Sample Category Title

London Gas Oil Futures Hold above Ascending Trend Line; Bearish Correction in Short-Term

London Gas Oil Futures are on course to lose the gains that were posted on Monday as the price is set to complete the second bearish day in a row. The technical indicators, though, continue to send bearish signals, suggesting that the softness in the market is not over yet.

The RSI has fallen below the threshold of 50, indicating that the market could weaken a little bit in the short-term, while the MACD supports a bearish picture as well, since the index continues to increase negative momentum below its red-signal line.

Should prices decline, immediate support could be found around the ascending trend line near the 621.70 barrier. Then a leg below that level, the pair could meet the 600.00 psychological level shifting the bullish picture to negative.

However, if the market manages to pick up speed, the 50-day simple moving average (SMA) at 662.92 could offer nearby resistance. A significant close above the latter would drive the price until the 704.60 resistance, taken from the high on May 17, raising chances for further increases.

In the longer-timeframe, oil has been trading in ascending movement over the last year, but the bullish structure could change if the price drops below the diagonal line.

ECB forum live: Draghi, Powell, Lowe, Kuroda

Policy panel

- Mario Draghi, President, European Central Bank

- Philip Lowe, Governor, Reserve Bank of Australia

- Jerome Powell, Chair, Board of Governors of the Federal Reserve System

- Haruhiko Kuroda, Governor, Bank of Japan (tbc)

Moderator: Stephanie Flanders, Bloomberg Economics

https://www.youtube.com/watch?v=hyLow3nYn_Y

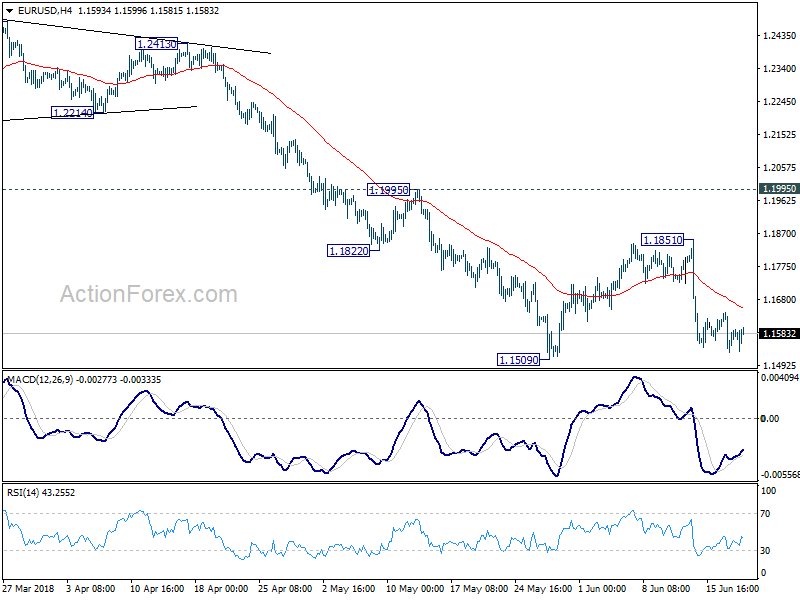

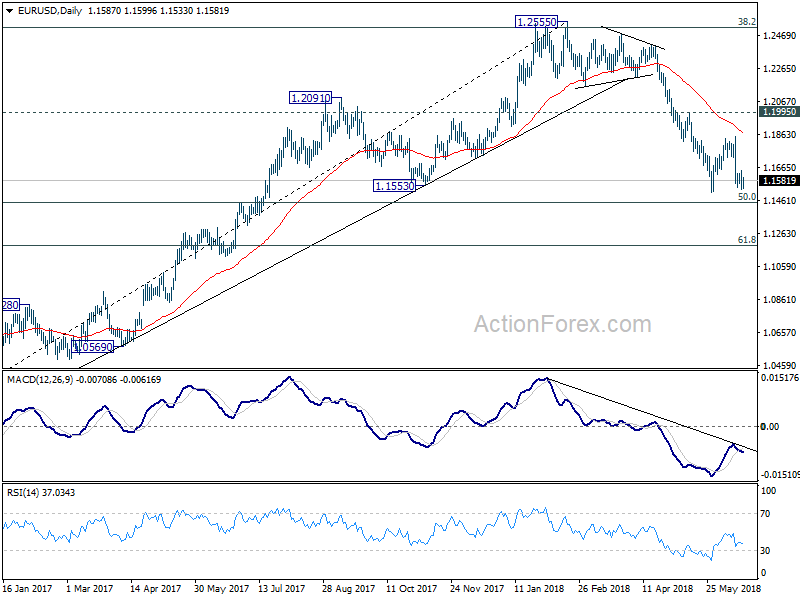

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1532; (P) 1.1589 (R1) 1.1646; More.....

