Sample Category Title

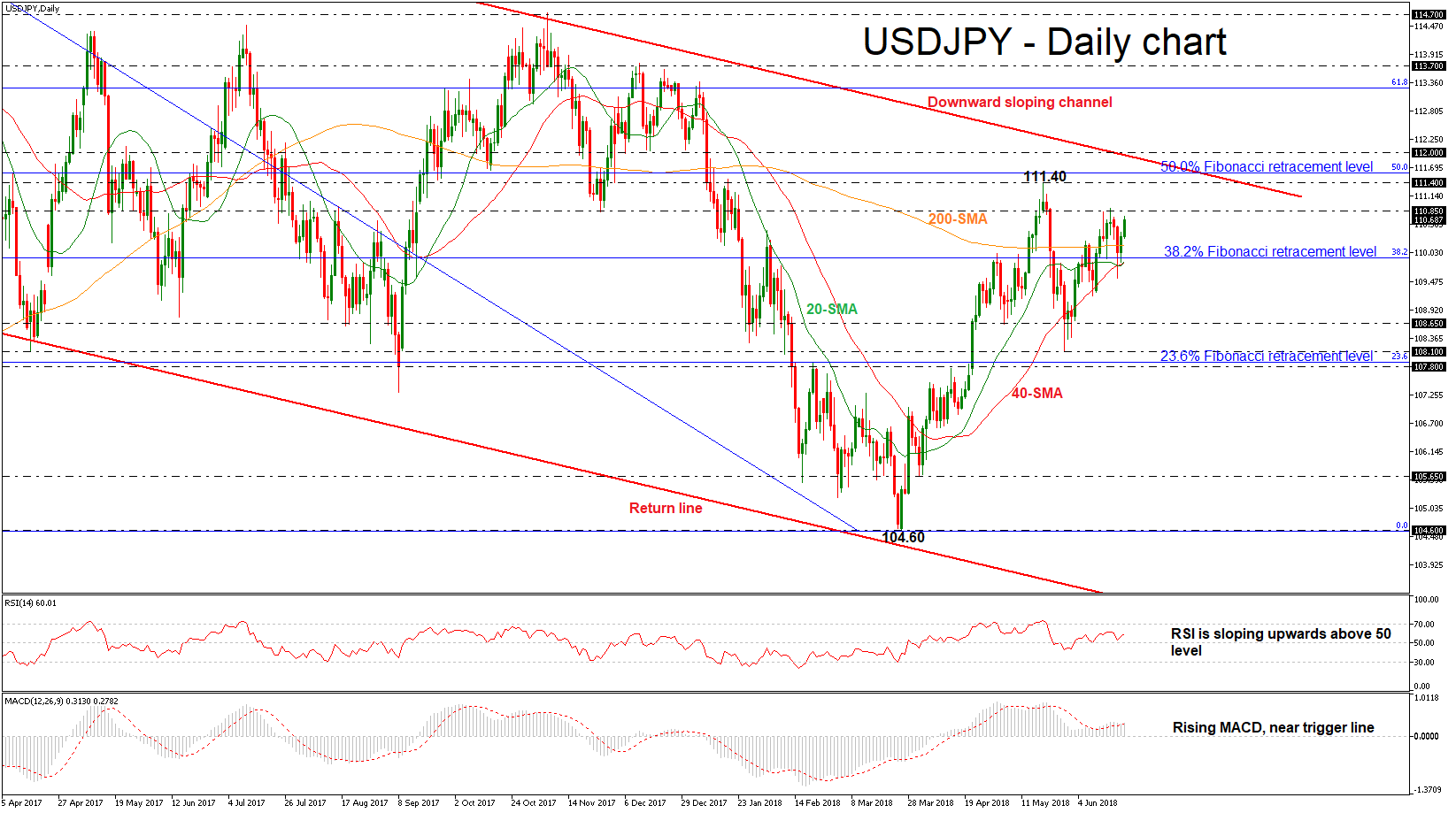

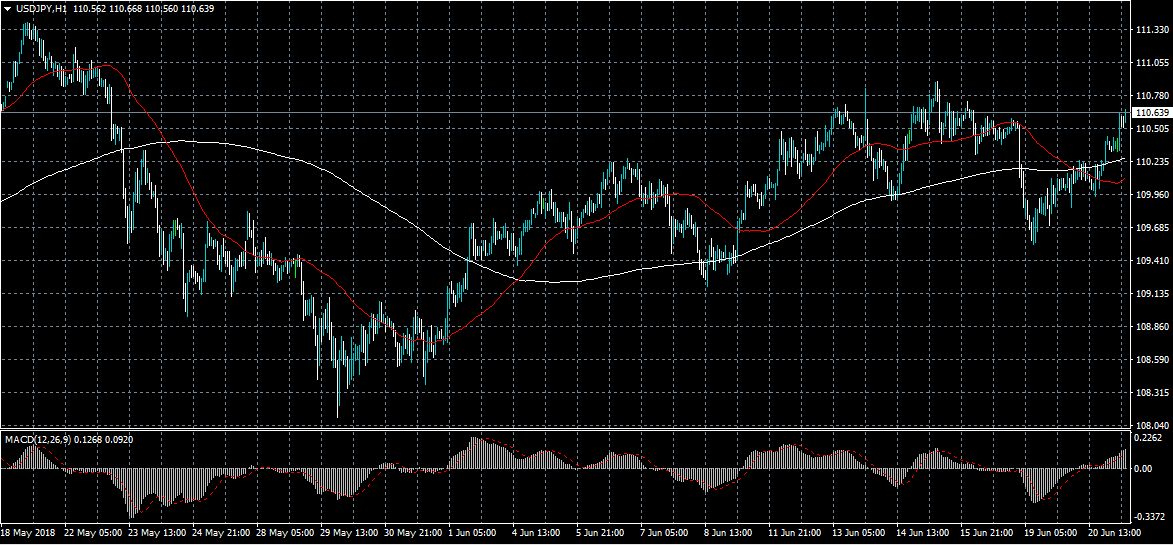

USDJPY Regains Some Ground After Surpassing 200-Day SMA

USDJPY has struggled in a narrow range over the last few daily sessions with upper boundary the 110.85 resistance level and lower boundary the 38.2% Fibonacci retracement level of the downleg from 118.60 to 104.60, around 109.95. The price is set to complete the second bullish day in a row after the bullish crossover within the 20- and 40-simple moving averages (SMAs) in the daily timeframe.

From the technical point of view, the technical indicators are endorsing the scenario for further upside potential move. The price remains above the significant 200-day SMA signaling for bullish pressure. The RSI indicator is sloping upwards above the threshold of 50, while the MACD oscillator lies near its trigger line and is rising with weak momentum above the zero line.

