Sample Category Title

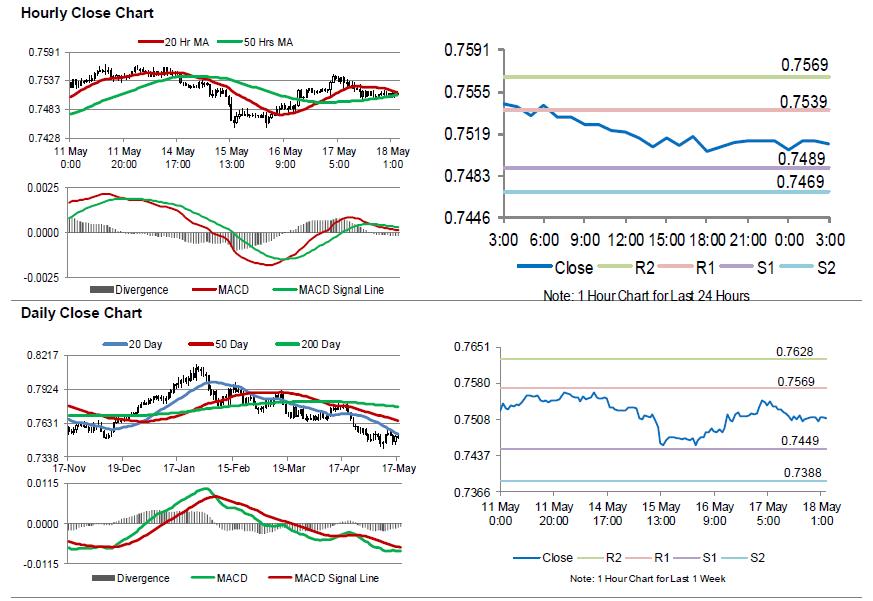

Aussie Trading Slightly Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.12% against the USD and closed at 0.7512.

LME Copper prices rose 0.95% or $ 64.5/MT to $ 6838.0/MT. Aluminium prices declined 1.70% or $39.5/MT to $2280.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7510, with the AUD trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7489, and a fall through could take it to the next support level of 0.7469. The pair is expected to find its first resistance at 0.7539, and a rise through could take it to the next resistance level of 0.7569.

Next week, traders would look forward to Australia’s Westpac leading index and construction work done data.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

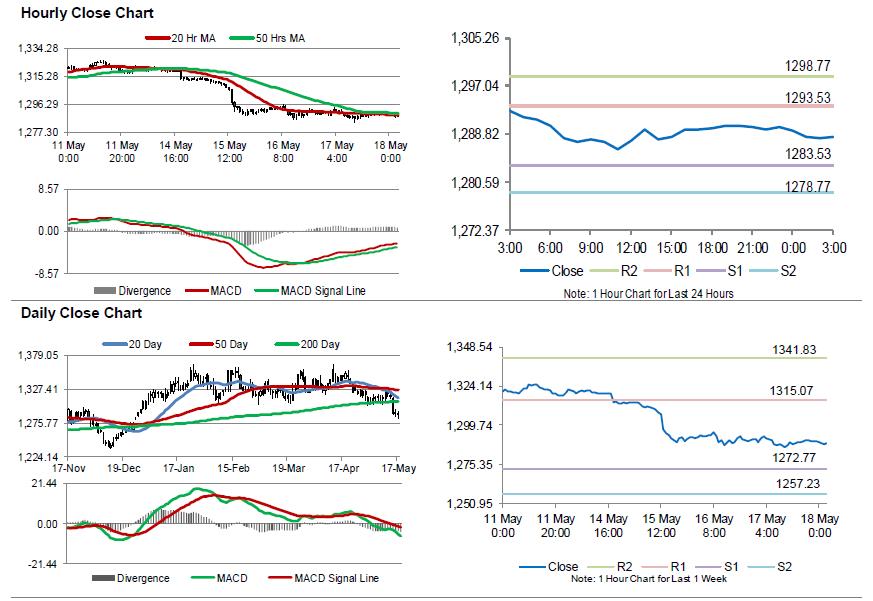

Gold: Yellow Metal Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, Gold declined 0.11% against the USD and closed at USD1289.70 per ounce, as strength in the greenback dented demand for the safe haven asset.