EUR/USD is staying in consolidation and intraday bias remains neutral first. In case of another recovery, upside should be limited below 1.1851 resistance to bring fall resumption. Firm break of 1.1509 will resume larger decline from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

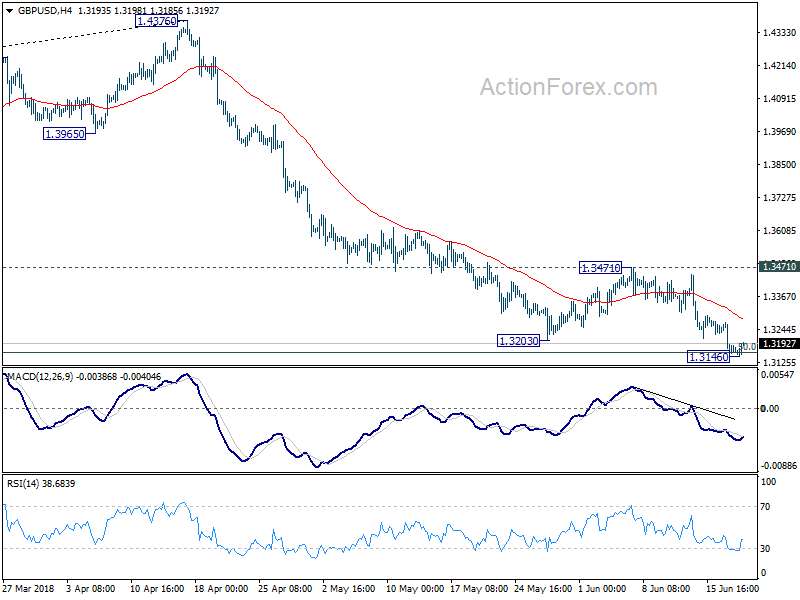

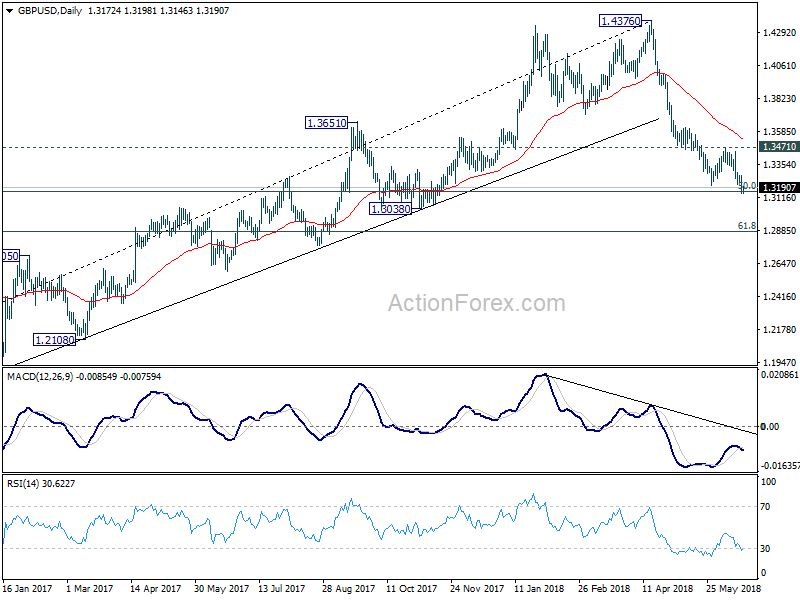

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3125; (P) 1.3199; (R1) 1.3249; More...

