Sample Category Title

(SNB) Swiss National Bank Leaves Expansionary Monetary Policy Unchanged

The Swiss National Bank (SNB) is maintaining its expansionary monetary policy, thereby stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB remains at −0.75% and the target range for the three-month Libor is unchanged at between −1.25% and −0.25%. The SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration.

All in all, the value of the Swiss franc has barely changed since the monetary policy assessment of March 2018. The currency remains highly valued. Following the March assessment, the Swiss franc initially depreciated slightly against the US dollar and the euro. However, in light of political uncertainty in Italy, we have since seen countermovement, particularly against the euro. The situation on the foreign exchange market thus remains fragile, and the negative interest rate and our willingness to intervene in the foreign exchange market as necessary therefore remain essential. These measures keep the attractiveness of Swiss franc investments low and ease pressure on the currency.

The new conditional inflation forecast for the coming quarters is slightly higher than it was in March 2018 due to a marked rise in the price of oil; this price rise ceases to affect annual inflation after the first quarter of 2019. From mid-2019, the new conditional forecast is lower than it was in March 2018, mainly due to the muted outlook in the euro area. At 0.9%, the inflation forecast for 2018 is 0.3 percentage points higher than projected at the March assessment. For 2019, the SNB continues to anticipate inflation of 0.9%. For 2020, we expect to see inflation of 1.6%, compared with 1.9% forecast in the last quarter. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon.

Overall, global economic growth was solid in the first quarter. Growth in the US and China was strong and broad-based. The pace of economic expansion slowed in the euro area, however, albeit partly due to temporary factors. The economic signals for the coming months remain favourable. The SNB's baseline scenario therefore assumes that the global economy will continue to grow above its potential.

The risks to the SNB's baseline scenario are more to the downside. Chief among them are political developments in certain countries as well as potential international tensions and protectionist tendencies.

Switzerland's economy continued to recover as expected, with GDP once again growing faster than estimated potential in the first quarter. Overall capacity utilisation improved further on the back of this positive development. The SNB still anticipates GDP growth of around 2% for the current year and expects to see unemployment falling further.

Imbalances on the mortgage and real estate markets persist. While growth in mortgage lending has been only moderate over the last few quarters, real estate prices have continued to rise. Particularly in the residential investment property segment, there is the risk of a correction due to the strong increase in prices in recent years. The SNB will continue to monitor developments on the mortgage and real estate markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.

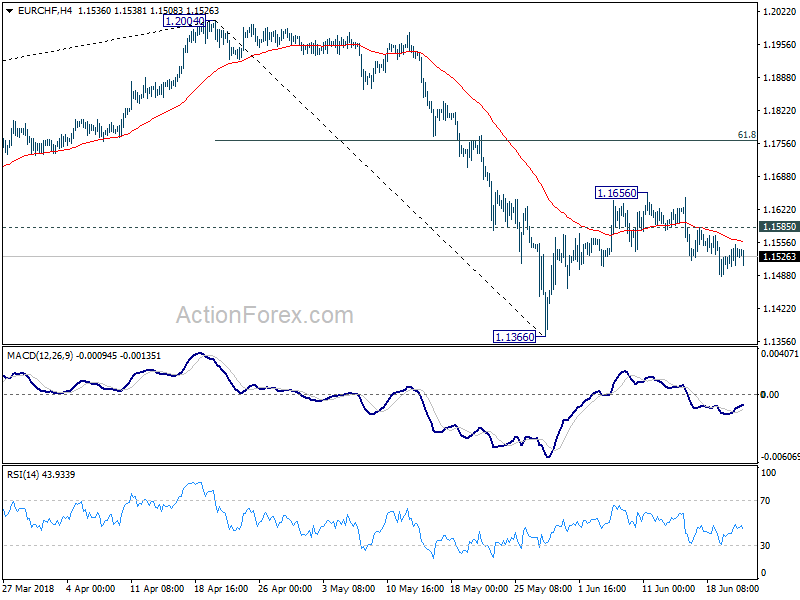

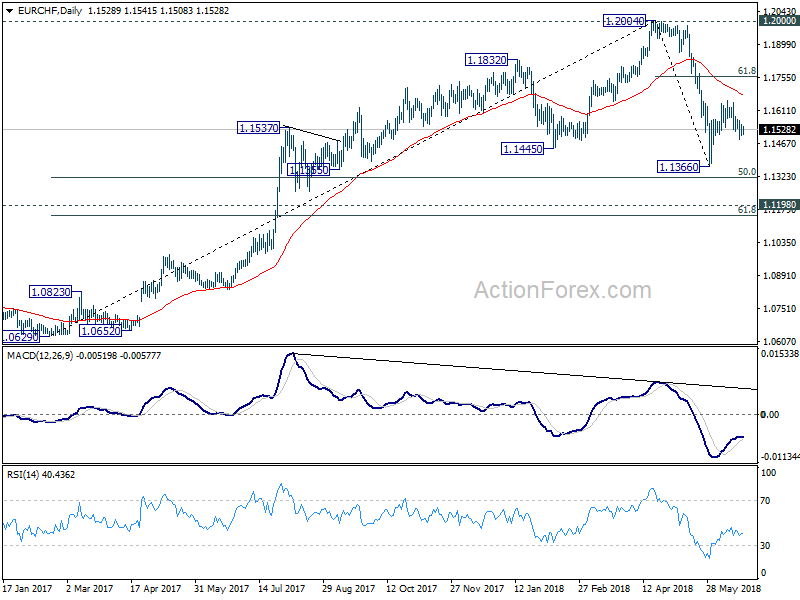

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1509; (P) 1.1531; (R1) 1.1554; More....

