Sample Category Title

High-level conversations still going on NAFTA talks

Several high level Canadian officials are in Washington today to work out a path for NAFTA negotiation ahead. The delegation include Brian Clow, Prime Minister Office's coordinator of US affairs.

Canada's ambassador to the US, David MacNaughton, also said there are high-level conversations going on. He said "we will do an assessment of where are we and is there a chance of pulling all this together in a fairly rapid fashion or not?" He added that "we're pretty close" even though there are still "some tough issues to deal with".

Also MacNaughton noted that the US objective in the talks was to reduce trade deficit. And, "eighty per cent of that deficit has to do with autos. We're that close on autos."

Sunset Market Commentary

Markets

Tensions on core bond markets eased today following a hectic trading week. 5SM and Lega officials confirmed ahead the opening bell that a debt write-off and/or leaving the euro are not part the government’s plans. It’s sufficient to stop the rod on the BTP market for now, but not enough to put the genie back in the bottle. The US Note future stabilized near yesterday’s sell-off low with the US 10-yr yield still above the key 3.07% level. US eco data remain very strong with jobless claims hovering near historically low levels and the Philly Fed Business Outlook confirming that US Q2 GDP growth will be strong after a blip in Q1. Today, it wasn’t sufficient to add another downleg in the US Note future. Higher oil prices, with Brent crude above $80/barrel, also failed to do the trick. The German yield curve bear steepens at the time of writing with yields 0.6 bps (2-yr) to 2.4 bps (30-yr) higher. 10-yr yield spread changes versus Germany range between -2 bps (Portugal) and +1 bp (Italy) with Greece underperforming (+7 bps. The US yield curve steepens with yield changes varying between -1.2 bps (2-yr) and +0.9 bps (30-yr).

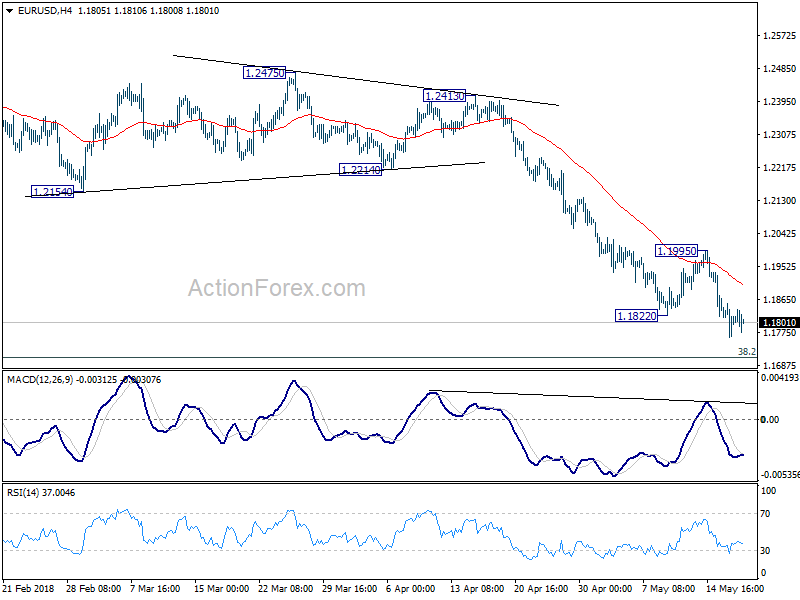

FX trading faced quite some diffuse signals. On the euro side of the story, the 5SM and Lega parties in Italy are still finalizing negotiations to form a new government. Comments from the negotiating parties indicated that the aim for a €250 bln write-down on ECB debt is no longer on the table. Other topics that might potentially unnerve the EU (and markets) will remain in the government agreement. This is still a euro negative. EUR/USD dropped again below the 1.18 mark late in the European morning session. At the same time, US yields are holding at/near cycle peaks. In this respect, the Philly Fed business outlook printed much stronger than expected. For now, the report didn’t widen the interest rate differential between the dollar and the euro. EUR/USD hovers in the 1.18 area. USD/JPY outperforms USD/EUR, trending higher in the 110 big figure (currently 110.75). To summarize: the dollar remains well bid, but the decline in EUR/USD slows as US/EMU interest rate differentials don’t widen any further for now. Euro investors also await the specifics of the Italian government deal.