A temporary low is in place at 1.3146 after hitting 50% retracement of 1.1946 to 1.4376 at 1.3161. Intraday bias is turned neutral for some consolidations. Recovery should be limited well below 1.3471 resistance to bring fall resumption. Break of 1.3146 will extend the whole decline from 1.4376 to 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

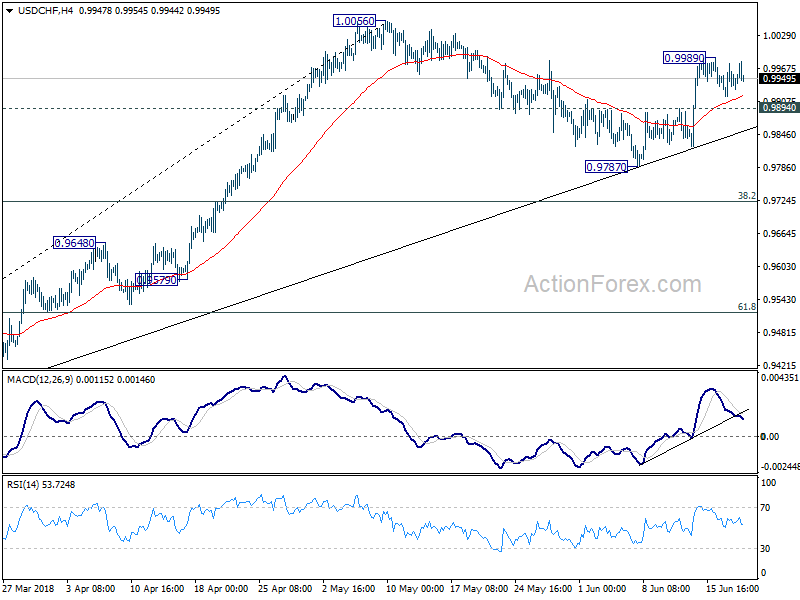

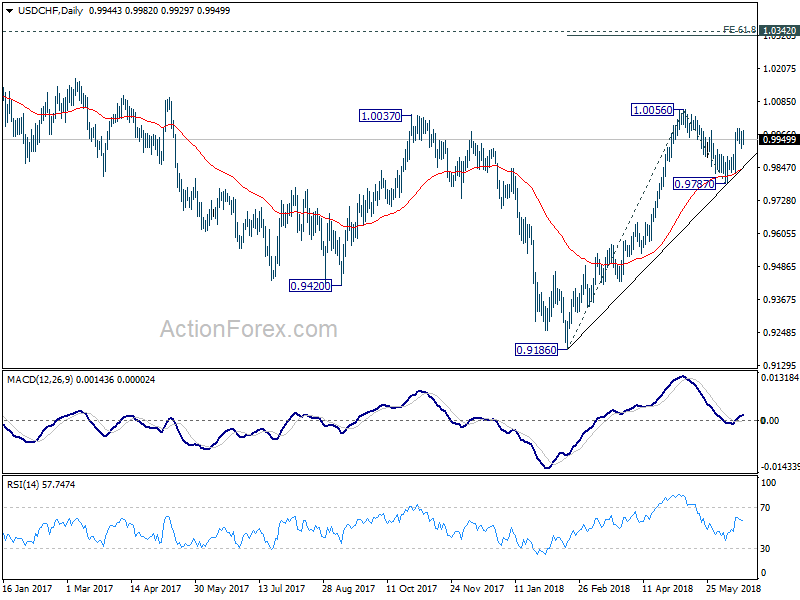

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9913; (P) 0.9945; (R1) 0.9974; More...

Intraday bias remains neutral as consolidation continues below 0.9989 temporary top. Outlook is unchanged that corrective fall from 1.0056 should have completed at 0.9787. Further rally is expected as long as 0.9894 minor support holds. On the upside, above 0.9989 will bring retest of 1.0056 first. Break will resume the rise from 0.9186 and target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, break of 0.9894 will likely extend the correction, possibly through 0.9787 before completion.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

