Sample Category Title

SNB: The Song Remains The Same

The Swiss National Bank (SNB) is widely expected to keep its policy unchanged when it meets on Thursday, at 0730 GMT. Markets will look for hints on whether the Bank is contemplating an eventual exit from its ultra-loose policies. Although Swiss economic data are painting a more colorful picture, it still appears too early for policymakers to signal an exit from negative interest rates. Continued dovish signals would argue for a weaker franc over time, absent any global risk-off developments.

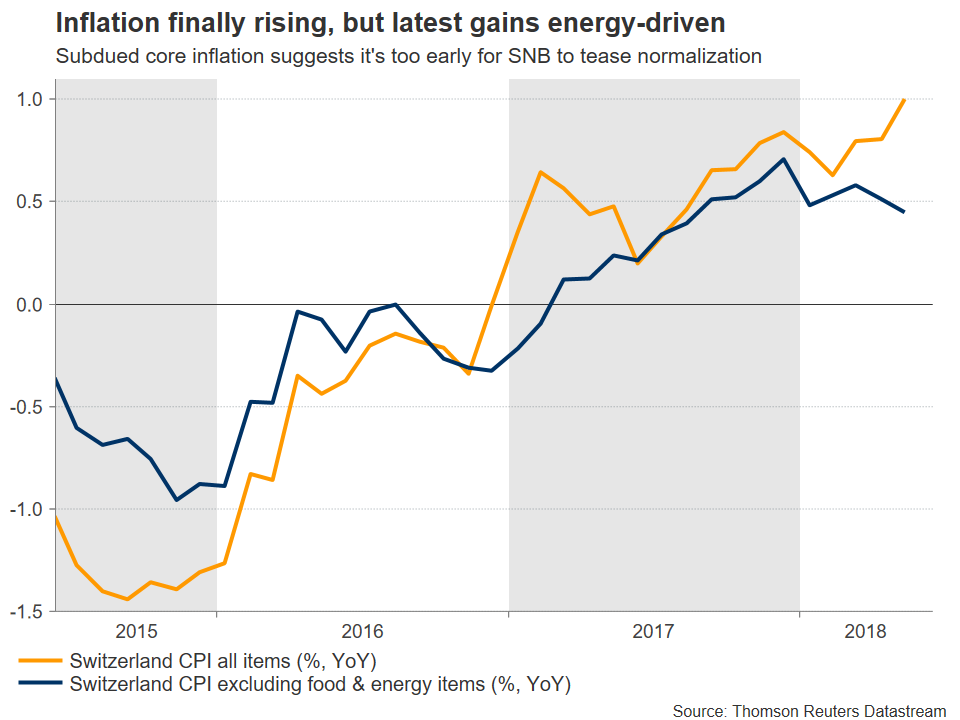

Up until the beginning of May, things were looking rosy for SNB officials. The domestic economy was posting gains, inflation was on a slow but steady uptrend, and the Swiss franc was losing substantial ground against both the dollar and the euro. As a reminder, the SNB pays close attention to the exchange rate. A stronger currency tends to hold back inflation by lowering import prices, and since the franc appreciates in times of turmoil due to its safe-haven status, the Bank has regularly intervened in FX markets to keep the currency weaker.

Even though economic data have remained upbeat – with solid GDP growth in Q1, the unemployment rate reaching a decade-low and inflation touching a seven-year high of 1.0% on an annual basis in May – the franc has also gained substantially against the euro lately, threatening to disrupt the progress in inflation. While dollar/franc has not moved much, given that Switzerland trades mostly with the EU, the franc’s value relative to the euro is much more important for price pressures. Another factor likely to keep the Bank cautious is that most of the improvement in inflation is owed to higher energy prices – not the healthy demand-driven rising prices officials would like to see. Core inflation that excludes volatile items like fresh food and energy, rose only 0.4% year-over-year in May.

Still-subdued core inflation combined with the latest gains in the franc will likely be enough to dissuade the SNB from appearing too optimistic on the economy. Even mentioning the words “normalization” or “hike” could lead to a sharp rally in the franc that undermines the Bank’s inflation-lifting efforts, so officials will probably avoid that route. Not to mention that the ECB – whose actions the SNB mostly mimics with a lag – just signaled it will not raise interest rates for at least another year, implying the SNB is highly unlikely to take any action over that timeframe either.

If the Bank exhibits no signs it is considering normalization, that would be a factor arguing for a weaker franc over time from a relative rates perspective, especially against currencies of nations that are normalizing their policy, like the US dollar. The key risk to this assessment would be another wave of risk aversion that causes the franc to attract safe-haven inflows, for instance, due to a further escalation in global trade tensions.

