Sample Category Title

Canadian Dollar Steady Ahead of Canadian, U.S Job Reports

The Canadian dollar is steady in the Thursday session, after posting gains on Wednesday. Currently, USD/CAD is trading at 1.2778, down 0.10% on the day. In economic news, Canada releases Foreign Securities Purchases and ADP Nonfarm Employment Change. In the U.S, the Philly Fed Manufacturing Index is expected to drop to 21.2, while unemployment claims are forecast to rise to 216 thousand.

Negotiations over a new NAFTA agreement have failed to reach a conclusion, and the parties haven’t even reached an ‘agreement in principle’. Although there is no official deadline to wrap up a deal, there are upcoming events which could mean that a deal won’t be made in 2018. Mexico holds general elections in June and the U.S holds congressional mid-term elections in November. Meanwhile, the Trump administration has given both Canada and Mexico another 30-day exemption on steel and aluminum tariffs, lasting until June 1. Earlier in the week, U.S Commerce Secretary Wilbur Ross said that further extensions could be granted, depending on the progress made in the NAFTA talks. Ottawa has demanded “full and permanent” exemptions from the tariffs, but may have to cough up more concessions in the NAFTA talks in order to convince Washington to exempt Canadian steel and aluminum imports from tariffs.

The U.S economy continues to perform well, but the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%, and the US dollar could continue to make broad gains as we get closer to the June policy meeting.

US Treasury Yields Lead Dollar Versus Yen To 4-Month Highs

Here are the latest developments in global markets:

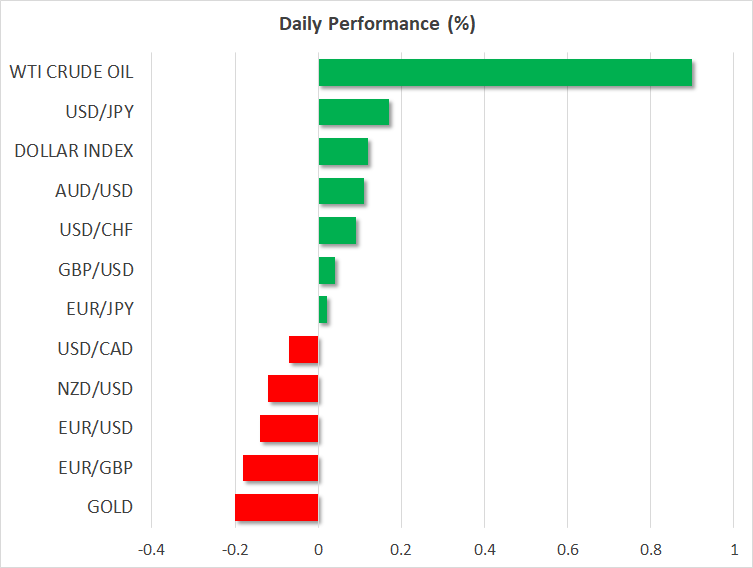

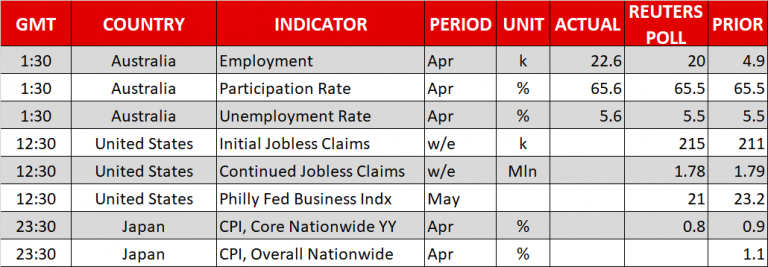

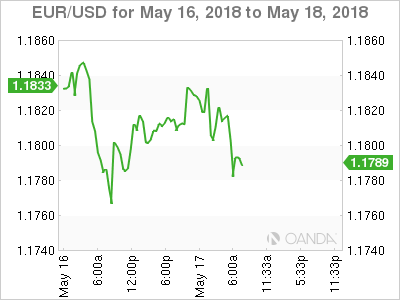

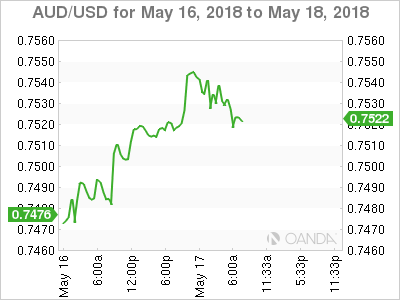

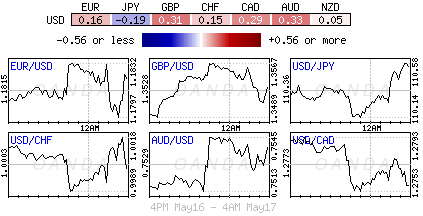

FOREX: The US dollar is set to extend its gains for the fourth day in a row against the Japanese yen (+0.25%). The pair posted a fresh 4-month high of 110.73 during the early European session as the long-term US Treasury yields continued to rally, touching 3.12%, the highest level reached since 2011. The US dollar index tried to create further gains, moving higher by 0.03%. Euro/dollar fell by 0.14% so far on the day and is approaching the 5-month low of 1.1762, achieved on Wednesday. The pair is affected by political uncertainty in Italy, as parties are trying to create a common platform to lead the next government. Sterling gained 0.06% versus the greenback after the announcement of Prime Minister Theresa May that the UK could stay in customs union after Brexit. Antipodean currencies traded mixed on Thursday, while the Australian jobs data drove the aussie/dollar higher by 0.11% as the employment market grew by 22.6k in April, slightly above expectation of 20.0k. However, the unemployment rate rose by 0.1 percentage points to 5.6% from 5.5% before. Kiwi/dollar traded 0.10% lower, having started the day in positive territory as the country’s Labour-led government forecasted a larger surplus for the year ending June. Dollar/loonie declined by 0.16% to 1.2765.

STOCKS: European equities were mostly in the green at 1030 GMT. The pan-European STOXX 600 was up by 0.15%, while the blue-chip Euro STOXX 50 was down by 0.06%. The German DAX 30 rose by 0.21%, the British FTSE 100 climbed by 0.13%, while the Spanish IBEX 35 jumped by 0.22%, set to post a green day after three consecutive sessions. On the other hand, the Italian FTSE MIB declined by 0.25%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in negative territory, pointing to a lower open today.

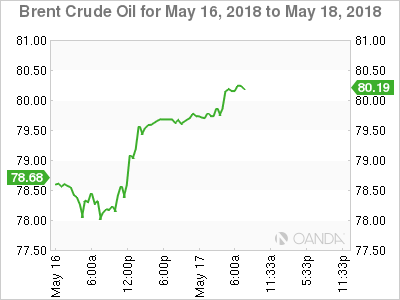

COMMODITIES: Oil prices reached their highest level since November 2014 on Thursday. WTI crude oil jumped above the $72 handle, adding 1.01% to its performance, while Brent crude flirted with $80 level, rising by 0.87%. The prospects of a drop in oil exports by Iran in the next few months due to new US sanctions after President Donald Trump decision to leave the 2015 Iranian nuclear deal has lifted oil prices in the previous sessions. In precious metals, gold posted further declines (-0.19%), creating a fresh 5-month low of $1,286 on Wednesday.

Day ahead: Brexit & Italian political developments in the spotlight

As the day goes on, the focus will remain on the political front as upcoming economic releases scheduled for today have relatively limited potential to move the markets. Moves in US treasury yields, which jumped back above the 3.0% psychological level this week, could be eyed as well.

Particularly, the political situation in Italy is likely to keep investors cautious on the euro on concerns that the two populist parties, the anti-establishment Five-Star Movement and the right-wing League, who are said to be near signing a coalition deal, could propose ideas against Eurozone’s budget program. Yesterday, media reports stated that the Eurosceptic parties are planning to ask for a 250 billion euros debt write-off from the ECB. Although the League party, which still wants Italy to leave the euro, dismissed those leaks later on, talks around a potential debt forgiveness continue to weigh on traders’ confidence.

Meanwhile in the UK, news that the British government is preparing to remain in the EU’s custom union beyond 2021 continued to spur buying pressures in the pound market even after the UK Prime Minister said today that the “UK will be leaving the customs union”. Note that the transitional period agreed between the UK and the EU expires in December 2020 and an extension of this deadline must be agreed between the sides before the submission of a final withdrawal bill, probably in October. Moreover, PM May, who is scheduled to meet the President of the European Council Donald Tusk today could seek to clarify her Brexit plans before June’s EU summit.

Developments around the 2015 Iranian nuclear deal could also be under the spotlight after the French President Emannuel Macron said on Thursday that the European Union should protect business with Iran if the US reimposes sanctions on the oil-exporting nation.

As of today’s data releases, US initial jobless claims, and Philadelphia’s Fed Business index will come into view at 1230 GMT, while at 2330 GMT national CPI readings out of Japan will be under review.