Should the market extend gains and surpass the 110.85 resistance level support could be met between the 111.40 resistance level and the 50.0% Fibonacci mark near 111.60. A leg above this area could send prices towards the 112.00 psychological barrier, which currently fluctuates near the descending trend line of the longer-term falling sloping channel. In case of an upside violation of this level could shift the bearish bias to bullish.

Conversely, if the pair bounces down, immediate support could come at the 38.2% Fibonacci of 109.95, which stands near the 20- and 40-SMAs. Steeper decreases could drive the pair south towards the 108.65 hurdle.

Broadly, USDJPY has been trading within a downward sloping channel since December 2016, while in the short-term the market holds in an ascending movement after the rebound on the 104.60 support.

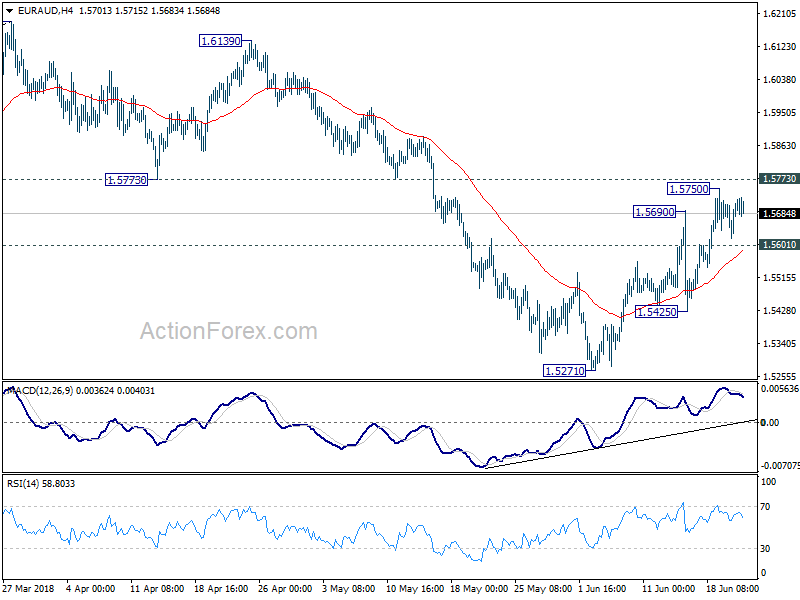

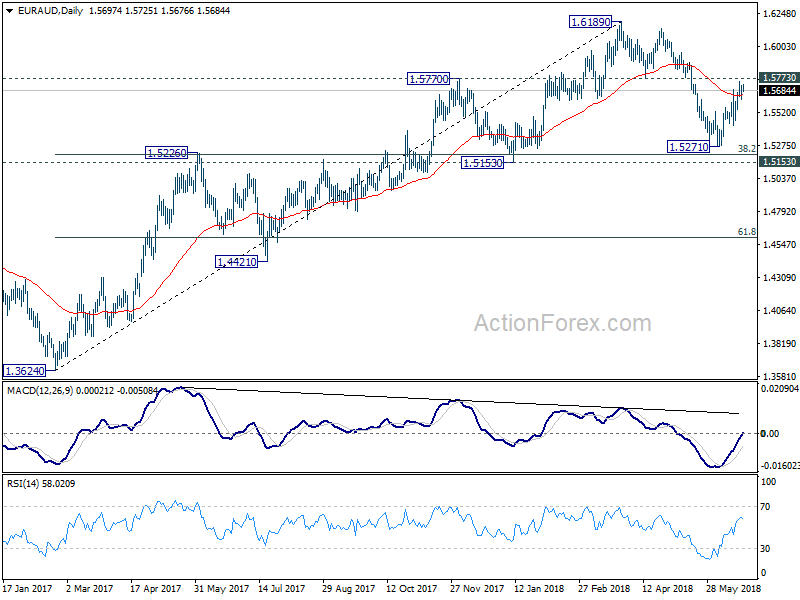

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5644; (P) 1.5684; (R1) 1.5750; More....