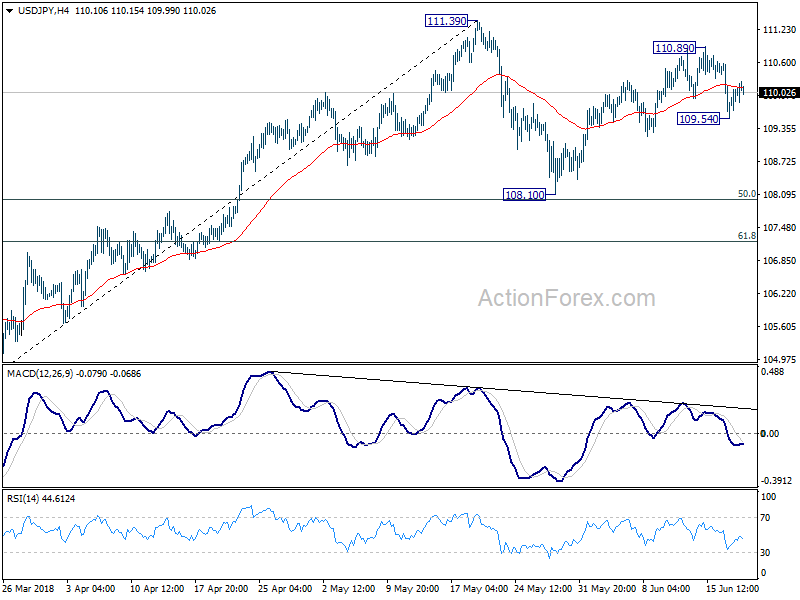

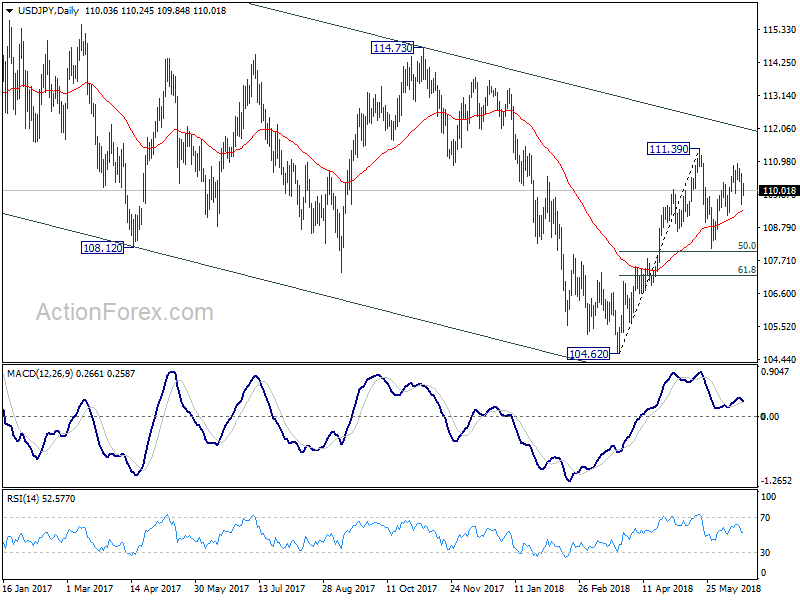

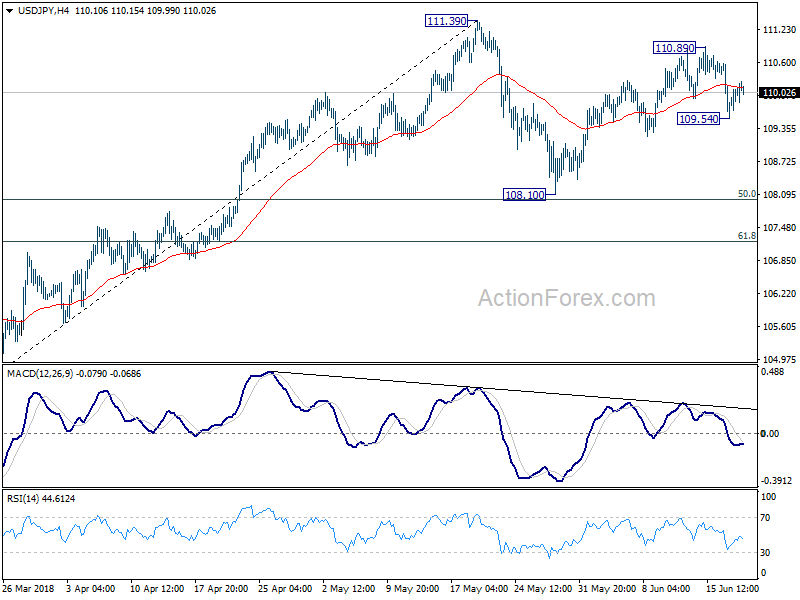

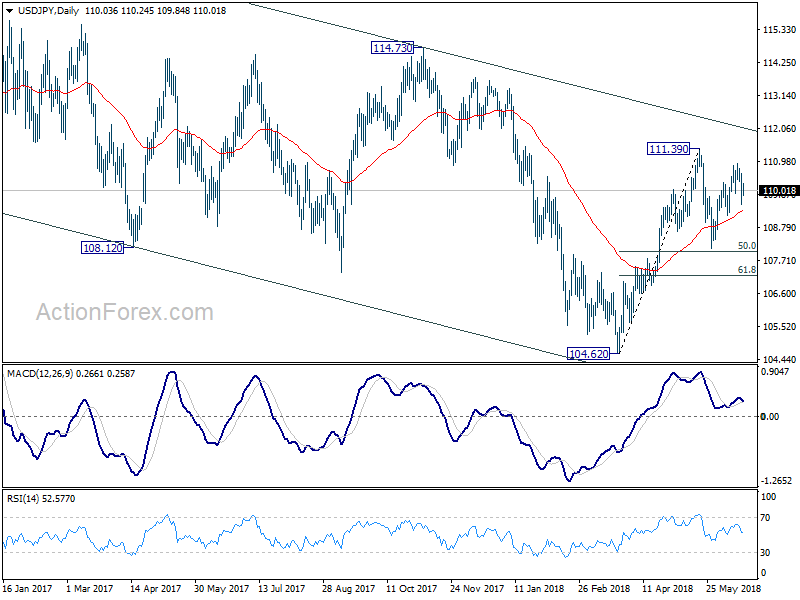

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.54; (P) 110.07; (R1) 110.60; More...

Intraday bias in USD/JPY remains neutral for the moment. We maintain the view that corrective pattern from 111.39 is unfolding with fall from 110.89 as the third leg. Deeper decline is expected and below 109.54 will target 108.10 and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, though, above 110.89 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Forex Markets Calmed in Range, Focus Turns to Central Bankers

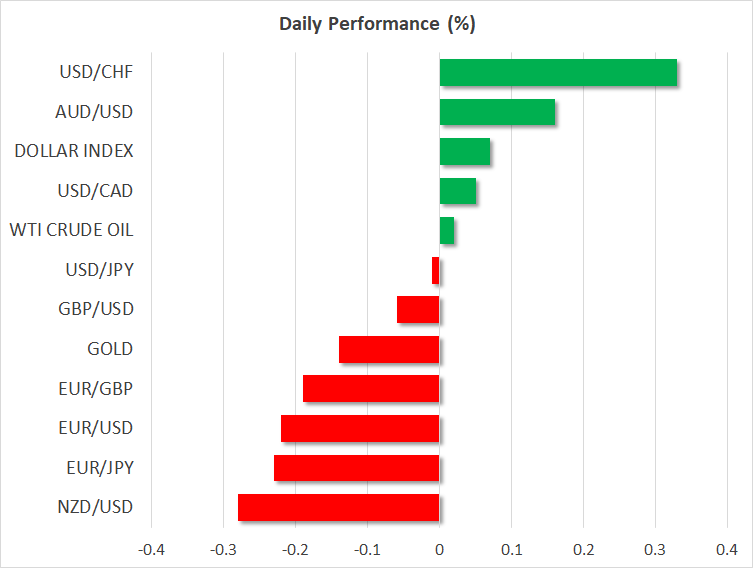

The forex markets are relatively steady today as sentiments stabilized a bit. Yen and Sterling are so far the strongest ones today but for different reasons. The Japanese Yen is digesting this week's strong risk aversion move, and seller could gather much momentum. Meanwhile, Sterling trying to pare back this week's decline as markets await BoE rate decision tomorrow. The more notable move is indeed seen in New Zealand Dollar, which is catching up in the race as the biggest loser this week. AUD/NZD's rebound from 1.0656 support is seen as the main trigger as the selloff in the Kiwi.