With 1.1585 minor resistance intact, deeper fall is still mildly in favor in EUR/CHF for 1.1366 support. Break there will resume the corrective fall from 1.2004. On the upside, though, above 1.1585 will likely extend the rebound from 1.1366 through 1.1656. But in that case, upside should be limited by 61.8% retracement of 1.2004 to 1.1366 at 1.1760.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

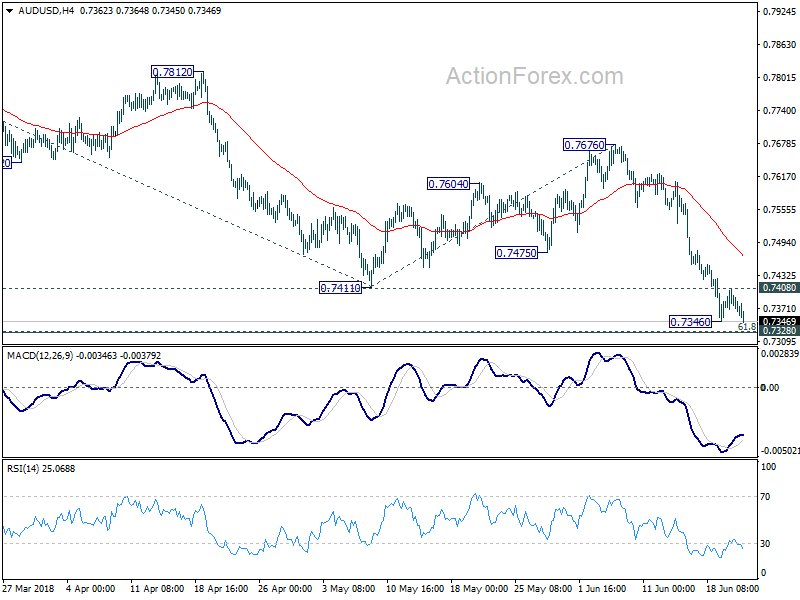

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7354; (P) 0.7381; (R1) 0.7397; More...

Breach of 1.7346 temporary low suggests fall resumption after brief consolidation. Intraday bias is back on the downside for 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). Firm break of 0.7382 will target 61.8% projection of 0.8135 to 0.7411 from 0.7676 at 0.7229 next. Nonetheless, above 0.7408 minor resistance will turn bias neutral again to bring more consolidations first.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

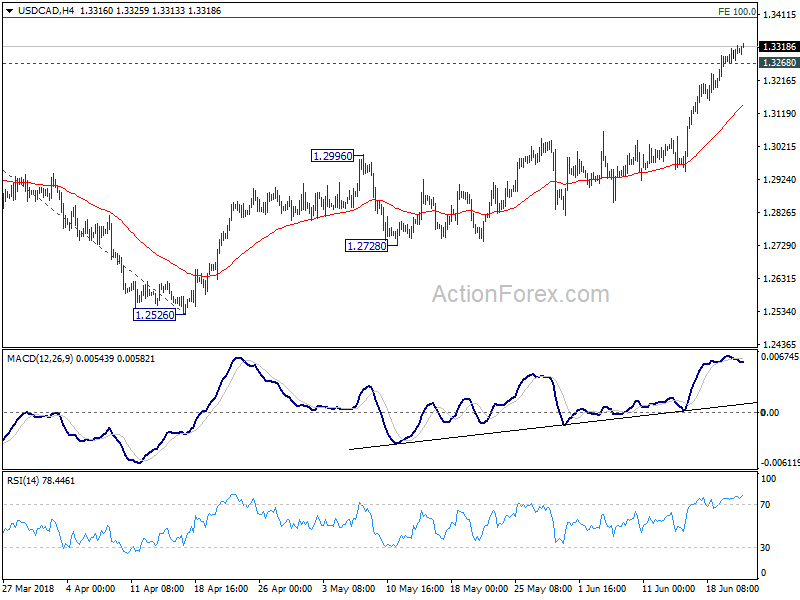

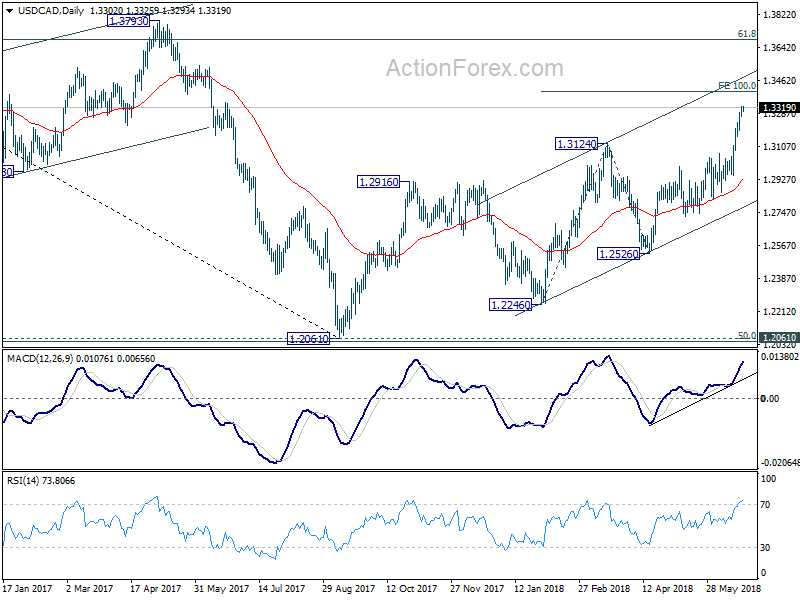

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3273; (P) 1.3302; (R1) 1.3340; More...