In the Asian session, at GMT0300, the pair is trading at 1288.30, with gold trading 0.11% lower against the USD from yesterday’s close.

The pair is expected to find support at 1283.53, and a fall through could take it to the next support level of 1278.77. The pair is expected to find its first resistance at 1293.53, and a rise through could take it to the next resistance level of 1298.77.

The yellow metal is showing convergence with its 20 Hr and 50 Hr moving averages.

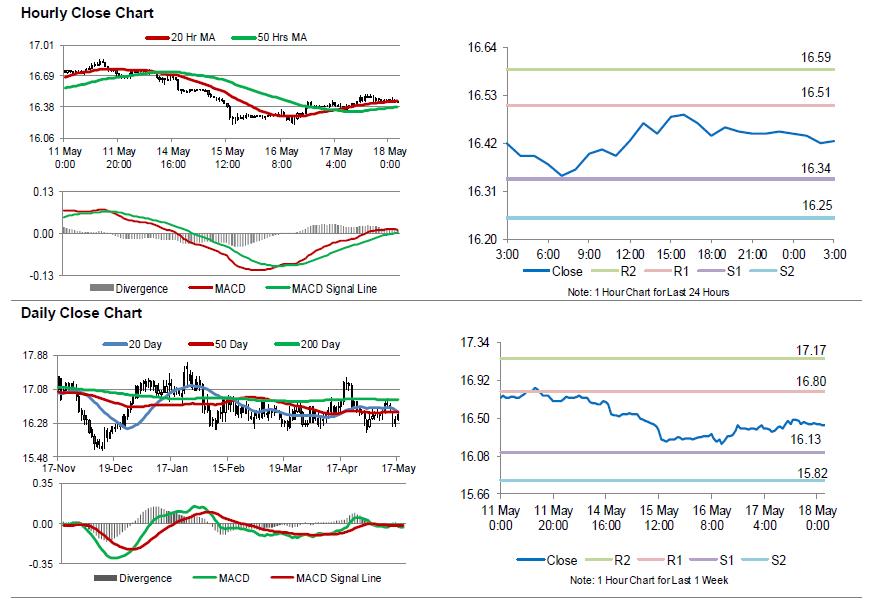

Silver: White Metal Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, Silver rose 0.40% against the USD and closed at USD16.45 per ounce, extending its prior session gains.

In the Asian session, at GMT0300, the pair is trading at 16.43, with silver trading 0.12% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.34, and a fall through could take it to the next support level of 16.25. The pair is expected to find its first resistance at 16.51, and a rise through could take it to the next resistance level of 16.59.