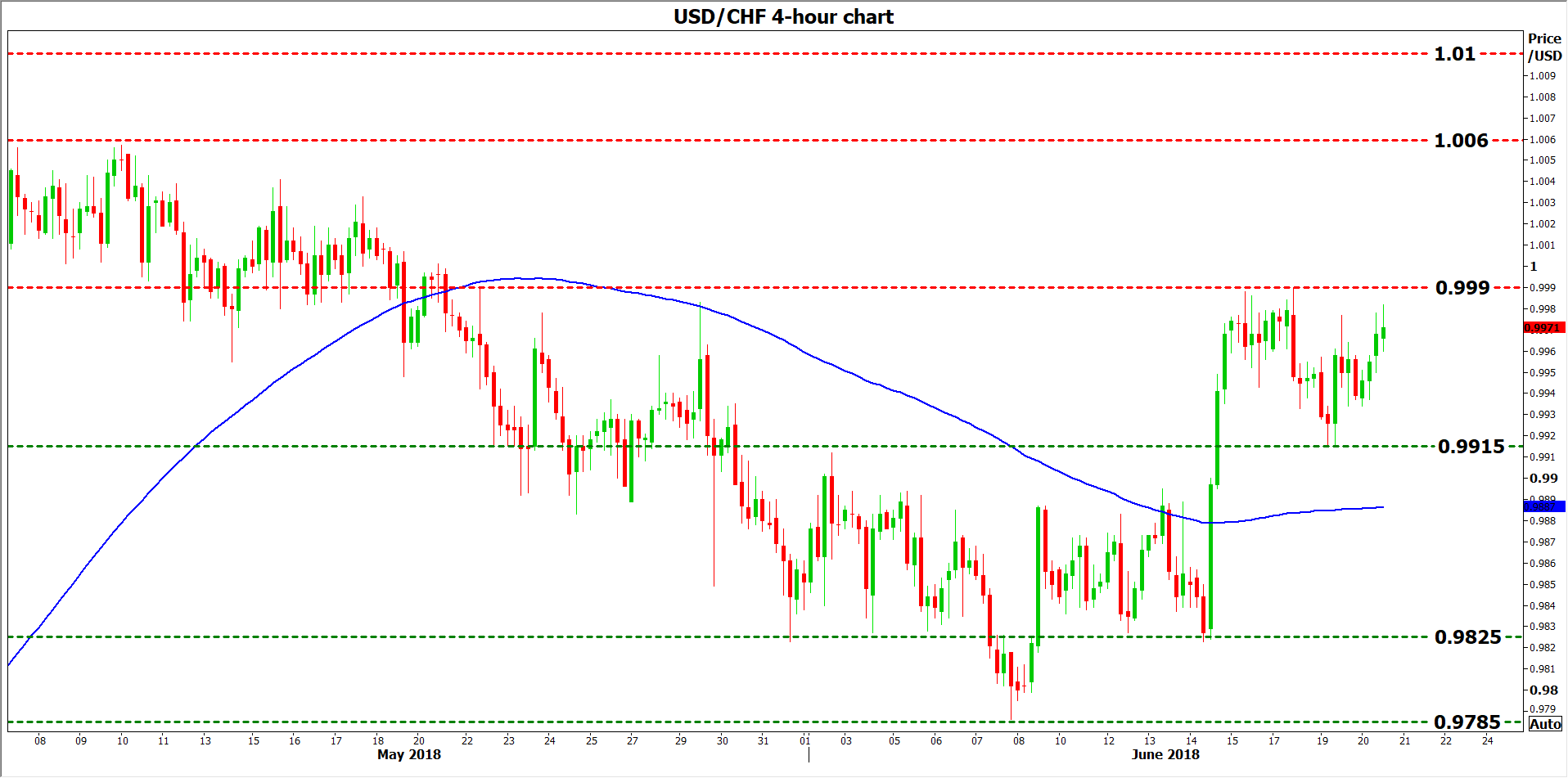

Technically, looking at dollar/franc, immediate resistance to advances may be found at the June 15 high of 0.9990. An upside break of that zone could aim for 1.0060, the peak from May 10. Even higher, the 1.0100 barrier would likely come into focus, defined by the top of 11 May 2017.

On the flipside – and in case the SNB surprises in a hawkish manner or risk-off developments increase the franc’s appeal – support to declines may come around 0.9915, the trough of June 19. If the bears overcome it, buy orders may be found near 0.9825 – a level which halted multiple declines in June. Lower still, the June 7 low of 0.9785 would increasingly attract attention.

USDCAD Breaks Above 1.33 As Trade War Fears Weigh On Loonie

The Canadian dollar is trading sideways in the Wednesday session. Currently, USD/CAD is trading at 1.3292, up 0.04% on the day. On the release front, there are Canadian events on the schedule. The U.S releases Existing Home Sales, which is expected to rise to 5.52 million. On Thursday, Canada releases ADP Nonfarm Employment Change and Wholesale Sales. The U.S will publish manufacturing and employment reports.

The Canadian currency continues to struggle, and is down 2.9% since June 11. Earlier on Wednesday, USD/CAD broke above the 1.33 line for the first time since June 2017. Investors are nervous over the escalating trade war between the U.S and China, and lower risk appetite could spell bad news for the Canadian dollar. The most recent round of the trade spat between China and the U.S started on Friday, when the U.S announced a 25 percent tariff on $50 billion in Chinese goods. After China responded with an identical move on U.S. imports, President Trump has now threatened to impose 10 percent tariffs on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate to this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that either side will blink first, the Canadian dollar could be sailing into nasty headwinds.