USD/CAD's rally is still in progress even though upside momentum is diminishing as seen in 4 hour MACD. Intraday bias stays on the upside for 100% projection of 1.2246 to 1.3124 from 1.2526 at 1.3404 next. On the downside, below 1.3268 minor support will turn intraday bias neutral and bring consolidation first, before staging another rise.

In the bigger picture, current development solidify the view of bullish trend reversal. That is fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. This will now be the preferred case as long as 1.2526 support holds, even in case of deep pull back.

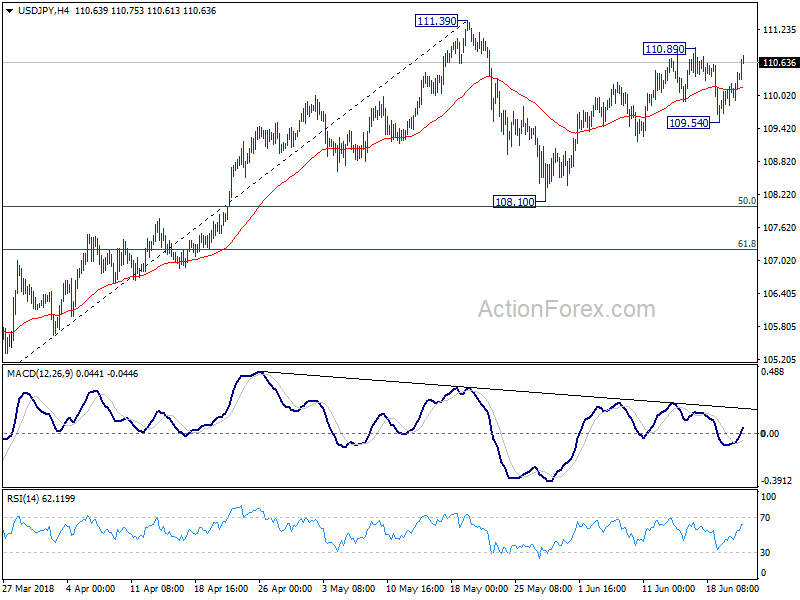

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.99; (P) 110.22; (R1) 110.59; More...

USD/JPY's rebound from 109.54 extends higher today but stays below 110.89. Intraday bias remains neutral first. On the upside, break of 110.89 will extend the rise from 108.10 towards 111.39. But we'd be cautious on strong resistance from there to limit upside. Corrective pattern from 111.39 could extend with another falling leg. Break of 109.54 will target 108.10 and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