There were no UK eco data today, but there was again plenty of Brexit noise. Sterling rallied overnight on press reports that Britain was considering to stay in the EU customs union beyond the transition period. This option could also provide a backstop in case no Brexit deal would be reached in time. EUR/GBP dropped to the 0.8715/20 area at the start of European dealings this morning. However, at the EU summit in Sofia, UK PM May repeated that the UK still intends to leave the EU and the customs union. The sterling rally stalled and EUR/GBP settled in a sideways range in the 0.8715/55 area. Cable is holding in the 1.35 area (within reach of recent lows) as the dollar continues to enjoy support from high US yields.

News Headlines

Strong demand and supply cuts led by the OPEC and Russia are fuelling the oil prices’ rally. Brent crude traded temporary above $80 p/b, the highest level since late 2014. WTI Crude, currently near $72, is also trading at a multiyear high.

The Philadelphia Fed Business Outlook came in much stronger (34.4) than expected (21.0). The indicator confirms a strong manufacturing sentiment across the US as the Empire Manufacturing in NY also surprised markets on Tuesday.

PM May’s inner cabinet has agreed on a plan to keep the UK aligned with the EU’s tariff rules for longer, according press rumors. The arrangement is said to be designed to potentially provide more time after the UK’s full departure from the EU/ transition period in 2021 and to break the stalemate on the issue of the Irish border.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1763; (P) 1.1808 (R1) 1.1854; More....

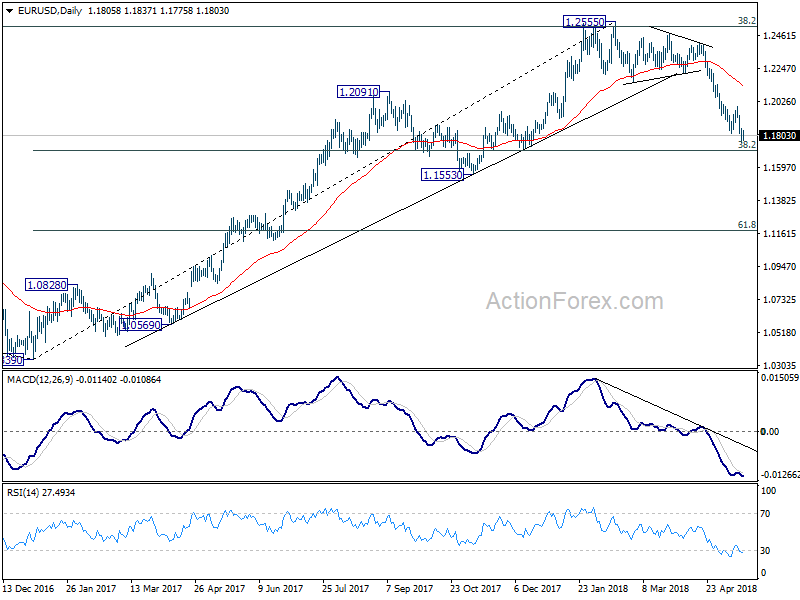

EUR/USD's decline is still in progress and intraday bias remains on the downside for 1.1708 medium term fibonacci level next. Break will target 1.1553 support. On the upside, break of 1.1995 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2162) holds.