Canada is particularly vulnerable to protectionist moves south of the border, as some 80% of Canadian exports go to the United States. With President Trump making good on his threat to slap tariffs on his trading partners, the Canadian government is scrambling to protect the economy. Trump has said the U.S could impose tariffs of 25 percent on Canadian-built vehicles, which would be disastrous for the Canadian automotive sector, which is worth some C$80 billion to the economy every year. The Trudeau government has promised to help sectors hit with US tariffs, but bailing out the auto industry would cost billions. Canada may have to provide the U.S with more concessions in the NAFTA negotiations, in order to stave off tariffs against Canadian vehicles, which could have a disastrous effect on economic growth.

UK Brent Crude Oil – Speculations About The OPEC Meeting On Friday

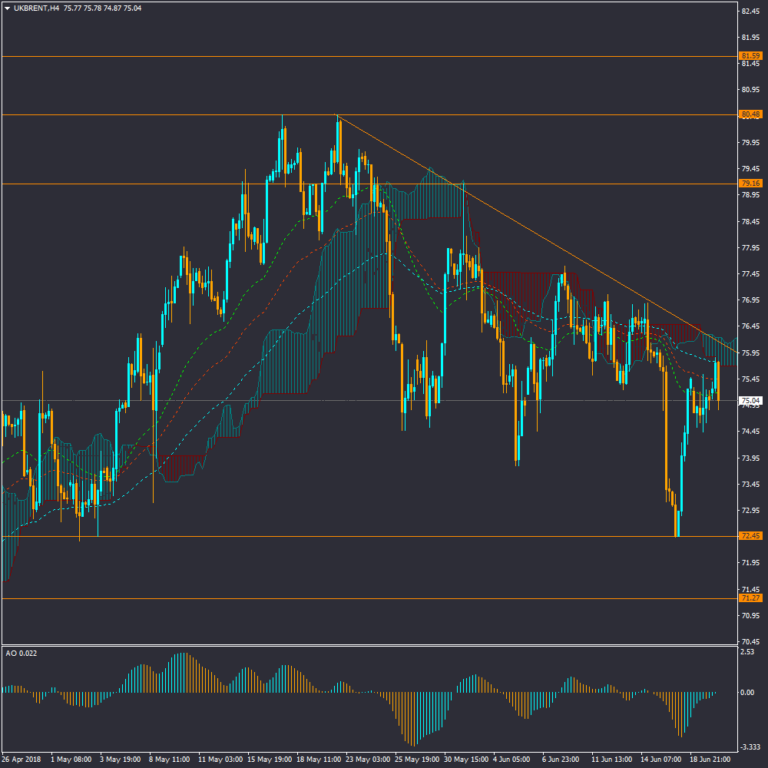

There are many speculations about the OPEC meeting on Friday in Austria. Saudi Arabia, the United Arab Emirates and Russia are pushing for an increase in OPEC production to Compensation the production deficit, whilst Iran, Iraq and Venezuela are opposed to this increase. The price of Crude Oil rose yesterday due to the opposition of the countries mentioned.

From a technical point, the price reached a bearish trend line mid-term and the price reaction will determine the trend to follow.

In addition, today, an announcement will be made for the changes in US crude oil inventories where a continuous decline is expected. This could increase demand for crude oil on international markets.

Support levels: 72.45, 71.27, 70.00

Resistance levels: 79.16, 80.48, 81.60

GBPUSD – All Eyes On The House Of Commons’ Vote On The Brexit

All eyes on the House of Commons' vote on the Brexit. If the majority opposes to this plan, this could reduce demand for the British pound.

Interest rates set by the Bank of England were expected to increase in August. The expectation is now lower, although the percentage still remains above 50%.

The price is expected to pass through a support level of 1.3204 and the probability will continue to rise in the short and mid-term.

Support levels: 1.3026, 1.3000, 1.2773

Resistance levels: 1.3472, 1.3711

EURUSD Back To The Support Level Range Of 1.1554 And 1.1510

During his speech yesterday, ECB Chairman Mario Draghi repeated the previous topic regarding expansionary policies and schedules. Market prices were not affected following the speech.

Today, Mr. Draghi and another three important Presidents of Central Banks will be delivering their speeches.

Meanwhile, the IFO published the estimated German economic growth rate at 1.8%, much lower than previous estimated rate of 2.6%.

Currently, the price is back to the support level range of 1.1554 and 1.1510. Following the short-term correction, it has returned to the bearish wave and a further short and mid-term decline is expected.

If the price crosses the supportive PRZ (Potential Reversal Zone), it will most likely lead to a bearish trend mid-term.