Intraday bias in EUR/AUD remains neutral at this point. On the downside, break of 1.5601 minor support will turn bias to the downside for 1.5425. Break there will confirm completion of rebound from 1.5271 and target this low again. Meanwhile, sustained break of 1.5773 will indicate that whole decline from 1.6189 has completed with three waves down to 1.5271 already. And retest of 1.6189 should be seen next.

In the bigger picture, focus is back on 1.5773 support turned resistance with the current strong rebound. Firm break there will argue that medium term rise from 1.3624 (2017 low) is not completed yet. Further break of 1.6189 will target 1.6587 key resistance (2015 high). Though, rejection by 1.5773 will revive the case of bearish trend reversal and target 61.8% retracement of 1.3624 to 1.6189 at 1.4604.

Dollar Reaches New Heights, Bank Of England At The Center Of Attention

Here are the latest developments in global markets:

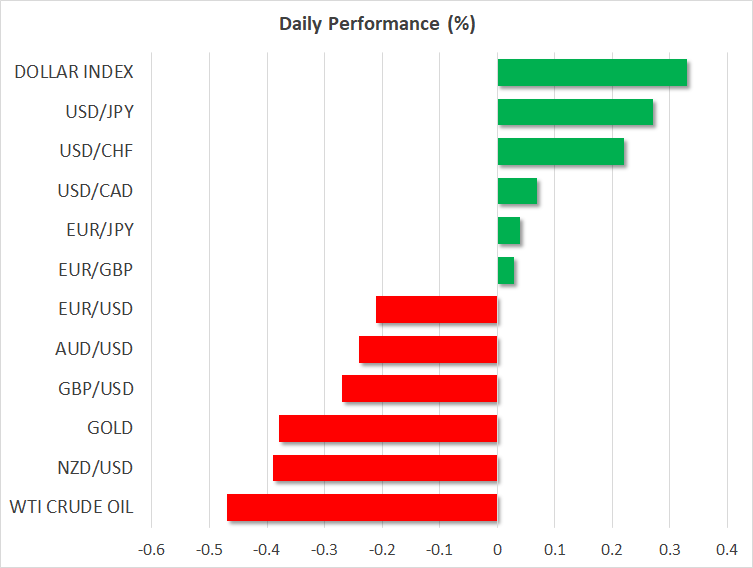

FOREX: The US dollar index is 0.3% higher on Thursday, touching a fresh high for 2018. Safe-haven currencies such as the yen and the Swiss franc are on the back foot, down by nearly 0.3% and 0.2% respectively against the greenback as trade concerns have moved to the background for now. Commodity-linked currencies like the loonie, aussie, kiwi, are also on the retreat, with the first two trading at one-year lows versus the dollar.

STOCKS:US markets closed mixed on Wednesday. The Nasdaq Composite rose 0.72%, bringing the tech-heavy index to a fresh all-time high, propelled higher by the likes of Facebook (+2.3%) and Netflix (+2.9%). Meanwhile, the S&P 500 managed to gain 0.17%, but the Dow Jones fell by the same percentage. Futures tracking the Dow, S&P, and Nasdaq 100 are also pointing to a higher open today. Markets in Asia, though, were mostly in the red. Japan was mixed, as the Nikkei 225 climbed by 0.61% while the Topix fell 0.12%. In Hong Kong, the Hang Seng dropped by 1.23%. Finally in Europe, futures suggest that all but one of the major indices are set to open higher today. The only exception is the German DAX 30.

COMMODITIES: Oil prices are lower on Thursday, amid signals that the 'resistance' to raise OPEC production this week is fading. WTI is down by almost 0.5% and Brent by 0.9%, following comments from Iran's oil minister on Wednesday that his nation could compromise and agree to a small increase in OPEC output – something he had ruled out in previous days. So the conversation now appears to have shifted from whether or not there will be an increase, to how much that increase will be, weighing on prices. In precious metals, gold is down by 0.4% on Thursday, touching fresh lows for 2018 as a stronger US dollar is exerting downward pressure on the dollar-denominated metal. The fact that even the increasingly realistic risk of an 'all out' US-China trade war was unable to lift gold suggests that buyers are in short supply right now, and unless tensions escalate much further or the US dollar reverses course, the current pattern may continue.

Major movers: Dollar touches fresh highs; safe-havens on the defensive

The US dollar index reached an 11-month high during the Asian trading session Thursday, drawing strength from an uptick in longer-term US Treasury yields, as well as a broad tumble in commodity-linked and safe-haven currencies.

In euro land, the common currency came under renewed pressure yesterday, after ECB Governing Council member Ewald Nowotny said that the divergence between ECB and Fed policy will probably have an impact on the exchange rate. His remarks were perceived as a soft 'jawboning' of the euro.

Meanwhile, media reports suggest the ECB is 'growing increasingly concerned that a looming trade war could derail the euro zone's recovery'. Although to a lesser extent, a similar sentiment was echoed yesterday by the heads of the Fed, ECB, and BoJ at the ECB's conference in Sintra, Portugal. All three noted that boiling trade tensions could have implications for monetary policy, implicitly suggesting such risks could slow their respective paths towards normalization.

Staying on trade, the 'trade war' narrative appears to have moved to the background for now, as markets remained in recovery-mode yesterday. US stock markets closed mostly higher, while havens like the yen and the franc retreated alongside gold. A similar pattern appears to be in the works on Thursday, as the yen is already down by nearly 0.3% against the dollar, while US stock futures are pointing to a higher open.