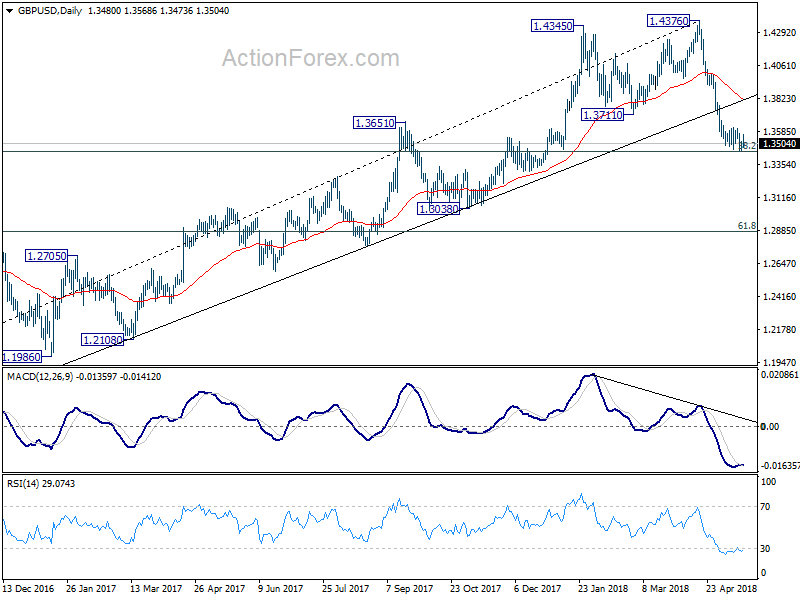

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3451; (P) 1.3495; (R1) 1.3535; More...

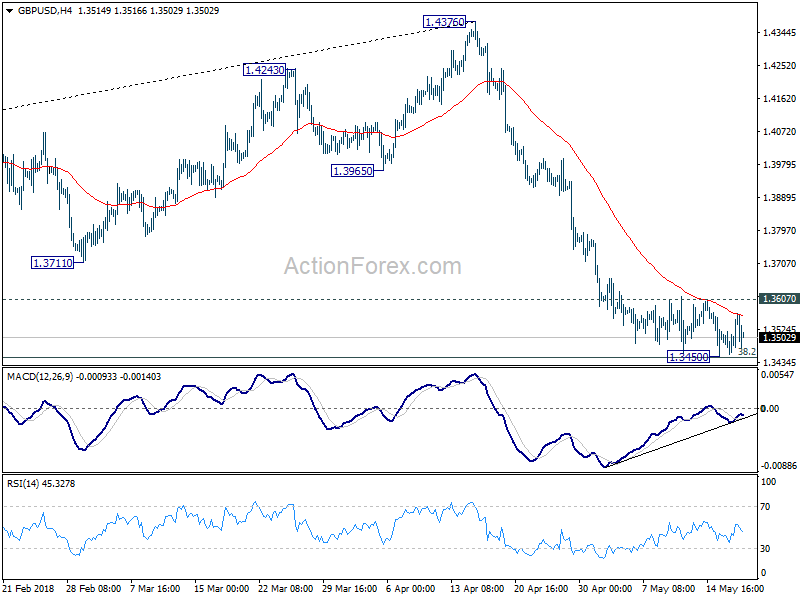

GBP/USD remains bounded in range of 1.3450/3607 and intraday bias stays neutral. Near term outlook will remain bearish as long as 1.3607 minor resistance holds and deeper decline is expected. Firm break of 1.3448 will pave the way to next fibonacci level at 1.2874. However, break of 1.3607 will indicate near term bottoming, with bullish convergence condition in 4 hour MACD. Intraday bias will then be turned back to the upside for 55 day EMA (now at 1.3815).

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 was almost met. Break there will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3815) holds, even in case of strong rebound.