In terms of public appearances, the ECB Vice President Vitor Constancio will be speaking at the third annual ECB macroprudential policy and research conference at 1200 GMT. Minneapolis and Dallas Fed Presidents, Neel Kashkari and Robert Kaplan, will be also delivering comments at 1445 GMT and 1730 GMT respectively; neither holds voting rights within the FOMC in 2018. A meeting between the US President Donald Trump and NATO Secretary General Jens Stoltenberg in Washington to discuss on Israel, Iran, Syria and North Korea is also expected to attract interest.

Retail giant Walmart will be releasing its quarterly results before today’s opening bell on Wall Street.

DAX Steady As Investors Look For Cues

The DAX has posted slight gains and pushed above the symbolic 13,000 level in the Thursday session. Currently, the DAX is at 13,025, up 0.22% on the day. On the release front, there are no German or eurozone indicators on the schedule. On Friday, Germany releases inflation reports and the eurozone publishes current account and trade balance.

The eurozone economy has performed well in 2018, but inflation has lagged behind and remains well below the ECB inflation target of around 2 percent. German Final CPI for April dropped to a flat 0.0%. Although this matched the forecast, this marked a 3-month low. Eurozone inflation indicators followed a similar trend, losing ground in April. Final CPI edged lower to 1.2%, down from 1.3% a month earlier. Final Core CPI followed a similar trend, dropping from 1.0% to 0.7%. Weak inflation levels could have a significant impact on ECB fiscal policy, as policymakers may have to consider extending its stimulus scheme, which is scheduled to run until September.

The DAX hasn't been making headlines, but the index continues to gain ground. The DAX touched the 1350 line earlier on Thursday, marking its highest level since late January. Investors continue to give a thumbs-up to the robust German economy, but there are some clouds on the horizon. A growing concern is the rising price of crude, which remains above the $70 level. Higher oil prices could trigger higher inflation and hamper economic growth, which could send the markets lower.

Dollar Consolidates Ahead Of Today’s Event Risk

Thursday May 17: Five things the markets are talking about

Italian political uncertainty continues to dominate European domestic asset prices.

Since yesterday, Italian bond yields have ballooned on reports of a draft government program, penned by the proposed populist coalition, the introduction of procedures within the eurozone to allow countries to quit the euro. The draft copy indicated that Italy would ask the ECB to write off €250B of government debt.

For Euro supporters, the 5-Star Movement and League have said that their most recent discussions did not put Italy's membership in the common currency into question.

Elsewhere, the U.S 10-year note yields have extended their advances, rallying through the key resistance at +3.1% as investors continue to adjust to an upbeat outlook for the world's largest economy.

That aside, most of the markets efforts is now focused on trying to second-guess issues stretching from peace on the Korean peninsula to Italian populists forming a government and Sino-U.S trade talks in Washington today.

On tap: U.S jobless claims are due at 08:30 am EDT, while Chinese Vice-Premier Liu is expected in Washington for more trade talks.

1. Stocks gain some traction

In Japan, the Nikkei share average advanced overnight, following Wall Street, with financial stocks rallying on an increase in sovereign bond yields while tech shares attracted buyers after the yen (¥110.66) weakened. The Nikkei ended +0.5% higher, while the broader Topix gained +0.4%.

Down-under, Australian shares ended lower on Thursday as the country's second largest bank went ex-dividend, though gains in materials and energy sectors helped limit the overall losses. The S&P/ASX 200 index closed -0.2% lower, the weakest level in over a week. In S. Korea, doubts on a N. Korea/U.S summit occurring have pressured stocks. The Kospi closed down -0.5%.

In Hong Kong, the benchmark stock index fell overnight as investors turned cautious as the U.S/China are set to resume trade talks today. The Hang Seng index fell -0.5%, while the China Enterprises Index lost -1.3%.

In China, stocks also fall on caution as Sino-U.S trade talks resume. The blue-chip CSI300 index fell -0.7% while the Shanghai Composite Index lost -0.5%.

In Europe, regional bourses trade mostly higher with a rebound in Italian stocks as well as talk the U.K plans to stay in the customs union after Brexit is helping to provide positive momentum.

U.S stocks are set to open in the ‘red' (-0.2%).

