Sample Category Title

USD/CHF Mid-Day Outlook

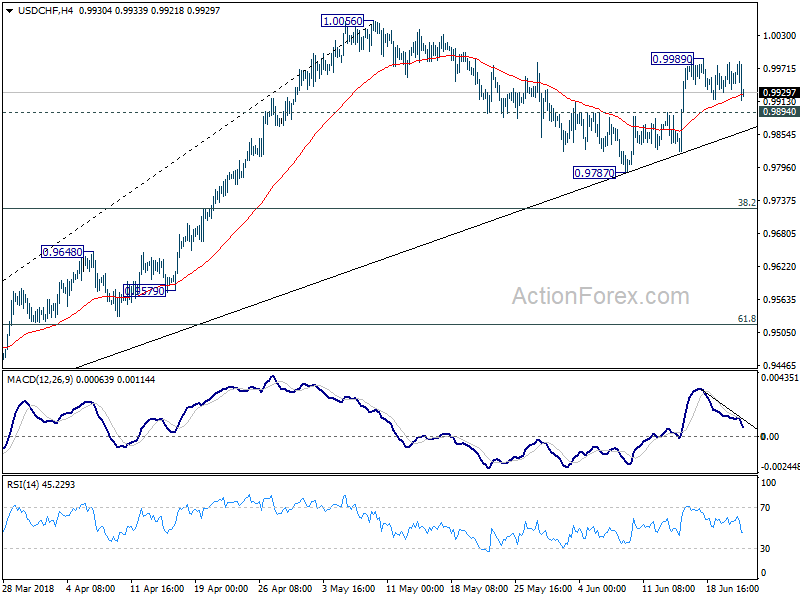

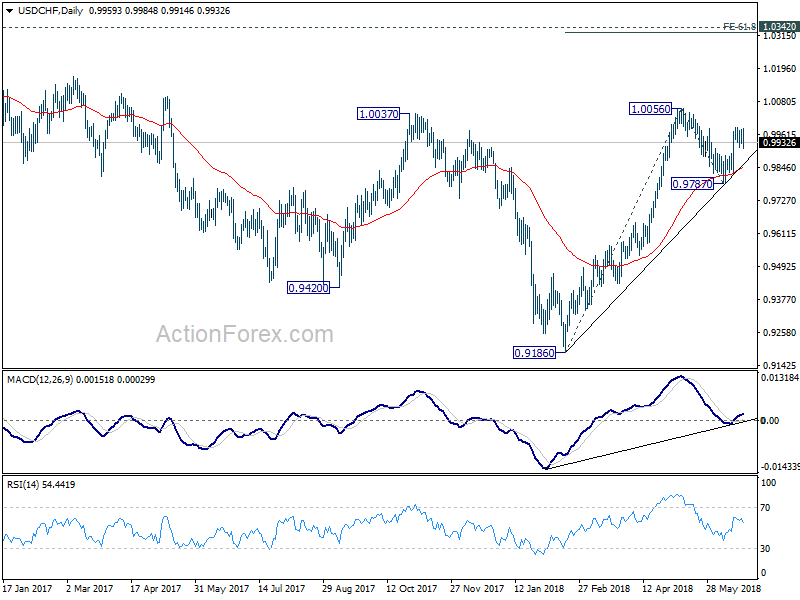

Daily Pivots: (S1) 0.9937; (P) 0.9960; (R1) 0.9984; More...

USD/CHF failed to take out 0.9989 temporary top and retreats. Intraday bias remains neutral at this point. Outlook is unchanged that corrective fall from 1.0056 should have completed at 0.9787. Further rally is expected as long as 0.9894 minor support holds. On the upside, above 0.9989 will bring retest of 1.0056 first. Break will resume the rise from 0.9186 and target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, break of 0.9894 will likely extend the correction, possibly through 0.9787 before completion.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