In other markets, US futures point to slightly higher open and DOW could have triple digit gain at initial trading. European indices are also mildly higher, with FTSE up 0.9%, DAX and CAC up more than 0.3% at the time of writing. China's Shanghai composite ended 0.27% higher, Nikkei gained 1.24%. WTI crude oil continue to recover and is now at 65.4, awaiting oil inventory and OPEC decision on production raise. Gold, now at 1275, stays weak after this week's sharp decline is struggles to find any moment to regain 1300.

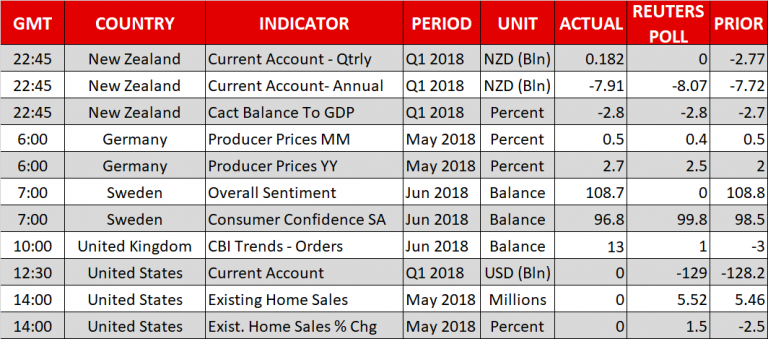

The economic calendar is very light today. US current account deficit widened to USD -124B in Q1. UK CBI trends total orders rose to 13 in June. Germany PPI rose 0.5% mom, 2.7% yoy in May. Australia Westpac leading index dropped -0.2% in May. Focus will turn to a panel discussions of big gun central bankers at the ECB forum, where ECB President Mario Draghi, BoJ Governor Haruhiko Kuroda, RBA Governor Philip Lowe and Fed Chair Jerome Powell are featured.