The white metal is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

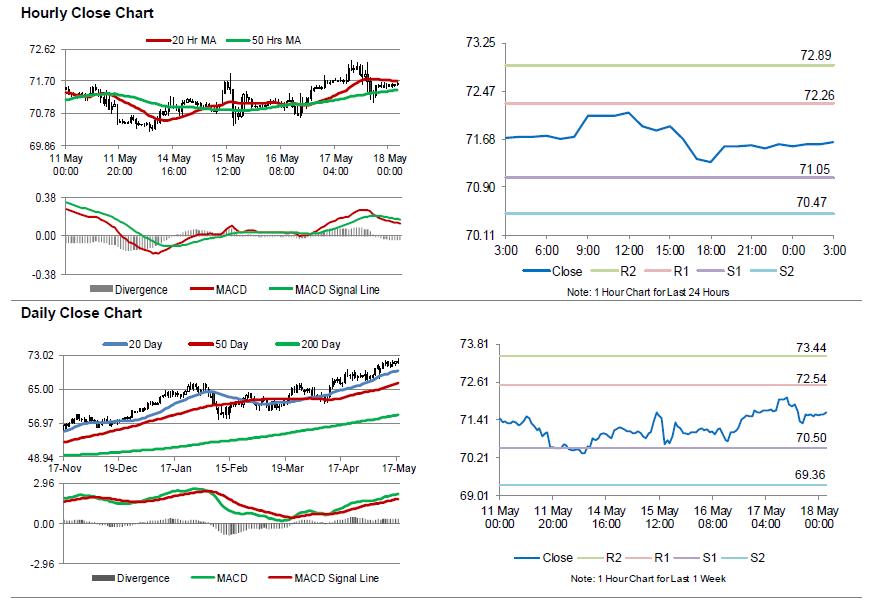

Crude Oil: Oil Extends Its Gains, Ahead Of Baker Hughes Weekly Rig Count Data

For the 24 hours to 23:00 GMT, Crude Oil rose 0.11% against the USD and closed at USD71.60 per barrel, lifted by persistent concerns over potential disruption to global crude supplies.

In the Asian session, at GMT0300, the pair is trading at 71.64, with oil trading 0.06% higher against the USD from yesterday’s close.

The pair is expected to find support at 71.05, and a fall through could take it to the next support level of 70.47. The pair is expected to find its first resistance at 72.26, and a rise through could take it to the next resistance level of 72.89.