EUR/USD Mid-Day Outlook

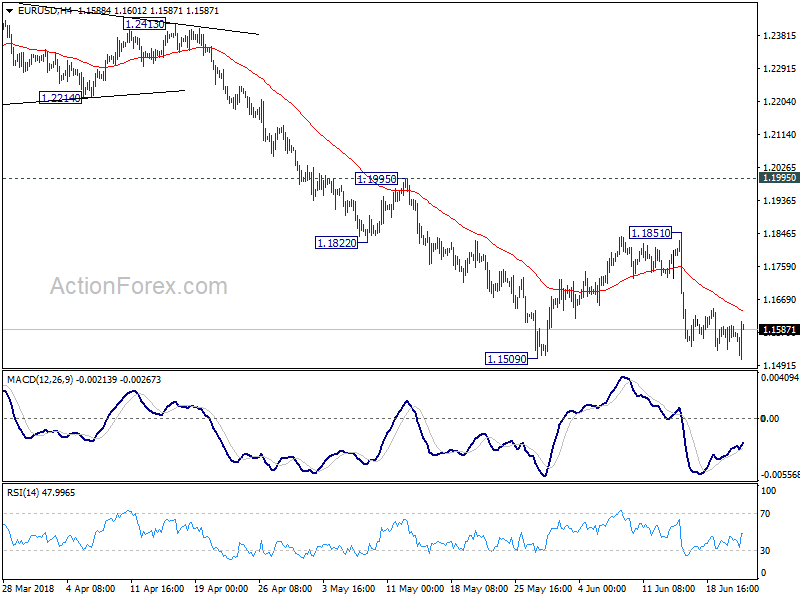

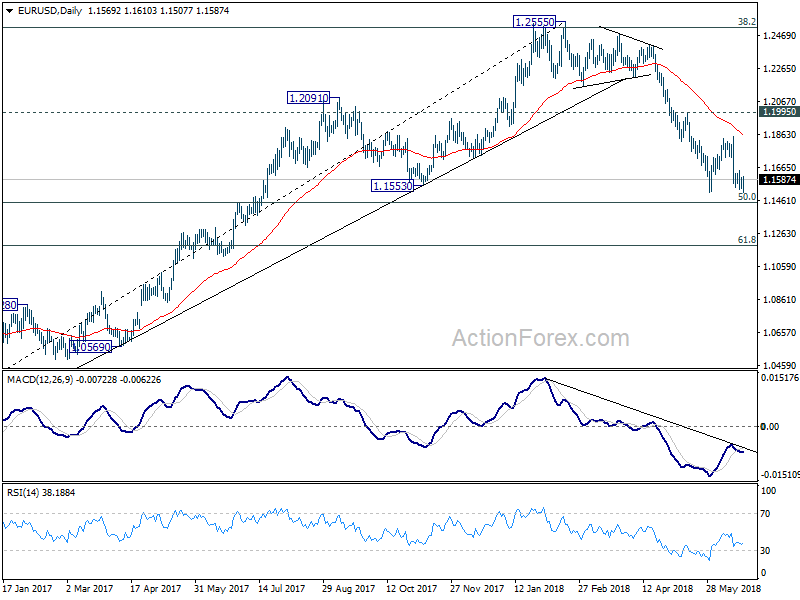

Daily Pivots: (S1) 1.1541; (P) 1.1572 (R1) 1.1606; More.....

EUR/USD quickly recovers after breaching 1.1509 to 1.1507 and intraday bias remains neutral first. More consolidation could be seen and another recovery cannot be ruled out. But upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

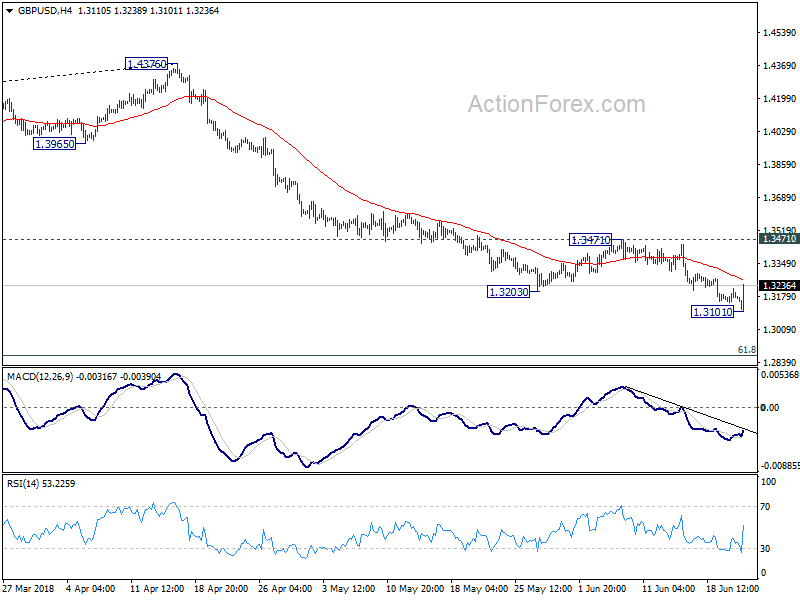

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3142; (P) 1.3179; (R1) 1.3211; More...

GBP/USD rebounds strongly after edging lower to 1.3101. As a temporary low is formed, intraday bias is turned neutral for consolidation. But still, near term outlook will remain bearish as long as 1.3471 resistance holds. And larger decline is expected to continue. On the downside, break of 1.3101 will resume the fall from 1.4376 for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Sterling Rebounds on Hawkish BoE Split, Gold Tumbles

The British Pound was thrown a much-needed lifeline today following an unexpectedly hawkish statement and MPC vote split from the Bank of England.

Market expectations over a possible UK interest rate hike this year were boosted after the monetary policy committee voted 6-3 in favour of keeping rates unchanged. Policymakers expressed optimism over the tepid first-quarter economic growth being temporary, which opened the door to a potential rate hike in August. While today’s hawkish surprise from the BoE could boost the Pound, which remains highly sensitive to monetary policy speculation, gains are likely to be capped further down the road. With Brexit-related uncertainty not only damaging buying sentiment towards the Pound but also potentially obstructing the BoE’s path towards monetary policy normalization, Sterling remains vulnerable to further weakness.

King Dollar clobbers Gold

Gold has been repeatedly attacked by a broadly stronger Dollar for the most part of this trading week.

One would have expected heightened trade concerns to elevate the yellow metal, but prices simply remained at depressed levels. Hawkish comments from Fed Chair Jerome Powell at the ECB Forum simply worsened matters for zero-yielding Gold, with prices tumbling to fresh six-month lows. While uncertainty over global trade tensions may offer some support further down the road, investors seem more concerned with an appreciating Dollar and Fed hike expectations. Focusing solely on the technical picture, Gold is firmly bearish on the daily charts. Sustained weakness below the $1280 level could open a path towards $1260.

