Sample Category Title

Will The BoE Lay The Groundwork For August Hike?

Was recent data enough to ease concerns about first quarter downturn?

The Bank of England meeting on Thursday should be another interesting affair following a week in which two other major central banks – the Federal Reserve and ECB – have announced new tightening measures.

- No rate hike expected this month

- Markets still not convinced about August

- Sterling could respond positively to hike clues

The BoE was close to doing the same in May and had it not been for a slowdown in the first quarter, it may well have raised interest rates by 25 basis points, taking them above 0.5% for the first time since March 2009.

Instead, the Monetary Policy Committee opted to wait for evidence that the downturn in the first quarter was in fact temporary and not the start of a more worrying trend. The fact that inflation has fallen back to more palatable levels also gave them the freedom to do so.

Will we see a rate hike on Thursday?

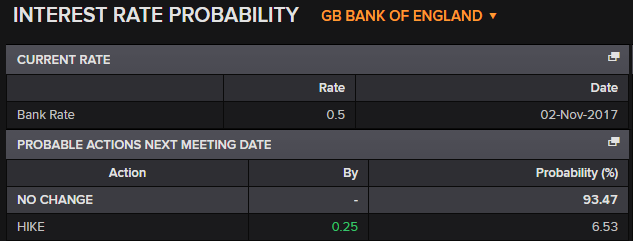

While we shouldn’t write off the possibility of a rate hike this month, it looks extremely unlikely and with markets only pricing in a 6% probability of an increase, investors would appear to agree.

There hasn’t been sufficient evidence yet that the downturn in the first quarter was a blip. The recent retail sales data was encouraging and there has been some improvement in the PMI surveys which provides hope but I’m not convinced that will be enough.

There’s also no press conference or new economic projections accompanying this decision which at this stage of the tightening cycle I think policy makers would prefer.

The central bank has also been heavily criticized for misleading investors, so to raise interest rates without warning would just invite more criticism and raise questions over the banks forward guidance, or lack of.

Finally, with Brexit negotiations at such a critical stage, it would seem an odd time to be hiking interest rates. Later in the year when we have more clarity would surely be more suitable.

What does all of this mean for sterling?

With a rate hike almost entirely priced out, it would come as a major shock if the central bank decided to pull the trigger, something I expect would send the pound sharply higher.

Assuming this doesn’t happen, traders will be looking for more subtle clues about when we can expect the next rate hike with the next meeting in August being one of those that does include new economic projections and a press conference, otherwise known as Super Thursday.

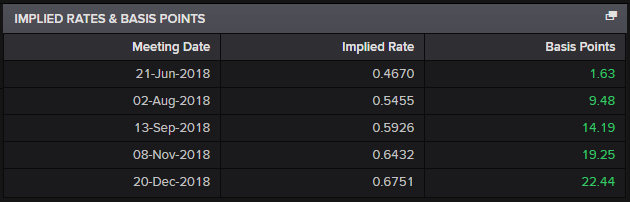

With the markets currently pricing in only a small chance – roughly 40% – of a hike in August, this may be where the potential for surprise lies. A strong signal that the central bank is going to push ahead with a hike at the next meeting – either in an accompanying statement or with more policy makers voting for a hike – could also be bullish for the pound.

Gold Steady As Markets Brace For Next Salvo In Trade War

Gold has inched lower on the Wednesday session. In North American trade, the spot price for one ounce of gold is $1274.11, down 0.06% on the day. On the release front, the U.S current account deficit narrowed to $124 billion, beating the forecast of $129 billion. As well, Existing Home Sales dropped to a 3-month low. The reading of 5.43 million was well shy of the estimate of 5.52 million. On Thursday, the U.S releases manufacturing and employment reports.

In times of crisis, nervous investors often turn to gold, a safe-haven asset. However, since the start of the new round of tit-for tat tariffs between China and the U.S began on Friday, gold has defied expectations and lost ground. The base metal has declined 2.2% since Friday, as the U.S dollar has flexed is muscles against gold as well as other major currencies.

Investor risk appetite has waned this week, as the nasty trade war rhetoric between the United States and China continues to worsen. There are growing fears of a global trade war, which would take a toll on the global economy and could trigger a worldwide recession. The most recent round of the trade spat between China and the U.S started on Friday, when the U.S announced a 25 percent tariff on $50 billion in Chinese goods. After China responded with an identical move on U.S. imports, President Trump shook up the markets after he threatened to impose a 10 percent tariff on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate to this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that either side will blink first, traders should be prepared for further volatility in the markets.