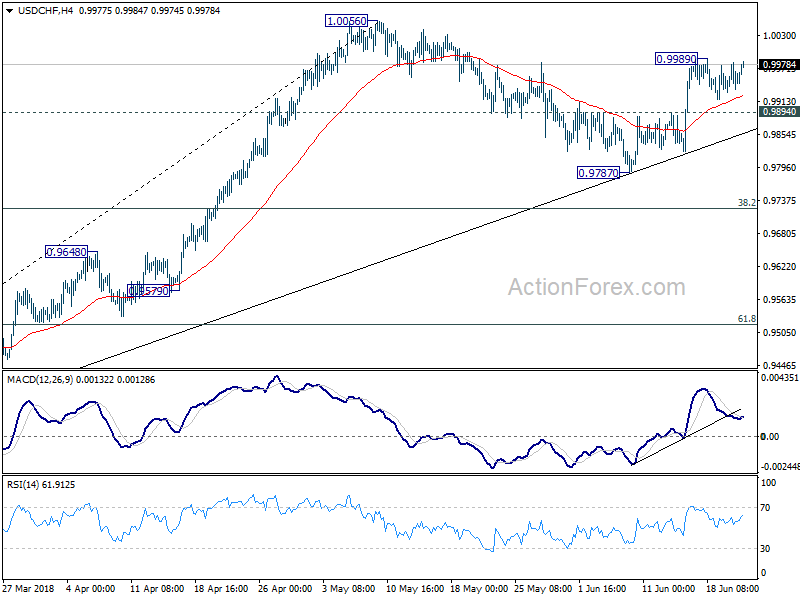

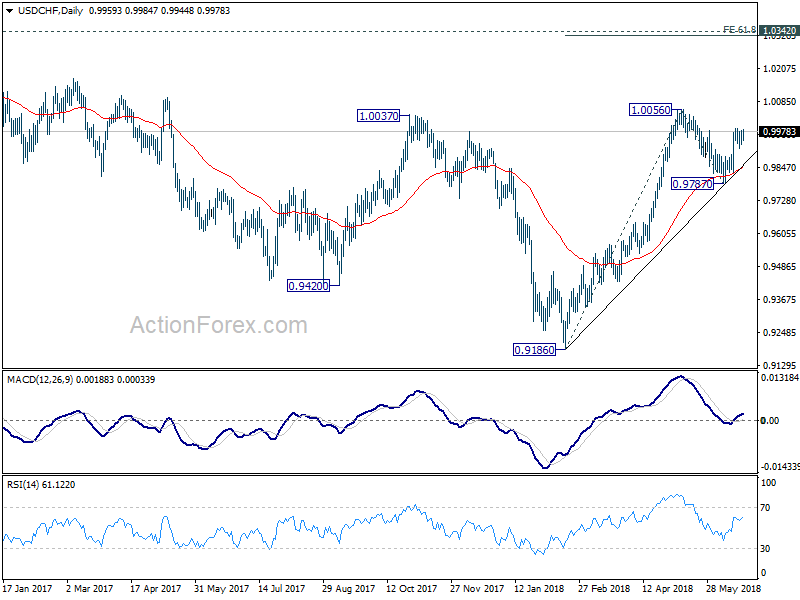

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9937; (P) 0.9960; (R1) 0.9984; More...

USD/CHF is still staying below 0.9989 temporary top for the moment and intraday bias stays neutral. Outlook is unchanged that corrective fall from 1.0056 should have completed at 0.9787. Further rally is expected as long as 0.9894 minor support holds. On the upside, above 0.9989 will bring retest of 1.0056 first. Break will resume the rise from 0.9186 and target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, break of 0.9894 will likely extend the correction, possibly through 0.9787 before completion.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

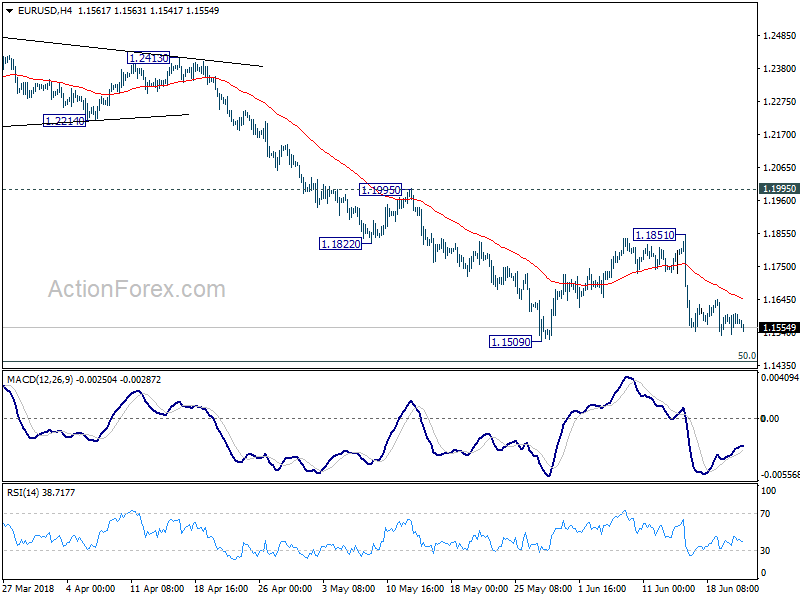

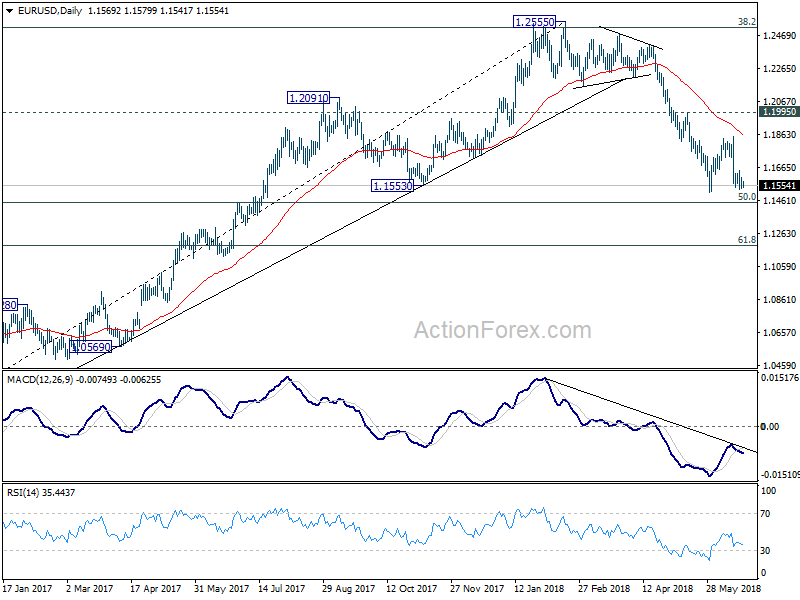

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1541; (P) 1.1572 (R1) 1.1606; More.....