Sterling Jumps as Chance of August BoE Hike Revived by Haldane

Sterling trades as the strongest one today as markets were surprised by the voting on BoE Bank Rate. With the highly respected Chief Economist Andrew Haldane voted for a hike, the chance of an August move in interest rate is heavily boosted. The statement also showed a lot of confidence among policy makers on the growth and inflation outlook. Meanwhile, Swiss Franc is also firm after SNB gave the markets no surprise with the monetary policy decision and the statement. Though, the Franc lags behind Aussie, which is trading as the second strongest. On the other hand, Euro is broadly lower today as the weakest, follow by Yen.

Technically, however, the outlook remains largely unchanged despite today's movements. Firstly, while GBP/USD's rebound is strong, it's kept well below 1.3471 key near term resistance. Bearish outlook remains and GBP/USD could be having just more consolidations first. EUR/GBP is still bounded in range of 0.8693/8844 and stays neutral. GBP/JPY is also held below 146.46 minor resistance, which favors more downside ahead. Euro, dipped to 1.1507 but recovered and it's holding on to 1.1509 support so far. There is no confirmation of breakout yet.

From the US, initial jobless claims dropped to 218k in the week ended June 16. Philly Fed manufacturing index dropped to 19.9 in June. Canada wholesale sales rose 0.1% mom in April.

Sterling surges as BoE chief economist Haldane joined hawks to vote for rate hike

Sterling surges BoE kept bank rate unchanged 0.50% with 6-3 vote. The usual suspects Ian McCafferty and Michael Saunders voted for a hike to 0.75%. And to many's surprise, chief economist Andrew Haldane voted for a hike too. His vote carries much significance.

On growth, BoE noted the judgement that the dip in Q1 was temporary "appears broadly on track". It pointed to the rebound in household consumption and sentiments as evidence while "employment growth has remained solid". Despite decline in manufacturing output in April, surveys of business activity have been stable. And overall, the data "point to growth in the second quarter in line with the Committee's May projections.

On inflation, BoE expects CPI to "pick up by slightly more than projected" in the near term. That reflects " higher dollar oil prices and a weaker sterling exchange rate." And, indicators of wage growth also picked up with labor markets remains tight. "Domestic cost pressures will continue to firm gradually, as expected."

On forward guidance, BoE expects to maintain the size of assets purchased at GBP 435B and use the Bank Rate as "primary instrument" for momentary policy for now. And BoE will NOT reduce the size of the assets until Bank Rate reaches around 1.50%, lowered from prior guidance of around 2.00%.

Also from UK, public sector net borrowing dropped to GBP 3.4B in May.

SNB stands pat, raised 2018 inflation forecasts, but lowered 2020's

SNB left monetary policy unchanged as widely expected. Sight deposit rate is held at -0.75%. Three-month Libor target range is kept at -1.25% to -0.25%. SNB also pledge to stand by for intervention and "remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration".

2018 inflation forecast was raised to 0.9%, up from March projection of 0.6%. That's due to a "marked rise in the price of oil". 2019 inflation forecast was kept unchanged at 0.9%. Though, from mid-2019, the new condition forecast is lowered due to "muted outlook in the euro area". For 2020, inflation forecast was lowered to 1.6%, down from March projection of 1.9%.

All the inflation forecasts were based on assumption the three month Libor remains at -0.75% over the entire forecast horizon.

On global growth, SNB expected economy to continue to grow above its potential. But risks are "more to the downside" due to "political developments in certain countries as well as potential international tensions and protectionist tendencies." Swiss GDP is projected to growth at around 2% in 208, unchanged. And unemployment is expected to fall further.

Also from Swiss, trade surplus widened to CHF 2.76B in May.

EU Malmstrom urges New Zealand to lead by example together on multilateral trade

EU Trade Commissioner Cecilia Malmstrom launched free trade negotiation with New Zealand in Wellington today. Trade negotiation teams from both sides would start the first round of talks in Brussels over July 16-20. Malmstrom said in a press conference after meeting New Zealand trade minister David Parker that "today is an important milestone in EU- New Zealand relations. Together, we can conclude a win-win agreement that offers benefits to business and citizens alike."

She also emphasized that "This agreement is an excellent opportunity to set ambitious common rules and shape globalization, making trade easier while safeguarding sustainable development. We can lead by example."

Malmstrom also hailed New Zealand as "a friend, an ally". And she urged that "together we stand up for common values … of sustainable trade, open trade, transparent trade, and trade that is done in compliance with international rules in the multilateral system."

The New Zealand government recently launched its "Trade for All Agenda", calling for a "progressive and inclusive" approach to negotiating trade deals. Parker said "we can not only do good for ourselves in this trade agreement but we can actually set out rules for how trading agreements should look for the betterment of the world."

Parker also hailed that Malmstrom has asked negotiators to work through the complicated areas early, so as not to cause delays in the end. He said "I think that demonstrates a willingness on the part of the European side of the negotiation, which we share, to bring this to a conclusion as soon as we can."

New Zealand GDP growth slowed to 0.5% qoq in Q1

New Zealand GDP grew 0.5% qoq in the March quarter, slowed from 0.6% qoq in the prior quarter and met expectation. Over the year, GDP grew 2.7% ended March 2018. Per capita GDP was unchanged, down from 0.1% qoq rise in the prior quarter. Services industries grew 0.6%, notably slowed from prior 1.1%. Good-producing industries were flat as jump in manufacturing was offset by fall in constructions. Primary industries rebounded by growing 0.6%, up from prior quarter's -2.6%.

Chinese Vice Premier to meet European Commission Vice President Katainen next week on trade

Chinese Vice Premier Liu He will be meeting with European Commission Vice President Jyrki Katainen in Beijing on June 25. That's the seventh China-EU high level economic and trade summit since 2007, when the mechanism was established.