Indices: Stoxx600 +0.1% at 393.4, FTSE flat at 7732.4, DAX +0.1% at 13004, CAC-40 +0.3% at 5583, IBEX-35 +0.4% at 10152, FTSE MIB +0.5% at 23851, SMI -0.3% at 8948, S&P 500 Futures -0.2%

2. Oil nears $80, gold prices lower

Oil prices have hit their highest level in four-years in the Euro session, with Brent crude creeping closer to +$80 per barrel as supplies tighten and tensions with Iran simmer.

Brent crude futures have rallied +32c to $+79.60 per barrel, while U.S West Texas Intermediate (WTI) crude futures are up +29c at +$71.78 a barrel.

The prospects of a sharp drop in Iranian oil exports in the coming months due to renewed U.S sanction continues to support oil prices on any pullbacks.

Global inventories of crude oil and refined products have dropped sharply in recent months due to robust demand and production cuts by OPEC. This scenario is expected to only get worse as U.S peak summer driving season nears – it should offset increases in U.S shale output.

Ahead of the U.S open, gold prices have erased their early gains overnight and are edging closer to its five-month low, hit in the previous session, as the dollar pared losses against G10 currency pairs and traded within sight of its 2018 peak. Spot gold has fallen -0.1% to +$1,288.65 per ounce, while U.S gold futures for June delivery are nearly -0.3% lower at +$1,288 per ounce.

3. Italy 10-year bond yield at two-month high

Future price action in Italian government bonds (BTP's) will depend on the details of the program to be published by the League and the Five Star Movement and party rhetoric.

The 10-year Italian BTP yield has backed an aggressive +15 bps since yesterday and the spread over equivalent German Bunds has surged on a leaked draft agreement of the two parties in which they advocated for the write-off of +€250B in Italian debt and for the creation of a procedure to allow a country to exit the Euro. Ahead of the U.S open, the 10-year BTP yield is down -1.5 bps at +2.096%,

Elsewhere, the yield on 10-year Treasuries has increased +2 bps to +3.11%, reaching the highest yield in about seven-years on its fifth straight advance. In Germany, the 10-year Bund yield has rallied +3 bps to +0.64%. In the U.K, the 10-year Gilt yield has climbed +4 bps to +1.503%, the highest in more than three-months.

4. Dollar consolidates ahead of event risk

The USD is experiencing some mild consolidation of this week's gains, but the ongoing marginal steepening of the U.S yield curve is working in favour of a stronger dollar.

EUR/USD (€1.1804) continues to hover atop of some key support levels as investors focus on Italy and on the formation of the next Italian government.

The GBP (£1.3492) rallied during the Asian session after reports circulated that U.K was planning to tell E.U leaders that it was prepared to stay in a customs union beyond 2021 – akin to a ‘soft' Brexit. However, the report has since been refuted by a government spokesperson in the Euro session.

USD/JPY (¥110.66) has hit its highest level since late January aided by the rising of U.S bond yields.

Elsewhere, most EM currencies are little changed or only slightly lower against the dollar as U.S 10-year Treasury yields continue to rally. The exception is TRY, which is getting battered again. USD/TRY is last up +0.7% at $4.4448, although it has eased from yesterday's high of $4.50. The consensus believes that without emergency interest rate increases USD/TRY is likely to move above the $4.50 level persistently.

5. Aussie employment on target

Data overnight showed that Australia's jobless rate rose to a nine-month peak of +5.6% last month as more people entered the labor market, however, the number employed beat expectations with more full-time jobs added.

Overall, +22.6K net new jobs were added in April, topping forecasts of +20K. Digging deeper, full-time jobs jumped +32.7K.

While job growth topped expectations, the uptick in Australia's unemployment to 5.6% in April is expected to worry the RBA as they continue to fret about low wage growth.

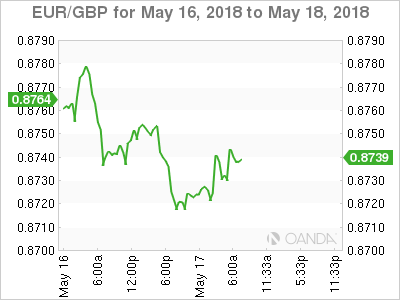

Euro Trading Sideways On Lack Of Eurozone Data

EUR/USD is showing little movement in the Thursday session. Currently, the pair is trading at 1.1817, up 0.07% on the day. On the release front, there are no German or eurozone indicators. In the U.S, there are two key events, which could impact on the movement of EUR/USD. The Philly Fed Manufacturing Index is expected to drop to 21.2, while unemployment claims are forecast to rise to 216 thousand. On Friday, Germany releases PPI and the eurozone publishes current account and trade balance.