Eco Data 6/21/18

[php_everywhere instance="1"]

US Crude Inventory Fell More Than Expected, All Eyes on OPEC Meeting This Friday

Crude oil prices recovered US inventory fell more than expected. The focus this week is undoubtedly the OPEC meeting in Vienna on June 22-23. the cartel members, together with some non-OPEC producers, would discuss the possibility of raising output. A Bloomberg report suggests that the producers are considering an increase in output by 0.3M- 0.6M bpd. Yet, Iran, Iraq and Venezuela signal that they might veto the proposal.

EIA Weekly Inventory Report

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks climbed +0.19 mmb to 1208.16 mmb in the week ended June 15. Crude oil inventory fell -5.91 mmb (consensus: -1.9 mmb) to 426.53 mmb, as inventories decreased in ALL PADDs. PADD II saw inventory draw of -4.17 mmb Cushing stock slipped -1.3 mmb to 32.62 mmb. Utilization rate added +1% to 96.7%. Meanwhile, crude production steadied at 10.9M bpd for the week.

Refined oil product inventories rose further. Gasoline inventory soared +3.28 mmb to 240.04 mmb as demand plunged -5.6% to 9.33M bpd. The market had anticipated a +0.19 mmb increase in stockpile. Production fell -3.37% to 10.1M bpd while imports rose +3.16% to 0.85M bpd during the week.

Distillate inventory increased +2.72 mmb to 117.41 mmb. The market had anticipated a -0.16 mmb drop. This came in as a result of a -13.15% decline in demand to 3.83M bpd. Production gained +6.99% to 5.47M bpd while imports slumped -52.9% to 0.05M bpd during the week.

Released after market close on Tuesday, the industry- sponsored API estimated that crude oil inventory dropped -1.9 mmb during the week. For refined oil products, gasoline stockpile rose +2.11 mmb while distillate added -0.75 mmb.

British Pound Breaks Slide, BoE Rate Announcement Next

The British pound is almost unchanged in the Wednesday session. In North American trade, GBP/USD is trading at 1.3180, up 0.05% on the day. On the release front, British CBI Industrial Order Expectations sparkled, with a reading of 13 points. This easily beat the forecast of 1 point. On the release front, the U.S current account deficit narrowed to $124 billion, beating the forecast of $129 billion. As well, Existing Home Sales dropped to a 3-month low. The reading of 5.43 million was well shy of the estimate of 5.52 million. On Thursday, the BoE holds a policy meeting and is expected to maintain the benchmark rate at 0.50%. The U.S will release manufacturing and employment reports.

The worsening trade spat between the United States and China has boosted the U.S dollar, at the expense of the British pound and other major currencies. The pound is currently trading at its lowest level since early November. The most recent round of the trade spat between China and the U.S started on Friday, when the U.S announced a 25 percent tariff on $50 billion in Chinese goods. After China responded with an identical move on U.S. imports, President Trump has now threatened to impose 10 percent tariffs on some $200 billion in Chinese goods. Not surprisingly, China has threatened to retaliate against this latest move. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. With the first of the U.S tariffs scheduled to take effect on July 6 and no signs that either side will blink first, the pound could continue to lose ground.

Negotiations between the European Union and the U.K are deadlocked, as the sides remain far apart on a number of key issues. The Europeans are exasperated by the lack of direction from the May government and are in no mood to show flexibility as Britain prepares to leave the club. Key outstanding issues remain the Irish border, the role of the European Court of Justice on EU citizens living in Britain, and the nature of trade relations between Britain and EU members in the post-Brexit era. Both sides are preparing for the possibility that a deal will not be reached by March 2019. The scenario of a ‘hard Brexit’ could sour investor sentiment towards the U.K and put pressure on the struggling British pound.