Spokesman of the Ministry of Commerce said in a regular briefing that the meeting is an important platform for for communications and coordinations of economic and trade policies. And it's an important time when "trade and economic cooperation faces new historical opportunities."

Issues to be discussed will include " global economic governance, trade and investment, innovation-driven development, and interconnection that are of common concern to both sides". And, it's a "positive signal between China and the EU to oppose unilateralism and protectionism and support the multilateral trading system."

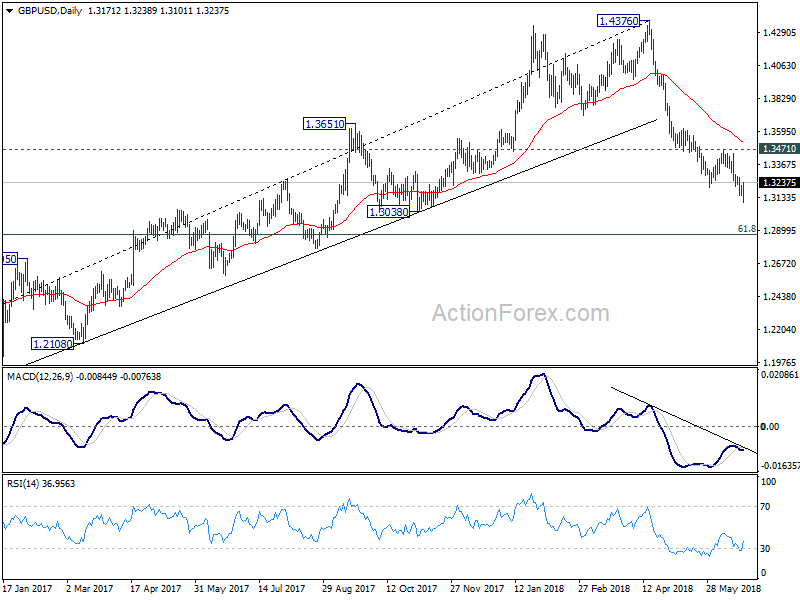

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3142; (P) 1.3179; (R1) 1.3211; More...

GBP/USD rebounds strongly after edging lower to 1.3101. As a temporary low is formed, intraday bias is turned neutral for consolidation. But still, near term outlook will remain bearish as long as 1.3471 resistance holds. And larger decline is expected to continue. On the downside, break of 1.3101 will resume the fall from 1.4376 for 61.8% retracement of 1.1946 to 1.4376 at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 0.50% | 0.50% | 0.60% | |

| 06:00 | CHF | Trade Balance (CHF) May | 2.76B | 1.89B | 2.29B | 2.24B |

| 07:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 07:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 07:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 08:30 | GBP | Public Sector Net Borrowing May | 3.4B | 5.1B | 6.2B | 5.3B |

| 11:00 | GBP | BoE Official Bank Rate | 0.50% | 0.50% | 0.50% | |

| 11:00 | GBP | BoE Asset Purchase Target Jun | 435B | 435B | 435B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 3--0--6 | 2--0--7 | 2--0--7 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.10% | 0.50% | 1.10% | 1.40% |