The exception to this modest recovery have been the commodity-linked currencies – the loonie, aussie, and kiwi. The loonie touched fresh one-year lows versus the dollar even despite relatively stable oil prices and optimistic comments from US Commerce Secretary Ross that he expects NAFTA to be renegotiated soon. The tide may turn with tomorrow's CPI data out of Canada. A strong set of prints could lead investors to fully factor in a BoC rate hike in July, currently priced in with a 66% probability, and thereby help the loonie to rebound.

In the UK, PM Theresa May scored a 'victory' yesterday, as the bill that would have given Parliament a meaningful vote on the final Brexit deal was defeated via a 319-303 vote. Cable jumped on the outcome, but quickly came back down to touch fresh lows for the year amid broad dollar-demand. Focus now turns to the BoE policy decision today.

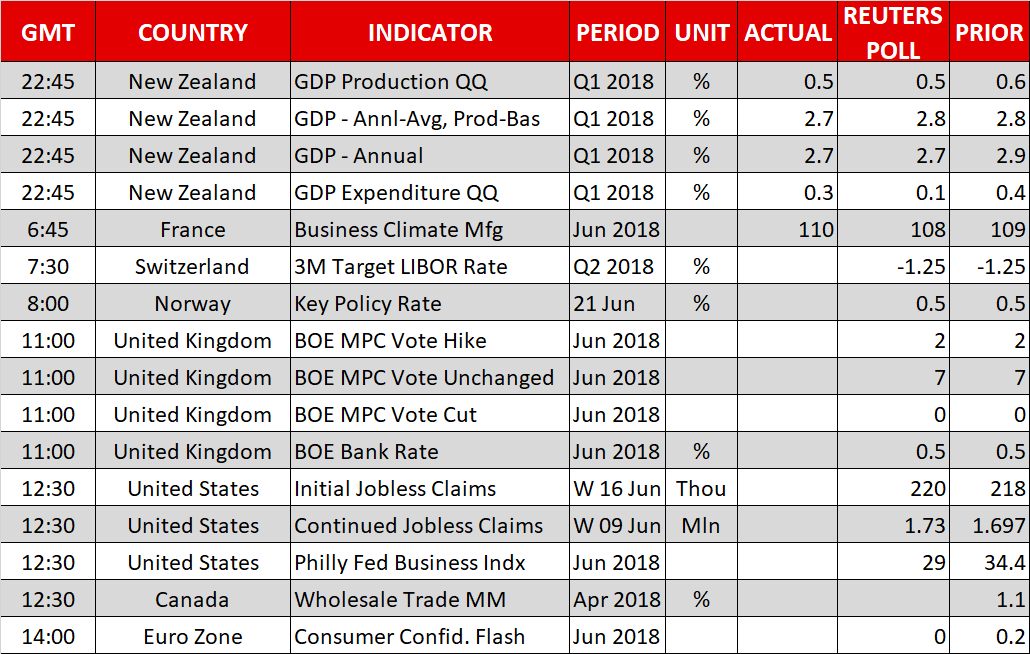

Day ahead: Bank of England decides; SNB and Norges Bank also on the agenda; US jobless claims and eurozone consumer confidence due

The highlight out of Thursday's calendar is the Bank of England (BoE) rate decision. Beyond this and in terms of releases, jobless claims figures are on the agenda out of the US, while the eurozone will be on the receiving end of data on consumer sentiment. Meanwhile, the Swiss National Bank (SNB) and Norges Bank will also be completing their respective meetings on monetary policy.

The Bank of England's rate decision and meeting minutes are scheduled for release at 1100 GMT, with the Bank widely expected to hold its policy rate unchanged at 0.5%. Given that the current meeting does not feature a press conference by Governor Carney or updated growth and inflation forecasts, the Monetary Policy Committee (MPC) members' language in the meeting's minutes is likely to drive positioning on sterling pairs. Specifically, the attention will fall on what the Bank's policymakers will signal regarding upcoming meetings and in particular the one in August. Market participants are assigning a 31% probability for a 25bps interest rate rise during that meeting according to UK overnight index swaps. Should policymakers stoke the odds for such an outcome, then the British pound is expected to post some gains relative to other currencies; the opposite holds true as well.

Overall, the risk may be tilted to the downside for the pound, as the recent largely soft patch of data, in conjunction with uncertainties over Brexit, may cause MPC members to strike a cautious tone in their assessment of the economy.

Meanwhile, the SNB (0730 GMT) and the Norges Bank (0800 GMT) will also be deciding on monetary policy today. Similar to the BoE, they're projected to maintain to hold their policies unchanged. News conferences will follow after the decisions of the two central banks are made public.

US weekly jobless claims data are due at 1230 GMT, with June's Philly Fed Business Index scheduled for release at the same time.

Also at 1230 GMT, Canadian wholesale trade data for April will be hitting the markets.

Out of the eurozone, the European Commission's Directorate General for Economic and Financial Affairs will release its flash consumer confidence figure for June at 1400 GMT; consumer morale in the euro area as gauged by the indicator is anticipated to fall to zero from 0.2 in May.

UK Finance Minister Philip Hammond and BoE Governor Carney will be making their Mansion House speeches on Thursday; the latter will be giving a speech at 2015 GMT. Some remarks on monetary policy by Bundesbank chief Jens Weidmann at 0945 GMT will also be attracting interest.