Technically, Yen remains on the driving seat but it' just awaiting another wave of buying. The step up in trade tensions and verbal attacks between the US and China has taken the Yen so far. Some more inspiration is needed to push the Yen further.

EU to start retaliation on EUR 2.8B US imports on June 22, EUR 3.6B to come later

European Commission formally announced retaliation to US steel and aluminum tariffs today. The total EU exports to the US affected by the US measures is at EUR 6.4B. For now, EU will target US products in EUR 2.8B worth first, effective on Friday June 22. Duties on the remaining EUR 3.6B in US goods will take place at a later stage, "in three years' time or after a positive finding in WTO dispute settlements.

Commissioner for Trade Cecilia Malmström said: "We did not want to be in this position. However, the unilateral and unjustified decision of the US to impose steel and aluminium tariffs on the EU means that we are left with no other choice. The rules of international trade, which we have developed over the years hand in hand with our American partners, cannot be violated without a reaction from our side. Our response is measured, proportionate and fully in line with WTO rules. Needless to say, if the US removes its tariffs, our measures will also be removed."

This is the list of products for rebalancing.

BoJ minutes: Timing of reaching inflation target was merely a projection

BoJ released minutes of the April 26-27 meeting today. The only surprise out of that meeting was that BoJ dropped the time frame it set for achieving the 2% inflation target. The minutes provided more details on the discussions. Many members believed that the timing of reaching the 2% inflation was "merely a projection". At the some time, "some market participants perceived this projection as a deadline for achieving 2 percent inflation, linking changes in said timing to policy adjustments, and this view was deeply entrenched among them."

Some members expressed that "attracting excessive attention merely to forecast figures would not be appropriate from the perspective of communication with the markets". And, most members expressed that " it was appropriate to cease providing a description on the projected timing of achieving the price stability target". And that was with the aim to clarify that the timing was "not a specific deadline" for meeting inflation target. Nonetheless, one member expressed the concern that dropping the time frame could "weaken the effects of the commitment" of BoJ to hit target.

Asian business sentiments deteriorated on trade war risks

Sentiments of Asian Business deteriorated in Q2 according to a survey by Thomson Reuters and INSEAD, over June 1-15. The sentiment index, representing six-month outlook from 61 firms, dropped -5pts to 74 in Q2. It hit a seven-year high of 79 in Q1. That's also the first decline since September 2017 even though reading above 50 still indicates a positive outlook.

Antonio Fatas, a Singapore-based economics professor at global business school INSEAD, said in the released that "Trade war is not a risk but a reality." He added that "U.S. tariffs are going up against China but also against some of its traditional allies, such as Canada and the European Union. They are all about to retaliate and today we do not see an easy way out." Fatas also said "companies can try to go around tariffs by moving production to other countries, this is costly and inefficient. It is a short-term solution but not optimal."

Among responses, worries of global trade war, higher interest rates, rising oil/commodity prices and foreign exchange fluctuation are see as the biggest perceived risks to business outlook.

BoE to stand pat tomorrow, August hike uncertain

BoE will most likely keep the Bank Rate unchanged at 0.50% tomorrow. Known hawks Ian McCafferty and Michael Saunders are expected to vote for rate hike while others would vote for standing pat. There will be no inflation report but just the meeting minutes. And attention will on whether the minutes give any hint on an August hike.

According to the latest Bloomberg survey, only 55% of respondents forecast a hike in August. That's even down from 60% in a similar survey in May. The economists projected UK economy to growth 1.4% in 2018, better than May projection of 1.3%, after some positive economic data. Inflation forecast was unchanged at 2.5% yoy in 2018 and 2.1% yoy in 2019.

One side note to mention is that McCafferty will end his term on August 31. He will be replaced by Jonathan Haskel, an professor of economics at Imperial College Business School. At this point, it's unsure how the replace with reshape the MPC.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.54; (P) 110.07; (R1) 110.60; More...