Only “Trump Risk” Left to Lift the Yen

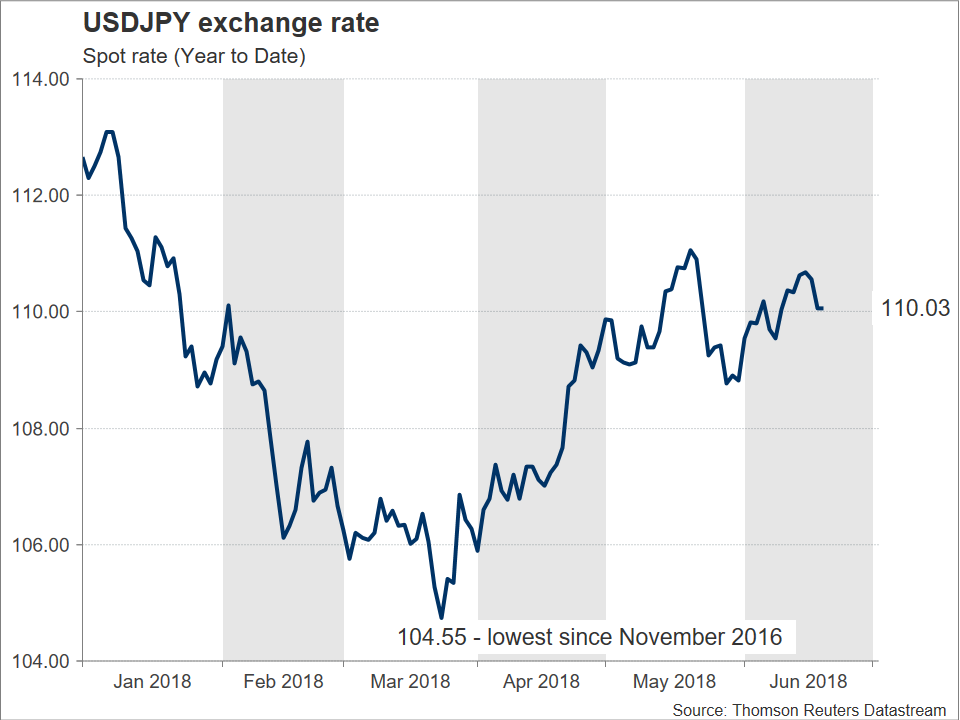

The yen appreciated by 3.9% versus the US currency in 2017, which marked the worst year for the greenback since 2003. During the first few months of the current year, the Japanese currency managed to build on last year’s positive momentum, in part due to rising market expectations for a Bank of Japan that is getting closer to normalizing policy. Indicatively, the dollar/yen pair touched its lowest since late 2016 of 104.55 on March 26. However, as we’re approaching the end of Q2 the BoJ normalization story has lost steam. Instead, it seems as if only safe-haven flows can prevent a rally in USDJPY.