A eurozone finance ministers meeting (1500 GMT) that is to decide, among others, on possible new debt relief measures for Greece might generate attention.

Lastly, it should be stressed that trade developments remain in the background and could spur volatility in case of any updates.

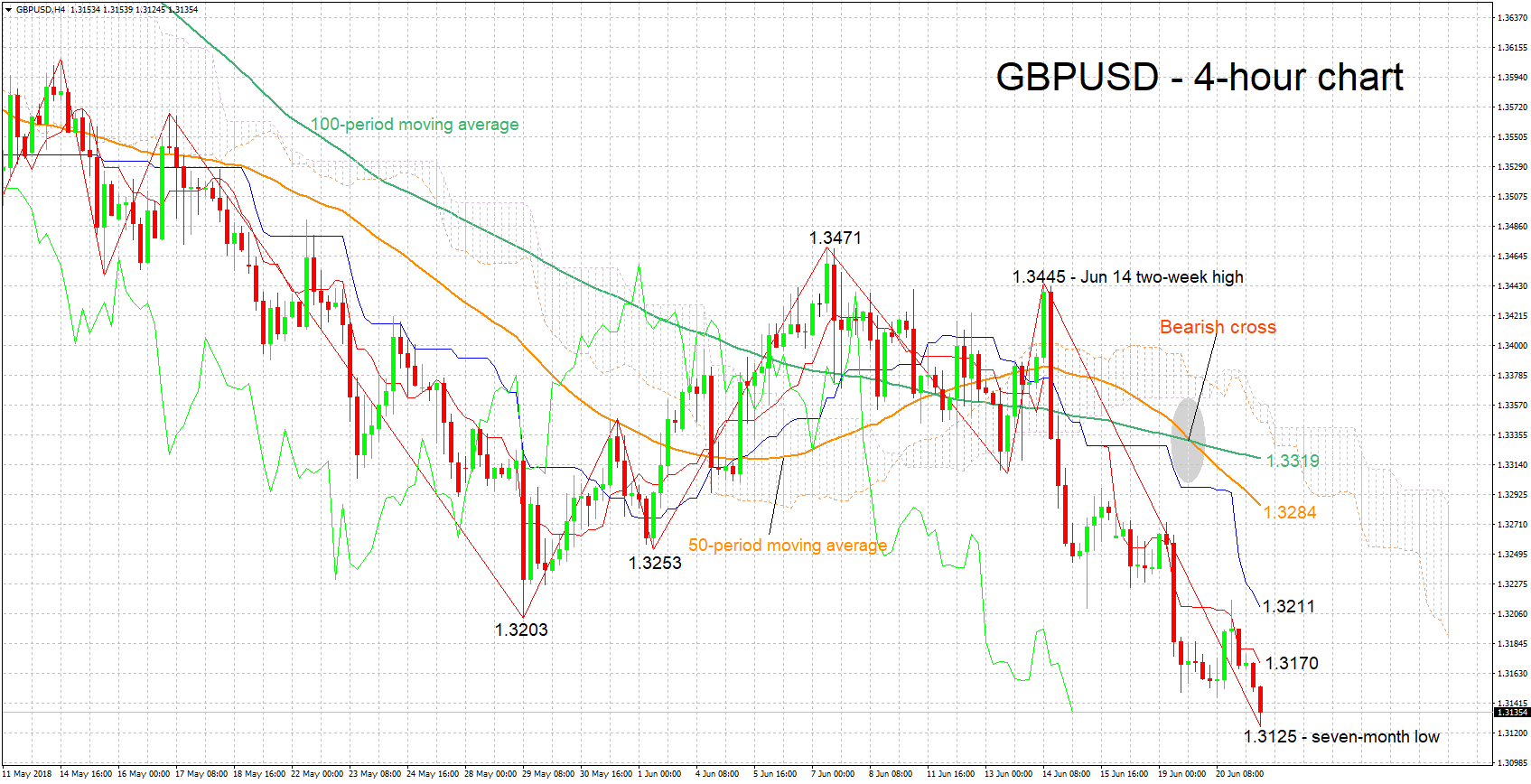

Technical Analysis: GBPUSD bearish at 7-month low; possibly oversold

GBPUSD has declined considerably after hitting a two-week high of 1.3445 around mid-June. Earlier on Thursday, it recorded a fresh seven-month low of 1.3125. The short-term picture is bearish as also evidenced by the negatively-aligned Tenkan- and Kijun-sen lines. The Chikou Span, however, may be pointing to an oversold market; a reversal in the near-term should not be ruled out.

A hawkish Bank of England later on Thursday is expected to boost the pair. Resistance to gains could come around the current levels of the Tenkan- and Kijun-sen lines at 1.3170 and 1.3211 respectively; the region around the latter also encapsulates the 1.32 round figure, as well as a bottom from late May at 1.3203.

On the downside and in case of a cautious BoE that exerts selling pressure on GBPUSD, support could be met around 1.31 and subsequently – and in case of sharper losses – the 1.30 handle.

Currencies: Dollar Gets Benefit Of The Doubt As Trade Tensions Linger

Rates: Risk improvement drives global trading

Yesterday's improvement in risk sentiment is set to continue today and will probably set the tone for global trading. The division between US and EMU monetary policies and Q2 eco data (US outperforming EMU) could trigger a further underperformance of the US Note future against the German Bund.