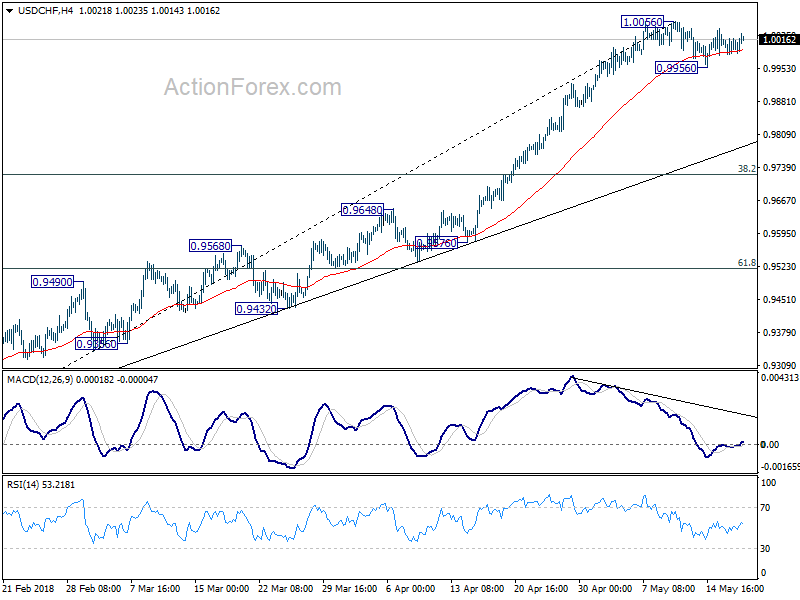

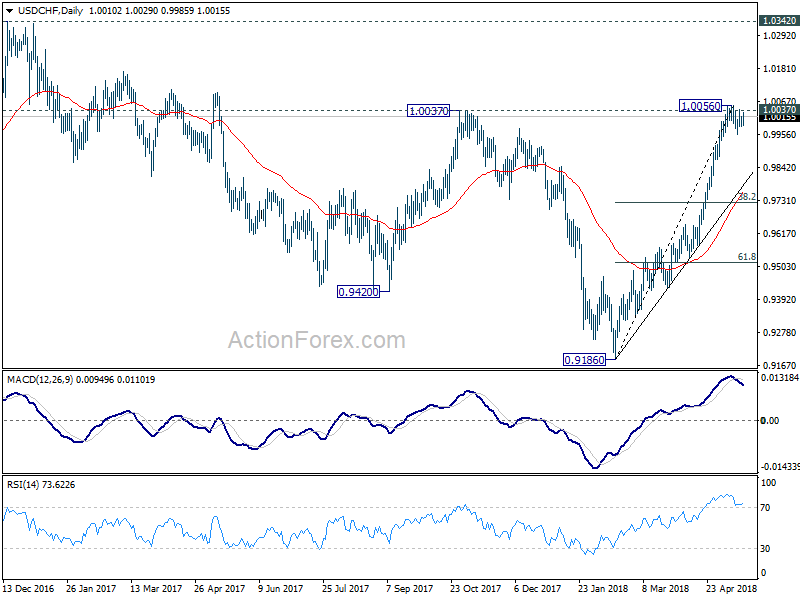

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9990; (P) 1.0005; (R1) 1.0026; More...

Intraday bias in USD/CHF remains neutral as consolidation from 1.0056 is still extending. Another fall cannot be ruled out and below 0.9956 will turn bias to the downside. But in that case, downside should be contained by trend line support (now at 0.9784) to bring rebound. On the upside, sustained break of 1.0037 will resume recent rise for 1.0342 key resistance next.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

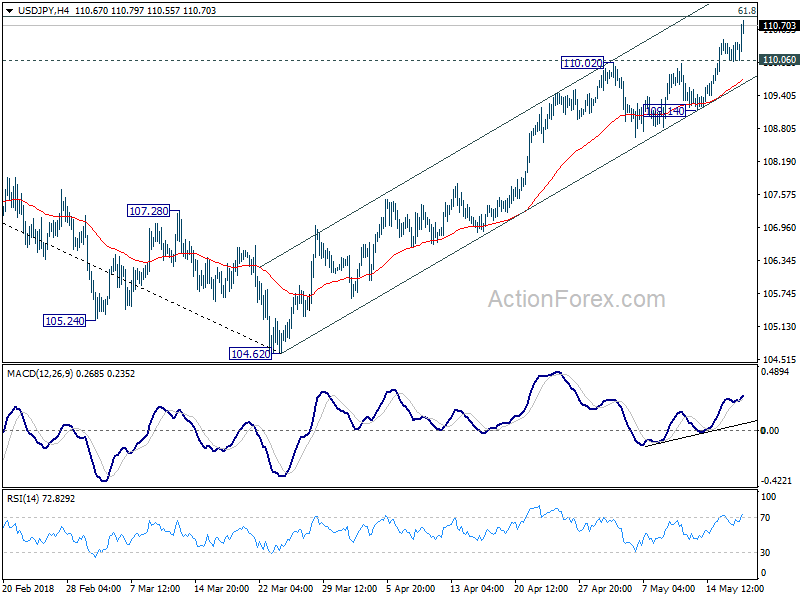

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.16; (P) 110.28; (R1) 110.54; More...

USD/JPY's rally continues today and reaches as high as 110.79 so far. Intraday bias remains on the upside for target 61.8% retracement of 114.73 to 104.62 at 110.86 next. Firm break there will target medium term trend line resistance at 112.43. On the downside, below 110.06 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 109.13 support holds.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.30) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

USDJPY Surges as 10 Year Yield Breaks 3.1, Sterling Pares Gains after May Dismissed Customs Union Stay

Dollar is extending its rally against Yen today, hitting as high as 110.79 so far. Persistent strength in treasury yield is giving the greenback some lift. 10 year yield reached as high as 3.12 earlier today and is staying firm at around 3.1. Nonetheless, while Dollar is firm against Euro, it's staying range bound against Sterling, Swiss Franc, Aussie and Canadian. The focus will now be on whether the strength in Dollar would spread to other pairs.