Intraday bias in EUR/USD remains neutral as consolidative trading continues. In case of another recovery, upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

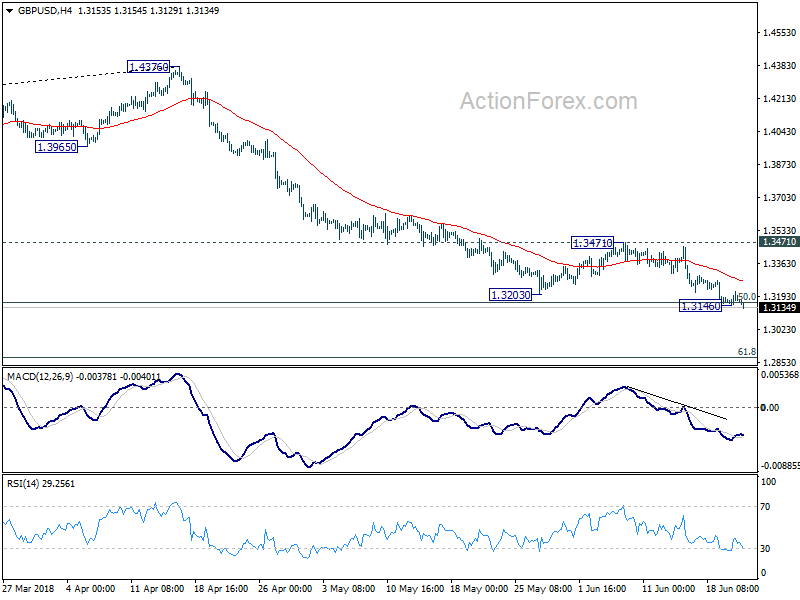

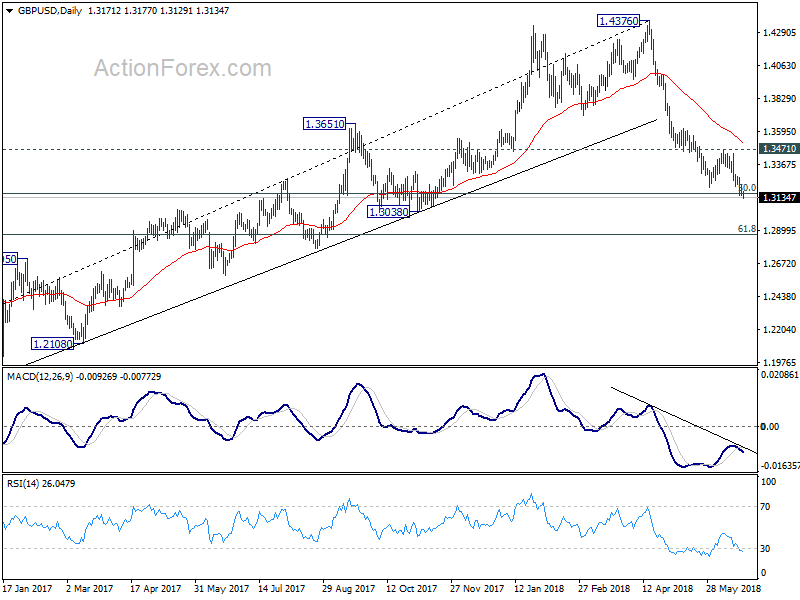

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3142; (P) 1.3179; (R1) 1.3211; More...

GBP/USD's decline resumes after brief consolidation and reaches as low as 1.3129 so far. Intraday bias is back on the downside. Sustained trading below 50% retracement of 1.1946 to 1.4376 at 1.3161 will extend the fall from 1.4376 to 61.8% retracement at 1.2875 next. On the upside, break of 1.3471 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of another recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Sterling and Swiss Mixed ahead of BoE and SNB, Dollar Surges as Lifted by Yields

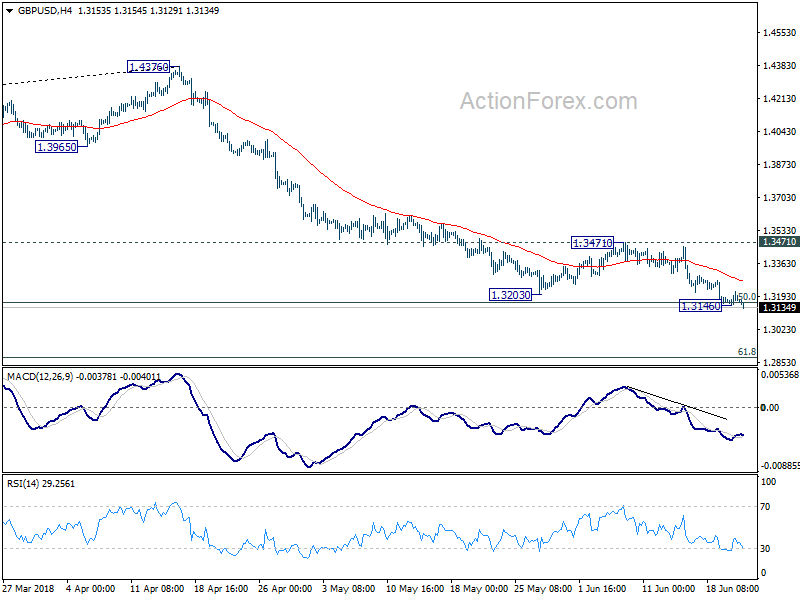

Dollar overtakes Yen as the strongest current for the week as buying merges today. Overnight's rebound in treasury yield gives the greenback a helping hand. 10 year yield gained 0.035 to close the regular session at 2.928 and it breached 2.95 in Asia. Gold also extends recent slump on a strong Dollar and hits as low as 1265. Sterling and Swiss are are mixed as markets await BoE and SNB rate decisions. Kiwi is the weakest one as GDP report confirmed slow down while Australian Dollar is also weak. But Canadian Dollar is trying to recover, except versus Dollar, as WTI crude oil is back pressing 66.

