Sample Category Title

Euro Softens Ahead Of ECB Decision, Draghi In Focus

There is a growing air of anticipation across financial markets ahead of the European Central Bank rate decision and press conference later in the day.

Although the ECB is broadly expected to keep monetary policy unchanged in April, the main focus and potential action will probably revolve around Draghi’s post-meeting press conference. While Mario Draghi is likely to reiterate the message he delivered during March’s policy meeting, when the ECB dropped its easing bias, this could be presented with dovish touch. With Eurozone economic data disappointing in recent months, inflation still below the golden 2% target and lingering trade tensions weighing on sentiment, doves could steal the show today.

A key question on the mind of many investors is whether the soft economic data during Q1 will result in the ECB delaying the QE exit decision. With speculation rising over the ECB pushing back the taper timeline, it will be interesting to hear Mario Draghi’s thoughts on this topic during his press conference. The Euro remains at risk of extending losses against the Dollar if Draghi strikes a cautious tone.

This is certainly shaping up to be a bearish trading week for the Euro, which has tumbled to levels not seen since the 1 March – below 1.2160. Focusing on the technical picture, the EURUSD is at risk of tumbling lower, if bears are able to maintain control below the 1.2200 level. Previous support around 1.2200 could transform into a dynamic resistance, that invites a decline towards 1.2150 and 1.2090.

Commodity spotlight – WTI Oil

WTI Crude appreciated on Thursday morning, as market expectations over the United States re-imposing sanctions against Iran and a drop in Venezuela’s oil production fuelled fears of supply shortages.

It is becoming increasingly clear that oil bulls remain heavily reliant on geopolitical tensions to sustain the current rally. While further upside could be on the cards in the near term amid OPEC optimism, gains are likely to be capped down the road by soaring production from U.S Shale. Taking a look at the technical picture, WTI Crude continues to fulfil the prerequisites of a bullish trend as there have been consistently higher highs and higher lows. WTI has the potential to challenge $70 if prices are able to keep above $67.50. Alternatively, if bulls become exhausted and fail to defend $67.50, the next level of interest will be at $66.00.

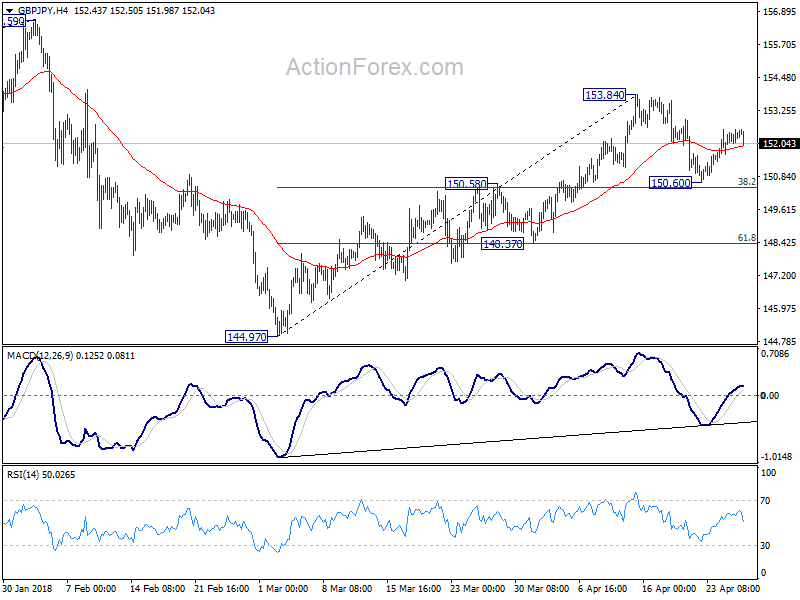

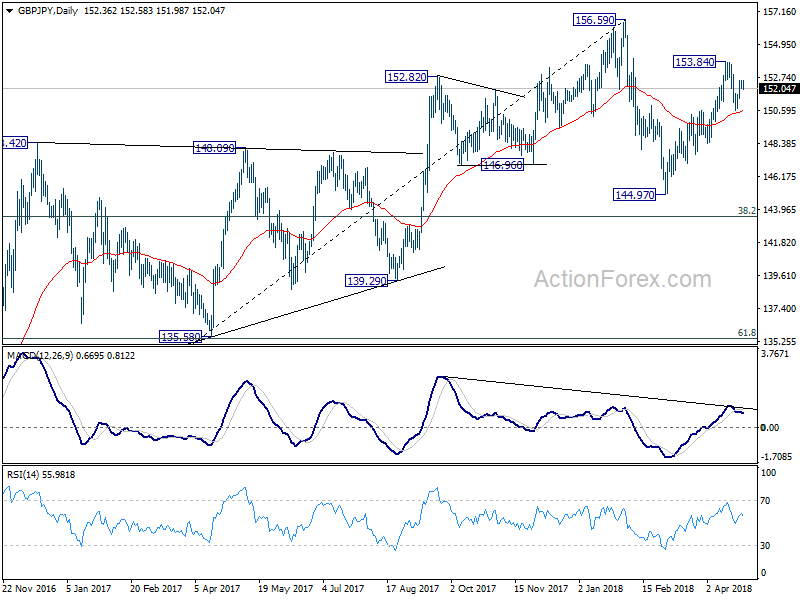

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.09; (P) 152.33; (R1) 152.65; More...