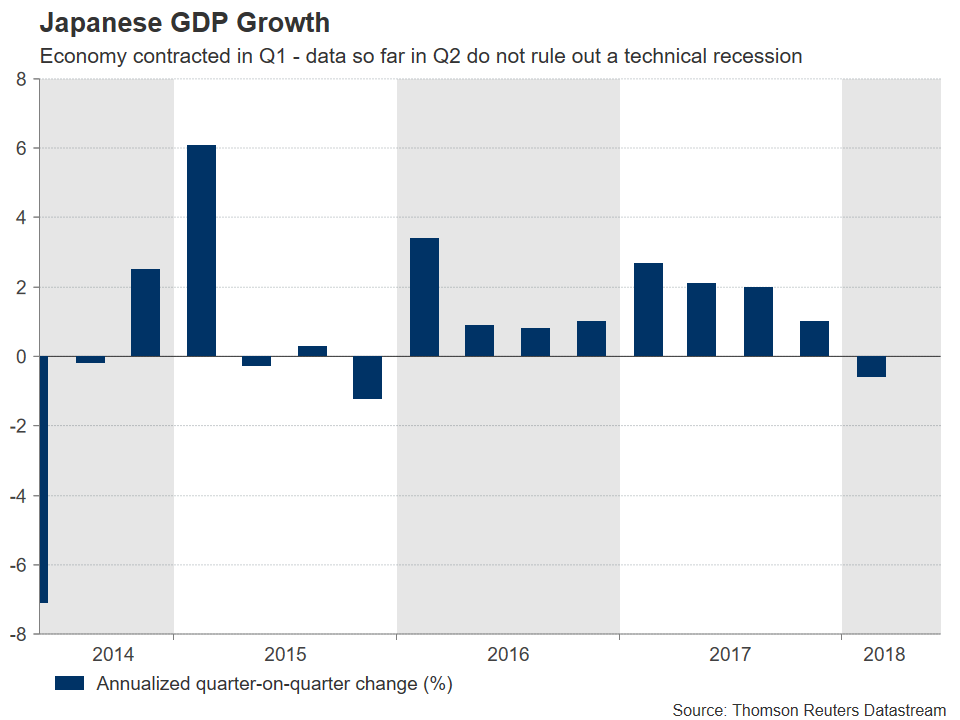

As of late June, then yen remains the only major currency that is decisively trading in the green in 2018 against the dollar (the Norwegian krone is only marginally up versus the US currency during the same period). Specifically, at 110.03, dollar/yen is down by 2.3% year-to-date. However, and as evidenced by the chart below, the pair has been in an uptrend for almost the whole of Q2 and there are numerous factors supporting the view for a continuation of the trend in place.

Firstly, economic fundamentals as reflected by recent data releases are not painting a rosy picture for the Japanese economy. After economic activity contracted in Q1, April’s industrial output and household spending numbers came in well short of analysts’ forecasts, with the latter recording its third straight month of negative growth in April. On the bright side, machinery orders strongly rebounded during the same month. Overall though, the figures out of Japan are such that they are not ruling out a technical recession – defined as two consecutive quarters of GDP contraction – in Q2.

Contrast the above with the situation in the US and the greenback emerges as the likely “victor” versus the yen: US releases feeding into GDP forecasting models are putting growth in the world’s largest economy at the 4-handle on an annualized basis during Q2, the highest pace since 2014. In particular, one such estimate derived by the Atlanta Fed’s GDPNow model, places the annual rate of expansion in Q2 at 4.7%.

Turning to monetary policy, in late 2017 – early 2018, the BoJ normalization story appeared so engrained in traders’ minds that they were much more willing to short the dollar/yen pair on the back of any hawkish-perceived comments by BoJ Governor Haruhiko Kuroda, compared to going long on remarks that cast doubt on monetary policy tightening expectations, pushing them way back into the future.

Fast forward to the present: market participants seem to have come to terms with a Japanese central bank that will remain ultra-accommodative for the foreseeable future; easing inflationary pressures have also contributed to this “cause”. Attesting to this is the fact that despite the BoJ once again reducing the amount of Japanese government bonds (JGBs) it will purchase as part of its operations in June, the markets are largely shying away from viewing this as tapering as they have in the past. Instead, they see it for what it is: achieving the BoJ’s target of a yield of around zero percent on 10-year JGBs happens to require the purchase of fewer bonds.