Support levels: 1.1554, 1.1510, 1.1445

Resistance levels: 1.1848, 1.2000

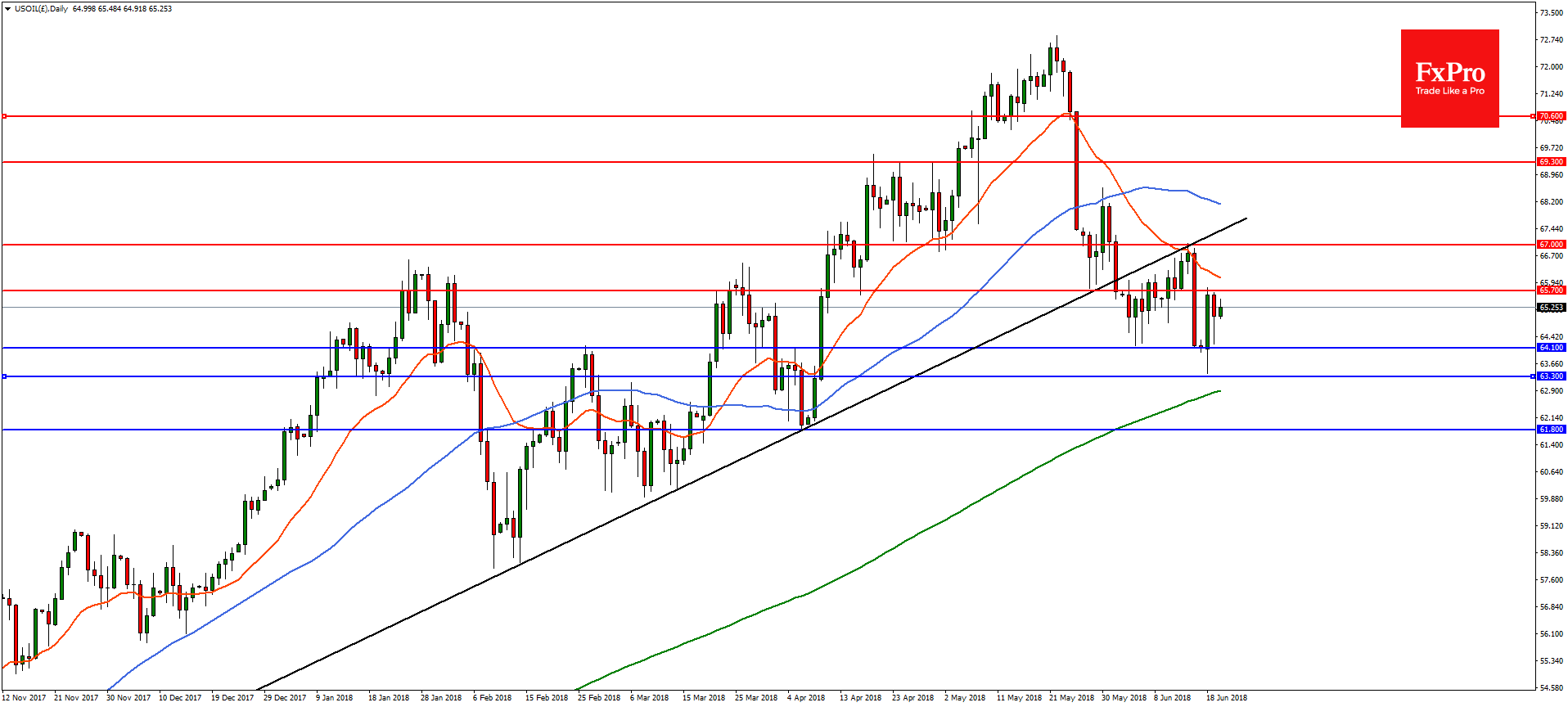

Forex Analysis: US WTI Oil

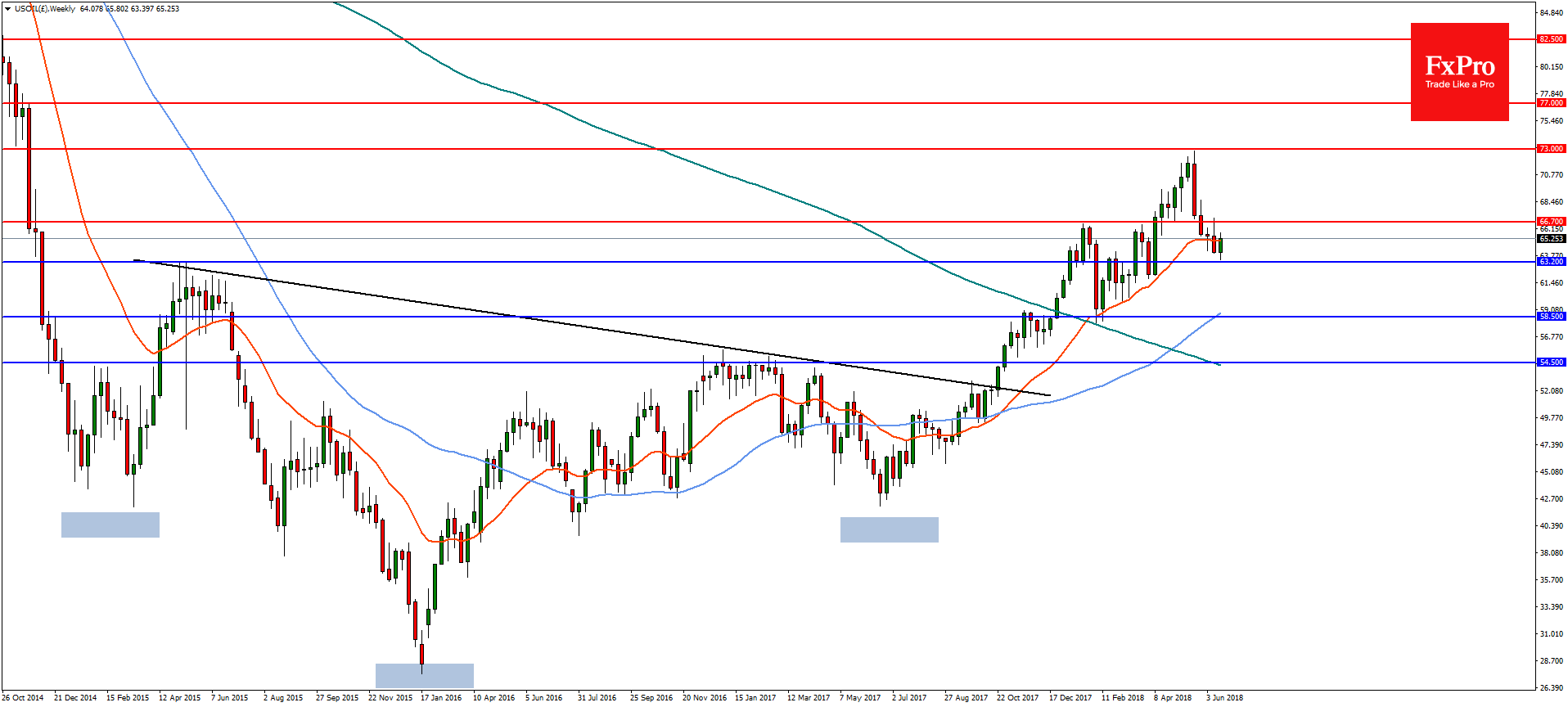

Crude oil is set to enter a volatile period with the start of the OPEC meeting in Vienna on Friday. Traders should also remain alert to market moving headlines ahead of the meeting as ministers from OPEC members are attending the OPEC international seminar and may give interviews to the media. Oil prices have been falling in recent weeks due to the possibility of OPEC agreeing to higher production. Additionally, President Trump has been applying pressure on OPEC to increase production to reduce oil prices but it is questionable that this a genuine request as the high prices support US shale oil production.

The API data on Wednesday reported a draw of 3.02 million barrels in US crude inventory for the week. Focus will now turn to inventory data reported by the Energy Information Administration (EIA) later today which is expected to show a draw of 2.43 million barrels.