Intraday bias in GBP/JPY remains neutral at this point. We're holding on to the view that corrective rise from 144.97 should have completed at 153.84 already. Hence, another decline is expected in the cross. Break of 150.60 will target 148.37 support first. Break will bring retest of 144.97 low. However, firm break of 153.84 will invalidate our view and extend the rise from 144.97 towards 156.59 high.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

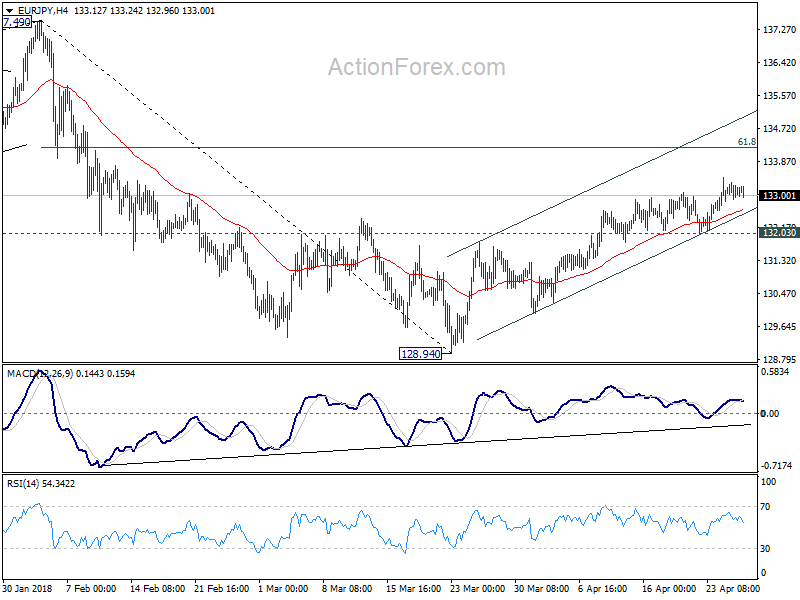

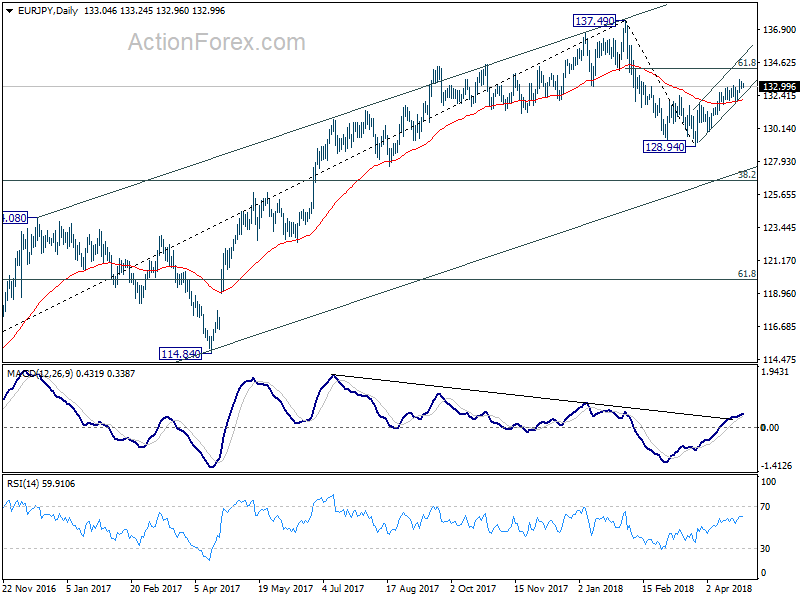

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.87; (P) 133.10; (R1) 133.29; More....

With 132.03 minor support intact, EUR/JPY's recovery from 128.94 could extend higher. But after all, it's seen as a corrective move. Therefore, we expect strong resistance from 61.8% retracement of 137.49 to 128.94 at 134.22 to limit upside. Break of 132.03 will turn bias to the downside for retesting 128.94 low. However, sustained break of 134.22 will turn focus back to 137.49 high instead.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 week EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.