Crude oil is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

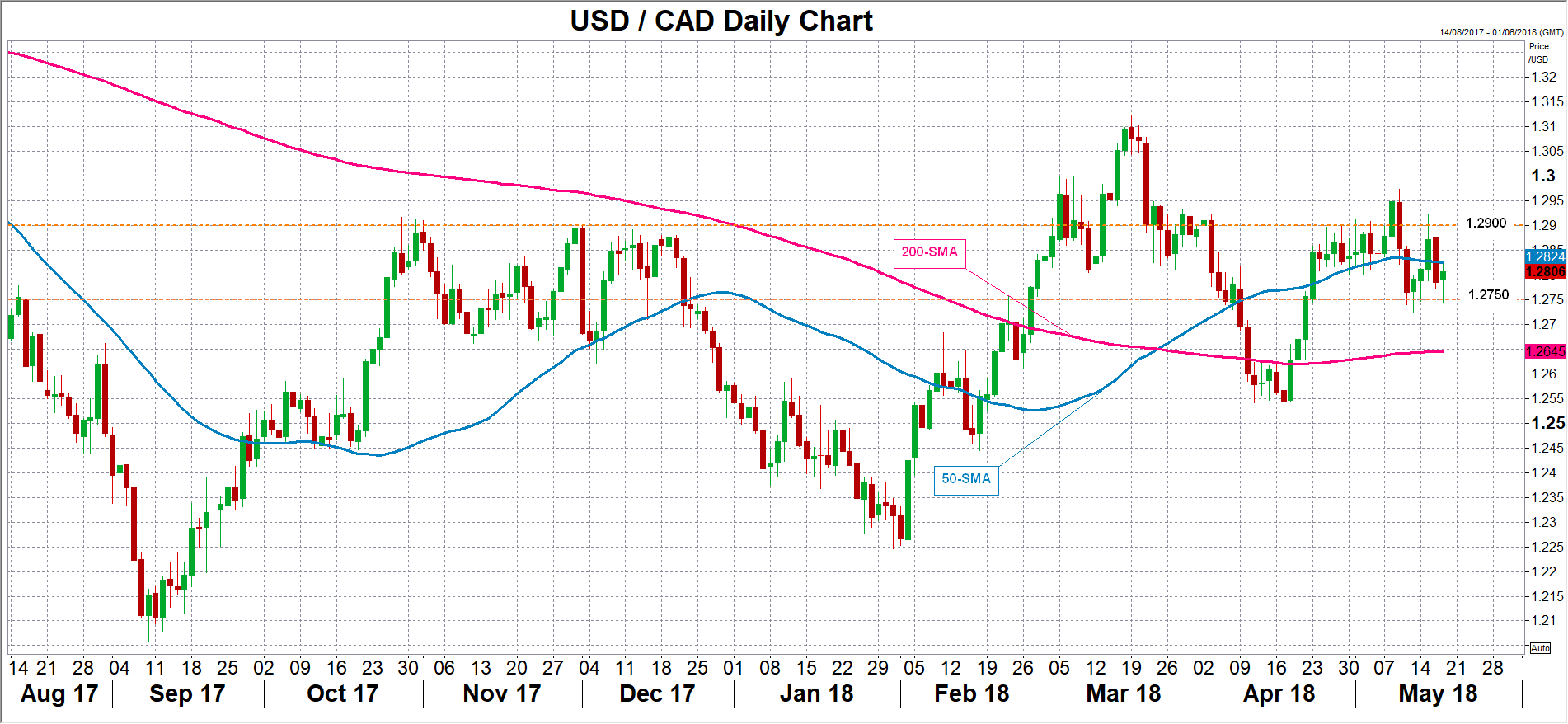

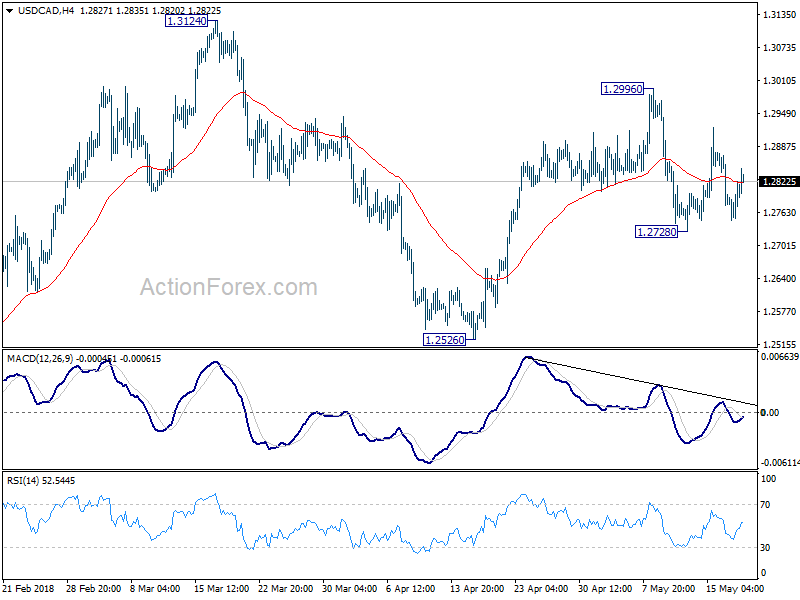

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2760; (P) 1.2794; (R1) 1.2843; More....

Intraday bias in USD/CAD remains neutral for the moment. For now, we're still favoring the bullish case that rise from 1.2061 is still in progress. Above 1.2996 resistance will affirm this view and target 1.3124 and above. However, break of 1.2728 will now dampen our bullish view and turn focus back to 1.2526 support instead.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048

Canadian Dollar Lower on NAFTA Deadlock, Awaits CPI and Retail Sales

Dollar remains the strongest one for the week as supported by treasury yields. 10 year yield extended recent rally to close at 3.109 overnight, and it hits as high as 3.127 in Asian session. 30 year yield also jumped to near 30 year high at 3.246, breaking a key near term resistance at 3.221. Nonetheless, the current round of Dollar buying was mainly centered against Euro and Yen. The greenback remains bounded in established range against other major currencies.