Currencies: Dollar gets benefit of the doubt as trade tensions linger

Yesterday, sentiment turned risk-on, but it didn't help the euro. The dollar remains in pole position. Investors apparently assume that the trade conflict won't break the US growth momentum, at least not short term. At the same time, ongoing low interest rates weigh on the euro. Sterling doesn't profit going into the BoE policy decision even as PM May survived a key Brexit vote

The Sunrise Headlines

- US equity markets recovered and closed in green for the first time this week, with NASDAQ outperforming. The Asian markets opened mostly with losses. Only the Japanese markets remain slightly positive.

- Therese May has defeated pro-European brexiteers on the ‘meaningful vote' yesterday. She keeps all negotiation power at the table with Europe but had to assure parliament time for debate in the event exit talks break down.

- Chinese Vice Premier Liu He will meet with a senior EU delegation in Beijing next week, where the EU-China High-Level Economic Dialogue is held. Vice President of the European Commission Jykri Katainen is representing EU values.

- North-Korean leader Kim Jong Un and Chinese President Xi Jinping had a promising meeting this week. They agreed to boost strategic and tactical cooperation, among the understanding of North-Korea's denuclearization.

- Bank of Japan board member Yukitoshi Funo said that the central bank will remain its current policy of strong monetary easing since prices remain very weak. He said the 2% inflation remains a distant goal.

- New Zealand's recent data showed a slower pace of economic growth in Q1. The 0.5% GDP growth (QoQ) was expected, but down from 0.6%. Together with a strong USD, the New Zealand dollar slipped to its lowest point this year.

- The eco calendar contains US weekly jobless claims, Philly Fed Business Outlook and EMU consumer confidence. UK, Norwegian and Swiss central banks meet. ECB's Nowotny, BdF Governor Villeroy and Bundesbank Weidmann speak

Currencies: Dollar Gets Benefit Of The Doubt As Trade Tensions Linger

Dollar gets benefit of the doubt

Yesterday, trade tensions moved to the background, but the better global risk sentiment didn't help the euro much. The trade war isn't over yet. ECB comments also confirmed the FED/ECB divergence, indicating that the euro won't get interest rate support anytime soon. EUR/USD mostly hovered in the upper half of the 1.15 figure. The pair closed the day at 1.1572 (from 1.1590). The USD/JPY risk rebound was also far from impressive, but the pair finally got some support from a rebound in US yields. USD/JPY finished the day at 110.36 (from 110.06). This morning, markets show a diffuse picture, China and Korea underperforming. At the same time, US equity futures show again modest gains. The trade-weighted dollar tries to regain the 95 resistance area. USD/JPY is trending higher in the 110 big figure. EUR/USD still develops a lacklustre trading pattern (currently 1.1560). New-Zealand Q1 GDP slowed to 0.5% Q/Q, as expected. The ‘soft patch' in the economy reinforces the view that the RBNZ shouldn't be in a hurry to raise rates. NZD/USD dropped below the 0.6850 support area this morning.

Today, the US jobless claims and the Philly Fed business outlook will be published. Markets apparently grow more confident that the trade war won't derail US growth soon. The impact on other regions, including Europe, is more uncertain. If markets continue to play this card, the dollar might get further interest rate support. The next step in the spiral of retaliation between the US and its trading partners might kick in at any time. It might slow the rise of USD/JPY. For the euro, we have the impression that any sustained rebound is difficult for now, whatever the next step in the trade conflict. Policy divergance between the Fed and the ECB hampers a euro rebound, even if risk sentiment improves. Of late, we advocated that a retest of the 1.1510 correction low is possible. We maintain that view. The dollar can stay strong for longer.

Yesterday, the UK government winning the vote on the ‘meaningful vote' didn't help sterling much. The visibility on the next steps in the Brexit process remains very foggy. Today, the focus turns to the BoE policy meeting. Markets will look for an indication on an August rate hike. However, we assume that recent UK data were not strong enough for BoE's Carney to prepare markets already again for a rate hike in August, after he had to backtrack on its guidance for the May meeting. He probably will keep the timing open. We assume more sideways trading in EUR/GBP near the 0.88 pivot

Tradeweighted USD (DXY): USD to prepair a next step higher

EU Malmstrom urges New Zealand to lead by example together on multilateral trade

EU Trade Commissioner Cecilia Malmstrom launched free trade negotiation with New Zealand in Wellington today. Trade negotiation teams from both sides would start the first round of talks in Brussels over July 16-20. Malmstrom said in a press conference after meeting New Zealand trade minister David Parker that "today is an important milestone in EU- New Zealand relations. Together, we can conclude a win-win agreement that offers benefits to business and citizens alike."

She also emphasized that "This agreement is an excellent opportunity to set ambitious common rules and shape globalization, making trade easier while safeguarding sustainable development. We can lead by example."

Malmstrom also hailed New Zealand as "a friend, an ally". And she urged that "together we stand up for common values ... of sustainable trade, open trade, transparent trade, and trade that is done in compliance with international rules in the multilateral system."

The New Zealand government recently launched its "Trade for All Agenda", calling for a "progressive and inclusive" approach to negotiating trade deals. Parker said "we can not only do good for ourselves in this trade agreement but we can actually set out rules for how trading agreements should look for the betterment of the world."