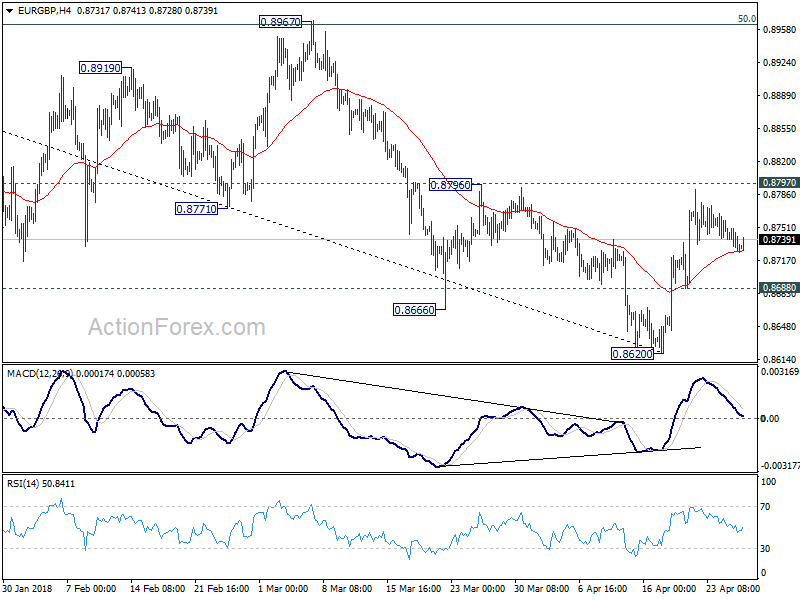

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8722; (P) 0.8736; (R1) 0.8744; More...

EUR/USD is staying in consolidative trading and intraday bias remains neutral first. Further rise is expected as long as 0.8688 minor support holds. Break of 0.8797 will extend the rise from 0.8620 to key cluster resistance at 0.8967 (50% retracement of 0.9305 to 0.8620 at 0.8963) next. On the downside, break of 0.8688 minor support will dampen the bullish case and turn focus back to 0.8620 instead.