The eurozone economy has performed well in 2018, but inflation has lagged behind and remains well below the ECB inflation target of around 2 percent. German Final CPI for April dropped to a flat 0.0%. Although this matched the forecast, this marked a 3-month low. Eurozone inflation indicators followed a similar trend, losing ground in April. Final CPI edged lower to 1.2%, down from 1.3% a month earlier. Final Core CPI followed a similar trend, dropping from 1.0% to 0.7%. Weak inflation levels could have a significant impact on ECB fiscal policy, as policymakers may have to consider extending its stimulus scheme, which is scheduled to run until September.

Bank of France Governor Francois Villeroy de Galhau raised some eyebrows this week after making hawkish comments about ECB interest rates hikes. Villeroy said that the ECB could soon provide additional guidance on the timing of a rate hike. In its last rate statement, the ECB said that any rate hikes would occur ‘well past’ the wrap-up of the stimulus program, which is slated to end in September. Villeroy stated that ‘well past’ could be a matter of quarters, rather than years. Investors snapped up euros on Monday after Villeroy’s comment, but the euro failed to hold onto these gains and ended the Monday session with small losses.

The U.S economy continues to perform well, but the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%, and the US dollar could continue to make broad gains as we get closer to the June policy meeting.

GBPUSD Sellers Testing 1.3500 Once More

The British pound continues to whipsaw against the US dollar, as speculation grows over the whether the United Kingdom will stay in the Customs Union after Brexit. The trading action on the GBPUSD pair this morning has been driven by reports that British PM Theresa May, issued a denial over the UK remaining in the Customs Union after Brexit. Going forward, the 1.3500 level remains key daily support, while the 1.3568 level is the key daily resistance area to watch before 1.3606.

The GBPUSD pair remains bearish while trading below the 1.3500 level. Further losses towards the 1.3458 and 1.3425 levels appear possible.

If GBPUSD buyers continues to hold above the 1.3500 level, buyers may again test towards the 1.3568 and 1.3606 resistance levels.

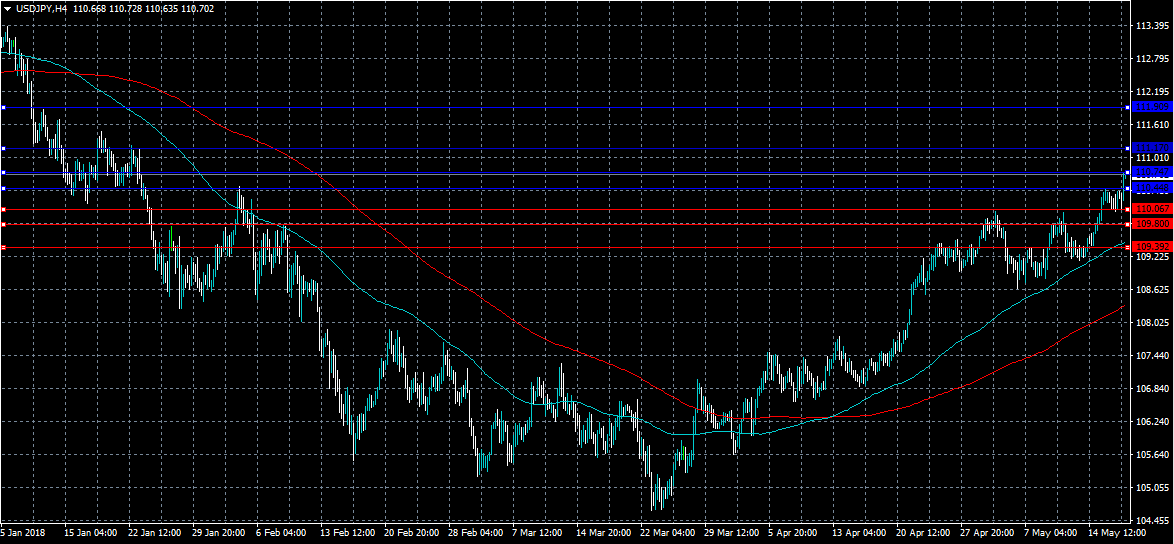

USDJPY Strongly Bullish Above 110.44 Level

The US dollar has moved to its highest trading level since January this year against the Japanese yen, hitting 110.74, after more weaker than expected Japanese economic data. The USDJPY pair currently trades close to the highs of the day, with buyers now looking towards a bullish break of the 111.00 technical level. Traders continue to watch for further buying in the USDJPY pair, as the bullish inverted head and shoulder pattern unfolds.