As for today, Canadian Dollar is trading as the weakest one. The May 17 deadline of NAFTA negotiation passed without any progress, and could be no where close to a deal. Canadian Dollar traders also turned a bit cautious ahead of inflation and retail sales data to be featured today. Technically, focus will remain on 1.3450/3607 range edges in GBP/USD, 0.9956/1.0056 range edges in USD/CHF.

EU to use Blocking Statute against extraterritorial effects of US sanctions of Iran

EU leaders showed unity in clashing with US President Donald Trump on preserving the Iran nuclear deal. European Council President Donald Tusk said after the summit in Sofia that "on Iran nuclear deal, we agreed unanimously that the EU will stay in the agreement as long as Iran remains fully committed to it. Additionally the Commission was given a green light to be ready to act whenever European interests are affected."

European Commission President Jean-Claude Juncker added that the "the effects of the US sanctions will be felt" And, "it is the duty of the EU therefore to protect European business and that applies particularly to smaller and medium-size businesses." He also said in strong words that "we will not negotiate with the sword of Damocles hanging over our heads" and "it's a matter of dignity, and it's a matter of principle".

Juncker will begin a legal process to prohibit EU companies to comply with US sanctions on Iran. The "blocking statue" process will begin, accord to Juncker, to "neutralise the extraterritorial effects of US sanctions in the EU". And "we will do it tomorrow [Friday] morning at 10.30." In addition, Juncker said EU "also decided to allow the European Investment Bank to facilitate European companies' investment in Iran"

German Chancellor Angel Merkel noted "All European Union member states are still backing this agreement, despite the fact the United States has decided not to, and we will continue talks with the United States". She added "we can see whether we can give small and medium-sized companies certain relief. That is being examined ... As for compensating all businesses in a comprehensive way for such measures by the United States of America, I think we cannot and must not create illusions."

USTR Lighthizer: Nowhere near close to a NAFTA deal

US Trade Representative Robert Lighthizer poured cold water after the May 17 deadline for NAFTA negotiation passed without breakthrough. He said "the NAFTA countries are nowhere near close to a deal." with "gaping differences" on a number of issues. He pledged to work towards the "best possible deal for American farmers, ranchers, workers, and businesses."

Just hours before Lighthizer's comments, Canadian Prime Minister Justin Trudeau said he was "positive" about NAFTA talks. He said "it's right down to the last conversations. ... I'm feeling positive about this, but it won't be done until it's done."

Mexico's economy minister Ildefonso Guajardo also said a deal could be reached by the end of May. But he didn't rule out extending the talks beyond July 1 Mexican presidential election.

May 17 was a deadline House Speaker Paul Ryan told the NAFTA countries for having the deal approved by the current Congress by the end of this year.

Falls in World Trade Outlook indicator could be linked to increased trade tensions

The World Trade Outlook Indicator of the WTO dropped to 101.8 as of May 17, down from 102.3 back in February.

WTO noted that the value remains "above the baseline value of 100" which suggests "continued solid trade growth in Q2. However, it's "probably at a somewhat slow pace" than Q1.

It also pointed out that the dip in WTOI reflects declines in export orders and air freight. And that "may be linked to rising economic uncertainty due to increased trade tensions."

Japan CPI core slowed to 0.7% yoy, missed expectation

Japan national CPI core, ex-food, slowed to 0.7% yoy in April, down from 0.9% yoy and below expectation of 0.8% yoy. That's the second month of decline and it moved further away from BoJ's 2% target. It's also the lowest level since September 2017 and off recent cyclical high of 1.0% set in February. Overall CPI slowed to 0.6% yoy, down from 1.1% yoy. Ex-food, ex-energy CPI slowed to just 0.4% yoy, down from 0.5% yoy.

Recently, BoJ just dropped the time frame for meeting the 2% inflation target. And it maintained the stance to continue with ultra loose monetary easing. While recent surge in oil price could help lift overall and ex-food CPI ahead, the core-core CPI remained worryingly weak.