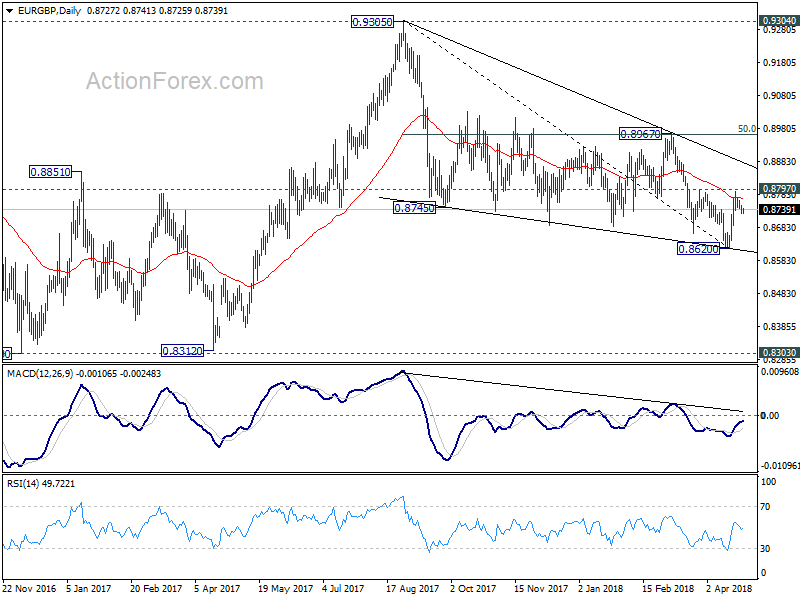

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

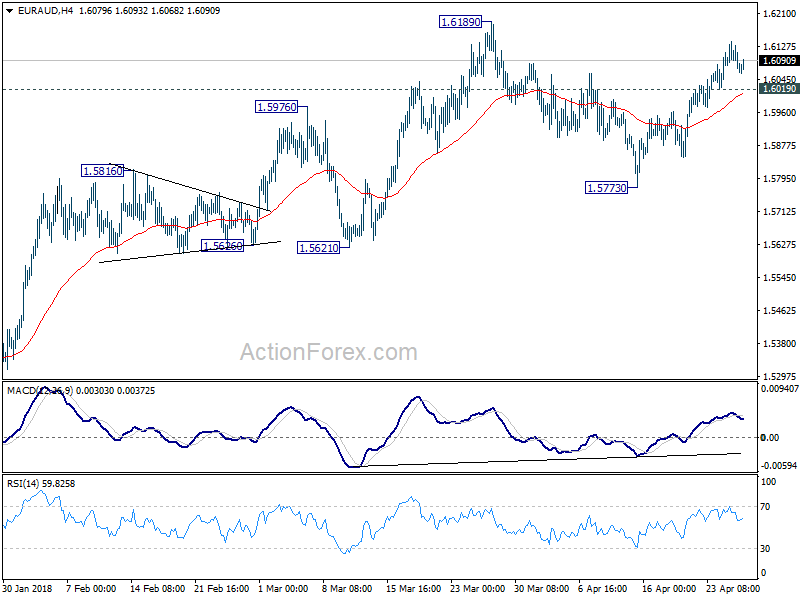

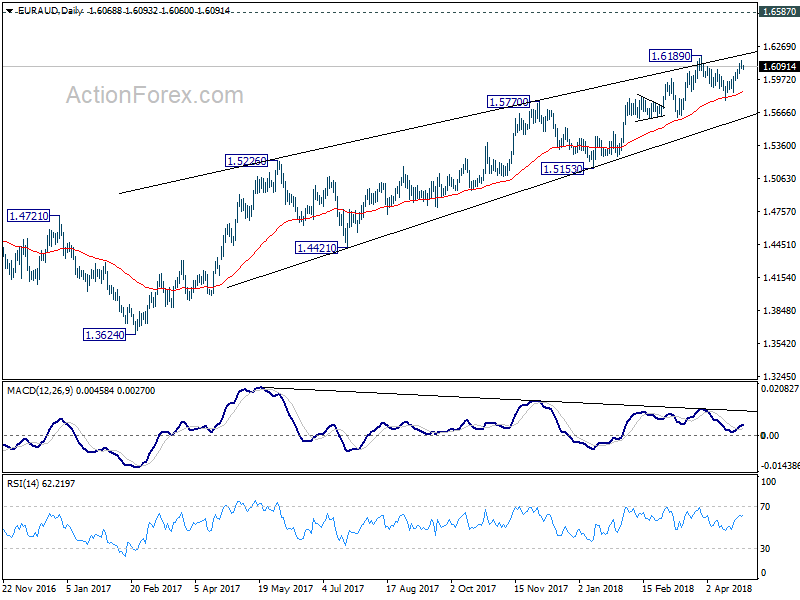

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6053; (P) 1.6096; (R1) 1.6119; More....

EUR/AUD lost some upside momentum as seen in 4 hour MACD. But with 1.6015 minor support intact, further rise is mildly in favor to 1.6189 high. Firm break there will resume medium term rise from 1.3624 and target 1.6587 key resistance. On the downside, below 1.6019 minor support will turn focus back to 1.5773 instead.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. EUR/AUD also drew strong support from 55 day EMA and rebounded. Current rally from 1.3624 could still extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal.