On the weekly chart, WTI found resistance at the 73.00 level and has retraced back to horizontal support at 63.20. A weekly close above 66.70 is needed to open the way for WTI to continue to trend towards the inverted head and shoulders target at 82.50 with resistance at 73.00 and then the 61.8% Fibonacci at 77.00. However, a break of 63.20 would result in more downside with support at 58.50.

On the daily chart, the pullback in WTI found support at 64.10 ahead of OPEC. A break of the 23.6% retracement at 65.70 is needed for the upside to resume with resistance near the trend line at 67.00 and then at the 61.8% retracement level of 69.30. On the flip-side, a break of 64.10 could result is a downside move to support at 63.30 and then 61.80.

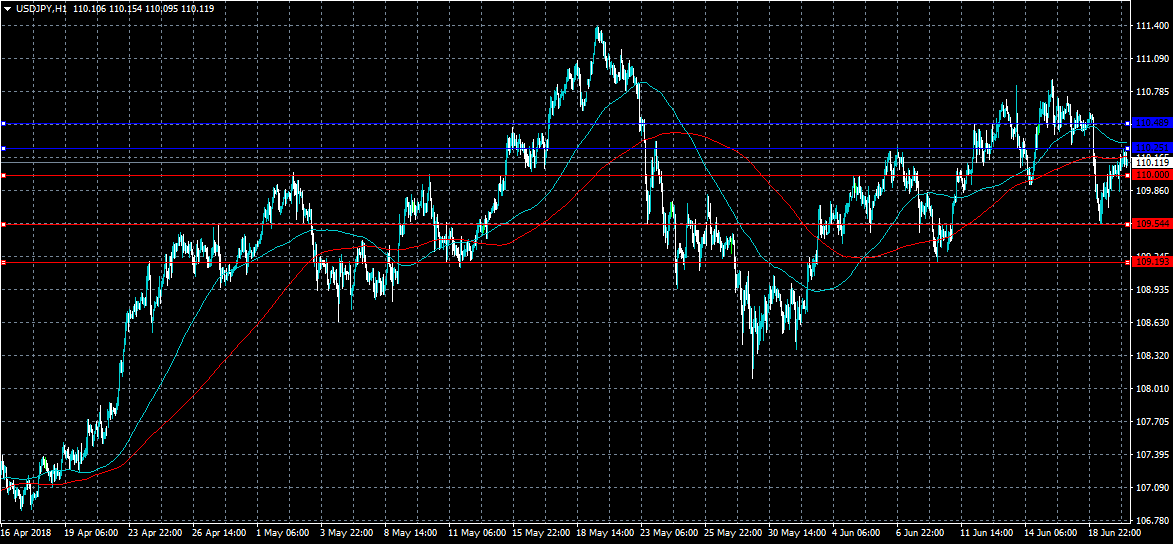

USDJPY Still Bearish Below 110.25

The US dollar has recovered above the 110.00 level against the Japanese yen currency after sellers failed to push price below the 109.54 support level. The USDJPY pair has so far found technical resistance from the 110.25 level, and currently price trades just above the key 110.00 level. The intraday sentiment surrounding the USDJPY pair remains bearish while price trades below the 110.25 level.