Technically, GBP/USD's fall resumes after brief consolidations and it's now on course for next medium term fibonacci level at 1.2875. AUD/USD follows and breaks this week's low at 0.7346 to resume recent decline. Focus will now be on 0.9989 temporary top in USD/CHF, and 1.1509 support in EUR/USD for today, to confirm Dollar's broad based strength.

BoE and SNB to stand pat today

BoE and SNB meetings are the biggest focuses for today. BoE is widely expected to keep monetary policy unchanged. That is, the bank rate will be held at 0.50% while asset purchase target will be kept at GBP 435B. Known hawks Ian McCafferty and Michael Saunders are expected to vote for rate hike while others would vote for standing pat. The June meeting does not include updated economic projection nor a press conference. As such the meeting minutes would be in focus, serving as an indicator for the likelihood of an August rate hike. If hopes of an August rate hike falter, the chance of a November hike would be more remote. Hawkish Ian McCafferty is leaving the Committee and would be replaced by Jonathan Haskel, an Imperial College Business School professor. It remains to be seen how Haskel is. More in BOE Preview – Focus on June Meeting Minutes.

SNB is also widely expected to stand pat, keeping three-month Libor range between -1.25 and -0.25%. The central bank will also likely maintain the the commitment to intervene the FX market when needed, reiterating that it would 'remain active in the foreign exchange market as necessary', while 'taking the overall currency situation into consideration'. EUR/CHF hit SNB's prior imposed floor at 1.2 back in April. But political turmoil in Italy and fear of global trade war send the cross down to as low as 1.1366 back in late. With EUR/CHF currently at around 1.15, there is little chance for SNB to sound more relaxed.

Canadian Trudeau can't accept why Trump damages his own auto industry

Canadian Prime Minister Justin Trudeau said yesterday that he couldn't imagine Trump damaging the car industry of the US by imposing auto tariffs. He said, "I have a hard time accepting that any leader might do the kind of damage to his own auto industry that would happen if he were to bring in such a tariff on Canadian auto manufacturers, given the integration of the parts supply chains or the auto supply chains through the Canada-U.S. border."

Trudeau tried to tone down Trump's personal attack on him. He said that "I'm not in a position to opine on motivations of the president. I'm going to stay focused on the relationship that we're building, on defending Canada's interests, on looking for ways to further push the benefits of improving and modernizing NAFTA ... in all three of our countries."

Accord to a recent poll by Ipsos conducted between June 13-15, approval rating of Trudeau jumped to 50%, with 12% of Canadian strongly supporting him and 39% somewhat supporting. That's a notable increase from the low of 44% at the end of March. That came after Trump's personal attack on Trudeau saying that he acted so "meek and mild" during the G7 meeting. And, Trump's trade advisor Peter Navarro said "there is a special place in hell" for Trudeau.

Chinese Vice Premier to meet European Commission Vice President Katainen next week on trade

Chinese Vice Premier Liu He will be meeting with European Commission Vice President Jyrki Katainen in Beijing on June 25. That's the seventh China-EU high level economic and trade summit since 2007, when the mechanism was established.

Spokesman of the Ministry of Commerce said in a regular briefing that the meeting is an important platform for for communications and coordinations of economic and trade policies. And it's an important time when "trade and economic cooperation faces new historical opportunities."

Issues to be discussed will include " global economic governance, trade and investment, innovation-driven development, and interconnection that are of common concern to both sides". And, it's a "positive signal between China and the EU to oppose unilateralism and protectionism and support the multilateral trading system."

New Zealand GDP growth slowed to 0.5% qoq in Q1

New Zealand GDP grew 0.5% qoq in the March quarter, slowed from 0.6% qoq in the prior quarter and met expectation. Over the year, GDP grew 2.7% ended March 2018. Per capita GDP was unchanged, down from 0.1% qoq rise in the prior quarter. Services industries grew 0.6%, notably slowed from prior 1.1%. Good-producing industries were flat as jump in manufacturing was offset by fall in constructions. Primary industries rebounded by growing 0.6%, up from prior quarter's -2.6%.

On the data front

Swiss will release trade balance today. UK will release public sector net borrowing. Canada will release wholesale sales. US will release jobless claims, Philly Fed survey, house price index and leading indicators.