Parker also hailed that Malmstrom has asked negotiators to work through the complicated areas early, so as not to cause delays in the end. He said "I think that demonstrates a willingness on the part of the European side of the negotiation, which we share, to bring this to a conclusion as soon as we can."

Joint press conference of Parker and Malmstrom.

https://www.youtube.com/watch?v=Kvda65RJXTU

USDJPY Recover To Strengthen Above 111.00

The US dollar continues to gain ground against the Japanese yen currency, as global equity markets rebound after Federal Reserve Chair Jerome Powell’s hawkish speech on Wednesday. The USDJPY pair is currently trading around the 110.60 level, as the recovery from the early-week drop to the 109.54 support level gathers pace. Buyers will look for further gains above the 111.00 level, while sellers will try to move price below the key 110.25 level.

The USDJPY pair is strongly bullish while trading above the 111.00 level, further gains towards the 111.39 and 111.70 levels remains possible.

If the USDJPY pair falls below the 110.25 level, sellers will likely test towards the 110.00 and 109.54 levels.

EURUSD Under Pressure Below 1.1554 Level

The euro currency remains under heavy technical selling pressure against the US dollar after the price was strongly rejected from the 1.1600 level on Wednesday. The EURUSD pair has moved back towards critical weekly support around the 1.1554 level, as bearish short and medium-term selling pressure continues to build. Sellers will try to break the 1.1510 level, while buyers will attempt to move the price back above the 1.1600 resistance level.

The EURUSD pair is strongly bearish while trading below the 1.1554 level, key technical support is now located at the 1.1510 and 1.1480 levels.

If the EURUSD pair moves above the 1.1600 level, key technical resistance can be found at the 1.1610 and 1.1644 levels.

Spotlight Shifts To BoE Rate Decision On Thursday

Monetary policy is front and centre on Thursday as the Bank of England (BOE) delivers its latest interest-rate verdict. Although BOE officials are expected to stand pat, the official statement may provide clues about the pace and timing of future policy adjustments.

Action begins bright and early with a Swiss government trade report due for 06:00 GMT. Switzerland's trade surplus is forecast to narrow significantly for May as import growth outpaces exports.

The Swiss National Bank (SNB) will deliver its policy verdict at 07:30 GMT. Interest rates are projected to hold steady at -0.75%.

The Bank of England's Monetary Policy Committee will conclude its meeting in the afternoon local time, giving rise to the official rate statement at 11:00 GMT. A median estimate of economists is forecasting a 7-2 vote in favor of keeping the benchmark interest rate at 0.5% and the size of the asset purchase facility at £435 billion.

Policymakers will likely deliberate about ongoing Brexit talks as Prime Minister Theresa May looks for a clean break out of the European Union (EU). That is proving to be a difficult sell as Brexit talks continue to drag on.

In North America, payrolls processor ADP Inc. will report on Canadian employment for the month of May. ADP's April report showed a monthly gain of 30,200 workers to payrolls.

In the United States, the Department of Labor will release its weekly jobless claims report for the week ended 16 June. The number of Americans filing for first-time unemployment benefits is projected to rise 2,000 to a seasonally adjusted 220,000.

Meanwhile, the Housing Finance Agency will report on home prices at 13:00 GMT. The housing price index is projected to rise 0.3% for April.

Bank of England Governor Mark Carney is expected to deliver a speech late in North American trade. The speech is currently scheduled for 20:15 GMT.

EUR/USD

Europe's common currency rebounded Wednesday from its current brush with yearly lows. After bottoming near 1.1540 on Tuesday, EUR/USD has recovered to around 1.1570. The bulls are capped firmly below 1.1600, with immediate support now located at 1.1536.

GBP/USD

Cable bounced back from seven-month lows on Wednesday, but the upside was severely limited. GBP/USD reached a session high of 1.3209 but was later sent all the way back to the 1.3160 handle, where it now trades. The intraday high from Wednesday is likely to serve as a short-term barrier for price action.

USD/CHF

The trading of USD/CHF has been choppy over the past week as the pair consolidated post-FOMC gains. USD/CHF is currently trading at 0.9965, with the bulls eyeing the psychological 1.000 level as the next major hurdle. On the flipside, near-term support is located at 0.9920.

Turkish Election Represents Market Event Investors Unable To Ignore

In a week where market headlines continue to be driven by a potential trade war breaking out between the United States and China along with the latest OPEC meeting in Vienna, traders are unable to ignore the likelihood that the upcoming weekend election in Turkey could create further volatility in the financial markets.

The Turkish Lira has been in complete freefall in the lead up to the general election scheduled for 24 June, with the currency having lost 25% of its value this year. The rapid depreciation in the Lira has also contributed to a wide range of different emerging market currencies taking a hit, as a result of investors becoming less attracted towards taking on risk. If the Lira does hit the floor once again in the aftermath of the election, it is possible that risk appetite will be threatened, meaning that the emerging markets are in danger of being exposed to further weakness depending on how the market reacts to the outcome.

Concerns that the incumbent President Recep Tayyip Erdogan will exert heavy influence on economic matters and on Turkey's interest rate policy if he wins the election has been the major factor behind the Lira crisis. The currency has hit repeated historic lows over the course of the second quarter. These concerns are still distressing investors, and the Lira at time of writing continues to trade above 4.75 against the Dollar. This is only a marginable distance away from the historic low above 4.90 on 23 May and in spite of the best efforts from the central bank to raise interest rates by 4.25% since this date. The moves from the Turkish central bank to defend the Lira have largely been ignored by investors because they are so distressed that the higher interest rates will only be a temporary measure if Erdogan wins.