The USDJPY pair is intraday bearish while trading below the 110.25 level, futher losses towards the 109.54 and 109.19 levels seems likely.

If the USDJPY pair moves above the 110.25 level, buyers may test towards the 110.48 and 111.00 levels.

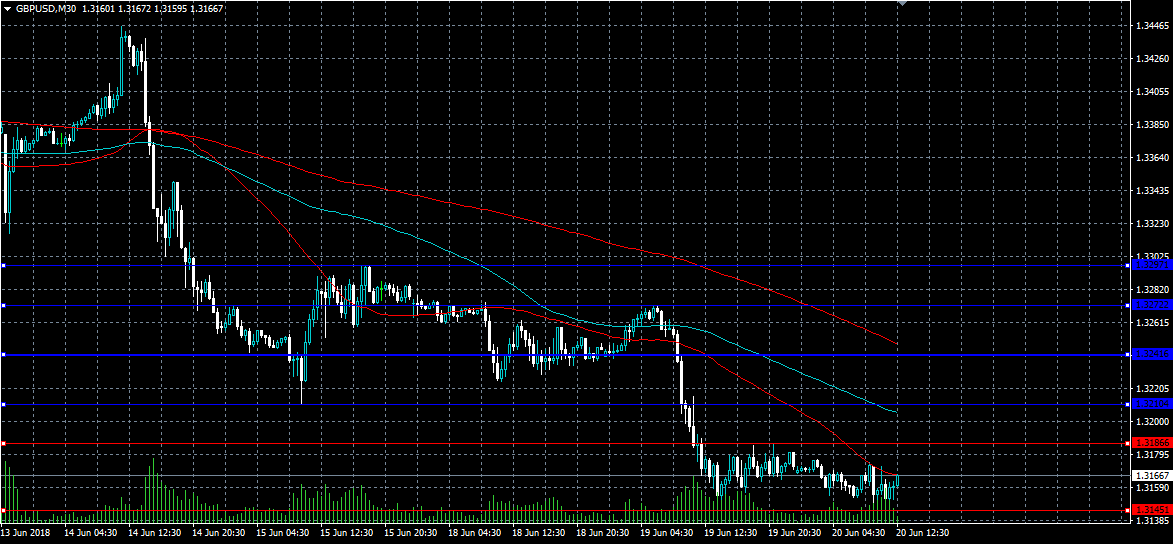

GBPUSD Further Bearish Below 1.3150

The British pound remains under heavy selling pressure against the US dollar, with the pair earlier hitting a new 2018 trading-low, at 1.3145, as political uncertainty in the United Kingdom continues to grow. The GBPUSD pair currently trades around the 1.3160 level, ahead of another key Brexit bill vote in the House of Commons later today. Sterling could come under heavy selling pressure later if the UK Conservative Party lose the key vote.

The GBPUSD pair is further bearish while trading below the 1.3150 level, key technical support is now located at the 1.3100 and 1.3062 levels

If the GBPUSD pair moves above the 1.3186 level, intraday technical resistance is found at the 1.3210 and 1.3241 levels.

Calm Trying To Reassert Itself In The Markets

Notes/Observations

- Calm trying to reassert itself into the markets. base case remains that the trade conflict with China would be settled before it progressed significantly

Asia:

- Bank of Japan (BoJ) April 26-27th Policy Meeting Minutes (2 meetings ago): Many agreed as there was still a long way to go to achieve the price stability target of 2%, it was necessary to maintain the current highly accommodative financial conditions

Europe:

- Franco-German agreement to establish a European fiscal authority; Merkel and Macron found "some common ground" about euro-area reform

- EU Chief Brexit Negotiator Barnier: Still serious divergence on protocols for Irish border in Brexit talks

- France stats agency INSEE raised its 2018 GDP from 1.6% to 1.7%, saw risks from protectionism and a stronger EUR

- Spain Debt Agency (Tesoro): ECB tapering of QE was a benign scenario for the Spanish bond market. Relative lack of turbulence after recent political uncertainty showed nation’s resilience

- Italy Debt Agency (Tesoro) official: Recent short-dated bonds volatility partly due to technical factors. To continue to issue bond market liquidity across all maturity lines

- Portugal Debt Agency (IGCP) chief Casalinho: Contagion has subsided since euro zone debt crisis peak

- PM May stated that could fund her NHS promise without breaking election manifesto pledges by only imposing new taxes after 2022

Energy:

- Weekly API Oil Inventories: Crude: -3M v +0.8M prior

Economic Data:

- (DE) Germany May PPI M/M: 0.5% v 0.4%e; Y/Y: 2.7% v 2.5%e

- (JP) Japan May Convenience Store Sales Y/Y: -1.2% v +0.7% prior

- (SE) Sweden Jun Consumer Confidence: 96.8 v 100.0e; Manufacturing Confidence: 116.1 v 116.0e, Economic Tendency Survey: 108.7 v 108.6 prior

- (TH) Thailand Central Bank (BOT) left its Benchmark Interest Rate unchanged at 1.50%, as expected