Looking ahead

Germany WPI and PPI will be featured in European session. Eurozone will release current account and trade balance. Canadian data is the main focus in US session with CPI and retail sales scheduled.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2760; (P) 1.2794; (R1) 1.2843; More....

Intraday bias in USD/CAD remains neutral for the moment. For now, we're still favoring the bullish case that rise from 1.2061 is still in progress. Above 1.2996 resistance will affirm this view and target 1.3124 and above. However, break of 1.2728 will now dampen our bullish view and turn focus back to 1.2526 support instead.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Apr | 0.70% | 0.80% | 0.90% | |

| 06:00 | EUR | German WPI M/M Apr | 0.20% | 0.00% | ||

| 06:00 | EUR | German PPI Y/Y Apr | 1.80% | 1.90% | ||

| 06:00 | EUR | German PPI M/M Apr | 0.30% | 0.10% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Mar | 35.1B | 35.1B | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 21.1B | 21.0B | ||

| 12:30 | CAD | Retail Sales M/M Mar | 0.40% | 0.40% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Mar | 0.50% | 0.00% | ||

| 12:30 | CAD | CPI M/M Apr | 0.30% | 0.30% | ||

| 12:30 | CAD | CPI Y/Y Apr | 2.30% | 2.30% | ||

| 12:30 | CAD | CPI Core - Common Y/Y Apr | 1.90% | 1.90% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Apr | 2.10% | 2.10% | ||

| 12:30 | CAD | CPI Core - Trim Y/Y Apr | 2.10% | 2.00% |

Japan CPI core slowed to 0.7% yoy, missed expectation

Japan national CPI core, ex-food, slowed to 0.7% yoy in April, down from 0.9% yoy and below expectation of 0.8% yoy.

That's the second month of decline and it moved further away from BoJ's 2% target. It's also the lowest level since September 2017 and off recent cyclical high of 1.0% set in February.

Overall CPI slowed to 0.6% yoy, down from 1.1% yoy. Ex-food, ex-energy CPI slowed to just 0.4% yoy, down from 0.5% yoy.

Recently, BoJ just dropped the time frame for meeting the 2% inflation target. And it maintained the stance to continue with ultra loose monetary easing. While recent surge in oil price could help lift overall and ex-food CPI ahead, the core-core CPI remained worryingly weak.

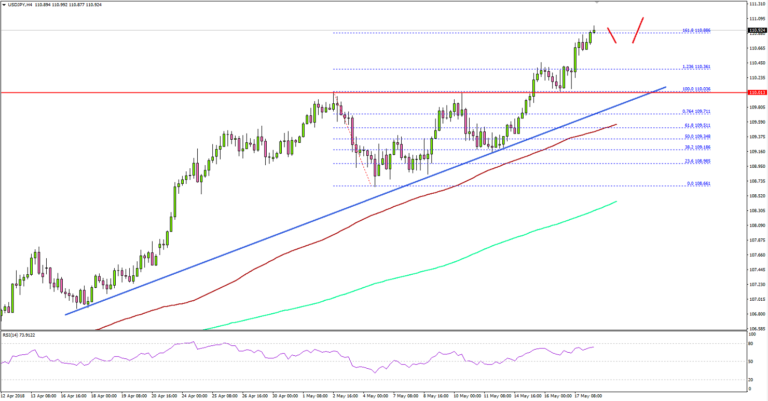

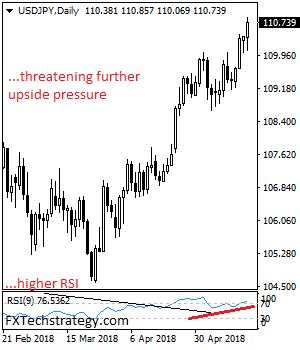

USD/JPY Remains In Crucial Uptrend Above 110.00

Key Highlights

- The US Dollar traded higher this week and settled above 110.00 against the Japanese Yen.