| 12:30 | USD | Initial Jobless Claims (JUN 16) | 218K | 220K | 218K | 221K |

| 12:30 | USD | Philly Fed Manufacturing Index Jun | 19.9 | 25 | 34.4 | |

| 13:00 | USD | House Price Index M/M Apr | 0.30% | 0.10% | ||

| 14:00 | USD | Leading Index May | 0.40% | 0.40% | ||

| 14:00 | EUR | Eurozone Consumer Confidence (JUN A) | 0 | 0 | ||

| 14:30 | USD | Natural Gas Storage | 96B |

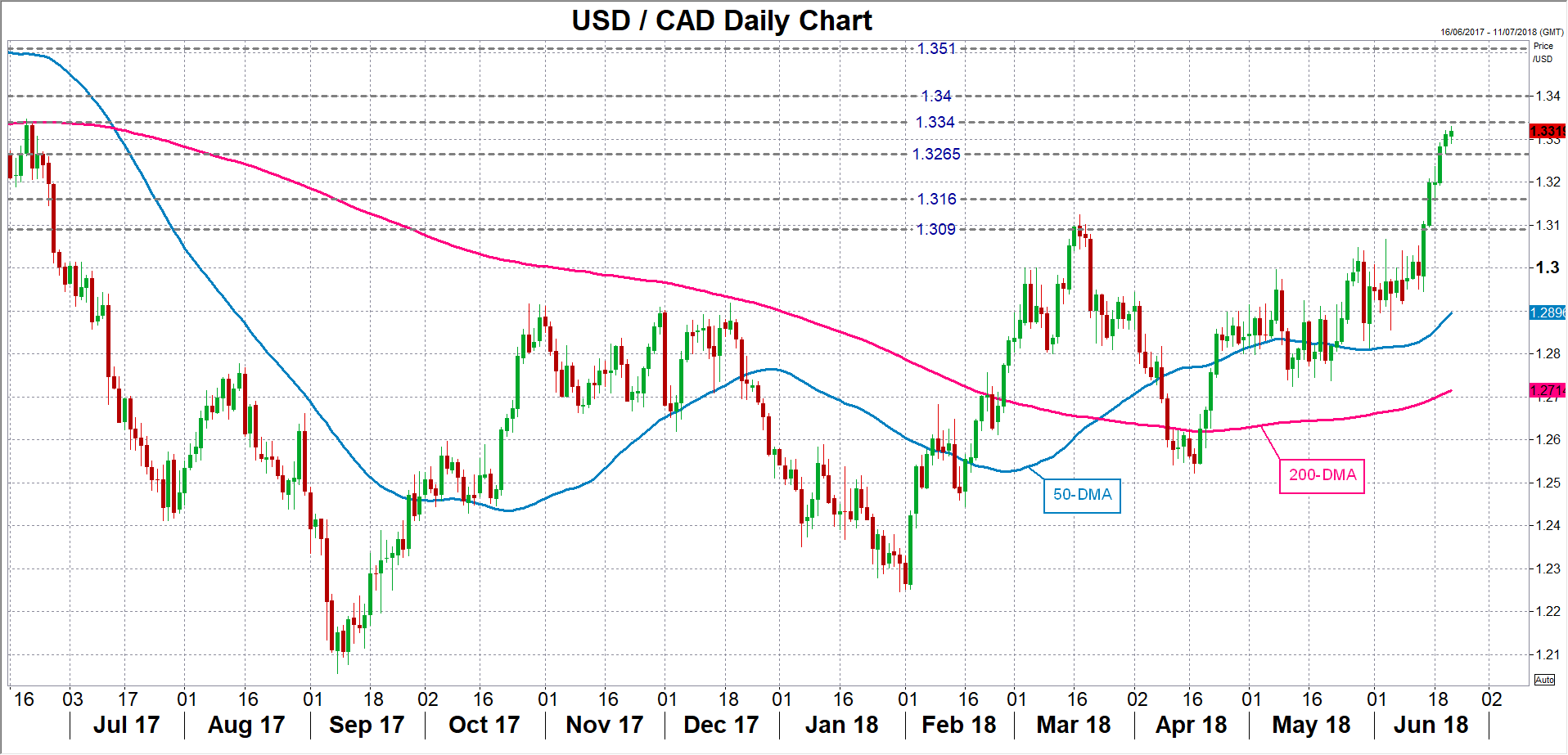

Canadian Dollar Steady ahead of U.S, Canadian Employment Data

The Canadian dollar is showing little movement in the Thursday session. Currently, USD/CAD is trading at 1.3319, up 0.06% on the day. On the release front, there are employment releases on both sides of the border. Canada will publish ADP Nonfarm Employment Change and Wholesale Sales. In the U.S, Philly Fed Manufacturing Index is forecast to drop to 28.9 points. As well, unemployment claims are expected to edge up to 220 thousand.

With trade tensions making investors increasingly nervous, the Canadian dollar has hit some significant headwinds. USD/CAD has declined 3.0% since June 11 and continues to struggle at 12-month lows. Canada is particularly vulnerable to protectionist moves south of the border, as some 80% of Canadian exports go to the United States. With President Trump making good on his threat to slap tariffs on his trading partners, the Canadian government is scrambling to protect the economy. Trump has said the U.S could impose tariffs of 25 percent on Canadian-built vehicles, which would be disastrous for the Canadian automotive sector, which is worth some C$80 billion to the economy every year. The Trudeau government has promised to help sectors hit with US tariffs, but bailing out the auto industry would cost billions. Canada may have to provide the U.S with more concessions in the NAFTA negotiations, in order to stave off tariffs against Canadian vehicles, which could have a disastrous effect on economic growth.

Into US session: Sterling strongest on BoE, but it’s not bullish yet

Entering into US session, Sterling is now the strongest one today as boosted by hawkish BoE hold. Most importantly, heavy weight Chief Economist Andy Haldane joined known hawks Ian McCafferty and Michael Saunders to vote for a hike. Euro is now trading as the second weakest, followed by Yen and New Zealand Dollar.

GBPUSD H and 6H action bias has turned neutral with the rebound, after a string of downside red bars. Still, it's kept well below 1.3471 near term resistance. Overall outlook remains bearish though but some more consolidation could come first.

Meanwhile, EUR/GBP is still clearly held in range with a neutral outlook.

GBP/JPY is also neutral as the corrective pattern from 144.37 extends.

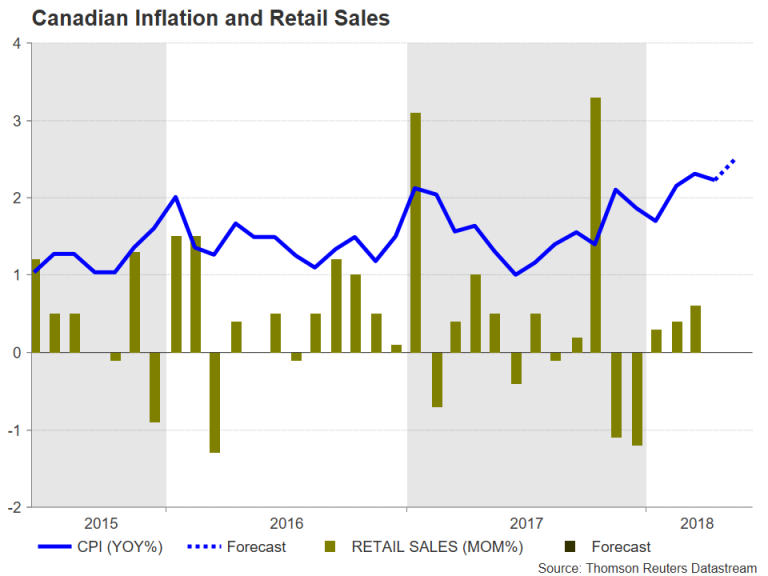

Canadian Inflation Data Likely To Add To Dilemma For Bank Of Canada

Canada will see the release of monthly inflation and retail sales figures on Friday at 12:30 GMT. The data comes just under three weeks before the Bank of Canada holds its next policy meeting on July 11 when policymakers will ponder whether to raise interest rates for a second time this year. While strong numbers on Friday would boost rate hike expectations for next month, the Canadian dollar may struggle to find much support from the data amid a worsening trade row with the United States.