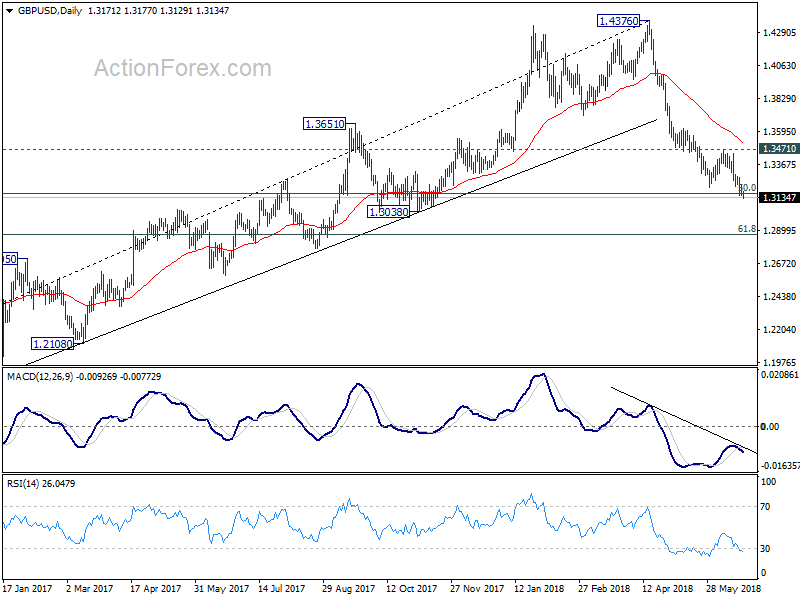

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3142; (P) 1.3179; (R1) 1.3211; More...

GBP/USD's decline resumes after brief consolidation and reaches as low as 1.3129 so far. Intraday bias is back on the downside. Sustained trading below 50% retracement of 1.1946 to 1.4376 at 1.3161 will extend the fall from 1.4376 to 61.8% retracement at 1.2875 next. On the upside, break of 1.3471 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of another recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 0.50% | 0.50% | 0.60% | |

| 6:00 | CHF | Trade Balance (CHF) May | 2.76B | 1.89B | 2.29B | |

| 7:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | ||

| 7:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | ||

| 7:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | ||

| 8:30 | GBP | Public Sector Net Borrowing May | 5.1B | 6.2B | ||

| 11:00 | GBP | BoE Official Bank Rate | 0.50% | 0.50% | ||

| 11:00 | GBP | BoE Asset Purchase Target Jun | 435B | 435B | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 2--0--7 | ||

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.50% | 1.10% | ||

| 12:30 | USD | Initial Jobless Claims (JUN 16) | 220K | 218K | ||

| 12:30 | USD | Philly Fed Manufacturing Index Jun | 25 | 34.4 | ||

| 13:00 | USD | House Price Index M/M Apr | 0.30% | 0.10% | ||

| 14:00 | USD | Leading Index May | 0.40% | 0.40% | ||

| 14:00 | EUR | Eurozone Consumer Confidence (JUN A) | 0 | 0 | ||

| 14:30 | USD | Natural Gas Storage | 96B |

Equities And Yields Move Higher As Trade Tensions Continue Between US And China

General Trend:

- Asian equity markets trade mixed; Shanghai Composite and Hang Seng pare gains

- Australian equities outperform, consumer discretionary companies gain amid M&A

- South Korean chipmakers rise after earnings/guidance from Micron

- South Korea sold 50-year bonds at lower yield

- New Zealand sold 20-year bonds at lower bid to cover and higher yield; yields rose following auction result

- BoJ official Funo noted ‘large’ downside risk to medium to long-term inflation expectations

- China Commerce Ministry confirms to issue new list related to foreign investment by July 1st

- Peso strengthens 0.2% after Philippines Central Bank raises rates

- Upcoming BoE meeting in focus

- Japan May CPI figures due on Friday’s session

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%

- TOPIX Info & Communications index +0.7%, Real Estate +0.5%; Marine Transportation -0.9%, Securities -0.9%, Iron & Steel -0.8%

- Megabanks trade generally lower

- (JP) According to an IMF official Japan's consumption tax should be raised to 15%; Social security cuts also needed to curb unsustainable debt - Nikkei

- (JP) Japan and EU to sign free trade agreement (FTA) on July 11th

- Toyota Motor, 7203.JP Said to have started reductions in sales and marketing costs, including cancellation of contracts with China unit of Dentsu - financial press

- (JP) Japan Investors Net Buying of Foreign Bonds: +¥1.49T v -¥488.5B prior week; Foreign Net Buying of Japan Stocks: -¥40.8B v -¥108.5B prior week

- (JP) Bank of Japan (BOJ) Funo: Reiterates need to patiently promote strong monetary easing under current framework

- (JP) BOJ Dep Gov Amamiya: Inflation is expected to elevated towards the 2% target; corporate sector's price/wage setting remains cautious and prices have been weak relative to economic growth and labor market tightening - speaking at Shinkin banking convention

- (JP) Japan MoF sells ¥2.0T v ¥2.0T indicated in 0.10% (prior 0.10%) 5-yr bonds; avg yield -0.1130% v -0.1030% prior; bid to cover 3.88x v 4.22x prior

Korea

- Kospi opened 0.0%

- LG Display [034220.KR] declines over 3%; Speculated to consider offering early retirement to certain workers (South Korean Press)

- (KR) South Korea May PPI Y/Y: 2.2% v 1.6% prior

- (KR) North Korea Leader Kim was satisfied with trip to China - KCNA, North Korean state media

- (KR) Real estate market booming on China/North Korea border amid hopes of a peaceful peninsula – Nikkei

- (KR) South Korea June 1-20 Exports Y/Y: -4.8% v +14.8% prior; Imports Y/Y: +13.0% v 10.7% y/y