Meanwhile, Sterling is still the strongest one so far. It was lifted by rumors that UK will stay in the customs union after Brexit. But Prime Minister Theresa May quickly denied the news reports. The Pound just pared back earlier gains after the dismissal. And there was no avalanche selling. Still, focus is back on 1.3448.50 in GBP/USD.

US initial jobless claims rose 11k, continuing claims dropped 45-year low

US initial jobless claims rose 11k to 222k in the week ended May 12, slightly above expectation of 215k. Four week moving average dropped 2.75k to 213.25k, lowest since December 13, 1969. Continuing claims dropped -87k to 1.71m in the week ended May 7, lowest since December 1, 1973. Philadelphia Fed Business outlook rose to 34.4 in May, up from 23.2, better than expectation of 21.1.

From Canada, international securities transactions rose to CAD 6.15b in March.

PM Theresa May cleared the air: "The United Kingdom will be leaving the customs union"

The rumors that UK would stay in the customs union after Brexit triggered a strong rebound in the Pound earlier today. But UK Prime Minister Theresa May was quick to clear up the air.

She said, "No, we are not [climbing down]. The United Kingdom will be leaving the customs union, we are leaving the European Union. Of course we will be negotiating future customs arrangements with the European Union and I have set three objectives; the government has three objectives in those."

"We need to be able to have our own independent trade policy, we want as frictionless a border [as possible] between the UK and the EU so that trade can continue and we want to ensure there is no hard border between Northern Ireland and Ireland."

German Merkel to Trump: Tariff exemptions first, before reciprocal trade talks

Regarding US steel tariffs, German Chancellor Angela Merkel said "we have a common position. We want a permanent exemption and then we are ready to talk how we can reciprocally reduce the barriers to trade." That's seen as having a firm stance as US has to concede the steel tariffs before trade talks. And the talks have to be "reciprocally.

Separately, French President Emmanuel Macron expressed his backing on the proposals by the European Commission to protect European companies affected by US sanctions for Iran. Macron said arriving a summit of EU in Sofia, Bulgaria that EU must stand by smaller companies which were willing to carry on Iran businesses.

He added "international companies with interests in many countries make their own choices according to their own interests. They should continue to have this freedom." "But what is important is that companies and especially medium-sized companies which are perhaps less exposed to other markets, American or others, can make this choice freely."

Australia jobs added 22.6k, participation rate made another record high

Australia employment market grew 22.6k in April (seasonally adjusted), slightly above expectation of 20.0k. Full time employment grew 32.7k while part time jobs dropped -10k. Unemployment rate rose 0.1% to 5.6%, above expectation of being unchanged at 5.5%. Participation rate rose to a further record high of 65.6%. ABS Chief Economist Bruce Hockman said "the labour force participation rate was the highest it has been since the series began in 1978, indicating increasing attachment to the labour force." Also from Australia consumer inflation expectation rose to 3.7% in May.

New Zealand PPI input slowed to 0.6% qoq in Q1 but beat expectation of 0.3% qoq. PPI output slowed to 0.2% qoq, in line with consensus.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.16; (P) 110.28; (R1) 110.54; More...

USD/JPY's rally continues today and reaches as high as 110.79 so far. Intraday bias remains on the upside for target 61.8% retracement of 114.73 to 104.62 at 110.86 next. Firm break there will target medium term trend line resistance at 112.43. On the downside, below 110.06 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 109.13 support holds.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.30) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | 0.60% | 0.30% | 0.90% | |

| 22:45 | NZD | PPI Output Q/Q Q1 | 0.20% | 0.20% | 1.00% | |

| 23:50 | JPY | Machine Orders M/M Mar | -3.90% | -2.80% | 2.10% | |

| 01:00 | AUD | Consumer Inflation Expectation May | 3.70% | 3.60% | ||

| 01:30 | AUD | Employment Change Apr | 22.5k | 20.0k | 4.9k | -0.7k |

| 01:30 | AUD | Unemployment Rate Apr | 5.60% | 5.50% | 5.50% | |

| 12:30 | CAD | International Securities Transactions (CAD) Mar | 6.15B | 3.00B | 3.96B | 4.32B |

| 12:30 | USD | Initial Jobless Claims (MAY 12) | 222K | 215K | 211K | |

| 12:30 | USD | Philadelphia Fed Business Outlook May | 34.4 | 21.1 | 23.2 | |

| 14:00 | USD | Leading Index Apr | 0.40% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 89B |