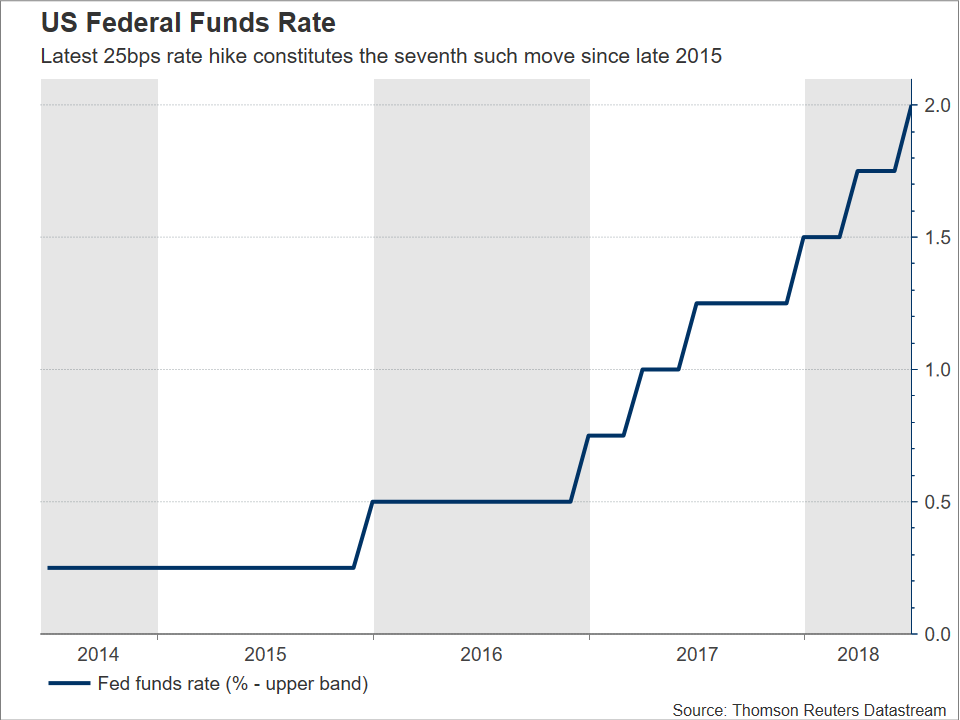

Again, contrast with the US: the Federal Reserve remains firmly on a path of policy normalization, having recently delivered its seventh quarter percentage point interest rate increase since it started hiking rates in late 2015. Meanwhile, the meeting concluding on June 13 saw FOMC policymakers tilting hawkish by revising their rate-path projections for 2018 to signal four rate increases in total, from three previously. Putting everything together, in the absence of a market shock, peak policy divergence between the US and Japan, translating into higher yield differentials and favoring a stronger USDJPY, has yet to materialize.

Case closed then? Should the growth trajectories of Japan and the US, as well as monetary policy divergence (of course the two are directly related), allow us to safely predict a dollar/yen that will be on the rise as the year unfolds? Yes and (partially) no: this is where “Trump risk” gets into the equation and complicates matters.

Japan is the world’s biggest creditor nation and there is a broadly held assumption that Japanese investors will repatriate funds in case of a crisis. This renders the yen a safe-haven harbor, gaining at times of heightened uncertainty. The US-China trade relationship has been put to the test numerous times over the course of the year, with the Japanese currency rising whenever Sino-US tensions intensified. The latest threat from US President Donald Trump for tariffs on an additional $200 billion of Chinese goods imported in the US is pushing the world’s two largest economies closer to a trade war.

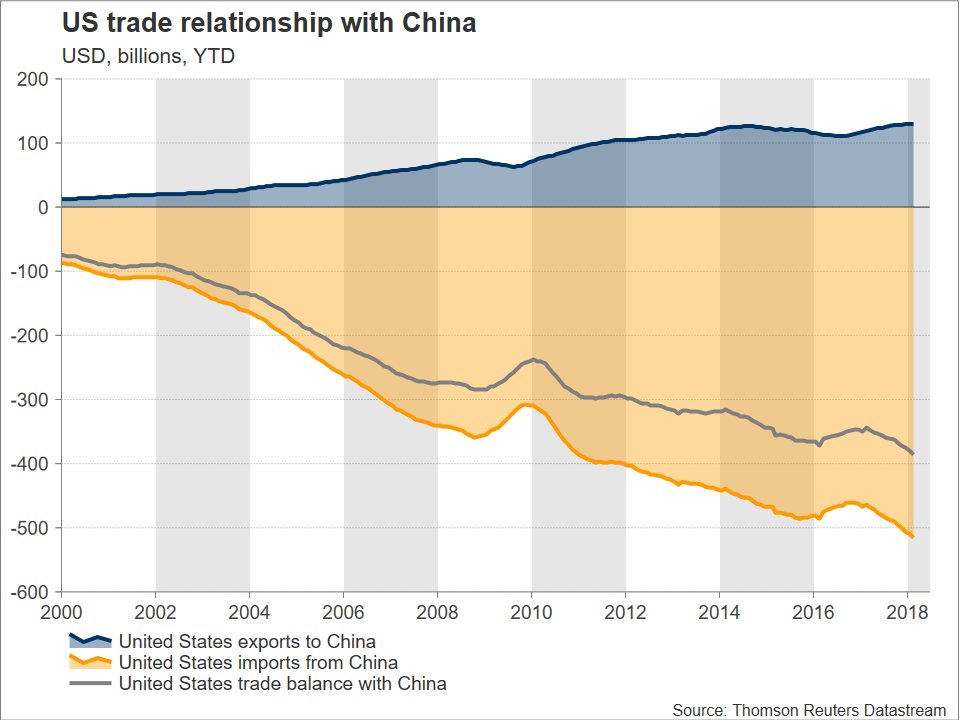

It has long been argued that the aforementioned trade spat does not have much room to run. The Trump administration’s rhetoric was seen as merely a negotiating tactic to generate leverage ahead of talks, and China’s disadvantage of having far more to lose in case of increased barriers to trade (see chart below), were enough to ease concerns over a trade war.