Intraday bias in USD/JPY remains neutral for the moment. We maintain the view that corrective pattern from 111.39 is unfolding with fall from 110.89 as the third leg. Deeper decline is expected and below 109.54 will target 108.10 and possibly below. But, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, though, above 110.89 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes | ||||

| 00:30 | AUD | Westpac Leading Index M/M May | -0.20% | 0.20% | ||

| 06:00 | EUR | German PPI Y/Y May | 2.70% | 2.50% | 2.00% | |

| 06:00 | EUR | German PPI M/M May | 0.50% | 0.50% | 0.50% | |

| 10:00 | GBP | CBI Trends Total Orders Jun | 13 | 1 | -3 | |

| 12:30 | USD | Current Account Balance Q1 | -124B | -129B | -128B | -116B |

| 14:00 | USD | Existing Home Sales May | 5.55M | 5.46M | ||

| 14:30 | USD | Crude Oil Inventories | -2.1M | -4.1M |

Sterling Ticks Down to Fresh 7-Month Lows ahead of Parliamentary Vote

Here are the latest developments in global markets:

FOREX: In the absence of key data releases, the dollar was trading flat against the safe-haven yen at 110.04 , while the dollar index was also steady at 95.07 as investors were eagerly waiting to see how the tit-for-tat game between China and the US will evolve. The euro continued to struggle for the second day, changing hands lower at 1.1557 (-0.26%), with the European Commission giving its final approval for tariffs to be imposed on imported US goods worth of 2.8 billion euros. The measures will take effect this Friday. Meanwhile, ECB Governing council member Francois Villeroy clarified that there will not be any change in interest rates “until at least summer 2019” as ECB chief, Mario Draghi, messaged yesterday, while ECB member Ewald Nowotny said that euro/dollar could see further depreciation. Pound/dollar remained under pressure, falling to a seven-month low of 1.3146 before it inched up to 1.3180 (-0.07%) ahead of a Brexit vote in the House of Commons later today. If lawmakers favor the changes in May’s Brexit plan, a “hard Brexit” could be accepted by the government if talks fail to progress. Otherwise, a defeat could put May’s leadership at risk again. Euro/pound was down at 0.8784 (-0.13%). In antipodean currencies, aussie/dollar and kiwi dollar were moving in opposite directions. Aussie/dollar improved to 0.7393 (+0.15%) in the absence of any new trade threats, while kiwi/dollar declined to 0.6887 (-0.17%) after Westpac’s Q2 consumer confidence index missed forecasts earlier today. Dollar/loonie recorded a respectable rally for the fourth consecutive day, breaking above the 1.33 key-level before it slid to 1.3295 (+0.10%). China’s yuan managed to advance against the greenback after the People’s Bank of China lowered its midpoint rate per dollar less than analysts forecasted, with dollar/yuan onshore retreating to 6.47 (-0.14%).

STOCKS: European stocks erased part of yesterday’s losses, which were fueled by concerns over the US-China trade spat. The pan-European STOXX 600 and the blue-chip Euro STOXX were up by 0.63% and 0.73% at 1150 GMT, with all sectors being in the green. The German DAX 30 rose by 0.16%, the French CAC 40 climbed by 0.25% and the Italian FTSE MIB jumped by 0.64%. The UK FTSE 100 and the Spanish IBEX 35 posted a stronger rally, surging by 0.75% and 0.97% respectively. In Asia, benchmark stock indices closed in positive territory, while in the US, futures tracking the major stock indices were pointing to a positive open.

COMMODITIES: Oil prices dropped after Iran’s energy minister said that Iran is not in favor of higher oil prices, blaming the US for destabilizing the oil market by intensifying political tensions. However, prices managed to rebound afterwards, with WTI crude and Brent crawling up to $65.21/barrel (+0.22%) and to $75.23/barrel (+0.20%) respectively. Meanwhile, Iran’s OPEC governor expressed that OPEC and its allies should keep the current supply cut deal until the end of 2018 as was initially agreed despite Saudi Arabia and Russia supporting a supply hike.WTI crude and Brent were last seen at $In precious metals, gold eased further to $1,273/ounce as the dollar continued advancing.

Day Ahead: ECB Forum panel discussion attracting attention; US existing home sales on the calendar

Looking at the day’s upcoming events, the US Department of Commerce and the Bureau of Economic Analysis are scheduled to publish current account data at 1230 GMT. Analysts expect the current account deficit to have widened from -$128.2 billion to -$129.0 billion in the first quarter of 2018.