Annual inflation in Canada hit a 3½-year high of 2.3% in March before easing slightly to 2.2% in April. It is expected to head back up again in May, rising to 2.5%, which would make it a 6-year high. On a month-on-month basis, CPI is forecast to rise by 0.3%. If confirmed, it would take inflation closer to the BoC's upper target band of 3%, increasing pressure on the central bank to tighten monetary policy at its July meeting. But the BoC will also be watching its core CPI indicator, which stood significantly below the headline rate in April, at 1.5%.

Also due on Friday are retail sales numbers for April. Retail sales grew by a solid 0.6% m/m in March – double the expected rate. However, this was mainly on the back of strong vehicle sales, and excluding autos, sales were down over the month. The opposite trend is forecast for April with retail sales expected to post no growth during the month, but the core measure is anticipated to rebound by 0.5% m/m.

If Friday's data points to a strengthening in price pressures and consumption, the Bank of Canada would be more inclined to raise its key policy rate by 0.25% in July. Market betters are currently pricing about a 70% probability that the BoC will act next month. However, stronger-than-expected numbers ahead of the BoC meeting may not be enough to convince policymakers to raise rates given the somewhat disappointing first quarter growth and May employment figures, and not to mention the growing trade tensions with the US – Canada's biggest trading partner by far.

The Canadian dollar has taken a hammering over the past week as an intensifying trade dispute between the US and China has dampened the chances of a quick resolution of the NAFTA renegotiation. The growing trade risks drove the loonie to a one-year low of C$1.3329 to the US dollar on Thursday and the currency is at risk of further losses from the escalation in trade tensions.

A negative set of data on Friday could deepen the loonie's woes and clear the way to the C$1.3340 level (a low from June 2017). Above this area, support could come from the psychological C$1.34 handle. A break above this mark would bring into scope the C$1.3510 level.

However, with the loonie looking oversold, a broadly positive release could trigger a sharp technical correction against the greenback. Immediate resistance is likely to come at the C$1.3265 level in the event of a reversal. Further gains could see the next hurdle coming at C$1.3160 followed by the C$1.3090 region.

Norway Clarifies Timing For 1st Potential Rate Hike, Italy Appoints A Euro-Skeptic To A Key Govt Committee

Notes/Observations

- No surprises in central bank rate decision in session (SNB, Norges and Taiwan all keeping policy steady)

- Norway fines tunes its 1st potential rate hike to Sept (from after summer)

- Italy appoints a Euro-skeptic to head its Parlaimentary Finance Committee, Italian yield s higher, Euro currency at 3-week lows

Asia:

- BOJ Funo reiterated need to patiently promote strong monetary easing under current framework

- New Zealand Q1 GDP in line (Q/Q: 0.5% v 0.5%e; Y/Y: 2.7% v 2.7%e)

Europe:

- ECB reportedly sees more reinvestments from QE in 2019 with at least €160B QE debt maturing next year expected to be reinvested

- UK govt won a vote in parliament, defeating Brexit 'meaningful vote' amendment (As expected after compromise made earlier)

- S&P affirmed EU sovereign rating at AA; outlook Stable

- EU draft proposal on migrants: to strengthen external border protection; members agree to support migrant reception and resettlement outside of the EU

Americas:

- Fed Chair Powell: gradual rate hike case was broadly supported on FOMC; despite uncertainty around full employment level, case for gradual hikes is strong

- President Trump said to be considering plans to curb Chinese investment in more than 1,000 US companies

- Brazil Central Bank (BCB) left its Selic Target Rate unchanged at 6.50% (as expected) for its 2nd straight pause in the current easing cycle

Energy:

- Saudi Arabia said to be seeking a 600-800K bpd production increase from OPEC+ producers

Economic Data:

- (NL) Netherlands Jun Consumer Confidence: 23 v 23 prior

- (NL) Netherlands May Unemployment Rate: 3.9% v 3.9%e

- (NL) Netherlands Apr Consumer Spending Y/Y: 3.0% v 3.2% prior

- (CH) Swiss May Trade Balance (CHF): 2.8B v 2.3B prior, Real Exports M/M: 0.0% v 0.4% prior, Real Imports M/M: +3.1% v -0.4% prior

- (DK) Denmark Jun Consumer Confidence: 10.6 v 8.5e

- (NL) Netherlands May House Price Index M/M: 0.9% v 0.4% prior; Y/Y: 8.9% v 8.8% prior

- (HU) Hungary Q1 Current Account: €1.0B v €0.9Be

- (FR) France Jun Business Confidence: 106 v 106e; Manufacturing Confidence: 110 v 108e, Own-Company Production Outlook: 14 v 16e, Production Outlook Indicator: # v 15 prior - (CH) Swiss May M3 Money Supply Y/Y: 2.9% v 3.3% prior