However, the US keeps on exerting pressure on China, and the latter – much to the surprise of many market commentators – responds in retaliatory fashion, at least up to now. A tit-for-tat escalation that will drive the situation out of hand is anticipated to lend support to the yen, driving dollar/yen even lower.

Overall on trade, it is clear that the risk for a full-blown trade war has dramatically risen lately. Despite this, given that such an outcome would be a “lose-lose” situation from an economic standpoint for China and the US, it remains an unlikely – tail risk – event.

Taking everything into account, and under a base case scenario that does not see a trade war materializing, if a projection for dollar/yen were to be made spanning until the end of Q3, then it would be one for an elevated pair. A dollar/yen piercing through the 112 handle, coming close to neutral year to date, should not be ruled out.

Japanese Yen Trading Sideways after BoJ Minutes

The Japanese yen has inched higher in the Wednesday session. In the North American trade, USD/JPY is trading at 110.17, up 0.10% on the day. On the release front, Japan released the minutes of the April policy meeting. At the ECB Forum in Sintra, the heads of the Federal Reserve and Bank of Japan will participate in a panel. In economic news, the U.S current account deficit narrowed to $124 billion, beating the forecast of $129 billion. On the housing front, Existing Home Sales dropped to a 3-month low. The reading of 5.43 million was well shy of the estimate of 5.52 million.

There were no surprises from the minutes of the Bank of Japan’s April policy meeting. At the meeting, policymakers maintained interest rates at -0.10%. As well, the bank also dropped the timeframe for achieving its inflation target of 2 percent, a signal that the bank has no plans to increase stimulus. The minutes indicated that most members wanted to maintain current monetary policy, holding rates at -0.10% and the 10-year bond yield around zero percent. BoJ policymakers appear resigned to the fact that the inflation target will not be reached anytime soon, but the BoJ nevertheless is sticking to its 2 percent target.

Investor risk appetite has waned this week, as the nasty trade war rhetoric between the United States and Japan continues to worsen. There are growing fears of a global trade war, which would take a toll on the global economy and could trigger a worldwide recession. On Tuesday, President Trump raised the stakes and threatened to impose a 10 percent tariff on some $200 billion in Chinese goods. Trump has vowed to take action on the $375 billion trade deficit that the U.S has with China, claiming that the latter is guilty of unfair trade practices. The Japanese economy relies heavily on exports, and a rash of tariffs would likely hamper the country’s economy. Although the yen is a safe-haven currency, the latest tariff tussle has seen investors flock to the U.S dollar rather than the Japanese yen.

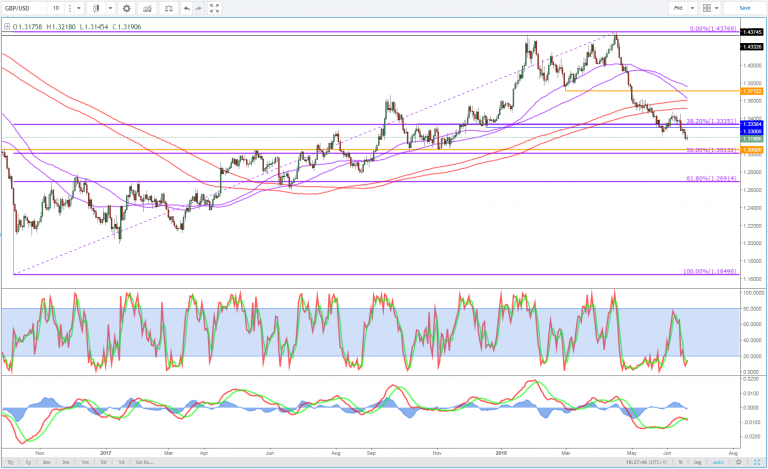

GBPUSD: Broader Bias Remains Lower

GBPUSD - The pair faces further price weakness despite its present price hesitation. Support lies at the 1.3150 level where a break will turn attention to the 1.3100 level. Further down, support lies at the 1.3050 level. Below here will set the stage for more weakness towards the 1.3000 level. Conversely, resistance stands at the 1.3250 levels with a turn above here allowing more strength to build up towards the 1.3300 level. Further out, resistance resides at the 1.3350 level followed by the 1.3400 level. On the whole, GBPUSD remains biased to downside.