US initial jobless claims rose 11k, continuing claims dropped 45-year low

US initial jobless claims rose 11k to 222k in the week ended May 12, slightly above expectation of 215k. Four week moving average dropped 2.75k to 213.25k, lowest since December 13, 1969. Continuing claims dropped -87k to 1.71m in the week ended May 7, lowest since December 1, 1973.

Philadelphia Fed Business outlook rose to 34.4 in May, up from 23.2, better than expectation of 21.1.

From Canada, international securities transactions rose to CAD 6.15b in March.

US – China Trade Talks in Focus, Gold Hammered

Asian stocks closed mostly mixed, while European shares have struggled for direction ahead of today’s high-level trade talks between the US and China.

Global sentiment could receive a boost if there are any signs of the two sides finding a middle ground through trade negotiations. While another “no deal” scenario has the potential to negatively impact risk appetite, ongoing talks between the US and China could continue to soothe concerns of a potential global trade war.

Dollar bulls unstoppable

Heightened market expectations of higher US interest rates this year have ensured Dollar strength remains a dominant market theme.

The combination of positive domestic economic data, rising US bond yields and speculation of higher rates have elevated the Dollar to its strongest levels in five months. Price action suggests that bulls are clearly back in town, with further upside on the cards as the interest rate differentials continue to favour King Dollar.

Focusing on the technical picture, the Dollar Index is firmly bullish on the daily charts, as there have been consistently higher highs and higher lows. A breakout above 93.50 could encourage an incline higher towards 94.00 and 94.20, respectively. Alternatively, a failure for bulls to keep prices above 93.50 could encourage a decline towards 93.00.

Commodity spotlight – Gold

After over four months bouncing within a wide $60 range, Gold has finally broken below the $1300 psychological support level this week.

The primary culprit behind Gold’s steep decline could be growing expectations over the Federal Reserve potentially raising US interest rates four times this year. An aggressively appreciating Dollar has also left Gold vulnerable to steep losses, with prices sinking towards a fresh yearly low at $1285 as of writing. With appetite for the zero-yielding metal at risk of eroding in a high-interest rate environment, further losses could be on the cards.

Taking a look at the technical picture, bears won the tug of war following the breakdown and daily close below the $1300 support level. Previous support could transform into a dynamic resistance that encourages a decline towards $1280.

Currency spotlight – EURUSD

The Euro has been hammered by political uncertainty in Italy while a strengthening Dollar continues to rub salt in the wound. This has been an incredibly bearish trading week for the EURUSD, which dipped to a fresh 2018 low of 1.1763 on Wednesday. Taking a look at the technical picture, the EURUSD fulfils the prerequisites of a bearish trend, as there have been consistently lower lows and lower highs. Previous support around 1.1800 could transform into a dynamic resistance that encourages a decline towards 1.1720.