The view of Erdogan is that low interest rates will encourage investment into Turkey because investors will become encouraged to take advantage of lower borrowing costs. This view is not economically incorrect, but it also does not fully take into account the dangerous effect the Lira depression is having on the Turkish economy.

Inflation, which is already beyond double-digits is at risk of moving beyond 15% as we enter the third quarter of the year and will have negative ramifications on the cost on the cost of living in Turkey. This will have an impact on disposable income and as a result, reduced consumer sentiment, which will ultimately mean less consumer spending. The Lira crisis will also create havoc with the current account deficit, with Turkey's current debt levels at risk of being increased due to most emerging market debt being priced in Dollars.

The outspoken tone of Erdogan's views on interest rate policy has come at a cost of fears over a serious breach in central bank independence and has resulted in what we are seeing as an extreme loss of confidence in investing in Turkish assets. The market reaction to the potential Erdogan victory over the weekend is still likely not priced into the Lira, suggesting that the currency will face the risk of meeting a new historic low. The Turkish Lira falling below 5 against the Dollar as a result of an Erdogan victory is something that certainly cannot be ruled out of the equation.

My view is that investors have not yet concluded pricing in as much negative news into the Lira as the currency has already received in recent months, because there is no way to truly project what impact the Lira crisis is going to have on the domestic economy over the medium-to-longer term.

If Erdogan does win, as he is expected to do so, investors need to closely monitor how the Lira reacts in case it causes a ripple effect on other global markets. At a time where emerging market sentiment is already in a very fragile state due to the concerns over the resurgence of investor appetite towards buying the Dollar, and President Trump's China trade rhetoric moving to new levels, we can't afford to look at the weekend Turkey election as an idiosyncratic event.

SNB stands pat, raised 2018 inflation forecasts, but lowered 2020’s, full statement

SNB left monetary policy unchanged as widely expected. Sight deposit rate is held at -0.75%. Three-month Libor target range is kept at -1.25% to -0.25%.

SNB also pledge to stand by for intervention and "remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration".

2018 inflation forecast was raised to 0.9%, up from March projection of 0.6%. That's due to a "marked rise in the price of oil".

2019 inflation forecast was kept unchanged at 0.9%. Though, from mid-2019, the new condition forecast is lowered due to "muted outlook in the euro area".

For 2020, inflation forecast was lowered to 1.6%, down from March projection of 1.9%.

All the inflation forecasts were based on assumption the three month Libor remains at -0.75% over the entire forecast horizon.

On global growth, SNB expected economy to continue to grow above its potential. But risks are "more to the downside" due to "political developments in certain countries as well as potential international tensions and protectionist tendencies."

Swiss GDP is projected to growth at around 2% in 208, unchanged. And unemployment is expected to fall further.

Full release below.

Full release below.

Swiss National Bank leaves expansionary monetary policy unchanged

The Swiss National Bank (SNB) is maintaining its expansionary monetary policy, thereby stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB remains at −0.75% and the target range for the three-month Libor is unchanged at between −1.25% and −0.25%. The SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration.

All in all, the value of the Swiss franc has barely changed since the monetary policy assessment of March 2018. The currency remains highly valued. Following the March assessment, the Swiss franc initially depreciated slightly against the US dollar and the euro. However, in light of political uncertainty in Italy, we have since seen countermovement, particularly against the euro. The situation on the foreign exchange market thus remains fragile, and the negative interest rate and our willingness to intervene in the foreign exchange market as necessary therefore remain essential. These measures keep the attractiveness of Swiss franc investments low and ease pressure on the currency.

The new conditional inflation forecast for the coming quarters is slightly higher than it was in March 2018 due to a marked rise in the price of oil; this price rise ceases to affect annual inflation after the first quarter of 2019. From mid-2019, the new conditional forecast is lower than it was in March 2018, mainly due to the muted outlook in the euro area. At 0.9%, the inflation forecast for 2018 is 0.3 percentage points higher than projected at the March assessment. For 2019, the SNB continues to anticipate inflation of 0.9%. For 2020, we expect to see inflation of 1.6%, compared with 1.9% forecast in the last quarter. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon.

Overall, global economic growth was solid in the first quarter. Growth in the US and China was strong and broad-based. The pace of economic expansion slowed in the euro area, however, albeit partly due to temporary factors. The economic signals for the coming months remain favourable. The SNB's baseline scenario therefore assumes that the global economy will continue to grow above its potential.

The risks to the SNB's baseline scenario are more to the downside. Chief among them are political developments in certain countries as well as potential international tensions and protectionist tendencies.

Switzerland's economy continued to recover as expected, with GDP once again growing faster than estimated potential in the first quarter. Overall capacity utilisation improved further on the back of this positive development. The SNB still anticipates GDP growth of around 2% for the current year and expects to see unemployment falling further.

Imbalances on the mortgage and real estate markets persist. While growth in mortgage lending has been only moderate over the last few quarters, real estate prices have continued to rise. Particularly in the residential investment property segment, there is the risk of a correction due to the strong increase in prices in recent years. The SNB will continue to monitor developments on the mortgage and real estate markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.