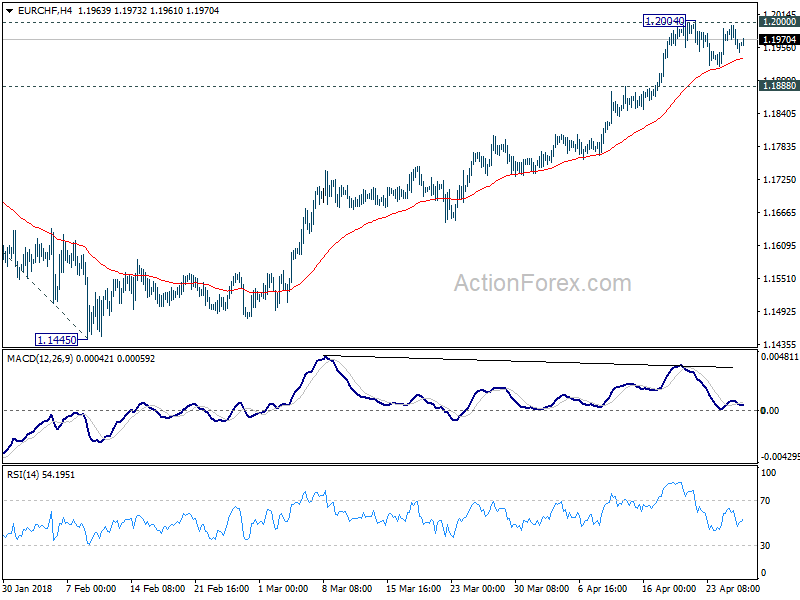

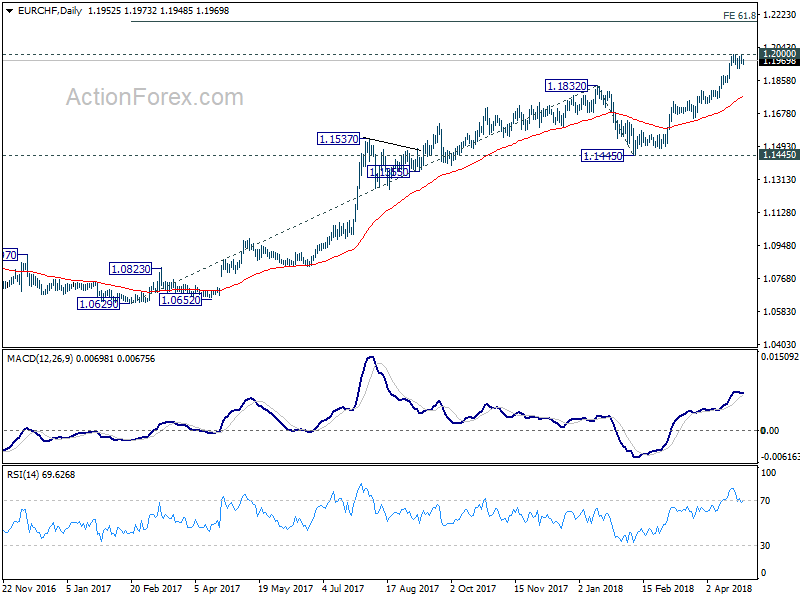

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1941; (P) 1.1969; (R1) 1.1983; More...

EUR/CHF is still bounded in consolidation pattern from 1.2004 temporary top. Intraday bias remains neutral at this point. On the upside, decisive break of 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, considering bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.