- (ZA) South Africa May CPI M/M: 0.2% v 0.4%e; Y/Y: 4.4% v 4.6%e

- (ZA) South Africa May CPI Core M/M: 0.0% v 0.2%e; Y/Y: 4.4% v 4.5%e

- (PH) Philippines Central Bank (BSP) raised its Overnight Borrowing Rate by 25bps to 3.50% (as expected)

Fixed Income Issuance:

- (DK)Denmark sold total DKK2.36B in 2020 and 2027 DGB bonds

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

- (SE) Sweden sold SEK5.0B vs. SEK5.0B indicated in 6-month Bills; Avg Yield: -0.8391% v -0.8233%prior; bid-to-cover: 1.91x v 1.57x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.7% at 386.0, FTSE +1.1% at 7687, DAX +0.4% at 12729, CAC-40 +0.3% at 5406, IBEX-35 +1.0% at 9854, FTSE MIB +0.8% at 22270, SMI +0.9% at 8536, S&P 500 Futures +0.3%]

- Market Focal Points/Key Themes: European Indices rebound from recent weakness with the FTSE 100 outperforming once again, trading over 1% higher, while the Dax and the CAC underperform. On the earnings front Berkeley Group trades lower after guiding FY19 profits lower; DSM trades lower after announces new targets to 2021. In the M&A space Recordati trades higher after interest in its pharma unit from CVC, Ceconomy rebounds after acquiring 15% of M.Video, while Engie remains little changed after divesting its stake in Glow for €2.6B. Elsewhere Maersk trades higher after naming former Assa Abloy CFO its new CFO, Remy Cointreau trades lower after an analyst downgrade. Looking ahead notable earner include Winnebago and Actuant.

Movers

- Consumer Discretionary Ceconomy [CEC.DE] +4.2% (Acquires 15% of M.Video, cuts outlook), Remy Cointreau [RCO.FR] -3.1% (Analyst downgrade)

- Industrials Maersk [MAERSKB] +2.5% (New CFO) -Materials BHP [BLT.UK] +1.9% (Private equity firm EMR Capital to acquire Cerro Colorado copper mine in Chile for $230M), DSM [DSM.NL] -2.4% (Sets new financial targets)

- Healthcare [Pihlajalinna [PIHLIS.FI] -6.7% (Cuts outlook), Recordati [REC.IT] +3.2% (CVC said to be in discussions over stake in pharma unit)

- Real Estate [Berkeley Group [BKG.UK] -4.4% (Earnings)

Speakers

- ECB’s Villeroy (France): Net asset purchases should end by Dec with 1st rate hike seen in summer 2019 (in-line with Draghi post rate decision press conference). Monetary policy to remain accommodative. Domestic growth within France remained good, should see unemployment rate fall during the year

- ECB’s Nowotny (Austria) stated that he saw the Euro depreciating against the USD due to differences on FED-ECB policies

- France Fin Min Le Maire stated that the govt to maintain its 2018 GDP growth forecast at 1.8%, no extra spending cuts seen this year

- Leading pro-EU Tory lawmaker Grieve: To vote against the Govt unless a deal is reached on the meaningful vote

- Sweden Think Tank NIER Economic Forecastscut its 2018 GDP from 2.8% to 2.4% and 2019 GDP from 2.1% to 1.9%. Raised 2018 CPIF from 1.8% to 2.0% and 2019 CPIF from 1.8% to 2.0%. It saw the 1st potential rate hike by Riksbank in spring 2019

- German CSU's Soeder (Prime Minister of Bavaria): Skeptical of Euro proposals made between Chancellor Merkel and France President Macron

- EU said to be on course to complete a pre Brexit UK tax probe this year; which could see UK companies face a tax bill above £1B

- BOJ Dep Gov Amamiya stated that high possibility that strong global growth to continue. Saw improvement in household spending; FY20 growth in Japan could slow on sales tax effect and Capex slowdown

- Thailand Central Bank Policy Statement noted that the vote to keep policy steady was 5-1 (dissenter sought a 25bps hike to 1.75%) . Monetary policy should stay accommodative

- Philippines Central Bank ( Policy Statement reiterated its support for carefully coordinated efforts. Inflation expectations remained elevated with upside risk related to wages and fare hike petition. Inflation to be above target in 2018 and move back within the range in 2019. Govt to implement non-monetary measures to curb CPI

- China Foreign Ministry official reiterated view that prefered dialogue to resolve trade disputes

- Various Oil and Energy officials comment ahead of the OPEC and OPEC+ meetings

- Saudi Crown Prince stated that the oil market fundamentals remained healthy. OPEC to discuss bring more supply to the market

- Russia First Dep Energy Min Teksler: Russia maintained its position for an oil production increase but was ready to discuss any OPEC + proposal. Did expect an agreement in Vienna this week

- Oman Oil Min stated that saw a consensus forming at the Jun 22nd OPEC meeting

Currencies

- FX markets remained aware of potential volatility but for the time being a sense of calm was trying to reassert itself into the markets. Most analysts still believed that their base case scenario remained that the trade conflict with China would be settled before it progressed significantly.

- The USD/JPY was back above the 110 handle with the Nikkei closing higher by over 1%.

- EUR/USD remained below the 1.16 level. Comments on policy divergence by ECB’s Nowotny kept the Euro on the defensive as he saw that he saw the Euro depreciating against the USD due to differences on FED-ECB policies

- GBP/USD was steady in the mid-1.31 area ahead of the House of Commons debate and vote on the "meaningful vote” on Brexit. It appears that PM May has enough voted to ward off any attempt by the Tory rebels to defeat her on this amendment.