The USDJPY pair is strongly bullish while trading above the 110.44 level, key intraday technical resistance is now found at the 111.17 and 111.90 levels.

If the USDJPY trades below the 110.44 level, the pair may retrace towards the 110.06 and 109.80 support levels.

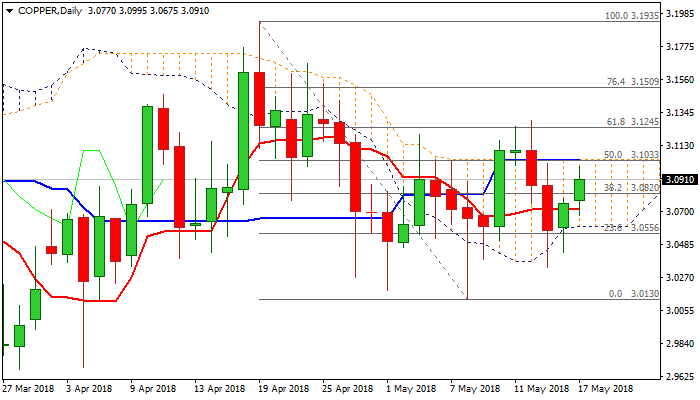

Copper – Recovery Attempts Face Strong Headwinds From Daily Cloud Top Barrier

Copper extended recovery into second straight day on Thursday, but gains faced strong headwinds from significant barrier at $3.1033 (daily cloud top / Kijun-sen).

Price pulled back on fresh strength of the US dollar and concerns about weaker demand from China - metal’s top world consumer.

Signals from daily chart are mixed as strong bullish momentum supports the advance, but the price was so far unable to break above a cluster of daily MA’s between $3.0840 and $3.0986 and today’s advance capped by 200SMA.

Risk of deeper pullback would persist while near-term price action holds below 200SMA / daily cloud top.

Boundaries of daily cloud are key, as close above cloud top would generate bullish signal for extension towards next strong barriers at $3.1245 (Fibo 61.8% of $3.1935/$3.0130) and $3.1295 (14 May high).

Conversely, return and close below daily cloud would weaken near-term structure for retest of $3.0335 (15 May low) and possible extension towards $3.0130 (08 May spike low).

Res: 3.0986, 3.1033, 3.1245, 3.1295

Sup: 3.0820, 3.0675, 3.0605, 3.0430

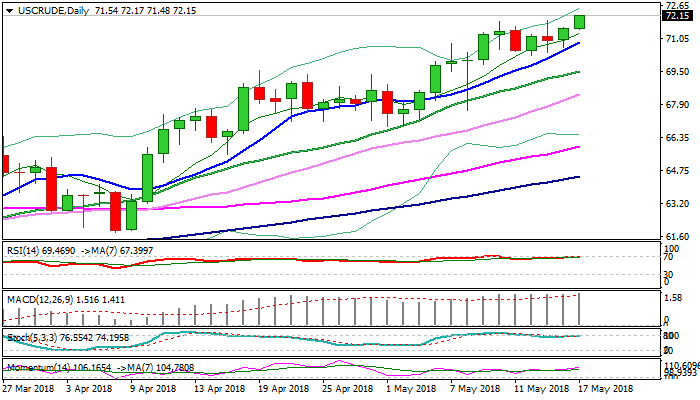

WTI OIL Hits New 3 ½ Year High On Break Above $72

WTI oil broke above psychological $72 barrier and hit new high at $72.15 (the highest since Nov 2014) on Thursday.

Persisting geopolitical tension keep oil price supported with fall in US crude stocks (EIA report on Wednesday) adding to bullish sentiment.

The global oil market is expected to remain tight despite forecasts for lower global oil demand and rising US shale oil production.

Fresh bullish extension eyes Fibo projections at $72.48/85 as initial targets but oil price could rise further and attack barriers at $74.94 (Oct 2011 low) and $76.35 (Fibo 61.8% of 107.45/$26.04 fall) in extension.

Rising 10SMA continues to track the advance and offers solid support (currently at $70.86) which is expected to contain dips.