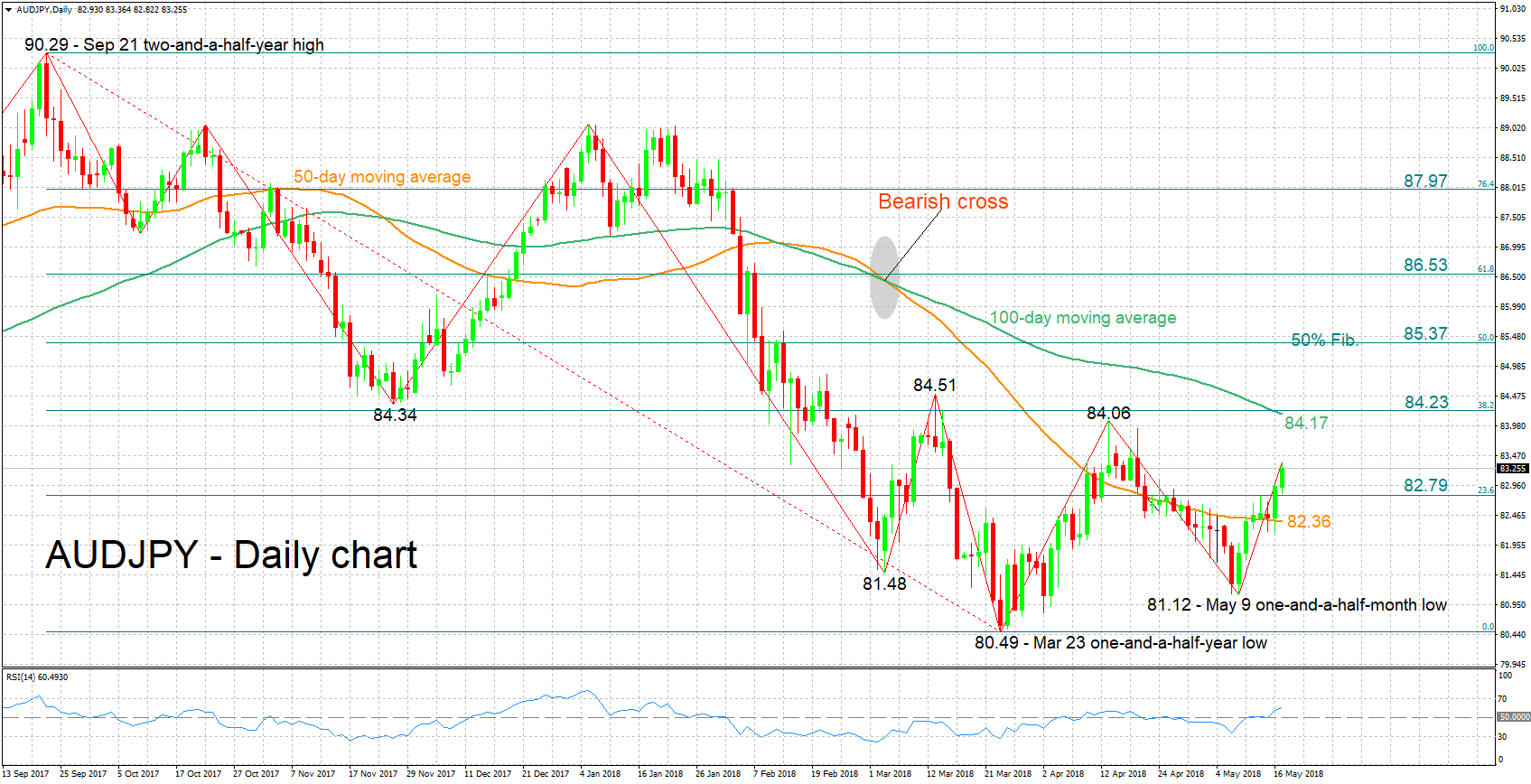

AUDJPY Hits 4-Week High; Looking Neutral in the Medium Term

AUDJPY posted a four-week high of 83.36 earlier on Thursday, while it is currently trading not far below that peak.

Indicative of the positive momentum is the fact the pair finished higher in five of the last six trading days, while it is looking set for a positive close today as well. Adding to the view for a positive short-term bias is the RSI indicator which is in bullish territory above 50 and continues to rise.

Resistance to further gains might come around the 38.2% Fibonacci retracement level of the September 21 to March 23 downleg at 84.23. The region around this level includes the 84 round figure, as well as the current level of the 100-day moving average and a few tops and bottoms from the past. Stronger bullish movement would increasingly start bringing into focus the 50% Fibonacci mark at 85.37.

On the downside, support could be met around the 23.6% Fibonacci level at 82.79 – including the 83 handle – and further below from the area around the current level of the 50-day moving average at 82.36.

In terms of the medium-term outlook, a bearish cross was recorded in early March when the 50-day MA moved below the 100-day one. However, the price crossing above the 50-day MA recently and being roughly equidistant from the current levels of the 50- and 100-day MAs at the moment, is on balance projecting a mostly neutral medium-term picture.

Overall, the short-term bias is looking bullish and the medium-term looks predominantly neutral.