- There is a major bullish trend line forming with support at 109.80 on the 4-hours chart of USD/JPY.

- Japan’s National Consumer Price Index in April 2018 came in at 0.6%, compared with the forecast of 0.7% (YoY).

- The National Consumer Price Index Ex Fresh Food posted 0.7%, less than the last 0.9%.

USDJPY Technical Analysis

The US Dollar started a major upward move from the 109.20 level against the Japanese Yen. The USD/JPY pair traded higher and settled above the 110.00 resistance to set the pace for more gains.

Looking at the 4-hours chart, there is a clear uptrend in place from the 109.00 support zone. The pair followed a bullish path and moved above the 1.236 Fib extension of the last decline from the 110.03 high to 108.66 low.

It settled above 110.00 and is currently poised to extend gains. It even tested the 1.618 Fib extension of the last decline from the 110.03 high to 108.66 low at 110.88.

On the downside, there are many supports around the 110.00 level. There is also a major bullish trend line forming with support at 109.80 on the 4-hours chart of USD/JPY.

Moreover, the 100 simple moving average (4-hour, red) is positioned below the trend line with a bullish angle at 109.50. Therefore, if the pair corrects lower, it is likely to find bids near 110.10, 110.00 and 109.80.

Recently, the US Initial Jobless Claims for the week ending May 12, 2018 was released by the US Department of Labor. The market was looking for a rise in claims from 211K to 215K.

The actual result was disappointing as there was a rise in claims to 222K. The report added that:

The 4-week moving average was 213,250, a decrease of 2,750 from the previous week’s unrevised average of 216,000. This is the lowest level for this average since December 13, 1969 when it was 210,750.

Overall, the US Dollar remains in an uptrend. EUR/USD and GBP/USD pairs are likely to struggle, whereas USD/JPY may continue to rise in the near term.

Economic Releases to Watch Today

- Euro Zone Trade Balance March 2018 – Forecast €20.7B versus €21.0B previous.

- Canadian Consumer Price Index April 2018 (MoM) – Forecast +0.4%, versus +0.3% previous.

- Canadian Consumer Price Index April 2018 (YoY) – Forecast +2.3%, versus +2.3% previous.

- Canadian Retail Sales March 2018 (MoM) – Forecast +0.3%, versus +0.4% previous.

- Canadian Retail Sales ex Autos March 2018 (MoM) – Forecast +0.5%, versus 0% previous.

USDJPY – Bullish, Remains Biased To The Upside

USDJPY - The pair faces further upside threats as it closed higher on Thursday. On the downside, support lies at the 110.00 level where a break if seen will aim at the 109.50 level. A cut through here will turn focus to the 109.00 level and possibly lower towards the 108.50 level. On the upside, resistance resides at the 111.00 level. Further out, we envisage a possible move towards the 111.50 level. Further out, resistance resides at the 112.00 level with a turn above here aiming at the 112.50 level. On the whole, USDJPY faces further upside pressure.