- (HU) Hungary Apr Average Gross Wages Y/Y: 12.6% v 10.5%e

- (TR) Turkey Jun Consumer Confidence: 70.3 v 69.9 prior

- (MY) Malaysia Mid-Jun Foreign Reserves: $107.9B v $108.5B prior

- (CH) Swiss National Bank (SNB) left its Sight Deposit Interest Rate unchanged at -0.75% (as expected) and maintained its 3-month Libor Range between -0.25% to -1.25%

- (TW) Taiwan May Export Orders Y/Y: 11.7% v 8.6%e

- (NO) Norway Central Bank (Norges) left its Deposit Rates unchanged at 0.50% (as expected)

- (PL) Poland May Retail Sales M/M: 2.7% v 1.9%e; Y/Y: 7.6% v 7.4%e, Real Retail Sales Y/Y: 6.1% v 6.0%e

- (ZA) South Africa Q1 Current Account (ZAR): -229B v -188Be; Current Account to GDP Ratio: -4.8% v -3.9%

- (ES) Spain Apr Trade Balance: -€3.1B v -€0.8B prior

- (UK) May Public Finances (PSNCR): +£4.5B v -£9.7B prior; Public Sector Net Borrowing: £3.4B v £4.9Be; Central Govt NCR: +£6.9B v -£6.1B prior; PSNB (ex-banking): £5.0B v £6.3Be

- (HK) Hong Kong May CPI Composite Y/Y: 2.1% v 2.1%e

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €5.0B vs. €4.5-5.5B indicated range in 2023, 2025, 2033 and 2044 Bonds

- Sold €2.0B in 0.35% July 2023 SPGB; Avg yield: 0.336% v 0.440% prior; Bid-to-cover: 1.61x v 2.88x prior

- Sold €1.176B in 1.60% Apr 2025 SPGB bond; Avg Yield: 0.699% v 1.073% prior; Bid-to-cover:1.71x v 1.94x prior

- Sold €743M in 2.35% July 2033 SPGB; Avg Yield: 1.830% v 1.723% prior; Bid-to-cover: 1.99x v 1.96x prior

- Sold €1.087B in Oct 5.15% 2044 SPGB bond; Avg Yield: 2.353% v 2.775% prior; Bid-to-cover: 1.33x v 1.25x prior

- (FR) France Debt Agency (AFT) sold total €8.494B vs. €7.5-8.5B indicated range in 2021, 2022 and 2024 Bonds

- Sold €2.409B in 0.0% Feb 2021 Oat; Avg Yield: -0.46% v -0.30% prior; Bid-to-cover: 3.25x v 1.97x prior

- Sold €1.889B in 3.00% Apr 2022 Oat; Avg yield: -0.34% v -0.26% prior; Bid-to-cover: 2.71x v 1.91x prior

- Sold €4.196B in 0.0% Mar 2024 Oat; Avg Yield: 0.03% v 0.10% prior; Bid-to-cover: 1.97x v 2.42x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 flat at 384.2, FTSE +0.2% at 7643, DAX -0.5% at 12634, CAC-40 -0.2% at 5363, IBEX-35 -0.7% at 9723, FTSE MIB -1.0% at 21891, SMI +0.1% at 8562, S&P 500 Futures -0.2%]

- Market Focal Points/Key Themes: European Indices come off the highs, lead by the Dax which is weighed lower by Automakers following a profit warning from Car giant Daimler, citing potential auto tariffs and clamp down on diesel emission cars. BMW and Volkswagen also trade lower in sympathy. Elsewhere Dixons Carphone rebounds following there full year results, whilst Bpost falls after seeing FY EBIT at lower end of prior range. In the Healthcare space Novo Nordisk trades higher after its diabetes drug showed positive results. Looking ahead notable earners include Kroger, Darden and Patterson Companies.

Movers

- Consumer Discretionary Dixons Carphone [DC.UK] +4.2% (Earnings), Page Group [PAGE.UK] +3.5% (Analyst upgrade)

- Industrials Daimler [DAI.DE] -4.1% (Profit warning), BMW [BMW.DE] -3.2%, Volkswagen [VOW3.DE] -2.1% (In sympathy with Daimler), Bpost [BPOST.BE] -7.5% (Mid term outlook), Chemring [CHG.UK] +0.8% (Earnings)

- Healthcare Novo Nordisk [NOVOB.DK] +4.3% (Trial data)

Speakers

- ECB's Villeroy (France) reiterated that inflation was moving in the right direction but might be a bit less certain on where we were in the economic cycle. Risk of a global trade war is no longer unthinkable

- SNB Quarterly Policy Statement reiterated its view that CHF currency (franc) remained highly valued while FX market remained fragile. It also reiterated that negative interest rates and FX intervention pledge remained essential. SNB maintained its 2018 GDP growth forecast but did raise its CPI forecast to 0.9%. It noted that the risks to its baseline scenario were more to the downside

- Norway Central Bank (Norges) Policy Decision noted that the vote was to keep policy steady was unanimous . It tweaked its language on 1st potential rate hike to be likely in Sept (**Note: prior view was 'after summer). Outlook suggested a cautious approach to rate hikes and saw gradual hikes in the years ahead. Upturn in economy was continuing and saw wage inflation further out

- Norway Central Bank (Norges) Gov Olsen post rate decision press conference reiterated its earlier statement that Sept rate hike was most likely scenario

- SNB's Jordan post rate decision press conference stated that was keeping an eye on ECB policy. He did not see any reason to change its policy and would not give forecasts on its rate path

- Eurogroup chief Centeno: Greece had complied with all prior bailout actions. Eurogroup to deliver on Greek debt package