- (KR) South Korea sells KRW540B v KRW500B indicated in 50-yr bonds; avg yield 2.51% v 2.64% prior; bid to cover 2.0x

China/Hong Kong

- Hang Seng opened +0.2%, Shanghai Composite -0.1%

- Hang Seng Energy index -1%, Industrial goods -0.8%, Telecom -0.8%, Financials -0.6%

- (CN) China said to consider allowing pension funds to make investments overseas – China Daily

- (HK) Property developers in Hong Kong said to seek to rush sales of apartments ahead of vacancy tax – HK Press

- (CN) China PBoC Open Market Operation (OMO): Injects CNY100B in 7 and 14 day reverse repos v CNY100B injected in 7 and 14 day reverse repos prior: Net: CNY30B injection v CNY40B injected prior

- (CN) China PBoC sets yuan reference rate at 6.4706 v 6.4586 prior

- (CN) China PBoC expects banking system liquidity to rise further; reverse repo operations aim to stabilize end of June liquidity – financial press

- (CN) China Commerce Ministry: Have no choice in implementing new tariffs on certain US products in segments where China announced broader tariff cuts; hope US will be fair in its anti-dumping probe against Chinese firms

- (US) President Trump said to be considering plans to curb Chinese investment in more than 1,000 US companies - US press

Australia/New Zealand

- ASX 200 opened +0.2%

- ASX 200 Consumer Discretionary index +1.9%, Resources +1.1%, Financials +1%, REIT +1%

- Ramsay Health Care [RHC.AU] declines over 7% after cutting forecast

- Fletcher Building, FBU.NZ Affirms FY18 (NZ$) EBIT ex- B+I 680-720M (incl -660M); to announce new operating model July 1st, to reduce overhead by NZ$30M/yr - strategy day

- (AU) Australia Parliament passes income-tax package: includes A$144B in personal income tax cuts (over 10 years)

- (AU) Australia revised Espionage and Foreign Interference bill expected to pass parliament this week is angering China; Bill was introduced amid fears of Chinese meddling in Australia's democracy - Press

- (NZ) NEW ZEALAND Q1 GDP Q/Q: 0.5% V 0.5%E; Y/Y: 2.7% V 2.7%E

- WOW.AU BP will not continue with proposed acquisition of petrol business

- Atlas Iron, AGO.AU Withdraws recommendation of Mineral Resources offer; recommends Hancock's offer of A$0.042/share

- APN Outdoor, [+12%], APO.AU Receives indicative and non-binding proposal to be acquired by JCDecaux for A$6.52/shr valued at A$1.1B

- (AU) Reserve Bank of Australia (RBA) issues quarterly bulletins: Private Non-mining Investment in Australia and Labour Market Outcomes for Younger People

- (AU) Australia May RBA Govt FX Transactions (A$): -672M v -630M prior

- (NZ) New Zealand sells NZ$200M v NZ$200M indicated in 2.75% April 2037 bonds, avg yield 3.2631% v 3.2423% prior, bid to cover 1.2x x v 2.45x prior

- (AU) RBA Gov Lowe: Australia is hoping to extend its no recession streak; Confident we can return to 2.5% inflation; Sudden shift in trade policies is very worrisome; very concerned about big global event from trade - comments in Sintra (overnight)

North America

- US equity markets ended mixed: Dow -0.2%, S&P500 +0.2%, Nasdaq +0.7%, Russell 2000 +0.8%

- S&P500 Telecom +1.2%, Real Estate +1.1%

- (US) President Trump: Renegotiating trade deals left and right, was time to do something on trade deals; Will be very close to reaching 4% GDP

- Micron, MU Reports Q3 $3.15 v $3.14e, Rev $7.80B v $7.70Be

- (SA) Reportedly Saudi Arabia now seeking a 600-800K bpd production increase from OPEC+ producers - press

- (CN) State-controlled The Global Times: China could take action against US firms listed on the Dow Jones index if US President Trump continues to worsen trade tensions

- (CN) Executives from China Energy Investment Corp canceled a trip to West Virginia amid trade dispute; meeting was said to focus on a ~$84B investment for the state – financial press

Europe

- (UK) UK govt wins vote in parliament, defeating Brexit 'meaningful vote' amendment (As expected after compromise made earlier); PM May wins in narrow 319-303 vote

- (UK) Prime Min May: govt to publish an EU relationship white paper over next few weeks - press

- (EU) EU draft proposal on migrants: to strengthen external border protection; members agree to support migrant reception and resettlement outside of the EU - press

- (DE) Germany May Tax Rev +6.8% y/y - Finance Ministry

- (CN) China Commerce Ministry: Vice premier Liu He to attend June 25th meeting with Europe delegation in Beijing

- Daimler [DAI.DE]: Cut FY18 EBIT outlook

Levels as of 01:30ET

- Hang Seng -1.0%; Shanghai Composite -0.4%; Kospi -0.6%; Nikkei225 +0.7%; ASX 200 +1.1%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.4%, Dax +0.4%; FTSE100 +0.3%

- EUR 1.1537-1.1600; JPY 110.32-110.74; AUD 0.7356-0.7381;NZD 0.6833-0.6880

- Aug Gold -0.6% at $1,266/oz; Aug Crude Oil -0.4% at $65.48/brl; Jul Copper -0.2% at $3.03/lb