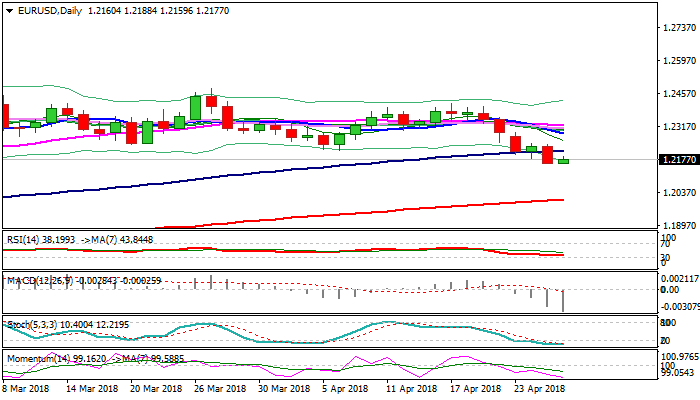

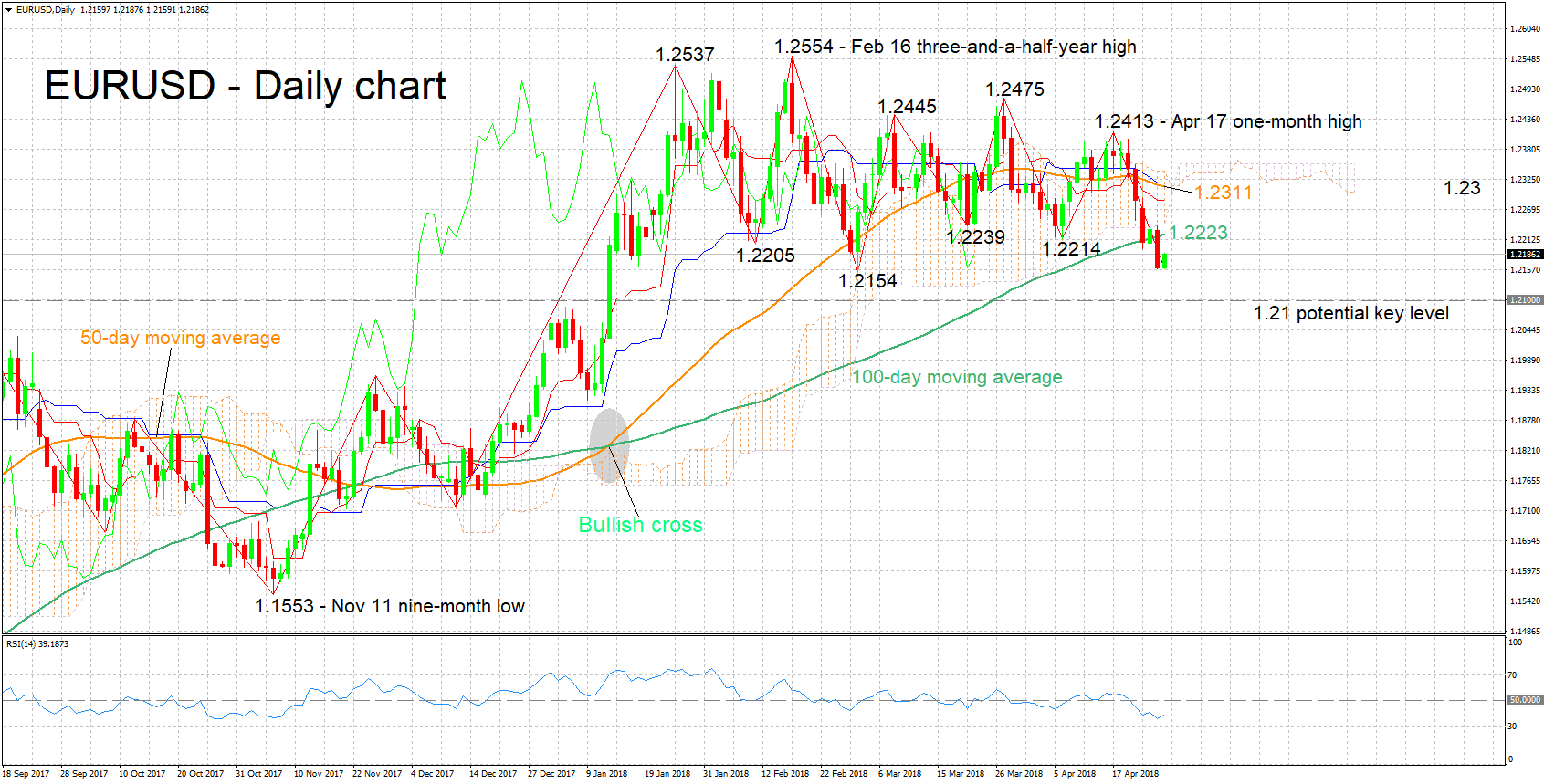

EURUSD Bounces From New Four-Month Low Ahead Of ECB

The Euro moved higher in early Thursday's trading after retesting low at 1.2159, posted on strong fall of Wednesday.

Larger bears found footstep here and bounce could be positioning for fresh weakness, as overall picture is negative.

Yesterday's close below key 1.2172 Fibo support was bearish signal but so far without clear break lower.

Sustained break below critical supports at 1.2172/53 (Fibo 38.2% of 1.1553/1.2555 / low of multi-month 1.2153/1.2555 congestion) is needed to confirm reversal.

ECB meeting is the key event for Euro today. The central bank is expected to leave policy unchanged and ECB chief Mario Draghi is expected to play down recent softness in the bloc's economy, while traders will be focusing on comments about bond buying program, as Draghi may signal withdrawal of 2.5 trillion euros worth stimulus, which was introduced to boost growth and reduce borrowing cost, despite failing to lift inflation which remains below projected targets.

More hawkish tone from Draghi, which would include further clues about reducing / ending bond-buying program and signal possible rate hike, would boost the single currency.

Positive scenario requires firm break above 100SMA (1.2213) and penetration of narrowing daily cloud (cloud base lies at 1.2239) to generate bullish signal and open way for stronger retracement of 1.2413/1.2159 fall.

Conversely, dovish tone from the ECB President would increase existing pressure on Euro for clear break through 1.2172/53 pivots, which could accelerate towards psychological 1.20 support, reinforced by 200SMA).

Res: 1.2213, 1.2239, 1.2286, 1.2320

Sup: 1.2153, 1.2092, 1.2054, 1.2000

SNB Q1 USD holding unchanged at 35%, EUR holding dropped 1%

SNB reported CHF 6.8B loss in Q1 of 2018.That includes CHF 7.0B loss on currency positions and CHF 0.2B loss on gold holdings. The losses were partly offset by CHF 0.5B gain in Swiss Franc positions, mainly from negative interest rates.

Current allocations in the foreign exchange reserves were largely unchanged.

- USD holdings unchanged at 35%

- EUR holdings dropped to 39% vs 40% prior

- GBP holdings unchanged at 7%

- JPY holdings unchanged at 8%

- CAD holdings unchanged at 3%

Dollar Remains Elevated, ECB In The Spotlight

Here are the latest developments in global markets:

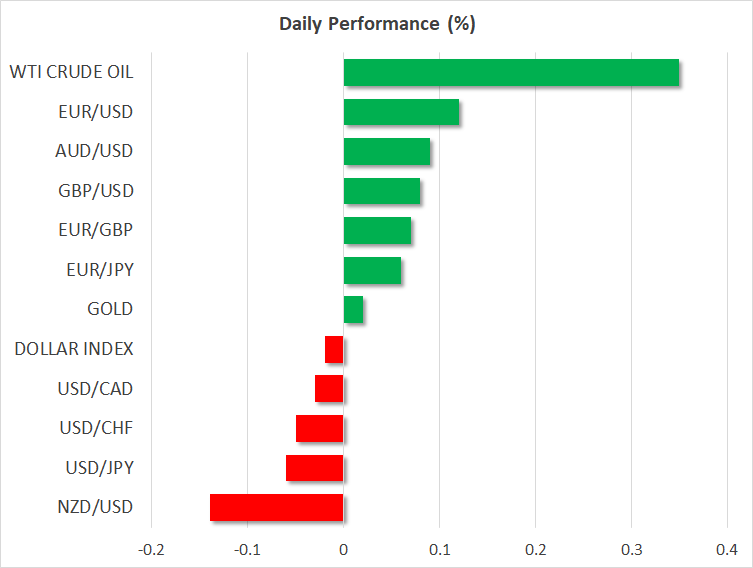

FOREX: The US dollar index inched lower on Thursday, but by less than 0.1%, giving back some of the gains it achieved yesterday on the back of surging US bond yields. The euro was relatively steady ahead of today's main event, the ECB's monetary policy decision, while both the aussie and the kiwi continued to collapse.