Remaining in the US, at 1400 GMT existing home sales figures for the month of May will be attracting interest. Growth in sales is projected to rebound from -2.8% m/m to 1.5% m/m.

In energy markets, investors will look to the EIA report on US crude oil inventories. According to forecasts, crude inventories are anticipated to drop by 1.898 million barrels in the week ending June 15 compared to a fall of 4.143 million in the preceding week. On the other hand, gasoline inventories and distillate stocks are anticipated to increase.

New Zealand will publish GDP figures for the first quarter at 2245 GMT. Investors will be cautious for any clues that could change RBNZ’s dovish narrative on interest rates. Economic growth is expected to have slowed down further in the first quarter of 2018. Analysts are estimating New Zealand’s economy to have grown by just 0.5% in the three months to the end of March, easing slightly from the previous expansion of 0.6% recorded in the previous two quarters. On an annual basis, GDP is expected to have expanded by 2.7% versus 2.9% in the preceding period.

In terms of public appearances, at 1330 GMT, ECB President Mario Draghi, Fed Chairman Jerome Powell, Bank of Japan Governor Haruhiko Kuroda and Reserve Bank of Australia Governor Philip Lowe will be participating in a panel discussion on central bank policy at the ECB Forum in Sintra, Portugal.

On the political front, in the UK, with no major economic data releases on the agenda, investors are likely to focus on UK politics and the return of the Brexit bill back to the House of Commons at 1830 GMT today.

Pound Wobbles Ahead Of Brexit Showdown In House Of Commons

It has been a terrible trading week thus far for the British Pound, as domestic political risk haunted investor attraction towards the currency.

There was a sense of uncertainty after the government suffered a crushing defeat earlier in the week in a Lords vote to give Parliament a “meaningful vote” on the final Brexit deal. With the European Union Withdrawal Bill returning to the House of Commons today for a second vote, this could be a major leadership test for Prime Minister Theresa May. Another defeat for the government may spark fears over continued political uncertainty in the UK at a time where the Brexit deadline is slowly approaching.

The outlook for Sterling remains tilted to the downside, especially when factoring in how Brexitrelated uncertainty and political risk may force the Bank of England to delay monetary policy normalization this summer.

Regarding the technical picture, the GBPUSD continues to fulfil the prerequisites of a bearish trend on the daily charts. There have been consistently lower lows and lower highs since the middle of April 2018. The solid daily close below 1.3200 could inject bears with enough confidence to confront 1.3130 and 1.3100, respectively. With an appreciating Dollar likely to compound to the GBPUSD’s downside, the outlook for the currency pair remains firmly bearish in the short to medium term.

Global stocks rebound but trade fears linger

Asian and European stocks rose today as markets attempted to shrug off trade war threats. While the improved risk appetite could elevate stock markets higher, the sustainability should be questioned as fears over trade tensions remain a key market theme. Global equity bears could transform the current rebound into a classical dead cat bounce if trade tensions between the United States and China continue to escalate.

Commodity spotlight – Gold

Gold has failed to garner any support from the lingering uncertainty and caution over the simmering trade tensions between the United States and China. Price action suggests that the yellow metal remains heavily pressured by a firmer Dollar and prospects of higher US interest rates. With the Federal Reserve expected to raise rates at least two more times in 2018, zeroyielding Gold may find itself in trouble.

Taking a peek at the technicals, Gold could be gearing for a heavy selloff on the daily and weekly charts. The $1280 level has the ability to transform into a firm resistance that invites a steep decline towards $1264. In an alternative perspective, a rebound and daily close back above $1280 may reopen a path towards $1289 and $1300, respectively.

EU to start retaliation on EUR 2.8B US imports on June 22, EUR 3.6B to come later

European Commission formally announced retaliation to US steel and aluminum tariffs today. The total EU exports to the US affected by the US measures is at EUR 6.4B. For now, EU will target US products in EUR 2.8B worth first, effective on Friday June 22. Duties on the remaining EUR 3.6B in US goods will take place at a later stage, "in three years' time or after a positive finding in WTO dispute settlements.

Commissioner for Trade Cecilia Malmström said: "We did not want to be in this position. However, the unilateral and unjustified decision of the US to impose steel and aluminium tariffs on the EU means that we are left with no other choice. The rules of international trade, which we have developed over the years hand in hand with our American partners, cannot be violated without a reaction from our side. Our response is measured, proportionate and fully in line with WTO rules. Needless to say, if the US removes its tariffs, our measures will also be removed."