Res: 72.15, 72.48, 72.85, 73.09

Sup: 71.86, 71.48, 70.86, 70.25

EU Leaders Gather In Bulgaria

Notes/Observations

- EU Leaders meet in Bulgaria

- Focus remains on the formation of Italian govt and any anti-European stance

Asia:

- Australia Apr Employment Change: +22.6K v +20.0Ke; Unemployment Rate: 5.6% v 5.5%e (9-month high)

- China Vice Premier Liu He meets with US lawmakers and said to be optimistic a trade deal can get done. To continue talks on China/US trade problems and proactively seek appropriate resolutions. US and China should properly handle trade dispute with mutual respect

- China Commerce Ministry (MOFCOM) spokesperson Gao Feng: To levy reciprocal tax on some US product, to halt US tariff concession on US fruit and pork

Europe:

- UK said to be planning to tell EU it was prepared to stay in a customs union beyond 2021. A dividend UK cabinet reportedly agreed to a new backstop plan as a last resort to avoid a hard Irish border. Foreign Min Johnson and Environment Secretary Gove, strong Brexit proponents, were "outgunned" during the meeting and reluctantly accepted the plans

- PM May defeated Labour Party effort to force the govt to disclose details of the two Brexit customs proposals. Labour had tried to force her government to reveal details of its two Brexit customs proposals, thwarting efforts to embarrass her divided team

Americas:

- Brazil Central Bank (BCB) left its Selic Rate unchanged at 6.50% for its 1st pause in the yearlong easing cycle

- Fed’s Bullard (dove, non-voter): Additional rate hikes might depress inflation expectations; Fed action that inverted yield curve was a very negative sign. Lots of support for Fed on FOMC for debate on policy framework

- Bank of Canada' (BOC) Schembri: Economy was operating close to potential. Closely looking at expansion in economic capacity to guide us in the goal of low and stable inflation

Economic Data:

- (NL) Netherlands Apr Unemployment Rate: 3.9% v 3.9% prior

- (EU) EU27 Apr New Car Registrations: +9.6% v -5.3% prior

- (IT) Italy Mar Total Trade Balance: €4.5B v €3.1B prior; Trade Balance EU: €0.7B v €1.1B prior

- (HK) Hong Kong Apr Unemployment Rate: 2.8% v 2.9%e (lowest level since 1998)

- (IL) Israel May CPI 12-month Forecast: 0.9% v 0.8% prior

- (EU) Euro Zone Mar Construction Output M/M: -0.3% v -0.7% prior; Y/Y: 0.8% v 0.2% prior

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €4.36B vs. €4.0-5.0B indicated range in 2023, 2026 and 2028 Bonds

- Sold €2.58B in new 0.35% July 2023 SPGB; Avg yield: 0.443% v 0.194% prior; Bid-to-cover: 1.83x v 1.32x prior

- Sold €0.74B in 5.90% July 2026 SPGB; Avg Yield 1.073% v 1.267% prior; Bid-to-cover: 1.94x v 1.86x prior

- Sold €1.04B in 1.40% Apr 2028 SPGB; Avg yield: 1.370% v 1.288% prior, Bid-to-cover: 2.25x v 2.01x prior

- (FR) France Debt Agency (Aft) sold total €7.497B vs. €6.5-7.5B indicated range in 2021 and 2023 Oats

- Sold €5.051B in 0.0% Feb 2021 Oat; Avg Yield: -0.30% v -0.32% prior; Bid-to-cover: 1.97x v 2.68x prior

- Sold €2.446B in 0.0% Mar 2023 Oat; Avg Yield: 0.10% v 0.06% prior; bid-to-cover: 2.42x v 2.07x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.1% at 393.4, FTSE flat at 7732.4, DAX +0.1% at 13004, CAC-40 +0.3% at 5583, IBEX-35 +0.4% at 10152, FTSE MIB +0.5% at 23851, SMI -0.3% at 8948, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes:

- European Indices trade mostly higher with a rebound in Italian Stocks as well as talk the UK plans to stay in the customs union after Brexit helping provided positive momentum.

- Ocado is a notable outperformer rising over 40% after announcing a deal with Kroger in which Kroger will acquire a 5% stake. Uk Gambling stocks were in focus after the UK government confirmed new £2 machine betting limits with William Hill, Paddy Power, GVC and 888 initially trading lower following the announcement.

- On the earnings front Altice Europe, Ceconomy, trade higher with Royal Mail, CGG and Bouygues notable fallers.

- Looking ahead expecting notable earnings from retail names Walmart, JC Penney, Dillards and Childrens Place.