STOCKS: US markets closed slightly higher yesterday, with the exception being the Nasdaq Composite, which fell, though only by 0.05%. Meanwhile, the Dow Jones and the S&P 500 climbed by 0.25% and 0.18% respectively, as encouraging earnings helped to calm the nerves of investors concerned with rising US bond yields. As for today, futures tracking the Dow and the S&P are pointing to a slightly lower open, while those tracking the Nasdaq 100 are flashing green, probably due to the strong earnings reported by tech giants such as Facebook and Twitter after yesterday's closing bell. Asia was mixed, with Japan's Nikkei 225 and Topix rising by 0.47% and 0.25% correspondingly, but Hong Kong's Hang Seng index tumbling by 1.39%. In Europe, futures tracking the major indices were mostly in positive territory.

COMMODITIES: Oil prices are higher on Thursday, extending some gains from yesterday. WTI and Brent crude are up by 0.35% and 0.45% respectively, both hovering near their three-and-a-half year highs. Prices appear to be supported by ever-increasing expectations that the US will impose fresh sanctions on Iran soon, after French President Macron said yesterday he anticipates the US to pull out of the Iran deal. Even a surprising build in US crude inventories was not enough to keep prices down. In precious metals, gold is fractionally higher today, recovering some of the losses it posted yesterday as the US dollar continued to climb. Besides a stronger dollar weighing on demand, the broader theme of rising interest rates is also a negative factor for gold, which pays no interest to hold and thus becomes less attractive in such an environment.

Major movers: Dollar keeps climbing alongside US yields, antipodean collapse in full swing

Wednesday was another relatively calm day in terms of news flow, with most of the price action in the FX market being driven by the continued climb in longer-term US Treasury yields. The yield on 10-year notes climbed to 3.035% before retreating slightly, lending support to the US dollar, which was the stark outperformer among the major currencies. Euro/dollar touched a two-month low, while dollar/yen rose to a three month high.

It will be most interesting to see how this surge in yields plays out. The break above the widely-touted 3.0% handle in 10-year US yields earlier in the week seems to have opened the way for even higher levels. While a pullback in yields shouldn't be ruled out in the coming days given that the current rally seems a little overextended, the trend is clearly to the upside and should it continue, the dollar may continue to regain lost ground.

On the contrary, a sustained advance in yields would likely spell bad news for stock markets. Major indices have been struggling recently, as investors adjust to the reality of rising borrowing costs for most of these firms, which could hinder their ability to buy back their own stocks, and also increase the cost of financing their old debt, squeezing profits.

Elsewhere, aussie/dollar and kiwi/dollar continued to collapse yesterday, both reaching fresh four-month lows. The aussie has now slid for five consecutive days against the dollar, while the kiwi is on an eight-day losing streak, with price action in both pairs increasingly resembling 'a falling knife'.