Fixed Income

- Bund Futures trade 12 ticks lower at 161.38 as risk assets stabilize. Upside targets 162.25 followed by 162.75, while a return lower targets the 158.75 level.

- Gilt futures trade at 122.90 lower by 12 ticks following the move from US Treasuries. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Wednesday's liquidity report showed Monday's excess liquidity fell from €1.849T to €1.845T. Use of the marginal lending facility fell from €116M to €97M.

- Corporate issuance saw Oneok raise $1.3B in the primary market

Looking Ahead

- (BR) Brazil Jun CNI Industrial Confidence: No est v 55.5 prior

- 05:30 (DE) Germany to sell €1.5 B in 2.5% July 2044 Bunds

- 05:30 (UK DMO to sell £1.25B in new 0.125% Aug 2028 Inflation-links Gilts

- 05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.25B in 3-month and 12-month Bills

- 05:45 (NL) ECB’s Knot (Netherlands) in Amsterdam

- 06:00 (UK) Jun CBI Industrial Trends Total Orders: +2e v -3 prior; Selling Prices: No est v 19 prior

- 06:00 (IL) Israel Apr Manufacturing Production M/M: No est v 0.3% prior

- 06:00 (PT) Portugal Monthly Economy Survey

- 06:00 (CZ) Czech Republic to sell 2028 and 2033 Bonds

- 06:30 (FR) ECB's Coeure (France) chairing a panel in Sintra, Portugal

- 06:45 (US) Daily Libor Fixing

- 07:00 (US) MBA Mortgage Applications w/e Jun 15th: No est v -1.5% prior

- 07:00 (RU) Russia to sell RUB10B in Nov 2022 Floating-rate OFZ bonds

- 08:00 (UK) House of Commons likely to begin debate on "meaningful vote"

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Q1 Current Account: -$129.0Be v -$128.2B prior

- 09:00 (BE) Belgium Jun Consumer Confidence: No est v 0 prior

- 09:00 (MX) Mexico Q1 Aggregate Supply and Demand: 2.4%e v 3.0% prior

- 09:00 (RU) Russia May Unemployment Rate: 4.9%e v 4.9% prior; Real Disposable Income Y/Y: 5.0%e v 5.7% prior; Real Wages Y/Y: 7.5%e v 7.8% prior

- 09:00 (RU) Russia May Real Retail Sales Y/Y: 2.3%e v 2.4% prior

- 09:30 (EU) ECB chief Draghi, RBA Gov Lowe and Fed Chair Powell speak in Sintra, Portugal

- 09:30 (UK) House of Commons potential vote if Parliament should have a "meaningful vote"

- 10:00 (US) May Existing Home Sales: 5.52Me v 5.45M prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:00 (CO) Colombia Apr Trade Balance: -$0.4Be v -$0.4B prior; Total Imports: $4.3Be v $3.9BV prior

- 12:00 (CA) Canada to sell 10-year notes

- 15:00 (MX) Mexico Citibanamex Survey of Economists

- (BR) Brazil Central Bank (BCB) Interest Rate Decision: Expected to leave Selic Target Rate unchanged at 6.50% (no set time)

DAX Stops Slide – The Lull Before The Storm?

The DAX index has posted gains in the Wednesday session. Currently, the DAX is at 12,740, up 0.44% since the Tuesday close. On the release front, there are no major German or eurozone indicators. German PPI remained steady at 0.5%, edging above the estimate of 0.4%. The ECB Forum continues on Wednesday, with ECB head Mario Draghi and Fed chair and Jerome Powell participating in a panel discussion. On Thursday, the eurozone releases consumer confidence.

After a dismal start to the week, the DAX has steadied, and the reversal could be linked to a calm message from Mario Draghi, who opened the ECB forum on Tuesday. Draghi counseled patience regarding the bank’s interest rate policy. Last week, the ECB announced last week that it was winding up its asset-purchase plan by the end of the year, but added that it would not raise interest rates before next summer. This dovish message sent the euro sharply lower. Draghi said that the ECB will be “patient in determining the timing of the first rate rise”. Draghi also made reference to inflation, saying that “inflation expectations remain well anchored”. However, analysts were quick to note that eurozone inflation has fallen short of the bank’s target of just below 2 percent for five years. Draghi acknowledged that there were external factors which could weigh on inflation, including the threat of global protectionism and higher oil prices. There is also the vexing problem that higher wages have failed to translate into increased inflation. Draghi would like to get through the European Forum without shaking up the fragile equity markets and so far he has succeeded.

Investors remain wary this week, as the trade war rhetoric between the United States and China continues to escalate. On Tuesday, the DAX fell to its lowest level since May 31. The trouble started on Friday, when the U.S announced a 25 percent tariff on $50 billion in Chinese goods. After China responded with an identical move on U.S. imports, President Trump threatened to impose 10 percent tariffs on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate against this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that any side will blink first, the markets should be preparing for stormy weather ahead. It will be interesting to see if central bank heads Draghi and Powell address the tariff spat on Wednesday at the ECB Forum.