Movers

- Consumer Discretionary William Hill [WMH.UK] -1.7%, GVC [GVC.UK] 0%, 888 [888.UK] -0.7%, Paddy Power [PPB.UK] +0.4% (UK Gov announces new FOBT staking limits), Ceconomy [CEC.DE] +5.6% (Earnings), Lagadere [MMB.FR] +2.3% (earnings)

- Industrials Bouygues [EN.FR] -1.3% (Earnings), Royal Mail [RMG.UK] -5.7% (Earnings)

- Financials Experian [EXPN.UK] +2.8% (Earnings)

- Utilities Suez [SEV.FR] +2.7% (Earnings)

- Telecoms Altice Europe [ATC.NL] +11.7% (Earnings)

- Technology Ocado [OCDO.UK] +43% (Partnership with Kroger)

- Energy CGG [CGG.FR] -2.7% (Earnings)

- Real Estate Foxtons [FOXT.UK] -0.6% (Earnings)

Speakers

- PM May's office said to dismiss reports that UK was ready to stay in customs union beyond 2021 (**Reminder: Telegraph reported that UK govt planned to tell EU it was prepared to stay in a customs union beyond 2021)

- Five Star Movement and League said to have dropped request for ECB debt write-off

- Italy Five Star Movement official confirmed that its program contained the debt accounting change (**Note: refers to reports that debt bough t by ECB should not be calculated in EU stability pact evaluations for all countries)

- IMF's Cottarelli: Unlikely that rules would be changed on debt accounting. Saw increased spending in Italy's populist plans. Did believe that Italy would put together a populist govt but did foresaw any very negative reaction in near future

- Fed staffers said to be resisting adding capital demand for the largest banks; said to be discussing counter cyclical buffers

Currencies

- The USD experienced a very mild consolidation of its recent gains but dealers noted that the marginal steepening of the US curve worked in favor of the greenback

- The GBP rallied during the Asian session after reports circulated that UK was planning to tell EU leaders at a Summit that it was prepared to stay in a customs union beyond 2021 (aka softening of its Brexit stance). The report was refuted by a govt spokesperson during the EU morning.

- EUR/USD hovered around the 1.18 level with the focus remaining on the formation of the Italian govt.

- USD/JPY hit its highest level since late Jan at 110.70 aided by the rising US bond yields.

Fixed Income

- Bund Futures trade 15 ticks lower at 157.94 as concerns over Italy didn't appear to spread across the eurozone. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 121.16 lower by 36 ticks as the UK said to consider a customs compromise. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Thursday’s liquidity report showed Wednesday's excess liquidity stayed fell from €1.913T to €1.909T. Use of the marginal lending facility decreased from €90M to €58M.

- Corporate issuance saw Harley Davidson as the lone issuer

Looking Ahead

- (ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to raise 7-Day Reverse Repo Rate by 25bps to 4.50%

- (SA) Saudi Arabia Mar Oil Production: No est v 9.935Mbpd prior – JODI

- 05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month bills

- 05:50 France Debt Agency (AFT) to sell €1.25-1.75B in 2022, 2027 and 2047 I/L bonds (Oatei)

- 06:00 (CZ) Czech Republic. to sell Bills

- 06:00 (RO) Romania to sell Bonds

- 06:30 ECB’s Constancio (Portugal, outgoing)

- 06:45 (US) Daily Libor Fixing

- 08:00 (EU) EU leaders meet in Sofia, Bulgaria

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) May Philadelphia Fed Business Outlook: 21.0e v 23.2 prior

- 08:30 (US) Initial Jobless Claims: 215Ke v 211K prior; Continuing Claims: 1.78Me v 1.790M prior

- 08:30 (CA) Canada Apr ADP Payrolls Report: No est v 42.8K prior

- 08:30 (CA) Canada Mar Int'l Securities Transactions (CAD): No est v 4.0B prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (RU) Russia Gold and Forex Reserve w/e May 11th: No est v $458.4B prior

- 10:00 (US) Apr Leading Index: 0.4%e v 0.3% prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 10:45 (US) Fed's Kashkari (dove, nn-voter) in Minneapolis

- 11:00 (US) Treasury announcement on upcoming 2-year, 5-year and 7-year auctions

- 12:00 (UK) BOE’s Haldane in London

- 13:00 (US) Treasury to sell 10-Year TIPS Reopening

- 13:30 (US) Fed’s Kaplan (dove, non-voter) in Texas

- 14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to leave Overnight Rate unchanged at 7.50%

- 19:30 (JP) Japan Apr National CPI Y/Y: 0.7%e v 1.1% prior; CPI Ex Fresh Food (Core) Y/Y: 0.8%e v 0.9% prior, CPI Ex Fresh Food, Energy (core-core) Y/Y: 0.4%e v 0.5% prior

- 13:30 (US) Fed’s Kaplan (dove, non-voter) in Texas