Day ahead: ECB meeting the day's highlight, US durable goods orders due

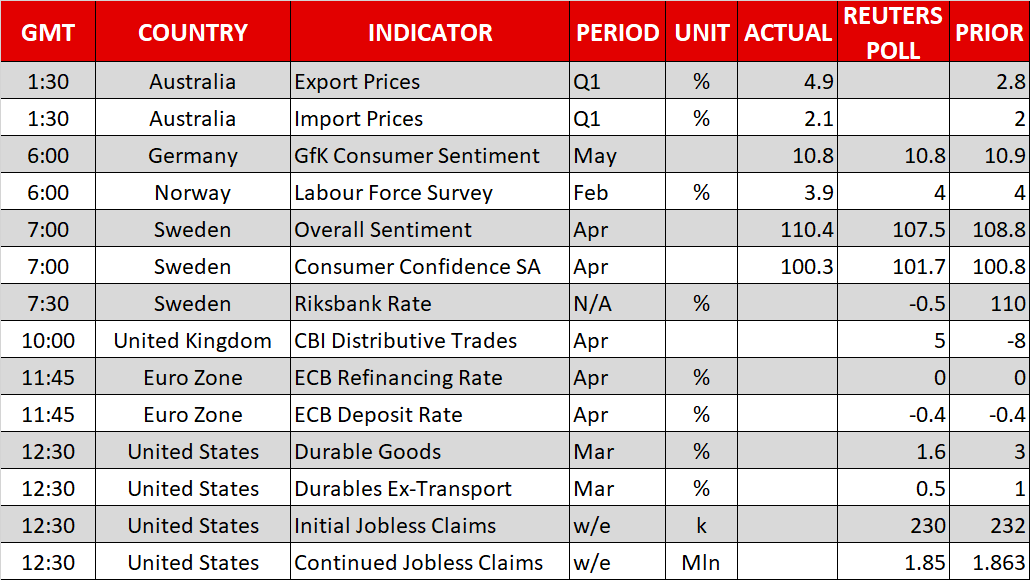

Thursday features the conclusion of the European Central Bank's two-day meeting on monetary policy. Although no change in policy is expected, the Bank's communication – its forward guidance –is of importance and is likely to lead to movements in euro pairs.

The Riksbank's interest rate decision is due at 0730 GMT. No change in rates is expected, though the Swedish central bank may lift its inflation forecast, something that could support the krona which has declined considerably year-to-date relative to majors including the dollar and the euro. Stefan Ingves, the Bank's governor will be holding a press conference at 0900 GMT.

At 1145 GMT, the ECB's decision on interest rates will be made public. The Bank is widely anticipated to stand pat, but it would be interesting to see whether it starts to signal that it will end its asset purchases by the end of the year, or if it appears more cautious in the face of weakening economic momentum and inflation pressures as projected by recent data releases. If it's the latter, then the euro is expected to depreciate, likely hitting fresh lows versus the greenback, earlier in the day euro/dollar revisited the near two-month low of 1.2159 hit yesterday. ECB President Mario Draghi's press conference beginning at 1230 GMT will also be closely watched, with market moving comments 'being on the agenda'.

Earlier in the day (1000 GMT), the UK will see the release of the Confederation of British Industry's distributive trades retail sales balance for April. An improvement is anticipated for the figure to rise back into positive territory.

The attention will next turn to the US: durable goods orders for March and initial & continued jobless claims for the week ending April 20 are scheduled for release at 1230 GMT. Durable goods orders, which gauge business spending on equipment, are forecast to expand for the second straight month, albeit at a softer pace relative to February. The number on core durable goods that excludes transportation will also be attracting interest.

In equities, Microsoft and Amazon, the world's third and fourth largest companies by market cap will be releasing quarterly results on Thursday, both companies' reports will be made public after the US market close.

Technical Analysis: EURUSD revisits near 2-month low, mostly bearish in the short-term

EURUSD has experienced considerable declines after recording a one-month high of 1.2413 on April 17. Earlier on Thursday, it fell to 1.2159, matching yesterday's near two-month low. The Tenkan-sen line is below the Kijun-sen in support of a bearish short-term picture. The RSI, having retreated below its 50 neutral-perceived level, also supports the view for negative momentum, though it seems to have stalled its decline, this could be an indication of a weakening bearish bias.

A hawkish message by the ECB later on Thursday is likely to boost the pair. Resistance to advances could come around the current level of the 100-day moving average at 1.2223, the area around this level encapsulates a few bottoms from previous months, the Ichimoku cloud bottom (1.2242), as well as the 1.22 round figure. Further above, the range around the 1.23 handle would be eyed (which again includes numerous points that may be of importance),

Conversely, a dovish ECB is expected to exert downward pressure in EURUSD. Immediate support to declines could come around 1.2154, this being March 1's three-and-a-half-month low. A downside violation would turn the attention to the 1.21 handle, with 1.20 being the focus next in case of even steeper losses.

USDJPY Trades Around 2-Month High, Extends Its Bullish Rally With Next Stop 110.00

USDJPY extends its gains after the penetration of the 108.20 strong barrier during Monday’s session. Earlier today the price recorded a fresh more than two-month high of 109.46 and has added more than 250 pips over the last six trading days.

From the technical point of view, in the daily timeframe, the price is developing well above the 50-day simple moving average SMA, while it lost some momentum over the last few hours. The RSI indicator is looking stronger as it enters the overbought zone after the bounce off the 50-neutral level. Also, the MACD oscillator is rising with strong momentum, both suggesting that the price would move north for a while longer.

Currently, there is no obstacle until the 110.00 resistance handle. This level is the 38.2% Fibonacci retracement of the downleg from 118.60 to 104.60. If the price penetrates 110.00 it could hit the 200-SMA around 110.20, which stands slightly below the next immediate resistance level of 110.50 taken from the peak on January 18.

However, should a downside reversal take form, immediate support will likely come from the 108.20 support level. A break below this level could drive the price towards the next barrier of 23.6% Fibonacci mark near 107.90, which holds slightly above the strong support of 107.80. The next key support to watch lower down is the 50-day SMA around 106.70.

As a side note, the pair has been consolidating within a downward sloping channel since December 2016 and touched the lower boundary at the end of March, creating a 16-month low of 104.60.