today in Vienna. The producers are trying to reach a consensus on easing the output cap, that is raising production, to cool oil prices.

Saudi Arabia's Energy Minister Khalid Al-Falih, the defacto leader of OPEC, said yesterday that he was "optimistic" on a deal as there was a "spirit of cooperation" among the group. And they would discuss how to raise production by around 1 million barrels per day.

The United Arab Emirates' minister of energy and industry, and OPEC president, Suhail Al- Mazrouei emphasized that OPEC is "not a political organization" but a "commercial organization". Iraq's Oil Minister Jabbar Ali al-Luaibi also said he's "confident that we will reach some sort of agreement".

However, Iran, Iraq and Venezuela are known to oppose the relaxation of production cut. Iranian Oil Minister Bijan Zanganeh said he doubted OPEC could reach a deal this week and he was feeling "very good" about the current production levels.

Russian Energy Minister Alexander Novak warned that "Oil demand usually grows at the steepest pace in the third quarter ... We could face a deficit if we don't take measures." And, "this could lead to market overheating." Russia is pushing up to 1.5 million barrels per day of output raise, OPEC and non-OPEC countries together.

USD/JPY Following Uptrend Above 110.00

Key Highlights

- The US Dollar traded higher recently and settled above 109.80 against the Japanese Yen.

- There is a major ascending channel in place with support at 110.00 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending June 16, 2018 posted a decline from the last revised reading of 221K to 218K.

- Today in the US, the preliminary reading of the Services PMI for June 2018 will be released, which is forecasted to decrease from 56.8 to 56.4.

USDJPY Technical Analysis

The US Dollar found decent support around the 109.50 level and recovered against the Japanese Yen. The USD/JPY pair moved above the 109.80 and 110.00 resistance levels to gain traction.

Looking at the 4-hours chart, the pair was rejected from the 100 (red) and 200 (green) simple moving average (4-hour). It bounced back sharply and traded above the 50% Fib retracement level of the last decline from the 110.90 high to 109.54 low.

However, it struggled to move above the 110.75 level and is currently consolidating in a rage. There is a major ascending channel in place with support at 110.00 on the 4-hours chart of USD/JPY.

As long as the channel support, 100 SMA, and the 200 SMA are intact, the pair remains in an uptrend for more gains above 110.75 and 111.00 in the near term.

Recently in the US, the Initial Jobless Claims for the week ending June 16, 2018 was released by the US Department of Labor. The market was looking for a rise from the last reading of 218K to 220K.

However, the result was neutral as there was a decline from the last revised reading of 221K to 218K. Therefore, there was no rise in the claims and the 4-week moving average was 221,000, a decrease of 4,000 from the previous revised reading.

Economic Releases to Watch Today

- Germany's Manufacturing PMI for June 2018 (Preliminary) – Forecast 56.2, versus 56.9 previous.

- Germany's Services PMI for June 2018 (Preliminary) – Forecast 52.1, versus 52.1 previous.

- Euro Zone Manufacturing PMI June 2018 (Preliminary) – Forecast 55.0, versus 55.5 previous.

- Euro Zone Services PMI for June 2018 (Preliminary) – Forecast 53.7, versus 53.8 previous.

- US Manufacturing PMI for June 2018 (Preliminary) – Forecast 56.5, versus 56.4 previous.

- US Services PMI for June 2018 (Preliminary) – Forecast 56.4, versus 56.8 previous.

- Canadian Retail Sales April 2018 (MoM) – Forecast 0%, versus +0.6% previous.

- Canadian Retail Sales ex Autos April 2018 (MoM) – Forecast +0.5%, versus -0.2% previous.

- Canadian Consumer Price Index May 2018 (MoM) – Forecast +0.3%, versus +0.3% previous.

- Canadian Consumer Price Index May 2018 (YoY) – Forecast +2.5%, versus +2.2% previous.

Japan CPI Core unchanged, PMI manufacturing improved

Released from Japan, all items CPI rose to 0.7% yoy in May, up from 0.6% yoy. Core CPI, less fresh food, was unchanged at 0.7% yoy. Core core CPI, less fresh food and energy even slowed to 0.3% yoy, down from 0.4% yoy. The data highlighted BoJ's inability to lift inflation and inflation expectation even with the ultra-loose monetary policy. And the central bank is still a long way from stimulus exit.

PMI manufacturing rose to 53.1 in June, up from 52.8, beat expectation of 52.6. Comments by Joe Hayes, Economist at IHS Markit:

"The final PMI reading of the second quarter revealed a quickened pace of growth across the Japanese manufacturing economy.

"The sector has sustained a relatively solid upward trend across 2018. June data indicated continued growth in new orders, a faster rate of job creation, rising backlogs of work and increasing output prices. As such, there appears to be further legs in the manufacturing growth cycle.

"That said, for the first time since August 2016, new export orders declined. With geopolitical risk aplenty, haven demand for the yen remains a downside risk to the country's manufacturing exporters."