- Italy Interior Min Salvini (also Dep PM) Confident that EU will be able to reach an agreement on immigration

- Italy Senate Finance Committee said to have named Euro-skeptic Bagnai as its head

- Ireland Foreign Min Coveney: Doubt that will see sufficient progress by end of Jun for Brexit talks

- Germany Finance Ministry cut its Q3 capital market issuance by €6B to €37B. Implementing the reduction by cutting the offer volumes at seven of the 13 nominal-bond auctions scheduled in 3Q

- Iraq Oil Min Al-Luaibi: Working to narrow the differences with Saudi officials. Was in favor keeping production at current level through end of 2018

- OPEC Secretariat said to be looking at higher production quotas if the group raises output

- Saudi Arabia Energy Ministry Al-Falih: Needed to release supplies to market as over compliance by OPEC was 1M bpd. Some members have stated that they could not increase supplies. World to face 1.6-1.8M bpd oil supply deficit in H2 and could not let this happen

Currencies

- USD maintained its firm tone against the major pairs in the session.

- EUR/USD was probing the lower end of the 1.15 level after reports circulated that Italy appointed a Euro-skeptic to head its Senate Finance Committee. The news sent Italian yield s higher

- USD/JPY in the mid-110 area aided by comments on Wed by US Secretary of Commerce Wilbur Ross who noted that he did not think the Chinese want a trade war any more than we did

- GBP/USD was in the lower end of the 1.31 area ahead of the BOE rate decision. Cable was weaker on the back of shaky political situation in the UK despite the recent govt victory on the meaningful exit vote. Analysts also noted that a dovish split in today MPC vote could further weigh upon the Pound currency

- EUR/NOK was lower by 0.7% to test below 9.40 level after Norway Central Bank gave a specific month for its 1st potential rate hike.

Fixed Income

- Bund Futures trade 16 ticks higher at 161.48 as the conciliatory US tone damps haven bid. Upside targets 162.25 followed by 162.75, while a return lower targets the 158.75 level.

- Gilt futures trade at 122.86 higher by 10 ticks following the move from US Treasuries. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Thursday's liquidity report showed Wednesday's excess liquidity fell from €1.845T to €1.840T. Use of the marginal lending facility fell from €97M to €83M.

- Corporate issuance saw Volkswagen and Danske pay up to attract to less in the primary market

Looking Ahead

- (UK) BOE Gov Carney’s annual Mansion House speech (evening local time)

- (IL) Israel May Leading 'S' Indicator M/M: No est v 0.4% prior

- (PT) Portugal Apr Current Account: No est v €0.3B prior

- (PT) Bank of Portugal June Economic Bulletin

- (AR) Argentina Jun Consumer Confidence: No est v 36.1 prior

- (TW) Taiwan Central Bank (CBC) Interest Rate Decision: Expected to leave Benchmark Interest Rate unchanged at 1.375% (no set time)

- 05:30 (HU) Hungary Debt Agency (AKK) to sell bonds (3 tranches)

- 05:50 (FR) France Debt Agency (AFT) to sell €1.5-2.0B in 2027, 2028 and 2047 inflation-linked bonds (Oatei)

- 06:00 (IL) Israel Apr Manufacturing Production M/M: % v 0.3% prior - 06:00 (RO) Romania to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (UK) Bank of England (BOE) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.50%

- 08:00 (BR) Brazil Mid-Jun IBGE Inflation IPCA-15 M/M: 1.0%e v 0.1% prior; Y/Y: 3.6%e v 2.7% prior

- 08:00 (PL) Poland Central Bank (NBP) Jun Minutes

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Jun Philadelphia Fed Business Outlook: 29.0e v 34.4 prior

- 08:30 (US) Initial Jobless Claims: 220Ke v 218K prior; Continuing Claims: 1.71Me v1.697M prior

- 08:30 (CA) Canada May ADP Payrolls Report: No est v +30.2K prior

- 08:30 (CA) Canada Apr Wholesale Trade Sales M/M: 0.3%e v 1.1% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (RU) Russia Gold and Forex Reserve w/e Jun 15th: No est v $461.0B prior

- 09:00 (US) Apr FHFA House Price Index M/M: 0.5%e v 0.1% prior

- 09:00 (EU) Eurogroup Finance Ministers meet in Luxembourg

- 10:00 (EU) Euro Zone Jun Advance Consumer Confidence: 0.0e v 0.2 prior

- 10:00 (US) May Leading Index: 0.4%e v 0.4% prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 13:00 (US) Treasury to sell 30-Year TIPS Reopening

- 14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to raise Overnight Rate by 25bps to 7.75%

- 15:00 (AR) Argentina May Trade Balance: -$0.6Be v -$0.9B prior

- 16:30 (US) Fed to release Dodd-Frank bank stress test results

GBPUSD Strongly Bearish Below 1.3100

The British pound has fallen to a fresh 2018 trading-low against the US dollar, as sterling comes under heavy selling pressure ahead of today’s Bank of England rate decision. Yesterday, sterling was strongly rejected from the 1.3215 level, despite British Prime Minister passing a key Brexit vote through the House of Commons. The GBPUSD pair currently trades around the 1.3110 level, with technical selling increasing following the earlier breach of the 1.3145 support level.

The GBPUSD pair is strongly bearish while trading below the 1.3100 level, key technical support is now located at the 1.3060 and 1.3000 levels

If the GBPUSD pair moves above the 1.3145 level, key technical resistance can be found at the 1.3190 and 1.3215 levels.