Sunset Market Commentary

Markets:

Over the previous days, core US and German bonds were modestly supported by safe haven flows as the trade conflict dominated the market headlines. Today, sentiment on risk improved, but it had no big (negative) impact on core bonds. Changes in US and European bond yields are mostly less than 1 bp. There was some intraday noise on comments from several ECB members. However, in the end, there was no good reason for markets to questions ECB Drahgi’s commitment at last week’s policy meeting to keep policy rates unchanged at least through the Summer of next year. In the same context, Fed president Powell at the Sintra conference repeated that the case for gradual Fed rate hikes is strong. The direct impact on US Treasuries stays limited. 10-y yield spreads changes versus Germany also hardly changed on a daily basis. Italy slightly outperforms (-2 bp).

EUR/USD. Today, sentiment on risk improved and global equities reversed part of this week’s losses. The euro was also a prominent ‘victim’ of the trade tensions, but doesn’t show any strong rebound momentum yet. Soft comments from ECB governors (at the Sintra ECB conference and elsewhere), were at least partially to blame. Remarkably, ECB’s Nowotny explicitly mentioned the (potential) negative impact from the divergent Fed-ECB policy as a driver for EUR/USD weakness. The headlines pushed EUR/USD briefly below the 1.1550 handle. However, with a better global risk sentiment; it was not enough to push EUR/USD for a test of the 1.1510 support area. EUR/USD settled in the upper half of the 1.15 big figure for the remainder of the session. USD/JPY also rebounded north of 110, but this move was not really convincing as well, despite the rebound in global equities. The lack of any meaningful rise in core US & Germany yields probably deprived USD/JPY (and EUR/JPY) of additional interest rate support.

Today, sterling traders were more or less obliged to take a wait-and-see approach ahead of a key vote on the ‘meaningful vote amendment’ in the House of Commons. EUR/GBP tested the 0.88 barrier this morning and then settled in a tight hovered range roughly between 0.8775 and 0.88. There were several articles/rumours indicating that the UK government was putting pressure on conservative pro-EU PM’s to support the government’s view. Question remains whether even a government ‘victory’ today will bring more calm/stability to the UK Brexit debate. Anyhow, sterling remained in the defensive. EUR/GBP trades in the 0.8785 area. Cable retested the 1.3150 area this morning and trades currently 1.3190 awaiting the outcome of the vote.

News Headlines:

After China’s retaliation measures on US tariffs on Chinese import, Europe will also start to charge import duties of 25 percent on €2.8bn worth of US goods. This rather limited retaliation is said to be in line with WTO rules and will be removed if the US backs down on and removes their import tariffs.

At the ECB Forum in Sintra, officials have stated that they have become increasingly concerned about a potential trade war. The outcome of Donald Trump’s current actions “could possibly derail the recovery in the euro zone and complicate an exit from the stimulus program”.

The CBI confirmed that optimism in the UK’s manufacturing sector has improved in the second quarter of this year with a balance of 13 (Reuters poll expected 1). However, they warn that the medium-term outlook remains clouded by Brexit and the ongoing trade war.

Fed Powell: Historical experience doesn’t shed much light on unemployment-inflation relationship

Fed Chair Jerome Powell's speech at the ECB Forum on Central Banking in Portugal was titled "Monetary Policy at a Time of Uncertainty and Tight Labor Markets". There he said that growth trend is "not as strong as we would like it to be". But labor market is "particular robust". Meanwhile, policymakers have "yet to see "if inflation could remain near to 2% target on "sustained basis".

Powell also compared the current labor market to the period from February 1966 through January 1970, when unemployment rate was below 4%. He pointed out that inflation jumped from 2% in 1965 to 5% in 1970. And the unsustainably low unemployment at the time had contributed to escalating inflation.

However, after half a century, Powell said the US economy has "changed in many ways". And the so called "natural rate of unemployment" is "substantially lower now. The Congressional Budget Office's estimated natural rate was at 5.75% in late 1960 but at 4.75% currently. Rising education levels was a factor that sent the natural rate down. Also, policymakers have a "greater appreciation" of the role of inflation expectation and and have clearer commitment to maintaining low and stable inflation.

So, Powell said that "historical comparison does not shed as much light as we might have hoped."