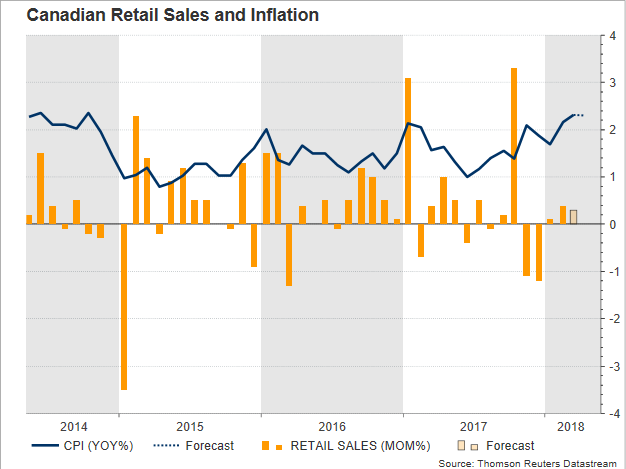

Canadian Inflation To Hold Above 2.0%, Retail Sales To Ease

Canada will see the release of both inflation and retail sales figures on Friday at 1230 GMT, with investors looking eagerly for signs of further economic recovery that could increase chances for a tighter monetary policy this year, given the Bank of Canada’s data dependence. Forecasts are for headline inflation to remain elevated above the mid-point of the BoC target range in April, while retail sales are expected to slip slightly in March. Still, with NAFTA talks on thin ice and household debt at elevated levels, a significant positive surprise may be needed in the data in order to boost the odds for a rate rise at the BoC upcoming policy meeting.

According to analysts, the Canadian headline consumer price index (CPI) is said to have increased by 2.3% y/y in April, the same as in March – the highest growth recorded since October 2014 –, with rising energy prices probably continuing to hold the measure above the 2.0% midpoint of the BoC target range of 1-3.0% on an annual basis. Still, as the BoC Governor Stephen Poloz said recently, a spike above the central bank’s 2.0% mid-point should not warrant a rate hike, as the factors underpinning the measure could be transitory. However, should the numbers surpass forecasts by far, speculation for a rate rise at the end of May could climb, driving the odds of this event above the current 40.83% according to Canadian overnight index swaps. An increase in the core CPI measure, as well as in the inflation gauges utilized by the Canadian central bank (CPI-trim, CPI-median, CPI-common), which trim for volatility and hence help policymakers to have a clear view of how inflation trends look like, could enhance these chances even further.

Regarding Canadian retail sales, businesses in the industry enjoyed a sales growth of 0.4% m/m in February on the back of gains in the car industry; this was the highest expansion since October. In March, though, a decline in demand for vehicles could have pressured the relevant reading, with analysts projecting it to slow down to 0.3% instead. Excluding automobiles, retail sales are projected to have risen by 0.5% m/m after posting no growth in the previous month. Yet, retailers could have done much better if households were less stressed about mounting debt levels. On May 1, Governor Poloz stated that the average Canadian owed $1.70 for every dollar of income earned per year after taxes, with the ratio of debt to disposable income continuing to rise, reaching fresh record high levels. On the other hand, employment stats in March indicated that average hourly earnings picked up from 3.1% to 3.3% y/y and full-time job positions rose at a faster pace.

Besides debt concerns, policymakers should also assess progress in the NAFTA talks before they decide whether to reduce monetary stimulus. But after nine months of talks, the member countries of the free-trade agreement, Canada, Mexico and the US, remain deadlocked on how to deliver an attractive agreement. Time is fast running out as the negotiating teams are rushing to find a common ground by Thursday, a deadline set by the House Speaker Paul Ryan in order for the deal to make it to Congress this year. The US Trade Representative, Robert Lighthizer said on Wednesday, though, that today’s deadline will probably not be met, signaling that conditions could get more complicated ahead of the Mexican presidential elections in July and the US mid-term elections in November. This in return could probably add further pressure to business sentiment and hence put the BoC on hold for longer than expected.

In forex markets, dollar/loonie could lose strength if the data impress – especially on the inflation front – encouraging investors that a BoC rate hike could be on the cards this month, or that the central bank could use a more hawkish tone. However, investors think that policymakers will likely raise borrowing costs in July, with the implied probability by futures markets currently running around 80%, giving some space for trade uncertainties to clear up. In the event of a positive data surprise dollar/loonie could look for immediate support around 1.2750, a frequently tested area. A break below from here could also send the pair down to the 1.2700 round level before the market heads towards the 200-day MA currently at 1.2645.

In the alternative scenario, worse-than-expected numbers could work in favor of the US dollar, driving the price up to the 50-day MA, which fluctuates around 1.2840. Further above, a stronger resistance could come from the 1.2900 psychological level, which has provided resistance several times in the past.